Deck 21: Transfer Pricing and Multinational Management Control Systems

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

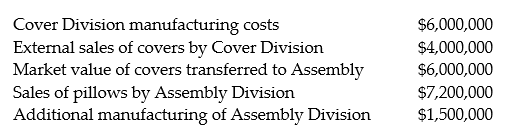

Bedtime Bedding Ltd. manufactures pillows. The Cover Division makes covers, and the Assembly Division makes the finished products. The covers can be sold separately for $5.00. The pillows sell for $6.00. The information related to manufacturing for the most recent year is as follows:

Required:

Compute the operating income for each division and the company as a whole. Use market value as the transfer price. Are all managers happy with this concept? Explain.

Required:

Compute the operating income for each division and the company as a whole. Use market value as the transfer price. Are all managers happy with this concept? Explain.

Question

Question

Question

Question

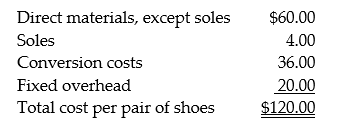

The Brownshoe Company has three specialized divisions. The Casual Shoe Division has asked the Sole Division to supply it with a large quantity of soles. The Sole Division is currently at capacity. The Sole Division sells soles outside for $5.00 each. The Casual Shoe Division, which is operating at 50 percent capacity, has offered to pay $4.00 per sole. The Sole Division has a variable cost of $3.60 per sole. The Casual Shoe Division has the following cost structure:

The manager of Casual Shoe believes that the $4 price from Sole is necessary if the division is to compete in the market for casual shoes.

Required:

a. As manager of Sole Division, would you recommend that your division supply the soles to Casual Shoe? Why?

b. Would it be desirable for the division to supply Casual Shoe with the soles for $4 assuming the Sole Division had excess capacity? Why?

c. What would be the corporate position assuming the Sole Division has excess capacity?

The manager of Casual Shoe believes that the $4 price from Sole is necessary if the division is to compete in the market for casual shoes.

Required:

a. As manager of Sole Division, would you recommend that your division supply the soles to Casual Shoe? Why?

b. Would it be desirable for the division to supply Casual Shoe with the soles for $4 assuming the Sole Division had excess capacity? Why?

c. What would be the corporate position assuming the Sole Division has excess capacity?

Question

Question

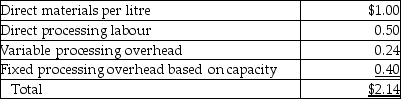

Better Food Company recently acquired an olive oil processing company that has an annual capacity of 2,000,000 litres and that processed and sold 1,400,000 litres last year at a market price of $4 per litre. The purpose of the acquisition was to furnish oil for the Cooking Division. The Cooking Division needs 800,000 litres of oil per year. It has been purchasing oil from suppliers at the market price. Production costs at capacity of the olive oil company, now a division, are as follows:

Management is trying to decide what transfer price to use for sales from the newly acquired company to the Cooking Division. The manager of the Olive Oil Division argues that $4, the market price, is appropriate. The manager of the Cooking Division argues that the cost of $2.14 should be used, or perhaps a lower price as fixed overhead cost should not be relevant. Any output of the Olive Oil Division not sold to the Cooking Division can be sold to outsiders for $4 per litre.

Management is trying to decide what transfer price to use for sales from the newly acquired company to the Cooking Division. The manager of the Olive Oil Division argues that $4, the market price, is appropriate. The manager of the Cooking Division argues that the cost of $2.14 should be used, or perhaps a lower price as fixed overhead cost should not be relevant. Any output of the Olive Oil Division not sold to the Cooking Division can be sold to outsiders for $4 per litre.

Required:

a. Compute the operating income for the Olive Oil Division using a transfer price of $4.

b. Compute the operating income for the Olive Oil Division using a transfer price of $2.14.

c. What transfer price(s) do you recommend? Justify your answer.

Management is trying to decide what transfer price to use for sales from the newly acquired company to the Cooking Division. The manager of the Olive Oil Division argues that $4, the market price, is appropriate. The manager of the Cooking Division argues that the cost of $2.14 should be used, or perhaps a lower price as fixed overhead cost should not be relevant. Any output of the Olive Oil Division not sold to the Cooking Division can be sold to outsiders for $4 per litre.Required:

a. Compute the operating income for the Olive Oil Division using a transfer price of $4.

b. Compute the operating income for the Olive Oil Division using a transfer price of $2.14.

c. What transfer price(s) do you recommend? Justify your answer.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

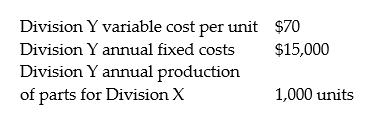

Mar Company has two decentralized divisions, X and Y. Division X has been purchasing certain component parts from Division Y at $75 per unit. Because Division Y plans to raise the price to $100 per unit, Division X desires to purchase these parts from external suppliers for $75 per unit. The following information is available:

If Division X buys from an external supplier, the facilities Division Y uses to manufacture these parts will be idle. Assuming Division Y's fixed costs cannot be avoided, what is the result if Mar requires Division X to buy from Division Y at a transfer price of $100 per unit?

If Division X buys from an external supplier, the facilities Division Y uses to manufacture these parts will be idle. Assuming Division Y's fixed costs cannot be avoided, what is the result if Mar requires Division X to buy from Division Y at a transfer price of $100 per unit?

Question

Question

Question

Question

Question

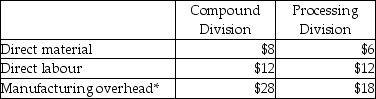

Payne Ltd. has two divisions. The Compound Division makes QZ54, an industrial compound, which is then transferred to the Processing Division. The Processing Division further processes the QZ54 and sells the final product to customers at $87/kg. Capacity in the Compound Division is 800,000 kg. QZ54 can be obtained on the external market at $50/kg Data regarding the costs per kilogram in each division are presented below:

*In the Compound Division the variable overhead is 80% of the total, and in Processing variable overhead represents 65% of the total. Fixed overhead rates are based on capacity of 800,000 kg. in each division.

*In the Compound Division the variable overhead is 80% of the total, and in Processing variable overhead represents 65% of the total. Fixed overhead rates are based on capacity of 800,000 kg. in each division.

In addition to the manufacturing costs, the Compound Division would incur $2 per kilogram of selling costs which would be avoided on internal transfers. Similarly the Processing Division would avoid $3/kg. of ordering costs on internal purchases.

Required:

a. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a market transfer price.

b. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a transfer pricing policy based on 125% of absorption manufacturing cost.

c. Comment on your calculations in a and b in terms of the respective division managers preferences.

d. Should the company transfer its 800,000 kg. assuming the Compound Division can sell all of its output on the external market?

*In the Compound Division the variable overhead is 80% of the total, and in Processing variable overhead represents 65% of the total. Fixed overhead rates are based on capacity of 800,000 kg. in each division.In addition to the manufacturing costs, the Compound Division would incur $2 per kilogram of selling costs which would be avoided on internal transfers. Similarly the Processing Division would avoid $3/kg. of ordering costs on internal purchases.

Required:

a. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a market transfer price.

b. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a transfer pricing policy based on 125% of absorption manufacturing cost.

c. Comment on your calculations in a and b in terms of the respective division managers preferences.

d. Should the company transfer its 800,000 kg. assuming the Compound Division can sell all of its output on the external market?

Question

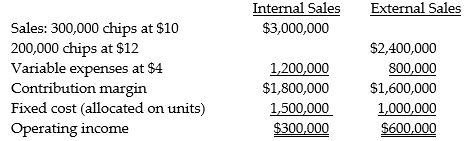

The Micro Division of Silicon Computers produces computer chips that are sold to the Personal Computer Division and to outsiders. Operating data for the Micro Division are as follows:

?

The Personal Computer Division has just received an offer from an outside supplier to furnish chips at $8.60 each. The manager of Micro Division is not willing to meet the $8.60 price. She argues that it costs her $9.00 to produce and sell each chip. Sales to outside customers are at a maximum of 200,000 chips.

Required:

a. Verify the Micro Division's $9.00 unit cost figure.

b. Should the Micro Division meet the outside price of $8.60? Explain on a per unit basis.

c. Prepare a Micro Division income statement for the sale to the Personal Computer Division assuming that the unit selling price of $8.60 is agreed. Comment on the allocation of fixed costs.

?

The Personal Computer Division has just received an offer from an outside supplier to furnish chips at $8.60 each. The manager of Micro Division is not willing to meet the $8.60 price. She argues that it costs her $9.00 to produce and sell each chip. Sales to outside customers are at a maximum of 200,000 chips.

Required:

a. Verify the Micro Division's $9.00 unit cost figure.

b. Should the Micro Division meet the outside price of $8.60? Explain on a per unit basis.

c. Prepare a Micro Division income statement for the sale to the Personal Computer Division assuming that the unit selling price of $8.60 is agreed. Comment on the allocation of fixed costs.

Question

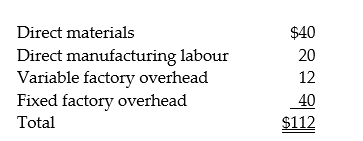

The Assembly Division of Canadian Car Company has offered to purchase 90,000 batteries from the Electrical Division for $104 per unit. At a normal volume of 250,000 batteries per year, production costs per battery are as follows:

The Electrical Division has been selling 250,000 batteries per year to outside buyers at $136 each. Capacity is 350,000 batteries per year. The Assembly Division has been buying batteries from outside sources for $130 each.

Required:

a. Should the Electrical Division manager accept the offer as is, make a counter offer, or reject the offer? Explain.

b. From the company's perspective, will the internal sales be of any benefit? Explain

The Electrical Division has been selling 250,000 batteries per year to outside buyers at $136 each. Capacity is 350,000 batteries per year. The Assembly Division has been buying batteries from outside sources for $130 each.

Required:

a. Should the Electrical Division manager accept the offer as is, make a counter offer, or reject the offer? Explain.

b. From the company's perspective, will the internal sales be of any benefit? Explain

Question

Question

Question

Question

Question

Question

Hendricks Ltd. of Calgary manufactures and sells computers. The Manufacturing Division is located in China and transfers 75% of its output to the Assembly Division in the Philippines. The balance of the product is sold in the local market at 2,100 yuan/unit. The Philippines division sells 20% of its output in the local market at 31,500 pesos/unit, with the balance shipped to Calgary. The Calgary operation packages the units and sells the final product at $1,900 Canadian per unit.

The following budget data are available:

Exchange rates are: $1 Canadian = 7 yuan and $1 Canadian = 45 pesos

Tax rates are 45% in China, 20% in the Philippines and 40% in Canada. Income taxes are not included in the calculation of cost-based transfer prices. Assume that Hendricks does not pay Canadian tax on amounts already taxed in foreign jurisdictions. Take each calculation to 2 decimal places.

Required:

The company has determined that it may transfer units at 250% of variable cost or at market and comply with all existing tax legislation. Which transfer pricing method should the company pursue? Support your recommendation with appropriate calculations.

The following budget data are available:

Exchange rates are: $1 Canadian = 7 yuan and $1 Canadian = 45 pesos

Tax rates are 45% in China, 20% in the Philippines and 40% in Canada. Income taxes are not included in the calculation of cost-based transfer prices. Assume that Hendricks does not pay Canadian tax on amounts already taxed in foreign jurisdictions. Take each calculation to 2 decimal places.

Required:

The company has determined that it may transfer units at 250% of variable cost or at market and comply with all existing tax legislation. Which transfer pricing method should the company pursue? Support your recommendation with appropriate calculations.

Question

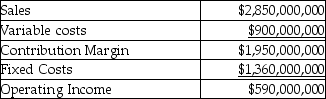

Clark Industries Ltd. manufactures monochromators that are used in a variety of applications. The Monochromator Division (M Division) sells its monochromators both internally and externally. It is operating at 80% of its 250,000 unit capacity and internal sales account for approximately 20% of its current sales volume. Internally the monochromators are transferred into the Aerospace Division (A Division) at a transfer price of $11,250 each. Variable production costs are the same for internal and external sales.

The income statement for the M Division is presented below:

The A Division uses one component in the production of its final product that sells for $75,000/unit. Other variable costs in the A Division are 40% of sales. and fixed costs per unit at its current capacity of 40,000 units are $17,250.

The A Division uses one component in the production of its final product that sells for $75,000/unit. Other variable costs in the A Division are 40% of sales. and fixed costs per unit at its current capacity of 40,000 units are $17,250.

The Aerospace Division is operating at its full capacity of 40,000 units and is evaluating whether it should invest to increase capacity. The investment would cost $900,000,000 and would have a useful life of 3 years. The equipment could be sold for $800,000 at the end of its useful life. For tax purposes it would be sold on January 1 of year 4. The machine would be used to manufacture a variation of its current product with the same transfer price. This new product would sell for $68,000 per unit. The variable cost ratio will be 45% of the selling price. The additional capacity of the new machine would be 14,000 units. It would qualify for a 30% CCA rate and the company would continue to have assets in the pool.

Required:

a. Evaluate the current transfer pricing policy from the standpoint of each division manager as well as the company as a whole.

b. Using net present value (NPV) analysis, would the A Division manager want to invest in the new equipment if the required rate of return is 12% and the tax rate is 25%?

c. If the investment is evaluated from a corporate perspective using NPV analysis and the 12% discount rate, does the decision change? Explain.

The income statement for the M Division is presented below:

The A Division uses one component in the production of its final product that sells for $75,000/unit. Other variable costs in the A Division are 40% of sales. and fixed costs per unit at its current capacity of 40,000 units are $17,250.The Aerospace Division is operating at its full capacity of 40,000 units and is evaluating whether it should invest to increase capacity. The investment would cost $900,000,000 and would have a useful life of 3 years. The equipment could be sold for $800,000 at the end of its useful life. For tax purposes it would be sold on January 1 of year 4. The machine would be used to manufacture a variation of its current product with the same transfer price. This new product would sell for $68,000 per unit. The variable cost ratio will be 45% of the selling price. The additional capacity of the new machine would be 14,000 units. It would qualify for a 30% CCA rate and the company would continue to have assets in the pool.

Required:

a. Evaluate the current transfer pricing policy from the standpoint of each division manager as well as the company as a whole.

b. Using net present value (NPV) analysis, would the A Division manager want to invest in the new equipment if the required rate of return is 12% and the tax rate is 25%?

c. If the investment is evaluated from a corporate perspective using NPV analysis and the 12% discount rate, does the decision change? Explain.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/45

Play

Full screen (f)

Deck 21: Transfer Pricing and Multinational Management Control Systems

1

The president of Silicon Company has just returned from a week of professional development courses and is very excited that she will not have to change the organization from a centralized structure to a decentralized structure just to have responsibility centres. However, she is somewhat confused about how responsibility centres relate to centralized organizations where a few managers have most of the authority.

Required: Explain how a centralized organization might allow for responsibility centres.

Required: Explain how a centralized organization might allow for responsibility centres.

It does not make any difference what type of organizational structure exists when it comes to defining responsibility centres. If a centralized organization desires to hold its managers responsible for their actions it can design a reporting system that assigns all costs and revenues to their controllable managers. It's just that in a centralized organization, each manager may have more items to control than are reasonably possible.

2

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Gathering information may be very expensive.

A) both

B) decentralization

C) centralization

-Gathering information may be very expensive.

A) both

B) decentralization

C) centralization

decentralization

3

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Greater responsiveness to user needs.

A) both

B) decentralization

C) centralization

-Greater responsiveness to user needs.

A) both

B) decentralization

C) centralization

decentralization

4

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Have few interdependencies among divisions.

A) both

B) decentralization

C) centralization

-Have few interdependencies among divisions.

A) both

B) decentralization

C) centralization

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

5

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Maximization of benefits over costs.

A) both

B) decentralization

C) centralization

-Maximization of benefits over costs.

A) both

B) decentralization

C) centralization

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

6

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Minimization of duplicate functions.

A) both

B) decentralization

C) centralization

-Minimization of duplicate functions.

A) both

B) decentralization

C) centralization

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

7

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Minimum of sub optimal decision making.

A) both

B) decentralization

C) centralization

-Minimum of sub optimal decision making.

A) both

B) decentralization

C) centralization

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

8

For each of the following activities, characteristics, and applications, tell whether they are primarily labelled as being found in a centralized organization, a decentralized organization, or both types of organizations

-Profit centres

A) both

B) decentralization

C) centralization

-Profit centres

A) both

B) decentralization

C) centralization

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

9

Use the information below to answer the following question(s).

Bon Accord uses two divisions in the production of soybean burgers. Division A sells soybean paste internally to Division B, which, in turn, produces soybean burgers that sell for $5 per kilogram. Division A incurs costs of $0.75 per kilogram, while Division B incurs additional costs of $2.50 per kilogram.

-What is Division A's operating income per kilogram assuming the transfer price of the soybean paste is set at $1.25 per kilogram?

A) $0.500

B) $0.875

C) $1.250

D) $1.625

E) $1.525

Bon Accord uses two divisions in the production of soybean burgers. Division A sells soybean paste internally to Division B, which, in turn, produces soybean burgers that sell for $5 per kilogram. Division A incurs costs of $0.75 per kilogram, while Division B incurs additional costs of $2.50 per kilogram.

-What is Division A's operating income per kilogram assuming the transfer price of the soybean paste is set at $1.25 per kilogram?

A) $0.500

B) $0.875

C) $1.250

D) $1.625

E) $1.525

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

10

Use the information below to answer the following question(s).

Bon Accord uses two divisions in the production of soybean burgers. Division A sells soybean paste internally to Division B, which, in turn, produces soybean burgers that sell for $5 per kilogram. Division A incurs costs of $0.75 per kilogram, while Division B incurs additional costs of $2.50 per kilogram.

-What is Division B's operating income per kilogram assuming the transfer price of the soybean paste is set at $1.25 per kilogram?

A) $0.500

B) $0.875

C) $1.250

D) $1.625

E) $1.525

Bon Accord uses two divisions in the production of soybean burgers. Division A sells soybean paste internally to Division B, which, in turn, produces soybean burgers that sell for $5 per kilogram. Division A incurs costs of $0.75 per kilogram, while Division B incurs additional costs of $2.50 per kilogram.

-What is Division B's operating income per kilogram assuming the transfer price of the soybean paste is set at $1.25 per kilogram?

A) $0.500

B) $0.875

C) $1.250

D) $1.625

E) $1.525

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

11

The Mill Flow Company has two divisions. The Cutting Division prepares timber at its sawmills. The Assembly Division prepares the cut lumber into finished wood for the furniture industry. No inventories exist in either division at the beginning of the year. During the year, the Cutting Division prepared 60,000 cords of wood at a cost of $660,000. All the lumber was transferred to the Assembly Division, where additional operating costs of $6 per cord were incurred. The 60,000 cords of finished wood were sold for $2,500,000.

Required:

a. Determine the operating income for each division if the transfer price from Cutting to Assembly is at cost.

b. Determine the operating income for each division if the transfer price is $9 per cord.

c. Since the Cutting Division sells all of its wood internally to the Assembly Division, does the manager care what price is selected? Why? Should the Cutting Division be a cost centre or a profit centre under the circumstances?

Required:

a. Determine the operating income for each division if the transfer price from Cutting to Assembly is at cost.

b. Determine the operating income for each division if the transfer price is $9 per cord.

c. Since the Cutting Division sells all of its wood internally to the Assembly Division, does the manager care what price is selected? Why? Should the Cutting Division be a cost centre or a profit centre under the circumstances?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

12

Alsation Ltd. has two divisions:. The Machining Division prepares the raw materials into component parts, and the Assembly Division assembles the components into finished product. No inventories exist in either division at the beginning of the year. During the year the Machining Division prepared 80,000 square metres of sheet metal at a cost of $480,000. All production was transferred to the Assembly Division where the metal was converted into 80,000 units of finished product at an additional costs of $5 per unit. The 80,000 units were sold for $2,000,000.

Required:

a. Determine the operating income for each division if the transfer price from Machining to Assembly is at cost.

b. Determine the operating income for each division if the transfer price is $5/square metre.

c. Since the Machining Division has all of its sales internally to the Assembly Division, does the manager care what price is selected? Why? Should the Machining Division be a cost centre or a profit centre under the circumstances?

Required:

a. Determine the operating income for each division if the transfer price from Machining to Assembly is at cost.

b. Determine the operating income for each division if the transfer price is $5/square metre.

c. Since the Machining Division has all of its sales internally to the Assembly Division, does the manager care what price is selected? Why? Should the Machining Division be a cost centre or a profit centre under the circumstances?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

13

Vancouver Valley Ltd. has two divisions, Computer Services and Management Advisory Services. In addition to its external customers, each division performs work for the other division. The external fees earned by each division in the past year were $200,000 for Computer Services and $350,000 for Management Advisory Services. Computer Services worked 3,000 hours for Management Advisory Services and Management Advisory Services in turn worked 1,200 hours for Computer Services. The total costs of external services performed were $110,000 by Computer Services, and $240,000 by Management Advisory Services.

Required:

a. Determine the operating income for each division and for the company as a whole if the transfer price from Computer Services to Management Advisory Services is $15 per hour and the transfer price from Management Advisory Services to Computer Services is $12.50 per hour.

b. Determine the operating income for each division and for the company as a whole if the transfer price from each to the other is $15 per hour.

c. What are the operating income results for each division and for the company as a whole if the two divisions net their hours worked for each other and charge $12.50 per hour for the one with the excess? Which division manager prefers this arrangement?

Required:

a. Determine the operating income for each division and for the company as a whole if the transfer price from Computer Services to Management Advisory Services is $15 per hour and the transfer price from Management Advisory Services to Computer Services is $12.50 per hour.

b. Determine the operating income for each division and for the company as a whole if the transfer price from each to the other is $15 per hour.

c. What are the operating income results for each division and for the company as a whole if the two divisions net their hours worked for each other and charge $12.50 per hour for the one with the excess? Which division manager prefers this arrangement?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

14

Bedtime Bedding Ltd. manufactures pillows. The Cover Division makes covers, and the Assembly Division makes the finished products. The covers can be sold separately for $5.00. The pillows sell for $6.00. The information related to manufacturing for the most recent year is as follows:

Required:

Compute the operating income for each division and the company as a whole. Use market value as the transfer price. Are all managers happy with this concept? Explain.

Required:

Compute the operating income for each division and the company as a whole. Use market value as the transfer price. Are all managers happy with this concept? Explain.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

15

Sportswear Ltd. manufactures socks. The Athletic Division sells its socks for $6 a pair to outsiders.

Socks have manufacturing variable and fixed costs of $2.50 and $1.50, respectively. The division's total fixed manufacturing costs are $105,000 at the normal volume of 70,000 units.

The European Division has offered to buy 15,000 socks at the full cost of $4. The Athletic Division

has excess capacity and the 15,000 units can be produced without interfering with the current outside

sales of 70,000. The 85,000 volume is within the division's relevant operating range.

Explain whether the Athletic Division should accept the offer.

Socks have manufacturing variable and fixed costs of $2.50 and $1.50, respectively. The division's total fixed manufacturing costs are $105,000 at the normal volume of 70,000 units.

The European Division has offered to buy 15,000 socks at the full cost of $4. The Athletic Division

has excess capacity and the 15,000 units can be produced without interfering with the current outside

sales of 70,000. The 85,000 volume is within the division's relevant operating range.

Explain whether the Athletic Division should accept the offer.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

16

Xenon Autocar Company manufactures automobiles. The Fastback Car Division sells its cars for $50,000 each to the general public. The fastback cars have manufacturing costs of $25,000 each for variable and $15,000 each for fixed costs. The division's total fixed manufacturing costs are $75,000,000 at the normal volume of 5,000 units.

The Coupe Car Division has been unable to meet the demand for its cars this year. It has offered to buy 1,000 cars from the Fastback Car Division at the full cost of $40,000. The Fastback Car Division has excess capacity and the 1,000 units can be produced without interfering with the current outside sales of 5,000. The 6,000 volume is within the division's relevant operating range.

Explain whether the Fastback Car Division should accept the offer.

The Coupe Car Division has been unable to meet the demand for its cars this year. It has offered to buy 1,000 cars from the Fastback Car Division at the full cost of $40,000. The Fastback Car Division has excess capacity and the 1,000 units can be produced without interfering with the current outside sales of 5,000. The 6,000 volume is within the division's relevant operating range.

Explain whether the Fastback Car Division should accept the offer.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

17

Centralia Components Ltd. manufactures cable assemblies used in transportation, recreational products and medical industries . The capacity of the Manufacturing Division is currently 200,000 units and it sells 160,000 units to the outside market at an average price of $96/unit. Cost to manufacture the cable assemblies are $42 variable and $8 fixed. Fixed costs per unit are based on its normal volume of 160,000 units.

Centralia's Mobility Division uses cable assemblies in the manufacture of wheelchairs. It has offered to buy 25,000 units from the Manufacturing Division at $48 per unit. Calculate the operating income of the Manufacturing Division with and without the offer from the Mobility Division. Should the Manufacturing Division management accept the offer?

Centralia's Mobility Division uses cable assemblies in the manufacture of wheelchairs. It has offered to buy 25,000 units from the Manufacturing Division at $48 per unit. Calculate the operating income of the Manufacturing Division with and without the offer from the Mobility Division. Should the Manufacturing Division management accept the offer?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

18

The Brownshoe Company has three specialized divisions. The Casual Shoe Division has asked the Sole Division to supply it with a large quantity of soles. The Sole Division is currently at capacity. The Sole Division sells soles outside for $5.00 each. The Casual Shoe Division, which is operating at 50 percent capacity, has offered to pay $4.00 per sole. The Sole Division has a variable cost of $3.60 per sole. The Casual Shoe Division has the following cost structure:

The manager of Casual Shoe believes that the $4 price from Sole is necessary if the division is to compete in the market for casual shoes.

Required:

a. As manager of Sole Division, would you recommend that your division supply the soles to Casual Shoe? Why?

b. Would it be desirable for the division to supply Casual Shoe with the soles for $4 assuming the Sole Division had excess capacity? Why?

c. What would be the corporate position assuming the Sole Division has excess capacity?

The manager of Casual Shoe believes that the $4 price from Sole is necessary if the division is to compete in the market for casual shoes.

Required:

a. As manager of Sole Division, would you recommend that your division supply the soles to Casual Shoe? Why?

b. Would it be desirable for the division to supply Casual Shoe with the soles for $4 assuming the Sole Division had excess capacity? Why?

c. What would be the corporate position assuming the Sole Division has excess capacity?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

19

Sandra's Sheet Metal Company has two divisions. The Raw Material Division prepares sheet metal at its warehouse facility. The Fabrication Division prepares the cut sheet metal into finished products for the air conditioning industry. No inventories exist in either division at the beginning of 2015. During the year, the Raw Material Division prepared 450,000 square metres of sheet metal at a cost of $1,800,000. All the sheet metal was transferred to the Fabrication Division, where additional operating costs of $1.50 per square metre were incurred. The 450,000 square metres of finished fabricated sheet metal products were sold for $3,875,000.

Required:

a. Determine the operating income for each division if the transfer price from Raw Material to Fabrication is at a cost of $4 per square metre.

b. Determine the operating income for each division if the transfer price is $5 per square metre.

c. Since the Raw Materials Division sells all of its sheet metal internally to the Fabrication Division, does the Raw Materials manager care what price is selected? Why? Should the Raw Materials Division be a cost center or a profit center under the circumstances?

Required:

a. Determine the operating income for each division if the transfer price from Raw Material to Fabrication is at a cost of $4 per square metre.

b. Determine the operating income for each division if the transfer price is $5 per square metre.

c. Since the Raw Materials Division sells all of its sheet metal internally to the Fabrication Division, does the Raw Materials manager care what price is selected? Why? Should the Raw Materials Division be a cost center or a profit center under the circumstances?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

20

Better Food Company recently acquired an olive oil processing company that has an annual capacity of 2,000,000 litres and that processed and sold 1,400,000 litres last year at a market price of $4 per litre. The purpose of the acquisition was to furnish oil for the Cooking Division. The Cooking Division needs 800,000 litres of oil per year. It has been purchasing oil from suppliers at the market price. Production costs at capacity of the olive oil company, now a division, are as follows:

Management is trying to decide what transfer price to use for sales from the newly acquired company to the Cooking Division. The manager of the Olive Oil Division argues that $4, the market price, is appropriate. The manager of the Cooking Division argues that the cost of $2.14 should be used, or perhaps a lower price as fixed overhead cost should not be relevant. Any output of the Olive Oil Division not sold to the Cooking Division can be sold to outsiders for $4 per litre.

Required:

a. Compute the operating income for the Olive Oil Division using a transfer price of $4.

b. Compute the operating income for the Olive Oil Division using a transfer price of $2.14.

c. What transfer price(s) do you recommend? Justify your answer.

Management is trying to decide what transfer price to use for sales from the newly acquired company to the Cooking Division. The manager of the Olive Oil Division argues that $4, the market price, is appropriate. The manager of the Cooking Division argues that the cost of $2.14 should be used, or perhaps a lower price as fixed overhead cost should not be relevant. Any output of the Olive Oil Division not sold to the Cooking Division can be sold to outsiders for $4 per litre.Required:

a. Compute the operating income for the Olive Oil Division using a transfer price of $4.

b. Compute the operating income for the Olive Oil Division using a transfer price of $2.14.

c. What transfer price(s) do you recommend? Justify your answer.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

21

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-Bargaining between selling and buying units

A) cost-based

B) market-based

C) negotiated

D) any method

-Bargaining between selling and buying units

A) cost-based

B) market-based

C) negotiated

D) any method

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

22

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-Budgeted costs

A) cost-based

B) market-based

C) negotiated

D) any method

-Budgeted costs

A) cost-based

B) market-based

C) negotiated

D) any method

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

23

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-145% of full costs

A) cost-based

B) market-based

C) negotiated

D) any method

-145% of full costs

A) cost-based

B) market-based

C) negotiated

D) any method

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

24

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-Prices listed in a trade journal

A) cost-based

B) market-based

C) negotiated

D) any method

-Prices listed in a trade journal

A) cost-based

B) market-based

C) negotiated

D) any method

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

25

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-Selling price less normal sales commissions

A) cost-based

B) market-based

C) negotiated

D) any method

-Selling price less normal sales commissions

A) cost-based

B) market-based

C) negotiated

D) any method

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

26

For each of the following transfer price descriptions or operating situations, tell which of the general methods of transfer pricing it is most appropriate.

-Variable manufacturing cost plus a mark-up

A) cost-based

B) market-based

C) negotiated

D) any method

-Variable manufacturing cost plus a mark-up

A) cost-based

B) market-based

C) negotiated

D) any method

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

27

A market is said to be perfectly-competitive when

A) there is no opportunity costs incurred by the vendor nor by the buyer.

B) the market may be dominated by one or two major companies, but there are many smaller companies also in the market.

C) there is a homogeneous product, equivalent buying and selling prices, and no individual buyers or sellers can affect those prices by their own actions.

D) there are any number of products, equivalent buying and selling prices, and individual buyers or sellers can affect those prices by their own actions.

E) there are any number of products, equivalent buying and selling prices, and individual buyers or sellers can affect those prices by their own actions, but there are no opportunity costs for buyers or sellers.

A) there is no opportunity costs incurred by the vendor nor by the buyer.

B) the market may be dominated by one or two major companies, but there are many smaller companies also in the market.

C) there is a homogeneous product, equivalent buying and selling prices, and no individual buyers or sellers can affect those prices by their own actions.

D) there are any number of products, equivalent buying and selling prices, and individual buyers or sellers can affect those prices by their own actions.

E) there are any number of products, equivalent buying and selling prices, and individual buyers or sellers can affect those prices by their own actions, but there are no opportunity costs for buyers or sellers.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

28

In a time of distress prices, which of the following is TRUE?

A) The vendor division should set the transfer price at the distress price on a long-term basis for stability within the overall company.

B) The vendor division should cease production.

C) The purchasing division should pay normal prices.

D) In the short-term, the transfer price should be the distress price as long as this exceeds the incremental costs.

E) The distress price should be ignored as it is a function of the market, not of the internal capacities of the overall company.

A) The vendor division should set the transfer price at the distress price on a long-term basis for stability within the overall company.

B) The vendor division should cease production.

C) The purchasing division should pay normal prices.

D) In the short-term, the transfer price should be the distress price as long as this exceeds the incremental costs.

E) The distress price should be ignored as it is a function of the market, not of the internal capacities of the overall company.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

29

The Transportation Division of Petrolia Paint Company can purchase paint from an independent producer at $12.60 per litre. The company has three divisions: Production, Transportation, and Paint. The company's Transportation Division is currently buying paint from the Paint Division for $24 per litre. Transfer prices are based on 125 percent of full cost. Which of the following would occur if the company uses dual pricing to record the Transportation Division purchases of paint from the Paint Division?

A) debit the Paint Division for $24.00

B) credit the corporate cost account for $11.40

C) debit the Transportation Division for $12.60

D) credit the Paint Division for $12.60

E) credit the Paint Division for $32.40

A) debit the Paint Division for $24.00

B) credit the corporate cost account for $11.40

C) debit the Transportation Division for $12.60

D) credit the Paint Division for $12.60

E) credit the Paint Division for $32.40

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

30

Use the information below to answer the following question(s).

Crush Company makes internal transfers at 180% of full cost. The Soda Refining division purchases 30,000 containers of carbonated water per day, on average, from a local supplier, who delivers the water for $30 per container via an external shipper. In order to reduce costs the company located an independent producer in Manitoba who is willing to sell 30,000 containers at $20 each, delivered to Crush Company's shipping division in Manitoba. The company's Shipping Division in Manitoba can ship the 30,000 containers at a variable cost of $2.50 per container and a full cost, based on practical capacity, of $4.00 per container. When the company's Manitoba shipping division ships for external customers is charges $6.00 per container.

-What is the total cost to Crush Company if the carbonated water is purchased from the local supplier?

A) $900,000

B) $1,200,000

C) $975,000

D) $1,080,000

E) $1,620,000

Crush Company makes internal transfers at 180% of full cost. The Soda Refining division purchases 30,000 containers of carbonated water per day, on average, from a local supplier, who delivers the water for $30 per container via an external shipper. In order to reduce costs the company located an independent producer in Manitoba who is willing to sell 30,000 containers at $20 each, delivered to Crush Company's shipping division in Manitoba. The company's Shipping Division in Manitoba can ship the 30,000 containers at a variable cost of $2.50 per container and a full cost, based on practical capacity, of $4.00 per container. When the company's Manitoba shipping division ships for external customers is charges $6.00 per container.

-What is the total cost to Crush Company if the carbonated water is purchased from the local supplier?

A) $900,000

B) $1,200,000

C) $975,000

D) $1,080,000

E) $1,620,000

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

31

Mar Company has two decentralized divisions, X and Y. Division X has been purchasing certain component parts from Division Y at $75 per unit. Because Division Y plans to raise the price to $100 per unit, Division X desires to purchase these parts from external suppliers for $75 per unit. The following information is available:

If Division X buys from an external supplier, the facilities Division Y uses to manufacture these parts will be idle. Assuming Division Y's fixed costs cannot be avoided, what is the result if Mar requires Division X to buy from Division Y at a transfer price of $100 per unit?

If Division X buys from an external supplier, the facilities Division Y uses to manufacture these parts will be idle. Assuming Division Y's fixed costs cannot be avoided, what is the result if Mar requires Division X to buy from Division Y at a transfer price of $100 per unit?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

32

A company has two divisions. The Bottle Division produces products that have variable costs of $3 per unit. For the current year, sales were 150,000 to outsiders at $5 per unit and 40,000 units to the Mixing Division at 140 percent of variable costs. Under a dual transfer pricing system, the Mixing Division pays only the variable cost per unit. The fixed costs of Bottle Division were $125,000 per year.

Mixing sells its finished products to outside customers for $11.50 per unit. Mixing has variable costs of $2.50 per unit in addition to the costs from Bottle. The annual fixed costs of Mixing were $85,000. There were no beginning or ending inventories during the year.

Required:

What are the operating incomes of the two divisions and the company as a whole for the year? Explain why the company operating income is less than the sum of the two divisions' total income.

Mixing sells its finished products to outside customers for $11.50 per unit. Mixing has variable costs of $2.50 per unit in addition to the costs from Bottle. The annual fixed costs of Mixing were $85,000. There were no beginning or ending inventories during the year.

Required:

What are the operating incomes of the two divisions and the company as a whole for the year? Explain why the company operating income is less than the sum of the two divisions' total income.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

33

The Home Office Company makes all types of office desks. The Computer Desk Division is currently producing 10,000 desks per year with a capacity of 15,000. The variable costs assigned to each desk are $300 and annual fixed costs of the division are $900,000. The computer desks sell for $400.

The Executive Division wants to buy 5,000 desks at $280 for its custom office design business. The Computer Desk manager refuses the order because the price is below variable cost. The Executive manager argues that the order should be accepted because it will lower the fixed cost per desk from $90 to $60 and will take the division to its capacity, thereby causing operations to be at their most efficient level.

Required:

a. Should the order from Executive Division be accepted by Computer Desk? Explain why or why not.

b. From the perspective of the Computer Desk Division and the company, should the order be accepted if the Executive Division plans on selling the chairs in the outside market for $420 after incurring additional costs of $100 per desk?

c. What action should the company president take?

The Executive Division wants to buy 5,000 desks at $280 for its custom office design business. The Computer Desk manager refuses the order because the price is below variable cost. The Executive manager argues that the order should be accepted because it will lower the fixed cost per desk from $90 to $60 and will take the division to its capacity, thereby causing operations to be at their most efficient level.

Required:

a. Should the order from Executive Division be accepted by Computer Desk? Explain why or why not.

b. From the perspective of the Computer Desk Division and the company, should the order be accepted if the Executive Division plans on selling the chairs in the outside market for $420 after incurring additional costs of $100 per desk?

c. What action should the company president take?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

34

Bradford Manufacturing Ltd. manufactures custom metal perforating and fabricating. Its Fabricating Division can transfer the perforated metal components to Bradford's Automotive Division or it can sell its products on the external market. Fabricating currently produces and sells 350,000 units per year to the external market at an average price of $38 per unit. Variable costs of production average $22.50 and fixed costs of $6.50/unit. Fabricating incurs $2.50 of variable selling costs on external sales. Fixed costs are based on the practical capacity of the plant which is 400,000 per year. The Automotive Division is interested in acquiring up to 50,000 units per year.

Required:

a. From the standpoint of Bradford Manufacturing Ltd., should the units be transferred? Determine the financial benefit or cost of your recommendation.

b. Using the general guidelines for transfer pricing, what is the minimum transfer price Fabricating should accept?

c. What is the range of acceptable transfer prices?

d. Now assume that demand in the external market for the components is expected to increase by 8%. The Automotive Division has negotiated with an external supplier to supply 50,000 units at a price of $34.50/unit. However, if the Automotive Division reduces its volume below the 50,000 unit volume, it must pay $39 per unit. What is the optimum sourcing arrangement for the company?

Required:

a. From the standpoint of Bradford Manufacturing Ltd., should the units be transferred? Determine the financial benefit or cost of your recommendation.

b. Using the general guidelines for transfer pricing, what is the minimum transfer price Fabricating should accept?

c. What is the range of acceptable transfer prices?

d. Now assume that demand in the external market for the components is expected to increase by 8%. The Automotive Division has negotiated with an external supplier to supply 50,000 units at a price of $34.50/unit. However, if the Automotive Division reduces its volume below the 50,000 unit volume, it must pay $39 per unit. What is the optimum sourcing arrangement for the company?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

35

Walton Industries has two divisions: Machining and Assembly. The Assembly Division is looking to source 20,000 units annually of specialized component product from Machining Division. The special components have variable costs of $260 per unit in variable production costs. The Machine Products Division has a bid from an outside supplier of $445 per unit. However, to meet the requirements of the Assembly Division, Machining would have to cut back production of an existing product. This product sells for $565 per unit, and requires $369 per unit in variable production costs. Packaging and shipping costs of the existing product are $12 per unit, but these would be slashed by 75% for the specialized component for Assembly. Machining currently sells 120,000 units of the existing product and this volume would have to be reduced by 25% to meet the Assembly Division's demand.

Required:

Should the transfer take place, and if so, what would be the range of acceptable transfer prices?

Required:

Should the transfer take place, and if so, what would be the range of acceptable transfer prices?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

36

Payne Ltd. has two divisions. The Compound Division makes QZ54, an industrial compound, which is then transferred to the Processing Division. The Processing Division further processes the QZ54 and sells the final product to customers at $87/kg. Capacity in the Compound Division is 800,000 kg. QZ54 can be obtained on the external market at $50/kg Data regarding the costs per kilogram in each division are presented below:

*In the Compound Division the variable overhead is 80% of the total, and in Processing variable overhead represents 65% of the total. Fixed overhead rates are based on capacity of 800,000 kg. in each division.

In addition to the manufacturing costs, the Compound Division would incur $2 per kilogram of selling costs which would be avoided on internal transfers. Similarly the Processing Division would avoid $3/kg. of ordering costs on internal purchases.

Required:

a. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a market transfer price.

b. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a transfer pricing policy based on 125% of absorption manufacturing cost.

c. Comment on your calculations in a and b in terms of the respective division managers preferences.

d. Should the company transfer its 800,000 kg. assuming the Compound Division can sell all of its output on the external market?

*In the Compound Division the variable overhead is 80% of the total, and in Processing variable overhead represents 65% of the total. Fixed overhead rates are based on capacity of 800,000 kg. in each division.In addition to the manufacturing costs, the Compound Division would incur $2 per kilogram of selling costs which would be avoided on internal transfers. Similarly the Processing Division would avoid $3/kg. of ordering costs on internal purchases.

Required:

a. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a market transfer price.

b. Calculate the operating incomes for each division assuming 800,000 kg. of QZ54 are transferred and the company uses a transfer pricing policy based on 125% of absorption manufacturing cost.

c. Comment on your calculations in a and b in terms of the respective division managers preferences.

d. Should the company transfer its 800,000 kg. assuming the Compound Division can sell all of its output on the external market?

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

37

The Micro Division of Silicon Computers produces computer chips that are sold to the Personal Computer Division and to outsiders. Operating data for the Micro Division are as follows:

?

The Personal Computer Division has just received an offer from an outside supplier to furnish chips at $8.60 each. The manager of Micro Division is not willing to meet the $8.60 price. She argues that it costs her $9.00 to produce and sell each chip. Sales to outside customers are at a maximum of 200,000 chips.

Required:

a. Verify the Micro Division's $9.00 unit cost figure.

b. Should the Micro Division meet the outside price of $8.60? Explain on a per unit basis.

c. Prepare a Micro Division income statement for the sale to the Personal Computer Division assuming that the unit selling price of $8.60 is agreed. Comment on the allocation of fixed costs.

?

The Personal Computer Division has just received an offer from an outside supplier to furnish chips at $8.60 each. The manager of Micro Division is not willing to meet the $8.60 price. She argues that it costs her $9.00 to produce and sell each chip. Sales to outside customers are at a maximum of 200,000 chips.

Required:

a. Verify the Micro Division's $9.00 unit cost figure.

b. Should the Micro Division meet the outside price of $8.60? Explain on a per unit basis.

c. Prepare a Micro Division income statement for the sale to the Personal Computer Division assuming that the unit selling price of $8.60 is agreed. Comment on the allocation of fixed costs.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

38

The Assembly Division of Canadian Car Company has offered to purchase 90,000 batteries from the Electrical Division for $104 per unit. At a normal volume of 250,000 batteries per year, production costs per battery are as follows:

The Electrical Division has been selling 250,000 batteries per year to outside buyers at $136 each. Capacity is 350,000 batteries per year. The Assembly Division has been buying batteries from outside sources for $130 each.

Required:

a. Should the Electrical Division manager accept the offer as is, make a counter offer, or reject the offer? Explain.

b. From the company's perspective, will the internal sales be of any benefit? Explain

The Electrical Division has been selling 250,000 batteries per year to outside buyers at $136 each. Capacity is 350,000 batteries per year. The Assembly Division has been buying batteries from outside sources for $130 each.

Required:

a. Should the Electrical Division manager accept the offer as is, make a counter offer, or reject the offer? Explain.

b. From the company's perspective, will the internal sales be of any benefit? Explain

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

39

River Road Paint Company has two divisions. The Production Division produces base colours used by the Mixing Division. In 2015 the Production Division had external sales of 200,000 units at $8.00 per unit; and, transferred 60,000 units to the Mixing Division. The variable costs in the Production Division were $5 per unit and the fixed costs were $520,000 based on a practical capacity of 260,000 units. The Mixing Division sells its finished product to customers for $11.20 per unit. The Mixing Division had variable costs of $2.50 per unit and the annual fixed costs were $150,000. There were no beginning or ending inventories during the year.

Required:

Prepare the general journal entry for the transfer assuming that a dual pricing arrangement has been agreed to that requires the Mixing Department to pay the variable cost and the Production Department to receive the market price.

Required:

Prepare the general journal entry for the transfer assuming that a dual pricing arrangement has been agreed to that requires the Mixing Department to pay the variable cost and the Production Department to receive the market price.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

40

Sonora Manufacturing Inc. designs and builds off-road vehicles. The Frame Division builds frames that are used by the Assembly Division, and also sells frames externally to companies that produce vehicles such as golf carts. The Frame Division has an annual practical capacity of 5,000 units; a theoretical capacity of 7,300 units; and, a master-budget capacity of 4,000 units. The master-budget capacity is composed of 2,500 units produced for internal requirements, and the remainder sold externally for $800 per unit. The Frame Division has $150,000 of fixed costs. The variable costs for the units produced for internal purposes are $900 per unit, and for external sales $475. Sonora Manufacturing Inc. company policy is that internal transfers are to be done at full cost.

The Frame Division has been approached by a golf cart manufacturer who has offered to purchase 3,000 frames as a one-time special order for $650 per unit. This is an all or none order.

The Assembly Division can contract out the production of frames for $1,050 per unit.

Required:

a. Determine Frame Division's full cost per unit for the frames produced for internal use and the frames that a produced for external sales. Justify your choice of denominator activity level when calculating the fixed cost per unit.

b. Using the general guidelines for transfer pricing, what is the minimum transfer price the Frame Division should accept? Hint: There will be separate minimum transfer prices for the existing external customers and the one-time special order.

c. From a corporate point of view should the one-time special offer be accepted. Justify your answer on quantitative and qualitative considerations.

The Frame Division has been approached by a golf cart manufacturer who has offered to purchase 3,000 frames as a one-time special order for $650 per unit. This is an all or none order.

The Assembly Division can contract out the production of frames for $1,050 per unit.

Required:

a. Determine Frame Division's full cost per unit for the frames produced for internal use and the frames that a produced for external sales. Justify your choice of denominator activity level when calculating the fixed cost per unit.

b. Using the general guidelines for transfer pricing, what is the minimum transfer price the Frame Division should accept? Hint: There will be separate minimum transfer prices for the existing external customers and the one-time special order.

c. From a corporate point of view should the one-time special offer be accepted. Justify your answer on quantitative and qualitative considerations.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

41

Global Giant, a multinational corporation, has a producing subsidiary in a low tax rate country and a marketing subsidiary in a high tax country. If Global Giant wants to minimize its worldwide tax liability, we would expect Global Giant to

A) stop producing in the low tax rate country.

B) stop marketing in the high tax rate country.

C) establish a low transfer price when the producing unit sells to the marketing unit.

D) establish a high transfer price when the producing unit sells to the marketing unit.

E) be indifferent as to its transfer pricing policy.

A) stop producing in the low tax rate country.

B) stop marketing in the high tax rate country.

C) establish a low transfer price when the producing unit sells to the marketing unit.

D) establish a high transfer price when the producing unit sells to the marketing unit.

E) be indifferent as to its transfer pricing policy.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

42

Empire Ltd. has two divisions. Division C is located in Canada where the income tax rate is 40%. Division K is located in Korea where the income tax rate is 30%. Division C produces an intermediate product at a variable cost of $100 per unit and transfers the product to Division K where it is finished and sold for $500 per unit. Variable costs in Division K are $80 per unit. Fixed costs are $75,000 per year in Division C and $90,000 per year in Division K. Assume 1,000 units are produced and transferred annually and the minimum transfer price allowed by the Canadian tax authorities is the variable cost. Also assume operating income in each country is equal to taxable income.

Required:

a. What transfer price should be set for Empire to minimize its total income taxes? Show your calculations.

b. If Empire desires to minimize its total income taxes, calculate the amount of tax liability in each country.

Required:

a. What transfer price should be set for Empire to minimize its total income taxes? Show your calculations.

b. If Empire desires to minimize its total income taxes, calculate the amount of tax liability in each country.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

43

Stavanger Ltd. is a Canadian company with a fully owned subsidiary in Ireland. The Irish subsidiary produces a component for off shore gas compressors that are sold in Canada. The components have a variable cost of 1,700 Euros and a full cost of 2,100 Euros. The 2,000 components required can be purchased in Canada for $3,500. Assume the minimum transfer price allowed by the Canadian tax authorities is the variable cost and the maximum is the market value. Also assume operating income in each country is equal to taxable income. One Euro is worth $1.45 Canadian. The marginal tax rate in Canada is 25% and in Ireland 12.5%.

Required:

a. What transfer price should be set for Stavanger Ltd. to minimize its total income taxes? Show your calculations.

b. If Stavanger Ltd. desires to minimize its total income taxes, calculate the amount of tax liability in each country in Canadian dollars.

Required:

a. What transfer price should be set for Stavanger Ltd. to minimize its total income taxes? Show your calculations.

b. If Stavanger Ltd. desires to minimize its total income taxes, calculate the amount of tax liability in each country in Canadian dollars.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

44

Hendricks Ltd. of Calgary manufactures and sells computers. The Manufacturing Division is located in China and transfers 75% of its output to the Assembly Division in the Philippines. The balance of the product is sold in the local market at 2,100 yuan/unit. The Philippines division sells 20% of its output in the local market at 31,500 pesos/unit, with the balance shipped to Calgary. The Calgary operation packages the units and sells the final product at $1,900 Canadian per unit.

The following budget data are available:

Exchange rates are: $1 Canadian = 7 yuan and $1 Canadian = 45 pesos

Tax rates are 45% in China, 20% in the Philippines and 40% in Canada. Income taxes are not included in the calculation of cost-based transfer prices. Assume that Hendricks does not pay Canadian tax on amounts already taxed in foreign jurisdictions. Take each calculation to 2 decimal places.

Required:

The company has determined that it may transfer units at 250% of variable cost or at market and comply with all existing tax legislation. Which transfer pricing method should the company pursue? Support your recommendation with appropriate calculations.

The following budget data are available:

Exchange rates are: $1 Canadian = 7 yuan and $1 Canadian = 45 pesos

Tax rates are 45% in China, 20% in the Philippines and 40% in Canada. Income taxes are not included in the calculation of cost-based transfer prices. Assume that Hendricks does not pay Canadian tax on amounts already taxed in foreign jurisdictions. Take each calculation to 2 decimal places.

Required:

The company has determined that it may transfer units at 250% of variable cost or at market and comply with all existing tax legislation. Which transfer pricing method should the company pursue? Support your recommendation with appropriate calculations.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

45

Clark Industries Ltd. manufactures monochromators that are used in a variety of applications. The Monochromator Division (M Division) sells its monochromators both internally and externally. It is operating at 80% of its 250,000 unit capacity and internal sales account for approximately 20% of its current sales volume. Internally the monochromators are transferred into the Aerospace Division (A Division) at a transfer price of $11,250 each. Variable production costs are the same for internal and external sales.

The income statement for the M Division is presented below:

The A Division uses one component in the production of its final product that sells for $75,000/unit. Other variable costs in the A Division are 40% of sales. and fixed costs per unit at its current capacity of 40,000 units are $17,250.

The Aerospace Division is operating at its full capacity of 40,000 units and is evaluating whether it should invest to increase capacity. The investment would cost $900,000,000 and would have a useful life of 3 years. The equipment could be sold for $800,000 at the end of its useful life. For tax purposes it would be sold on January 1 of year 4. The machine would be used to manufacture a variation of its current product with the same transfer price. This new product would sell for $68,000 per unit. The variable cost ratio will be 45% of the selling price. The additional capacity of the new machine would be 14,000 units. It would qualify for a 30% CCA rate and the company would continue to have assets in the pool.

Required:

a. Evaluate the current transfer pricing policy from the standpoint of each division manager as well as the company as a whole.

b. Using net present value (NPV) analysis, would the A Division manager want to invest in the new equipment if the required rate of return is 12% and the tax rate is 25%?

c. If the investment is evaluated from a corporate perspective using NPV analysis and the 12% discount rate, does the decision change? Explain.

The income statement for the M Division is presented below:

The A Division uses one component in the production of its final product that sells for $75,000/unit. Other variable costs in the A Division are 40% of sales. and fixed costs per unit at its current capacity of 40,000 units are $17,250.The Aerospace Division is operating at its full capacity of 40,000 units and is evaluating whether it should invest to increase capacity. The investment would cost $900,000,000 and would have a useful life of 3 years. The equipment could be sold for $800,000 at the end of its useful life. For tax purposes it would be sold on January 1 of year 4. The machine would be used to manufacture a variation of its current product with the same transfer price. This new product would sell for $68,000 per unit. The variable cost ratio will be 45% of the selling price. The additional capacity of the new machine would be 14,000 units. It would qualify for a 30% CCA rate and the company would continue to have assets in the pool.

Required:

a. Evaluate the current transfer pricing policy from the standpoint of each division manager as well as the company as a whole.

b. Using net present value (NPV) analysis, would the A Division manager want to invest in the new equipment if the required rate of return is 12% and the tax rate is 25%?

c. If the investment is evaluated from a corporate perspective using NPV analysis and the 12% discount rate, does the decision change? Explain.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 45 flashcards in this deck.