Deck 2: Partnerships: Organization and Operation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

May goodwill appropriately be recognized in the journal entry to record the admission of a new partner to an existing limited liability partnership for an investment of:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

The partners of Wohl, Xavier, and Yepp LLP shared net income and losses in a 5:3:2 ratio, respectively. The capital account balances on April 30, 2006, were as follows:  The carrying amounts of the assets and liabilities of the partnership were the same as their current fair values. Zabb was to be admitted to the partnership with a 20% capital interest and a 20% share of net income and losses in exchange for a cash investment. No goodwill or bonus was to be recognized. The amount of cash that Partner Zabb should invest in the partnership is:

The carrying amounts of the assets and liabilities of the partnership were the same as their current fair values. Zabb was to be admitted to the partnership with a 20% capital interest and a 20% share of net income and losses in exchange for a cash investment. No goodwill or bonus was to be recognized. The amount of cash that Partner Zabb should invest in the partnership is:

A) $30,000

B) $36,000

C) $37,500

D) $40,000

E) Some other amount

The carrying amounts of the assets and liabilities of the partnership were the same as their current fair values. Zabb was to be admitted to the partnership with a 20% capital interest and a 20% share of net income and losses in exchange for a cash investment. No goodwill or bonus was to be recognized. The amount of cash that Partner Zabb should invest in the partnership is:A) $30,000

B) $36,000

C) $37,500

D) $40,000

E) Some other amount

Question

The appropriate format of the January 31, 2006, closing entry for App & Brie Limited Liability Partnership, whose two partners had withdrawn their salaries from the partnership during January, 2006, is (explanation omitted):

A)

B)

C)

D)

A)

B)

C)

D)

Question

Alf and Ben, partners in Alf & Ben LLP who share net income and losses equally, had capital account balances of $40,000 and $60,000, respectively, on September 25, 2006, on which date the following journal entry was prepared for the partnership:

The foregoing journal entry:

The foregoing journal entry:

A) Is acceptable

B) Should be replaced by an entry allocating an $8,000 bonus equally to Alf and to Ben

C) Should be replaced by an entry allocating a $24,000 bonus equally to Alf and to Ben

D) Should not reflect either a bonus or goodwill

The foregoing journal entry:A) Is acceptable

B) Should be replaced by an entry allocating an $8,000 bonus equally to Alf and to Ben

C) Should be replaced by an entry allocating a $24,000 bonus equally to Alf and to Ben

D) Should not reflect either a bonus or goodwill

Question

On June 30, 2006, the balance sheet for Coll, Maduro & Prieto LLP (together with the income-sharing ratio) was as follows:  Coll decided to retire from the partnership. By mutual agreement, the partnership assets were to be adjusted to their current fair value of $216,000 on June 30, 2006. It was agreed that the partnership would pay Coll $61,200 cash for Coll's partnership interest, including Coll's loan that was to be repaid in full. No goodwill was to be recognized. After Coll's retirement, the balance of Maduro's capital account is:

Coll decided to retire from the partnership. By mutual agreement, the partnership assets were to be adjusted to their current fair value of $216,000 on June 30, 2006. It was agreed that the partnership would pay Coll $61,200 cash for Coll's partnership interest, including Coll's loan that was to be repaid in full. No goodwill was to be recognized. After Coll's retirement, the balance of Maduro's capital account is:

A) $36,450

B) $39,000

C) $45,450

D) $46,200

E) Some other amount

Coll decided to retire from the partnership. By mutual agreement, the partnership assets were to be adjusted to their current fair value of $216,000 on June 30, 2006. It was agreed that the partnership would pay Coll $61,200 cash for Coll's partnership interest, including Coll's loan that was to be repaid in full. No goodwill was to be recognized. After Coll's retirement, the balance of Maduro's capital account is:A) $36,450

B) $39,000

C) $45,450

D) $46,200

E) Some other amount

Question

Are per unit amounts disclosed in a limited partnership's:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Roe, Soh, & Tow Limited Liability Partnership was organized and began operations on February 1, 2005, with the following capital account balances: Roe, $50,000; Soh, $70,000; Tow, $80,000. The income-sharing arrangement provided for the following:

For the fiscal year ended January 31, 2006, Roe, Soh, & Tow Limited Liability Partnership had income of $180,000, before recognition of salaries expense, and the partners withdrew their authorized salaries in cash.

For the fiscal year ended January 31, 2006, Roe, Soh, & Tow Limited Liability Partnership had income of $180,000, before recognition of salaries expense, and the partners withdrew their authorized salaries in cash.

Prepare journal entries (omit explanations) for Roe, Soh, & Tow Limited Liability Partnership on January 31, 2006.

For the fiscal year ended January 31, 2006, Roe, Soh, & Tow Limited Liability Partnership had income of $180,000, before recognition of salaries expense, and the partners withdrew their authorized salaries in cash.Prepare journal entries (omit explanations) for Roe, Soh, & Tow Limited Liability Partnership on January 31, 2006.

Question

Question

Question

Question

Question

The capital account balances for Ray & Randall LLP on May 31, 2006, were as follows:

Ray and Randall shared net income and losses in the ratio of 3:2, respectively. The partners agreed to admit Appleton to the partnership with a 35% interest in partnership capital and net income. Appleton invested $80,000 cash, and no goodwill was recognized.

Ray and Randall shared net income and losses in the ratio of 3:2, respectively. The partners agreed to admit Appleton to the partnership with a 35% interest in partnership capital and net income. Appleton invested $80,000 cash, and no goodwill was recognized.

Prepare a working paper to compute the capital account balance for each partner immediately after Appleton was admitted to Ray, Randall & Appleton LLP on May 31, 2003.

Ray and Randall shared net income and losses in the ratio of 3:2, respectively. The partners agreed to admit Appleton to the partnership with a 35% interest in partnership capital and net income. Appleton invested $80,000 cash, and no goodwill was recognized.Prepare a working paper to compute the capital account balance for each partner immediately after Appleton was admitted to Ray, Randall & Appleton LLP on May 31, 2003.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/39

Play

Full screen (f)

Deck 2: Partnerships: Organization and Operation

1

A limited liability partnership is a taxable entity under federal income tax laws.

False

2

The balances of limited liability partners' drawing ledger accounts are closed to the partners' capital accounts at the end of an accounting period.

True

3

The Interest Expense ledger account is debited when interest on partners' capital account balances is credited to partners in the distribution of limited liability partnership net income.

False

4

A limited liability partnership generally is considered to be an association of persons rather than a separate accounting entity.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

5

A limited liability partnership contract provision for the allowance of interest on partners' capital account balances in the allocation of net income must be applied when the partnership has a net loss.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

6

From a legal standpoint, the admission or withdrawal of a partner does not terminate the existence of a limited liability partnership.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

7

The acquisition of an ownership interest by a new partner directly from an existing partner does not change either total assets or net assets of a limited liability partnership.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

8

A bonus to a partner based on income after the bonus is recognized as an expense by the limited liability partnership.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

9

In a limited partnership, the personal liability of one or more of the partners for the unpaid debts of the partnership is limited to the amounts those partners had invested in the partnership.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

10

The value assigned to noncash assets invested by partners in a limited liability partnership is the cost of the assets or the current fair value of the assets at the time of investment, whichever is lower.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

11

A guarantee of a minimum income of $15,000 or a salary allowance of $15,000 to a partner will give the partner the same share of partnership net income, whether the limited liability partnership has a net income or a net loss.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

12

Goodwill may be recognized as part of the investment of a new partner only when the new partner invests the identifiable net assets of a business enterprise that are expected to generate superior earnings for the limited liability partnership.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

13

Limited partnerships may be required to file registration statements with the Securities and Exchange Commission.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

14

Partners' drawings are displayed in a limited liability partnership's statement of cash flows as cash flows from operating activities.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

15

A partner's withdrawal of assets from a limited liability partnership that is considered a permanent reduction in that partner's equity is debited to the partner's:

A) Drawing account

B) Retained Earnings account

C) Capital account

D) Loan Receivable account

A) Drawing account

B) Retained Earnings account

C) Capital account

D) Loan Receivable account

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

16

The drawing ledger accounts of limited liability partners are used:

A) To record the partners' salaries

B) To reduce the partners' capital account balances at the end of an accounting period

C) In the same manner as the partners' loan accounts

D) To record the partners' share of net income or loss for an accounting period

A) To record the partners' salaries

B) To reduce the partners' capital account balances at the end of an accounting period

C) In the same manner as the partners' loan accounts

D) To record the partners' share of net income or loss for an accounting period

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

17

The partnership contract for Cole & Dane LLP provides that Cole is to receive a bonus of 20% of net income (after the bonus) and that the remaining net income is to be divided equally. If the partnership income before the bonus for Year 2006 is $57,600, Cole's share of the pre-bonus income is:

A) $28,800

B) $33,600

C) $34,560

D) $43,200

E) Some other amount

A) $28,800

B) $33,600

C) $34,560

D) $43,200

E) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

18

May goodwill appropriately be recognized in the journal entry to record the admission of a new partner to an existing limited liability partnership for an investment of:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

19

Morse and Niguel, partners of Morse & Niguel Limited Liability Partnership, shared net income and losses equally. On March 1, 2006, Odmark was admitted to the partnership; the new ratio for sharing net income and losses was Morse, 25%; Niguel, 25%; and Odmark, 50%. Odmark invested the net assets of a single proprietorship. The value of Odmark's proprietorship as a going concern was $120,000, and the current fair value of the proprietorship's identifiable net assets was $90,000. The difference of $30,000 between the going-concern value and the identifiable net assets value is recognized as:

A) Goodwill credited to Odmark's capital account

B) Goodwill credited $15,000 each to the capital accounts of Morse and Niguel

C) A bonus of $15,000 each to Morse and Niguel

D) A bonus of $30,000 to Odmark with offsetting debits of $15,000 each to the capital accounts of Morse and Niguel

A) Goodwill credited to Odmark's capital account

B) Goodwill credited $15,000 each to the capital accounts of Morse and Niguel

C) A bonus of $15,000 each to Morse and Niguel

D) A bonus of $30,000 to Odmark with offsetting debits of $15,000 each to the capital accounts of Morse and Niguel

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

20

The partnership contract for Pyle & Quan LLP provided that Pyle was to receive a salary of $12,000 a year, Quan was to receive a salary of $15,000 a year, and the resultant net income or loss after partners' salaries expense was to be divided 60% to Pyle and 40% to Quan. A partnership income of $20,000 before partners' salaries expense for the fiscal year ended May 31, 2006, is allocated:

A) $12,000 to Pyle and $8,000 to Quan

B) $8,889 to Pyle and $11,111 to Quan

C) $7,800 to Pyle and $12,200 to Quan

D) In some other amounts

A) $12,000 to Pyle and $8,000 to Quan

B) $8,889 to Pyle and $11,111 to Quan

C) $7,800 to Pyle and $12,200 to Quan

D) In some other amounts

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

21

Bruce Chapman was admitted to the Adams & Bye Limited Liability Partnership on May 31, 2006, by an investment of $40,000 cash for a 20% interest in partnership net assets. Prior to the admission of Chapman, the capital accounts of Adams and Bye, who shared net income and losses equally, had balances of $70,000 and $30,000, respectively. The preferable accounting method for the admission of Chapman includes credits of:

A) $6,000 each to the capital accounts of Adams and Bye

B) $30,000 each to the capital accounts of Adams and Bye

C) $28,000 and $12,000, respectively, to the capital accounts of Adams and Bye

D) Some other amounts to the capital accounts of Adams and Bye

A) $6,000 each to the capital accounts of Adams and Bye

B) $30,000 each to the capital accounts of Adams and Bye

C) $28,000 and $12,000, respectively, to the capital accounts of Adams and Bye

D) Some other amounts to the capital accounts of Adams and Bye

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

22

On January 31, 2006, Amy Reid withdrew from Reid, Sayle & Todd LLP, whose partners had an income-sharing ratio of 40%, 35%, and 25%, respectively, for a cash payment of $121,000, despite Reid's having a capital account balance of $100,000 on that date. The preferable method of accounting for Reid's withdrawal includes a:

A) $12,250 debit to Sayle, Capital

B) $21,000 debit to Goodwill

C) $52,500 debit to Goodwill

D) $5,250 debit to Todd, Capital

A) $12,250 debit to Sayle, Capital

B) $21,000 debit to Goodwill

C) $52,500 debit to Goodwill

D) $5,250 debit to Todd, Capital

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

23

The partners of Ames, Brod, and Chan LLP had capital account balances of $75,000, $45,000, add $30,000, respectively, and shared net income and losses equally. For an investment of $75,000 cash, Dell was admitted to the partnership with a 25% interest in capital and net income. Based on this information, which of the following may justify the amount of investment?

A) Dell received a bonus from Ames, Brod, and Chan.

B) Partnership net assets were overvalued immediately prior to Dell's admission to the partnership.

C) The carrying amount of the partnership's net assets was less than their current fair value immediately prior to Dell's admission to the partnership.

D) Dell apparently invested goodwill in the partnership.

A) Dell received a bonus from Ames, Brod, and Chan.

B) Partnership net assets were overvalued immediately prior to Dell's admission to the partnership.

C) The carrying amount of the partnership's net assets was less than their current fair value immediately prior to Dell's admission to the partnership.

D) Dell apparently invested goodwill in the partnership.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

24

If a partner who retires from a limited liability partnership receives an amount of cash less than the partner's capital account balance:

A) Identifiable net assets of the partnership should be written down

B) Bonuses should be allocated to the continuing partners

C) "Negative goodwill" should be recognized by the partnership

D) None of the foregoing should take place

A) Identifiable net assets of the partnership should be written down

B) Bonuses should be allocated to the continuing partners

C) "Negative goodwill" should be recognized by the partnership

D) None of the foregoing should take place

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

25

The partners of Wohl, Xavier, and Yepp LLP shared net income and losses in a 5:3:2 ratio, respectively. The capital account balances on April 30, 2006, were as follows: The carrying amounts of the assets and liabilities of the partnership were the same as their current fair values. Zabb was to be admitted to the partnership with a 20% capital interest and a 20% share of net income and losses in exchange for a cash investment. No goodwill or bonus was to be recognized. The amount of cash that Partner Zabb should invest in the partnership is:

A) $30,000

B) $36,000

C) $37,500

D) $40,000

E) Some other amount

The carrying amounts of the assets and liabilities of the partnership were the same as their current fair values. Zabb was to be admitted to the partnership with a 20% capital interest and a 20% share of net income and losses in exchange for a cash investment. No goodwill or bonus was to be recognized. The amount of cash that Partner Zabb should invest in the partnership is:A) $30,000

B) $36,000

C) $37,500

D) $40,000

E) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

26

The appropriate format of the January 31, 2006, closing entry for App & Brie Limited Liability Partnership, whose two partners had withdrawn their salaries from the partnership during January, 2006, is (explanation omitted):

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

27

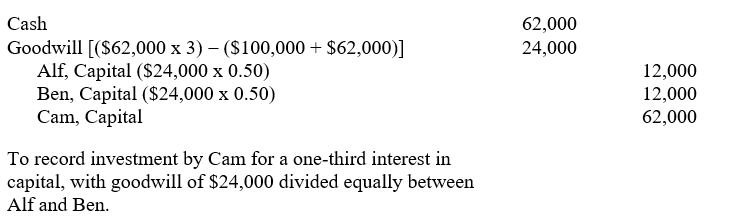

Alf and Ben, partners in Alf & Ben LLP who share net income and losses equally, had capital account balances of $40,000 and $60,000, respectively, on September 25, 2006, on which date the following journal entry was prepared for the partnership:

The foregoing journal entry:

A) Is acceptable

B) Should be replaced by an entry allocating an $8,000 bonus equally to Alf and to Ben

C) Should be replaced by an entry allocating a $24,000 bonus equally to Alf and to Ben

D) Should not reflect either a bonus or goodwill

The foregoing journal entry:A) Is acceptable

B) Should be replaced by an entry allocating an $8,000 bonus equally to Alf and to Ben

C) Should be replaced by an entry allocating a $24,000 bonus equally to Alf and to Ben

D) Should not reflect either a bonus or goodwill

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

28

On June 30, 2006, the balance sheet for Coll, Maduro & Prieto LLP (together with the income-sharing ratio) was as follows: Coll decided to retire from the partnership. By mutual agreement, the partnership assets were to be adjusted to their current fair value of $216,000 on June 30, 2006. It was agreed that the partnership would pay Coll $61,200 cash for Coll's partnership interest, including Coll's loan that was to be repaid in full. No goodwill was to be recognized. After Coll's retirement, the balance of Maduro's capital account is:

A) $36,450

B) $39,000

C) $45,450

D) $46,200

E) Some other amount

Coll decided to retire from the partnership. By mutual agreement, the partnership assets were to be adjusted to their current fair value of $216,000 on June 30, 2006. It was agreed that the partnership would pay Coll $61,200 cash for Coll's partnership interest, including Coll's loan that was to be repaid in full. No goodwill was to be recognized. After Coll's retirement, the balance of Maduro's capital account is:A) $36,450

B) $39,000

C) $45,450

D) $46,200

E) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

29

Are per unit amounts disclosed in a limited partnership's:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

30

When Elsa Martin withdrew from Lewis, Martin, Noll & Ordway LLP on January 31, 2006, she was paid $80,000, although her capital account balance was only $60,000. The four partners shared net income and losses equally. The journal entry of the partnership to record Martin's withdrawal on January 31, 2006, preferably should include a debit of:

A) $6,667 to Lewis, Capital

B) $20,000 to Goodwill

C) $80,000 to Goodwill

D) $80,000 to Martin, Drawing

A) $6,667 to Lewis, Capital

B) $20,000 to Goodwill

C) $80,000 to Goodwill

D) $80,000 to Martin, Drawing

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

31

The owners' equity ledger accounts for a limited liability partnership are:

A) Capital accounts

B) Drawing accounts

C) Loans payable to partners

D) a and b only

E) a and c only

A) Capital accounts

B) Drawing accounts

C) Loans payable to partners

D) a and b only

E) a and c only

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

32

On September 1, 2005, Fox & George LLP admitted Lucille Hayes to a 20% interest in net assets for an investment of $50,000 cash. Prior to the admission of Hayes, Fox & George LLP had net assets of $100,000 and an income-sharing ratio of Fox-25%, George-75%. After the admission of Hayes, the partnership contract included the following provisions:

Salary of $40,000 a year to Hayes, to be recognized as partnership expense

Resultant net income in ratio Fox-20%, George-60%, Hayes-20%

During the fiscal year ended August 31, 2006, Fox, George & Hayes LLP had an income of $90,000 prior to recognition of salary to Hayes.

Prepare journal entries for Fox, George & Hayes LLP to record the admission of Hayes on September 1, 2005, and the division of income among the partners on August 31, 2006.

Salary of $40,000 a year to Hayes, to be recognized as partnership expense

Resultant net income in ratio Fox-20%, George-60%, Hayes-20%

During the fiscal year ended August 31, 2006, Fox, George & Hayes LLP had an income of $90,000 prior to recognition of salary to Hayes.

Prepare journal entries for Fox, George & Hayes LLP to record the admission of Hayes on September 1, 2005, and the division of income among the partners on August 31, 2006.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

33

Roe, Soh, & Tow Limited Liability Partnership was organized and began operations on February 1, 2005, with the following capital account balances: Roe, $50,000; Soh, $70,000; Tow, $80,000. The income-sharing arrangement provided for the following:

For the fiscal year ended January 31, 2006, Roe, Soh, & Tow Limited Liability Partnership had income of $180,000, before recognition of salaries expense, and the partners withdrew their authorized salaries in cash.

Prepare journal entries (omit explanations) for Roe, Soh, & Tow Limited Liability Partnership on January 31, 2006.

For the fiscal year ended January 31, 2006, Roe, Soh, & Tow Limited Liability Partnership had income of $180,000, before recognition of salaries expense, and the partners withdrew their authorized salaries in cash.Prepare journal entries (omit explanations) for Roe, Soh, & Tow Limited Liability Partnership on January 31, 2006.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

34

For the fiscal year ended May 31, 2006, Ace, Bay & Cap Limited Liability Partnership had an operating loss of $120,000 before recognition of partners' salaries expense. The partnership contract provided for the following:

Salaries of $20,000 to Ace, $30,000 to Bay, and $40,000 to Cap, to be recognized as expense by the partnership

Bonus of 20% of income after the bonus to Ace

Residual income or loss 20% to Ace, 50% to Bay, and 30% to Cap

Prepare journal entries (omit explanations) for Ace, Bay & Cap Limited Liability Partnership on May 31, 2006.

Salaries of $20,000 to Ace, $30,000 to Bay, and $40,000 to Cap, to be recognized as expense by the partnership

Bonus of 20% of income after the bonus to Ace

Residual income or loss 20% to Ace, 50% to Bay, and 30% to Cap

Prepare journal entries (omit explanations) for Ace, Bay & Cap Limited Liability Partnership on May 31, 2006.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

35

The partners of Rann & Sloe LLP shared net income and losses in a 3:2 ratio and had capital account balances of $87,000 and $48,000, respectively. Trey was admitted to the partnership with the investment of a single proprietorship having identifiable net assets with a current fair value of $47,250 and was given a one-third interest in the net income or losses and the net assets of the new partnership.

Prepare a journal entry to record the admission of Trey to Rann, Sloe & Trey LLP.

Prepare a journal entry to record the admission of Trey to Rann, Sloe & Trey LLP.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

36

The partners of Bentsen & Cole LLP had capital account balances of $45,000 and $25,000, respectively. They shared net income and losses in a 3:1 ratio.

Prepare journal entries to record the admission of Diaz to the limited liability partnership under the (1) bonus method, and (2) goodwill method for each of the following assumptions:

a. Diaz invested a single proprietorship with identifiable assets having a current fair value of $40,000 and liabilities having a current fair value of $10,000 for a 25% interest in the net assets of the partnership.

b. Diaz invested a single proprietorship with identifiable assets having a current fair value of $40,000 and liabilities having a current fair value of $10,000 for a

33 1/3% interest in the net assets of the partnership.

Prepare journal entries to record the admission of Diaz to the limited liability partnership under the (1) bonus method, and (2) goodwill method for each of the following assumptions:

a. Diaz invested a single proprietorship with identifiable assets having a current fair value of $40,000 and liabilities having a current fair value of $10,000 for a 25% interest in the net assets of the partnership.

b. Diaz invested a single proprietorship with identifiable assets having a current fair value of $40,000 and liabilities having a current fair value of $10,000 for a

33 1/3% interest in the net assets of the partnership.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

37

In 2005, the partners of Julio & Fong LLP shared net income and losses equally, but in 2006 the income-sharing ratio was changed to 60% for Julio and 40% for Fong. On December 31, 2005, inventories were understated by $12,000. On December 31, 2006, employees' salaries payable in the amount of $5,400 and short-term prepayments of $2,700 had not been recognized in the accounting records.

Prepare a correcting journal entry on December 31, 2006, assuming that the accounting records had been closed for 2006. Show supporting computations.

Prepare a correcting journal entry on December 31, 2006, assuming that the accounting records had been closed for 2006. Show supporting computations.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

38

The capital account balances for Ray & Randall LLP on May 31, 2006, were as follows:

Ray and Randall shared net income and losses in the ratio of 3:2, respectively. The partners agreed to admit Appleton to the partnership with a 35% interest in partnership capital and net income. Appleton invested $80,000 cash, and no goodwill was recognized.

Prepare a working paper to compute the capital account balance for each partner immediately after Appleton was admitted to Ray, Randall & Appleton LLP on May 31, 2003.

Ray and Randall shared net income and losses in the ratio of 3:2, respectively. The partners agreed to admit Appleton to the partnership with a 35% interest in partnership capital and net income. Appleton invested $80,000 cash, and no goodwill was recognized.Prepare a working paper to compute the capital account balance for each partner immediately after Appleton was admitted to Ray, Randall & Appleton LLP on May 31, 2003.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

39

The balance sheet of Elsa Laing, CPA (a single proprietorship) had total assets of $200,000, including unimpaired goodwill of $15,000 recognized when Laing had acquired the accounting practice of another sole practitioner, and total liabilities of $30,000. In Laing's negotiations with the partners of Burns & Damon LLP for the acquisition of her proprietorship by the limited liability partnership, she insists on a capital account balance of $190,000, pointing out her higher-than-typical earnings over the past five years. Partners Ralph Burns and Linda Damon maintain that the current fair value of Laing's proprietorship identifiable net assets is $155,000 (their carrying amount); they offer to admit Laing to Burns, Damon & Laing LLP for a capital account balance of $175,000.

Do you support the position of Elsa Laing or of Ralph Burns and Linda Damon? Explain.

Do you support the position of Elsa Laing or of Ralph Burns and Linda Damon? Explain.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 39 flashcards in this deck.