Deck 6: Understanding Financial Markets and Institutions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Forecasting Interest Rates On May 23, 20XX, the existing or current (spot) one-year, two-year, three-year, and four-year zero-coupon Treasury security rates were as follows:

Using the unbiased expectations theory, what is the one-year forward rate on zero-coupon Treasury bonds for year four as of May 23, 20XX?

A.5.925%

B.6.45%

C.7.05%

D. 10.32%

Using the unbiased expectations theory, what is the one-year forward rate on zero-coupon Treasury bonds for year four as of May 23, 20XX?

A.5.925%

B.6.45%

C.7.05%

D. 10.32%

Question

Question

Question

Question

Question

Question

Question

Liquidity Premium Hypothesis Based on economists' forecasts and analysis, one-year Treasury bill rates and liquidity premiums for the next four years are expected to be as follows:  Using the liquidity premium hypothesis, what is the current rate on a four-year Treasury security?

Using the liquidity premium hypothesis, what is the current rate on a four-year Treasury security?

A) 7.736%

B) 7.600%

C) 7.738%

D) 8.400%

Using the liquidity premium hypothesis, what is the current rate on a four-year Treasury security?A) 7.736%

B) 7.600%

C) 7.738%

D) 8.400%

Question

Question

Question

Question

Question

Question

Question

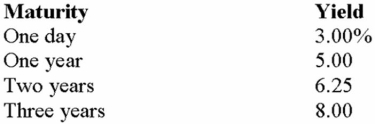

Forecasting Interest Rates You note the following yield curve in The Wall Street Journal. According to the unbiased expectations hypothesis, what is the one-year forward rate for the period beginning one year from today, 2f1?

A) 1.01%

B) 1.19%

C) 5.625%

D) 7.51%

A) 1.01%

B) 1.19%

C) 5.625%

D) 7.51%

Question

Question

Question

Question

Question

Unbiased Expectations Theory Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows:  Using the unbiased expectations theory, what is the current (long-term) rate for four-year-maturity Treasury securities?

Using the unbiased expectations theory, what is the current (long-term) rate for four-year-maturity Treasury securities?

A) 6.00%

B) 6.33%

C) 6.75%

D) 7.00%

Using the unbiased expectations theory, what is the current (long-term) rate for four-year-maturity Treasury securities?A) 6.00%

B) 6.33%

C) 6.75%

D) 7.00%

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

You note the following yield curve in The Wall Street Journal. According to the unbiased expectations hypothesis, what is the one-year forward rate for the period beginning one year from today, 2f1?

A) 7.6%

B) 8.6%

C) 9.0%

D) 10.2%

A) 7.6%

B) 8.6%

C) 9.0%

D) 10.2%

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/104

Play

Full screen (f)

Deck 6: Understanding Financial Markets and Institutions

1

This is the interest rate that is actually observed in financial markets.

A) nominal interest rates

B) real interest rates

C) real risk free rate

D) market premium

A) nominal interest rates

B) real interest rates

C) real risk free rate

D) market premium

nominal interest rates

2

Which of the following is NOT a money market instrument?

A) Treasury bills

B) Commercial paper

C) Corporate bonds

D) Banker's acceptances

A) Treasury bills

B) Commercial paper

C) Corporate bonds

D) Banker's acceptances

Corporate bonds

3

This is a comparison of market yields on securities, assuming all characteristics except maturity are the same.

A) liquidity risk

B) market risk

C) maturity risk

D) term structure of interest rates

A) liquidity risk

B) market risk

C) maturity risk

D) term structure of interest rates

term structure of interest rates

4

Once firms issue financial instruments in primary markets, these same stocks and bonds are then traded in which of these?

A) initial public offerings

B) direct transfers

C) secondary markets

D) over-the-counter stocks

A) initial public offerings

B) direct transfers

C) secondary markets

D) over-the-counter stocks

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

5

These money market instruments are short-term funds transferred between financial institutions, usually for no more than one day.

A) Treasury bills

B) Federal funds

C) Commercial paper

D) Banker acceptances

A) Treasury bills

B) Federal funds

C) Commercial paper

D) Banker acceptances

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

6

This is the risk that an asset's sale price will be lower than its purchase price.

A) default risk

B) liquidity risk

C) price risk

D) trading risk

A) default risk

B) liquidity risk

C) price risk

D) trading risk

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

7

In the U.S., these financial institutions arrange most primary market transactions for businesses.

A) investment banks

B) asset transformer

C) direct transfer agents

D) over-the-counter agents

A) investment banks

B) asset transformer

C) direct transfer agents

D) over-the-counter agents

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

8

This is the ease with which an asset can be converted into cash.

A) direct transfer

B) liquidity

C) primary market

D) secondary market

A) direct transfer

B) liquidity

C) primary market

D) secondary market

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

9

These markets trade currencies for immediate or for some future stated delivery.

A) money markets

B) primary markets

C) foreign exchange markets

D) over-the-counter stocks

A) money markets

B) primary markets

C) foreign exchange markets

D) over-the-counter stocks

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

10

This is the interest rate that would exist on a default-free security if no inflation were expected.

A) nominal interest rate

B) real interest rate

C) real risk free rate

D) market premium

A) nominal interest rate

B) real interest rate

C) real risk free rate

D) market premium

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

11

These capital market instruments are long-term loans to individuals or businesses to purchase homes, pieces of land, or other real property.

A) Treasury notes and bonds

B) Mortgages

C) Mortgage-backed securities

D) Corporate bonds

A) Treasury notes and bonds

B) Mortgages

C) Mortgage-backed securities

D) Corporate bonds

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

12

This is a security formalizing an agreement between two parties to exchange a standard quantity of an asset at a predetermined price on a specified date in the future.

A) derivative security

B) initial public offering

C) liquidity asset

D) trading volume

A) derivative security

B) initial public offering

C) liquidity asset

D) trading volume

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

13

This is the continual increase in the price level of a basket of goods and services.

A) deflation

B) inflation

C) recession

D) stagflation

A) deflation

B) inflation

C) recession

D) stagflation

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

14

Primary market financial instruments include stock issues from firms allowing their equity shares to be publicly traded on stock market for the first time. We usually refer to these first-time issues as which of the following?

A) initial public offerings

B) direct transfers

C) money market transfers

D) over-the-counter stocks

A) initial public offerings

B) direct transfers

C) money market transfers

D) over-the-counter stocks

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

15

These feature debt securities or instruments with maturities of one year or less.

A) money markets

B) primary markets

C) secondary markets

D) over-the-counter stocks

A) money markets

B) primary markets

C) secondary markets

D) over-the-counter stocks

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

16

This is the risk that a security issuer will miss an interest or principal payment or continue to miss such payments.

A) default risk

B) liquidity risk

C) maturity risk

D) price risk

A) default risk

B) liquidity risk

C) maturity risk

D) price risk

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

17

Which of these statements is true?

A) The higher the default risk, the higher the interest rate that security buyers will demand.

B) The lower the default risk, the higher the interest rate that security buyers will demand.

C) The higher the default risk, the lower the interest rate that security buyers will demand.

D) The default risk does not impact the interest rate that security buyers will demand.

A) The higher the default risk, the higher the interest rate that security buyers will demand.

B) The lower the default risk, the higher the interest rate that security buyers will demand.

C) The higher the default risk, the lower the interest rate that security buyers will demand.

D) The default risk does not impact the interest rate that security buyers will demand.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

18

Which of these does NOT perform vital functions to securities markets of all sorts by channeling funds from those with surplus funds to those with shortages of funds?

A) commercial banks

B) secondary markets

C) insurance companies

D) mutual funds

A) commercial banks

B) secondary markets

C) insurance companies

D) mutual funds

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

19

These provide a forum in which demanders of funds raise funds by issuing new financial instruments, such as stocks and bonds.

A) investment banks

B) money markets

C) primary markets

D) secondary markets

A) investment banks

B) money markets

C) primary markets

D) secondary markets

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is NOT a capital market instrument?

A) U.S. Treasury notes and bonds

B) U.S. Treasury bills

C) U.S. government agency bonds

D) Corporate stocks and bonds

A) U.S. Treasury notes and bonds

B) U.S. Treasury bills

C) U.S. government agency bonds

D) Corporate stocks and bonds

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

21

Forecasting Interest Rates On May 23, 20XX, the existing or current (spot) one-year, two-year, three-year, and four-year zero-coupon Treasury security rates were as follows:

Using the unbiased expectations theory, what is the one-year forward rate on zero-coupon Treasury bonds for year four as of May 23, 20XX?

A.5.925%

B.6.45%

C.7.05%

D. 10.32%

Using the unbiased expectations theory, what is the one-year forward rate on zero-coupon Treasury bonds for year four as of May 23, 20XX?

A.5.925%

B.6.45%

C.7.05%

D. 10.32%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

22

Unbiased Expectations Theory One-year Treasury bills currently earn 5.50 percent. You expect that one year from now, one-year Treasury bill rates will increase to 5.75 percent. If the unbiased expectations theory is correct, what should the current rate be on two-year Treasury securities?

A) 5.50%

B) 5.625%

C) 5.75%

D) 11.25%

A) 5.50%

B) 5.625%

C) 5.75%

D) 11.25%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

23

Interest rates A 2-year Treasury security currently earns 5.25 percent. Over the next two years, the real interest rate is expected to be 3.00 percent per year and the inflation premium is expected to be 2.00 percent per year. What is the maturity risk premium on the 2-year Treasury security?

A) 0.25%

B) 1.00%

C) 1.05%

D) 5.00%

A) 0.25%

B) 1.00%

C) 1.05%

D) 5.00%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

24

This is the expected or "implied" rate on a short-term security that will originate at some point in the future.

A) Current yield

B) Forward rate

C) Spot rate

D) Yield to maturity

A) Current yield

B) Forward rate

C) Spot rate

D) Yield to maturity

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

25

Liquidity Premium Hypothesis The Wall Street Journal reports that the rate on 3-year Treasury securities is 4.75 percent and the rate on 4-year Treasury securities is 5.00 percent. The one-year interest rate expected in three years is E(4r1), 5.25 percent. According to the liquidity premium hypotheses, what is the liquidity premium on the 4-year Treasury security, L4?

A) 0.0375%

B) 0.504%

C) 5.01%

D) 5.04%

A) 0.0375%

B) 0.504%

C) 5.01%

D) 5.04%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

26

According to this theory of term structure of interest rates, at any given point in time, the yield curve reflects the market's current expectations of future short-term rates.

A) Expectations Theory

B) Future Short-term Rates Theory

C) Term Structure of Interest Rates Theory

D) Unbiased Expectations Theory

A) Expectations Theory

B) Future Short-term Rates Theory

C) Term Structure of Interest Rates Theory

D) Unbiased Expectations Theory

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

27

Which of these is NOT a theory that explains the shape of the term structure of interest rates?

A) liquidity theory

B) market segmentation theory

C) short-term structure of interest rates theory

D) unbiased expectations theory

A) liquidity theory

B) market segmentation theory

C) short-term structure of interest rates theory

D) unbiased expectations theory

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

28

Liquidity Premium Hypothesis Based on economists' forecasts and analysis, one-year Treasury bill rates and liquidity premiums for the next four years are expected to be as follows: Using the liquidity premium hypothesis, what is the current rate on a four-year Treasury security?

A) 7.736%

B) 7.600%

C) 7.738%

D) 8.400%

Using the liquidity premium hypothesis, what is the current rate on a four-year Treasury security?A) 7.736%

B) 7.600%

C) 7.738%

D) 8.400%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

29

This theory argues that individual investors and financial institutions have specific maturity preferences, and to encourage buyers to hold securities with maturities other than their most preferred requires a higher interest rate.

A) Liquidity Premium Hypothesis

B) Market Segmentation Theory

C) Supply and Demand Theory

D) Unbiased Expectations Theory

A) Liquidity Premium Hypothesis

B) Market Segmentation Theory

C) Supply and Demand Theory

D) Unbiased Expectations Theory

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

30

Liquidity Premium Hypothesis Suppose we observe the following rates: 1R1 = 8%, 1R2 = 10%, and E(2r1) = 8%. If the liquidity premium theory of the term structure of interest rates holds, what is the liquidity premium for year 2, L2?

A) 1.02%

B) 4.04%

C) 6.15%

D) 12.03%

A) 1.02%

B) 4.04%

C) 6.15%

D) 12.03%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

31

Unbiased Expectations Theory Suppose we observe the following rates: 1R1 = 6%, 1R2 = 7.5%. If the unbiased expectations theory of the term structure of interest rates holds, what is the one-year interest rate expected one year from now, E(2r1)?

A) 6.75%

B) 7.50%

C) 9.02%

D) 13.5%

A) 6.75%

B) 7.50%

C) 9.02%

D) 13.5%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

32

Interest rates A corporation's 10-year bonds have an equilibrium rate of return of 7 percent. For all securities, the inflation risk premium is 1.50 percent and the real interest rate is 3.0 percent. The security's liquidity risk premium is 0.15 percent and maturity risk premium is 0.70 percent. The security has no special covenants. What is the bond's default risk premium?

A) 1.40%

B) 1.65%

C) 5.35%

D) 9.35%

A) 1.40%

B) 1.65%

C) 5.35%

D) 9.35%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

33

Interest rates The Wall Street Journal reports that the rate on 3-year Treasury securities is 7.00 percent, and the 6-year Treasury rate is 7.25 percent. From discussions with your broker, you have determined that expected inflation premium is 1.75 percent next year, 2.25 percent in Year 2, and 2.40 percent in Year 3 and beyond. Further, you expect that real interest rates will be 3.75 percent annually for the foreseeable future. What is the maturity risk premium on the 6-year Treasury security?

A) 0.83%

B) 0.983%

C) 1.10%

D) 1.233%

A) 0.83%

B) 0.983%

C) 1.10%

D) 1.233%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

34

Unbiased Expectations Theory The Wall Street Journal reports that the rate on 4-year Treasury securities is 4.75 percent and the rate on 5-year Treasury securities is 5.95 percent. According to the unbiased expectations hypotheses, what does the market expect the 1-year Treasury rate to be four years from today, E(5r1)?

A) 1.11%

B) 5.95%

C) 10.70%

D) 10.89%

A) 1.11%

B) 5.95%

C) 10.70%

D) 10.89%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

35

Forecasting Interest Rates You note the following yield curve in The Wall Street Journal. According to the unbiased expectations hypothesis, what is the one-year forward rate for the period beginning one year from today, 2f1?

A) 1.01%

B) 1.19%

C) 5.625%

D) 7.51%

A) 1.01%

B) 1.19%

C) 5.625%

D) 7.51%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

36

Interest rates A particular security's default risk premium is 3 percent. For all securities, the inflation risk premium is 2 percent and the real interest rate is 2.25 percent. The security's liquidity risk premium is 0.75 percent and maturity risk premium is 0.90 percent. The security has no special covenants. What is the security's equilibrium rate of return?

A) 1.78%

B) 3.95%

C) 8.90%

D) 17.8%

A) 1.78%

B) 3.95%

C) 8.90%

D) 17.8%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

37

Interest rates You are considering an investment in 30-year bonds issued by a corporation. The bonds have no special covenants. The Wall Street Journal reports that 1-year T-bills are currently earning 3.50 percent. Your broker has determined the following information about economic activity and the corporation bonds: Real interest rate = 2.50%

Default risk premium = 1.75%

Liquidity risk premium = 0.70%

Maturity risk premium = 1.50%

What is the inflation premium? What is the fair interest rate on the corporation's 30-year bonds?

A) 1% and 1.49%, respectively

B) 1% and 6.45%, respectively

C) 1% and 7.45%, respectively

D) 3.50% and 9.95%, respectively

Default risk premium = 1.75%

Liquidity risk premium = 0.70%

Maturity risk premium = 1.50%

What is the inflation premium? What is the fair interest rate on the corporation's 30-year bonds?

A) 1% and 1.49%, respectively

B) 1% and 6.45%, respectively

C) 1% and 7.45%, respectively

D) 3.50% and 9.95%, respectively

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

38

Interest rates A corporation's 10-year bonds are currently yielding a return of 7.75 percent. The expected inflation premium is 3.0 percent annually and the real interest rate is expected to be 3.00 percent annually over the next 10 years. The liquidity risk premium on the corporation's bonds is 0.50 percent. The maturity risk premium is 0.25 percent on 2-year securities and increases by 0.10 percent for each additional year to maturity. What is the default risk premium on the corporation's 10-year bonds?

A) 0.18%

B) 0.20%

C) 0.22%

D) 0.27%

A) 0.18%

B) 0.20%

C) 0.22%

D) 0.27%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

39

Liquidity Premium Hypothesis One-year Treasury bills currently earn 5.50 percent. You expect that one year from now, one-year Treasury bill rates will increase to 5.75 percent. The liquidity premium on two-year securities is 0.075 percent. If the liquidity theory is correct, what should the current rate be on two-year Treasury securities?

A) 3.775%

B) 5.625%

C) 5.662%

D) 11.325%

A) 3.775%

B) 5.625%

C) 5.662%

D) 11.325%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

40

Unbiased Expectations Theory Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows: Using the unbiased expectations theory, what is the current (long-term) rate for four-year-maturity Treasury securities?

A) 6.00%

B) 6.33%

C) 6.75%

D) 7.00%

Using the unbiased expectations theory, what is the current (long-term) rate for four-year-maturity Treasury securities?A) 6.00%

B) 6.33%

C) 6.75%

D) 7.00%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

41

Dakota Corporation 15-year bonds have an equilibrium rate of return of 9%. For all securities, the inflation risk premium is 1.95% and the real interest rate is 3.65%. The security's liquidity risk premium is 0.35% and maturity risk premium is 0.95%. The security has no special covenants. Calculate the bond's default risk premium.

A) 2.10%

B) 3.05%

C) 3.40%

D) 2.45%

A) 2.10%

B) 3.05%

C) 3.40%

D) 2.45%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

42

One-year Treasury bills currently earn 3.75 percent. You expect that one year from now, one-year Treasury bill rates will increase to 4.15 percent. If the unbiased expectations theory is correct, what should the current rate be on two-year Treasury securities?

A) 4.25%

B) 3.85%

C) 3.95%

D) 4.35%

A) 4.25%

B) 3.85%

C) 3.95%

D) 4.35%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

43

The Wall Street Journal reports that the rate on 3-year Treasury securities is 6.50%, and the 6-year Treasury rate is 6.80%. From discussions with your broker, you have determined that expected inflation premium is 2.25% next year, 2.50% in Year 2, and 2.60% in Year 3 and beyond. Further, you expect that real interest rates will be 3.4% annually for the foreseeable future. Calculate the maturity risk premium on the 3-year and the 6-year Treasury security.

A) 3-year: 0.6%; 6-year: 0.80%

B) 3-year: 0.5%; 6-year: 0.90%

C) 3-year: 0.6%; 6-year: 1.20%

D) 3-year: 0.5%; 6-year: 0.80%

A) 3-year: 0.6%; 6-year: 0.80%

B) 3-year: 0.5%; 6-year: 0.90%

C) 3-year: 0.6%; 6-year: 1.20%

D) 3-year: 0.5%; 6-year: 0.80%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

44

The Wall Street Journal reports that the rate on 3-year Treasury securities is 7.00%, and the 6-year Treasury rate is 6.20%. From discussions with your broker, you have determined that expected inflation premium is 2.25% next year, 2.50% in Year 2, and 2.50% in Year 3 and beyond. Further, you expect that real interest rates will be 4.4% annually for the foreseeable future. Calculate the maturity risk premium on the 3-year Treasury security.

A) 0.00%

B) 0.10%

C) 4.50%

D) 2.60%

A) 0.00%

B) 0.10%

C) 4.50%

D) 2.60%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

45

Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows: 1R1 = 5%, E(2r1) = 6%, E(3r1) = 7.5% E(4r1) = 6.85%

Using the unbiased expectations theory, calculate the current (long-term) rates for one-, two-, three-, and four-year-maturity Treasury securities.

A) 5.00%; 5.50%; 6.16%; 6.33%

B) 5.00%; 5.25%; 6.10%; 6.27%

C) 5.00%; 5.50%; 6.10%; 6.23%

D) 5.00%; 5.25%; 6.16%; 6.49%

Using the unbiased expectations theory, calculate the current (long-term) rates for one-, two-, three-, and four-year-maturity Treasury securities.

A) 5.00%; 5.50%; 6.16%; 6.33%

B) 5.00%; 5.25%; 6.10%; 6.27%

C) 5.00%; 5.50%; 6.10%; 6.23%

D) 5.00%; 5.25%; 6.16%; 6.49%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

46

Unbiased Expectations Theory The Wall Street Journal reports that the rate on 3-year Treasury securities is 6.25 percent and the rate on 5-year Treasury securities is 6.45 percent. According to the unbiased expectations hypotheses, what does the market expect the 2-year Treasury rate to be three years from today, E(4r2)?

A) 6.35%

B) 6.75%

C) 7.25%

D) 7.45%

A) 6.35%

B) 6.75%

C) 7.25%

D) 7.45%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

47

One-year Treasury bills currently earn 4.5 percent. You expect that one year from now, one-year Treasury bill rates will increase to 6.65 percent. The liquidity premium on two-year securities is 0.05 percent. If the liquidity theory is correct, what should the current rate be on two-year Treasury securities?

A) 5.24%

B) 5.59%

C) 5.65%

D) 5.95%

A) 5.24%

B) 5.59%

C) 5.65%

D) 5.95%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

48

Nikki G's Corporation's 10-year bonds are currently yielding a return of 9.25%. The expected inflation premium is 2.0% annually and the real interest rate is expected to be 3.10% annually over the next 10 years. The liquidity risk premium on Nikki G's bonds is 0.1%. The maturity risk premium is 0.10% on 2-year securities and increases by 0.05% for each additional year to maturity. Calculate the default risk premium on Nikki G's 10-year bonds.

A) 2.55%

B) 5.65%

C) 3.55%

D) 1.85%

A) 2.55%

B) 5.65%

C) 3.55%

D) 1.85%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

49

Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill rates over the following 3 years (i.e., years 2, 3 and 4 respectively) are as follows: 1R1 = 5%, E(2r1) = 6%, E(3r1) = 7.5% E(4r1) = 7.85%

Using the unbiased expectations theory, calculate the current (long-term) rates for three-year- and four-year-maturity Treasury securities.

A) One-year: 6.16%; Two-year: 6.58%

B) One-year: 6.16%; Two-year: 6.78%

C) One-year: 6.25%; Two-year: 6.45%

D) One-year: 5.95%; Two-year: 6.45%

Using the unbiased expectations theory, calculate the current (long-term) rates for three-year- and four-year-maturity Treasury securities.

A) One-year: 6.16%; Two-year: 6.58%

B) One-year: 6.16%; Two-year: 6.78%

C) One-year: 6.25%; Two-year: 6.45%

D) One-year: 5.95%; Two-year: 6.45%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

50

You are considering an investment in 30-year bonds issued by Moore Corporation. The bonds have no special covenants. The Wall Street Journal reports that 1-year T-bills are currently earning 3.55%. Your broker has determined the following information about economic activity and Moore Corporation bonds: Real interest rate = 2.75%

Default risk premium = 1.05%

Liquidity risk premium = 0.50%

Maturity risk premium = 1.85%

What is the fair interest rate on Moore Corporation 30-year bonds?

A) 3.80%

B) 6.45%

C) 6.95%

D) 9.70%

Default risk premium = 1.05%

Liquidity risk premium = 0.50%

Maturity risk premium = 1.85%

What is the fair interest rate on Moore Corporation 30-year bonds?

A) 3.80%

B) 6.45%

C) 6.95%

D) 9.70%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

51

Unbiased Expectations Theory Suppose we observe the three-year Treasury security rate (1R3) to be 6 percent, the expected one-year rate next year E(2r1) to be 3 percent, and the expected one-year rate the following year E(3r1) to be 5 percent. If the unbiased expectations theory of the term structure of interest rates holds, what is the one-year Treasury security rate, 1R1?

A) 3.00%

B) 10.13%

C) 14.00%

D) 19.88%

A) 3.00%

B) 10.13%

C) 14.00%

D) 19.88%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

52

Interest rates The Wall Street Journal reports that the current rate on 10-year Treasury bonds is 6.75 percent, on 20-year Treasury bonds is 7.25 percent, and on a 20-year corporate bond is 8.50 percent. Assume that the maturity risk premium is zero. If the default risk premium and liquidity risk premium on a 10-year corporate bond is the same as that on the 20-year corporate bond, what is the current rate on a 10-year corporate bond.

A) 7.50%

B) 8.00%

C) 8.50%

D) 8.75%

A) 7.50%

B) 8.00%

C) 8.50%

D) 8.75%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

53

Suppose that the current one-year rate (one-year spot rate) and expected one-year T-bill rates over the following 3 years (i.e., years 2, 3 and 4, respectively) are as follows: 1R1 = 5%, E(2r1) = 7%, E(3r1) = 7.5% E(4r1) = 7.85%

Using the unbiased expectations theory, calculate the current (long-term) rates for one-year and two-year -maturity Treasury securities.

A) One-year: 5.00%; Two-year: 5.50%

B) One-year: 5.00%; Two-year: 6.00%

C) One-year: 5.50%; Two-year: 6.15%

D) One-year: 5.50%; Two-year: 5.75%

Using the unbiased expectations theory, calculate the current (long-term) rates for one-year and two-year -maturity Treasury securities.

A) One-year: 5.00%; Two-year: 5.50%

B) One-year: 5.00%; Two-year: 6.00%

C) One-year: 5.50%; Two-year: 6.15%

D) One-year: 5.50%; Two-year: 5.75%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

54

Based on economists' forecasts and analysis, one-year Treasury bill rates and liquidity premiums for the next four years are expected to be as follows: R1 = 5.95%

E(r2) = 6.25% L2 = 0.05%

E(r3) = 6.75% L3 = 0.10%

E(r4) = 7.15% L4 = 0.12%

Using the liquidity premium hypothesis, what should be the current rate on four-year Treasury securities?

A) 6.59%

B) 6.75%

C) 6.82%

D) 7.13%

E(r2) = 6.25% L2 = 0.05%

E(r3) = 6.75% L3 = 0.10%

E(r4) = 7.15% L4 = 0.12%

Using the liquidity premium hypothesis, what should be the current rate on four-year Treasury securities?

A) 6.59%

B) 6.75%

C) 6.82%

D) 7.13%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

55

You are considering an investment in 30-year bonds issued by Moore Corporation. The bonds have no special covenants. The Wall Street Journal reports that 1-year T-bills are currently earning 3.55%. Your broker has determined the following information about economic activity and Moore Corporation bonds: Real interest rate = 2.75%

Default risk premium = 1.05%

Liquidity risk premium = 0.50%

Maturity risk premium = 1.85%

What is the inflation premium?

A) 0.80%

B) 1.25%

C) 6.25%

D) 8.00%

Default risk premium = 1.05%

Liquidity risk premium = 0.50%

Maturity risk premium = 1.85%

What is the inflation premium?

A) 0.80%

B) 1.25%

C) 6.25%

D) 8.00%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

56

A 2-year Treasury security currently earns 5.13%. Over the next 2 years, the real interest rate is expected to be 2.15% per year and the inflation premium is expected to be 1.75% per year. Calculate the maturity risk premium on the 2-year Treasury security.

A) 5.13%

B) 3.38%

C) 2.98%

D) 1.23%

A) 5.13%

B) 3.38%

C) 2.98%

D) 1.23%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

57

Forecasting Interest Rates A recent edition of The Wall Street Journal reported interest rates of 3.10 percent, 3.50 percent, 3.75 percent, and 3.95 percent for three-year, four-year, five-year, and six-year Treasury security yields, respectively, According to the unbiased expectation theory of the term structure of interest rates, what are the expected one-year rates for year 6?

A) 3.575%

B) 3.95%

C) 4.96%

D) 5.33%

A) 3.575%

B) 3.95%

C) 4.96%

D) 5.33%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

58

A particular security's default risk premium is 3%. For all securities, the inflation risk premium is 1.75% and the real interest rate is 4.2%. The security's liquidity risk premium is 0.35% and maturity risk premium is 0.95%. The security has no special covenants. Calculate the security's equilibrium rate of return.

A) 8.50%

B) 6.05%

C) 10.25%

D) 9.90%

A) 8.50%

B) 6.05%

C) 10.25%

D) 9.90%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

59

Forecasting Interest Rates Assume the current interest rate on a one-year Treasury bond (1R1) is 5.00 percent, the current rate on a two-year Treasury bond (1R2) is 5.75 percent, and the current rate on a three-year Treasury bond (1R3) is 6.25 percent. If the unbiased expectations theory of the term structure of interest rates is correct, what is the one-year interest rate expected on Treasury bills during year 3, 3f1?

A) 5.00%

B) 5.67%

C) 7.26%

D) 8.00%

A) 5.00%

B) 5.67%

C) 7.26%

D) 8.00%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

60

Interest rates The Wall Street Journal reports that the current rate on 5-year Treasury bonds is 6.50 percent and on 10-year Treasury bonds is 6.75 percent. Assume that the maturity risk premium is zero. Calculate the expected rate on a 5-year Treasury bond purchased five years from today, E(5r1).

A) 6.625%

B) 6.75%

C) 7.00%

D) 7.58%

A) 6.625%

B) 6.75%

C) 7.00%

D) 7.58%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

61

The Wall Street Journal reports that the current rate on 10-year Treasury bonds is 6.25%, on 20-year Treasury bonds is 7.95%, and on a 20-year corporate bond is 10.75%. Assume that the maturity risk premium is zero. If the default risk premium and liquidity risk premium on a 10-year corporate bond is the same as that on the 20-year corporate bond, calculate the current rate on a 10-year corporate bond.

A) 9.05%

B) 6.15%

C) 7.60%

D) 8.70%

A) 9.05%

B) 6.15%

C) 7.60%

D) 8.70%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

62

The Wall Street Journal reports that the current rate on 5-year Treasury bonds is 6.45% and on 10-year Treasury bonds is 7.75%. Assume that the maturity risk premium is zero. Calculate the expected rate on a 5-year Treasury bond purchased five years from today, E(5r5).

A) 7.25%

B) 8.12%

C) 9.07%

D) 10.16%

A) 7.25%

B) 8.12%

C) 9.07%

D) 10.16%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

63

Suppose we observe the three-year Treasury security rate (1R3) to be 11%, the expected one-year rate next year E(2r1) to be 4%, and the expected one-year rate the following year E(3r1) to be 5%. If the unbiased expectations theory of the term structure of interest rates holds, what is the one-year Treasury security rate, 1R1?

A) 18.57%

B) 10.19%

C) 23.19%

D) 25.24%

A) 18.57%

B) 10.19%

C) 23.19%

D) 25.24%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

64

On May 23, 20XX, the existing or current (spot) one-year, two-year, three-year, and four-year zero-coupon Treasury security rates were as follows: 1R1 = 4.55%, 1R2 = 4.75%, 1R3 = 5.25%, 1R4 = 5.95%

Using the unbiased expectations theory, calculate the one-year forward rates on zero-coupon Treasury bonds for years two, three, and four as of May 23, 20XX.

A) Year 1: 4.95%; Year 2: 6.26%; Year 3: 8.08%

B) Year 1: 3.75%; Year 2: 6.02%; Year 3: 9.00%

C) Year 1: 4.95%; Year 2: 7.26%; Year 3: 8.08%

D) Year 1: 3.65%; Year 2: 6.32%; Year 3: 11.08%

Using the unbiased expectations theory, calculate the one-year forward rates on zero-coupon Treasury bonds for years two, three, and four as of May 23, 20XX.

A) Year 1: 4.95%; Year 2: 6.26%; Year 3: 8.08%

B) Year 1: 3.75%; Year 2: 6.02%; Year 3: 9.00%

C) Year 1: 4.95%; Year 2: 7.26%; Year 3: 8.08%

D) Year 1: 3.65%; Year 2: 6.32%; Year 3: 11.08%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following statements is correct?

A) If the unbiased expectations theory is correct, we could see an inverted yield curve.

B) If a yield curve is inverted, long-term bonds have higher yields than short-term bonds.

C) If the maturity risk premium is zero, the yield curve would be flat.

D) If the unbiased expectations theory is correct, the maturity risk premium is zero.

A) If the unbiased expectations theory is correct, we could see an inverted yield curve.

B) If a yield curve is inverted, long-term bonds have higher yields than short-term bonds.

C) If the maturity risk premium is zero, the yield curve would be flat.

D) If the unbiased expectations theory is correct, the maturity risk premium is zero.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following statements is correct?

A) According to the unbiased expectations theory, the return for holding a 2-year bond to maturity is equal to the nominal rate divided by the real interest rate.

B) The rate on a 10-year Corporate can never be less than the rate on a 10-year Treasury.

C) We usually observe the inverted yield curve.

D) The rate on a 3-year Treasury can never be less than the rate on a 15-year Treasury.

A) According to the unbiased expectations theory, the return for holding a 2-year bond to maturity is equal to the nominal rate divided by the real interest rate.

B) The rate on a 10-year Corporate can never be less than the rate on a 10-year Treasury.

C) We usually observe the inverted yield curve.

D) The rate on a 3-year Treasury can never be less than the rate on a 15-year Treasury.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following statements is correct?

A) The default risk premium of Baa 20-year corporate bonds over Aaa 20-year corporate bonds does not vary.

B) The market segmentation theory assumes that borrowers and investors do not want to shift from one maturity sector to another without an interest rate premium.

C) Real interest rates are the rates that are quoted in the news.

D) All of these statements are correct.

A) The default risk premium of Baa 20-year corporate bonds over Aaa 20-year corporate bonds does not vary.

B) The market segmentation theory assumes that borrowers and investors do not want to shift from one maturity sector to another without an interest rate premium.

C) Real interest rates are the rates that are quoted in the news.

D) All of these statements are correct.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

68

Assume the current interest rate on a one-year Treasury bond (1R1) is 5.50%, the current rate on a two-year Treasury bond (1R2) is 5.95%, and the current rate on a three-year Treasury bond (1R3) is 8.50%. If the unbiased expectations theory of the term structure of interest rates is correct, what is the one-year interest rate expected on Treasury bills during year 3, 3f1?

A) 13.79%

B) 12.29%

C) 11.69%

D) 10.29%

A) 13.79%

B) 12.29%

C) 11.69%

D) 10.29%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

69

One-year interest rates are 3%. The market expects one-year rates to be 5% one year from now. The market also expects one-year rates to be 7% two years from now. Assume that the unbiased expectations theory holds. Which of the following is correct?

A) The yield curve is downward sloping.

B) The yield curve is flat.

C) The yield curve is upward sloping.

D) We need the maturity risk premiums to be able to answer this question.

A) The yield curve is downward sloping.

B) The yield curve is flat.

C) The yield curve is upward sloping.

D) We need the maturity risk premiums to be able to answer this question.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

70

One-year Treasury bill rates in 20XX averaged 5.15% and inflation for the year was 7.3%. If investors had expected the same inflation rate as that realized, calculate the real interest rate for 20XX according to the Fisher effect.

A) 0.00%

B) -2.15%

C) 2.15%

D) 3.95%

A) 0.00%

B) -2.15%

C) 2.15%

D) 3.95%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

71

You note the following yield curve in The Wall Street Journal. According to the unbiased expectations hypothesis, what is the one-year forward rate for the period beginning one year from today, 2f1?

A) 7.6%

B) 8.6%

C) 9.0%

D) 10.2%

A) 7.6%

B) 8.6%

C) 9.0%

D) 10.2%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

72

If the yield curve is downward sloping, what is the yield to maturity on a 30-year Treasury bond relative to a 10-year Treasury bond?

A) The yield on the 10-year bond must be greater than the yield on the 30-year bond.

B) The yield on the 10-year bond must be less than the yield on the 30-year bond.

C) The yields on the two bonds are equal.

D) We need to know the other risk premiums to answer this question.

A) The yield on the 10-year bond must be greater than the yield on the 30-year bond.

B) The yield on the 10-year bond must be less than the yield on the 30-year bond.

C) The yields on the two bonds are equal.

D) We need to know the other risk premiums to answer this question.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

73

Suppose we observe the following rates: 1R1 = 13%, 1R2 = 16%, and E(2r1) = 10%. If the liquidity premium theory of the term structure of interest rates holds, what is the liquidity premium for year 2, L2?

A) 8.7%

B) 9.1%

C) 9.7%

D) 10.0%

A) 8.7%

B) 9.1%

C) 9.7%

D) 10.0%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

74

The Wall Street Journal states that the yield curve for Treasuries is downward sloping and there is no liquidity premium or maturity risk premium. Given this information, which of the following statements is correct?

A) A 30-year corporate bond must have a higher yield than a 5-year corporate bond.

B) A 5-year corporate bond must have a higher yield than a 30-year Treasury bond.

C) A 5-year Treasury bond must have a higher yield than a 5-year corporate bond.

D) All of these statements are correct.

A) A 30-year corporate bond must have a higher yield than a 5-year corporate bond.

B) A 5-year corporate bond must have a higher yield than a 30-year Treasury bond.

C) A 5-year Treasury bond must have a higher yield than a 5-year corporate bond.

D) All of these statements are correct.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

75

The Wall Street Journal reports that the rate on 4-year Treasury securities is 7.50% and the rate on 5-year Treasury securities is 9.15%. According to the unbiased expectations hypotheses, what does the market expect the 1-year Treasury rate to be four years from today, E(5r1)?

A) 16.0%

B) 18.4%

C) 15.9%

D) 13.7%

A) 16.0%

B) 18.4%

C) 15.9%

D) 13.7%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

76

Which of the following statements is correct?

A) An IPO is an example of a primary market transaction.

B) Money markets are subject to wider price fluctuations and are therefore more risky than capital market instruments.

C) A direct transfer of funds is more efficient than utilizing financial institutions.

D) The market segmentation theory argues that the different investors have different risk preferences which determine the shape of the yield curve.

A) An IPO is an example of a primary market transaction.

B) Money markets are subject to wider price fluctuations and are therefore more risky than capital market instruments.

C) A direct transfer of funds is more efficient than utilizing financial institutions.

D) The market segmentation theory argues that the different investors have different risk preferences which determine the shape of the yield curve.

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

77

Suppose we observe the following rates: 1R1 = 12%, 1R2 = 15%. If the unbiased expectations theory of the term structure of interest rates holds, what is the one-year interest rate expected one year from now, E(2r1)?

A) 13.5%

B) 14.2%

C) 15.6%

D) 18.0%

A) 13.5%

B) 14.2%

C) 15.6%

D) 18.0%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

78

In 20XX, the 10-year Treasury rate was 4.5% while the average 10-year Aaa corporate bond debt carried an interest rate of 6.0%. What is the average default risk premium on Aaa corporate bonds?

A) 0.75%

B) 1.5%

C) 1.95%

D) 2.25%

A) 0.75%

B) 1.5%

C) 1.95%

D) 2.25%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

79

Assume that you observe the following rates on long-term bonds: U.S. Treasury bonds = 4.15%

AAA Corporate bonds = 6.2%

BBB Corporate bonds = 7.15%

The main reason for the differences in the interest rates is:

A) Maturity risk premium

B) Inflation premium

C) Default risk premium

D) Convertibility premium

AAA Corporate bonds = 6.2%

BBB Corporate bonds = 7.15%

The main reason for the differences in the interest rates is:

A) Maturity risk premium

B) Inflation premium

C) Default risk premium

D) Convertibility premium

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

80

The Wall Street Journal reports that the rate on 3-year Treasury securities is 7.25% and the rate on 4-year Treasury securities is 8.50%. The one-year interest rate expected in three years is E(4r1), 4.10%. According to the liquidity premium hypotheses, what is the liquidity premium on the 4-year Treasury security, L4?

A) 6.7%

B) 7.1%

C) 8.2%

D) 9.6%

A) 6.7%

B) 7.1%

C) 8.2%

D) 9.6%

Unlock Deck

Unlock for access to all 104 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 104 flashcards in this deck.