Deck 12: Perfect Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

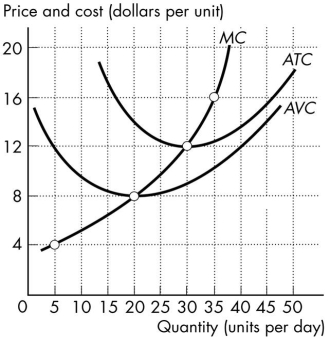

Use the figure below to answer the following questions.

Figure 12.1.1

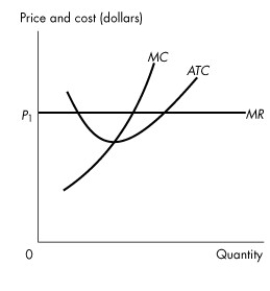

Refer to Figure 12.1.1. The firm competes in a perfectly competitive market.Curve A is a straight line because the firm

A)is a price taker.

B)faces constant returns to scale.

C)wants to maximize profits.

D)has perfect information.

E)has constant marginal cost.

Figure 12.1.1

Refer to Figure 12.1.1. The firm competes in a perfectly competitive market.Curve A is a straight line because the firm

A)is a price taker.

B)faces constant returns to scale.

C)wants to maximize profits.

D)has perfect information.

E)has constant marginal cost.

Question

Question

Question

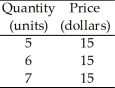

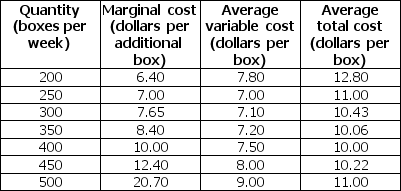

Use the table below to answer the following questions.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 5 units of output, total revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 5 units of output, total revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Question

Question

Use the table below to answer the following questions.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 6 units of output, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 6 units of output, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Question

Question

Question

Question

Use the figure below to answer the following questions.

Figure 12.1.1

Refer to Figure 12.1.1.The firm competes in a perfectly competitive market.Curve A represents the firm's

A)total fixed cost curve.

B)average fixed cost curve.

C)average variable cost curve.

D)total revenue curve.

E)marginal revenue curve.

Figure 12.1.1

Refer to Figure 12.1.1.The firm competes in a perfectly competitive market.Curve A represents the firm's

A)total fixed cost curve.

B)average fixed cost curve.

C)average variable cost curve.

D)total revenue curve.

E)marginal revenue curve.

Question

Use the table below to answer the following questions.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the quantity sold by the firm rises from 5 to 6, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the quantity sold by the firm rises from 5 to 6, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Question

Question

Question

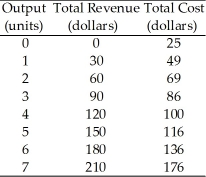

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 3 units of output, it will

A)make an economic profit of $4.

B)make an economic profit of $90.

C)incur an economic loss of $4.

D)break even.

E)incur an economic loss of $86.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 3 units of output, it will

A)make an economic profit of $4.

B)make an economic profit of $90.

C)incur an economic loss of $4.

D)break even.

E)incur an economic loss of $86.

Question

Question

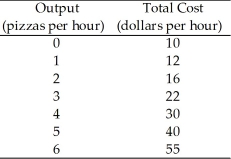

Use the table below to answer the following questions.

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If the price of a pizza is $7, what is Chip's profit-maximizing output per hour?

A)zero pizzas

B)1 pizza

C)2 pizzas

D)3 pizzas

E)4 pizzas

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If the price of a pizza is $7, what is Chip's profit-maximizing output per hour?

A)zero pizzas

B)1 pizza

C)2 pizzas

D)3 pizzas

E)4 pizzas

Question

Question

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.Economic profit is maximized when the firm produces ________ units of output.

A)zero

B)7

C)3

D)6

E)5

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.Economic profit is maximized when the firm produces ________ units of output.

A)zero

B)7

C)3

D)6

E)5

Question

Question

Use the table below to answer the following questions.

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If Chip shuts down in the short run, his total cost is

A)$0.

B)$10 an hour.

C)$12 an hour.

D)$22 an hour.

E)$40 an hour.

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If Chip shuts down in the short run, his total cost is

A)$0.

B)$10 an hour.

C)$12 an hour.

D)$22 an hour.

E)$40 an hour.

Question

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 2 units of output, it

A)makes an economic profit of $9.

B)makes an economic profit of $60.

C)incurs an economic loss of $9.

D)incurs an economic loss of $60.

E)incurs an economic loss of $69.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 2 units of output, it

A)makes an economic profit of $9.

B)makes an economic profit of $60.

C)incurs an economic loss of $9.

D)incurs an economic loss of $60.

E)incurs an economic loss of $69.

Question

Question

Use the table below to answer the following questions.

Table 12.2.3

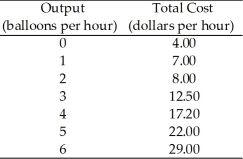

Refer to Table 12.2.3 which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average variable cost of producing the 1st balloon is

A)$1.00.

B)$4.00.

C)$2.00.

D)$4.80.

E)$3.00.

Table 12.2.3

Refer to Table 12.2.3 which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average variable cost of producing the 1st balloon is

A)$1.00.

B)$4.00.

C)$2.00.

D)$4.80.

E)$3.00.

Question

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal revenue received from the sale of the 4th unit of output is

A)$3.

B)$15.

C)$10.

D)$120.

E)$30.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal revenue received from the sale of the 4th unit of output is

A)$3.

B)$15.

C)$10.

D)$120.

E)$30.

Question

Question

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal cost of increasing production from 4 units to 5 units is

A)$16.

B)$128.

C)$100.

D)$116.

E)$30.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal cost of increasing production from 4 units to 5 units is

A)$16.

B)$128.

C)$100.

D)$116.

E)$30.

Question

Use the table below to answer the following questions.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average fixed cost of producing the 4th balloon is

A)$4.30.

B)$4.80.

C)$4.70.

D)$4.50.

E)$1.00.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average fixed cost of producing the 4th balloon is

A)$4.30.

B)$4.80.

C)$4.70.

D)$4.50.

E)$1.00.

Question

Use the table below to answer the following questions.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The marginal cost of increasing production from 4 balloons an hour to 5 balloons an hour is

A)$1.00.

B)$4.50.

C)$4.70.

D)$4.80.

E)$4.40.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The marginal cost of increasing production from 4 balloons an hour to 5 balloons an hour is

A)$1.00.

B)$4.50.

C)$4.70.

D)$4.80.

E)$4.40.

Question

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The short-run equilibrium price of one unit of the good is

A)$3.

B)$10.

C)$15.

D)$25.

E)$30.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The short-run equilibrium price of one unit of the good is

A)$3.

B)$10.

C)$15.

D)$25.

E)$30.

Question

Question

Use the table below to answer the following questions.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.Brenda's total fixed cost is

A)$3 an hour.

B)$4 an hour.

C)$7 an hour.

D)$29 an hour.

E)zero.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.Brenda's total fixed cost is

A)$3 an hour.

B)$4 an hour.

C)$7 an hour.

D)$29 an hour.

E)zero.

Question

Question

Question

Question

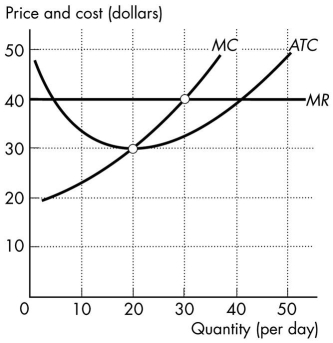

Use the figure below to answer the following questions.

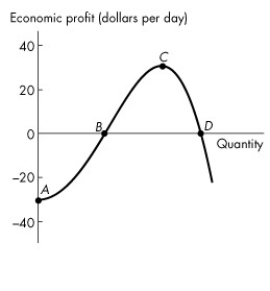

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is incurring a loss at

A)point A.

B)point B.

C)point C.

D)point D.

E)both points B and D.

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is incurring a loss at

A)point A.

B)point B.

C)point C.

D)point D.

E)both points B and D.

Question

Question

Use the figure below to answer the following question.

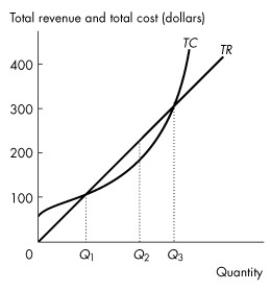

Figure 12.2.1

Refer to Figure 12.2.1, which shows a perfectly competitive firm's total revenue and total cost curves.Which one of the following statements is false?

A)Economic profit is the vertical distance between the total revenue curve and the total cost curve.

B)At an output of Q₁ units a day, the firm makes zero economic profit.

C)At an output greater than Q₃ units a day, the firm incurs an economic loss.

D)At an output of Q₂ units a day, the firm incurs an economic loss.

E)At an output less than Q₁ units a day, the firm incurs an economic loss.

Figure 12.2.1

Refer to Figure 12.2.1, which shows a perfectly competitive firm's total revenue and total cost curves.Which one of the following statements is false?

A)Economic profit is the vertical distance between the total revenue curve and the total cost curve.

B)At an output of Q₁ units a day, the firm makes zero economic profit.

C)At an output greater than Q₃ units a day, the firm incurs an economic loss.

D)At an output of Q₂ units a day, the firm incurs an economic loss.

E)At an output less than Q₁ units a day, the firm incurs an economic loss.

Question

Use the table below to answer the following question.

Table 12.2.4

Refer to Table 12.2.4.The market is perfectly competitive and there are 1,000 firms that produce paper. The top table sets out the market demand schedule for paper.

Each producer of paper has the costs shown in the bottom table when it uses its least-cost plant size.

The market price is ________ a box and the market output is ________ boxes. The output produced by each firm is ________ boxes.Each firm ________.

A)$7.00; 250,000; 250; incurs an economic loss of $1,000 a week

B)$8.40; 350,000; 350; makes zero economic profit

C)$7.65; 300,000; 300; incurs an economic loss of $834 a week

D)$8.40; 350,000; 350; incurs an economic loss of $581 a week

E)$7.65; 350,000; 300; makes zero economic profit

Table 12.2.4

Refer to Table 12.2.4.The market is perfectly competitive and there are 1,000 firms that produce paper. The top table sets out the market demand schedule for paper.

Each producer of paper has the costs shown in the bottom table when it uses its least-cost plant size.

The market price is ________ a box and the market output is ________ boxes. The output produced by each firm is ________ boxes.Each firm ________.

A)$7.00; 250,000; 250; incurs an economic loss of $1,000 a week

B)$8.40; 350,000; 350; makes zero economic profit

C)$7.65; 300,000; 300; incurs an economic loss of $834 a week

D)$8.40; 350,000; 350; incurs an economic loss of $581 a week

E)$7.65; 350,000; 300; makes zero economic profit

Question

Question

Question

Use the figure below to answer the following questions.

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is breaking even at points

A)A and C.

B)A and D.

C)B and C.

D)B and D.

E)C and D.

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is breaking even at points

A)A and C.

B)A and D.

C)B and C.

D)B and D.

E)C and D.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the figure below to answer the following question.

Figure 12.3.4

Refer to Figure 12.3.4, which shows cost curves of Paul's Picture Frames Inc.The picture frame market is perfectly competitive and the market price is $12 a frame.Paul produces ________ frames each week and makes ________ total revenue.

A)20; $240

B)20; $96

C)zero; zero

D)30; $360

E)30; zero

Figure 12.3.4

Refer to Figure 12.3.4, which shows cost curves of Paul's Picture Frames Inc.The picture frame market is perfectly competitive and the market price is $12 a frame.Paul produces ________ frames each week and makes ________ total revenue.

A)20; $240

B)20; $96

C)zero; zero

D)30; $360

E)30; zero

Question

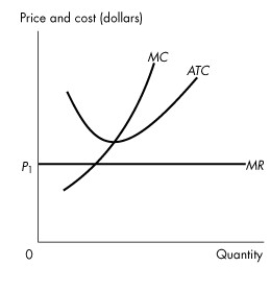

Use the figure below to answer the following question.

Figure 12.3.3

Refer to Figure 12.3.3, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)at its shutdown point.

E)larger than the other firms in the industry.

Figure 12.3.3

Refer to Figure 12.3.3, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)at its shutdown point.

E)larger than the other firms in the industry.

Question

Use the figure below to answer the following questions.

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, the firm will

A)exit from the industry.

B)break even.

C)make an economic profit.

D)incur an economic loss.

E)close down.

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, the firm will

A)exit from the industry.

B)break even.

C)make an economic profit.

D)incur an economic loss.

E)close down.

Question

Question

Question

Use the figure below to answer the following question.

Figure 12.3.2

Refer to Figure 12.3.2, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry, The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)not maximizing economic profit.

E)going to close down temporarily.

Figure 12.3.2

Refer to Figure 12.3.2, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry, The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)not maximizing economic profit.

E)going to close down temporarily.

Question

Question

Question

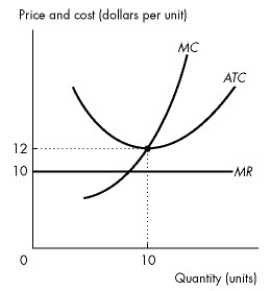

Use the figure below to answer the following question.

Figure 12.3.5

Refer to Figure 12.3.5, which shows the cost curves and the marginal revenue curve for a perfectly competitive firm.To maximize its profit, the firm produces ________ units of output and the price is ________ a unit.

A)30; $40

B)30; $30

C)20; $40

D)20; $30

E)30; $32.50

Figure 12.3.5

Refer to Figure 12.3.5, which shows the cost curves and the marginal revenue curve for a perfectly competitive firm.To maximize its profit, the firm produces ________ units of output and the price is ________ a unit.

A)30; $40

B)30; $30

C)20; $40

D)20; $30

E)30; $32.50

Question

Use the figure below to answer the following questions.

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, if the market price of the good is $10, the firm produces ________ units of output and ________.

A)10; incurs an economic loss of $20

B)10; incurs an economic loss of $40

C)less than 10; incurs an economic loss of $20

D)10; makes an economic profit of $20

E)less than 10; incurs an economic loss of less than $20

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, if the market price of the good is $10, the firm produces ________ units of output and ________.

A)10; incurs an economic loss of $20

B)10; incurs an economic loss of $40

C)less than 10; incurs an economic loss of $20

D)10; makes an economic profit of $20

E)less than 10; incurs an economic loss of less than $20

Question

Question

Question

Question

Question

Question

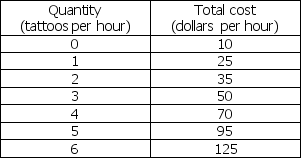

Use the table below to answer the following questions.

Table 12.2.5

Refer to Table 12.2.5.Archibald's Tattoos is a perfectly competitive firm.The firm's total costs are shown in the table.The price at Archibald's shut-down point is

A)$10.00.

B)$15.00.

C)$12.50.

D)$13.33.

E)$17.00.

Table 12.2.5

Refer to Table 12.2.5.Archibald's Tattoos is a perfectly competitive firm.The firm's total costs are shown in the table.The price at Archibald's shut-down point is

A)$10.00.

B)$15.00.

C)$12.50.

D)$13.33.

E)$17.00.

Question

Question

Use the table below to answer the following questions.

Table 12.2.5

Refer to Table 12.2.5.Archibald's Tattoos is a perfectly competitive firm.The firm's total costs are shown in the table.If the price of a tattoo is $12.50, Archibald's economic profit is

A)-$10.00 an hour.

B)zero.

C)$12.50 an hour.

D)$10.00 an hour.

E)maximized.

Table 12.2.5

Refer to Table 12.2.5.Archibald's Tattoos is a perfectly competitive firm.The firm's total costs are shown in the table.If the price of a tattoo is $12.50, Archibald's economic profit is

A)-$10.00 an hour.

B)zero.

C)$12.50 an hour.

D)$10.00 an hour.

E)maximized.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/117

Play

Full screen (f)

Deck 12: Perfect Competition

1

In a perfectly competitive market, the market demand curve is illustrated by

A)a downward-sloping curve.

B)a line that is vertical at the market output.

C)an upward-sloping curve.

D)a line that is horizontal at the market price.

E)a curve that is bowed towards the origin.

A)a downward-sloping curve.

B)a line that is vertical at the market output.

C)an upward-sloping curve.

D)a line that is horizontal at the market price.

E)a curve that is bowed towards the origin.

A

2

For perfect competition to arise, it is necessary that market demand be

A)inelastic.

B)elastic.

C)perfectly elastic.

D)large relative to the minimum efficient scale of a single firm.

E)small relative to the minimum efficient scale of a single firm.

A)inelastic.

B)elastic.

C)perfectly elastic.

D)large relative to the minimum efficient scale of a single firm.

E)small relative to the minimum efficient scale of a single firm.

D

3

The slope of a perfectly competitive firm's demand curve is

A)infinity.

B)zero.

C)1.

D)greater than 1.

E)negative.

A)infinity.

B)zero.

C)1.

D)greater than 1.

E)negative.

B

4

Lin's fortune cookies are identical to the fortune cookies made by dozens of other firms, and there is free entry in the fortune cookie market.Buyers and sellers are well informed about prices.Lin's fortune cookies operates in a ________ market.

A)challenging

B)monopolistic

C)perfectly competitive

D)noncompetitive

E)perfectly competent

A)challenging

B)monopolistic

C)perfectly competitive

D)noncompetitive

E)perfectly competent

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

5

Economic profit equals

A)total fixed cost plus total variable cost.

B)total revenue minus marginal cost.

C)marginal revenue minus marginal cost.

D)total revenue minus total cost.

E)total revenue minus total variable cost.

A)total fixed cost plus total variable cost.

B)total revenue minus marginal cost.

C)marginal revenue minus marginal cost.

D)total revenue minus total cost.

E)total revenue minus total variable cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

6

A perfectly competitive market is characterized by

A)firms that are price setters.

B)firms that each face a downward-sloping demand curve.

C)firms that each sell a unique good or service.

D)buyers who are unaware of the price charged by each firm.

E)no restrictions on entry into the market.

A)firms that are price setters.

B)firms that each face a downward-sloping demand curve.

C)firms that each sell a unique good or service.

D)buyers who are unaware of the price charged by each firm.

E)no restrictions on entry into the market.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

7

Which one of the following does not occur in perfect competition?

A)No single firm can exert a significant influence on the market price of the good.

B)There are many buyers.

C)There are significant restrictions on entry into the market.

D)Sellers and buyers are well informed about prices.

E)Established firms have no advantage over new ones.

A)No single firm can exert a significant influence on the market price of the good.

B)There are many buyers.

C)There are significant restrictions on entry into the market.

D)Sellers and buyers are well informed about prices.

E)Established firms have no advantage over new ones.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

8

Perfect competition occurs in a market where there are many firms, each selling

A)an identical product.

B)a similar product.

C)a unique product.

D)a capital-intensive product.

E)a competitive product.

A)an identical product.

B)a similar product.

C)a unique product.

D)a capital-intensive product.

E)a competitive product.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

9

Use the figure below to answer the following questions.

Figure 12.1.1

Refer to Figure 12.1.1. The firm competes in a perfectly competitive market.Curve A is a straight line because the firm

A)is a price taker.

B)faces constant returns to scale.

C)wants to maximize profits.

D)has perfect information.

E)has constant marginal cost.

Figure 12.1.1

Refer to Figure 12.1.1. The firm competes in a perfectly competitive market.Curve A is a straight line because the firm

A)is a price taker.

B)faces constant returns to scale.

C)wants to maximize profits.

D)has perfect information.

E)has constant marginal cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

10

An example of a perfectly competitive industry is the

A)airline industry.

B)beer industry.

C)running shoe industry.

D)fast food industry.

E)wheat industry.

A)airline industry.

B)beer industry.

C)running shoe industry.

D)fast food industry.

E)wheat industry.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

11

A price taker is a firm that

A)must lower its price if it wants to sell more output.

B)sets the market price.

C)cannot influence the market price.

D)is incurring an economic loss.

E)can raise its price if it lowers output.

A)must lower its price if it wants to sell more output.

B)sets the market price.

C)cannot influence the market price.

D)is incurring an economic loss.

E)can raise its price if it lowers output.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

12

Use the table below to answer the following questions.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 5 units of output, total revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 5 units of output, total revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

13

A price-taking firm faces a

A)perfectly inelastic demand.

B)downward-sloping marginal revenue curve.

C)downward-sloping supply curve.

D)perfectly elastic demand.

E)downward-sloping demand curve.

A)perfectly inelastic demand.

B)downward-sloping marginal revenue curve.

C)downward-sloping supply curve.

D)perfectly elastic demand.

E)downward-sloping demand curve.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

14

Use the table below to answer the following questions.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 6 units of output, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the firm sells 6 units of output, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

15

If a firm faces a perfectly elastic demand for its product, then

A)it is not a price taker.

B)it will want to lower its price to increase sales.

C)it will want to raise its price to increase total revenue.

D)its marginal revenue curve is horizontal at the market price.

E)it will always make zero economic profit.

A)it is not a price taker.

B)it will want to lower its price to increase sales.

C)it will want to raise its price to increase total revenue.

D)its marginal revenue curve is horizontal at the market price.

E)it will always make zero economic profit.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

16

Assume that the leather market is a perfectly competitive market.The market demand curve for leather is ________ and each individual leather producer's demand curve is ________.

A)vertical; downward sloping

B)downward sloping; horizontal

C)downward sloping; vertical

D)horizontal; horizontal

E)horizontal; downward sloping

A)vertical; downward sloping

B)downward sloping; horizontal

C)downward sloping; vertical

D)horizontal; horizontal

E)horizontal; downward sloping

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

17

Lin's fortune cookies are identical to the fortune cookies made by dozens of other firms, and there is free entry in the fortune cookie market.Buyers and sellers are well informed about prices.The price of a fortune cookie is determined by ________.The marginal revenue of a fortune cookie equals ________.

A)market demand and market supply; price

B)the ingredients that Lin's uses to produce his fortune cookies; average total cost

C)the number of cookies that Lin's produces; average variable cost

D)the freshness of the fortune cookies; average fixed cost

E)market demand and market supply; the price elasticity of demand

A)market demand and market supply; price

B)the ingredients that Lin's uses to produce his fortune cookies; average total cost

C)the number of cookies that Lin's produces; average variable cost

D)the freshness of the fortune cookies; average fixed cost

E)market demand and market supply; the price elasticity of demand

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

18

Use the figure below to answer the following questions.

Figure 12.1.1

Refer to Figure 12.1.1.The firm competes in a perfectly competitive market.Curve A represents the firm's

A)total fixed cost curve.

B)average fixed cost curve.

C)average variable cost curve.

D)total revenue curve.

E)marginal revenue curve.

Figure 12.1.1

Refer to Figure 12.1.1.The firm competes in a perfectly competitive market.Curve A represents the firm's

A)total fixed cost curve.

B)average fixed cost curve.

C)average variable cost curve.

D)total revenue curve.

E)marginal revenue curve.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

19

Use the table below to answer the following questions.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the quantity sold by the firm rises from 5 to 6, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Table 12.1.1

Refer to Table 12.1.1 which gives the demand schedule for a perfectly competitive firm.If the quantity sold by the firm rises from 5 to 6, marginal revenue is

A)$15.

B)$30.

C)$75.

D)$90.

E)$105.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

20

Marginal revenue is

A)the change in total quantity that results from a one-unit increase in the price of the good.

B)the change in total revenue that results from a one-unit increase in the quantity sold.

C)economic profit divided by the quantity sold.

D)the change in economic profit that results from a one-unit increase in the quantity sold.

E)total revenue minus total cost.

A)the change in total quantity that results from a one-unit increase in the price of the good.

B)the change in total revenue that results from a one-unit increase in the quantity sold.

C)economic profit divided by the quantity sold.

D)the change in economic profit that results from a one-unit increase in the quantity sold.

E)total revenue minus total cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

21

When a firm is a "price taker," the firm

A)can charge any price that it wants to charge, that is, "take" any price it chooses.

B)pays a fixed price for all of its fixed inputs.

C)will accept ("take")the lowest price that its customers offer.

D)pays a fixed price for all of its variable inputs.

E)cannot influence the market price of the good that it sells.

A)can charge any price that it wants to charge, that is, "take" any price it chooses.

B)pays a fixed price for all of its fixed inputs.

C)will accept ("take")the lowest price that its customers offer.

D)pays a fixed price for all of its variable inputs.

E)cannot influence the market price of the good that it sells.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

22

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 3 units of output, it will

A)make an economic profit of $4.

B)make an economic profit of $90.

C)incur an economic loss of $4.

D)break even.

E)incur an economic loss of $86.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 3 units of output, it will

A)make an economic profit of $4.

B)make an economic profit of $90.

C)incur an economic loss of $4.

D)break even.

E)incur an economic loss of $86.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

23

A firm shuts down if price is

A)above minimum average variable cost.

B)below minimum average variable cost.

C)above minimum average fixed cost.

D)less than marginal cost.

E)below average total cost.

A)above minimum average variable cost.

B)below minimum average variable cost.

C)above minimum average fixed cost.

D)less than marginal cost.

E)below average total cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

24

Use the table below to answer the following questions.

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If the price of a pizza is $7, what is Chip's profit-maximizing output per hour?

A)zero pizzas

B)1 pizza

C)2 pizzas

D)3 pizzas

E)4 pizzas

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If the price of a pizza is $7, what is Chip's profit-maximizing output per hour?

A)zero pizzas

B)1 pizza

C)2 pizzas

D)3 pizzas

E)4 pizzas

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

25

Use the information below to answer the following questions.

Fact 12.1.1 Money in the Bank

Two gas stations stand on opposite sides of the road: Rutter's Farm Store and Sheetz gas station. Rutter's doesn't even have to look across the highway to know when Sheetz changes its price for gas. When Sheetz raises the price, Rutter's pumps are busy. When Sheetz lowers prices, there's not a car in sight. Both gas stations survive but each has no control over the price.

Source: The Mining Journal, May 24, 2008

Refer to Fact 12.1.1.These gas stations operate in a ________market.

A)competitive

B)noncompetitive

C)monopolistic

D)challenging

E)consumer's

Fact 12.1.1 Money in the Bank

Two gas stations stand on opposite sides of the road: Rutter's Farm Store and Sheetz gas station. Rutter's doesn't even have to look across the highway to know when Sheetz changes its price for gas. When Sheetz raises the price, Rutter's pumps are busy. When Sheetz lowers prices, there's not a car in sight. Both gas stations survive but each has no control over the price.

Source: The Mining Journal, May 24, 2008

Refer to Fact 12.1.1.These gas stations operate in a ________market.

A)competitive

B)noncompetitive

C)monopolistic

D)challenging

E)consumer's

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

26

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.Economic profit is maximized when the firm produces ________ units of output.

A)zero

B)7

C)3

D)6

E)5

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.Economic profit is maximized when the firm produces ________ units of output.

A)zero

B)7

C)3

D)6

E)5

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

27

Use the information below to answer the following questions.

Fact 12.1.1 Money in the Bank

Two gas stations stand on opposite sides of the road: Rutter's Farm Store and Sheetz gas station. Rutter's doesn't even have to look across the highway to know when Sheetz changes its price for gas. When Sheetz raises the price, Rutter's pumps are busy. When Sheetz lowers prices, there's not a car in sight. Both gas stations survive but each has no control over the price.

Source: The Mining Journal, May 24, 2008

Refer to Fact 12.1.1.The price of gasoline is determined by ________.The marginal revenue from gasoline equals ________.

A)the quantity of gasoline that Rutter's and Sheetz sells; average variable cost

B)the number of tourists who drive by Rutter's and Sheetz; average fixed cost

C)the other goods and services that Rutter's and Sheetz sell; average total cost

D)market demand and market supply; price

E)the price elasticity of demand of gasoline; the change in total revenue that occurs when the price of a litre of gasoline rises by an incremental amount

Fact 12.1.1 Money in the Bank

Two gas stations stand on opposite sides of the road: Rutter's Farm Store and Sheetz gas station. Rutter's doesn't even have to look across the highway to know when Sheetz changes its price for gas. When Sheetz raises the price, Rutter's pumps are busy. When Sheetz lowers prices, there's not a car in sight. Both gas stations survive but each has no control over the price.

Source: The Mining Journal, May 24, 2008

Refer to Fact 12.1.1.The price of gasoline is determined by ________.The marginal revenue from gasoline equals ________.

A)the quantity of gasoline that Rutter's and Sheetz sells; average variable cost

B)the number of tourists who drive by Rutter's and Sheetz; average fixed cost

C)the other goods and services that Rutter's and Sheetz sell; average total cost

D)market demand and market supply; price

E)the price elasticity of demand of gasoline; the change in total revenue that occurs when the price of a litre of gasoline rises by an incremental amount

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

28

Use the table below to answer the following questions.

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If Chip shuts down in the short run, his total cost is

A)$0.

B)$10 an hour.

C)$12 an hour.

D)$22 an hour.

E)$40 an hour.

Table 12.2.2

Refer to Table 12.2.2, which gives the total cost schedule for Chip's Pizza Palace, a perfectly competitive firm.If Chip shuts down in the short run, his total cost is

A)$0.

B)$10 an hour.

C)$12 an hour.

D)$22 an hour.

E)$40 an hour.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

29

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 2 units of output, it

A)makes an economic profit of $9.

B)makes an economic profit of $60.

C)incurs an economic loss of $9.

D)incurs an economic loss of $60.

E)incurs an economic loss of $69.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 2 units of output, it

A)makes an economic profit of $9.

B)makes an economic profit of $60.

C)incurs an economic loss of $9.

D)incurs an economic loss of $60.

E)incurs an economic loss of $69.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

30

Use the information below to answer the following questions.

Fact 12.1.1 Money in the Bank

Two gas stations stand on opposite sides of the road: Rutter's Farm Store and Sheetz gas station. Rutter's doesn't even have to look across the highway to know when Sheetz changes its price for gas. When Sheetz raises the price, Rutter's pumps are busy. When Sheetz lowers prices, there's not a car in sight. Both gas stations survive but each has no control over the price.

Source: The Mining Journal, May 24, 2008

Refer to Fact 12.1.1.Each of these gas stations has little control over the price of gasoline because

A)the price of gasoline is determined by head office.

B)lowering the price will eliminate competition and the government mandates that gasoline stations must have competition.

C)if it raises its price, the station will lose customers.

D)the price of gasoline is set according to the price of oil.

E)the demand for gasoline is perfectly inelastic.

Fact 12.1.1 Money in the Bank

Two gas stations stand on opposite sides of the road: Rutter's Farm Store and Sheetz gas station. Rutter's doesn't even have to look across the highway to know when Sheetz changes its price for gas. When Sheetz raises the price, Rutter's pumps are busy. When Sheetz lowers prices, there's not a car in sight. Both gas stations survive but each has no control over the price.

Source: The Mining Journal, May 24, 2008

Refer to Fact 12.1.1.Each of these gas stations has little control over the price of gasoline because

A)the price of gasoline is determined by head office.

B)lowering the price will eliminate competition and the government mandates that gasoline stations must have competition.

C)if it raises its price, the station will lose customers.

D)the price of gasoline is set according to the price of oil.

E)the demand for gasoline is perfectly inelastic.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

31

Use the table below to answer the following questions.

Table 12.2.3

Refer to Table 12.2.3 which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average variable cost of producing the 1st balloon is

A)$1.00.

B)$4.00.

C)$2.00.

D)$4.80.

E)$3.00.

Table 12.2.3

Refer to Table 12.2.3 which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average variable cost of producing the 1st balloon is

A)$1.00.

B)$4.00.

C)$2.00.

D)$4.80.

E)$3.00.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

32

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal revenue received from the sale of the 4th unit of output is

A)$3.

B)$15.

C)$10.

D)$120.

E)$30.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal revenue received from the sale of the 4th unit of output is

A)$3.

B)$15.

C)$10.

D)$120.

E)$30.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

33

A firm that temporarily shuts down and produces no output incurs a loss equal to its

A)total fixed cost.

B)total variable cost.

C)marginal cost.

D)average fixed cost.

E)average total cost.

A)total fixed cost.

B)total variable cost.

C)marginal cost.

D)average fixed cost.

E)average total cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

34

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal cost of increasing production from 4 units to 5 units is

A)$16.

B)$128.

C)$100.

D)$116.

E)$30.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The marginal cost of increasing production from 4 units to 5 units is

A)$16.

B)$128.

C)$100.

D)$116.

E)$30.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

35

Use the table below to answer the following questions.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average fixed cost of producing the 4th balloon is

A)$4.30.

B)$4.80.

C)$4.70.

D)$4.50.

E)$1.00.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The average fixed cost of producing the 4th balloon is

A)$4.30.

B)$4.80.

C)$4.70.

D)$4.50.

E)$1.00.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

36

Use the table below to answer the following questions.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The marginal cost of increasing production from 4 balloons an hour to 5 balloons an hour is

A)$1.00.

B)$4.50.

C)$4.70.

D)$4.80.

E)$4.40.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.The marginal cost of increasing production from 4 balloons an hour to 5 balloons an hour is

A)$1.00.

B)$4.50.

C)$4.70.

D)$4.80.

E)$4.40.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

37

Use the table below to answer the following questions.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The short-run equilibrium price of one unit of the good is

A)$3.

B)$10.

C)$15.

D)$25.

E)$30.

Table 12.2.1

Refer to Table 12.2.1, which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.The short-run equilibrium price of one unit of the good is

A)$3.

B)$10.

C)$15.

D)$25.

E)$30.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

38

Suppose a firm is trying to decide whether or not to temporarily shut down to minimize total loss.If price equals average variable cost, then

A)total revenue equals total fixed cost, and the loss equals total variable cost.

B)total revenue equals total variable cost, and the loss equals total fixed cost.

C)total fixed cost is zero.

D)total variable cost equals total fixed cost.

E)total cost equals total variable cost.

A)total revenue equals total fixed cost, and the loss equals total variable cost.

B)total revenue equals total variable cost, and the loss equals total fixed cost.

C)total fixed cost is zero.

D)total variable cost equals total fixed cost.

E)total cost equals total variable cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

39

Use the table below to answer the following questions.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.Brenda's total fixed cost is

A)$3 an hour.

B)$4 an hour.

C)$7 an hour.

D)$29 an hour.

E)zero.

Table 12.2.3

Refer to Table 12.2.3, which gives the total cost schedule for Brenda's Balloon Shop, a perfectly competitive firm.Brenda's total fixed cost is

A)$3 an hour.

B)$4 an hour.

C)$7 an hour.

D)$29 an hour.

E)zero.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

40

A firm will shut down temporarily when the price is so low that total revenue is insufficient to cover the

A)total cost of production.

B)total variable cost of production.

C)total fixed cost of production.

D)marginal cost of production.

E)average variable cost of production.

A)total cost of production.

B)total variable cost of production.

C)total fixed cost of production.

D)marginal cost of production.

E)average variable cost of production.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

41

In a perfectly competitive market, the market price is $8.An individual firm is producing the output at which MC = $8.AVC at that output is $10.What should the firm do to maximize its economic profit in the short run?

A)shut down

B)expand output

C)contract output but continue to produce

D)leave output unchanged

E)raise the price

A)shut down

B)expand output

C)contract output but continue to produce

D)leave output unchanged

E)raise the price

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

42

A firm maximizes profit by producing the output at which marginal cost equals

A)marginal revenue.

B)minimum average total cost.

C)minimum average variable cost.

D)average fixed cost.

E)total revenue.

A)marginal revenue.

B)minimum average total cost.

C)minimum average variable cost.

D)average fixed cost.

E)total revenue.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

43

Use the figure below to answer the following questions.

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is incurring a loss at

A)point A.

B)point B.

C)point C.

D)point D.

E)both points B and D.

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is incurring a loss at

A)point A.

B)point B.

C)point C.

D)point D.

E)both points B and D.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

44

If price falls below minimum average variable cost, the best a firm can do is

A)increase production and incur a loss equal to total variable cost.

B)increase production and incur a loss equal to total fixed cost.

C)stop production and incur a loss equal to total fixed cost.

D)stop production and incur a loss equal to total variable cost.

E)stay at the same production level and incur a loss equal to the difference between total cost and total revenue.

A)increase production and incur a loss equal to total variable cost.

B)increase production and incur a loss equal to total fixed cost.

C)stop production and incur a loss equal to total fixed cost.

D)stop production and incur a loss equal to total variable cost.

E)stay at the same production level and incur a loss equal to the difference between total cost and total revenue.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

45

Use the figure below to answer the following question.

Figure 12.2.1

Refer to Figure 12.2.1, which shows a perfectly competitive firm's total revenue and total cost curves.Which one of the following statements is false?

A)Economic profit is the vertical distance between the total revenue curve and the total cost curve.

B)At an output of Q₁ units a day, the firm makes zero economic profit.

C)At an output greater than Q₃ units a day, the firm incurs an economic loss.

D)At an output of Q₂ units a day, the firm incurs an economic loss.

E)At an output less than Q₁ units a day, the firm incurs an economic loss.

Figure 12.2.1

Refer to Figure 12.2.1, which shows a perfectly competitive firm's total revenue and total cost curves.Which one of the following statements is false?

A)Economic profit is the vertical distance between the total revenue curve and the total cost curve.

B)At an output of Q₁ units a day, the firm makes zero economic profit.

C)At an output greater than Q₃ units a day, the firm incurs an economic loss.

D)At an output of Q₂ units a day, the firm incurs an economic loss.

E)At an output less than Q₁ units a day, the firm incurs an economic loss.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

46

Use the table below to answer the following question.

Table 12.2.4

Refer to Table 12.2.4.The market is perfectly competitive and there are 1,000 firms that produce paper. The top table sets out the market demand schedule for paper.

Each producer of paper has the costs shown in the bottom table when it uses its least-cost plant size.

The market price is ________ a box and the market output is ________ boxes. The output produced by each firm is ________ boxes.Each firm ________.

A)$7.00; 250,000; 250; incurs an economic loss of $1,000 a week

B)$8.40; 350,000; 350; makes zero economic profit

C)$7.65; 300,000; 300; incurs an economic loss of $834 a week

D)$8.40; 350,000; 350; incurs an economic loss of $581 a week

E)$7.65; 350,000; 300; makes zero economic profit

Table 12.2.4

Refer to Table 12.2.4.The market is perfectly competitive and there are 1,000 firms that produce paper. The top table sets out the market demand schedule for paper.

Each producer of paper has the costs shown in the bottom table when it uses its least-cost plant size.

The market price is ________ a box and the market output is ________ boxes. The output produced by each firm is ________ boxes.Each firm ________.

A)$7.00; 250,000; 250; incurs an economic loss of $1,000 a week

B)$8.40; 350,000; 350; makes zero economic profit

C)$7.65; 300,000; 300; incurs an economic loss of $834 a week

D)$8.40; 350,000; 350; incurs an economic loss of $581 a week

E)$7.65; 350,000; 300; makes zero economic profit

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

47

If a perfectly competitive firm is producing in the short run at an output where price is less than average total cost, the firm

A)will shut down.

B)is breaking even.

C)is still making a positive economic profit.

D)is incurring an economic loss but will continue to operate as long as price is above minimum average fixed cost.

E)is incurring an economic loss but will continue to operate as long as price is above minimum average variable cost.

A)will shut down.

B)is breaking even.

C)is still making a positive economic profit.

D)is incurring an economic loss but will continue to operate as long as price is above minimum average fixed cost.

E)is incurring an economic loss but will continue to operate as long as price is above minimum average variable cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

48

If a perfectly competitive firm's marginal revenue is greater than its marginal cost, the firm

A)cannot increase its economic profit.

B)must be making an economic profit.

C)will decrease its output to increase economic profit.

D)will increase its output to increase economic profit.

E)will lower the price.

A)cannot increase its economic profit.

B)must be making an economic profit.

C)will decrease its output to increase economic profit.

D)will increase its output to increase economic profit.

E)will lower the price.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

49

Use the figure below to answer the following questions.

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is breaking even at points

A)A and C.

B)A and D.

C)B and C.

D)B and D.

E)C and D.

Figure 12.2.2

Refer to Figure 12.2.2, which shows a perfectly competitive firm's economic profit and loss.The firm is breaking even at points

A)A and C.

B)A and D.

C)B and C.

D)B and D.

E)C and D.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

50

A perfectly competitive firm's supply curve includes its marginal cost curve at all prices above minimum

A)average total cost.

B)average fixed cost.

C)total cost.

D)average variable cost.

E)total variable cost.

A)average total cost.

B)average fixed cost.

C)total cost.

D)average variable cost.

E)total variable cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

51

If a perfectly competitive firm's marginal revenue is less than its marginal cost, the firm

A)cannot increase its economic profit.

B)must be making an economic profit.

C)will decrease its output to increase economic profit.

D)will increase its output to increase economic profit.

E)must raise the price.

A)cannot increase its economic profit.

B)must be making an economic profit.

C)will decrease its output to increase economic profit.

D)will increase its output to increase economic profit.

E)must raise the price.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

52

In the price range below minimum average variable cost, a perfectly competitive firm's supply curve is

A)horizontal at the market price.

B)vertical at zero output.

C)the same as its marginal cost curve.

D)the same as its average variable cost curve.

E)the same as its total variable cost curve.

A)horizontal at the market price.

B)vertical at zero output.

C)the same as its marginal cost curve.

D)the same as its average variable cost curve.

E)the same as its total variable cost curve.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

53

The maximum loss a firm will experience in the short run equals

A)zero.

B)its total fixed cost.

C)its total variable cost.

D)its total cost.

E)its marginal cost.

A)zero.

B)its total fixed cost.

C)its total variable cost.

D)its total cost.

E)its marginal cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

54

A perfectly competitive firm is maximizing profit if

A)marginal cost equals price and price is not below minimum average variable cost.

B)marginal cost equals price and price is not below minimum average fixed cost.

C)total revenue is at a maximum.

D)average variable cost is at a minimum.

E)average total cost is at a minimum.

A)marginal cost equals price and price is not below minimum average variable cost.

B)marginal cost equals price and price is not below minimum average fixed cost.

C)total revenue is at a maximum.

D)average variable cost is at a minimum.

E)average total cost is at a minimum.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

55

A firm is producing the profit-maximizing amount of output when it is producing where its ________ curve intersects its ________ curve.

A)marginal cost; average total cost

B)marginal cost; average variable cost

C)marginal cost; marginal revenue

D)average total cost; average variable cost

E)total cost; total revenue

A)marginal cost; average total cost

B)marginal cost; average variable cost

C)marginal cost; marginal revenue

D)average total cost; average variable cost

E)total cost; total revenue

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

56

In a perfectly competitive market, a firm maximizes its profit by producing the quantity of output at which

A)market price equals average fixed cost.

B)market price equals marginal cost.

C)average variable cost equals average fixed cost.

D)market price equals minimum average variable cost.

E)market price equals marginal revenue.

A)market price equals average fixed cost.

B)market price equals marginal cost.

C)average variable cost equals average fixed cost.

D)market price equals minimum average variable cost.

E)market price equals marginal revenue.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

57

In the price range above minimum average variable cost, a perfectly competitive firm's supply curve is

A)horizontal at the market price.

B)vertical at zero output.

C)the same as its marginal cost curve.

D)the same as its average variable cost curve.

E)the same as its total variable cost curve.

A)horizontal at the market price.

B)vertical at zero output.

C)the same as its marginal cost curve.

D)the same as its average variable cost curve.

E)the same as its total variable cost curve.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

58

The shutdown point occurs at the point of minimum

A)marginal cost.

B)average variable cost.

C)average fixed cost.

D)total cost.

E)average total cost.

A)marginal cost.

B)average variable cost.

C)average fixed cost.

D)total cost.

E)average total cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

59

If a perfectly competitive firm is producing an output at which price is equal to average total cost, the firm

A)should shut down.

B)is breaking even.

C)is making an economic profit.

D)is incurring an economic loss.

E)is not producing its profit-maximizing quantity.

A)should shut down.

B)is breaking even.

C)is making an economic profit.

D)is incurring an economic loss.

E)is not producing its profit-maximizing quantity.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

60

A perfectly competitive firm is producing at the point at which marginal cost equals marginal revenue. If the firm increases production, total revenue ________ and economic profit ________.

A)increases; increases

B)increases; decreases

C)decreases; decreases

D)decreases; increases

E)increases; remains unchanged

A)increases; increases

B)increases; decreases

C)decreases; decreases

D)decreases; increases

E)increases; remains unchanged

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

61

Use the figure below to answer the following question.

Figure 12.3.4

Refer to Figure 12.3.4, which shows cost curves of Paul's Picture Frames Inc.The picture frame market is perfectly competitive and the market price is $12 a frame.Paul produces ________ frames each week and makes ________ total revenue.

A)20; $240

B)20; $96

C)zero; zero

D)30; $360

E)30; zero

Figure 12.3.4

Refer to Figure 12.3.4, which shows cost curves of Paul's Picture Frames Inc.The picture frame market is perfectly competitive and the market price is $12 a frame.Paul produces ________ frames each week and makes ________ total revenue.

A)20; $240

B)20; $96

C)zero; zero

D)30; $360

E)30; zero

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

62

Use the figure below to answer the following question.

Figure 12.3.3

Refer to Figure 12.3.3, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)at its shutdown point.

E)larger than the other firms in the industry.

Figure 12.3.3

Refer to Figure 12.3.3, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)at its shutdown point.

E)larger than the other firms in the industry.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

63

Use the figure below to answer the following questions.

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, the firm will

A)exit from the industry.

B)break even.

C)make an economic profit.

D)incur an economic loss.

E)close down.

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, the firm will

A)exit from the industry.

B)break even.

C)make an economic profit.

D)incur an economic loss.

E)close down.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

64

Use the information below to answer the following questions.

Fact 12.2.1 Chevy Volt Production Temporarily Shut Down

GM will temporarily lay off 1,300 employees as the company stops production of the electric car, Chevy Volt, for five weeks. GM had hoped to sell 10,000 Volts last year, but ended up selling just 7,671. It plans to maintain inventory levels by adjusting production to match demand.

Source: Politico, March 2, 2012

Refer to Fact 12.2.1.The shutdown decision maximizes GM's economic profit (or minimizes its loss)when price is less than

A)average variable cost.

B)total variable cost.

C)average fixed cost.

D)total fixed cost.

E)average total cost.

Fact 12.2.1 Chevy Volt Production Temporarily Shut Down

GM will temporarily lay off 1,300 employees as the company stops production of the electric car, Chevy Volt, for five weeks. GM had hoped to sell 10,000 Volts last year, but ended up selling just 7,671. It plans to maintain inventory levels by adjusting production to match demand.

Source: Politico, March 2, 2012

Refer to Fact 12.2.1.The shutdown decision maximizes GM's economic profit (or minimizes its loss)when price is less than

A)average variable cost.

B)total variable cost.

C)average fixed cost.

D)total fixed cost.

E)average total cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

65

If a profit-maximizing firm in a perfectly competitive market is making an economic profit, then it must be producing a level of output where

A)price is greater than marginal cost.

B)price is greater than marginal revenue.

C)marginal cost is greater than marginal revenue.

D)marginal cost is greater than average total cost.

E)average total cost is greater than marginal cost.

A)price is greater than marginal cost.

B)price is greater than marginal revenue.

C)marginal cost is greater than marginal revenue.

D)marginal cost is greater than average total cost.

E)average total cost is greater than marginal cost.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

66

Use the figure below to answer the following question.

Figure 12.3.2

Refer to Figure 12.3.2, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry, The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)not maximizing economic profit.

E)going to close down temporarily.

Figure 12.3.2

Refer to Figure 12.3.2, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry, The firm is

A)making an economic profit.

B)incurring an economic loss.

C)breaking even.

D)not maximizing economic profit.

E)going to close down temporarily.

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

67

In which one of the following situations will a perfectly competitive firm make an economic profit?

A)MR > AVC

B)MR > ATC

C)ATC > MC

D)ATC > MR

E)MC > AVC

A)MR > AVC

B)MR > ATC

C)ATC > MC

D)ATC > MR

E)MC > AVC

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

68

In a perfectly competitive market, which of the following increases the price that the firms charge in the short run?

A)an increase in the number of firms

B)an increase in the price of a good that is a complement of the good produced in this market

C)an increase in market supply

D)a decrease in the price of a good that is a substitute for the good produced in this market

E)an increase in market demand

A)an increase in the number of firms

B)an increase in the price of a good that is a complement of the good produced in this market

C)an increase in market supply

D)a decrease in the price of a good that is a substitute for the good produced in this market

E)an increase in market demand

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

69

Use the figure below to answer the following question.

Figure 12.3.5

Refer to Figure 12.3.5, which shows the cost curves and the marginal revenue curve for a perfectly competitive firm.To maximize its profit, the firm produces ________ units of output and the price is ________ a unit.

A)30; $40

B)30; $30

C)20; $40

D)20; $30

E)30; $32.50

Figure 12.3.5

Refer to Figure 12.3.5, which shows the cost curves and the marginal revenue curve for a perfectly competitive firm.To maximize its profit, the firm produces ________ units of output and the price is ________ a unit.

A)30; $40

B)30; $30

C)20; $40

D)20; $30

E)30; $32.50

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

70

Use the figure below to answer the following questions.

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, if the market price of the good is $10, the firm produces ________ units of output and ________.

A)10; incurs an economic loss of $20

B)10; incurs an economic loss of $40

C)less than 10; incurs an economic loss of $20

D)10; makes an economic profit of $20

E)less than 10; incurs an economic loss of less than $20

Figure 12.3.1

Refer to Figure 12.3.1, which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run, if the market price of the good is $10, the firm produces ________ units of output and ________.

A)10; incurs an economic loss of $20

B)10; incurs an economic loss of $40

C)less than 10; incurs an economic loss of $20

D)10; makes an economic profit of $20

E)less than 10; incurs an economic loss of less than $20

Unlock Deck

Unlock for access to all 117 flashcards in this deck.

Unlock Deck

k this deck

71

Use the information below to answer the following questions.

Fact 12.2.1 Chevy Volt Production Temporarily Shut Down

GM will temporarily lay off 1,300 employees as the company stops production of the electric car, Chevy Volt, for five weeks. GM had hoped to sell 10,000 Volts last year, but ended up selling just 7,671. It plans to maintain inventory levels by adjusting production to match demand.

Source: Politico, March 2, 2012

Refer to Fact 12.2.1.The shutdown decision ________ total fixed cost and ________ total variable cost.

A)decreases; decreases

B)does not change; decreases

C)does not change; does not change

D)increases; does not change

E)does not change; increases

Fact 12.2.1 Chevy Volt Production Temporarily Shut Down