Deck 3: Audit Reports

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

To emphasize the fact that the auditor is independent, a typical addressee of the audit report could be

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

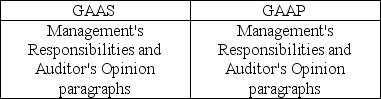

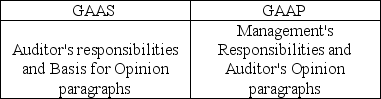

The standard audit report for nonpublic entities refers to GAAS and GAAP in which sections?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

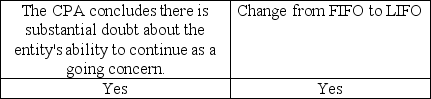

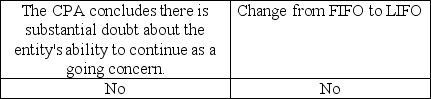

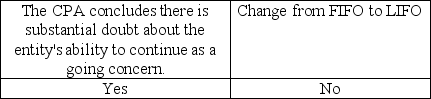

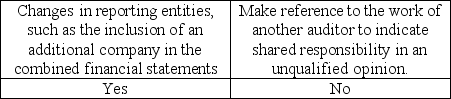

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

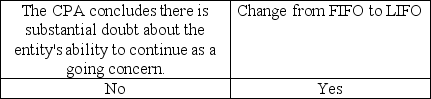

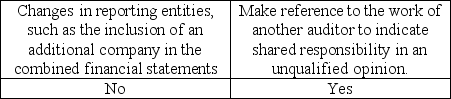

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

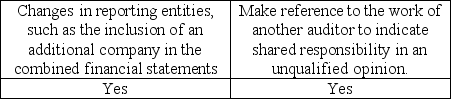

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

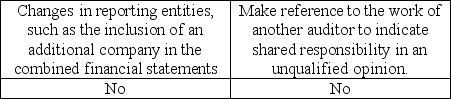

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/170

Play

Full screen (f)

Deck 3: Audit Reports

1

If the balance sheet of a private company is dated December 31, 2018, the audit report is dated February 8, 2019, and both are released on February 15, 2019, this indicates that the auditor has searched for subsequent events that occurred up to

A) December 31, 2018.

B) January 1, 2019.

C) February 8, 2019.

D) February 15, 2019.

A) December 31, 2018.

B) January 1, 2019.

C) February 8, 2019.

D) February 15, 2019.

C

2

The audit report date on a standard unmodified opinion audit report indicates

A) the last day of the fiscal period.

B) the date on which the financial statements were filed with the Securities and Exchange Commission.

C) the last date on which users may institute a lawsuit against either the client or the auditor.

D) the last day of the auditor's responsibility for the review of significant events that occurred after the date of the financial statements.

A) the last day of the fiscal period.

B) the date on which the financial statements were filed with the Securities and Exchange Commission.

C) the last date on which users may institute a lawsuit against either the client or the auditor.

D) the last day of the auditor's responsibility for the review of significant events that occurred after the date of the financial statements.

D

3

AICPA auditing standards provide uniform wording for the auditor's report to enable users of the financial statements to understand the audit report.

True

4

The auditor's opinion paragraph of the auditor's report states that the auditor is responsible for the preparation, presentation and opinion on the financial statements.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

5

Users of the financial statements rely on the auditor's report because of the absolute assurance the report provides.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

6

The management's responsibilities section of the standard unmodified opinion audit report for a nonpublic company states that the financial statements are

A) the responsibility of the auditor.

B) the responsibility of management.

C) the joint responsibility of management and the auditor.

D) none of the above.

A) the responsibility of the auditor.

B) the responsibility of management.

C) the joint responsibility of management and the auditor.

D) none of the above.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

7

To emphasize the fact that the auditor is independent, a typical addressee of the audit report could be

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

8

The appropriate audit report date for a standard unmodified opinion audit report for a nonpublic entity should be

A) the date the financial statements are given to the Board of Directors.

B) the date of the financial statements.

C) the date the auditor completed the auditing procedures in the field.

D) 60 days after the date of the financial statements as required by the SEC.

A) the date the financial statements are given to the Board of Directors.

B) the date of the financial statements.

C) the date the auditor completed the auditing procedures in the field.

D) 60 days after the date of the financial statements as required by the SEC.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

9

The standard audit report for nonpublic entities refers to GAAS and GAAP in which sections?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

10

The auditor's responsibilities section of the standard unmodified opinion audit report states that the audit is designed to

A) discover all errors and/or irregularities.

B) discover material errors and/or irregularities.

C) conform to generally accepted accounting principles.

D) obtain reasonable assurance whether the statements are free of material misstatement.

A) discover all errors and/or irregularities.

B) discover material errors and/or irregularities.

C) conform to generally accepted accounting principles.

D) obtain reasonable assurance whether the statements are free of material misstatement.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

11

Auditing standards require that the audit report must be titled and that the title must

A) include the word "independent."

B) indicate if the auditor is a CPA.

C) indicate if the auditor is a proprietorship, partnership, or corporation.

D) indicate the type of audit opinion issued.

A) include the word "independent."

B) indicate if the auditor is a CPA.

C) indicate if the auditor is a proprietorship, partnership, or corporation.

D) indicate the type of audit opinion issued.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

12

Most auditors believe that financial statements are "presented fairly" when the statements are in accordance with GAAP, and that it is also necessary to

A) determine that they are not in violation of FASB statements.

B) examine the substance of transactions and balances for possible misinformation.

C) review the statements using the accounting principles promulgated by the SEC.

D) assure investors that net income reported this year will be exceeded in the future.

A) determine that they are not in violation of FASB statements.

B) examine the substance of transactions and balances for possible misinformation.

C) review the statements using the accounting principles promulgated by the SEC.

D) assure investors that net income reported this year will be exceeded in the future.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

13

The auditor's responsibilities section of the standard unmodified opinion audit report states that the auditor is

A) responsible for the financial statements and the opinion on them.

B) responsible for the financial statements.

C) exercising professional judgment throughout the audit.

D) expressing an opinion on the effectiveness of internal controls.

A) responsible for the financial statements and the opinion on them.

B) responsible for the financial statements.

C) exercising professional judgment throughout the audit.

D) expressing an opinion on the effectiveness of internal controls.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is not explicitly stated in the standard unmodified opinion audit report?

A) The financial statements are the responsibility of management.

B) The audit was conducted in accordance with generally accepted accounting principles.

C) The auditors believe that the audit evidence provides a reasonable basis for their opinion.

D) An audit includes assessing the accounting estimates used.

A) The financial statements are the responsibility of management.

B) The audit was conducted in accordance with generally accepted accounting principles.

C) The auditors believe that the audit evidence provides a reasonable basis for their opinion.

D) An audit includes assessing the accounting estimates used.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

15

The audit report date is the date the auditor completed audit procedures in the field.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is a correct statement regarding the standard unmodified opinion audit report?

A) The format of the audit report for public and nonpublic entities are identical.

B) The auditor's responsibility paragraph includes a statement that the auditors are responsible for selecting the appropriate accounting principles.

C) The audit report includes the name of the lead partner on the audit.

D) The auditor's responsibilities paragraph includes a statement that the auditor considers internal controls when designing the audit procedures performed.

A) The format of the audit report for public and nonpublic entities are identical.

B) The auditor's responsibility paragraph includes a statement that the auditors are responsible for selecting the appropriate accounting principles.

C) The audit report includes the name of the lead partner on the audit.

D) The auditor's responsibilities paragraph includes a statement that the auditor considers internal controls when designing the audit procedures performed.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

17

The standard unmodified opinion audit report for a nonpublic entity must

A) have a report title that includes the word "CPA."

B) be addressed to the company's stockholders and creditors.

C) be dated.

D) include an explanatory paragraph.

A) have a report title that includes the word "CPA."

B) be addressed to the company's stockholders and creditors.

C) be dated.

D) include an explanatory paragraph.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

18

An audit provides a guarantee that a material misstatement will not exist in the financial statements.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following statements are true for the standard unmodified opinion audit report of a nonpublic entity for fiscal years ending on or after June 15, 2019?

I) The management's responsibilities paragraph states that management is responsible for the preparation and the fair presentation of the financial statements.

II) The opinion paragraph is stated as a statement of absolute fact and a guarantee by the auditor.

A) I only

B) II only

C) I and II

D) Neither I nor II

I) The management's responsibilities paragraph states that management is responsible for the preparation and the fair presentation of the financial statements.

II) The opinion paragraph is stated as a statement of absolute fact and a guarantee by the auditor.

A) I only

B) II only

C) I and II

D) Neither I nor II

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

20

The first paragraph of the standard unmodified opinion audit report for a nonpublic company effective for audits of financial statements for fiscal years ending on or after June 15, 2019 performs which of the following functions?

I) Presents the auditors' opinion, first.

II) Provides additional information related to the responsibilities of management for preparing the financial statements.

III) Provides additional information regarding the responsibilities of the auditor in conducting the audit.

A) I only

B) I and II

C) II and III

D) I and III

I) Presents the auditors' opinion, first.

II) Provides additional information related to the responsibilities of management for preparing the financial statements.

III) Provides additional information regarding the responsibilities of the auditor in conducting the audit.

A) I only

B) I and II

C) II and III

D) I and III

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

21

The European Union has not yet implemented requirements for mandatory audit rendering and auditor rotation despite many years of debate on this subject.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

22

EPM, Inc., is a publicly listed manufacturing company with a calendar year-end. Their financial statements include a balance sheet, a statement of income, statement of cash flows, and statement of stockholders' equity. For the most recent audit, Harrington and Perry, LLP, from Denver, Colorado, audited the 2018 and 2019 financial statements. The auditors completed all significant fieldwork on March 5, 2020 and issued the audit report on March 16, 2020.

Required:

Consider all the facts given and write the PCAOBs new standard unmodified opinion audit report.

Required:

Consider all the facts given and write the PCAOBs new standard unmodified opinion audit report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

23

An audit of historical financial statements most commonly includes the

A) balance sheet, statement of retained earnings, and the statement of cash flows.

B) income statement, the statement of cash flows, and the statement of net working capital.

C) statement of cash flows, balance sheet, and the statement of retained earnings.

D) balance sheet, income statement, statement of cash flows, and the statement of changes in stockholders' equity.

A) balance sheet, statement of retained earnings, and the statement of cash flows.

B) income statement, the statement of cash flows, and the statement of net working capital.

C) statement of cash flows, balance sheet, and the statement of retained earnings.

D) balance sheet, income statement, statement of cash flows, and the statement of changes in stockholders' equity.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

24

The basis of opinion section of the audit report issued for financial statements of a nonpublic company should refer to auditing standards generally accepted in the United States of America.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

25

The phrase "auditing standards generally accepted in the United States of America" can be found in the auditor's opinion paragraph of a standard unmodified opinion report for a nonpublic company.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

26

The date of the auditor's report is indicative of the last day of the auditor's responsibility for the review of significant events occurring after the balance sheet date.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

27

The PCAOB and the AICPA recently adopted new auditor reporting standards which are designed to make the standard audit report less informative for users.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

28

Financial statement users are normally much more concerned about a disclaimer than an unmodified opinion audit report that contains an additional emphasis-of-matter paragraph.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

29

The phrase "Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material error" is included in the auditor's opinion section of an audit report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

30

When analyzing the various types of audit reports,

A) the unmodified opinion with an emphasis-of-matter paragraph is the most common type of report.

B) companies will generally make the appropriate changes to their accounting records to avoid a qualification by the auditor.

C) management is more concerned about a qualified report than a disclaimer report.

D) an adverse report is issued when the auditor is unable to form an opinion on the financial statements.

A) the unmodified opinion with an emphasis-of-matter paragraph is the most common type of report.

B) companies will generally make the appropriate changes to their accounting records to avoid a qualification by the auditor.

C) management is more concerned about a qualified report than a disclaimer report.

D) an adverse report is issued when the auditor is unable to form an opinion on the financial statements.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

31

There are four conditions that must be met before an auditor can issue a standard unmodified opinion audit report for the audit of a private company. Please discuss each of these four conditions.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

32

An auditor will issue a disclaimer when he or she concludes that the financial statements are not fairly presented.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

33

Whenever an auditor issues an audit report for a public company, the auditor can choose to issue a report in which of the following forms?

I) A combined report on financial statements and internal control over financial reporting

II) Separate reports on financial statements and internal control over financial reporting

A) I only

B) II only

C) either I or II

D) neither I nor II

I) A combined report on financial statements and internal control over financial reporting

II) Separate reports on financial statements and internal control over financial reporting

A) I only

B) II only

C) either I or II

D) neither I nor II

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

34

Describe the standard unmodified opinion audit report to be issued for an audit of a private company issued for fiscal years ending on or after June 15, 2019. Begin by specifying the eight parts of the report, and then discuss the contents of each part.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

35

The phrase "accounting principles generally accepted in the United States of America" can be found in the auditor's opinion paragraph of a standard unmodified opinion report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

36

In the auditor's responsibilities paragraph of the audit report issued for financial statements of a nonpublic company, the auditor expresses an opinion about the internal controls of the company.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

37

What category of audit report will be issued if the auditor concludes that the financial statements are not fairly presented?

A) disclaimer

B) qualified

C) standard unmodified opinion

D) adverse

A) disclaimer

B) qualified

C) standard unmodified opinion

D) adverse

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

38

The standard unmodified audit report

A) is sometimes called a clean opinion.

B) can be issued only with an explanatory paragraph.

C) can be issued if only a balance sheet and income statement are included in the financial statements.

D) is sometimes called a disclaimer report.

A) is sometimes called a clean opinion.

B) can be issued only with an explanatory paragraph.

C) can be issued if only a balance sheet and income statement are included in the financial statements.

D) is sometimes called a disclaimer report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

39

The Auditing Standards Board (ASB) sets auditing standards in the U.S. for nonpublic entities.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

40

The audit report is normally addressed to the company's president or chief executive officer.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

41

The PCAOB expects that in most audits, the auditor will determine that at least one matter involved especially challenging, subjective, or complex auditor judgment.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

42

The unqualified opinion audit report for public entities includes which of the following sections and/or paragraphs?

A) report title, address, and opinion

B) basis for opinion and discussion of critical audit areas

C) auditor information and date

D) All of the above are included.

A) report title, address, and opinion

B) basis for opinion and discussion of critical audit areas

C) auditor information and date

D) All of the above are included.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

43

Examples of unmodified opinions which contain modified wording (without adding an emphasis-of-matter paragraph) include

A) reports involving other auditors.

B) the lack of consistent application of generally accepted accounting principles.

C) substantial doubt about the audited company (or the entity) continuing as a going concern.

D) lack of consistent application of GAAP.

A) reports involving other auditors.

B) the lack of consistent application of generally accepted accounting principles.

C) substantial doubt about the audited company (or the entity) continuing as a going concern.

D) lack of consistent application of GAAP.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

44

Auditors of public company financial statements must issue separate reports on internal control over financial reporting.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

45

The separate report on internal control over financial reporting

A) cannot contain a cross-reference to the auditor's report on the financial statements.

B) includes a paragraph that addresses the inherent limitations of internal controls.

C) is addressed to the PCAOB.

D) includes a scope paragraph which refers to the framework used to evaluate internal controls.

A) cannot contain a cross-reference to the auditor's report on the financial statements.

B) includes a paragraph that addresses the inherent limitations of internal controls.

C) is addressed to the PCAOB.

D) includes a scope paragraph which refers to the framework used to evaluate internal controls.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

46

The critical audit matters section of the auditor's report notes that this communication of critical audit matters alters the auditor's opinion on the financial statements.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

47

PCAOB standards use the term "unqualified opinion" to refer to the standard unmodified opinion audit report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

48

PCAOB auditing standards require the disclosure of the audit engagement partner's name and other accounting firms participating in the audit engagement in the audit report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

49

The critical audit matters section of the audit report is required for audits of fiscal years ending on or after June 30, 2019 for large companies, and fiscal years ending on or after December 31, 2020 for all other audits to which these requirements apply.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

50

PCAOB audit report requirements require the auditor to include the auditor's signature, tenure, city and state where the audit firm is located, as well as the audit report date.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

51

If the auditor concludes there are no critical audit matters, the auditor is not required to disclose this fact in the audit report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

52

If the auditor also issues a separate report on internal control over financial reporting for a public company, the additional paragraph following the opinion paragraph is included to reference the audit report on internal control.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

53

All of the following are causes for the addition of an emphasis of a matter paragraph under both AICPA and PCAOB standards except for

A) emphasis of a matter.

B) reports involving other auditors.

C) lack of consistent application of generally accepted accounting principles.

D) auditor agrees with a departure from promulgated accounting principles.

A) emphasis of a matter.

B) reports involving other auditors.

C) lack of consistent application of generally accepted accounting principles.

D) auditor agrees with a departure from promulgated accounting principles.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

54

With regards to critical audit matters as defined by the PCAOB, the auditor would likely consider what type(s) of issues that involved "especially challenging, subjective, or complex auditor judgment" matters?

Name at least three specific matters.

Name at least three specific matters.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

55

Similar to AICPA standards, the new PCAOB standard requires the auditor to disclose critical audit matters in the auditor's report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

56

Under PCAOB standards,

A) the standard unmodified opinion audit report is referred to as an unqualified opinion audit report.

B) the scope paragraph states that the financial statements are the responsibility of management.

C) internal controls of a public company must be audited every five years.

D) the scope paragraph is the same as the scope paragraph for private companies.

A) the standard unmodified opinion audit report is referred to as an unqualified opinion audit report.

B) the scope paragraph states that the financial statements are the responsibility of management.

C) internal controls of a public company must be audited every five years.

D) the scope paragraph is the same as the scope paragraph for private companies.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

57

A CPA may wish to emphasize specific matters regarding the financial statements even though an unqualified opinion will be issued. Normally, such explanatory information is

A) included in the scope paragraph.

B) included in the opinion paragraph.

C) included in a separate paragraph in the report.

D) included in the introductory paragraph.

A) included in the scope paragraph.

B) included in the opinion paragraph.

C) included in a separate paragraph in the report.

D) included in the introductory paragraph.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

58

The basis for opinion paragraph of the audit report for a public company is worded exactly the same as the basis for opinion section for a U.S. nonpublic company.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

59

Section 404(b) of the Sarbanes Oxley Act requires that the auditor of a public company attest to management's report on the efficiency of internal controls over financial reporting.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

60

Auditing standards for public companies are established by the

A) SEC.

B) FASB.

C) PCAOB.

D) IRS.

A) SEC.

B) FASB.

C) PCAOB.

D) IRS.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

61

When a company's financial statements contain a departure from GAAP with which the auditor concurs, the departure should be explained in

A) the scope paragraph.

B) an introductory paragraph.

C) the opinion paragraph.

D) a separate paragraph.

A) the scope paragraph.

B) an introductory paragraph.

C) the opinion paragraph.

D) a separate paragraph.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

62

A company has changed its method of inventory valuation from an unacceptable one to one in conformity with generally accepted accounting principles. The auditor's report on the financial statements of the year of the change should include

A) no reference to consistency.

B) a reference to a prior period adjustment in the opinion paragraph.

C) an explanatory paragraph that justifies the change and explains the impact of the change on reported net income.

D) an explanatory paragraph explaining the change.

A) no reference to consistency.

B) a reference to a prior period adjustment in the opinion paragraph.

C) an explanatory paragraph that justifies the change and explains the impact of the change on reported net income.

D) an explanatory paragraph explaining the change.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

63

All of the following would require an emphasis of matter paragraph except for

A) the existence of material related party transactions.

B) the lack of auditor independence.

C) important events occurring subsequent to the balance sheet date.

D) material uncertainties disclosed in the footnotes.

A) the existence of material related party transactions.

B) the lack of auditor independence.

C) important events occurring subsequent to the balance sheet date.

D) material uncertainties disclosed in the footnotes.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

64

No reference is made in the auditor's report to other auditors who perform a portion of the audit when I. the other auditor audited an immaterial portion of the audit.

II) the other auditor is well known or closely supervised by the principle auditor.

III) the principle auditor has thoroughly reviewed the work of the other auditor.

A) I and II

B) I and III

C) II and III

D) I, II and III

II) the other auditor is well known or closely supervised by the principle auditor.

III) the principle auditor has thoroughly reviewed the work of the other auditor.

A) I and II

B) I and III

C) II and III

D) I, II and III

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

65

When there is uncertainty about a company's ability to continue as a going concern, the auditor's concern is the possibility that the client may not be able to continue its operations or meet its obligations for a "reasonable period of time." For this purpose, a reasonable period of time is considered not to exceed

A) six months from the date of the financial statements.

B) one year from the date of the financial statements.

C) six months from the date of the audit report.

D) one year from the date of the audit report.

A) six months from the date of the financial statements.

B) one year from the date of the financial statements.

C) six months from the date of the audit report.

D) one year from the date of the audit report.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

66

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is least likely to cause uncertainty about the ability of an entity to continue as a going concern?

A) The entity is suing a competitor for a minor patent infringement.

B) The entity has lost a major customer.

C) The entity has significant recurring operating losses.

D) The entity has working capital deficiencies.

A) The entity is suing a competitor for a minor patent infringement.

B) The entity has lost a major customer.

C) The entity has significant recurring operating losses.

D) The entity has working capital deficiencies.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

68

When an auditor is trying to determine how changes can affect consistency and/or comparability, he or she should keep in mind that

A) changes that affect comparability but not consistency require an explanatory paragraph.

B) items that materially affect the comparability of financial statements requires a disclaimer of opinion.

C) changes that affect consistency require an explanatory paragraph if they are material.

D) changes that involve either comparability or consistency only need to be mentioned in the footnotes.

A) changes that affect comparability but not consistency require an explanatory paragraph.

B) items that materially affect the comparability of financial statements requires a disclaimer of opinion.

C) changes that affect consistency require an explanatory paragraph if they are material.

D) changes that involve either comparability or consistency only need to be mentioned in the footnotes.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

69

The term "explanatory paragraph" was replaced in the AICPA auditing standards with

A) going concern paragraph.

B) emphasis-of-matter paragraph.

C) departure from principles paragraph.

D) consistency paragraph.

A) going concern paragraph.

B) emphasis-of-matter paragraph.

C) departure from principles paragraph.

D) consistency paragraph.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following requires recognition in the auditor's opinion as to consistency?

A) the correction of an error in the prior year's financial statements resulting from a mathematical mistake in capitalizing interest

B) a change in the estimate of provisions for warranty costs

C) the change from the cost method to the equity method of accounting for investments in common stock

D) a change in depreciation method which has no effect on current year's financial statements but is certain to affect future years

A) the correction of an error in the prior year's financial statements resulting from a mathematical mistake in capitalizing interest

B) a change in the estimate of provisions for warranty costs

C) the change from the cost method to the equity method of accounting for investments in common stock

D) a change in depreciation method which has no effect on current year's financial statements but is certain to affect future years

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

71

When there is a lack of consistent application in accounting principles,

A) the nature and impact of the change should be adequately disclosed.

B) the auditor should discuss the nature of the change and point the reader to the footnote that discusses the change.

C) the materiality of the change is evaluated based on the current year effect of the change.

D) all of the above.

A) the nature and impact of the change should be adequately disclosed.

B) the auditor should discuss the nature of the change and point the reader to the footnote that discusses the change.

C) the materiality of the change is evaluated based on the current year effect of the change.

D) all of the above.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is false concerning the principal CPA firm's alternatives when issuing a report when another CPA firm performs part of the audit?

A) Issue a joint report signed by both CPA firms.

B) Make no reference to the other CPA firm in the audit report, and issue the standard unqualified opinion.

C) Make reference to the other auditor in the report by using modified wording (a shared opinion or report).

D) A qualified opinion or disclaimer, depending on materiality, is required if the principal auditor is not willing to assume any responsibility for the work of the other auditor.

A) Issue a joint report signed by both CPA firms.

B) Make no reference to the other CPA firm in the audit report, and issue the standard unqualified opinion.

C) Make reference to the other auditor in the report by using modified wording (a shared opinion or report).

D) A qualified opinion or disclaimer, depending on materiality, is required if the principal auditor is not willing to assume any responsibility for the work of the other auditor.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

73

William Gregory, CPA, is the principal auditor for an international corporation. Another CPA has examined and reported on the financial statements of a significant subsidiary of the corporation. Gregory is satisfied with the independence and professional reputation of the other auditor, as well as the quality of the other auditor's examination. With respect to his report on the consolidated financial statements, taken as a whole, Gregory

A) must not refer to the examination of the other auditor.

B) must refer to the examination of the other auditor.

C) may refer to the examination of the other auditor.

D) must refer to the examination of the other auditors along with the percentage of consolidated assets and revenue that they audited.

A) must not refer to the examination of the other auditor.

B) must refer to the examination of the other auditor.

C) may refer to the examination of the other auditor.

D) must refer to the examination of the other auditors along with the percentage of consolidated assets and revenue that they audited.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

74

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

75

When the auditor concludes that there is substantial doubt about the entity's ability to continue as a going concern, the appropriate audit report could be I. an unmodified opinion audit report with an explanatory paragraph.

II) a disclaimer of opinion.

A) I only

B) II only

C) I or II

D) Neither I nor II

II) a disclaimer of opinion.

A) I only

B) II only

C) I or II

D) Neither I nor II

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

76

Under AICPA auditing standards, the primary auditor issuing the opinion on the financial statements is called the

A) component auditor.

B) principal auditor.

C) group engagement partner.

D) majority auditor.

A) component auditor.

B) principal auditor.

C) group engagement partner.

D) majority auditor.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

77

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following modifications of the auditor's report does not include an explanatory paragraph?

A) A qualified report is due to a GAAP departure.

B) The report includes an emphasis of a matter.

C) There is a very material scope limitation.

D) A principal auditor accepts the work of another auditor.

A) A qualified report is due to a GAAP departure.

B) The report includes an emphasis of a matter.

C) There is a very material scope limitation.

D) A principal auditor accepts the work of another auditor.

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

79

Indicate which change(s) would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following are changes that affect the comparability of financial statements but not the consistency and therefore, do not have to be included in the auditor's report?

A) error corrections not involving principles

B) changes in accounting estimates

C) variations in the format and presentation of financial information

D) all of the above

A) error corrections not involving principles

B) changes in accounting estimates

C) variations in the format and presentation of financial information

D) all of the above

Unlock Deck

Unlock for access to all 170 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 170 flashcards in this deck.