Deck 13: Risk and the Pricing of Options

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

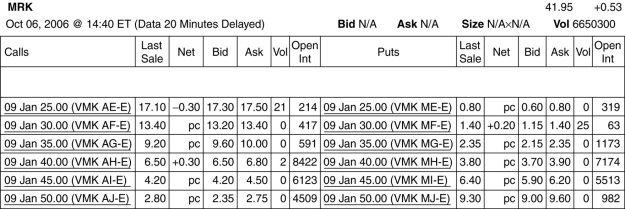

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to buy one options contract with an exercise price closest to being at-the-money and that expires January 2009.The current price that you would have to pay for such a contract is:

A) $680

B) $380

C) $650

D) $420

E) $450

Consider the following information on options from the CBOE for Merck:

Assume you want to buy one options contract with an exercise price closest to being at-the-money and that expires January 2009.The current price that you would have to pay for such a contract is:

A) $680

B) $380

C) $650

D) $420

E) $450

Question

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2009 put option that is closest to being at-the-money is:

A) 7174

B) 982

C) 319

D) 8422

E) 5513

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2009 put option that is closest to being at-the-money is:

A) 7174

B) 982

C) 319

D) 8422

E) 5513

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are in-the-money?

A) 2

B) 4

C) 1

D) 3

E) 0

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are in-the-money?

A) 2

B) 4

C) 1

D) 3

E) 0

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $1750

B) $2000

C) $3500

D) $3900

E) $4400

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $1750

B) $2000

C) $3500

D) $3900

E) $4400

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the December 2010 put options are in-the-money?

A) 1

B) 2

C) 3

D) 4

E) 5

Consider the following information on options from the CBOE for Merck:

How many of the December 2010 put options are in-the-money?

A) 1

B) 2

C) 3

D) 4

E) 5

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $4500

B) $2600

C) $3900

D) $4000

E) $3500

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $4500

B) $2600

C) $3900

D) $4000

E) $3500

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to buy five call option contracts with an exercise price closest to being at-the-money and that expires December 2010.The current price that you would have to pay for such a contract is:

A) $550

B) $110

C) $475

D) $300

E) $525

Consider the following information on options from the CBOE for Merck:

Assume you want to buy five call option contracts with an exercise price closest to being at-the-money and that expires December 2010.The current price that you would have to pay for such a contract is:

A) $550

B) $110

C) $475

D) $300

E) $525

Question

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2011 call option that is closest to being at-the-money is:

A) 1436

B) 2245

C) 872

D) 523

E) 117

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2011 call option that is closest to being at-the-money is:

A) 1436

B) 2245

C) 872

D) 523

E) 117

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Question

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to buy 10 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would have to pay for such a contract is:

A) $1750

B) $2000

C) $1950

D) $2200

E) $2550

Consider the following information on options from the CBOE for Merck:

Assume you want to buy 10 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would have to pay for such a contract is:

A) $1750

B) $2000

C) $1950

D) $2200

E) $2550

Question

Question

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are in-the-money?

A) 1

B) 3

C) 2

D) 4

E) 0

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are in-the-money?

A) 1

B) 3

C) 2

D) 4

E) 0

Question

Question

Question

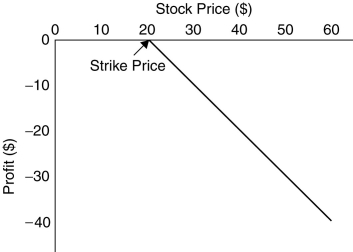

Use the figure for the question(s) below.

This graph depicts the payoffs of a

A) short position in a put option at expiration.

B) short position in a call option at expiration.

C) long position in a put option at expiration.

D) long position in a call option at expiration.

E) long position in a call option before expiration.

This graph depicts the payoffs of a

A) short position in a put option at expiration.

B) short position in a call option at expiration.

C) long position in a put option at expiration.

D) long position in a call option at expiration.

E) long position in a call option before expiration.

Question

Question

Question

Question

Use the figure for the question(s) below.

You pay $3.25 for a call option on Luther Industries that expires in three months with a strike price of $40.00.Three months later,at expiration,Luther Industries is trading at $41.00 per share.Your profit per share on this transaction is closest to:

A) -$1.00

B) $1.00

C) -$2.25

D) $2.25

E) $0

You pay $3.25 for a call option on Luther Industries that expires in three months with a strike price of $40.00.Three months later,at expiration,Luther Industries is trading at $41.00 per share.Your profit per share on this transaction is closest to:

A) -$1.00

B) $1.00

C) -$2.25

D) $2.25

E) $0

Question

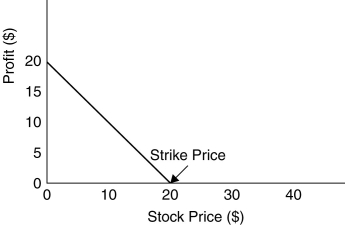

Use the figure for the question(s) below.

This graph depicts the payoffs of a

A) a long position in a put option at expiration.

B) short position in a call option at expiration.

C) a short position in a put option at expiration.

D) a long position in a call option at expiration.

E) a long position in a call option before expiration.

This graph depicts the payoffs of a

A) a long position in a put option at expiration.

B) short position in a call option at expiration.

C) a short position in a put option at expiration.

D) a long position in a call option at expiration.

E) a long position in a call option before expiration.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the figure for the question(s) below.

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $60 in three months,what will you owe for each share in the contract?

A) $0

B) $60

C) $50

D) $10

E) $40

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $60 in three months,what will you owe for each share in the contract?

A) $0

B) $60

C) $50

D) $10

E) $40

Question

Question

Question

Question

Question

Use the figure for the question(s) below.

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $45 in three months,what will you owe for each share in the contract?

A) $0

B) $50

C) $60

D) $10

E) $40

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $45 in three months,what will you owe for each share in the contract?

A) $0

B) $50

C) $60

D) $10

E) $40

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the figure for the question(s) below.

What is the short position of an options contract?

What is the short position of an options contract?

Question

Question

Use the figure for the question(s) below.

What is the long position of an options contract?

What is the long position of an options contract?

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/112

Play

Full screen (f)

Deck 13: Risk and the Pricing of Options

1

The holder of a put option has

A) the obligation to sell a security for a given price.

B) the right to buy a security for a given price.

C) the right to sell a security for a given price.

D) the obligation to buy a security for a given price.

E) the short position in the contract.

A) the obligation to sell a security for a given price.

B) the right to buy a security for a given price.

C) the right to sell a security for a given price.

D) the obligation to buy a security for a given price.

E) the short position in the contract.

the right to sell a security for a given price.

2

When the exercise price of an option is equal to the current price of the stock,the option is said to be

A) at-the-money.

B) in-the-money.

C) out-of-the-money.

D) trading at par.

E) trading below par.

A) at-the-money.

B) in-the-money.

C) out-of-the-money.

D) trading at par.

E) trading below par.

at-the-money.

3

When the exercise price of a call option is lower than the current price of the stock,the option is said to be

A) at-the-money.

B) in-the-money.

C) out-of-the-money.

D) trading at par.

E) trading below par.

A) at-the-money.

B) in-the-money.

C) out-of-the-money.

D) trading at par.

E) trading below par.

in-the-money.

4

A put option gives the owner the right to ________ an asset at a fixed price at some future date.

A) sell

B) buy

C) hold

D) obtain

E) purchase

A) sell

B) buy

C) hold

D) obtain

E) purchase

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

5

________ options allow the holder to exercise the option only on the expiration date.

A) Canadian

B) American

C) European

D) Brazilian

E) Chinese

A) Canadian

B) American

C) European

D) Brazilian

E) Chinese

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

6

Standard stock options are traded and bought and sold through dealers only and cannot be bought via an exchange.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

7

Using an option to reduce the risk of a portfolio is called ________,while using options to bet on the direction of the market or an asset is called ________.

A) hedging, speculation

B) hedging, verification

C) verification, hedging

D) speculation, hedging

E) verification, speculation

A) hedging, speculation

B) hedging, verification

C) verification, hedging

D) speculation, hedging

E) verification, speculation

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

8

The ________ side of an options contract has the option to exercise,while the ________ side has an obligation to fulfill the contract.

A) long, long

B) short, long

C) long, short

D) short, short

E) short, other

A) long, long

B) short, long

C) long, short

D) short, short

E) short, other

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

9

Hedging is accomplished by holding contracts or securities whose payoffs are positively correlated with some risk exposure that already exists.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

10

American options allow their holders to exercise the option only on the expiration date.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

11

Using options to reduce risk is called

A) speculation.

B) a naked position.

C) hedging.

D) a covered position.

E) risk-taking.

A) speculation.

B) a naked position.

C) hedging.

D) a covered position.

E) risk-taking.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

12

The price at which the holder of an option buys or sells a share of stock when the option is exercised is called the ________ price.

A) strike

B) American

C) dilutive

D) closing

E) spot

A) strike

B) American

C) dilutive

D) closing

E) spot

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

13

Options are also called derivative assets because they derive their value solely from the price of another asset.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

14

When the exercise price of a call option is higher than the current price of the stock,the option is said to be

A) at-the-money.

B) in-the-money.

C) out-of-the-money.

D) trading at par.

E) trading below par.

A) at-the-money.

B) in-the-money.

C) out-of-the-money.

D) trading at par.

E) trading below par.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

15

________ options allow the holder to exercise the option on any date up to and including the expiration date.

A) Canadian

B) American

C) European

D) French

E) Chinese

A) Canadian

B) American

C) European

D) French

E) Chinese

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

16

When a company writes a call option on new stock in the company,it is called a

A) convertible bond.

B) put option.

C) stock option.

D) warrant.

E) stock.

A) convertible bond.

B) put option.

C) stock option.

D) warrant.

E) stock.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

17

The ________ is the total number of contracts of a particular option that have been written and not yet closed.

A) market interest

B) open interest

C) turnover

D) local turnover

E) volume

A) market interest

B) open interest

C) turnover

D) local turnover

E) volume

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

18

The writer of a call option has

A) the obligation to sell a security for a given price.

B) the obligation to buy a security for a given price.

C) the right to sell a security for a given price.

D) the right to buy a security for a given price.

E) the long position in the contract.

A) the obligation to sell a security for a given price.

B) the obligation to buy a security for a given price.

C) the right to sell a security for a given price.

D) the right to buy a security for a given price.

E) the long position in the contract.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

19

A call option gives the owner the right to ________ an asset at a fixed price at some future date.

A) sell

B) buy

C) hold

D) exchange

E) provide

A) sell

B) buy

C) hold

D) exchange

E) provide

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

20

An options contract gives the owner the ________ but not the ________ to buy or sell an asset at a fixed price at some future date.

A) obligation, right

B) right, option

C) right, obligation

D) option, right

E) obligation, option

A) obligation, right

B) right, option

C) right, obligation

D) option, right

E) obligation, option

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

21

When is an option out-the-money?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

22

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to buy one options contract with an exercise price closest to being at-the-money and that expires January 2009.The current price that you would have to pay for such a contract is:

A) $680

B) $380

C) $650

D) $420

E) $450

Consider the following information on options from the CBOE for Merck:

Assume you want to buy one options contract with an exercise price closest to being at-the-money and that expires January 2009.The current price that you would have to pay for such a contract is:

A) $680

B) $380

C) $650

D) $420

E) $450

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

23

What is a call option?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

24

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

25

When is an option in-the-money?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

26

What are European options?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

27

Using options to place a bet on the direction in which you believe the market is likely to move is called

A) speculation.

B) hedging.

C) a covered position.

D) a naked position.

E) diversification.

A) speculation.

B) hedging.

C) a covered position.

D) a naked position.

E) diversification.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

28

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2009 put option that is closest to being at-the-money is:

A) 7174

B) 982

C) 319

D) 8422

E) 5513

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2009 put option that is closest to being at-the-money is:

A) 7174

B) 982

C) 319

D) 8422

E) 5513

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

29

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are in-the-money?

A) 2

B) 4

C) 1

D) 3

E) 0

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are in-the-money?

A) 2

B) 4

C) 1

D) 3

E) 0

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

30

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $1750

B) $2000

C) $3500

D) $3900

E) $4400

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $1750

B) $2000

C) $3500

D) $3900

E) $4400

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

31

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the December 2010 put options are in-the-money?

A) 1

B) 2

C) 3

D) 4

E) 5

Consider the following information on options from the CBOE for Merck:

How many of the December 2010 put options are in-the-money?

A) 1

B) 2

C) 3

D) 4

E) 5

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

32

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $4500

B) $2600

C) $3900

D) $4000

E) $3500

Consider the following information on options from the CBOE for Merck:

Assume you want to sell 20 call option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would receive for such a contract is:

A) $4500

B) $2600

C) $3900

D) $4000

E) $3500

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

33

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to buy five call option contracts with an exercise price closest to being at-the-money and that expires December 2010.The current price that you would have to pay for such a contract is:

A) $550

B) $110

C) $475

D) $300

E) $525

Consider the following information on options from the CBOE for Merck:

Assume you want to buy five call option contracts with an exercise price closest to being at-the-money and that expires December 2010.The current price that you would have to pay for such a contract is:

A) $550

B) $110

C) $475

D) $300

E) $525

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

34

What are American options?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

35

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2011 call option that is closest to being at-the-money is:

A) 1436

B) 2245

C) 872

D) 523

E) 117

Consider the following information on options from the CBOE for Merck:

The open interest for a January 2011 call option that is closest to being at-the-money is:

A) 1436

B) 2245

C) 872

D) 523

E) 117

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

36

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 call options are out-of-the-money?

A) 0

B) 1

C) 2

D) 3

E) 4

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

37

When is an option at-the-money?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

38

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

Assume you want to buy 10 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would have to pay for such a contract is:

A) $1750

B) $2000

C) $1950

D) $2200

E) $2550

Consider the following information on options from the CBOE for Merck:

Assume you want to buy 10 put option contracts with an exercise price closest to being at-the-money and that expires January 2011.The current price that you would have to pay for such a contract is:

A) $1750

B) $2000

C) $1950

D) $2200

E) $2550

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

39

What is a put option?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

40

Use the table for the question(s) below.

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are in-the-money?

A) 1

B) 3

C) 2

D) 4

E) 0

Consider the following information on options from the CBOE for Merck:

How many of the January 2009 put options are in-the-money?

A) 1

B) 3

C) 2

D) 4

E) 0

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

41

An investor purchases a call option and its underlying stock on the same day.If the stock appreciates by 25%,the call option will appreciate by:

A) more than 25%

B) less than 25%

C) exactly 25%

D) 0%

E) less than 0%

A) more than 25%

B) less than 25%

C) exactly 25%

D) 0%

E) less than 0%

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

42

When a stock price appreciates by a certain percentage,a call option on the same stock appreciates by a lower percentage amount.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

43

Use the figure for the question(s) below.

This graph depicts the payoffs of a

A) short position in a put option at expiration.

B) short position in a call option at expiration.

C) long position in a put option at expiration.

D) long position in a call option at expiration.

E) long position in a call option before expiration.

This graph depicts the payoffs of a

A) short position in a put option at expiration.

B) short position in a call option at expiration.

C) long position in a put option at expiration.

D) long position in a call option at expiration.

E) long position in a call option before expiration.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

44

A put option on a stock has an exercise price of $74.If the stock price at expiration is $79,what is the option payoff for a long put position?

A) $0

B) $5

C) -$5

D) $79

E) -$79

A) $0

B) $5

C) -$5

D) $79

E) -$79

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

45

Although the payouts on a long position in an options contract are never negative,the profit from purchasing and holding it could be negative.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

46

A put option on a stock has an exercise price of $31.If the stock price at expiration is $29.45,what is the option payoff for a long put position?

A) $29.45

B) $0

C) $1.55

D) -$1.55

E) -$29.45

A) $29.45

B) $0

C) $1.55

D) -$1.55

E) -$29.45

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

47

Use the figure for the question(s) below.

You pay $3.25 for a call option on Luther Industries that expires in three months with a strike price of $40.00.Three months later,at expiration,Luther Industries is trading at $41.00 per share.Your profit per share on this transaction is closest to:

A) -$1.00

B) $1.00

C) -$2.25

D) $2.25

E) $0

You pay $3.25 for a call option on Luther Industries that expires in three months with a strike price of $40.00.Three months later,at expiration,Luther Industries is trading at $41.00 per share.Your profit per share on this transaction is closest to:

A) -$1.00

B) $1.00

C) -$2.25

D) $2.25

E) $0

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

48

Use the figure for the question(s) below.

This graph depicts the payoffs of a

A) a long position in a put option at expiration.

B) short position in a call option at expiration.

C) a short position in a put option at expiration.

D) a long position in a call option at expiration.

E) a long position in a call option before expiration.

This graph depicts the payoffs of a

A) a long position in a put option at expiration.

B) short position in a call option at expiration.

C) a short position in a put option at expiration.

D) a long position in a call option at expiration.

E) a long position in a call option before expiration.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

49

The payoff to the holder of a put option is given by:

A) P = max(K - S, 0)

B) P= max(S - K, 0)

C) P = min(S - K, 0)

D) P = max(K, 0)

E) P = max(S - K, 0)

A) P = max(K - S, 0)

B) P= max(S - K, 0)

C) P = min(S - K, 0)

D) P = max(K, 0)

E) P = max(S - K, 0)

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

50

A put option on a stock has an exercise price of $42.If the stock price at expiration is $35,what is the option payoff for a short put position?

A) $0

B) $7

C) -$7

D) $35

E) -$35

A) $0

B) $7

C) -$7

D) $35

E) -$35

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

51

A call option on a stock has an exercise price of $12.15.If the stock price at expiration is $11,what is the option payoff for a short call position?

A) $-11

B) $11

C) $1.15

D) -$1.15

E) $0

A) $-11

B) $11

C) $1.15

D) -$1.15

E) $0

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

52

A call option on a stock has an exercise price of $34.50.If the stock price at expiration is $37.50,what is the option payoff for a short call position?

A) $34.50

B) $0

C) $3

D) -$3

E) -$34.50

A) $34.50

B) $0

C) $3

D) -$3

E) -$34.50

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

53

Suppose you purchase a call option for $4 and a strike price of $30.On the expiration day,the price of the stock is $40.What is the return on the call option if you hold your position until maturity?

A) 125%

B) 130%

C) 150%

D) 170%

E) 250%

A) 125%

B) 130%

C) 150%

D) 170%

E) 250%

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

54

A put option on a stock has an exercise price of $31.If the stock price at expiration is $33.40,what is the option payoff for a short put position?

A) $33.40

B) -$2.40

C) $2.40

D) $0

E) -$33.40

A) $33.40

B) -$2.40

C) $2.40

D) $0

E) -$33.40

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

55

A call option on a stock has an exercise price of $14.If the stock price at expiration is $13.50,what is the option payoff for a long call position?

A) $0.50

B) $0

C) -$0.50

D) $13.50

E) $14

A) $0.50

B) $0

C) -$0.50

D) $13.50

E) $14

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

56

Suppose you purchase a call option for $5 and a strike price of $20.On the expiration day,the price of the stock is $30.What is the return on the call option if you hold your position until maturity?

A) 25%

B) 50%

C) 75%

D) 100%

E) 0%

A) 25%

B) 50%

C) 75%

D) 100%

E) 0%

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

57

A call option on a stock has an exercise price of $22.25.If the stock price at expiration is $25,what is the option payoff for a long call position?

A) $2.75

B) $0

C) -$2.75

D) $25

E) $22.25

A) $2.75

B) $0

C) -$2.75

D) $25

E) $22.25

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

58

Suppose you purchase a call option for $5 and a strike price of $40.On the expiration day,the price of the stock is $55.What is the return on the call option if you hold your position until maturity?

A) 125%

B) 200%

C) 275%

D) 300%

E) -100%

A) 125%

B) 200%

C) 275%

D) 300%

E) -100%

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

59

The payoff to the holder of a call option is given by:

A) C = max(S - K, 0)

B) C = min(K, 0)

C) C = max(K - S, 0)

D) C = min(K - S, 0)

E) C = min(S - K, 0)

A) C = max(S - K, 0)

B) C = min(K, 0)

C) C = max(K - S, 0)

D) C = min(K - S, 0)

E) C = min(S - K, 0)

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

60

Use the figure for the question(s) below.

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $60 in three months,what will you owe for each share in the contract?

A) $0

B) $60

C) $50

D) $10

E) $40

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $60 in three months,what will you owe for each share in the contract?

A) $0

B) $60

C) $50

D) $10

E) $40

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

61

The value of a call option ________ with the risk-free rate,and the value of a put option ________ with the risk-free rate.

A) increases, increases

B) decreases, decreases

C) increases, decreases

D) decreases, increases

E) increases, does not change

A) increases, increases

B) decreases, decreases

C) increases, decreases

D) decreases, increases

E) increases, does not change

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

62

Suppose a stock is currently trading for $12,and in one period it will either increase to $15 or decrease to $8.If the one-period risk-free rate is 4%,what is the price of a European put option that expires in one period and has an exercise price of $10?

A) $0.96

B) $1.92

C) $1.00

D) $2.00

E) $0.69

A) $0.96

B) $1.92

C) $1.00

D) $2.00

E) $0.69

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

63

Suppose a stock is currently trading for $35,and in one period it will either increase to $38 or decrease to $33.If the one-period risk-free rate is 6%,what is the price of a European put option that expires in one period and has an exercise price of $36?

A) $1.55

B) $1.50

C) $3.00

D) $0.51

E) $2.49

A) $1.55

B) $1.50

C) $3.00

D) $0.51

E) $2.49

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

64

The value of an otherwise identical call option is ________ if the stock price is ________.

A) higher, higher

B) lower, higher

C) higher, lower

D) unchanged, higher

E) unchanged, lower

A) higher, higher

B) lower, higher

C) higher, lower

D) unchanged, higher

E) unchanged, lower

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

65

Use the figure for the question(s) below.

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $45 in three months,what will you owe for each share in the contract?

A) $0

B) $50

C) $60

D) $10

E) $40

You have shorted a call option on WSJ stock with a strike price of $50.The option will expire in exactly six months.If the stock is trading at $45 in three months,what will you owe for each share in the contract?

A) $0

B) $50

C) $60

D) $10

E) $40

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

66

A European option on a stock is more valuable than an otherwise similar American option on the same stock.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following will increase the value of a call option?

A) a decrease in the time to maturity

B) a decrease in the stock price

C) a decrease in the stock's volatility

D) a decrease in the exercise price

E) a decrease in the risk-free rate

A) a decrease in the time to maturity

B) a decrease in the stock price

C) a decrease in the stock's volatility

D) a decrease in the exercise price

E) a decrease in the risk-free rate

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

68

In practice,option prices are not very sensitive to changes in the risk-free rate.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

69

The value of an otherwise identical call option is ________ if the strike price the holder must pay to buy the stock is ________.

A) higher, higher

B) lower, lower

C) higher, lower

D) unchanged, lower

E) unchanged, higher

A) higher, higher

B) lower, lower

C) higher, lower

D) unchanged, lower

E) unchanged, higher

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

70

Suppose a stock is currently trading for $23,and in one period it will either increase to $30 or decrease to $20.If the one-period risk-free rate is 5%,what is the price of a European put option that expires in one period and has an exercise price of $25?

A) $2.79

B) $2.50

C) $2.38

D) $2.21

E) $2.66

A) $2.79

B) $2.50

C) $2.38

D) $2.21

E) $2.66

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following will increase the value of a put option?

A) a decrease in the time to maturity

B) an increase in the stock price

C) a decrease in the stock's volatility

D) a decrease in the exercise price

E) a decrease in the risk-free rate

A) a decrease in the time to maturity

B) an increase in the stock price

C) a decrease in the stock's volatility

D) a decrease in the exercise price

E) a decrease in the risk-free rate

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

72

What effect does volatility of the underlying asset have on the price of the option?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

73

A European option with a later exercise date may trade potentially for less than an otherwise identical option with an earlier exercise date.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

74

Suppose a stock is currently trading for $35,and in one period it will either increase to $38 or decrease to $33.If the one-period risk-free rate is 6%,what is the price of a European call option that expires in one period and has an exercise price of $36?

A) $1.55

B) $0.80

C) $2.00

D) $1.63

E) $1.00

A) $1.55

B) $0.80

C) $2.00

D) $1.63

E) $1.00

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

75

Use the figure for the question(s) below.

What is the short position of an options contract?

What is the short position of an options contract?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

76

The binomial option pricing model calculates the option price by creating a replicating portfolio out of a risk-free bond and the underlying stock.

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

77

Use the figure for the question(s) below.

What is the long position of an options contract?

What is the long position of an options contract?

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

78

Suppose a stock is currently trading for $12,and in one period it will either increase to $15 or decrease to $8.If the one-period risk-free rate is 4%,what is the price of a European call option that expires in one period and has an exercise price of $7?

A) $4.68

B) $4.50

C) $5.27

D) $5.00

E) $7.00

A) $4.68

B) $4.50

C) $5.27

D) $5.00

E) $7.00

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

79

Suppose a stock is currently trading for $23,and in one period it will either increase to $30 or decrease to $20.If the one-period risk-free rate is 5%,what is the price of a European call option that expires in one period and has an exercise price of $25?

A) $1.25

B) $1.98

C) $1.50

D) $2.21

E) $2.50

A) $1.25

B) $1.98

C) $1.50

D) $2.21

E) $2.50

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

80

The value of an otherwise identical American call option is ________ if the exercise date is ________.

A) higher, longer

B) lower, longer

C) higher, closer

D) unchanged, closer

E) unchanged, longer

A) higher, longer

B) lower, longer

C) higher, closer

D) unchanged, closer

E) unchanged, longer

Unlock Deck

Unlock for access to all 112 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 112 flashcards in this deck.