Deck 12: Risk/Return and Asset Pricing Models

Full screen (f)

Question

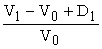

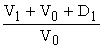

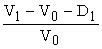

Which of the below is the equation for the return on a portfolio where V₀ = the portfolio market value at the beginning of the interval, V₁ = the portfolio market value at the end of the interval, and D₁ = the cash distributions to the investor during the interval?

A) Rp =

B) Rp =

C) Rp =

D) Rp = (V₁ -V₀ + D₁) × V₀

A) Rp =

B) Rp =

C) Rp =

D) Rp = (V₁ -V₀ + D₁) × V₀

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/56

Play

Full screen (f)

Deck 12: Risk/Return and Asset Pricing Models

1

Which of the below is the equation for the return on a portfolio where V₀ = the portfolio market value at the beginning of the interval, V₁ = the portfolio market value at the end of the interval, and D₁ = the cash distributions to the investor during the interval?

A) Rp =

B) Rp =

C) Rp =

D) Rp = (V₁ -V₀ + D₁) × V₀

A) Rp =

B) Rp =

C) Rp =

D) Rp = (V₁ -V₀ + D₁) × V₀

A

2

The Treasury bill rate is 4.50% and the return on the market is estimated to be 9.50%. If you form a portfolio with a beta of 1.2, what should be your rate of return according to the CAPM?

A) 9.00%

B) 9.50%

C) 9.75%

D) 10.50%

A) 9.00%

B) 9.50%

C) 9.75%

D) 10.50%

D

3

Consider an investor who holds a risky portfolio that has the same risk as the market portfolio. If the beta is one then the investor should expect to earn ________. Consider another investor who holds a riskless portfolio such as Treasury bills. If the beta is zero then the investor should earn ________.

A) the riskless rate of return; the market portfolio rate of return.

B) the risky return; the riskless rate of return.

C) the market portfolio rate of return; the riskless rate of return.

D) the market portfolio rate of return; the corporate bond rate of return.

A) the riskless rate of return; the market portfolio rate of return.

B) the risky return; the riskless rate of return.

C) the market portfolio rate of return; the riskless rate of return.

D) the market portfolio rate of return; the corporate bond rate of return.

C

4

A problem with a portfolio return computation is: ________.

A) the underlying assumption is that all cash payments and inflows are made and received at the beginning of the period

B) we have to rely on the formula that is able to adjust portfolio returns with the same time horizon.

C) if two investments have the same return, but one investment makes a cash payment early and the other late, the one with early payment will be overstated

D) we cannot rely on the formula to compare return on a one-month investment with that on a 10-year return portfolio.

A) the underlying assumption is that all cash payments and inflows are made and received at the beginning of the period

B) we have to rely on the formula that is able to adjust portfolio returns with the same time horizon.

C) if two investments have the same return, but one investment makes a cash payment early and the other late, the one with early payment will be overstated

D) we cannot rely on the formula to compare return on a one-month investment with that on a 10-year return portfolio.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

5

The two major standards of risk are: ________.

A) total risk and the relative index of systematic or nondiversifiable risk.

B) standard deviation and unsystematic risk.

C) total risk and the standard deviation.

D) beta and the relative index of systematic or nondiversifiable risk (beta).

A) total risk and the relative index of systematic or nondiversifiable risk.

B) standard deviation and unsystematic risk.

C) total risk and the standard deviation.

D) beta and the relative index of systematic or nondiversifiable risk (beta).

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

6

What is the return on a portfolio on a portfolio if the portfolio market value at the beginning of the interval is $1,350, the portfolio market value at the end of the interval is $1,185, and the cash distributions to the investor during the interval is $115.52?

A) 12.85%

B) 5.24%

C) -1.78%

D) -3.67%

A) 12.85%

B) 5.24%

C) -1.78%

D) -3.67%

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

7

Consider an investor who owns three assets: asset 1, asset 2, and asset 3 and invests equally in each of the three assets. If the beta of asset 1 is 1.2, the beta of asset 2 is 1.5 and the Beta of asset 3 is zero, then what is the beta of the investor's portfolio.

A) 0.75

B) 0.90

C) 1.10

D) 1.25

A) 0.75

B) 0.90

C) 1.10

D) 1.25

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

8

________ will not systematically affect the portfolio return, but it will reduce the variability (standard deviation) of return with this variability reduced when there is ________ among security returns.

A) Diversification; more variance

B) Differentiation; less correlation

C) Diversification; less correlation

D) Diversification; less variance

A) Diversification; more variance

B) Differentiation; less correlation

C) Diversification; less correlation

D) Diversification; less variance

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

9

In designing a portfolio, investors seek to maximize the expected return from their investment, given some level of risk they are willing to accept. Portfolios that satisfy this requirement are called ________ portfolios.

A) magnificent (or maximal)

B) sufficient (or minimal)

C) efficient (or optimal)

D) inefficient (or suboptimal)

A) magnificent (or maximal)

B) sufficient (or minimal)

C) efficient (or optimal)

D) inefficient (or suboptimal)

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the below statements is FALSE?

A) The systematic risk of a portfolio is simply the market value-weighted average of the systematic risk of the individual securities.

B) The beta (β) for a portfolio consisting of all stocks is 1.00.

C) The beta of a security or portfolio can be estimated using statistical analysis.

D) There will be no difference in the calculated beta depending on the length of time over which a return is calculated and the number of observations used

A) The systematic risk of a portfolio is simply the market value-weighted average of the systematic risk of the individual securities.

B) The beta (β) for a portfolio consisting of all stocks is 1.00.

C) The beta of a security or portfolio can be estimated using statistical analysis.

D) There will be no difference in the calculated beta depending on the length of time over which a return is calculated and the number of observations used

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

11

Consider an investor who owns two assets: the risky market portfolio where the investor puts two-thirds of her money and a riskless asset where the investor puts one-third of her money. What is the beta of her portfolio?

A) zero

B) 0.33

C) 0.50

D) 0.67

A) zero

B) 0.33

C) 0.50

D) 0.67

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

12

What is the return on a portfolio if the portfolio market value at the beginning of the interval is $1,250, the portfolio market value at the end of the interval is $1,385, and the cash distributions to the investor during the interval is $55.52?

A) 15.12%

B) 15.24%

C) 15.36%

D) 15.48%

A) 15.12%

B) 15.24%

C) 15.36%

D) 15.48%

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

13

Returns expected by investors logically should be related to ________ as opposed to total risk

A) unsystematic

B) systematic risk

C) diversifiable

D) the standard deviation

A) unsystematic

B) systematic risk

C) diversifiable

D) the standard deviation

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

14

The riskless rate is 5.00% and the return on the market is 10.00%. If you form a portfolio with a beta of 0.8, what should be your rate of return according to the CAPM?

A) 8.00%

B) 8.50%

C) 9.00%

D) 9.50%

A) 8.00%

B) 8.50%

C) 9.00%

D) 9.50%

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

15

We can distinguish between a security's ________, which can be washed away by mixing the security with other securities in a diversified portfolio, and its ________, which cannot be eliminated by diversification.

A) systematic risk; unsystematic risk

B) portfolio risk; systematic risk

C) unsystematic risk; T-Bill risk

D) unsystematic risk; systematic risk

A) systematic risk; unsystematic risk

B) portfolio risk; systematic risk

C) unsystematic risk; T-Bill risk

D) unsystematic risk; systematic risk

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the below statements is TRUE?

A) A particularly useful way to quantify the uncertainty about the portfolio return is to specify the probability associated with each of the possible future returns.

B) The expected return is simply the mean or average of possible outcomes without regard to each outcome's probability or weight.

C) One measure of risk is the extent to which possible future portfolio values are likely to diverge from the last value.

D) If risk is defined as the chance of achieving returns lower than expected, it would seem logical to measure risk by the dispersion of the possible returns above the expected value.

A) A particularly useful way to quantify the uncertainty about the portfolio return is to specify the probability associated with each of the possible future returns.

B) The expected return is simply the mean or average of possible outcomes without regard to each outcome's probability or weight.

C) One measure of risk is the extent to which possible future portfolio values are likely to diverge from the last value.

D) If risk is defined as the chance of achieving returns lower than expected, it would seem logical to measure risk by the dispersion of the possible returns above the expected value.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the below statements is FALSE?

A) The major difficulty in testing the CAPM is that the model is stated in terms of investors' expectations and not in terms of realized returns.

B) The expected risk premium should be equal to the quantity of risk (as measured by beta) and the market price of risk (as measured by the expected market risk premium).

C) Empirical tests find a significant positive relationship between realized returns and systematic risk as measured by beta but the estimate of the average market risk premium is usually less than that predicted by the CAPM.

D) Empirical tests find evidence of significant curvature in the risk/return relationship.

A) The major difficulty in testing the CAPM is that the model is stated in terms of investors' expectations and not in terms of realized returns.

B) The expected risk premium should be equal to the quantity of risk (as measured by beta) and the market price of risk (as measured by the expected market risk premium).

C) Empirical tests find a significant positive relationship between realized returns and systematic risk as measured by beta but the estimate of the average market risk premium is usually less than that predicted by the CAPM.

D) Empirical tests find evidence of significant curvature in the risk/return relationship.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

18

In the development of the CAPM, a number of assumptions are required if the model is to be established on a rigorous basis allowing a for a single derivation of the model. These assumptions involve investor behavior and conditions in the capital markets. Which of the below is not one of these underlying assumptions?

A) The market is made up of risk-averse investors who measure risk in terms of standard deviation of portfolio return

B) All investors have a common time horizon for investment decision making (for example, one month, one year, and so on).

C) Some investors are assumed to have different expectations about future security returns and risks.

D) Capital markets are perfect in the sense that all assets are completely divisible, there are no transactions costs or differential taxes, and borrowing and lending rates are equal to each other and the same for all investors.

A) The market is made up of risk-averse investors who measure risk in terms of standard deviation of portfolio return

B) All investors have a common time horizon for investment decision making (for example, one month, one year, and so on).

C) Some investors are assumed to have different expectations about future security returns and risks.

D) Capital markets are perfect in the sense that all assets are completely divisible, there are no transactions costs or differential taxes, and borrowing and lending rates are equal to each other and the same for all investors.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

19

A security's return in equal to its systematic return plus its unsystematic return where ________.

A) the security return, R, may be expressed as R = βRm + ε'.

B) the systematic return is proportional to the market return and it can be expressed as the symbol beta (or β) times the market return, Rm.

C) unsystematic return, which is independent of market returns, is usually represented by the symbol epsilon (ε').

D) All of these

A) the security return, R, may be expressed as R = βRm + ε'.

B) the systematic return is proportional to the market return and it can be expressed as the symbol beta (or β) times the market return, Rm.

C) unsystematic return, which is independent of market returns, is usually represented by the symbol epsilon (ε').

D) All of these

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

20

Empirically, a comparison of the distribution of historical returns for a large portfolio of randomly selected stocks (say, 50 stocks) with the distribution of historical returns for an individual stock in the portfolio has indicated a curious relationship in that it can be common to find ________.

A) that the standard deviation of return for the individual stocks in the portfolio is considerably smaller than that of the portfolio.

B) that the average return of an individual stock is less than the portfolio return.

C) that the return for all individual stocks in the portfolio is each considerably larger than that of the portfolio itself.

D) that the standard deviation of return for the portfolio is always zero.

A) that the standard deviation of return for the individual stocks in the portfolio is considerably smaller than that of the portfolio.

B) that the average return of an individual stock is less than the portfolio return.

C) that the return for all individual stocks in the portfolio is each considerably larger than that of the portfolio itself.

D) that the standard deviation of return for the portfolio is always zero.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

21

The relevant risk of any individual security is not total variability in returns but rather systematic variability, which is that portion of total variability that cannot be eliminated by combining it with other securities in a diversified portfolio.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

22

There have been two major attacks on standard portfolio theory. Which of the below is ONE of these?

A) One is the attack by the behavioral finance camp as to how consumers make decisions.

B) One is the attack on the nature of the return distribution based on what has been theoretically decreed for financial assets.

C) One is the attack on binomial distribution of returns assumed for financial assets.

D) One is the attack by the behavioral finance camp as to how investors make decisions.

A) One is the attack by the behavioral finance camp as to how consumers make decisions.

B) One is the attack on the nature of the return distribution based on what has been theoretically decreed for financial assets.

C) One is the attack on binomial distribution of returns assumed for financial assets.

D) One is the attack by the behavioral finance camp as to how investors make decisions.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

23

The CAPM can be extended to describe "extra-market" sources of risk referred to as factors, so as to create an extended model called a ________.

A) multifactor CAPM.

B) bifactor CAPM

C) "extra-market" CAPM.

D) extended CAPM.

A) multifactor CAPM.

B) bifactor CAPM

C) "extra-market" CAPM.

D) extended CAPM.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

24

The concept of heuristics means a rule-of-thumb strategy or good guide to follow in order to shorten the time it takes to make a decision. Psychology literature tells us that heuristics can lead to systematic biases in decision making, what psychologists refer to as cognitive biases. In the context of finance, these biases lead to errors in making ________.

A) accounting decisions.

B) investment decisions.

C) heuristic decisions.

D) psychological decisions.

A) accounting decisions.

B) investment decisions.

C) heuristic decisions.

D) psychological decisions.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

25

Empirical studies suggest four possible economic factors for the APT. Which of the below include these economic factors?

A) 1. Unanticipated changes in industrial production.

2. Unanticipated changes in the spread between the yield on low-grade and high-grade bonds.

3. Unanticipated changes in interest rates and the shape of the yield curve.

4. Unanticipated changes in inflation. It is interesting to note that one study expands that list to five factors, some similar to the previous group and some new.

B) 1. Unanticipated changes in industrial production.

2. Unanticipated changes in the spread between the yield on low-grade and high-grade bonds.

3. Unanticipated changes in interest rates and the shape of the yield curve.

4. Unanticipated changes in inflation. It is interesting to note that one study expands that list to five factors, some similar to the previous group and some new.

C) 1. The business cycle, as measured by the Index of Industrial Production.

2. Interest rates, as given by the yields on long-term government bonds.

3. Unanticipated changes in industrial production.

4. Short-term inflation, as measured by month-to-month changes in the Consumer Price Index.

D) 1 . The business cycle, as measured by the Index of Industrial Production.

2. Interest rates, as given by the yields on long-term government bonds.

3. Unanticipated changes in industrial production.

4. Unanticipated changes in industrial production.

A) 1. Unanticipated changes in industrial production.

2. Unanticipated changes in the spread between the yield on low-grade and high-grade bonds.

3. Unanticipated changes in interest rates and the shape of the yield curve.

4. Unanticipated changes in inflation. It is interesting to note that one study expands that list to five factors, some similar to the previous group and some new.

B) 1. Unanticipated changes in industrial production.

2. Unanticipated changes in the spread between the yield on low-grade and high-grade bonds.

3. Unanticipated changes in interest rates and the shape of the yield curve.

4. Unanticipated changes in inflation. It is interesting to note that one study expands that list to five factors, some similar to the previous group and some new.

C) 1. The business cycle, as measured by the Index of Industrial Production.

2. Interest rates, as given by the yields on long-term government bonds.

3. Unanticipated changes in industrial production.

4. Short-term inflation, as measured by month-to-month changes in the Consumer Price Index.

D) 1 . The business cycle, as measured by the Index of Industrial Production.

2. Interest rates, as given by the yields on long-term government bonds.

3. Unanticipated changes in industrial production.

4. Unanticipated changes in industrial production.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the below statements is TRUE?

A) The APT states that the return on a security is dependent on its market sensitivity index and an unsystematic return.

B) The CAPM states that the return on a security is linearly related to H factors.

C) The APT asserts that an investor is compensated for accepting unsystematic risk

D) The APT states that investors want to be compensated for all the factors that systematically affect the return of a security.

A) The APT states that the return on a security is dependent on its market sensitivity index and an unsystematic return.

B) The CAPM states that the return on a security is linearly related to H factors.

C) The APT asserts that an investor is compensated for accepting unsystematic risk

D) The APT states that investors want to be compensated for all the factors that systematically affect the return of a security.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the below reasons is NOT a reason an APT advocate would offer in support of the APT over either the CAPM or the multifactor CAPM?

A) The APT makes less restrictive assumptions about investor preferences toward risk and return.

B) The APT assumes that the investors trade off between risk and return depends solely on the basis of the expected returns and standard deviations of prospective investments.

C) The APT does not rely on identifying the true market index, the theory is potentially testable.

D) The APT makes no assumptions are made about the distribution of security returns.

A) The APT makes less restrictive assumptions about investor preferences toward risk and return.

B) The APT assumes that the investors trade off between risk and return depends solely on the basis of the expected returns and standard deviations of prospective investments.

C) The APT does not rely on identifying the true market index, the theory is potentially testable.

D) The APT makes no assumptions are made about the distribution of security returns.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

28

The index of the sensitivity of a security's returns to movement in the market is the security's standard deviation, which can be estimated with regression techniques from historical data.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

29

In the multifactor CAPM, besides investing in the market portfolio, investors will also allocate funds to something equivalent to a mutual fund that ________.

A) confronts heads on a particular extra-market risk

B) invests in particular extra-market risk

C) hedges a particular extra-market risk

D) exposes a particular extra-market risk

A) confronts heads on a particular extra-market risk

B) invests in particular extra-market risk

C) hedges a particular extra-market risk

D) exposes a particular extra-market risk

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

30

Themes of behavioral finance asset include:

1: Investors err in making investment decisions because they rely on ________.

2: Investors are influenced by form as well substance in making ________.

3: Prices in the financial market are affected ________ and decision frames.

A) errors; investment decisions; by rules of thumb

B) rules of thumb; accounting decisions; by errors

C) errors; accounting decisions; by rules of thumb

D) rules of thumb; investment decisions; by errors

1: Investors err in making investment decisions because they rely on ________.

2: Investors are influenced by form as well substance in making ________.

3: Prices in the financial market are affected ________ and decision frames.

A) errors; investment decisions; by rules of thumb

B) rules of thumb; accounting decisions; by errors

C) errors; accounting decisions; by rules of thumb

D) rules of thumb; investment decisions; by errors

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

31

________ postulates that a security's expected return is influenced by a variety of factors, as opposed to just the single market index.

A) The arbitrage pricing theory model

B) The CAPM

C) The multifactor CAPM

D) The capital asset pricing model

A) The arbitrage pricing theory model

B) The CAPM

C) The multifactor CAPM

D) The capital asset pricing model

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

32

An important implication of asset returns following a stable Paretian distribution is that the standard deviation is ________.

A) normal.

B) infinite.

C) brief.

D) stable.

A) normal.

B) infinite.

C) brief.

D) stable.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

33

Objections to the fully rational approach are that the ________.

A) calculations needed to implement this approach are somewhat difficult to do.

B) "alleged psychology biases are arbitrary."

C) experiments performed by research that find alleged psychological biases are arbitrary.

D) empirical evidence in the finance literature does not support rational behavior by investors.

A) calculations needed to implement this approach are somewhat difficult to do.

B) "alleged psychology biases are arbitrary."

C) experiments performed by research that find alleged psychological biases are arbitrary.

D) empirical evidence in the finance literature does not support rational behavior by investors.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the below statements is TRUE?

A) In modeling the stock market, the interactions of borrowers are modeled.

B) The computer simulations of mathematical models have been found to generate thin tails and other statistical characteristics that have been observed in real-world financial markets.

C) Support for return distributions not being well characterized by a normal distribution comes from the collaborative efforts of economists and physicists who have developed mathematical models of the stock market.

D) Mathematical models are by their nature accurate replications of real-world financial markets providing sufficient structure to analyze return distributions.

A) In modeling the stock market, the interactions of borrowers are modeled.

B) The computer simulations of mathematical models have been found to generate thin tails and other statistical characteristics that have been observed in real-world financial markets.

C) Support for return distributions not being well characterized by a normal distribution comes from the collaborative efforts of economists and physicists who have developed mathematical models of the stock market.

D) Mathematical models are by their nature accurate replications of real-world financial markets providing sufficient structure to analyze return distributions.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

35

Stock returns exhibit ________.

A) a normal distribution.

B) symmetry in probability distributions and are not skewed.

C) fat tails or heavy tails where the "tails" of the distribution are where the extreme values occur.

D) periods when there are changes that are not much higher than the normal distribution predicts.

A) a normal distribution.

B) symmetry in probability distributions and are not skewed.

C) fat tails or heavy tails where the "tails" of the distribution are where the extreme values occur.

D) periods when there are changes that are not much higher than the normal distribution predicts.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

36

Risk aversion means that investors want to minimize risk for any given level of expected return, or want to maximize return, for any given level of risk.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

37

The multifactor CAPM approach entails that a security's return has ________.

A) an alpha like sensitivity to each factor.

B) a riskless performance for each factor.

C) a standard deviation type performance for each factor.

D) a beta like sensitivity to each factor.

A) an alpha like sensitivity to each factor.

B) a riskless performance for each factor.

C) a standard deviation type performance for each factor.

D) a beta like sensitivity to each factor.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

38

Based on numerous experiments, psychologists demonstrated that the actions of decision makers are inconsistent with the assumptions made by ________.

A) sociologists.

B) psychologists.

C) physicists.

D) economists.

A) sociologists.

B) psychologists.

C) physicists.

D) economists.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

39

The market model is the hypothesis that a security's return may be attributed to two forces, the returns on securities in general, and events related to the market itself.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

40

The ________ is a special case of the ________.

A) APT; CAPM

B) CAPM; APT

C) multifactor CAPM; CAPM

D) multifactor CAPM; APT

A) APT; CAPM

B) CAPM; APT

C) multifactor CAPM; CAPM

D) multifactor CAPM; APT

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

41

An repelling feature of the APT model is that it makes few assumptions about investors and the structure of the market.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

42

Describe two of the three major results of the empirical tests conducted on relationship between return and systematic risk.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

43

A major strength of the CAPM is that it is basically testable because the true market portfolio is an attainable portfolio diversified across all risky assets in the world.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

44

The multifactor CAPM posits that extra-market factors influence expected returns on securities or portfolios.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

45

The use of variance of returns in standard portfolio theory depends on whether the return distribution is symmetric with fat-tails.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

46

The capital asset pricing model (or CAPM) hypothesizes that assets with the same level of systematic risk should experience the same level of returns.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

47

Supporters of the APT model argue that it has several major advantages over the CAPM or the multifactor CAPM. Describe two of these advantages.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

48

Explain the concept of framing.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

49

Explain how diversification can help investors realize their investment goal of maximizing return while minimizing risk. In your answer give an estimate of how many stocks are needed to achieve your investment goal.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

50

The multifactor CAPM says that investors want to be compensated only for market risk.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

51

Some reservations about the CAPM are inevitable because it makes many assumptions about investors' behavior and the structure of the market where assets are traded.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

52

The level of returns expected from any asset (which may be an individual security or a portfolio of securities) is an exponential function of the risk-free rate, the asset's beta, and the returns expected on the market portfolio of risky assets.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

53

Describe the multifactor CAPM and how it extends the CAPM.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

54

The first behavioral finance theme involves the concept of heuristics. This term means a rule-of-thumb strategy or good guide to follow in order to shorten the time it takes to make a decision.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

55

The arbitrage pricing theory (or APT) model postulates that a security's return is a function of several factors and the security's sensitivity to changes in each of them.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

56

If a security's market price were to deviate from the level justified by the APT factors and the security's price sensitivity to them, investors would engage in arbitrage and drive the market price to an appropriate level.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 56 flashcards in this deck.