Deck 6: Commodity Forwards and Futures

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Table 6.1

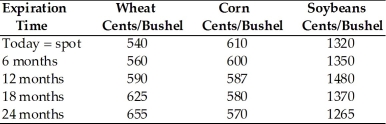

Refer to the table 6.1.If wheat farmers expect a return of 8.0% on their investment in wheat,what is the approximate implied increase in wheat commodity prices over the next 6 months?

A) 3.75%

B) 4.59%

C) 5.26%

D) 6.37%

Refer to the table 6.1.If wheat farmers expect a return of 8.0% on their investment in wheat,what is the approximate implied increase in wheat commodity prices over the next 6 months?

A) 3.75%

B) 4.59%

C) 5.26%

D) 6.37%

Question

Question

Table 6.1

Refer to the table 6.1.Given a lease rate of 7.0% on the 24-month corn forward contract,what is the approximate potential arbitrage profit per contract?

A) 3.68 cents

B) 4.48 cents

C) 5.84 cents

D) 6.90 cents

Refer to the table 6.1.Given a lease rate of 7.0% on the 24-month corn forward contract,what is the approximate potential arbitrage profit per contract?

A) 3.68 cents

B) 4.48 cents

C) 5.84 cents

D) 6.90 cents

Question

Table 6.1

Refer to the table 6.1.What is the approximate annualized lease rate on the 18-month soybean forward contract?

A) 0.69%

B) 1.52%

C) 2.69%

D) 3.31%

Refer to the table 6.1.What is the approximate annualized lease rate on the 18-month soybean forward contract?

A) 0.69%

B) 1.52%

C) 2.69%

D) 3.31%

Question

Question

Table 6.1

Refer to the table 6.1.Which of the following terms most accurately describes the forward curve for soybeans over the next two years?

A) Contango

B) Backwardation

C) Contango and backwardation

D) None of the above

Refer to the table 6.1.Which of the following terms most accurately describes the forward curve for soybeans over the next two years?

A) Contango

B) Backwardation

C) Contango and backwardation

D) None of the above

Question

Table 6.1

Refer to the table 6.1.What is the approximate annualized lease rate on the 12-month corn forward contract?

A) 0.00%

B) 2.25%

C) 3.92%

D) 7.84%

Refer to the table 6.1.What is the approximate annualized lease rate on the 12-month corn forward contract?

A) 0.00%

B) 2.25%

C) 3.92%

D) 7.84%

Question

Table 6.1

Refer to the table 6.1.The lease rate on the 6-month soybean contract is 0.35%.What is the implied annual storage cost if the cost is continuously paid and proportional?

A) 0.84%

B) 1.62%

C) 2.30%

D) 4.0%

Refer to the table 6.1.The lease rate on the 6-month soybean contract is 0.35%.What is the implied annual storage cost if the cost is continuously paid and proportional?

A) 0.84%

B) 1.62%

C) 2.30%

D) 4.0%

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/19

Play

Full screen (f)

Deck 6: Commodity Forwards and Futures

1

Forward prices for gold,in dollars per ounce,for the next five years are 1350,1400,1560,1675,and 1756,respectively.A mine can be opened for 3 years at a cost of $2,000.Annual mining costs are a constant $500 and interest rates are 5.0%.When should the mine be opened to maximize NPV?

A) Year 1

B) Year 2

C) Year 3

D) Never

A) Year 1

B) Year 2

C) Year 3

D) Never

C

2

The spot price of gasoline is 258 cents per gallon and the annualized risk free interest rate is 4.0%.Given a lease rate of 1.0%,a continuously paid storage rate of 0.5%,and a convenience yield of 0.75%,what is the no-arbitrage price range of a 1-year forward contract (in cents)?

A) 265.19 to 267.19

B) 258 to 265.19

C) 258 to 267.19

D) 247.16 to 265.19

A) 265.19 to 267.19

B) 258 to 265.19

C) 258 to 267.19

D) 247.16 to 265.19

A

3

Explain how a negative correlation between agricultural production and commodity prices creates a natural hedge.

The goal of hedging is to level the volatility in cash flows.The increased revenue,which accompanies higher output,will be offset by lower prices.Lower output and revenue,in turn,is offset by higher prices,thus,a natural hedge.

4

The 6-month futures price for oil is $96.60 per barrel (or 2.30 cents per gallon).The 6-month futures prices for gasoline and heating oil are 2.50 cents and 2.15 cents,respectively.What is the gross margin on a simple 3-2-1 crack spread?

A) $0.25

B) $0.35

C) $0.54

D) $0.68

A) $0.25

B) $0.35

C) $0.54

D) $0.68

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

5

Oil is selling at a spot price of $42.00 per barrel.Oil can be stored at a cost of $0.42 per barrel per month.The opportunity cost of capital is 7.2% per year (or 0.6% per month).What is the gain or loss realized by an oil refinery that floats its exposure and purchases oil on the spot market in 2 months at a price of $43.00 per barrel,instead of hedging with a forward contract?

A) $0.35 gain

B) $0.35 loss

C) $1.00 gain

D) $1.00 loss

A) $0.35 gain

B) $0.35 loss

C) $1.00 gain

D) $1.00 loss

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

6

Give one example of how price discovery functions in the commodity futures market.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

7

The spot price of corn is $5.85 per bushel.The opportunity cost of capital for an investor is 0.5% per month.If storage costs of $0.04 per bushel per month are factored in,all else being equal,what is the likely price of a 4-month forward contract?

A) $5.808

B) $5.736

C) $5.968

D) $6.006

A) $5.808

B) $5.736

C) $5.968

D) $6.006

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

8

Table 6.1

Refer to the table 6.1.If wheat farmers expect a return of 8.0% on their investment in wheat,what is the approximate implied increase in wheat commodity prices over the next 6 months?

A) 3.75%

B) 4.59%

C) 5.26%

D) 6.37%

Refer to the table 6.1.If wheat farmers expect a return of 8.0% on their investment in wheat,what is the approximate implied increase in wheat commodity prices over the next 6 months?

A) 3.75%

B) 4.59%

C) 5.26%

D) 6.37%

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

9

The spot price of corn is $5.82 per bushel.The opportunity cost of capital for an investor is 0.6% per month.If storage costs of $0.03 per bushel per month are factored in,all else being equal,what is the future value of storage costs over a 6-month period?

A) $0.1534

B) $0.1684

C) $0.1772

D) $0.1827

A) $0.1534

B) $0.1684

C) $0.1772

D) $0.1827

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

10

Table 6.1

Refer to the table 6.1.Given a lease rate of 7.0% on the 24-month corn forward contract,what is the approximate potential arbitrage profit per contract?

A) 3.68 cents

B) 4.48 cents

C) 5.84 cents

D) 6.90 cents

Refer to the table 6.1.Given a lease rate of 7.0% on the 24-month corn forward contract,what is the approximate potential arbitrage profit per contract?

A) 3.68 cents

B) 4.48 cents

C) 5.84 cents

D) 6.90 cents

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

11

Table 6.1

Refer to the table 6.1.What is the approximate annualized lease rate on the 18-month soybean forward contract?

A) 0.69%

B) 1.52%

C) 2.69%

D) 3.31%

Refer to the table 6.1.What is the approximate annualized lease rate on the 18-month soybean forward contract?

A) 0.69%

B) 1.52%

C) 2.69%

D) 3.31%

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

12

What function does the convenience yield serve in setting forward prices and how does this influence arbitrage opportunities?

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

13

Table 6.1

Refer to the table 6.1.Which of the following terms most accurately describes the forward curve for soybeans over the next two years?

A) Contango

B) Backwardation

C) Contango and backwardation

D) None of the above

Refer to the table 6.1.Which of the following terms most accurately describes the forward curve for soybeans over the next two years?

A) Contango

B) Backwardation

C) Contango and backwardation

D) None of the above

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

14

Table 6.1

Refer to the table 6.1.What is the approximate annualized lease rate on the 12-month corn forward contract?

A) 0.00%

B) 2.25%

C) 3.92%

D) 7.84%

Refer to the table 6.1.What is the approximate annualized lease rate on the 12-month corn forward contract?

A) 0.00%

B) 2.25%

C) 3.92%

D) 7.84%

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

15

Table 6.1

Refer to the table 6.1.The lease rate on the 6-month soybean contract is 0.35%.What is the implied annual storage cost if the cost is continuously paid and proportional?

A) 0.84%

B) 1.62%

C) 2.30%

D) 4.0%

Refer to the table 6.1.The lease rate on the 6-month soybean contract is 0.35%.What is the implied annual storage cost if the cost is continuously paid and proportional?

A) 0.84%

B) 1.62%

C) 2.30%

D) 4.0%

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

16

When is it possible for the lease rate to fall below zero?

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

17

A review of seasonality forward curves may lead students to adopt a technical analysis mentality.Ask students to explain why such ideas may pop into their heads.Proceed to inquire as to why the curves have the appearances they do.An actual numerical example may be in order.If any still hold fast to their technical roots,insist that they show the profit numerically after considering all storage and other costs.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

18

Why is the cash-and-carry strategy employed in the financial futures market not readily available in the commodity futures market?

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

19

Nine-month gold futures are trading for $1565 per ounce.The spot price is $1509 per ounce.LIBOR during each of the upcoming 4 quarters is listed as 1.04%,1.22%,1.30%,and 1.35%,respectively.Calculate the 9-month lease rate on the futures contract.

A) 2.4%

B) 2.1%

C) 1.3%

D) 0.0%

A) 2.4%

B) 2.1%

C) 1.3%

D) 0.0%

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 19 flashcards in this deck.