Deck 16: Accounting for Compensation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

In order to retain certain key executives, Tanner Corporation granted them incentive stock options on December 31, 2006. 50,000 options were granted at an option price of $35 per share. Market prices of the stock were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2007. The Black-Scholes option pricing model determines total compensation expense to be $500,000. What amount of compensation expense should Tanner recognize as a result of this plan for the year ended December 31, 2007 under the fair value method?

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2007. The Black-Scholes option pricing model determines total compensation expense to be $500,000. What amount of compensation expense should Tanner recognize as a result of this plan for the year ended December 31, 2007 under the fair value method?

A) $250,000

B) $500,000

C) $550,000

D) $1,750,000

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2007. The Black-Scholes option pricing model determines total compensation expense to be $500,000. What amount of compensation expense should Tanner recognize as a result of this plan for the year ended December 31, 2007 under the fair value method?A) $250,000

B) $500,000

C) $550,000

D) $1,750,000

Question

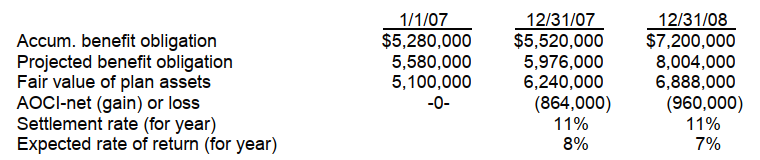

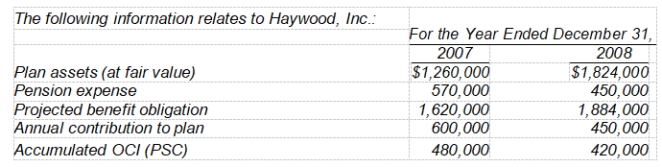

Presented below is pension information related to Tyler, Inc. for the year 2008:

The amount of pension expense to be reported for 2008 is

The amount of pension expense to be reported for 2008 is

A) $108,000.

B) $144,000.

C) $162,000.

D) $120,000.

The amount of pension expense to be reported for 2008 isA) $108,000.

B) $144,000.

C) $162,000.

D) $120,000.

Question

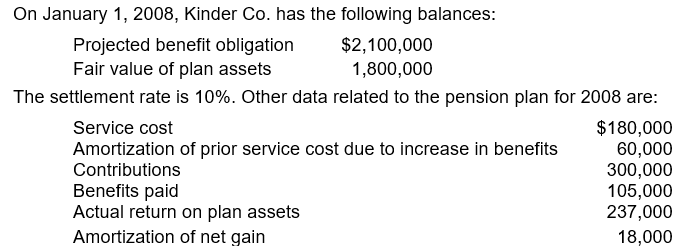

Randel, Inc. received the following information from its pension plan trustee concerning the operation of the company's defined-benefit pension plan for the year ended December 31, 2008.

Accounting for Compensation 16 - 15

Accounting for Compensation 16 - 15

The service cost component of pension expense for 2008 is $360,000 and the amortization of prior service cost due to an increase in benefits is $60,000. The settlement rate is 10% and the expected rate of return is 9%. What is the amount of pension expense for 2008?

The service cost component of pension expense for 2008 is $360,000 and the amortization of prior service cost due to an increase in benefits is $60,000. The settlement rate is 10% and the expected rate of return is 9%. What is the amount of pension expense for 2008?

A) $360,000

B) $522,000

C) $531,000

D) $432,000

Accounting for Compensation 16 - 15 The service cost component of pension expense for 2008 is $360,000 and the amortization of prior service cost due to an increase in benefits is $60,000. The settlement rate is 10% and the expected rate of return is 9%. What is the amount of pension expense for 2008?A) $360,000

B) $522,000

C) $531,000

D) $432,000

Question

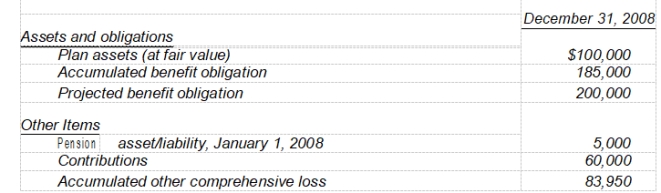

The following information for Monroe Enterprises is given below:

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.

-What is the pension expense that Monroe Enterprises should report for 2008?

A) $86,050

B) $110,000

C) $60,000

D) $83,950

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.-What is the pension expense that Monroe Enterprises should report for 2008?

A) $86,050

B) $110,000

C) $60,000

D) $83,950

Question

The following information for Monroe Enterprises is given below:

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.

-What is the amount that Monroe Enterprises should report as its pension liability on its balance sheet as of December 31, 2008?

A) $100,000

B) $15,000

C) $185,000

D) $200,000

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.-What is the amount that Monroe Enterprises should report as its pension liability on its balance sheet as of December 31, 2008?

A) $100,000

B) $15,000

C) $185,000

D) $200,000

Question

Presented below is pension information for Welch Company for the year 2008:

The amount of pension expense to be reported for 2008 is

The amount of pension expense to be reported for 2008 is

A) $93,000.

B) $69,000.

C) $60,000.

D) $45,000.

The amount of pension expense to be reported for 2008 isA) $93,000.

B) $69,000.

C) $60,000.

D) $45,000.

Question

Downing, Inc. received the following information from its pension plan trustee concerning the operation of the company's defined-benefit pension plan for the year ended December 31, 2008.

The service cost component of pension expense for 2008 is $840,000 and the amortization of unrecognized prior service cost is $180,000. The settlement rate is 10% and the expected rate of return is 8%. What is the amount of pension expense for 2008?

The service cost component of pension expense for 2008 is $840,000 and the amortization of unrecognized prior service cost is $180,000. The settlement rate is 10% and the expected rate of return is 8%. What is the amount of pension expense for 2008?

A) $1,716,000

B) $1,680,000

C) $1,608,000

D) $1,440,000

The service cost component of pension expense for 2008 is $840,000 and the amortization of unrecognized prior service cost is $180,000. The settlement rate is 10% and the expected rate of return is 8%. What is the amount of pension expense for 2008?A) $1,716,000

B) $1,680,000

C) $1,608,000

D) $1,440,000

Question

The following data are for the pension plan for the employees of Nickels Company.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.

-The actual return on plan assets in 2008 was

A) $900,000.

B) $765,000.

C) $600,000.

D) $465,000.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.-The actual return on plan assets in 2008 was

A) $900,000.

B) $765,000.

C) $600,000.

D) $465,000.

Question

The following data are for the pension plan for the employees of Nickels Company.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.

-Assume that the actual return on plan assets in 2008 was $765,000. The unexpected gain on plan assets in 2008 was

A) $156,000.

B) $135,000.

C) $114,000.

D) $72,000.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.-Assume that the actual return on plan assets in 2008 was $765,000. The unexpected gain on plan assets in 2008 was

A) $156,000.

B) $135,000.

C) $114,000.

D) $72,000.

Question

-The balance of the projected benefit obligation at December 31, 2008 is

A) $2,685,000.

B) $2,385,000.

C) $2,355,000.

D) $2,337,000.

Question

-The fair value of plan assets at December 31, 2008 is

A) $2,430,000.

B) $2,250,000.

C) $2,232,000.

D) $2,214,000.

Question

The following information relates to the pension plan for the employees of Polzin Co.:

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.

-The interest cost for 2008 is

A) $537,840.

B) $607,200.

C) $657,360.

D) $880,440.

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.-The interest cost for 2008 is

A) $537,840.

B) $607,200.

C) $657,360.

D) $880,440.

Question

The following information relates to the pension plan for the employees of Polzin Co.:

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.

-The actual return on plan assets in 2008 is

A) $408,000.

B) $456,000.

C) $588,000.

D) $648,000.

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.-The actual return on plan assets in 2008 is

A) $408,000.

B) $456,000.

C) $588,000.

D) $648,000.

Question

The following information relates to the pension plan for the employees of Polzin Co.:

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.

-The unexpected gain or loss on plan assets in 2008 is

A) $39,360 loss.

B) $22,560 gain.

C) $19,200 gain.

D) $214,560 gain.

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.-The unexpected gain or loss on plan assets in 2008 is

A) $39,360 loss.

B) $22,560 gain.

C) $19,200 gain.

D) $214,560 gain.

Question

Presented below is information related to Bitner Manufacturing Company as of December 31, 2008:

The amount for the prior service cost is related to a decrease in benefits. The fair value of the pension plan assets is $600,000.

The amount for the prior service cost is related to a decrease in benefits. The fair value of the pension plan assets is $600,000.

The pension asset/liability reported on the balance sheet at December 31, 2008 is a

A) $300,000.

B) $600,000.

C) $900,000.

D) $1,305,000.

The amount for the prior service cost is related to a decrease in benefits. The fair value of the pension plan assets is $600,000.The pension asset/liability reported on the balance sheet at December 31, 2008 is a

A) $300,000.

B) $600,000.

C) $900,000.

D) $1,305,000.

Question

Barkley Corporation received the following report from its actuary at the end of the year:

-The amount reported as the pension liability at December 31, 2007 is

A) $0.

B) $200,000.

C) $220,000.

D) $300,000.

-The amount reported as the pension liability at December 31, 2007 is

A) $0.

B) $200,000.

C) $220,000.

D) $300,000.

Question

Barkley Corporation received the following report from its actuary at the end of the year:

-The amount reported as the pension liability at December 31, 2008 is

A) $1,800,000.

B) $1,480,000.

C) $380,000.

D) $360,000.

-The amount reported as the pension liability at December 31, 2008 is

A) $1,800,000.

B) $1,480,000.

C) $380,000.

D) $360,000.

Question

-The amount reported as the liability for pensions on the December 31, 2007 balance sheet is

A) $0.

B) $30,000.

C) $360,000.

D) $390,000.

Question

-The amount reported as the liability for pensions on the December 31, 2008 balance sheet is

A) $0.

B) $60,000.

C) $1,884,000.

D) $520,000.

Question

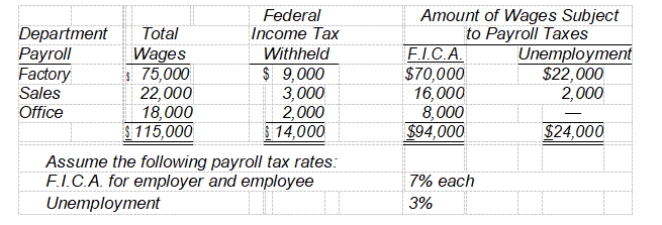

Quirk Corp.'s payroll for the pay period ended October 31, 2008 is summarized as follows:

What amount should Quirk accrue as its share of payroll taxes in its October 31, 2008 balance sheet?

What amount should Quirk accrue as its share of payroll taxes in its October 31, 2008 balance sheet?

A) $21,300

B) $14,720

C) $13,880

D) $7,300

What amount should Quirk accrue as its share of payroll taxes in its October 31, 2008 balance sheet?A) $21,300

B) $14,720

C) $13,880

D) $7,300

Question

On January 1, 2007, Doane Corp. granted an employee an option to purchase 6,000 shares of Doane's $5 par value common stock at $20 per share. The Black-Scholes option pricing model determines total compensation expense to be $140,000. The option became exercisable on December 31, 2008, after the employee completed two years of service. The market prices of Doane's stock were as follows:

For 2008, Doane should recognize compensation expense under the fair value method of

For 2008, Doane should recognize compensation expense under the fair value method of

A) $90,000.

B) $30,000.

C) $70,000.

D) $0.

For 2008, Doane should recognize compensation expense under the fair value method ofA) $90,000.

B) $30,000.

C) $70,000.

D) $0.

Question

The following information pertains to Mellon Co.'s pension plan:

If no change in actuarial estimates occurred during 2008, Mellon's projected benefit obligation at December 31, 2008 was

If no change in actuarial estimates occurred during 2008, Mellon's projected benefit obligation at December 31, 2008 was

A) $64,200.

B) $75,000.

C) $79,200.

D) $82,200.

If no change in actuarial estimates occurred during 2008, Mellon's projected benefit obligation at December 31, 2008 wasA) $64,200.

B) $75,000.

C) $79,200.

D) $82,200.

Question

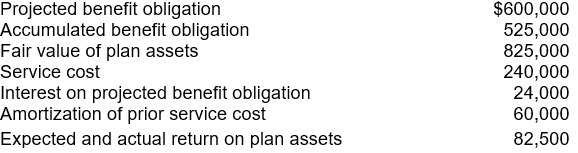

Reser Corp., a company whose stock is publicly traded, provides a noncontributory defined-benefit pension plan for its employees. The company's actuary has provided the following information for the year ended December 31, 2008:

The market -related asset value equals the fair value of plan assets. No contributions have been made for 2008 pension cost. In its December 31, 2008 balance sheet, Reser should report a(n)

The market -related asset value equals the fair value of plan assets. No contributions have been made for 2008 pension cost. In its December 31, 2008 balance sheet, Reser should report a(n)

A) $600,000 pension liability.

B) $824,000 pension asset.

C) $225,000 pension asset.

D) $525,000 pension liability.

The market -related asset value equals the fair value of plan assets. No contributions have been made for 2008 pension cost. In its December 31, 2008 balance sheet, Reser should report a(n)A) $600,000 pension liability.

B) $824,000 pension asset.

C) $225,000 pension asset.

D) $525,000 pension liability.

Question

Question

At December 31, 2008, the following information was provided by the Nilges Corp. pension plan administrator:

What is the amount of the pension liability that should be shown on Nilges' December 31, 2008 balance sheet?

What is the amount of the pension liability that should be shown on Nilges' December 31, 2008 balance sheet?

A) $7,200,000

B) $2,700,000

C) $1,620,000

D) $1,080,000

What is the amount of the pension liability that should be shown on Nilges' December 31, 2008 balance sheet?A) $7,200,000

B) $2,700,000

C) $1,620,000

D) $1,080,000

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/42

Play

Full screen (f)

Deck 16: Accounting for Compensation

1

If sick pay benefits accumulate but do not vest, accrual is permitted but not required.

True

2

Using the fair value method, total compensation expense is computed based on the fair value of the options expected to vest on the date the options are granted to the employees.

True

3

Under the intrinsic value method, total compensation cost is computed as the excess of the market price of the stock over the option price on the measurement date.

True

4

Interest on the liability (or interest expense) is the interest for the period on the projected benefit obligation outstanding during the period.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

5

When considering the interest rate component used in the determination of pension cost, the FASB concluded that the rate selected should reflect conservatism.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

6

The interest rate used to compute the projected benefit obligation should also be used as the rate of return on plan assets.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

7

Other Comprehensive Income (PSC) is reported as part of net income.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

8

In accounting for compensated absences, the difference between vested rights and accumulated rights is

A) vested rights are normally for a longer period of employment than are accumulated rights.

B) vested rights are not contingent upon an employee's future service.

C) vested rights are a legal and binding obligation on the company, whereas accumulated rights expire at the end of the accounting period in which they arose.

D) vested rights carry a stipulated dollar amount that is owed to the employee

A) vested rights are normally for a longer period of employment than are accumulated rights.

B) vested rights are not contingent upon an employee's future service.

C) vested rights are a legal and binding obligation on the company, whereas accumulated rights expire at the end of the accounting period in which they arose.

D) vested rights carry a stipulated dollar amount that is owed to the employee

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is not a characteristic of a defined-contribution pension plan?

A) The employer's contribution each period is based on a formula.

B) The benefits to be received by employees are usually determined by an employee's three highest years of salary.

C) The accounting for a defined-contribution plan is straightforward and uncomplicated.

D) The benefit of gain or the risk of loss from the assets contributed to the pension fund are borne by the employee.

A) The employer's contribution each period is based on a formula.

B) The benefits to be received by employees are usually determined by an employee's three highest years of salary.

C) The accounting for a defined-contribution plan is straightforward and uncomplicated.

D) The benefit of gain or the risk of loss from the assets contributed to the pension fund are borne by the employee.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

10

In accounting for a defined-benefit pension plan

A) an appropriate funding pattern must be established to ensure that enough monies will be available at retirement to meet the benefits promised.

B) the employer's responsibility is simply to make a contribution each year based on the formula established in the plan.

C) the expense recognized each period is equal to the cash contribution.

D) the liability is determined based upon known variables that reflect future salary levels promised to employees.

A) an appropriate funding pattern must be established to ensure that enough monies will be available at retirement to meet the benefits promised.

B) the employer's responsibility is simply to make a contribution each year based on the formula established in the plan.

C) the expense recognized each period is equal to the cash contribution.

D) the liability is determined based upon known variables that reflect future salary levels promised to employees.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

11

In computing the service cost component of pension expense, the FASB concluded that

A) the accumulated benefit obligation provides a more realistic measure of the pension obligation on a going concern basis.

B) a company should employ an actuarial funding method to report pension expense that best reflects the cost of benefits to employees.

C) the projected benefit obligation using future compensation levels provides a realistic measure of present pension obligation and expense.

D) all of these.

A) the accumulated benefit obligation provides a more realistic measure of the pension obligation on a going concern basis.

B) a company should employ an actuarial funding method to report pension expense that best reflects the cost of benefits to employees.

C) the projected benefit obligation using future compensation levels provides a realistic measure of present pension obligation and expense.

D) all of these.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

12

A company gives each of its 50 employees (assume they were all employed continuously through 2007 and 2008) 12 days of vacation a year if they are employed at the end of the year. The vacation accumulates and may be taken starting January 1 of the next year. The employees work 8 hours per day. In 2007, they made $14 per hour and in 2008 they made $16 per hour. During 2008, they took an average of 9 days of vacation each. The company's policy is to record the liability existing at the end of each year at the wage rate for that year. What amount of vacation liability would be reflected on the 2007 and 2008 balance sheets, respectively?

A) $67,200; $93,600

B) $76,800; $96,000

C) $67,200; $96,000

D) $76,800; $93,600

A) $67,200; $93,600

B) $76,800; $96,000

C) $67,200; $96,000

D) $76,800; $93,600

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

13

The total payroll of Waters Company for the month of October, 2008 was $360,000, of which $90,000 represented amounts paid in excess of $90,000 to certain employees. $300,000 represented amounts paid to employees in excess of the $7,000 maximum subject to unemployment taxes. $90,000 of federal income taxes and $9,000 of union dues were withheld. The state unemployment tax is 1%, the federal unemployment tax is .8%, and the current F.I.C.A. tax is 7.65% on an employee's wages to $90,000 and 1.45% in excess of $90,000. What amount should Waters record as payroll tax expense?

A) $118,620

B) $113,040

C) $23,040

D) $28,440

A) $118,620

B) $113,040

C) $23,040

D) $28,440

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

14

On December 31, 2007, Filmore Company granted some of its executives options to purchase 50,000 shares of the company's $10 par common stock at an option price of $50 per share. The options become exercisable on January 1, 2008, and represent compensation for executives' services over a three-year period beginning January 1, 2008. The Black-Scholes option pricing model determines total compensation expense to be $300,000. At December 31, 2008, none of the executives had exercised their options.

What is the impact on Filmore's net income for the year ended December 31, 2008 as a result of this transaction under the fair value method?

A) $100,000 increase

B) $0

C) $100,000 decrease

D) $300,000 decrease

What is the impact on Filmore's net income for the year ended December 31, 2008 as a result of this transaction under the fair value method?

A) $100,000 increase

B) $0

C) $100,000 decrease

D) $300,000 decrease

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

15

Yunger Corp. on January 1, 2004, granted stock options for 40,000 shares of its $10 par value common stock to its key employees. The market price of the common stock on that date was $23 per share and the option price was $20. The Black-Scholes option pricing model determines total compensation expense to be $240,000. The options are exercisable beginning January 1, 2007, provided those key employees are still in Yunger's employ at the time the options are exercised. The options expire on January 1, 2008.

On January 1, 2007, when the market price of the stock was $29 per share, all 40,000 options were exercised. The amount of compensation expense Yunger should record for 2006 under the fair value method is

A) $0.

B) $40,000.

C) $80,000.

D) $120,000.

On January 1, 2007, when the market price of the stock was $29 per share, all 40,000 options were exercised. The amount of compensation expense Yunger should record for 2006 under the fair value method is

A) $0.

B) $40,000.

C) $80,000.

D) $120,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

16

On December 31, 2007, Jansen Company granted some of its executives options to purchase 45,000 shares of the company's $50 par common stock at an option price of $60 per share. The Black-Scholes option pricing model determines total compensation expense to be $900,000. The options become exercisable on January 1, 2008, and represent compensation for executives' past and future services over a three-year period beginning January 1, 2008. What is the impact on Jansen's total stockholders' equity for the year ended December 31, 2007, as a result of this transaction under the fair value method?

A) $900,000 decrease

B) $300,000 decrease

C) $0

D) $300,000 increase

A) $900,000 decrease

B) $300,000 decrease

C) $0

D) $300,000 increase

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

17

On June 30, 2004, Sealey Corporation granted compensatory stock options for 30,000 shares of its $20 par value common stock to certain of its key employees. The market price of the common stock on that date was $36 per share and the option price was $30. The Black-Scholes option pricing model determines total compensation expense to be $360,000. The options are exercisable beginning January 1, 2007, provided those key employees are still in Sealey's employ at the time the options are exercised. The options expire on June 30, 2008.

On January 4, 2007, when the market price of the stock was $42 per share, all 30,000 options were exercised. What should be the amount of compensation expense recorded by Sealey Corporation for the calendar year 2006 using the fair value method?

A) $0

B) $144,000

C) $180,000

D) $360,000

On January 4, 2007, when the market price of the stock was $42 per share, all 30,000 options were exercised. What should be the amount of compensation expense recorded by Sealey Corporation for the calendar year 2006 using the fair value method?

A) $0

B) $144,000

C) $180,000

D) $360,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

18

In order to retain certain key executives, Tanner Corporation granted them incentive stock options on December 31, 2006. 50,000 options were granted at an option price of $35 per share. Market prices of the stock were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2007. The Black-Scholes option pricing model determines total compensation expense to be $500,000. What amount of compensation expense should Tanner recognize as a result of this plan for the year ended December 31, 2007 under the fair value method?

A) $250,000

B) $500,000

C) $550,000

D) $1,750,000

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2007. The Black-Scholes option pricing model determines total compensation expense to be $500,000. What amount of compensation expense should Tanner recognize as a result of this plan for the year ended December 31, 2007 under the fair value method?A) $250,000

B) $500,000

C) $550,000

D) $1,750,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

19

Presented below is pension information related to Tyler, Inc. for the year 2008:

The amount of pension expense to be reported for 2008 is

A) $108,000.

B) $144,000.

C) $162,000.

D) $120,000.

The amount of pension expense to be reported for 2008 isA) $108,000.

B) $144,000.

C) $162,000.

D) $120,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

20

Randel, Inc. received the following information from its pension plan trustee concerning the operation of the company's defined-benefit pension plan for the year ended December 31, 2008.

Accounting for Compensation 16 - 15

The service cost component of pension expense for 2008 is $360,000 and the amortization of prior service cost due to an increase in benefits is $60,000. The settlement rate is 10% and the expected rate of return is 9%. What is the amount of pension expense for 2008?

A) $360,000

B) $522,000

C) $531,000

D) $432,000

Accounting for Compensation 16 - 15 The service cost component of pension expense for 2008 is $360,000 and the amortization of prior service cost due to an increase in benefits is $60,000. The settlement rate is 10% and the expected rate of return is 9%. What is the amount of pension expense for 2008?A) $360,000

B) $522,000

C) $531,000

D) $432,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

21

The following information for Monroe Enterprises is given below:

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.

-What is the pension expense that Monroe Enterprises should report for 2008?

A) $86,050

B) $110,000

C) $60,000

D) $83,950

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.-What is the pension expense that Monroe Enterprises should report for 2008?

A) $86,050

B) $110,000

C) $60,000

D) $83,950

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

22

The following information for Monroe Enterprises is given below:

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.

-What is the amount that Monroe Enterprises should report as its pension liability on its balance sheet as of December 31, 2008?

A) $100,000

B) $15,000

C) $185,000

D) $200,000

There were no actuarial gains or losses at January 1, 2008. The average remaining service life of employees is 10 years.-What is the amount that Monroe Enterprises should report as its pension liability on its balance sheet as of December 31, 2008?

A) $100,000

B) $15,000

C) $185,000

D) $200,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

23

Presented below is pension information for Welch Company for the year 2008:

The amount of pension expense to be reported for 2008 is

A) $93,000.

B) $69,000.

C) $60,000.

D) $45,000.

The amount of pension expense to be reported for 2008 isA) $93,000.

B) $69,000.

C) $60,000.

D) $45,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

24

Downing, Inc. received the following information from its pension plan trustee concerning the operation of the company's defined-benefit pension plan for the year ended December 31, 2008.

The service cost component of pension expense for 2008 is $840,000 and the amortization of unrecognized prior service cost is $180,000. The settlement rate is 10% and the expected rate of return is 8%. What is the amount of pension expense for 2008?

A) $1,716,000

B) $1,680,000

C) $1,608,000

D) $1,440,000

The service cost component of pension expense for 2008 is $840,000 and the amortization of unrecognized prior service cost is $180,000. The settlement rate is 10% and the expected rate of return is 8%. What is the amount of pension expense for 2008?A) $1,716,000

B) $1,680,000

C) $1,608,000

D) $1,440,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

25

The following data are for the pension plan for the employees of Nickels Company.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.

-The actual return on plan assets in 2008 was

A) $900,000.

B) $765,000.

C) $600,000.

D) $465,000.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.-The actual return on plan assets in 2008 was

A) $900,000.

B) $765,000.

C) $600,000.

D) $465,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

26

The following data are for the pension plan for the employees of Nickels Company.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.

-Assume that the actual return on plan assets in 2008 was $765,000. The unexpected gain on plan assets in 2008 was

A) $156,000.

B) $135,000.

C) $114,000.

D) $72,000.

Nickels' contribution was $1,260,000 in 2008 and benefits paid were $1,125,000. Nickels esti-mates that the average remaining service life is 15 years.-Assume that the actual return on plan assets in 2008 was $765,000. The unexpected gain on plan assets in 2008 was

A) $156,000.

B) $135,000.

C) $114,000.

D) $72,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

27

-The balance of the projected benefit obligation at December 31, 2008 is

A) $2,685,000.

B) $2,385,000.

C) $2,355,000.

D) $2,337,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

28

-The fair value of plan assets at December 31, 2008 is

A) $2,430,000.

B) $2,250,000.

C) $2,232,000.

D) $2,214,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

29

The following information relates to the pension plan for the employees of Polzin Co.:

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.

-The interest cost for 2008 is

A) $537,840.

B) $607,200.

C) $657,360.

D) $880,440.

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.-The interest cost for 2008 is

A) $537,840.

B) $607,200.

C) $657,360.

D) $880,440.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

30

The following information relates to the pension plan for the employees of Polzin Co.:

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.

-The actual return on plan assets in 2008 is

A) $408,000.

B) $456,000.

C) $588,000.

D) $648,000.

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.-The actual return on plan assets in 2008 is

A) $408,000.

B) $456,000.

C) $588,000.

D) $648,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

31

The following information relates to the pension plan for the employees of Polzin Co.:

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.

-The unexpected gain or loss on plan assets in 2008 is

A) $39,360 loss.

B) $22,560 gain.

C) $19,200 gain.

D) $214,560 gain.

Polzin estimates that the average remaining service life is 16 years. Polzin's contribution was $756,000 in 2008 and benefits paid were $564,000.-The unexpected gain or loss on plan assets in 2008 is

A) $39,360 loss.

B) $22,560 gain.

C) $19,200 gain.

D) $214,560 gain.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

32

Presented below is information related to Bitner Manufacturing Company as of December 31, 2008:

The amount for the prior service cost is related to a decrease in benefits. The fair value of the pension plan assets is $600,000.

The pension asset/liability reported on the balance sheet at December 31, 2008 is a

A) $300,000.

B) $600,000.

C) $900,000.

D) $1,305,000.

The amount for the prior service cost is related to a decrease in benefits. The fair value of the pension plan assets is $600,000.The pension asset/liability reported on the balance sheet at December 31, 2008 is a

A) $300,000.

B) $600,000.

C) $900,000.

D) $1,305,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

33

Barkley Corporation received the following report from its actuary at the end of the year:

-The amount reported as the pension liability at December 31, 2007 is

A) $0.

B) $200,000.

C) $220,000.

D) $300,000.

-The amount reported as the pension liability at December 31, 2007 is

A) $0.

B) $200,000.

C) $220,000.

D) $300,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

34

Barkley Corporation received the following report from its actuary at the end of the year:

-The amount reported as the pension liability at December 31, 2008 is

A) $1,800,000.

B) $1,480,000.

C) $380,000.

D) $360,000.

-The amount reported as the pension liability at December 31, 2008 is

A) $1,800,000.

B) $1,480,000.

C) $380,000.

D) $360,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

35

-The amount reported as the liability for pensions on the December 31, 2007 balance sheet is

A) $0.

B) $30,000.

C) $360,000.

D) $390,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

36

-The amount reported as the liability for pensions on the December 31, 2008 balance sheet is

A) $0.

B) $60,000.

C) $1,884,000.

D) $520,000.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

37

Quirk Corp.'s payroll for the pay period ended October 31, 2008 is summarized as follows:

What amount should Quirk accrue as its share of payroll taxes in its October 31, 2008 balance sheet?

A) $21,300

B) $14,720

C) $13,880

D) $7,300

What amount should Quirk accrue as its share of payroll taxes in its October 31, 2008 balance sheet?A) $21,300

B) $14,720

C) $13,880

D) $7,300

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

38

On January 1, 2007, Doane Corp. granted an employee an option to purchase 6,000 shares of Doane's $5 par value common stock at $20 per share. The Black-Scholes option pricing model determines total compensation expense to be $140,000. The option became exercisable on December 31, 2008, after the employee completed two years of service. The market prices of Doane's stock were as follows:

For 2008, Doane should recognize compensation expense under the fair value method of

A) $90,000.

B) $30,000.

C) $70,000.

D) $0.

For 2008, Doane should recognize compensation expense under the fair value method ofA) $90,000.

B) $30,000.

C) $70,000.

D) $0.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

39

The following information pertains to Mellon Co.'s pension plan:

If no change in actuarial estimates occurred during 2008, Mellon's projected benefit obligation at December 31, 2008 was

A) $64,200.

B) $75,000.

C) $79,200.

D) $82,200.

If no change in actuarial estimates occurred during 2008, Mellon's projected benefit obligation at December 31, 2008 wasA) $64,200.

B) $75,000.

C) $79,200.

D) $82,200.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

40

Reser Corp., a company whose stock is publicly traded, provides a noncontributory defined-benefit pension plan for its employees. The company's actuary has provided the following information for the year ended December 31, 2008:

The market -related asset value equals the fair value of plan assets. No contributions have been made for 2008 pension cost. In its December 31, 2008 balance sheet, Reser should report a(n)

A) $600,000 pension liability.

B) $824,000 pension asset.

C) $225,000 pension asset.

D) $525,000 pension liability.

The market -related asset value equals the fair value of plan assets. No contributions have been made for 2008 pension cost. In its December 31, 2008 balance sheet, Reser should report a(n)A) $600,000 pension liability.

B) $824,000 pension asset.

C) $225,000 pension asset.

D) $525,000 pension liability.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

41

Ohlman, Inc. maintains a defined-benefit pension plan for its employees. As of December 31, 2008, the market value of the plan assets is less than the accumulated benefit obligation. The projected benefit obligation exceeds the accumulated benefit obligation. In its balance sheet as of December 31, 2008, Ohlman should report a minimum liability in the amount of the

A) excess of the projected benefit obligation over the fair value of the plan assets.

B) excess of the accumulated benefit obligation over the fair value of the plan assets.

C) projected benefit obligation.

D) accumulated benefit obligation.

A) excess of the projected benefit obligation over the fair value of the plan assets.

B) excess of the accumulated benefit obligation over the fair value of the plan assets.

C) projected benefit obligation.

D) accumulated benefit obligation.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

42

At December 31, 2008, the following information was provided by the Nilges Corp. pension plan administrator:

What is the amount of the pension liability that should be shown on Nilges' December 31, 2008 balance sheet?

A) $7,200,000

B) $2,700,000

C) $1,620,000

D) $1,080,000

What is the amount of the pension liability that should be shown on Nilges' December 31, 2008 balance sheet?A) $7,200,000

B) $2,700,000

C) $1,620,000

D) $1,080,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 42 flashcards in this deck.