Deck 7: Perfect Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

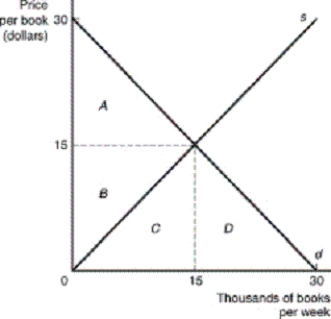

The following diagram represents the market for paperback books.Which area represents producer surplus?

A) A.

B) B.

C) C.

D) D.

E) None of the above.

A) A.

B) B.

C) C.

D) D.

E) None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

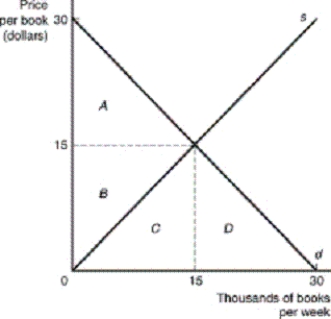

The following diagram represents the market for paperback books.In the market for paperback books,producer surplus is:

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

Question

Question

Question

Question

Question

Question

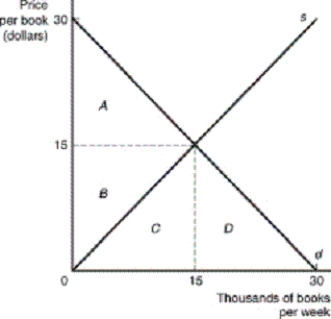

The following diagram represents the market for paperback books.In the market for paperback books,total surplus is:

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/39

Play

Full screen (f)

Deck 7: Perfect Competition

1

If price is above the average variable cost but below the average total cost of a representative firm in a competitive industry:

A) there will be entry to the industry over time.

B) there will be exit from the industry over time.

C) the firms in the industry are just earning a normal rate of return.

D) the firms in the industry are earning a supranormal rate of return.

E) the industry is in long-run equilibrium.

A) there will be entry to the industry over time.

B) there will be exit from the industry over time.

C) the firms in the industry are just earning a normal rate of return.

D) the firms in the industry are earning a supranormal rate of return.

E) the industry is in long-run equilibrium.

B

2

In the model of perfect competition,there:

A) are many firms producing differentiated products.

B) are a few firms producing undifferentiated products.

C) are a few firms producing differentiated products.

D) are many firms producing undifferentiated products.

E) is one firm producing a highly differentiated product.

A) are many firms producing differentiated products.

B) are a few firms producing undifferentiated products.

C) are a few firms producing differentiated products.

D) are many firms producing undifferentiated products.

E) is one firm producing a highly differentiated product.

D

3

If the perfectly competitive market demand for tanning beds shifts from QD,91 = 1,230 - 5P to QD,92 = 740 - 5P and the market supply is given by QS = -100 + 2P,then the change in equilibrium quantity will be:

A) 140 units.

B) 280 units.

C) -98 units.

D) -140 units.

E) -150 units.

A) 140 units.

B) 280 units.

C) -98 units.

D) -140 units.

E) -150 units.

D

4

If a representative firm with total cost given by TC = 20 + 20q + 5q2 operates in a competitive industry where the short-run market demand and supply curves are given by QD = 1,400 - 40P and QS = -400 + 20P,its short-run profit-maximizing level of output is:

A) 0 units.

B) 1 unit.

C) 2 units.

D) 4 units.

E) 6 units.

A) 0 units.

B) 1 unit.

C) 2 units.

D) 4 units.

E) 6 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

5

If labor produces output according to Q = 8L1/2,labor costs $10,and output sells for $100,then the optimal level of L is:

A) 8.

B) 16.

C) 1,600.

D) 2.

E) 10.

A) 8.

B) 16.

C) 1,600.

D) 2.

E) 10.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

6

Camel Records produces records according to Q = 4L - 0.15L2.If labor costs $5 and records sell for $2,the optimal quantity of labor is:

A) 0.

B) 2.

C) 10.

D) 5.

E) 17.

A) 0.

B) 2.

C) 10.

D) 5.

E) 17.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

7

In the model of perfect competition,firms maximize profits by producing where:

A) the difference between marginal revenue and marginal cost is maximized.

B) marginal revenue equals price.

C) the difference between price and marginal cost is maximized.

D) price equals marginal cost.

E) the difference between price and marginal revenue is maximized.

A) the difference between marginal revenue and marginal cost is maximized.

B) marginal revenue equals price.

C) the difference between price and marginal cost is maximized.

D) price equals marginal cost.

E) the difference between price and marginal revenue is maximized.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

8

If a representative firm with total cost given by TC = 20 + 20q + 5q2 operates in a competitive industry where the short-run market demand and supply curves are given by QD = 1,400 - 40P and QS = -400 + 20P,the number of firms operating in the short run will be:

A) 100.

B) 140.

C) 200.

D) 280.

E) 240.

A) 100.

B) 140.

C) 200.

D) 280.

E) 240.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

9

In the model of perfect competition,firms produce a:

A) standardized product with considerable control over price.

B) differentiated product with considerable control over price.

C) standardized product with no control over price.

D) differentiated product with no control over price.

E) standardized or differentiated product with some control over price.

A) standardized product with considerable control over price.

B) differentiated product with considerable control over price.

C) standardized product with no control over price.

D) differentiated product with no control over price.

E) standardized or differentiated product with some control over price.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

10

The following diagram represents the market for paperback books.Which area represents producer surplus?

A) A.

B) B.

C) C.

D) D.

E) None of the above.

A) A.

B) B.

C) C.

D) D.

E) None of the above.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

11

A representative firm with short-run total cost given by TC = 50 + 2q + 2q2 operates in a competitive industry where the short-run market demand and supply curves are given by QD = 1,410 - 40P and QS = -390 + 20P.Its short-run profit-maximizing level of output is:

A) 0 units.

B) 1 unit.

C) 2 units.

D) 5 units.

E) 7 units.

A) 0 units.

B) 1 unit.

C) 2 units.

D) 5 units.

E) 7 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

12

If the perfectly competitive market supply of pork bellies shifts from QS,93 = 250 + 50P to QS,94 = 400 + 40P,and the market demand is given by QD = +10,000 - 200P,then the change in equilibrium price will be:

A) $2.

B) $1.

C) $0.

D) -$1.

E) -$2.

A) $2.

B) $1.

C) $0.

D) -$1.

E) -$2.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

13

If the perfectly competitive market demand for gym shoes is given by QD = 100 - P and the market supply is given by QS = 10 + 2P,then the equilibrium price and quantity will be:

A) P = 50 and Q = 50.

B) P = 40 and Q = 90.

C) P = 40 and Q = 60.

D) P = 30 and Q = 70.

E) P = 25 and Q = 75.

A) P = 50 and Q = 50.

B) P = 40 and Q = 90.

C) P = 40 and Q = 60.

D) P = 30 and Q = 70.

E) P = 25 and Q = 75.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

14

Meteor Tie Company produces ties from fabric according to Q = 10 + 4F - (1/3)F3.If fabric is free and ties sell for $20,what is Meteor's optimal usage of fabric?

A) 0.

B) 2.

C) 4.

D) 6.

E) 8.

A) 0.

B) 2.

C) 4.

D) 6.

E) 8.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

15

If the perfectly competitive market demand for cholesterol-free cookies shifts from QD,93 = 1,150 - 5P to QD,94 = 1,640 - 5P,and the market supply is given by QS = -100 + 2P,then the change in equilibrium price will be:

A) $70.

B) $80.

C) $90.

D) $100.

E) $110.

A) $70.

B) $80.

C) $90.

D) $100.

E) $110.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

16

Paul's Pizza Parlor bakes pizza pies according to Q = 3L - 0.3L2.If labor costs $6 and pizza sells for $10,the optimal amount of labor is:

A) 6.

B) 5.

C) 4.

D) 3.

E) 2.

A) 6.

B) 5.

C) 4.

D) 3.

E) 2.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

17

Toy Productions makes toy trucks from steel according to Q = 50 + 100S - 0.5S2.If steel costs $49 and toy trucks sell for $7,the optimal level of steel usage is:

A) 50.

B) 43.

C) 100.

D) 93.

E) 133.

A) 50.

B) 43.

C) 100.

D) 93.

E) 133.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

18

If the perfectly competitive market supply of pork bellies shifts from QS,93 = 250 + 50P to QS,94 = 400 + 40P,and the market demand is given by QD = +10,000 - 200P,then the change in equilibrium quantity will be:

A) 200 units.

B) 100 units.

C) 0 units.

D) -100 units.

E) -200 units.

A) 200 units.

B) 100 units.

C) 0 units.

D) -100 units.

E) -200 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

19

In the model of perfect competition,there are:

A) high barriers to entry and no nonprice competition.

B) low barriers to entry and some advertising and product differentiation.

C) very high barriers to entry and some advertising and product differentiation.

D) high barriers to entry and some advertising and product differentiation.

E) low barriers to entry and no nonprice competition.

A) high barriers to entry and no nonprice competition.

B) low barriers to entry and some advertising and product differentiation.

C) very high barriers to entry and some advertising and product differentiation.

D) high barriers to entry and some advertising and product differentiation.

E) low barriers to entry and no nonprice competition.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

20

In a competitive market the equilibrium price is determined:

A) at the intersection of the firm's demand and the market supply curves.

B) at the intersection of the market demand and supply curves.

C) at the intersection of the firm's demand and marginal cost curves.

D) so as to cover the costs of the potential firms.

E) so as to cover the costs of the firms currently in the industry.

A) at the intersection of the firm's demand and the market supply curves.

B) at the intersection of the market demand and supply curves.

C) at the intersection of the firm's demand and marginal cost curves.

D) so as to cover the costs of the potential firms.

E) so as to cover the costs of the firms currently in the industry.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

21

If a representative firm with long-run total cost given by TC = 2,000 + 20q + 5q2 operates in a competitive industry where the market demand is given by QD = 10,000 - 40P,the long-run equilibrium output of the individual firm's will be:

A) 10 units.

B) 20 units.

C) 30 units.

D) 35 units.

E) 40 units.

A) 10 units.

B) 20 units.

C) 30 units.

D) 35 units.

E) 40 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

22

If a representative firm with long-run total cost given by TC = 2,000 + 20q + 5q2 operates in a competitive industry where the market demand is given by QD = 10,000 - 40P,in the long-run equilibrium there will be:

A) 60 firms.

B) 98 firms.

C) 106 firms.

D) 110 firms.

E) 120 firms.

A) 60 firms.

B) 98 firms.

C) 106 firms.

D) 110 firms.

E) 120 firms.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

23

Producer surplus is defined as:

A) the difference between the price the consumer actually pays for a product and the consumer's reservation price.

B) the profit that the firm earns on each unit of a product sold.

C) the profit that the firm earns after taxes.

D) the difference between the price received by the producer and the producer's reservation price.

E) the difference between the price paid by the consumer and the price received by the consumer.

A) the difference between the price the consumer actually pays for a product and the consumer's reservation price.

B) the profit that the firm earns on each unit of a product sold.

C) the profit that the firm earns after taxes.

D) the difference between the price received by the producer and the producer's reservation price.

E) the difference between the price paid by the consumer and the price received by the consumer.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

24

If the demand increases for the product of an increasing-cost industry:

A) short-run price goes up, but long-run price falls.

B) long-run output goes up, but long-run price may go up or down.

C) short-run output goes up, but long-run output may go up or down.

D) long-run output goes up, but short-run price remains constant.

E) short-run price goes up, and long-run price goes up.

A) short-run price goes up, but long-run price falls.

B) long-run output goes up, but long-run price may go up or down.

C) short-run output goes up, but long-run output may go up or down.

D) long-run output goes up, but short-run price remains constant.

E) short-run price goes up, and long-run price goes up.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

25

If a representative firm with long-run total cost given by TC = 50 + 2q + 2q2 operates in a competitive industry where the market demand is given by QD = 1,410 - 40P,in the long-run equilibrium there will be:

A) 60 firms.

B) 98 firms.

C) 106 firms.

D) 110 firms.

E) 120 firms.

A) 60 firms.

B) 98 firms.

C) 106 firms.

D) 110 firms.

E) 120 firms.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

26

A constant-cost industry is one in which:

A) input prices do not change over time.

B) technology does not change over time.

C) input prices and technology do not change as firms enter or exit the industry.

D) input prices and technology do not change over time.

E) firms have reached the maturity phase of the industry's life cycle.

A) input prices do not change over time.

B) technology does not change over time.

C) input prices and technology do not change as firms enter or exit the industry.

D) input prices and technology do not change over time.

E) firms have reached the maturity phase of the industry's life cycle.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

27

The following diagram represents the market for paperback books.In the market for paperback books,producer surplus is:

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

28

If a representative firm with long-run total cost given by TC = 50 + 2q + 2q2 operates in a competitive industry where the market demand is given by QD = 1,410 - 40P,the long-run equilibrium output of the industry will be:

A) 490 units.

B) 530 units.

C) 570 units.

D) 610 units.

E) 650 units.

A) 490 units.

B) 530 units.

C) 570 units.

D) 610 units.

E) 650 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

29

The long-run supply curve for a product is horizontal with ATC = 200.Market demand is defined as P = 1,000 - 5Q.The market is competitive and is in long-run equilibrium with 40 firms in the industry.If a $50 tax is imposed on sellers,how many firms will be in the industry at the new long-run equilibrium?

A) 44.

B) 37.

C) 32.

D) 29.

E) 28.

A) 44.

B) 37.

C) 32.

D) 29.

E) 28.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

30

A representative firm with long-run total cost given by TC = 20 + 20q + 5q2 operates in a competitive industry where the short-run market demand and supply curves are given by QD = 1,400 - 40P and QS = -400 + 20P.If it continues to operate in the long run,its profit-maximizing level of output is:

A) 1 unit.

B) 2 units.

C) 4 units.

D) 5 units.

E) 6 units.

A) 1 unit.

B) 2 units.

C) 4 units.

D) 5 units.

E) 6 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

31

If the demand increases for the product of a constant-cost industry:

A) long-run output goes up, but long-run price may go up or down.

B) short-run output goes up, but long-run output may go up or down.

C) short-run price goes up, but long-run price remains constant.

D) long-run output goes up, but short-run price remains constant.

E) long-run price goes up, but short-run price may go up or down.

A) long-run output goes up, but long-run price may go up or down.

B) short-run output goes up, but long-run output may go up or down.

C) short-run price goes up, but long-run price remains constant.

D) long-run output goes up, but short-run price remains constant.

E) long-run price goes up, but short-run price may go up or down.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

32

The long-run supply curve for a product is horizontal with ATC = 200.Market demand is defined as P = 1,000 - 4Q.The market is competitive and is in long-run equilibrium with 50 firms in the industry.If demand increases to P = 1,240 - 4Q,how many firms will be in the industry at the new long-run equilibrium?

A) 45.

B) 55.

C) 65.

D) 75.

E) 85.

A) 45.

B) 55.

C) 65.

D) 75.

E) 85.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

33

The following diagram represents the market for paperback books.In the market for paperback books,total surplus is:

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

A) $15.00.

B) $30.00.

C) $112.50.

D) $225.00.

E) None of the above.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

34

A representative firm with long-run total cost given by TC = 2,000 + 20q + 5q2 operates in a competitive industry where the market demand is given by QD = 10,000 - 40P.The long-run equilibrium output of the industry will be:

A) 1,200 units.

B) 1,800 units.

C) 2,200 units.

D) 2,600 units.

E) 3,200 units.

A) 1,200 units.

B) 1,800 units.

C) 2,200 units.

D) 2,600 units.

E) 3,200 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

35

The long-run supply curve for a product is horizontal with ATC = 400.Market demand is defined as P = 1,000 - 4Q.The market is competitive and is in long-run equilibrium with 50 firms in the industry.If demand increases to P = 1,240 - 4Q,how many firms will be in the industry at the new long-run equilibrium?

A) 30.

B) 40.

C) 50.

D) 60.

E) 70.

A) 30.

B) 40.

C) 50.

D) 60.

E) 70.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

36

If a representative firm with long-run total cost given by TC = 50 + 2q + 2q2 operates in a competitive industry where the short-run market demand and supply curves are given by QD = 1,410 - 40P and QS = -390 + 20P,its long-run profit-maximizing level of output is:

A) 0 units.

B) 1 unit.

C) 2 units.

D) 5 units.

E) 7 units.

A) 0 units.

B) 1 unit.

C) 2 units.

D) 5 units.

E) 7 units.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

37

Total surplus in a market is a measure of:

A) social welfare created by the market.

B) profits that accrue to the owners of firms in a particular market.

C) the rebates that consumers receive when they purchase certain goods or services.

D) excess inventory that remains at the end of a season.

E) planned inventory that a firm carries from one year to the next.

A) social welfare created by the market.

B) profits that accrue to the owners of firms in a particular market.

C) the rebates that consumers receive when they purchase certain goods or services.

D) excess inventory that remains at the end of a season.

E) planned inventory that a firm carries from one year to the next.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

38

A decreasing-cost industry is one in which:

A) input prices fall over time.

B) technology deteriorates over time.

C) input prices and technology do not change over time.

D) firms are in the growth phase of the industry's life cycle.

E) input prices fall or technology improves as firms enter the industry.

A) input prices fall over time.

B) technology deteriorates over time.

C) input prices and technology do not change over time.

D) firms are in the growth phase of the industry's life cycle.

E) input prices fall or technology improves as firms enter the industry.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

39

If the demand increases for the product of a decreasing-cost industry:

A) short-run price goes up, but long-run price falls.

B) long-run output goes up, but long-run price may go up or down.

C) short-run output goes up, but long-run output may go up or down.

D) long-run output goes up, but short-run price remains constant.

E) long-run price goes up, but short-run price may go up or down.

A) short-run price goes up, but long-run price falls.

B) long-run output goes up, but long-run price may go up or down.

C) short-run output goes up, but long-run output may go up or down.

D) long-run output goes up, but short-run price remains constant.

E) long-run price goes up, but short-run price may go up or down.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 39 flashcards in this deck.