Deck 5: Income Statement and Related Information

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Any gain or loss experienced by a concern, whether directly or indirectly related to operations, contributes to the long-run profitability and should be included in the computa-tion of net income. Those who favor such a philosophy adhere to the

Question

Question

To be classified on an income statement as an extraordinary item, the transaction or event must be material in nature and

Question

Question

Question

Question

Question

Question

Question

When a manufacturing company sells one of its plant assets at a price in excess of its book value, it should recognize

Question

Question

Question

Question

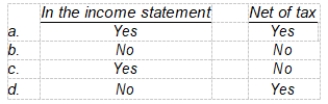

A correction of an error in prior periods' income will be reported

Question

Question

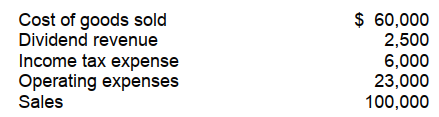

For Garret Wolfe Company, the following information is available:

-In Garret Wolfe's single-step income statement, gross profit

A) should not be reported.

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

-In Garret Wolfe's single-step income statement, gross profit

A) should not be reported.

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

Question

For Garret Wolfe Company, the following information is available:

-In Garret Wolfe's multiple-step income statement, gross profit

A) should not be reported

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

-In Garret Wolfe's multiple-step income statement, gross profit

A) should not be reported

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

Question

During the year 2008, Siska Corporation had the following information available related to its income statement:

Cost of goods sold for 2008 amounted to

Cost of goods sold for 2008 amounted to

A) $735,000.

B) $685,000.

C) $575,000.

D) $525,000.

Cost of goods sold for 2008 amounted toA) $735,000.

B) $685,000.

C) $575,000.

D) $525,000.

Question

Question

Question

Question

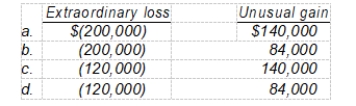

Carpino Corporation has an extraordinary loss of $200,000, an unusual gain of $140,000, and a tax rate of 40%. At what amount should Carpino report each item?

Question

Edmonds Corporation reports the following information:

Edmonds should report earnings per share of

A) $1.50.

B) $1.80.

C) $2.20.

D) $2.50.

Edmonds should report earnings per share of

A) $1.50.

B) $1.80.

C) $2.20.

D) $2.50.

Question

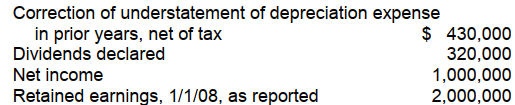

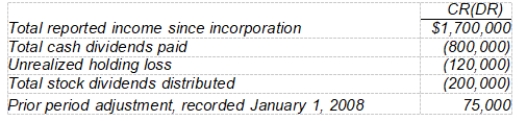

Simmons Corporation reports the following information:

Simmons should report retained earnings, 1/1/08, as adjusted at

Simmons should report retained earnings, 1/1/08, as adjusted at

A) $1,570,000.

B) $2,000,000.

C) $2,430,000.

D) $3,110,000.

Simmons should report retained earnings, 1/1/08, as adjusted atA) $1,570,000.

B) $2,000,000.

C) $2,430,000.

D) $3,110,000.

Question

Simmons Corporation reports the following information:

Simmons should report retained earnings, 12/31/08, as adjusted at

Simmons should report retained earnings, 12/31/08, as adjusted at

A) $1,570,000.

B) $2,250,000.

C) $2,680,000.

D) $3,110,000.

Simmons should report retained earnings, 12/31/08, as adjusted atA) $1,570,000.

B) $2,250,000.

C) $2,680,000.

D) $3,110,000.

Question

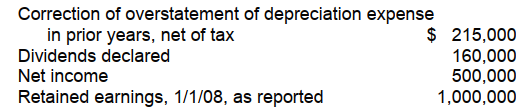

Joe Novak Corporation reports the following information:

oe Novak should report retained earnings, 12/31/08, at

oe Novak should report retained earnings, 12/31/08, at

A) $785,000.

B) $1,125,000.

C) $1,340,000.

D) $1,555,000.

oe Novak should report retained earnings, 12/31/08, atA) $785,000.

B) $1,125,000.

C) $1,340,000.

D) $1,555,000.

Question

The following information was extracted from the accounts of Boone Corporation at December 31, 2008:

What should be the balance of retained earnings at December 31, 2008?

A) $655,000

B) $700,000

C) $580,000

D) $775,000

What should be the balance of retained earnings at December 31, 2008?

A) $655,000

B) $700,000

C) $580,000

D) $775,000

Question

Silas Company reported the following information for 2008:

For 2008, Silas would report comprehensive income of

For 2008, Silas would report comprehensive income of

A) $117,000.

B) $115,000.

C) $97,000.

D) $20,000.

For 2008, Silas would report comprehensive income ofA) $117,000.

B) $115,000.

C) $97,000.

D) $20,000.

Question

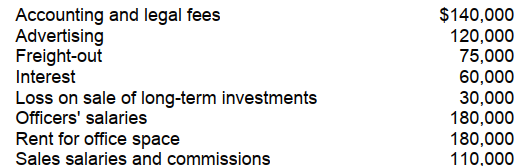

Meyer Corp. reports operating expenses in two categories: (1) selling and (2) general and administrative. The adjusted trial balance at December 31, 2008, included the following expense accounts:

One-half of the rented premises is occupied by the sales department

One-half of the rented premises is occupied by the sales department

-How much of the expenses listed above should be included in Meyer's selling expenses for 2008?

A) $230,000

B) $305,000

C) $320,000

D) $395,000

One-half of the rented premises is occupied by the sales department-How much of the expenses listed above should be included in Meyer's selling expenses for 2008?

A) $230,000

B) $305,000

C) $320,000

D) $395,000

Question

Meyer Corp. reports operating expenses in two categories: (1) selling and (2) general and administrative. The adjusted trial balance at December 31, 2008, included the following expense accounts:

One-half of the rented premises is occupied by the sales department

-How much of the expenses listed above should be included in Meyer's general and administrative expenses for 2008?

A) $410,000

B) $440,000

C) $470,000

D) $500,000

One-half of the rented premises is occupied by the sales department-How much of the expenses listed above should be included in Meyer's general and administrative expenses for 2008?

A) $410,000

B) $440,000

C) $470,000

D) $500,000

Question

The following items were among those that were reported on Nen Co.'s income statement for the year ended December 31, 2008:

The office space is used equally by Nen's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Nen's multiple-step income statement?

The office space is used equally by Nen's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Nen's multiple-step income statement?

A) $220,000

B) $255,000

C) $310,000

D) $430,000

The office space is used equally by Nen's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Nen's multiple-step income statement?A) $220,000

B) $255,000

C) $310,000

D) $430,000

Question

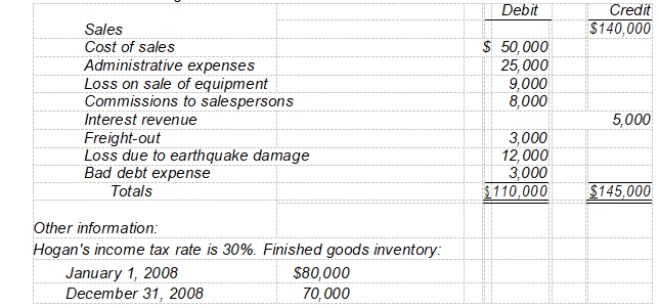

Hogan Corp.'s trial balance of income statement accounts for the year ended December 31, 2008 included the following:

On Hogan's multiple-step income statement for 2008,

On Hogan's multiple-step income statement for 2008,

-Inventory purchases are

A) $63,000.

B) $60,000.

C) $43,000.

D) $40,000.

On Hogan's multiple-step income statement for 2008,-Inventory purchases are

A) $63,000.

B) $60,000.

C) $43,000.

D) $40,000.

Question

Hogan Corp.'s trial balance of income statement accounts for the year ended December 31, 2008 included the following:

On Hogan's multiple-step income statement for 2008,

-Income before extraordinary item is

A) $64,000.

B) $47,000.

C) $32,900.

D) $24,500.

On Hogan's multiple-step income statement for 2008,-Income before extraordinary item is

A) $64,000.

B) $47,000.

C) $32,900.

D) $24,500.

Question

Hogan Corp.'s trial balance of income statement accounts for the year ended December 31, 2008 included the following:

On Hogan's multiple-step income statement for 2008,

-Extraordinary loss is

A) $8,400.

B) $12,000.

C) $14,700.

D) $21,000.

On Hogan's multiple-step income statement for 2008,-Extraordinary loss is

A) $8,400.

B) $12,000.

C) $14,700.

D) $21,000.

Question

Snead, Inc. incurred the following infrequent losses during 2008:

In its 2008 income statement, what amount should Snead report as total infrequent losses that are not considered extraordinary?

In its 2008 income statement, what amount should Snead report as total infrequent losses that are not considered extraordinary?

A) $170,000

B) $130,000

C) $110,000

D) $100,000

In its 2008 income statement, what amount should Snead report as total infrequent losses that are not considered extraordinary?A) $170,000

B) $130,000

C) $110,000

D) $100,000

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 5: Income Statement and Related Information

1

The multiple-step income statement recognizes a separation of operating transactions from nonoperating transactions and matches costs and expenses with related revenues.

True

2

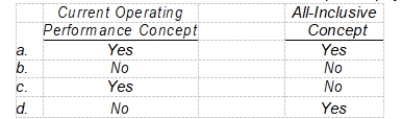

The advocates of the current operating performance approach include extraordinary items in the calculation of net income.

True

3

A manufacturer of computer hardware who sells all computer manufacturing facilities located in foreign countries can record the transaction as a disposal of a business component.

False

4

Phasing out of a product line or class of service is a disposal of assets that qualifies as a disposal of a component of a business.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

An example of an extraordinary loss is a large write-down of accounts receivable caused by the unexpected bankruptcy of a major customer.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

The FASB has specifically prohibited a net-of-tax treatment for gains and losses that are either unusual or nonrecurring but not both.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

Adjustments that grow out of the use of estimates in accounting are not classified as prior period adjustments.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

A change in accounting principle is considered appropriate only when it is demonstrated that the newly adopted principle is preferable to the old one.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Intraperiod tax allocation causes a reduction in total income tax expense for the period in which it is used.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

A prior period adjustment results from the correction of an error in the financial statements of a prior period discovered subsequent to their issuance.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

According to the FASB, displaying comprehensive income as a part of the statement of stockholders' equity is one of the acceptable ways of presenting comprehensive income items.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

The primary reason the income statement is so important to investors and creditors relates to its ability to provide information helpful in

A) determining the honesty of those involved in managing the enterprise.

B) assessing the financial position of the entity at a point in time.

C) predicting the amount, timing, and uncertainty of future cash flows.

D) determining the amount of future income the entity may generate from current operations.

A) determining the honesty of those involved in managing the enterprise.

B) assessing the financial position of the entity at a point in time.

C) predicting the amount, timing, and uncertainty of future cash flows.

D) determining the amount of future income the entity may generate from current operations.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

The occurrence that most likely would have no effect on 2008 net income (assuming that all amounts involved are material) is the

A) sale in 2008 of an office building contributed by a stockholder in 1983.

B) collection in 2008 of a receivable from a customer whose account was written off in 2007 by a charge to the allowance account.

C) settlement based on litigation in 2008 of previously unrecognized damages from a serious accident which occurred in 2006.

D) worthlessness determined in 2008 of stock purchased on a speculative basis in 2004.

A) sale in 2008 of an office building contributed by a stockholder in 1983.

B) collection in 2008 of a receivable from a customer whose account was written off in 2007 by a charge to the allowance account.

C) settlement based on litigation in 2008 of previously unrecognized damages from a serious accident which occurred in 2006.

D) worthlessness determined in 2008 of stock purchased on a speculative basis in 2004.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

The accountant for Orion Sales Company is preparing the income statement for 2008 and the balance sheet at December 31, 2008. The January 1, 2008 merchandise inventory balance will appear

A) only as an asset on the balance sheet.

B) only in the cost of goods sold section of the income statement.

C) as a deduction in the cost of goods sold section of the income statement and as a current asset on the balance sheet.

D) as an addition in the cost of goods sold section of the income statement and as a current asset on the balance sheet.

A) only as an asset on the balance sheet.

B) only in the cost of goods sold section of the income statement.

C) as a deduction in the cost of goods sold section of the income statement and as a current asset on the balance sheet.

D) as an addition in the cost of goods sold section of the income statement and as a current asset on the balance sheet.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

One of the primary benefits of the multiple-step income statement over the single-step income statement is that the multiple-step income statement

A) shows gross margin and recognizes different types of costs and expenses.

B) shows last year's figures in comparison with the current year.

C) discriminates between administrative and selling expenses.

D) recognizes no distinction in types of costs or expenses.

A) shows gross margin and recognizes different types of costs and expenses.

B) shows last year's figures in comparison with the current year.

C) discriminates between administrative and selling expenses.

D) recognizes no distinction in types of costs or expenses.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

Any gain or loss experienced by a concern, whether directly or indirectly related to operations, contributes to the long-run profitability and should be included in the computa-tion of net income. Those who favor such a philosophy adhere to the

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following asset disposals would qualify as a disposal of a component of a business?

A) Phasing out a product line or class of service

B) Changes occasioned by a technological improvement

C) Sale by an auto parts manufacturer of one of its five parts-manufacturing subsidiaries

D) Sale by a transportation company of its bus operations but not its airline operations

A) Phasing out a product line or class of service

B) Changes occasioned by a technological improvement

C) Sale by an auto parts manufacturer of one of its five parts-manufacturing subsidiaries

D) Sale by a transportation company of its bus operations but not its airline operations

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

To be classified on an income statement as an extraordinary item, the transaction or event must be material in nature and

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following should not be reported on the income statement as an extra-ordinary item?

A) The write-off of major assets as a result of new environmental laws prohibiting their use

B) The write-off of a large receivable resulting from a customer's bankruptcy proceedings

C) A large loss as a result of an earthquake

D) Expropriation of assets by a foreign government

A) The write-off of major assets as a result of new environmental laws prohibiting their use

B) The write-off of a large receivable resulting from a customer's bankruptcy proceedings

C) A large loss as a result of an earthquake

D) Expropriation of assets by a foreign government

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following should be reported on the income statement as an extraordinary item?

A) The gain on disposal of a component of a business

B) The write-down of receivables deemed uncollectible

C) The loss from volcanic activity

D) The gain from a sale of equipment

A) The gain on disposal of a component of a business

B) The write-down of receivables deemed uncollectible

C) The loss from volcanic activity

D) The gain from a sale of equipment

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

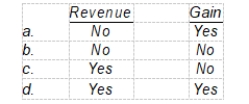

In general, the basic difference between the concepts of revenues and gains concerns

A) the materiality of the item being considered.

B) whether the event giving rise to the item relates to the typical activity of the enterprise.

C) whether the item is taxable in the current year.

D) the effect on total assets of the enterprise.

A) the materiality of the item being considered.

B) whether the event giving rise to the item relates to the typical activity of the enterprise.

C) whether the item is taxable in the current year.

D) the effect on total assets of the enterprise.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

When a company changes from one accounting principle to another, the income statement for the year of change

A) will normally not be affected, as this event is taken directly to Retained Earnings.

B) should include only footnote disclosure so readers will be aware of the change.

C) should include the cumulative effect, based on a retroactive computation, disclosed as a separate-line item.

D) should include the effect of the change related to the current year only and be disclosed as a separate line item.

A) will normally not be affected, as this event is taken directly to Retained Earnings.

B) should include only footnote disclosure so readers will be aware of the change.

C) should include the cumulative effect, based on a retroactive computation, disclosed as a separate-line item.

D) should include the effect of the change related to the current year only and be disclosed as a separate line item.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

Changing the basis of inventory pricing from FIFO to average cost is an example of a(n)

A) extraordinary item.

B) change in accounting principle.

C) change in estimate

D) discontinued operation.

A) extraordinary item.

B) change in accounting principle.

C) change in estimate

D) discontinued operation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

The concept that reports extraordinary items in the income statement is called the

A) phase-out period concept.

B) prior period adjustment concept.

C) current operating performance concept.

D) all-inclusive concept.

A) phase-out period concept.

B) prior period adjustment concept.

C) current operating performance concept.

D) all-inclusive concept.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

When a manufacturing company sells one of its plant assets at a price in excess of its book value, it should recognize

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

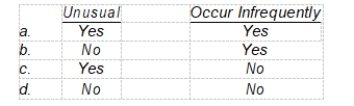

How should an unusual event not meeting the criteria for an extraordinary item be disclosed in the financial statements?

A) Shown as a separate item in operating revenues or expenses if material and supple-mented by a footnote if deemed appropriate.

B) Shown in operating revenues or expenses if material but not shown as a separate item.

C) Shown net of income tax after ordinary net earnings but before extraordinary items.

D) Shown net of income tax after extraordinary items but before net earnings.

A) Shown as a separate item in operating revenues or expenses if material and supple-mented by a footnote if deemed appropriate.

B) Shown in operating revenues or expenses if material but not shown as a separate item.

C) Shown net of income tax after ordinary net earnings but before extraordinary items.

D) Shown net of income tax after extraordinary items but before net earnings.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following is a required disclosure in the income statement when reporting the disposal of a component of the business?

A) The gain or loss on disposal should be reported as an extraordinary item.

B) Results of operations of a discontinued component should be disclosed immediately below extraordinary items.

C) Earnings per share from both continuing operations and net income should be disclosed on the face of the income statement.

D) The gain or loss on disposal should not be segregated, but should be reported together with the results of continuing operations.

A) The gain or loss on disposal should be reported as an extraordinary item.

B) Results of operations of a discontinued component should be disclosed immediately below extraordinary items.

C) Earnings per share from both continuing operations and net income should be disclosed on the face of the income statement.

D) The gain or loss on disposal should not be segregated, but should be reported together with the results of continuing operations.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following is true about intraperiod tax allocation?

A) It arises because certain revenue and expense items appear in the income statement either before or after they are included in the tax return.

B) It is required for extraordinary items and cumulative effect of accounting changes but not for prior period adjustments.

C) Its purpose is to allocate income tax expense evenly over a number of accounting periods.

D) Its purpose is to relate the income tax expense to the items which affect the amount of tax.

A) It arises because certain revenue and expense items appear in the income statement either before or after they are included in the tax return.

B) It is required for extraordinary items and cumulative effect of accounting changes but not for prior period adjustments.

C) Its purpose is to allocate income tax expense evenly over a number of accounting periods.

D) Its purpose is to relate the income tax expense to the items which affect the amount of tax.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

A correction of an error in prior periods' income will be reported

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

Shank Corporation made a very large arithmetical error in the preparation of its year-end financial statements by improper placement of a decimal point in the calculation of depreciation. The error caused the net income to be reported at almost double the proper amount. Correction of the error when discovered in the next year should be treated as

A) an increase in depreciation expense for the year in which the error is discovered.

B) a component of income for the year in which the error is discovered, but separately listed on the income statement and fully explained in a note to the financial statements.

C) an extraordinary item for the year in which the error was made.

D) a prior period adjustment.

A) an increase in depreciation expense for the year in which the error is discovered.

B) a component of income for the year in which the error is discovered, but separately listed on the income statement and fully explained in a note to the financial statements.

C) an extraordinary item for the year in which the error was made.

D) a prior period adjustment.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

For Garret Wolfe Company, the following information is available:

-In Garret Wolfe's single-step income statement, gross profit

A) should not be reported.

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

-In Garret Wolfe's single-step income statement, gross profit

A) should not be reported.

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

For Garret Wolfe Company, the following information is available:

-In Garret Wolfe's multiple-step income statement, gross profit

A) should not be reported

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

-In Garret Wolfe's multiple-step income statement, gross profit

A) should not be reported

B) should be reported at $13,500.

C) should be reported at $40,000.

D) should be reported at $42,500.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

During the year 2008, Siska Corporation had the following information available related to its income statement:

Cost of goods sold for 2008 amounted to

A) $735,000.

B) $685,000.

C) $575,000.

D) $525,000.

Cost of goods sold for 2008 amounted toA) $735,000.

B) $685,000.

C) $575,000.

D) $525,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

A review of the December 31, 2008, financial statements of Baden Corporation revealed that under the caption "extraordinary losses," Baden reported a total of $515,000. Further analysis revealed that the $515,000 in losses was comprised of the following items:

(1) Baden recorded a loss of $150,000 incurred in the abandonment of equipment formerly used in the business.

(2) In an unusual and infrequent occurrence, a loss of $250,000 was sustained as a result of hurricane damage to a warehouse.

(3) During 2008, several factories were shut down during a major strike by employees, resulting in a loss of $85,000.

(4) Uncollectible accounts receivable of $30,000 were written off as uncollectible.

Ignoring income taxes, what amount of loss should Baden report as extraordinary on its 2008 income statement?

A) $150,000

B) $250,000

C) $400,000

D) $515,000

(1) Baden recorded a loss of $150,000 incurred in the abandonment of equipment formerly used in the business.

(2) In an unusual and infrequent occurrence, a loss of $250,000 was sustained as a result of hurricane damage to a warehouse.

(3) During 2008, several factories were shut down during a major strike by employees, resulting in a loss of $85,000.

(4) Uncollectible accounts receivable of $30,000 were written off as uncollectible.

Ignoring income taxes, what amount of loss should Baden report as extraordinary on its 2008 income statement?

A) $150,000

B) $250,000

C) $400,000

D) $515,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

At Hall Company, events and transactions during 2008 included the following. The tax rate for all items is 30%.

(1) Depreciation for 2006 was found to be understated by $30,000.

(2) A strike by the employees of a supplier resulted in a loss of $25,000.

(3) The inventory at December 31, 2006 was overstated by $40,000.

(4) A flood destroyed a building that had a book value of $500,000. Floods are very uncommon in that area.

-The effect of these events and transactions on 2008 income from continuing operations net of tax would be

A) $17,500.

B) $38,500.

C) $66,500.

D) $416,500.

(1) Depreciation for 2006 was found to be understated by $30,000.

(2) A strike by the employees of a supplier resulted in a loss of $25,000.

(3) The inventory at December 31, 2006 was overstated by $40,000.

(4) A flood destroyed a building that had a book value of $500,000. Floods are very uncommon in that area.

-The effect of these events and transactions on 2008 income from continuing operations net of tax would be

A) $17,500.

B) $38,500.

C) $66,500.

D) $416,500.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

At Hall Company, events and transactions during 2008 included the following. The tax rate for all items is 30%.

(1) Depreciation for 2006 was found to be understated by $30,000.

(2) A strike by the employees of a supplier resulted in a loss of $25,000.

(3) The inventory at December 31, 2006 was overstated by $40,000.

(4) A flood destroyed a building that had a book value of $500,000. Floods are very uncommon in that area.

-The effect of these events and transactions on 2008 net income net of tax would be

A) $17,500.

B) $367,500.

C) $388,500.

D) $416,500.

(1) Depreciation for 2006 was found to be understated by $30,000.

(2) A strike by the employees of a supplier resulted in a loss of $25,000.

(3) The inventory at December 31, 2006 was overstated by $40,000.

(4) A flood destroyed a building that had a book value of $500,000. Floods are very uncommon in that area.

-The effect of these events and transactions on 2008 net income net of tax would be

A) $17,500.

B) $367,500.

C) $388,500.

D) $416,500.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

Carpino Corporation has an extraordinary loss of $200,000, an unusual gain of $140,000, and a tax rate of 40%. At what amount should Carpino report each item?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

Edmonds Corporation reports the following information:

Edmonds should report earnings per share of

A) $1.50.

B) $1.80.

C) $2.20.

D) $2.50.

Edmonds should report earnings per share of

A) $1.50.

B) $1.80.

C) $2.20.

D) $2.50.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

Simmons Corporation reports the following information:

Simmons should report retained earnings, 1/1/08, as adjusted at

A) $1,570,000.

B) $2,000,000.

C) $2,430,000.

D) $3,110,000.

Simmons should report retained earnings, 1/1/08, as adjusted atA) $1,570,000.

B) $2,000,000.

C) $2,430,000.

D) $3,110,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

Simmons Corporation reports the following information:

Simmons should report retained earnings, 12/31/08, as adjusted at

A) $1,570,000.

B) $2,250,000.

C) $2,680,000.

D) $3,110,000.

Simmons should report retained earnings, 12/31/08, as adjusted atA) $1,570,000.

B) $2,250,000.

C) $2,680,000.

D) $3,110,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

Joe Novak Corporation reports the following information:

oe Novak should report retained earnings, 12/31/08, at

A) $785,000.

B) $1,125,000.

C) $1,340,000.

D) $1,555,000.

oe Novak should report retained earnings, 12/31/08, atA) $785,000.

B) $1,125,000.

C) $1,340,000.

D) $1,555,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

The following information was extracted from the accounts of Boone Corporation at December 31, 2008:

What should be the balance of retained earnings at December 31, 2008?

A) $655,000

B) $700,000

C) $580,000

D) $775,000

What should be the balance of retained earnings at December 31, 2008?

A) $655,000

B) $700,000

C) $580,000

D) $775,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

Silas Company reported the following information for 2008:

For 2008, Silas would report comprehensive income of

A) $117,000.

B) $115,000.

C) $97,000.

D) $20,000.

For 2008, Silas would report comprehensive income ofA) $117,000.

B) $115,000.

C) $97,000.

D) $20,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

Meyer Corp. reports operating expenses in two categories: (1) selling and (2) general and administrative. The adjusted trial balance at December 31, 2008, included the following expense accounts:

One-half of the rented premises is occupied by the sales department

-How much of the expenses listed above should be included in Meyer's selling expenses for 2008?

A) $230,000

B) $305,000

C) $320,000

D) $395,000

One-half of the rented premises is occupied by the sales department-How much of the expenses listed above should be included in Meyer's selling expenses for 2008?

A) $230,000

B) $305,000

C) $320,000

D) $395,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

Meyer Corp. reports operating expenses in two categories: (1) selling and (2) general and administrative. The adjusted trial balance at December 31, 2008, included the following expense accounts:

One-half of the rented premises is occupied by the sales department

-How much of the expenses listed above should be included in Meyer's general and administrative expenses for 2008?

A) $410,000

B) $440,000

C) $470,000

D) $500,000

One-half of the rented premises is occupied by the sales department-How much of the expenses listed above should be included in Meyer's general and administrative expenses for 2008?

A) $410,000

B) $440,000

C) $470,000

D) $500,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

The following items were among those that were reported on Nen Co.'s income statement for the year ended December 31, 2008:

The office space is used equally by Nen's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Nen's multiple-step income statement?

A) $220,000

B) $255,000

C) $310,000

D) $430,000

The office space is used equally by Nen's sales and accounting departments. What amount of the above-listed items should be classified as general and administrative expenses in Nen's multiple-step income statement?A) $220,000

B) $255,000

C) $310,000

D) $430,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Hogan Corp.'s trial balance of income statement accounts for the year ended December 31, 2008 included the following:

On Hogan's multiple-step income statement for 2008,

-Inventory purchases are

A) $63,000.

B) $60,000.

C) $43,000.

D) $40,000.

On Hogan's multiple-step income statement for 2008,-Inventory purchases are

A) $63,000.

B) $60,000.

C) $43,000.

D) $40,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

Hogan Corp.'s trial balance of income statement accounts for the year ended December 31, 2008 included the following:

On Hogan's multiple-step income statement for 2008,

-Income before extraordinary item is

A) $64,000.

B) $47,000.

C) $32,900.

D) $24,500.

On Hogan's multiple-step income statement for 2008,-Income before extraordinary item is

A) $64,000.

B) $47,000.

C) $32,900.

D) $24,500.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

Hogan Corp.'s trial balance of income statement accounts for the year ended December 31, 2008 included the following:

On Hogan's multiple-step income statement for 2008,

-Extraordinary loss is

A) $8,400.

B) $12,000.

C) $14,700.

D) $21,000.

On Hogan's multiple-step income statement for 2008,-Extraordinary loss is

A) $8,400.

B) $12,000.

C) $14,700.

D) $21,000.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

Snead, Inc. incurred the following infrequent losses during 2008:

In its 2008 income statement, what amount should Snead report as total infrequent losses that are not considered extraordinary?

A) $170,000

B) $130,000

C) $110,000

D) $100,000

In its 2008 income statement, what amount should Snead report as total infrequent losses that are not considered extraordinary?A) $170,000

B) $130,000

C) $110,000

D) $100,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.