Deck 12: Perfect Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

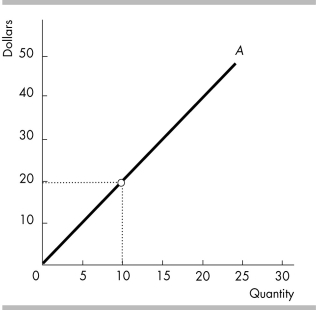

For a perfectly competitive firm, curve A in the above figure is the firm's

A) total fixed cost curve.

B) average fixed cost curve.

C) average variable cost curve.

D) total revenue curve.

Question

Question

The figure above portrays a total revenue curve for a perfectly competitive firm. Curve A is straight because the firm

A) is a price taker.

B) faces constant returns to scale.

C) wants to maximize its profits.

D) has perfect information.

Question

Question

Question

Question

Question

Question

The figure above portrays a total revenue curve for a perfectly competitive firm. The firm's marginal revenue from selling a unit of output

A) equals $0.50.

B) equals $1.00.

C) equals $2.00.

D) cannot be determined.

Question

Question

The above figure shows a firm's total revenue line. The firm must be in a market with

A) perfect competition.

B) monopolistic competition.

C) monopoly.

D) oligopoly.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

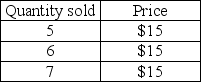

In the above table, if the quantity sold by the firm rises from 6 to 7, its marginal revenue is

A) $15.

B) $30.

C) $90.

D) $105.

Question

Question

Question

The figure above portrays a total revenue curve for a perfectly competitive firm. The price of the product in this industry

A) equals $0.50.

B) equals $1.00.

C) equals $2.00.

D) cannot be determined.

Question

Question

In the above figure showing a perfectly competitive firm's total revenue line, the firm's marginal revenue

A) falls as output increases.

B) does not change as output increases.

C) rises as output increases.

D) cannot be determined.

Question

Question

In the above table, if the quantity sold by the firm rises from 5 to 6, its marginal revenue is

A) $15.

B) $30.

C) $75.

D) $90.

Question

Question

Question

Question

Question

Question

In the above table, if the firm sells 5 units of output, its total revenue is

A) $15.

B) $30.

C) $75.

D) $90.

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/487

Play

Full screen (f)

Deck 12: Perfect Competition

1

In perfect competition, restrictions on entry into an market

A) apply to both capital and labor.

B) apply to labor but not to capital.

C) apply to capital but not to labor.

D) do not exist.

A) apply to both capital and labor.

B) apply to labor but not to capital.

C) apply to capital but not to labor.

D) do not exist.

do not exist.

2

Which of the following is NOT an assumption of perfect competition?

A) many firms

B) many buyers

C) restrictions on entry into the market

D) each firm sells an identical product

A) many firms

B) many buyers

C) restrictions on entry into the market

D) each firm sells an identical product

restrictions on entry into the market

3

Which of the following is TRUE regarding a perfectly competitive firm?

A) The firm can charge a lower price than its competitors and thereby sell more output and increase its profits.

B) The firm always earns a normal profit.

C) The firm's marginal revenue continually decreases.

D) The firm's minimum efficient scale is small relative to the market demand.

A) The firm can charge a lower price than its competitors and thereby sell more output and increase its profits.

B) The firm always earns a normal profit.

C) The firm's marginal revenue continually decreases.

D) The firm's minimum efficient scale is small relative to the market demand.

The firm's minimum efficient scale is small relative to the market demand.

4

The smallest quantity of output at which long-run average cost is at a minimum is a firm's ________.

A) maximum efficient scale

B) profit-maximizing output point

C) minimum efficient scale

D) efficient output point

A) maximum efficient scale

B) profit-maximizing output point

C) minimum efficient scale

D) efficient output point

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

5

In perfect competition, ________.

A) there are restrictions on entry into the market

B) firms in the market have advantages over firms that plan to enter the market

C) only firms know their competitors' prices

D) there are many firms that sell identical products

A) there are restrictions on entry into the market

B) firms in the market have advantages over firms that plan to enter the market

C) only firms know their competitors' prices

D) there are many firms that sell identical products

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is NOT an assumption of perfect competition?

A) There are many firms, each selling an identical product.

B) There are many buyers.

C) The price each firm sets differs from the prices set by the other firms.

D) There are no restrictions on entry into the market.

A) There are many firms, each selling an identical product.

B) There are many buyers.

C) The price each firm sets differs from the prices set by the other firms.

D) There are no restrictions on entry into the market.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

7

In perfect competition

A) many firms sell slightly different products to many buyers.

B) sellers are better informed about the prices than buyers.

C) firms face no restrictions on entry into market.

D) established firms have advantage over new ones.

A) many firms sell slightly different products to many buyers.

B) sellers are better informed about the prices than buyers.

C) firms face no restrictions on entry into market.

D) established firms have advantage over new ones.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

8

In perfect competition, the product of a single firm

A) has many perfect substitutes produced by other firms.

B) has many perfect complements produced by other firms.

C) is sold under many differing brand names.

D) is sold to different customers at different prices.

A) has many perfect substitutes produced by other firms.

B) has many perfect complements produced by other firms.

C) is sold under many differing brand names.

D) is sold to different customers at different prices.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

9

Perfect competition implies that

A) there are many firms in the market.

B) all firms are price takers.

C) all firms are producing the same identical product.

D) All of the above answers are correct.

A) there are many firms in the market.

B) all firms are price takers.

C) all firms are producing the same identical product.

D) All of the above answers are correct.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

10

Perfect competition arises if the ________ efficient scale of a single producer is ________ relative to the demand for the good or service.

A) minimum; small

B) minimum; large

C) maximum; small

D) maximum; large

A) minimum; small

B) minimum; large

C) maximum; small

D) maximum; large

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

11

If the minimum efficient scale of a firm is small relative to the demand for the good, then

A) many small firms can compete in the market.

B) several large firms will enter the market thereby reducing competition.

C) there will be no economic profits for any small firms, so no new firms will ever enter the market.

D) the firms already in the market have lower average total cost than any new firm entering the market.

A) many small firms can compete in the market.

B) several large firms will enter the market thereby reducing competition.

C) there will be no economic profits for any small firms, so no new firms will ever enter the market.

D) the firms already in the market have lower average total cost than any new firm entering the market.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

12

In a perfectly competitive market, there are

A) many buyers and many sellers.

B) many buyers, but there might be only one or two sellers.

C) many sellers, but there might be only one or two buyers.

D) one firm that sets the price for the others to follow.

A) many buyers and many sellers.

B) many buyers, but there might be only one or two sellers.

C) many sellers, but there might be only one or two buyers.

D) one firm that sets the price for the others to follow.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

13

A perfectly competitive market is characterized by

A) high barriers to entry.

B) firms that are price setters.

C) firms facing a downward sloping demand curve.

D) no restrictions on entry into the market.

A) high barriers to entry.

B) firms that are price setters.

C) firms facing a downward sloping demand curve.

D) no restrictions on entry into the market.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

14

A market is perfectly competitive if

A) each firm in it can influence the price of its product.

B) there are many firms in it, each selling a slightly different product.

C) there are many firms in it, each selling an identical product.

D) there are few firms in the market.

A) each firm in it can influence the price of its product.

B) there are many firms in it, each selling a slightly different product.

C) there are many firms in it, each selling an identical product.

D) there are few firms in the market.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is NOT an assumption of perfectly competitive markets?

A) many buyers and many sellers

B) no restriction on entry

C) complete information about prices

D) new entrants have higher costs

A) many buyers and many sellers

B) no restriction on entry

C) complete information about prices

D) new entrants have higher costs

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is NOT an assumption of perfect competition?

A) Firms compete by making their product different from products produced by other firms.

B) There are no restrictions on entry into the market.

C) Established firms have no advantage over new firms.

D) Sellers and buyers are well informed about prices.

A) Firms compete by making their product different from products produced by other firms.

B) There are no restrictions on entry into the market.

C) Established firms have no advantage over new firms.

D) Sellers and buyers are well informed about prices.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

17

Perfect competition exists in a market if

A) there are many firms producing an identical product.

B) there are many firms producing a similar product, each of which may have unique features.

C) the firm is protected by a barrier to entry.

D) the firm is always at the break-even point where it is earning only a normal profit.

A) there are many firms producing an identical product.

B) there are many firms producing a similar product, each of which may have unique features.

C) the firm is protected by a barrier to entry.

D) the firm is always at the break-even point where it is earning only a normal profit.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

18

In perfect competition, the

A) market demand for the good or service is large relative to the minimum efficient scale of a single producer.

B) market demand for the good or service is small relative to the minimum efficient scale of a single producer.

C) market demand for the good or service can be small relative to the minimum efficient scale of a single producer as long as the goods or services are not identical.

D) size of the market demand for the good or service relative to the minimum efficient scale of a single producer does not affect competition.

A) market demand for the good or service is large relative to the minimum efficient scale of a single producer.

B) market demand for the good or service is small relative to the minimum efficient scale of a single producer.

C) market demand for the good or service can be small relative to the minimum efficient scale of a single producer as long as the goods or services are not identical.

D) size of the market demand for the good or service relative to the minimum efficient scale of a single producer does not affect competition.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is TRUE regarding perfect competition? I. The firms are price takers.

II) Marginal revenue equals the price of the product.

III) Established firms have no advantage over new firms.

A) I and II

B) II and III

C) I, II and III

D) I only

II) Marginal revenue equals the price of the product.

III) Established firms have no advantage over new firms.

A) I and II

B) II and III

C) I, II and III

D) I only

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is a defining characteristic of a perfectly competitive market?

A) advertisements by well-known celebrities

B) persistent economic profits in the long run

C) no restrictions on entry into the industry

D) higher prices being charged for certain name brands

A) advertisements by well-known celebrities

B) persistent economic profits in the long run

C) no restrictions on entry into the industry

D) higher prices being charged for certain name brands

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

21

When a firm is considered to be a "price taker" that means that the firm

A) can charge any price that it wants to charge, that is, "take" any price it wants.

B) pays a fixed price for all of its inputs.

C) will accept ("take") the lowest price that its customers offer.

D) cannot influence the market price of the good that it sells.

A) can charge any price that it wants to charge, that is, "take" any price it wants.

B) pays a fixed price for all of its inputs.

C) will accept ("take") the lowest price that its customers offer.

D) cannot influence the market price of the good that it sells.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

22

The market for lawn services is perfectly competitive. Larry's Lawn Service cannot increase its total revenue by raising its price because ________.

A) Larry's supply of lawn services is perfectly inelastic

B) the demand for Larry's services is perfectly inelastic

C) Larry's supply of lawn services is inelastic

D) the demand for Larry's services is perfectly elastic

A) Larry's supply of lawn services is perfectly inelastic

B) the demand for Larry's services is perfectly inelastic

C) Larry's supply of lawn services is inelastic

D) the demand for Larry's services is perfectly elastic

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

23

Firms in perfectly competitive industries have a ________ individual demand curve when the price is on the vertical axis and the quantity is on the horizontal axis. The shape of the curve is result of the firm being a ________.

A) horizontal; price taker

B) downward sloping; price maker

C) vertical; price taker

D) downward sloping; price taker

A) horizontal; price taker

B) downward sloping; price maker

C) vertical; price taker

D) downward sloping; price taker

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is NOT a characteristic of a perfectly competitive industry?

A) There are many firms.

B) There are no restrictions on entry into the market.

C) Each firm produces a slightly differentiated product.

D) Each firm takes price as given, determined by the equilibrium of industry supply and industry demand.

A) There are many firms.

B) There are no restrictions on entry into the market.

C) Each firm produces a slightly differentiated product.

D) Each firm takes price as given, determined by the equilibrium of industry supply and industry demand.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

25

In perfect competition, an individual firm

A) sets the price and determines the quantity it sells in the marketplace.

B) sets the price but does not determine the quantity it sells in the marketplace.

C) determines the quantity it sells in the marketplace but has no influence over its price.

D) can not affect its price nor determine the quantity it sells in the marketplace.

A) sets the price and determines the quantity it sells in the marketplace.

B) sets the price but does not determine the quantity it sells in the marketplace.

C) determines the quantity it sells in the marketplace but has no influence over its price.

D) can not affect its price nor determine the quantity it sells in the marketplace.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

26

An example of a perfectly competitive industry is

A) a big city police department.

B) the market for corn in the United States.

C) the market for French impressionists' paintings.

D) the National Football League.

A) a big city police department.

B) the market for corn in the United States.

C) the market for French impressionists' paintings.

D) the National Football League.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

27

In a perfectly competitive market

A) each firm sets its own price so that it is different from its competitors.

B) an economic profit is certain.

C) each firm takes the good's price as given to it by the market.

D) consumers are persuaded by advertising.

A) each firm sets its own price so that it is different from its competitors.

B) an economic profit is certain.

C) each firm takes the good's price as given to it by the market.

D) consumers are persuaded by advertising.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

28

An example of a perfectly competitive firm is

A) an oat farmer in the United States.

B) the local cable TV company.

C) a U.S. automobile producer.

D) a big city newspaper.

A) an oat farmer in the United States.

B) the local cable TV company.

C) a U.S. automobile producer.

D) a big city newspaper.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

29

Price taking behavior exists in

A) perfectly competitive markets.

B) markets with a monopolist, where consumers have to take price as it is given to them by the monopolist.

C) automobile markets where consumers have to take the price set by the dealer.

D) Both answers B and C are correct.

A) perfectly competitive markets.

B) markets with a monopolist, where consumers have to take price as it is given to them by the monopolist.

C) automobile markets where consumers have to take the price set by the dealer.

D) Both answers B and C are correct.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

30

The assumption that a perfectly competitive industry has many sellers, each selling an identical product, leads to the conclusion that

A) consumers get to see a variety of outputs.

B) there are many buyers.

C) the economic profit will be positive in the long run.

D) firms are price takers.

A) consumers get to see a variety of outputs.

B) there are many buyers.

C) the economic profit will be positive in the long run.

D) firms are price takers.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

31

In perfect competition, the elasticity of demand for the product of a single firm is

A) 0.

B) between 0 and 1.

C) 1.

D) infinite.

A) 0.

B) between 0 and 1.

C) 1.

D) infinite.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

32

The price elasticity of demand for any particular perfectly competitive firm's output is

A) less than 1.

B) 1.

C) equal to zero.

D) infinite.

A) less than 1.

B) 1.

C) equal to zero.

D) infinite.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following is NOT a defining characteristic of perfectly competitive industries?

A) many buyers and sellers

B) unrestricted entry and exit

C) consumer knowledge about prices charged by each firm

D) higher prices being charged for certain name brands

A) many buyers and sellers

B) unrestricted entry and exit

C) consumer knowledge about prices charged by each firm

D) higher prices being charged for certain name brands

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

34

The demand for wheat from farm A is perfectly elastic because wheat from farm A is

A) a perfect complement for wheat from farm B.

B) a normal good.

C) a perfect substitute for wheat from farm B.

D) an inferior good.

A) a perfect complement for wheat from farm B.

B) a normal good.

C) a perfect substitute for wheat from farm B.

D) an inferior good.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

35

In perfect competition, the market demand for the good ________ perfectly elastic and the demand for the output of one firm ________ perfectly elastic.

A) is; is

B) is; is not

C) is not; is

D) is not; is not

A) is; is

B) is; is not

C) is not; is

D) is not; is not

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

36

In perfect competition, each firm ________.

A) can influence the price that it charges

B) produces as much as it can

C) is a price taker

D) faces a perfectly inelastic demand for its product

A) can influence the price that it charges

B) produces as much as it can

C) is a price taker

D) faces a perfectly inelastic demand for its product

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

37

In a perfectly competitive industry

A) each firm sets its own price so that it is different from the prices of its competitors.

B) earning an economic profit is certain.

C) each firm is a price taker.

D) consumers band together to demand the lowest price possible.

A) each firm sets its own price so that it is different from the prices of its competitors.

B) earning an economic profit is certain.

C) each firm is a price taker.

D) consumers band together to demand the lowest price possible.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

38

Individual firms in perfectly competitive industries are price takers because

A) the government sets all prices.

B) buyers set prices.

C) firms decide together on the best price to charge.

D) each individual firm is too small to affect the market price.

A) the government sets all prices.

B) buyers set prices.

C) firms decide together on the best price to charge.

D) each individual firm is too small to affect the market price.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

39

In a perfectly competitive industry, the demand for a single firm's product is perfectly elastic

A) because this firm's output is a perfect substitute for any other firm's output.

B) because this firm is a price maker.

C) only in the long run.

D) because there are many buyers in this market.

A) because this firm's output is a perfect substitute for any other firm's output.

B) because this firm is a price maker.

C) only in the long run.

D) because there are many buyers in this market.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

40

In perfect competition

A) each firm can influence the price of the good.

B) there are few buyers.

C) there are significant restrictions on entry.

D) all firms in the market sell their product at the same price.

A) each firm can influence the price of the good.

B) there are few buyers.

C) there are significant restrictions on entry.

D) all firms in the market sell their product at the same price.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

41

The difference between a firm's total revenue and its total opportunity cost is the firm's

A) normal profit.

B) economic profit.

C) marginal profit.

D) marginal revenue.

A) normal profit.

B) economic profit.

C) marginal profit.

D) marginal revenue.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

42

In perfect competition, the elasticity of demand for the product of a single firm is

A) zero because the firm produces a unique product.

B) zero because many other firms produce identical products.

C) infinite because the firm produces a unique product.

D) infinite because many other firms produce identical products.

A) zero because the firm produces a unique product.

B) zero because many other firms produce identical products.

C) infinite because the firm produces a unique product.

D) infinite because many other firms produce identical products.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

43

For a perfectly competitive firm, curve A in the above figure is the firm's

A) total fixed cost curve.

B) average fixed cost curve.

C) average variable cost curve.

D) total revenue curve.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

44

Because each perfectly competitive firm sells a product identical to that of the other firms

A) each firm tries to cut prices to increase its market share.

B) each firm's output is a perfect substitute for the output of any other firm.

C) each firm expects to earn some economic profit.

D) the demand for each firm's product is perfectly inelastic.

A) each firm tries to cut prices to increase its market share.

B) each firm's output is a perfect substitute for the output of any other firm.

C) each firm expects to earn some economic profit.

D) the demand for each firm's product is perfectly inelastic.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

45

The figure above portrays a total revenue curve for a perfectly competitive firm. Curve A is straight because the firm

A) is a price taker.

B) faces constant returns to scale.

C) wants to maximize its profits.

D) has perfect information.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

46

In perfect competition, the price of the product is determined where the market

A) elasticity of supply equals the market elasticity of demand.

B) supply curve and market demand curve intersect.

C) average variable cost equals the market average total cost.

D) fixed cost is zero.

A) elasticity of supply equals the market elasticity of demand.

B) supply curve and market demand curve intersect.

C) average variable cost equals the market average total cost.

D) fixed cost is zero.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

47

A competitive firm's total revenue minus its total opportunity cost equals its ________.

A) marginal revenue

B) economic profit

C) opportunity cost

D) normal profit

A) marginal revenue

B) economic profit

C) opportunity cost

D) normal profit

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

48

In perfect competition, each individual firm faces ________ demand curve.

A) an inelastic

B) an upward sloping

C) a perfectly elastic

D) a downward sloping

A) an inelastic

B) an upward sloping

C) a perfectly elastic

D) a downward sloping

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

49

The return that the entrepreneur can obtain in the best alternative business is called the

A) normal profit.

B) economic profit.

C) marginal profit.

D) marginal revenue.

A) normal profit.

B) economic profit.

C) marginal profit.

D) marginal revenue.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

50

A perfectly competitive firm's demand curve is

A) upward sloping.

B) downward sloping.

C) a vertical line.

D) a horizontal line.

A) upward sloping.

B) downward sloping.

C) a vertical line.

D) a horizontal line.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

51

The figure above portrays a total revenue curve for a perfectly competitive firm. The firm's marginal revenue from selling a unit of output

A) equals $0.50.

B) equals $1.00.

C) equals $2.00.

D) cannot be determined.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

52

In a perfectly competitive market, which of the following determines the market price?

A) market demand and a firm's supply

B) market supply and a firm's demand

C) a firm's demand and its supply

D) market demand and market supply

A) market demand and a firm's supply

B) market supply and a firm's demand

C) a firm's demand and its supply

D) market demand and market supply

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

53

The above figure shows a firm's total revenue line. The firm must be in a market with

A) perfect competition.

B) monopolistic competition.

C) monopoly.

D) oligopoly.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

54

In perfect competition, a firm that maximizes its economic profit will sell its good at a price that is

A) below the market price.

B) at the market price.

C) above the market price.

D) below the market price if its supply curve is inelastic and above the market price if its supply curve is elastic.

A) below the market price.

B) at the market price.

C) above the market price.

D) below the market price if its supply curve is inelastic and above the market price if its supply curve is elastic.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

55

Economic profit is ________.

A) included in the firm's total opportunity cost

B) equal to normal profit minus total opportunity cost

C) equal to total revenue minus marginal cost

D) equal to total revenue minus total opportunity cost

A) included in the firm's total opportunity cost

B) equal to normal profit minus total opportunity cost

C) equal to total revenue minus marginal cost

D) equal to total revenue minus total opportunity cost

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

56

The economic profit of a perfectly competitive firm

A) is less than its total revenue.

B) equals its total revenue.

C) is greater than its total revenue.

D) is less than its total revenue if its supply curve is inelastic and is greater than its total revenue if its supply curve is elastic.

A) is less than its total revenue.

B) equals its total revenue.

C) is greater than its total revenue.

D) is less than its total revenue if its supply curve is inelastic and is greater than its total revenue if its supply curve is elastic.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

57

Total economic profit is

A) total revenue minus total opportunity cost.

B) total revenue divided by total cost.

C) marginal revenue minus marginal cost.

D) marginal revenue divided by marginal cost.

A) total revenue minus total opportunity cost.

B) total revenue divided by total cost.

C) marginal revenue minus marginal cost.

D) marginal revenue divided by marginal cost.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

58

In perfect competition, an individual firm

A) faces unitary elasticity of demand.

B) has a price elasticity of supply equal to one.

C) faces a perfectly elastic demand.

D) has perfectly elastic supply.

A) faces unitary elasticity of demand.

B) has a price elasticity of supply equal to one.

C) faces a perfectly elastic demand.

D) has perfectly elastic supply.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

59

A perfectly competitive firm has a total revenue curve that is

A) upward sloping with an increasing slope.

B) downward sloping with a constant slope.

C) upward sloping with a decreasing slope.

D) upward sloping with a constant slope.

A) upward sloping with an increasing slope.

B) downward sloping with a constant slope.

C) upward sloping with a decreasing slope.

D) upward sloping with a constant slope.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

60

The goal of a perfectly competitive firm is to maximize its

A) normal profit.

B) revenue.

C) output.

D) economic profit.

A) normal profit.

B) revenue.

C) output.

D) economic profit.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

61

Marginal revenue is defined as

A) the value of a firm's sales.

B) the total revenue from the total amount the firm sells.

C) the change in total revenue that results from a one-unit increase in the quantity sold.

D) total revenue divided by the total quantity sold.

A) the value of a firm's sales.

B) the total revenue from the total amount the firm sells.

C) the change in total revenue that results from a one-unit increase in the quantity sold.

D) total revenue divided by the total quantity sold.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

62

In perfect competition, the firm's marginal revenue curve

A) cuts its demand curve from below, going from left to right.

B) cuts its demand curve from above, going from left to right.

C) always lies below its demand curve.

D) is the same as its demand curve.

A) cuts its demand curve from below, going from left to right.

B) cuts its demand curve from above, going from left to right.

C) always lies below its demand curve.

D) is the same as its demand curve.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

63

In the above table, if the quantity sold by the firm rises from 6 to 7, its marginal revenue is

A) $15.

B) $30.

C) $90.

D) $105.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

64

In a perfectly competitive industry, the demand for a single firm's product is

A) perfectly inelastic.

B) perfectly elastic.

C) as elastic as the market demand.

D) inelastic, but not perfectly inelastic.

A) perfectly inelastic.

B) perfectly elastic.

C) as elastic as the market demand.

D) inelastic, but not perfectly inelastic.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

65

If Steve's Apple Orchard, Inc. is a perfectly competitive firm, the demand for Steve's apples has

A) zero elasticity.

B) unitary elasticity.

C) elasticity equal to the price of apples.

D) infinite elasticity.

A) zero elasticity.

B) unitary elasticity.

C) elasticity equal to the price of apples.

D) infinite elasticity.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

66

The figure above portrays a total revenue curve for a perfectly competitive firm. The price of the product in this industry

A) equals $0.50.

B) equals $1.00.

C) equals $2.00.

D) cannot be determined.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

67

In a perfectly competitive market, the price elasticity of demand for the market demand is ________ and the price elasticity of demand for an individual firm's demand is ________.

A) infinite; infinite

B) less than infinite; infinite

C) infinite; less than infinite

D) less than infinite; less than infinite

A) infinite; infinite

B) less than infinite; infinite

C) infinite; less than infinite

D) less than infinite; less than infinite

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

68

In the above figure showing a perfectly competitive firm's total revenue line, the firm's marginal revenue

A) falls as output increases.

B) does not change as output increases.

C) rises as output increases.

D) cannot be determined.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

69

A perfectly competitive firm's marginal revenue

A) increases as the firm produces more output.

B) decreases as the firm produces more output.

C) is less than the market price of its product.

D) equals the market price of its product.

A) increases as the firm produces more output.

B) decreases as the firm produces more output.

C) is less than the market price of its product.

D) equals the market price of its product.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

70

In the above table, if the quantity sold by the firm rises from 5 to 6, its marginal revenue is

A) $15.

B) $30.

C) $75.

D) $90.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

71

The market demand for wheat is ________ and the demand for wheat produced by an individual farm is ________.

A) perfectly elastic; perfectly inelastic

B) not perfectly elastic; perfectly elastic

C) not perfectly inelastic; inelastic

D) elastic; unit elastic

A) perfectly elastic; perfectly inelastic

B) not perfectly elastic; perfectly elastic

C) not perfectly inelastic; inelastic

D) elastic; unit elastic

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

72

In perfect competition, the marginal revenue of an individual firm

A) is zero.

B) is positive but less than the price of the product.

C) equals the price of the product.

D) exceeds the price of the product.

A) is zero.

B) is positive but less than the price of the product.

C) equals the price of the product.

D) exceeds the price of the product.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

73

Marginal revenue is equal to

A) total revenue divided by price.

B) the change in total revenue divided by total output.

C) the change in total revenue divided by the change in quantity sold.

D) price divided by quantity sold.

A) total revenue divided by price.

B) the change in total revenue divided by total output.

C) the change in total revenue divided by the change in quantity sold.

D) price divided by quantity sold.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

74

For a perfectly competitive firm, no matter how much the firm produces, price always equals

A) marginal product.

B) average total cost.

C) minimum average total cost.

D) marginal revenue.

A) marginal product.

B) average total cost.

C) minimum average total cost.

D) marginal revenue.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

75

In perfect competition, at all levels of output the market price is the same as the firm's ________.

A) marginal revenue

B) normal profit

C) average variable cost

D) fixed cost

A) marginal revenue

B) normal profit

C) average variable cost

D) fixed cost

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

76

In the above table, if the firm sells 5 units of output, its total revenue is

A) $15.

B) $30.

C) $75.

D) $90.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

77

Which of the following is ALWAYS true for a perfectly competitive firm?

A) P = MR

B) P = ATC

C) MR = ATC

D) P = AVC

A) P = MR

B) P = ATC

C) MR = ATC

D) P = AVC

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

78

The market for fish is perfectly competitive. So, the price elasticity of demand for fish from a single fishing boat

A) is less than the elasticity of demand for fish overall.

B) equals the elasticity of demand for fish overall.

C) is greater than the elasticity of demand for fish overall.

D) is sometimes greater than and sometimes less than the elasticity of demand for fish overall.

A) is less than the elasticity of demand for fish overall.

B) equals the elasticity of demand for fish overall.

C) is greater than the elasticity of demand for fish overall.

D) is sometimes greater than and sometimes less than the elasticity of demand for fish overall.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

79

Because the demand for a perfectly competitive firm's product is perfectly elastic, marginal revenue is equal to

A) one.

B) zero.

C) the price of the product.

D) negative one.

A) one.

B) zero.

C) the price of the product.

D) negative one.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

80

For a perfectly competitive firm, price is the same as

A) marginal revenue.

B) average variable cost.

C) total revenue.

D) Both answers A and B are correct.

A) marginal revenue.

B) average variable cost.

C) total revenue.

D) Both answers A and B are correct.

Unlock Deck

Unlock for access to all 487 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 487 flashcards in this deck.