Deck 14: Perfectly Competitive Markets: Short-Run Analysis

Full screen (f)

Question

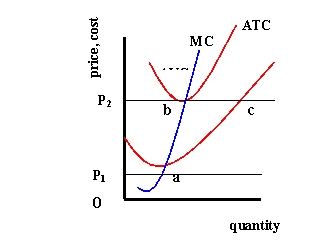

Refer to Exhibit 14-1. Which point represents an optimal quantity?

A) a

B) b

C) c

Question

Question

Question

Question

Refer to Exhibit 14.2. If the market price is $26, what quantity should the firm produce in order to maximize profits.

A) 5

B) 0

C) 26

Question

Question

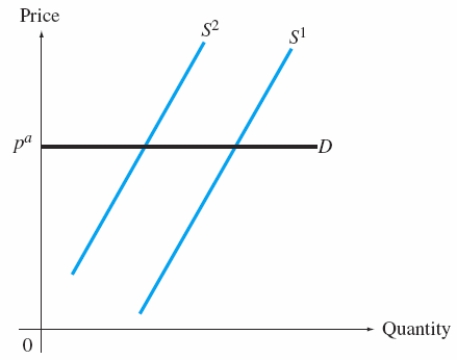

Refer to Exhibit 14-4. At which price will there be excess supply?

A) p1

B) pe

C) p2

Question

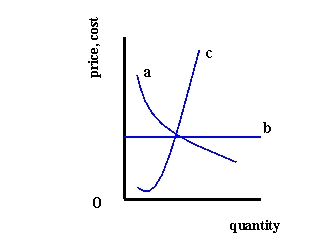

Refer to Exhibit 14-3. Which curve is most likely to be a supply curve for a perfectly competitive firm?

A) a

B) b

C) c

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Refer to Exhibit 14-1. Which point shows where the firm should produce zero output?

A) a

B) b

C) c

Question

Question

Question

Refer to Exhibit 14-4. At which price will there be excess demand?

A) p1

B) pe

C) p2

Question

Question

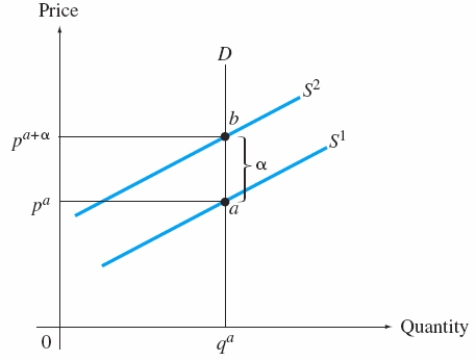

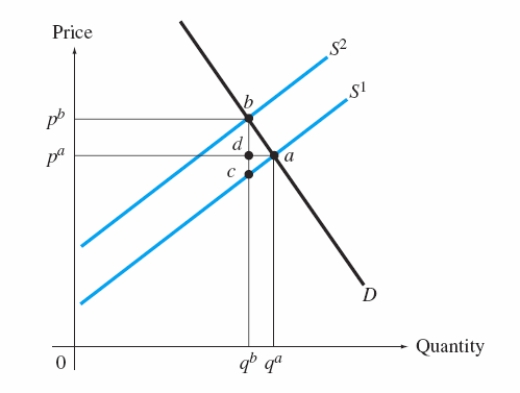

Refer to Exhibit 14-5. In such a market, on whom does the tax incidence fall?

A) both consumers and producers

B) producers only

C) consumers only

Question

Refer to Exhibit 14-7. In such a market, on whom does the tax incidence fall?

A) both consumers and producers

B) producers only

C) consumers only

Question

Question

Question

Question

Question

Question

Question

Refer to Exhibit 14-4. At which price will there be equilibrium?

A) p1

B) pe

C) p2

Question

Question

Refer to Exhibit 14-6. In such a market, on whom does the tax incidence fall?

A) both consumers and producers

B) producers only

C) consumers only

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/40

Play

Full screen (f)

Deck 14: Perfectly Competitive Markets: Short-Run Analysis

1

Refer to Exhibit 14-1. Which point represents an optimal quantity?

A) a

B) b

C) c

b

2

Provided that the market price is greater than AVC, the profit-maximizing quantity for a competitive firm to set in the short run is that quantity at which the price received __________________ the marginal cost of production.

A) is equal to

B) is greater than

C) is less than

A) is equal to

B) is greater than

C) is less than

is equal to

3

A government wage subsidy cannot rise indefinitely.

True

4

For prices above the lowest point on the AVC curve, the supply curve for a perfectly competitive firm corresponds to the firm's

A) MC curve

B) AVC curve

C) ATC curve

A) MC curve

B) AVC curve

C) ATC curve

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

5

Refer to Exhibit 14.2. If the market price is $26, what quantity should the firm produce in order to maximize profits.

A) 5

B) 0

C) 26

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

6

Tax incidence is the ultimate distribution of the benefits of a tax.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

7

Refer to Exhibit 14-4. At which price will there be excess supply?

A) p1

B) pe

C) p2

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

8

Refer to Exhibit 14-3. Which curve is most likely to be a supply curve for a perfectly competitive firm?

A) a

B) b

C) c

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

9

The market supply curve is derived by _______________ adding the supply curves of all the firms in the industry.

A) horizontally

B) diagonally

C) vertically

A) horizontally

B) diagonally

C) vertically

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

10

A market supply function (aggregate supply function) tells us how much of a product all of the firms in an industry will supply at any given market price.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

11

In a comparative static analysis, the economist examines the equilibrium of the market before and after a policy change to see the effect of the change on the market price and quantity.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

12

Perfectly competitive firms must take the market price as

A) given

B) being randomly determined

C) whatever the firms want it to be

A) given

B) being randomly determined

C) whatever the firms want it to be

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

13

A law that prescribes a floor below which wages cannot fall is known as a maximum wage law.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

14

An analysis in which the economist examines the path that the market will follow in moving from one equilibrium to another is known as dynamic analysis.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

15

The profit-maximizing quantity for a competitive firm to set in the short run is that quantity at which the price received equals the marginal cost of production, provided that this price is greater than the average variable cost of production.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

16

The price-quantity combination that will prevail in a perfectly competitive market in the short run is called short-run equilibrium.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

17

The major characteristic of perfectly competitive markets is that, in these markets, firms are large enough to change the price of the good on the market.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

18

A supply function specifies how much of a good a firm would be willing to sell given any hypothetical market price if all other factors remain constant.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

19

In the short run, the price that the firm receives must cover its average ___________ cost, but not necessarily its average ___________ cost.

A) variable, total

B) variable, marginal

C) total, variable

A) variable, total

B) variable, marginal

C) total, variable

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

20

Refer to Exhibit 14-1. Which point shows where the firm should produce zero output?

A) a

B) b

C) c

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

21

In general, the _______ elastic the demand for a product being taxed, the _______ the incidence of the tax will fall on the consumers.

A) more, more

B) more, less

C) less, less

A) more, more

B) more, less

C) less, less

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

22

If the demand curve for illegal drugs shifts to the left, then drug enforcement most likely is targeting

A) growers in foreign countries

B) dealers

C) users

A) growers in foreign countries

B) dealers

C) users

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

23

Refer to Exhibit 14-4. At which price will there be excess demand?

A) p1

B) pe

C) p2

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

24

What does a market supply curve reveal about costs?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

25

Refer to Exhibit 14-5. In such a market, on whom does the tax incidence fall?

A) both consumers and producers

B) producers only

C) consumers only

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

26

Refer to Exhibit 14-7. In such a market, on whom does the tax incidence fall?

A) both consumers and producers

B) producers only

C) consumers only

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

27

Explain why a perfectly competitive firm would produce at a price that is greater than average variable cost but less than average total cost.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

28

Do you favor minimum wage laws or government-subsidized wages? Why?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

29

When goverment sets a price ceiling in a market, government establishes a __________ price.

A) maximum

B) minimum

C) Neither answer is correct

A) maximum

B) minimum

C) Neither answer is correct

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

30

A government subsidy of wages will shift the demand curve for labor to the

A) left

B) right

C) The direction of the shift depends on the size of the subsidy

A) left

B) right

C) The direction of the shift depends on the size of the subsidy

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

31

Assuming that labor demand is downward-sloping, a minimum wage set above the equilibrium wage will cause the number of workers to

A) increase

B) stay unchanged

C) decrease

A) increase

B) stay unchanged

C) decrease

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

32

When government sets a price floor in a market, government establishes a __________ price.

A) maximum

B) minimum

C) Neither answer is correct

A) maximum

B) minimum

C) Neither answer is correct

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

33

Refer to Exhibit 14-4. At which price will there be equilibrium?

A) p1

B) pe

C) p2

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

34

Government can affect the working of a market by

A) the way in which it enforces laws

B) imposing taxes

C) Both answers are correct

A) the way in which it enforces laws

B) imposing taxes

C) Both answers are correct

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

35

Refer to Exhibit 14-6. In such a market, on whom does the tax incidence fall?

A) both consumers and producers

B) producers only

C) consumers only

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

36

In a market for illegal drugs, the supply curve represents the profit-maximizing decisions of the

A) dealers

B) police

C) users

A) dealers

B) police

C) users

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

37

When is a tougher drug enforcement policy beneficial to society on the whole?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

38

An increase in government drug enforcement targeted at dealers will cause the supply curve to

A) not shift at all

B) shift to the left

C) shift to the right

A) not shift at all

B) shift to the left

C) shift to the right

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

39

In the short run, can a perfectly competitive firm earn an extra-normal profit?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

40

When firms face an upward-sloping labor supply curve, increases in the minimum wage

A) may even increase employment

B) will always decrease employment

C) will alter the elasticity of labor demand

A) may even increase employment

B) will always decrease employment

C) will alter the elasticity of labor demand

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 40 flashcards in this deck.