Deck 14: Investments

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2008, Alton Co. purchased $100,000 of 10%, Olson, Inc. bonds with interest payable on July 1 and January 1 for $107,000. On February 1, 2008, Alton purchased $100,000 of 12%, Ehrlich Co. bonds with interest payable on August 1 and February 1 for $95,000. Alton classifies the Olson and Ehrlich bonds as trading debt securities. On December 31, 2008, the fair value of the Olson and Ehrlich bonds are $110,000 and $94,000, respectively. At December, 2008, what adjusting entry should be made by Alton?

A) No entry should be made.

B)

C)

D)

A) No entry should be made.

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The following information relates to Vernon Company for 2008:

Vernon's 2008 other comprehensive income is

Vernon's 2008 other comprehensive income is

A) $25,000.

B) $40,000.

C) $50,000.

D) $60,000.

Vernon's 2008 other comprehensive income isA) $25,000.

B) $40,000.

C) $50,000.

D) $60,000.

Question

Question

Unruh Corp. began operations in 2008. An analysis of Unruh's equity securities portfolio acquired in 2008 shows the following totals at December 31, 2008 for trading and available-for-sale securities:

What amount should Unruh report in its 2008 income statement for unrealized holding loss?

What amount should Unruh report in its 2008 income statement for unrealized holding loss?

A) $40,000

B) $10,000

C) $15,000

D) $25,000

What amount should Unruh report in its 2008 income statement for unrealized holding loss?A) $40,000

B) $10,000

C) $15,000

D) $25,000

Question

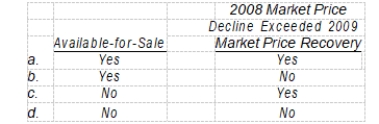

On December 29, 2009, Greer Co. sold an equity security that had been purchased on January 4, 2008. Greer owned no other equity securities. An unrealized holding loss was reported in the 2008 income statement. A realized gain was reported in the 2009 income statement. Was the equity security classified as available-for-sale and did its 2008 market price decline exceed its 2009 market price recovery?

Question

Question

Question

Question

Question

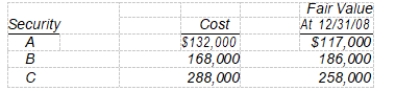

On December 31, 2007, Nance Co. purchased equity securities as trading securities. Pertinent data are as follows:

On December 31, 2008, Nance transferred its investment in security C from trading to available-for-sale because Nance intends to retain security C as a long- term investment. What total amount of gain or loss on its securities should be included in Nance's income statement for the year ended December 31, 2008?

On December 31, 2008, Nance transferred its investment in security C from trading to available-for-sale because Nance intends to retain security C as a long- term investment. What total amount of gain or loss on its securities should be included in Nance's income statement for the year ended December 31, 2008?

A) $3,000 gain

B) $27,000 loss

C) $30,000 loss

D) $45,000 loss

On December 31, 2008, Nance transferred its investment in security C from trading to available-for-sale because Nance intends to retain security C as a long- term investment. What total amount of gain or loss on its securities should be included in Nance's income statement for the year ended December 31, 2008?A) $3,000 gain

B) $27,000 loss

C) $30,000 loss

D) $45,000 loss

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/48

Play

Full screen (f)

Deck 14: Investments

1

Both debt securities and equity securities can be classified as held-to-maturity.

False

2

Amortization of discount or premium on available-for-sale debt securities is debited or credited to the Available-for-Sale Securities account.

True

3

Amortization of discount or premium on trading debt securities is debited or credited to the Securities Fair Value Adjustment (Trading) account.

False

4

The fair value method requires that companies classify equity securities at acquisition as held-to-maturity securities or available-for-sale securities.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

5

When an investor has holdings of less than 20% in an investee and the securities are classified as trading securities, unrealized holding gains or losses are reported as part of net income.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

6

In instances of "significant influence" (generally an investment of 20% or more), the investor is required to account for the investment using the equity method.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

7

The equity method gives recognition to the fact that investee earnings increase investee net assets that underlie the investment and investee losses and dividends decrease the net assets.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

8

Once the equity method is adopted by an investor, the method must continue in use until the investment to which it has been applied is sold or liquidated by some other means.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

9

Trading securities and available-for-sale securities are classified as current or noncurrent assets depending on the circumstances.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

10

When a company sells available-for-sale securities, a reclassification adjustment is neces-sary to avoid counting gains and losses twice.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

11

Held-to-maturity securities should be classified as current or noncurrent, based on the maturity date of the individual securities.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

12

For debt securities, the impairment test is to determine whether "it is probable that the investor will be unable to collect all amounts due according to the contractual terms."

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

13

Subsequent increases and decreases in the fair value of impaired available-for-sale securities are included in other comprehensive income.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

14

The transfer of securities from trading to available-for-sale and from available-for-sale to trading has the same impact on stockholders' equity and net income.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

15

When an investor's accounting period ends on a date that does not coincide with an interest receipt date for bonds held as an investment, the investor must

A) make an adjusting entry to debit Interest Receivable and to credit Interest Revenue for the amount of interest accrued since the last interest receipt date.

B) notify the issuer and request that a special payment be made for the appropriate portion of the interest period.

C) make an adjusting entry to debit Interest Receivable and to credit Interest Revenue for the total amount of interest to be received at the next interest receipt date.

D) do nothing special and ignore the fact that the accounting period does not coincide with the bond's interest period.

A) make an adjusting entry to debit Interest Receivable and to credit Interest Revenue for the amount of interest accrued since the last interest receipt date.

B) notify the issuer and request that a special payment be made for the appropriate portion of the interest period.

C) make an adjusting entry to debit Interest Receivable and to credit Interest Revenue for the total amount of interest to be received at the next interest receipt date.

D) do nothing special and ignore the fact that the accounting period does not coincide with the bond's interest period.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

16

Use of the effective-interest method in amortizing bond premiums and discounts results in

A) a greater amount of interest income over the life of the bond issue than would result from use of the straight-line method.

B) a varying amount being recorded as interest income from period to period.

C) a variable rate of return on the book value of the investment.

D) a smaller amount of interest income over the life of the bond issue than would result from use of the straight-line method.

A) a greater amount of interest income over the life of the bond issue than would result from use of the straight-line method.

B) a varying amount being recorded as interest income from period to period.

C) a variable rate of return on the book value of the investment.

D) a smaller amount of interest income over the life of the bond issue than would result from use of the straight-line method.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

17

Solo Co. purchased $300,000 of bonds for $315,000. If Solo intends to hold the securities to maturity, the entry to record the investment includes

A) a debit to Held-to-Maturity Securities at $300,000.

B) a credit to Premium on Investments of $15,000.

C) a debit to Held-to-Maturity Securities at $315,000.

D) none of these.

A) a debit to Held-to-Maturity Securities at $300,000.

B) a credit to Premium on Investments of $15,000.

C) a debit to Held-to-Maturity Securities at $315,000.

D) none of these.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

18

If a company has acquired a 20% to 50% interest in another corporation, this generally results in a(n)

A) insignificant level of influence. b passive level of influence.

B) passive level of influence.

C) significant level of influence.

D) controlling level of influence.

A) insignificant level of influence. b passive level of influence.

B) passive level of influence.

C) significant level of influence.

D) controlling level of influence.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

19

McCoy Corporation purchased 7,400 shares of Chudzick Company's common stock. The purchase price was $362,600, which is equal to 50% of Chudzick Company's retained earnings balance. Chudzick Company's 46,000 shares of common stock are actively traded, and each share has a par value of $10. McCoy Corporation should account for this long-term investment using the

A) fair value method.

B) equity method.

C) consolidation method.

D) amortized cost method.

A) fair value method.

B) equity method.

C) consolidation method.

D) amortized cost method.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

20

When a company holds between 20% and 50% of the outstanding stock of an investee, which of the following statements applies?

A) The investor should always use the equity method to account for its investment.

B) The investor should use the equity method to account for its investment unless circum-stances indicate that it is unable to exercise "significant influence" over the investee.

C) The investor must use the fair value method unless it can clearly demonstrate the ability to exercise "significant influence" over the investee.

D) The investor should always use the fair value method to account for its investment.

A) The investor should always use the equity method to account for its investment.

B) The investor should use the equity method to account for its investment unless circum-stances indicate that it is unable to exercise "significant influence" over the investee.

C) The investor must use the fair value method unless it can clearly demonstrate the ability to exercise "significant influence" over the investee.

D) The investor should always use the fair value method to account for its investment.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

21

On August 1, 2008, Witten Co. acquired 200, $1,000, 9% bonds at 97 plus accrued interest. The bonds were dated May 1, 2008, and mature on April 30, 2014, with interest paid each October 31 and April 30. The bonds will be added to Witten's available-for-sale portfolio. The preferred entry to record the purchase of the bonds on August 1, 2008 is

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

22

Oliver Company purchased $400,000 of 10% bonds of McGee Co. on January 1, 2008, paying $376,100. The bonds mature January 1, 2018; interest is payable each July 1 and January 1. The discount of $23,900 provides an effective yield of 11%. Oliver Company uses the effective-interest method and plans to hold these bonds to maturity.

-On July 1, 2008, Oliver Company should increase its Held-to-Maturity Debt Securities account for the McGee Co. bonds by

A) $2,392.

B) $1,371.

C) $1,196.

D) $686.

-On July 1, 2008, Oliver Company should increase its Held-to-Maturity Debt Securities account for the McGee Co. bonds by

A) $2,392.

B) $1,371.

C) $1,196.

D) $686.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

23

Oliver Company purchased $400,000 of 10% bonds of McGee Co. on January 1, 2008, paying $376,100. The bonds mature January 1, 2018; interest is payable each July 1 and January 1. The discount of $23,900 provides an effective yield of 11%. Oliver Company uses the effective-interest method and plans to hold these bonds to maturity.

-For the year ended December 31, 2008, Oliver Company should report interest revenue from the McGee Co. bonds of

A) $42,392.

B) $41,409.

C) $41,368.

D) $40,000.

-For the year ended December 31, 2008, Oliver Company should report interest revenue from the McGee Co. bonds of

A) $42,392.

B) $41,409.

C) $41,368.

D) $40,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

24

On October 1, 2008, Porter Co. purchased to hold to maturity, 1,000, $1,000, 9% bonds for $990,000 which includes $15,000 accrued interest. The bonds, which mature on February 1, 2017, pay interest semiannually on February 1 and August 1. Porter uses the straight-line method of amortization. The bonds should be reported in the December 31, 2008 balance sheet at a carrying value of

A) $975,000.

B) $975,750.

C) $990,000.

D) $990,250.

A) $975,000.

B) $975,750.

C) $990,000.

D) $990,250.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

25

On November 1, 2008, Little Company purchased 600 of the $1,000 face value, 9% bonds of Player, Incorporated, for $632,000, which includes accrued interest of $9,000. The bonds, which mature on January 1, 2013, pay interest semiannually on March 1 and September 1. Assuming that Little uses the straight-line method of amortization and that the bonds are appropriately classified as available-for-sale, the net carrying value of the bonds should be shown on Little's December 31, 2008, balance sheet at

A) $600,000.

B) $623,000.

C) $622,080.

D) $632,000.

A) $600,000.

B) $623,000.

C) $622,080.

D) $632,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

26

On November 1, 2008, Morton Co. purchased Gomez, Inc., 10-year, 9% bonds with a face value of $250,000, for $225,000. An additional $7,500 was paid for the accrued interest. Interest is payable semiannually on January 1 and July 1. The bonds mature on July 1, 2015. Morton uses the straight-line method of amortization. Ignoring income taxes, the amount reported in Morton's 2008 income statement as a result of Morton's available-for-sale investment in Gomez was

A) $4,375.

B) $4,167.

C) $3,750.

D) $3,333.

A) $4,375.

B) $4,167.

C) $3,750.

D) $3,333.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

27

On October 1, 2008, Lyman Co. purchased to hold to maturity, 200, $1,000, 9% bonds for $208,000. An additional $6,000 was paid for accrued interest. Interest is paid semiannually on December 1 and June 1 and the bonds mature on December 1, 2012. Lyman uses straight-line amortization. Ignoring income taxes, the amount reported in Lyman's 2008 income statement from this investment should be

A) $4,500.

B) $4,020.

C) $4,980.

D) $5,460.

A) $4,500.

B) $4,020.

C) $4,980.

D) $5,460.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

28

On January 1, 2008, Alton Co. purchased $100,000 of 10%, Olson, Inc. bonds with interest payable on July 1 and January 1 for $107,000. On February 1, 2008, Alton purchased $100,000 of 12%, Ehrlich Co. bonds with interest payable on August 1 and February 1 for $95,000. Alton classifies the Olson and Ehrlich bonds as trading debt securities. On December 31, 2008, the fair value of the Olson and Ehrlich bonds are $110,000 and $94,000, respectively. At December, 2008, what adjusting entry should be made by Alton?

A) No entry should be made.

B)

C)

D)

A) No entry should be made.

B)

C)

D)

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

29

On January 3, 2008, Slezak Company purchased 22% of Urban Corporation's common stock for $250,000. Shortly after the purchase, Slezak Company executives tried to obtain representation on Urban Corporation's board of directors and failed. During 2008, Urban reported net income of $150,000 and paid cash dividends of $80,000 on the common stock. The balance in Slezak Company's Investment in Urban Corporation account at December 31, 2008, should be

A) $265,400.

B) $234,600.

C) $250,000.

D) $300,600.

A) $265,400.

B) $234,600.

C) $250,000.

D) $300,600.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

30

On its December 31, 2007, balance sheet, Quinn Co. reported its investment in available-for-sale securities, which had cost $600,000, at fair value of $550,000. At December 31, 2008, the fair value of the securities was $585,000. What should Quinn report on its 2008 income statement as a result of the increase in fair value of the investments in 2008?

A) $0

B) Unrealized loss of $15,000

C) Realized gain of $35,000

D) Unrealized gain of $35,000

A) $0

B) Unrealized loss of $15,000

C) Realized gain of $35,000

D) Unrealized gain of $35,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

31

During 2007, Ellis Company purchased 20,000 shares of Hiller Corp. common stock for $315,000 as an available-for-sale investment. The fair value of these shares was $300,000 at December 31, 2007. Ellis sold all of the Hiller stock for $17 per share on December 3, 2008, incurring $14,000 in brokerage commissions. Ellis Company should report a realized gain on the sale of stock in 2008 of

A) $11,000.

B) $25,000.

C) $26,000.

D) $40,000.

A) $11,000.

B) $25,000.

C) $26,000.

D) $40,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

32

Garrison Co. owns 20,000 of the 50,000 outstanding shares of Steele, Inc. common stock.

During 2008, Steele earns $800,000 and pays cash dividends of $640,000.

-If the beginning balance in the investment account was $500,000, the balance at December 31, 2008 should be

A) $820,000.

B) $660,000.

C) $564,000.

D) $500,000.

During 2008, Steele earns $800,000 and pays cash dividends of $640,000.

-If the beginning balance in the investment account was $500,000, the balance at December 31, 2008 should be

A) $820,000.

B) $660,000.

C) $564,000.

D) $500,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

33

Garrison Co. owns 20,000 of the 50,000 outstanding shares of Steele, Inc. common stock.

During 2008, Steele earns $800,000 and pays cash dividends of $640,000.

-Garrison should report investment revenue for 2008 of

A) $320,000.

B) $256,000.

C) $64,000.

D) $0.

During 2008, Steele earns $800,000 and pays cash dividends of $640,000.

-Garrison should report investment revenue for 2008 of

A) $320,000.

B) $256,000.

C) $64,000.

D) $0.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

34

If Karter Company uses the equity method of accounting for its investment in Flynn Company, its Investment in Flynn Company account at December 31, 2008 should be

A) $290,000.

B) $300,000.

C) $330,000.

D) $340,000.

A) $290,000.

B) $300,000.

C) $330,000.

D) $340,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

35

Barry Corporation earns $240,000 and pays cash dividends of $80,000 during 2008. Glenon Corporation owns 3,000 of the 10,000 outstanding shares of Barry.

-What amount should Glenon show in the investment account at December 31, 2008 if the beginning of the year balance in the account was $320,000?

A) $392,000

B) $320,000

C) $368,000

D) $480,000

-What amount should Glenon show in the investment account at December 31, 2008 if the beginning of the year balance in the account was $320,000?

A) $392,000

B) $320,000

C) $368,000

D) $480,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

36

Barry Corporation earns $240,000 and pays cash dividends of $80,000 during 2008. Glenon Corporation owns 3,000 of the 10,000 outstanding shares of Barry.

-How much investment income should Glenon report in 2008?

A) $80,000

B) $72,000

C) $48,000

D) $240,000

-How much investment income should Glenon report in 2008?

A) $80,000

B) $72,000

C) $48,000

D) $240,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

37

Young Co. acquired a 60% interest in Tomlin Corp. on December 31, 2007 for $945,000. During 2008, Tomlin had net income of $600,000 and paid cash dividends of $150,000. At December 31, 2008, the balance in the investment account should be

A) $945,000.

B) $1,305,000.

C) $1,215,000.

D) $1,395,000.

A) $945,000.

B) $1,305,000.

C) $1,215,000.

D) $1,395,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

38

Stone Co. owns 4,000 of the 10,000 outstanding shares of Maye Corp. common stock. During 2008, Maye earns $120,000 and pays cash dividends of $40,000.

-If the beginning balance in the investment account was $240,000, the balance at December 31, 2008 should be

A) $240,000.

B) $272,000.

C) $288,000.

D) $320,000.

-If the beginning balance in the investment account was $240,000, the balance at December 31, 2008 should be

A) $240,000.

B) $272,000.

C) $288,000.

D) $320,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

39

Stone Co. owns 4,000 of the 10,000 outstanding shares of Maye Corp. common stock. During 2008, Maye earns $120,000 and pays cash dividends of $40,000.

-Stone should report investment revenue for 2008 of

A) $16,000.

B) $32,000.

C) $40,000.

D) $48,000.

-Stone should report investment revenue for 2008 of

A) $16,000.

B) $32,000.

C) $40,000.

D) $48,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

40

The following information relates to Vernon Company for 2008:

Vernon's 2008 other comprehensive income is

A) $25,000.

B) $40,000.

C) $50,000.

D) $60,000.

Vernon's 2008 other comprehensive income isA) $25,000.

B) $40,000.

C) $50,000.

D) $60,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

41

On October 1, 2007, Ming Co. purchased 600 of the $1,000 face value, 8% bonds of Loy, Inc., for $702,000, including accrued interest of $12,000. The bonds, which mature on January 1, 2014, pay interest semiannually on January 1 and July 1. Ming used the straight-line method of amortization and appropriately recorded the bonds as available-for-sale. On Ming's December 31, 2008 balance sheet, the carrying value of the bonds is

A) $690,000.

B) $684,000.

C) $681,600.

D) $672,000.

A) $690,000.

B) $684,000.

C) $681,600.

D) $672,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

42

Unruh Corp. began operations in 2008. An analysis of Unruh's equity securities portfolio acquired in 2008 shows the following totals at December 31, 2008 for trading and available-for-sale securities:

What amount should Unruh report in its 2008 income statement for unrealized holding loss?

A) $40,000

B) $10,000

C) $15,000

D) $25,000

What amount should Unruh report in its 2008 income statement for unrealized holding loss?A) $40,000

B) $10,000

C) $15,000

D) $25,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

43

On December 29, 2009, Greer Co. sold an equity security that had been purchased on January 4, 2008. Greer owned no other equity securities. An unrealized holding loss was reported in the 2008 income statement. A realized gain was reported in the 2009 income statement. Was the equity security classified as available-for-sale and did its 2008 market price decline exceed its 2009 market price recovery?

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

44

Kimm, Inc. acquired 30% of Carne Corp.'s voting stock on January 1, 2008 for $400,000. During 2008, Carne earned $160,000 and paid dividends of $100,000. Kimm's 30% interest in Carne gives Kimm the ability to exercise significant influence over Carne's operating and financial policies. During 2009, Carne earned $200,000 and paid dividends of $60,000 on April 1 and $60,000 on October 1. On July 1, 2009, Kimm sold half of its stock in Carne for $264,000 cash.

-Before income taxes, what amount should Kimm include in its 2008 income statement as

A result of the investment?

A) $160,000

B) $100,000

C) $48,000

D) $30,000

-Before income taxes, what amount should Kimm include in its 2008 income statement as

A result of the investment?

A) $160,000

B) $100,000

C) $48,000

D) $30,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

45

Kimm, Inc. acquired 30% of Carne Corp.'s voting stock on January 1, 2008 for $400,000. During 2008, Carne earned $160,000 and paid dividends of $100,000. Kimm's 30% interest in Carne gives Kimm the ability to exercise significant influence over Carne's operating and financial policies. During 2009, Carne earned $200,000 and paid dividends of $60,000 on April 1 and $60,000 on October 1. On July 1, 2009, Kimm sold half of its stock in Carne for $264,000 cash.

-The carrying amount of this investment in Kimm's December 31, 2008 balance sheet should be

A) $400,000.

B) $418,000.

C) $448,000.

D) $460,000.

-The carrying amount of this investment in Kimm's December 31, 2008 balance sheet should be

A) $400,000.

B) $418,000.

C) $448,000.

D) $460,000.

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

46

Kimm, Inc. acquired 30% of Carne Corp.'s voting stock on January 1, 2008 for $400,000. During 2008, Carne earned $160,000 and paid dividends of $100,000. Kimm's 30% interest in Carne gives Kimm the ability to exercise significant influence over Carne's operating and financial policies. During 2009, Carne earned $200,000 and paid dividends of $60,000 on April 1 and $60,000 on October 1. On July 1, 2009, Kimm sold half of its stock in Carne for $264,000 cash.

-What should be the gain on sale of this investment in Kimm's 2009 income statement?

A) $64,000

B) $55,000

C) $49,000

D) $40,000

-What should be the gain on sale of this investment in Kimm's 2009 income statement?

A) $64,000

B) $55,000

C) $49,000

D) $40,000

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

47

On January 1, 2008, Sloane Co. purchased 25% of Orr Corp.'s common stock; no goodwill resulted from the purchase. Sloane appropriately carries this investment at equity and the balance in Sloane's investment account was $720,000 at December 31, 2008. Orr reported net income of $450,000 for the year ended December 31, 2008, and paid common stock dividends totaling $180,000 during 2008. How much did Sloane pay for its 25% interest in Orr?

A) $652,500

B) $765,000

C) $787,500

D) $877,500

A) $652,500

B) $765,000

C) $787,500

D) $877,500

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

48

On December 31, 2007, Nance Co. purchased equity securities as trading securities. Pertinent data are as follows:

On December 31, 2008, Nance transferred its investment in security C from trading to available-for-sale because Nance intends to retain security C as a long- term investment. What total amount of gain or loss on its securities should be included in Nance's income statement for the year ended December 31, 2008?

A) $3,000 gain

B) $27,000 loss

C) $30,000 loss

D) $45,000 loss

On December 31, 2008, Nance transferred its investment in security C from trading to available-for-sale because Nance intends to retain security C as a long- term investment. What total amount of gain or loss on its securities should be included in Nance's income statement for the year ended December 31, 2008?A) $3,000 gain

B) $27,000 loss

C) $30,000 loss

D) $45,000 loss

Unlock Deck

Unlock for access to all 48 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 48 flashcards in this deck.