Deck 12: Accounting for Liabilities

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

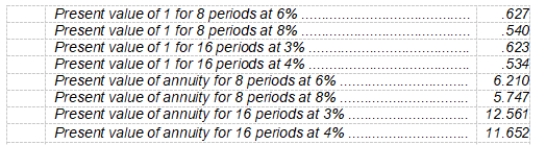

On January 1, 2008, Bleeker Co. issued eight-year bonds with a face value of $ 1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31. The bonds were sold to yield 8%. Table values are:

-The present value of the interest is

A) $344,820.

B) $349,560.

C) $372,600.

D) $376,830.

-The present value of the interest is

A) $344,820.

B) $349,560.

C) $372,600.

D) $376,830.

Question

On January 1, 2008, Bleeker Co. issued eight-year bonds with a face value of $ 1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31. The bonds were sold to yield 8%. Table values are:

-The issue price of the bonds is

A) $883,560.

B) $884,820.

C) $889,560.

D) $999,600.

-The issue price of the bonds is

A) $883,560.

B) $884,820.

C) $889,560.

D) $999,600.

Question

Question

The December 31, 2008, balance sheet of Eddy Corporation includes the following items:

The bonds were issued on December 31, 2007, at 103, with interest payable on July 1 and December 31 of each year. On January 2, 2009, Eddy retired $1,400,000 of these bonds at 98. What should Eddy record as a gain on retirement of these bonds? Ignore taxes.

The bonds were issued on December 31, 2007, at 103, with interest payable on July 1 and December 31 of each year. On January 2, 2009, Eddy retired $1,400,000 of these bonds at 98. What should Eddy record as a gain on retirement of these bonds? Ignore taxes.

A) $28,000

B) $37,800

C) $65,800

D) $70,000

The bonds were issued on December 31, 2007, at 103, with interest payable on July 1 and December 31 of each year. On January 2, 2009, Eddy retired $1,400,000 of these bonds at 98. What should Eddy record as a gain on retirement of these bonds? Ignore taxes.A) $28,000

B) $37,800

C) $65,800

D) $70,000

Question

Question

Question

Question

Question

Question

Question

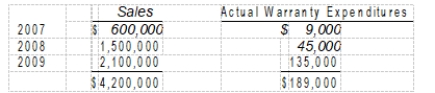

During 2007, Younger Co. introduced a new line of machines that carry a three-year warranty against manufacturer's defects. Based on industry experience, warranty costs are estimated at 2% of sales in the year of sale, 4% in the year after sale, and 6% in the second year after sale. Sales and actual warranty expenditures for the first three-year period were as follows:

What amount should Younger report as a liability at December 31, 2009?

What amount should Younger report as a liability at December 31, 2009?

A) $0

B) $15,000

C) $204,000

D) $315,000

What amount should Younger report as a liability at December 31, 2009?A) $0

B) $15,000

C) $204,000

D) $315,000

Question

Question

Kent Co. includes one coupon in each bag of dog food it sells. In return for eight coupons, customers receive a leash. The leashes cost Kent $2.00 each. Kent estimates that 40 percent of the coupons will be redeemed. Data for 2008 and 2009 are as follows:

-The premium expense for 2008 is

A) $25,000.

B) $30,000.

C) $35,000.

D) $50,000.

-The premium expense for 2008 is

A) $25,000.

B) $30,000.

C) $35,000.

D) $50,000.

Question

Kent Co. includes one coupon in each bag of dog food it sells. In return for eight coupons, customers receive a leash. The leashes cost Kent $2.00 each. Kent estimates that 40 percent of the coupons will be redeemed. Data for 2008 and 2009 are as follows:

-The estimated liability for premiums at December 31, 2008 is

A) $7,500.

B) $10,000.

C) $17,500.

D) $20,000.

-The estimated liability for premiums at December 31, 2008 is

A) $7,500.

B) $10,000.

C) $17,500.

D) $20,000.

Question

Question

Question

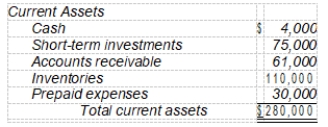

Presented below is information available for Norton Company.

Total current liabilities are $120,000. The acid-test ratio for Norton is

Total current liabilities are $120,000. The acid-test ratio for Norton is

A) 2.33 to 1.

B) 2.08 to 1.

C) 1.17 to 1.

D) .54 to 1.

Total current liabilities are $120,000. The acid-test ratio for Norton isA) 2.33 to 1.

B) 2.08 to 1.

C) 1.17 to 1.

D) .54 to 1.

Question

Question

Question

Question

Dexter Co. sells major household appliance service contracts for cash. The service contracts are for a one-year, two-year, or three-year period. Cash receipts from contracts are credited to unearned service contract revenues. This account had a balance of $480,000 at December 31, 2008 before year-end adjustment. Service contract costs are charged as incurred to the service contract expense account, which had a balance of $120,000 at December 31, 2008. Outstanding service contracts at December 31, 2008 expire as follows:

What amount should be reported as unearned service contract revenues in Dexter's December 31, 2008 balance sheet?

What amount should be reported as unearned service contract revenues in Dexter's December 31, 2008 balance sheet?

A) $360,000

B) $330,000

C) $240,000

D) $220,000

What amount should be reported as unearned service contract revenues in Dexter's December 31, 2008 balance sheet?A) $360,000

B) $330,000

C) $240,000

D) $220,000

Question

During 2008, Blass Co. introduced a new product carrying a two-year warranty against defects. The estimated warranty costs related to dollar sales are 2% within 12 months following sale and 4% in the second 12 months following sale. Sales and actual warranty expenditures for the years ended December 31, 2008 and 2009 are as follows:

At December 31, 2009, Blass should report an estimated warranty liability of

At December 31, 2009, Blass should report an estimated warranty liability of

A) $0.

B) $10,000.

C) $30,000.

D) $66,000.

At December 31, 2009, Blass should report an estimated warranty liability ofA) $0.

B) $10,000.

C) $30,000.

D) $66,000.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 12: Accounting for Liabilities

1

The only requirement for an obligation to be classified as a current liability is that it be liquidated within the operating cycle or one year, whichever is longer.

False

2

The currently maturing portion of a serial bond should not be classified as a current liability if it will be paid out of a long-term asset such as a sinking fund.

True

3

Preferred dividends in arrears should be recognized as a liability in the balance sheet.

False

4

A stock dividend distributable is classified as a long-term liability because it will not be liquidated using current assets.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

Generally, long-term debt, in whatever form, is issued subject to various covenants or restrictions for the protection of corporate stockholders.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

Revenue bonds are bonds whose interest rate is a function of the revenue earned by the company issuing the bonds.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

Bonds issued by a corporation represent a means of borrowing funds from the general public or institutional investors on a long-term basis.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

Bond discount should be reported in the balance sheet as a direct deduction from the face amount of the bond.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

The expenses associated with the issuance of bonds should be added to the bond discount or subtracted from the bond premium on the date the bonds are issued.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

Any excess of the net carrying amount over the reacquisition price is a loss from extinguishment.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

If a loss contingency is likely to occur and its amount can be reasonably estimated, it should be recorded in the accounts.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

One factor to consider in determining whether a liability should be recorded with respect to threatened litigation is the effect such a liability will have on a reported financial condition.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

To report a loss and a liability in the financial statements, the cause for litigation must have occurred on or before the date of the financial statements.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

Liabilities are generally measured by the present value of the future outlay of cash required to liquidate them.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

Long-term debt that matures within one year should be reported as a current liability, unless retirement is to be accomplished with other than current assets.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

Under the effective-interest method, semiannual interest expense is computed by multi-plying the effective-interest rate times a constant carrying value of the bonds.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

A liability has three essential characteristics. Which of the following is not one of them?

A) It is a present obligation that entails settlement by probable future transfer or use of cash, goods, or services.

B) The obligation must be liquidated using cash, goods, or services that were earned by the entity in the performance of its normal business operation.

C) The liability must be an unavoidable obligation.

D) The transaction or other event creating the obligation must have already occurred.

A) It is a present obligation that entails settlement by probable future transfer or use of cash, goods, or services.

B) The obligation must be liquidated using cash, goods, or services that were earned by the entity in the performance of its normal business operation.

C) The liability must be an unavoidable obligation.

D) The transaction or other event creating the obligation must have already occurred.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

Diana Co. issues a $208,000 6-month, zero-interest-bearing note to Tang National Bank. The present value of the note is $200,000. The entry to record this transaction by Diana Co. would include a

A) credit to Notes Payable of $200,000.

B) debit to Discount on Notes Payable of $8,000.

C) credit to Discount on Notes Payable of $8,000.

D) debit to Cash of $208,000.

A) credit to Notes Payable of $200,000.

B) debit to Discount on Notes Payable of $8,000.

C) credit to Discount on Notes Payable of $8,000.

D) debit to Cash of $208,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

The currently maturing portion of long-term debt should be classified as a current liability if

A) the debt is to be converted into capital stock.

B) the debt is to be refinanced on a long-term basis.

C) the funds used to liquidate it are currently classified as a long-term investment on the balance sheet.

D) the portion so classified will be liquidated within one year using current assets.

A) the debt is to be converted into capital stock.

B) the debt is to be refinanced on a long-term basis.

C) the funds used to liquidate it are currently classified as a long-term investment on the balance sheet.

D) the portion so classified will be liquidated within one year using current assets.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

If a corporation issues a debenture bond, it means the bond

A) is secured by stocks and bonds of other corporations.

B) matures in installments.

C) is unsecured.

D) may be converted into other securities of the corporation for a specified time after issuance.

A) is secured by stocks and bonds of other corporations.

B) matures in installments.

C) is unsecured.

D) may be converted into other securities of the corporation for a specified time after issuance.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

Bonds that are secured by stocks and bonds of other corporations are called

A) collateral trust bonds.

B) registered bonds.

C) serial bonds.

D) treasury bonds.

A) collateral trust bonds.

B) registered bonds.

C) serial bonds.

D) treasury bonds.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

A bond premium should be reported in the balance sheet

A) at the present value of the future reduction in bond interest expense due to the premium.

B) as a deferred credit.

C) along with other premium accounts such as those resulting from stock transactions.

D) as a direct addition to the face amount of the bond.

A) at the present value of the future reduction in bond interest expense due to the premium.

B) as a deferred credit.

C) along with other premium accounts such as those resulting from stock transactions.

D) as a direct addition to the face amount of the bond.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

Bond issue costs, such as printing costs, legal fees, commissions, etc. are most appropriately accounted for by

A) charging them to an expense account in the year the bonds are actually sold so there is revenue to charge them against on the income statement.

B) debiting them to Unamortized Bond-Issue Costs and amortizing them in a manner similar to bond discount over the life of the bond.

C) charging them to an expense account in the year the bonds are originally dated, whether or not they are sold in that year.

D) adding them to any discount on bonds or subtracting them from any premium on bonds when the bonds are sold.

A) charging them to an expense account in the year the bonds are actually sold so there is revenue to charge them against on the income statement.

B) debiting them to Unamortized Bond-Issue Costs and amortizing them in a manner similar to bond discount over the life of the bond.

C) charging them to an expense account in the year the bonds are originally dated, whether or not they are sold in that year.

D) adding them to any discount on bonds or subtracting them from any premium on bonds when the bonds are sold.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

When debt is extinguished before its maturity date, any difference between the reacquisi-tion price of outstanding debt and its net carrying amount per books should be

A) amortized over the remaining original life of the extinguished issue.

B) amortized over the life of the new issue.

C) recognized currently in income as a loss or gain.

D) treated as a prior period adjustment.

A) amortized over the remaining original life of the extinguished issue.

B) amortized over the life of the new issue.

C) recognized currently in income as a loss or gain.

D) treated as a prior period adjustment.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

The generally accepted method of accounting for gains or losses from the early extinguishment of debt treats any gain or loss as a(n)

A) adjustment to the cost basis of the asset obtained by the debt issue.

B) amount that should be considered a cash adjustment to the cost of any other debt issued over the remaining life of the old debt instrument.

C) amount received or paid to obtain a new debt instrument and, as such, should be amortized over the life of the new debt.

D) difference between the reacquisition price and the net carrying amount of the debt which should be recognized in the period of redemption.

A) adjustment to the cost basis of the asset obtained by the debt issue.

B) amount that should be considered a cash adjustment to the cost of any other debt issued over the remaining life of the old debt instrument.

C) amount received or paid to obtain a new debt instrument and, as such, should be amortized over the life of the new debt.

D) difference between the reacquisition price and the net carrying amount of the debt which should be recognized in the period of redemption.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

Mark Ward is a farmer who owns land which borders on the right-of-way of Northern Railroad. On August 10, 2008, due to Northern's admitted negligence, hay on the farm was set on fire and burned. Ward had had a dispute with the railroad for several years concerning the ownership of a small parcel of land. The representative of the railroad has offered to assign any rights which the railroad may have in the land to Ward in exchange for a release of his right to reimbursement for the loss he has sustained from the fire. Ward appears inclined to accept the railroad's offer. Northern Railroad's 2008 financial statements should include the following related to the incident:

A) recognition of a loss and creation of a liability for the value of the land.

B) recognition of a loss only.

C) creation of a liability only.

D) disclosure in note form only.

A) recognition of a loss and creation of a liability for the value of the land.

B) recognition of a loss only.

C) creation of a liability only.

D) disclosure in note form only.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

A contingency is defined by FASB Statement No. 5 as an

A) existing condition, situation, or set of circumstances involving uncertainty as to possible gain or loss to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur.

B) existing condition, situation, or set of circumstances involving uncertainty as to a possible loss to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur.

C) event that will result in the requirement to record a liability if it can be shown that an asset is in danger of being lost to the enterprise and the company has no ability to avoid the loss.

D) uncertain event that must have a reasonable chance of occurrence and the amount must be reasonably determinable by the company.

A) existing condition, situation, or set of circumstances involving uncertainty as to possible gain or loss to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur.

B) existing condition, situation, or set of circumstances involving uncertainty as to a possible loss to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur.

C) event that will result in the requirement to record a liability if it can be shown that an asset is in danger of being lost to the enterprise and the company has no ability to avoid the loss.

D) uncertain event that must have a reasonable chance of occurrence and the amount must be reasonably determinable by the company.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following loss contingencies is normally accrued?

A) Pending or threatened litigation

B) General or unspecified business risk

C) Obligations related to product warranties

D) Risk of property loss due to fire

A) Pending or threatened litigation

B) General or unspecified business risk

C) Obligations related to product warranties

D) Risk of property loss due to fire

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

If a loss is either probable or estimable, but not both, and if there is at least a reasonable possibility that a liability may have been incurred, the proper accounting treatment would be reflected by which of the following?

A) Record the loss and the related liability, but at an amount that is significantly conservative.

B) Record the loss and the related liability, but indicate in a footnote to the financial statements that this loss may not occur because one of the criteria may not be met.

C) Disclose in the footnotes to the financial statements (1) the nature of the contingency, and (2) an estimate of the possible loss or range of loss or a statement that an estimate cannot be made.

D) Do not record the contingency or make mention of it in the financial statements because it lacks meeting the required criteria.

A) Record the loss and the related liability, but at an amount that is significantly conservative.

B) Record the loss and the related liability, but indicate in a footnote to the financial statements that this loss may not occur because one of the criteria may not be met.

C) Disclose in the footnotes to the financial statements (1) the nature of the contingency, and (2) an estimate of the possible loss or range of loss or a statement that an estimate cannot be made.

D) Do not record the contingency or make mention of it in the financial statements because it lacks meeting the required criteria.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

Wilson Company is involved in a litigation suit concerning the clean-up of old underground oil storage tanks on property it sold to a housing development company five years ago. The attorneys for Wilson Company cannot give a best estimate for the probable liability; however, the attorneys state that the liability to Wilson Company will probably fall within a range of $2 million to $10 million. According to the SEC, what should Wilson Company record with regards to this environmental liability?

A) No entry is required.

B) A loss and liability of $10 million.

C) A loss and liability of $6 million.

D) A loss and liability of $2 million.

A) No entry is required.

B) A loss and liability of $10 million.

C) A loss and liability of $6 million.

D) A loss and liability of $2 million.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

Assume that a manufacturing corporation has (1) good quality control, (2) a one-year operating cycle, (3) a relatively stable pattern of annual sales, and (4) a continuing policy of guaranteeing new products against defects for three years that has resulted in material but rather stable warranty repair and replacement costs. Any liability for the warranty

A) should be reported as long-term.

B) should be reported as current.

C) should be reported as part current and part long-term.

D) need not be disclosed.

A) should be reported as long-term.

B) should be reported as current.

C) should be reported as part current and part long-term.

D) need not be disclosed.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

Lopez Corporation, a manufacturer of household paints, is preparing annual financial statements at December 31, 2008. Because of a recently proven health hazard in one of its paints, the government has clearly indicated its intention of having Lopez recall all cans of this paint sold in the last six months. The management of Lopez estimates that this recall would cost $800,000. What accounting recognition, if any, should be accorded this situation?

A) No recognition

B) Note disclosure only

C) Operating expense of $800,000 and liability of $800,000

D) Appropriation of retained earnings of $800,000

A) No recognition

B) Note disclosure only

C) Operating expense of $800,000 and liability of $800,000

D) Appropriation of retained earnings of $800,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

Information available prior to the issuance of the financial statements indicates that it is probable that, at the date of the financial statements, a liability has been incurred for obligations related to product warranties. The amount of the loss involved can be reasonably estimated. Based on the above facts, an estimated loss contingency should be

A) accrued.

B) disclosed but not accrued.

C) neither accrued nor disclosed.

D) classified as an appropriation of retained earnings.

A) accrued.

B) disclosed but not accrued.

C) neither accrued nor disclosed.

D) classified as an appropriation of retained earnings.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

Marx Company becomes aware of a lawsuit after the date of the financial statements, but before they are issued. A loss and related liability should be reported in the financial statements if the amount can be reasonably estimated, an unfavorable outcome is highly probable, and

A) Marx Company admits guilt.

B) the court will decide the case within one year.

C) the damages appear to be material.

D) the cause for action occurred during the accounting period covered by the financial statements.

A) Marx Company admits guilt.

B) the court will decide the case within one year.

C) the damages appear to be material.

D) the cause for action occurred during the accounting period covered by the financial statements.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is an example of "off-balance-sheet financing"?

1) Non-consolidated subsidiary

2) Special purpose entity

3) Operating leases

A) 1

B) 2

C) 3

D) All of these are examples of "off-balance-sheet financing."

1) Non-consolidated subsidiary

2) Special purpose entity

3) Operating leases

A) 1

B) 2

C) 3

D) All of these are examples of "off-balance-sheet financing."

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

When a business enterprise enters into what is referred to as off-balance-sheet financing, the company

A) is attempting to conceal the debt from shareholders by having no information about the debt included in the balance sheet.

B) wishes to confine all information related to the debt to the income statement and the statement of cash flows.

C) can enhance the quality of its financial position and perhaps permit credit to be obtained more readily and at less cost.

D) is in violation of generally accepted accounting principles.

A) is attempting to conceal the debt from shareholders by having no information about the debt included in the balance sheet.

B) wishes to confine all information related to the debt to the income statement and the statement of cash flows.

C) can enhance the quality of its financial position and perhaps permit credit to be obtained more readily and at less cost.

D) is in violation of generally accepted accounting principles.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following must be disclosed relative to long-term debt maturities and sinking fund requirements?

A) The present value of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

B) The present value of scheduled interest payments on long-term debt during each of the next five years.

C) The amount of scheduled interest payments on long-term debt during each of the next five years.

D) The amount of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

A) The present value of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

B) The present value of scheduled interest payments on long-term debt during each of the next five years.

C) The amount of scheduled interest payments on long-term debt during each of the next five years.

D) The amount of future payments for sinking fund requirements and long-term debt maturities during each of the next five years.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

Edson Corp. signed a three-month, zero-interest-bearing note on November 1, 2008 for the purchase of $150,000 of inventory. The face value of the note was $152,205. Assuming Edson used a "Discount on Note Payable" account to initially record the note and that the discount will be amortized equally over the 3-month period, the adjusting entry made at December 31, 2008 will include a

A) debit to Discount on Note Payable for $735.

B) debit to Interest Expense for $1,470.

C) credit to Discount on Note Payable for $735.

D) credit to Interest Expense for $1,470.

A) debit to Discount on Note Payable for $735.

B) debit to Interest Expense for $1,470.

C) credit to Discount on Note Payable for $735.

D) credit to Interest Expense for $1,470.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

On January 1, 2008, Bleeker Co. issued eight-year bonds with a face value of $ 1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31. The bonds were sold to yield 8%. Table values are:

-The present value of the interest is

A) $344,820.

B) $349,560.

C) $372,600.

D) $376,830.

-The present value of the interest is

A) $344,820.

B) $349,560.

C) $372,600.

D) $376,830.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

On January 1, 2008, Bleeker Co. issued eight-year bonds with a face value of $ 1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31. The bonds were sold to yield 8%. Table values are:

-The issue price of the bonds is

A) $883,560.

B) $884,820.

C) $889,560.

D) $999,600.

-The issue price of the bonds is

A) $883,560.

B) $884,820.

C) $889,560.

D) $999,600.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

On October 1, 2008, Sinatra Corporation issued 5%, 10-year bonds with a par value of $300,000 at 104. Interest is paid on October 1 and April 1. The entry to record the issuance of the bonds would include a

A)credit of $7,500 to Accrued Interest Payable.

B)credit of $12,000 to Premium on Bonds Payable.

C)credit of $288,000 to Bonds Payable.

D)debit of $12,000 to Discount on Bonds Payable.

A)credit of $7,500 to Accrued Interest Payable.

B)credit of $12,000 to Premium on Bonds Payable.

C)credit of $288,000 to Bonds Payable.

D)debit of $12,000 to Discount on Bonds Payable.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

The December 31, 2008, balance sheet of Eddy Corporation includes the following items:

The bonds were issued on December 31, 2007, at 103, with interest payable on July 1 and December 31 of each year. On January 2, 2009, Eddy retired $1,400,000 of these bonds at 98. What should Eddy record as a gain on retirement of these bonds? Ignore taxes.

A) $28,000

B) $37,800

C) $65,800

D) $70,000

The bonds were issued on December 31, 2007, at 103, with interest payable on July 1 and December 31 of each year. On January 2, 2009, Eddy retired $1,400,000 of these bonds at 98. What should Eddy record as a gain on retirement of these bonds? Ignore taxes.A) $28,000

B) $37,800

C) $65,800

D) $70,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

On January 1, 2002, Gonzalez Corporation issued $4,500,000 of 10%, ten-year bonds at 103. The bonds are callable at the option of Gonzalez at 105. On December 31, 2008, when the fair market value of the bonds was 96, Gonzalez repurchased $1,000,000 of the bonds in the open market at 96. The unamortized total premium at the date of repurchase was $40,500. Gonzalez has recorded interest and amortization for 2008. Ignoring income taxes and assuming that the gain is material, Gonzalez should report this reacquisition as

A) a loss of $49,000.

B) a gain of $49,000.

C) a loss of $61,000.

D) a gain of $61,000.

A) a loss of $49,000.

B) a gain of $49,000.

C) a loss of $61,000.

D) a gain of $61,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

The 10% bonds payable of Klein Company had a net carrying amount of $570,000 on December 31, 2007. The bonds, which had a face value of $600,000, were issued at a discount to yield 12%. Interest was paid on January 1 and July 1 of each year. On July 2, 2008, several years before their maturity, Klein retired the bonds at 102. The interest payment on July 1, 2008 was made as scheduled and $4,200 of the discount was amortized. What is the loss that Klein should record on the early retirement of the bonds on July 2, 2008? Ignore taxes.

A) $12,000

B) $37,800

C) $33,600

D) $42,000

A) $12,000

B) $37,800

C) $33,600

D) $42,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

A corporation called an outstanding bond obligation four years before maturity. At that time there was an unamortized discount of $300,000. To extinguish this debt, the company had to pay a call premium of $100,000. Ignoring income tax considerations, how should these amounts be treated for accounting purposes?

A) Amortize $400,000 over four years.

B) Charge $400,000 to a loss in the year of extinguishment.

C) Charge $100,000 to a loss in the year of extinguishment and amortize $300,000 over four years.

D) Either amortize $400,000 over four years or charge $400,000 to a loss immediately, whichever management selects.

A) Amortize $400,000 over four years.

B) Charge $400,000 to a loss in the year of extinguishment.

C) Charge $100,000 to a loss in the year of extinguishment and amortize $300,000 over four years.

D) Either amortize $400,000 over four years or charge $400,000 to a loss immediately, whichever management selects.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

A company offers a cash rebate of $1 on each $4 package of light bulbs sold during 2008. Historically, 10% of customers mail in the rebate form. During 2008, 4,000,000 packages of light bulbs are sold, and 140,000 $1 rebates are mailed to customers. What is the rebate expense and liability, respectively, shown on the 2008 financial statements dated December 31?

A) $400,000; $400,000

B) $400,000; $260,000

C) $260,000; $260,000

D) $140,000; $260,000

A) $400,000; $400,000

B) $400,000; $260,000

C) $260,000; $260,000

D) $140,000; $260,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

A company buys an oil rig for $1,000,000 on January 1, 2008. The life of the rig is 10 years and the expected cost to dismantle the rig at the end of 10 years is $200,000 (present value at 10% is $77,110). 10% is an appropriate interest rate for this company. What expense should be recorded for 2008 as a result of these events?

A) Depreciation expense of $120,000

B) Depreciation expense of $100,000 and interest expense of $7,711

C) Depreciation expense of $100,000 and interest expense of $20,000

D) Depreciation expense of $107,710 and interest expense of $7,711

A) Depreciation expense of $120,000

B) Depreciation expense of $100,000 and interest expense of $7,711

C) Depreciation expense of $100,000 and interest expense of $20,000

D) Depreciation expense of $107,710 and interest expense of $7,711

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

Wellman Company self insures its property for fire and storm damage. If the company were to obtain insurance on the property, it would cost them $1,000,000 per year. The company estimates that on average it will incur losses of $800,000 per year. During 2008, $350,000 worth of losses were sustained. How much total expense and/or loss should be recognized by Wellman Company for 2008?

A) $350,000 in losses and no insurance expense

B) $350,000 in losses and $450,000 in insurance expense

C) $0 in losses and $800,000 in insurance expense

D) $0 in losses and $1,000,000 in insurance expense

A) $350,000 in losses and no insurance expense

B) $350,000 in losses and $450,000 in insurance expense

C) $0 in losses and $800,000 in insurance expense

D) $0 in losses and $1,000,000 in insurance expense

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

During 2007, Younger Co. introduced a new line of machines that carry a three-year warranty against manufacturer's defects. Based on industry experience, warranty costs are estimated at 2% of sales in the year of sale, 4% in the year after sale, and 6% in the second year after sale. Sales and actual warranty expenditures for the first three-year period were as follows:

What amount should Younger report as a liability at December 31, 2009?

A) $0

B) $15,000

C) $204,000

D) $315,000

What amount should Younger report as a liability at December 31, 2009?A) $0

B) $15,000

C) $204,000

D) $315,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

Milner Frosted Flakes Company offers its customers a pottery cereal bowl if they send in 3 box tops from Milner Frosted Flakes boxes and $1.00. The company estimates that 60% of the box tops will be redeemed. In 2008, the company sold 675,000 boxes of Frosted Flakes and customers redeemed 330,000 box tops receiving 110,000 bowls. If the bowls cost Milner Company $2.50 each, how much liability for outstanding premiums should be recorded at the end of 2008?

A) $25,000

B) $37,500

C) $62,500

D) $87,500

A) $25,000

B) $37,500

C) $62,500

D) $87,500

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

Kent Co. includes one coupon in each bag of dog food it sells. In return for eight coupons, customers receive a leash. The leashes cost Kent $2.00 each. Kent estimates that 40 percent of the coupons will be redeemed. Data for 2008 and 2009 are as follows:

-The premium expense for 2008 is

A) $25,000.

B) $30,000.

C) $35,000.

D) $50,000.

-The premium expense for 2008 is

A) $25,000.

B) $30,000.

C) $35,000.

D) $50,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

Kent Co. includes one coupon in each bag of dog food it sells. In return for eight coupons, customers receive a leash. The leashes cost Kent $2.00 each. Kent estimates that 40 percent of the coupons will be redeemed. Data for 2008 and 2009 are as follows:

-The estimated liability for premiums at December 31, 2008 is

A) $7,500.

B) $10,000.

C) $17,500.

D) $20,000.

-The estimated liability for premiums at December 31, 2008 is

A) $7,500.

B) $10,000.

C) $17,500.

D) $20,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

Vernon Co. is being sued for illness caused to local residents as a result of negligence on the company's part in permitting the local residents to be exposed to highly toxic chemicals from its plant. Vernon's lawyer states that it is probable that Vernon will lose the suit and be found liable for a judgment costing Vernon anywhere from $1,200,000 to $6,000,000. However, the lawyer states that the most probable cost is $3,600,000. As a result of the above facts, Vernon should accrue

A) a loss contingency of $1,200,000 and disclose an additional contingency of up to $4,800,000.

B) a loss contingency of $3,600,000 and disclose an additional contingency of up to $2,400,000.

C) a loss contingency of $3,600,000 but not disclose any additional contingency.

D) no loss contingency but disclose a contingency of $1,200,000 to $6,000,000.

A) a loss contingency of $1,200,000 and disclose an additional contingency of up to $4,800,000.

B) a loss contingency of $3,600,000 and disclose an additional contingency of up to $2,400,000.

C) a loss contingency of $3,600,000 but not disclose any additional contingency.

D) no loss contingency but disclose a contingency of $1,200,000 to $6,000,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

On January 3, 2008, Alton Corp. owned a machine that had cost $200,000. The accumulated depreciation was $120,000, estimated salvage value was $12,000, and fair market value was $320,000. On January 4, 2008, this machine was irreparably damaged by Reed Corp. and became worthless. In October 2008, a court awarded damages of $320,000 against Reed in favor of Alton. At December 31, 2008, the final outcome of this case was awaiting appeal and was, therefore, uncertain. However, in the opinion of Alton's attorney, Reed's appeal will be denied. At December 31, 2008, what amount should Alton accrue for this gain contingency?

A) $320,000

B) $260,000

C) $200,000

D) $0

A) $320,000

B) $260,000

C) $200,000

D) $0

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

Presented below is information available for Norton Company.

Total current liabilities are $120,000. The acid-test ratio for Norton is

A) 2.33 to 1.

B) 2.08 to 1.

C) 1.17 to 1.

D) .54 to 1.

Total current liabilities are $120,000. The acid-test ratio for Norton isA) 2.33 to 1.

B) 2.08 to 1.

C) 1.17 to 1.

D) .54 to 1.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

On January 1, 2008, Didde Co. leased a building to Ellis Corp. for a ten-year term at an annual rental of $80,000. At inception of the lease, Didde received $320,000 covering the first two years' rent of $160,000 and a security deposit of $160,000. This deposit will not be returned to Ellis upon expiration of the lease but will be applied to payment of rent for the last two years of the lease. What portion of the $320,000 should be shown as a current and long-term liability, respectively, in Didde's December 31, 2008 balance sheet?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

On its December 31, 2007 balance sheet, Lane Corp. reported bonds payable of $6,000,000 and related unamortized bond issue costs of $320,000. The bonds had been issued at par. On January 2, 2008, Lane retired $3,000,000 of the outstanding bonds at par plus a call premium of $70,000. What amount should Lane report in its 2008 income statement as loss on extinguishment of debt (ignore taxes)?

A) $0

B) $70,000

C) $160,000

D) $230,000

A) $0

B) $70,000

C) $160,000

D) $230,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

On June 30, 2008, Rosen Co. had outstanding 8%, $3,000,000 face amount, 15-year bonds maturing on June 30, 2018. Interest is payable on June 30 and December 31. The unamortized balances in the bond discount and deferred bond issue costs accounts on June 30, 2008 were $105,000 and $30,000, respectively. On June 30, 2008, Rosen acquired all of these bonds at 94 and retired them. What net carrying amount should be used in computing gain or loss on this early extinguishment of debt?

A) $2,970,000

B) $2,895,000

C) $2,865,000

D) $2,820,000

A) $2,970,000

B) $2,895,000

C) $2,865,000

D) $2,820,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

Dexter Co. sells major household appliance service contracts for cash. The service contracts are for a one-year, two-year, or three-year period. Cash receipts from contracts are credited to unearned service contract revenues. This account had a balance of $480,000 at December 31, 2008 before year-end adjustment. Service contract costs are charged as incurred to the service contract expense account, which had a balance of $120,000 at December 31, 2008. Outstanding service contracts at December 31, 2008 expire as follows:

What amount should be reported as unearned service contract revenues in Dexter's December 31, 2008 balance sheet?

A) $360,000

B) $330,000

C) $240,000

D) $220,000

What amount should be reported as unearned service contract revenues in Dexter's December 31, 2008 balance sheet?A) $360,000

B) $330,000

C) $240,000

D) $220,000

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

During 2008, Blass Co. introduced a new product carrying a two-year warranty against defects. The estimated warranty costs related to dollar sales are 2% within 12 months following sale and 4% in the second 12 months following sale. Sales and actual warranty expenditures for the years ended December 31, 2008 and 2009 are as follows:

At December 31, 2009, Blass should report an estimated warranty liability of

A) $0.

B) $10,000.

C) $30,000.

D) $66,000.

At December 31, 2009, Blass should report an estimated warranty liability ofA) $0.

B) $10,000.

C) $30,000.

D) $66,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

In March 2008, an explosion occurred at Howe Co.'s plant, causing damage to area properties. By May 2008, no claims had yet been asserted against Howe. However, Howe's management and legal counsel concluded that it was reasonably possible that Howe would be held responsible for negligence, and that $4,000,000 would be a reasonable estimate of the damages. Howe's $5,000,000 comprehensive public liability policy contains a $400,000 deductible clause. In Howe's December 31, 2007 financial statements, for which the auditor's fieldwork was completed in April 2008, how should this casualty be reported?

A) As a note disclosing a possible liability of $4,000,000.

B) As an accrued liability of $400,000.

C) As a note disclosing a possible liability of $400,000.

D) No note disclosure of accrual is required for 2007 because the event occurred in 2008.

A) As a note disclosing a possible liability of $4,000,000.

B) As an accrued liability of $400,000.

C) As a note disclosing a possible liability of $400,000.

D) No note disclosure of accrual is required for 2007 because the event occurred in 2008.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

On January 1, 2008, Gomez Co. issued its 10% bonds in the face amount of $3,000,000, which mature on January 1, 2018. The bonds were issued for $3,405,000 to yield 8%, resulting in bond premium of $405,000. Gomez uses the effective-interest method of amortizing bond premium. Interest is payable annually on December 31. At December 31, 2008, Gomez's adjusted unamortized bond premium should be

A) $405,000.

B) $377,400.

C) $364,500.

D) $304,500.

A) $405,000.

B) $377,400.

C) $364,500.

D) $304,500.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

On July 1, 2006, Kitel, Inc. issued 9% bonds in the face amount of $5,000,000, which mature on July 1, 2016. The bonds were issued for $4,695,000 to yield 10%, resulting in a bond discount of $305,000. Kitel uses the effective-interest method of amortizing bond discount. Interest is payable annually on June 30. At June 30, 2008, Kitel's unamortized bond discount should be

A) $264,050.

B) $255,000.

C) $244,000.

D) $215,000.

A) $264,050.

B) $255,000.

C) $244,000.

D) $215,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.