Deck 4: Balance Sheet

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

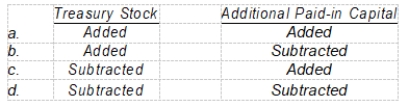

How are the following items handled in computing the total stockholders' equity section of the balance sheet?

Question

Question

Garret Company owns the following investments:

Garret will report investments in its current assets section of

Garret will report investments in its current assets section of

A) $0.

B) exactly $60,000.

C) $60,000 or an amount greater than $60,000, depending on the circumstances.

D) exactly $95,000.

Garret will report investments in its current assets section ofA) $0.

B) exactly $60,000.

C) $60,000 or an amount greater than $60,000, depending on the circumstances.

D) exactly $95,000.

Question

For Nicholson Company, the following information is available:

In Nicholson's balance sheet, intangible assets should be reported at

In Nicholson's balance sheet, intangible assets should be reported at

A) $65,000.

B) $75,000.

C) $265,000.

D) $275,000.

In Nicholson's balance sheet, intangible assets should be reported atA) $65,000.

B) $75,000.

C) $265,000.

D) $275,000.

Question

Horton Company owns the following investments:

Horton will report securities in its long-term investments section of

Horton will report securities in its long-term investments section of

A) exactly $95,000.

B) exactly $107,000.

C) exactly $142,000.

D) $82,000 or an amount less than $82,000, depending on the circumstances.

Horton will report securities in its long-term investments section ofA) exactly $95,000.

B) exactly $107,000.

C) exactly $142,000.

D) $82,000 or an amount less than $82,000, depending on the circumstances.

Question

For Mitchell Company, the following information is available:

In Mitchell's balance sheet, intangible assets should be reported at

In Mitchell's balance sheet, intangible assets should be reported at

A) $90,000.

B) $105,000.

C) $370,000.

D) $385,000.

In Mitchell's balance sheet, intangible assets should be reported atA) $90,000.

B) $105,000.

C) $370,000.

D) $385,000.

Question

Reese Corp.'s trial balance reflected the following account balances at December 31, 2008:

In Reese's December 31, 2008 balance sheet, the current assets total is

In Reese's December 31, 2008 balance sheet, the current assets total is

A) $90,000.

B) $82,000.

C) $77,000.

D) $73,000.

In Reese's December 31, 2008 balance sheet, the current assets total isA) $90,000.

B) $82,000.

C) $77,000.

D) $73,000.

Question

The following trial balance of Scott Corp. at December 31, 2008 has been properly adjusted except for the income tax expense adjustment.

Other financial data for the year ended December 31, 2008:

Other financial data for the year ended December 31, 2008:

• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current assets total is

A) $6,080,000.

B) $5,555,000.

C) $5,405,000.

D) $4,955,000.

Other financial data for the year ended December 31, 2008:• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current assets total is

A) $6,080,000.

B) $5,555,000.

C) $5,405,000.

D) $4,955,000.

Question

The following trial balance of Scott Corp. at December 31, 2008 has been properly adjusted except for the income tax expense adjustment.

Other financial data for the year ended December 31, 2008:

• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current liabilities total is

A) $1,850,000.

B) $1,915,000.

C) $2,375,000.

D) $2,440,000.

Other financial data for the year ended December 31, 2008:• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current liabilities total is

A) $1,850,000.

B) $1,915,000.

C) $2,375,000.

D) $2,440,000.

Question

The following trial balance of Scott Corp. at December 31, 2008 has been properly adjusted except for the income tax expense adjustment.

Other financial data for the year ended December 31, 2008:

• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The final retained earnings balance is

A) $4,451,000.

B) $4,536,000.

C) $4,976,000.

D) $4,905,000.

Other financial data for the year ended December 31, 2008:• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The final retained earnings balance is

A) $4,451,000.

B) $4,536,000.

C) $4,976,000.

D) $4,905,000.

Question

On January 4, 2008, Gregg Co. leased a building to Cole Corp. for a ten-year term at an annual rental of $75,000. At inception of the lease, Gregg received $300,000 covering the first two years' rent of $150,000 and a security deposit of $150,000. This deposit will not be returned to Cole upon expiration of the lease but will be applied to payment of rent for the last two years of the lease. What portion of the $300,000 should be shown as a current and long-term liability in Gregg's December 31, 2008 balance sheet?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/32

Play

Full screen (f)

Deck 4: Balance Sheet

1

The three general classes of items included in the balance sheet are assets, liabilities, and equity.

True

2

If cash is restricted for purposes other than the liquidation of current obligations, it should not be classified as a current asset.

True

3

Securities classified as available-for-sale should be reported at cost.

False

4

Current liabilities are the obligations that are reasonably expected to be liquidated either by creation of other current liabilities or through the use of current assets.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

5

The stockholders' equity accounts used by a corporation are the same as those used in accounting for a partnership or proprietorship.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

6

A contingent liability and an estimated liability are treated in the same manner for financial statement reporting purposes.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

7

Contracts and negotiations of significance, in addition to contingencies, are disclosed in footnotes to the financial statements.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

8

Notes are commonly used to disclose the existence and amount of any preferred stock dividends in arrears.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

9

The AICPA has recommended that the word "reserve" be used only to describe an appropriation of retained earnings.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

10

Solvency refers to the

A) ability of an enterprise to pay its debts as they mature.

B) amount of time that is expected to elapse until an asset is realized.

C) amount of time that is expected to elapse until a liability has to be paid.

D) amount of time that is expected to elapse until an asset is converted into cash.

A) ability of an enterprise to pay its debts as they mature.

B) amount of time that is expected to elapse until an asset is realized.

C) amount of time that is expected to elapse until a liability has to be paid.

D) amount of time that is expected to elapse until an asset is converted into cash.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

11

The primary purpose of the balance sheet is to reflect

A) the firm's potential for growth in stock values in the stock market.

B) items of value, debts, and net worth.

C) the value of items owned by the firm.

D) the status of the firm's assets in case of forced liquidation of the firm.

A) the firm's potential for growth in stock values in the stock market.

B) items of value, debts, and net worth.

C) the value of items owned by the firm.

D) the status of the firm's assets in case of forced liquidation of the firm.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

12

For accounting purposes, the operating cycle concept

A) has become obsolete.

B) affects the income statement but not the balance sheet.

C) permits some assets to be classified as current even though they are more than one year removed from becoming cash.

D) causes the distinction between current and noncurrent items to depend on whether they will affect cash within one year.

A) has become obsolete.

B) affects the income statement but not the balance sheet.

C) permits some assets to be classified as current even though they are more than one year removed from becoming cash.

D) causes the distinction between current and noncurrent items to depend on whether they will affect cash within one year.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

13

If $1,240 cash and a $4,760 note are given in exchange for a delivery truck to be used in a business,

A) assets and liabilities will change by the same amount.

B) owners' equity will be increased.

C) assets will increase and liabilities decrease.

D) assets and liabilities will increase but by different amounts.

A) assets and liabilities will change by the same amount.

B) owners' equity will be increased.

C) assets will increase and liabilities decrease.

D) assets and liabilities will increase but by different amounts.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is not a current asset?

A) Prepaid property taxes that relate to the next operating period

B) The cash surrender value of a life insurance policy carried by a corporation on its president

C) Marketable securities purchased as a temporary investment of cash

D) Installment notes receivable due over 15 months in accordance with normal trade practices

A) Prepaid property taxes that relate to the next operating period

B) The cash surrender value of a life insurance policy carried by a corporation on its president

C) Marketable securities purchased as a temporary investment of cash

D) Installment notes receivable due over 15 months in accordance with normal trade practices

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

15

Of the following statements, which best illustrates the fact that the formal distinction made between current and noncurrent assets is somewhat arbitrary?

A) Cash in a checking account is a current asset, while cash in a savings account is more permanent and is normally classified as noncurrent.

B) Inventory that may be sold next year, or in the subsequent year as demand dictates may be classified as current or noncurrent.

C) Accounts receivable due in less than one year or the operating cycle are classified as current assets, while accounts receivable due in longer than one year or the operating cycle are classified as noncurrent.

D) An amount equal to the current depreciation charge on buildings should be placed in the current assets section at the beginning of the year, because it will be consumed in the next operating cycle.

A) Cash in a checking account is a current asset, while cash in a savings account is more permanent and is normally classified as noncurrent.

B) Inventory that may be sold next year, or in the subsequent year as demand dictates may be classified as current or noncurrent.

C) Accounts receivable due in less than one year or the operating cycle are classified as current assets, while accounts receivable due in longer than one year or the operating cycle are classified as noncurrent.

D) An amount equal to the current depreciation charge on buildings should be placed in the current assets section at the beginning of the year, because it will be consumed in the next operating cycle.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following items should never be included in the current assets section of the balance sheet?

A) Receivable from a customer outstanding for more than a year

B) Deferred income taxes resulting from interperiod tax allocation

C) Three-year premium for fire insurance on plant and equipment

D) A pension fund

A) Receivable from a customer outstanding for more than a year

B) Deferred income taxes resulting from interperiod tax allocation

C) Three-year premium for fire insurance on plant and equipment

D) A pension fund

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

17

Of the following items, the one which should be classified as a current asset is

A) trade installment receivables normally collectible in 20 months.

B) a deposit on equipment ordered, delivery of which will be made within 7 months.

C) cash designated for the redemption of callable bonds.

D) cash surrender value of a life insurance policy of which the company is a beneficiary.

A) trade installment receivables normally collectible in 20 months.

B) a deposit on equipment ordered, delivery of which will be made within 7 months.

C) cash designated for the redemption of callable bonds.

D) cash surrender value of a life insurance policy of which the company is a beneficiary.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

18

Prepaid expenses are included in the current assets section of the balance sheet because

A) they will be converted into cash within one year or the operating cycle, whichever is longer.

B) if they had not been already paid they would require the use of cash during the next year or operating cycle.

C) they were already included in operating expenses on the income statement in the year cash was expended.

D) they reflect payments that were made in a prior period that will not be charged to expense in the current period.

A) they will be converted into cash within one year or the operating cycle, whichever is longer.

B) if they had not been already paid they would require the use of cash during the next year or operating cycle.

C) they were already included in operating expenses on the income statement in the year cash was expended.

D) they reflect payments that were made in a prior period that will not be charged to expense in the current period.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

19

One of the main reasons for separating liabilities into current and long-term is to

A) provide decision makers with information regarding currently maturing debts.

B) separate large and small debts.

C) separate capital into its component parts.

D) separate total equity into its two basic parts.

A) provide decision makers with information regarding currently maturing debts.

B) separate large and small debts.

C) separate capital into its component parts.

D) separate total equity into its two basic parts.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

20

A liability to be paid next year would not be included in the current liability section of the balance sheet if the debt is expected to be refinanced through another long-term issue, or

A) the operating cycle is less than one year.

B) the liability is to be paid with cash that the company expects to earn during the next year.

C) if the debt is to be retired out of noncurrent assets.

D) the liability is the result of a nonoperating debt instrument due within the next year.

A) the operating cycle is less than one year.

B) the liability is to be paid with cash that the company expects to earn during the next year.

C) if the debt is to be retired out of noncurrent assets.

D) the liability is the result of a nonoperating debt instrument due within the next year.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

21

A characteristic of all assets and liabilities comprising working capital is that they are

A) monetary.

B) marketable.

C) current.

D) cash equivalents.

A) monetary.

B) marketable.

C) current.

D) cash equivalents.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

22

How are the following items handled in computing the total stockholders' equity section of the balance sheet?

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following reflects proper use of the term "reserve" in the preparation of financial statements?

A) The term used to describe amounts deducted from assets, such as "reserve for depreciation."

B) The initial term used in connection with an estimated liability, such as "estimated reserve for product warranty."

C) The term used to describe the setting aside of funds for the subsequent payment of an existing liability, such as "reserve for bonds payable."

D) The term used to describe an appropriation of retained earnings in the stockholders' equity section of the balance sheet.

A) The term used to describe amounts deducted from assets, such as "reserve for depreciation."

B) The initial term used in connection with an estimated liability, such as "estimated reserve for product warranty."

C) The term used to describe the setting aside of funds for the subsequent payment of an existing liability, such as "reserve for bonds payable."

D) The term used to describe an appropriation of retained earnings in the stockholders' equity section of the balance sheet.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

24

Garret Company owns the following investments:

Garret will report investments in its current assets section of

A) $0.

B) exactly $60,000.

C) $60,000 or an amount greater than $60,000, depending on the circumstances.

D) exactly $95,000.

Garret will report investments in its current assets section ofA) $0.

B) exactly $60,000.

C) $60,000 or an amount greater than $60,000, depending on the circumstances.

D) exactly $95,000.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

25

For Nicholson Company, the following information is available:

In Nicholson's balance sheet, intangible assets should be reported at

A) $65,000.

B) $75,000.

C) $265,000.

D) $275,000.

In Nicholson's balance sheet, intangible assets should be reported atA) $65,000.

B) $75,000.

C) $265,000.

D) $275,000.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

26

Horton Company owns the following investments:

Horton will report securities in its long-term investments section of

A) exactly $95,000.

B) exactly $107,000.

C) exactly $142,000.

D) $82,000 or an amount less than $82,000, depending on the circumstances.

Horton will report securities in its long-term investments section ofA) exactly $95,000.

B) exactly $107,000.

C) exactly $142,000.

D) $82,000 or an amount less than $82,000, depending on the circumstances.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

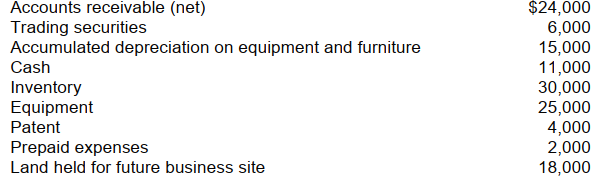

27

For Mitchell Company, the following information is available:

In Mitchell's balance sheet, intangible assets should be reported at

A) $90,000.

B) $105,000.

C) $370,000.

D) $385,000.

In Mitchell's balance sheet, intangible assets should be reported atA) $90,000.

B) $105,000.

C) $370,000.

D) $385,000.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

28

Reese Corp.'s trial balance reflected the following account balances at December 31, 2008:

In Reese's December 31, 2008 balance sheet, the current assets total is

A) $90,000.

B) $82,000.

C) $77,000.

D) $73,000.

In Reese's December 31, 2008 balance sheet, the current assets total isA) $90,000.

B) $82,000.

C) $77,000.

D) $73,000.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

29

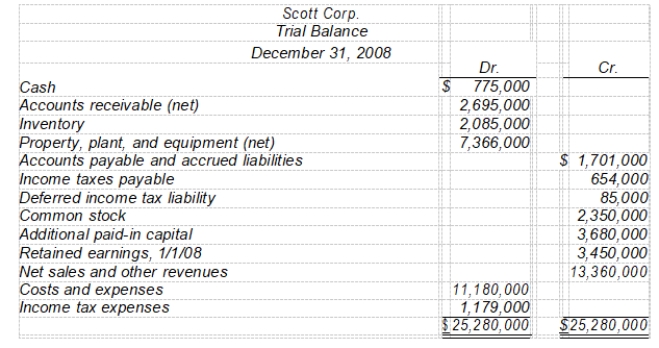

The following trial balance of Scott Corp. at December 31, 2008 has been properly adjusted except for the income tax expense adjustment.

Other financial data for the year ended December 31, 2008:

• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current assets total is

A) $6,080,000.

B) $5,555,000.

C) $5,405,000.

D) $4,955,000.

Other financial data for the year ended December 31, 2008:• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current assets total is

A) $6,080,000.

B) $5,555,000.

C) $5,405,000.

D) $4,955,000.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

30

The following trial balance of Scott Corp. at December 31, 2008 has been properly adjusted except for the income tax expense adjustment.

Other financial data for the year ended December 31, 2008:

• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current liabilities total is

A) $1,850,000.

B) $1,915,000.

C) $2,375,000.

D) $2,440,000.

Other financial data for the year ended December 31, 2008:• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The current liabilities total is

A) $1,850,000.

B) $1,915,000.

C) $2,375,000.

D) $2,440,000.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

31

The following trial balance of Scott Corp. at December 31, 2008 has been properly adjusted except for the income tax expense adjustment.

Other financial data for the year ended December 31, 2008:

• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The final retained earnings balance is

A) $4,451,000.

B) $4,536,000.

C) $4,976,000.

D) $4,905,000.

Other financial data for the year ended December 31, 2008:• Included in accounts receivable is $1,200,000 due from a customer and payable in quarterly installments of $150,000. The last payment is due December 29, 2010.

• The balance in the Deferred Income Tax Liability account pertains to a temporary difference that arose in a prior year, of which $20,000 is classified as a current liability.

• During the year, estimated tax payments of $525,000 were charged to income tax expense.

The current and future tax rate on all types of income is 30%.

-The final retained earnings balance is

A) $4,451,000.

B) $4,536,000.

C) $4,976,000.

D) $4,905,000.

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

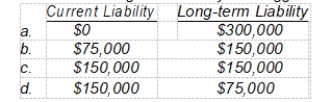

32

On January 4, 2008, Gregg Co. leased a building to Cole Corp. for a ten-year term at an annual rental of $75,000. At inception of the lease, Gregg received $300,000 covering the first two years' rent of $150,000 and a security deposit of $150,000. This deposit will not be returned to Cole upon expiration of the lease but will be applied to payment of rent for the last two years of the lease. What portion of the $300,000 should be shown as a current and long-term liability in Gregg's December 31, 2008 balance sheet?

Unlock Deck

Unlock for access to all 32 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 32 flashcards in this deck.