Deck 13: Implementing the Binomial Model

Full screen (f)

Question

Question

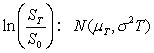

Stock ABC is currently trading at 100.The stock has lognormal returns with with  and

and  .What is the 95% confidence interval for the stock price in 3 months?

.What is the 95% confidence interval for the stock price in 3 months?

(a)

(b)

(c)

D)Cannot be calculated from the given information.

and .What is the 95% confidence interval for the stock price in 3 months?(a)

(b)

(c)

D)Cannot be calculated from the given information.

Question

Question

Question

Suppose the returns on a stock are lognormally distributed with  and

and  .The expected three-month simple returns on the stock are

.The expected three-month simple returns on the stock are

A)0.

B)0.25%

C)0.50%

D)1.01%

and .The expected three-month simple returns on the stock areA)0.

B)0.25%

C)0.50%

D)1.01%

Question

If  is normally distributed with mean

is normally distributed with mean  and variance

and variance  ,then

,then  is

is

A)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

is normally distributed with mean and variance ,then isA)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

Question

Assume that a stock has lognormal returns with mean  and standard deviation

and standard deviation  .The current stock price is $50.What is a 95% confidence interval for the stock price in six months?

.The current stock price is $50.What is a 95% confidence interval for the stock price in six months?

A)37.90,65.97

B)37.81,73.08

C)39.84,69.35

D)40.12,60.24

and standard deviation .The current stock price is $50.What is a 95% confidence interval for the stock price in six months?A)37.90,65.97

B)37.81,73.08

C)39.84,69.35

D)40.12,60.24

Question

Let  denote the time-

denote the time-  price of a stock and

price of a stock and  its current price.Suppose that for any

its current price.Suppose that for any  ,

,  for constant annual parameters

for constant annual parameters  and

and  .What does this imply about the returns process? Pick the most accurate of the following alternatives:

.What does this imply about the returns process? Pick the most accurate of the following alternatives:

A)The returns are independent and identically distributed over time.

B)The returns are independent over time.

C)The returns are normally distributed.

D)None of the above.

denote the time- price of a stock and its current price.Suppose that for any , for constant annual parameters and .What does this imply about the returns process? Pick the most accurate of the following alternatives:A)The returns are independent and identically distributed over time.

B)The returns are independent over time.

C)The returns are normally distributed.

D)None of the above.

Question

Question

If  is normally distributed with mean

is normally distributed with mean  and variance

and variance  ,then

,then  is

is

A)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

is normally distributed with mean and variance ,then isA)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

Question

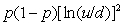

Consider a binomial tree in which the stock moves up by a factor  and down by a factor

and down by a factor  ,respectively with probabilities

,respectively with probabilities  and

and  .The variance of log-returns per time step is given by the following formula:

.The variance of log-returns per time step is given by the following formula:

(a)

(b)

(c)

(d)

and down by a factor ,respectively with probabilities and .The variance of log-returns per time step is given by the following formula:(a)

(b)

(c)

(d)

Question

In the Cox-Ross-Rubinstein (CRR)binomial model,the volatility is given as  .The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?

.The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?

A)0.45

B)0.50

C)0.55

D)0.60

.The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?A)0.45

B)0.50

C)0.55

D)0.60

Question

Question

Question

In the Jarrow-Rudd (JR)binomial model,the volatility is given as  .The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?

.The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?

A)0.45

B)0.50

C)0.55

D)0.60

.The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?A)0.45

B)0.50

C)0.55

D)0.60

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/16

Play

Full screen (f)

Deck 13: Implementing the Binomial Model

1

Suppose returns on a stock are lognormally distributed with expected (annualized)mean of of 0.10 and standard deviation of 0.20.What is the standard deviation of simple return on the stock for one month?

A)0.10

B)0.34

C)0.58

D)0.67

A)0.10

B)0.34

C)0.58

D)0.67

C

The variance of the simple return is The standard deviation of simple return is

The standard deviation of simple return is  .

.

The variance of the simple return is

The standard deviation of simple return is . 2

Stock ABC is currently trading at 100.The stock has lognormal returns with with and .What is the 95% confidence interval for the stock price in 3 months?

(a)

(b)

(c)

D)Cannot be calculated from the given information.

and .What is the 95% confidence interval for the stock price in 3 months?(a)

(b)

(c)

D)Cannot be calculated from the given information.

B

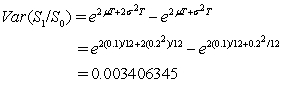

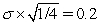

The standard deviation of three-month log returns is .So the 95% confidence interval for three-month log-returns is

.So the 95% confidence interval for three-month log-returns is  Exponentiating both sides and using the initial price of 100,we obtain the 95% confidence interval for the stock price in 3 months as

Exponentiating both sides and using the initial price of 100,we obtain the 95% confidence interval for the stock price in 3 months as  .

.

The standard deviation of three-month log returns is

.So the 95% confidence interval for three-month log-returns is Exponentiating both sides and using the initial price of 100,we obtain the 95% confidence interval for the stock price in 3 months as . 3

Suppose returns on a stock are lognormally distributed with expected (annualized)mean of of 0.10 and standard deviation of 0.20.What is the standard deviation of the continuously compounded return on the stock for one month?

A)1.77%

B)3.33%

C)5.77%

D)7.33%

A)1.77%

B)3.33%

C)5.77%

D)7.33%

C

The standard deviation is .

.

The standard deviation is

. 4

Suppose returns on a stock are lognormally distributed with expected (annualized)mean of of 0.10 and standard deviation of 0.20.What is the expected simple return on the stock for one month?

A)0.83

B)1.01

C)1.08

D)1.13

A)0.83

B)1.01

C)1.08

D)1.13

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

5

Suppose the returns on a stock are lognormally distributed with and .The expected three-month simple returns on the stock are

A)0.

B)0.25%

C)0.50%

D)1.01%

and .The expected three-month simple returns on the stock areA)0.

B)0.25%

C)0.50%

D)1.01%

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

6

If is normally distributed with mean and variance ,then is

A)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

is normally distributed with mean and variance ,then isA)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

7

Assume that a stock has lognormal returns with mean and standard deviation .The current stock price is $50.What is a 95% confidence interval for the stock price in six months?

A)37.90,65.97

B)37.81,73.08

C)39.84,69.35

D)40.12,60.24

and standard deviation .The current stock price is $50.What is a 95% confidence interval for the stock price in six months?A)37.90,65.97

B)37.81,73.08

C)39.84,69.35

D)40.12,60.24

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

8

Let denote the time- price of a stock and its current price.Suppose that for any , for constant annual parameters and .What does this imply about the returns process? Pick the most accurate of the following alternatives:

A)The returns are independent and identically distributed over time.

B)The returns are independent over time.

C)The returns are normally distributed.

D)None of the above.

denote the time- price of a stock and its current price.Suppose that for any , for constant annual parameters and .What does this imply about the returns process? Pick the most accurate of the following alternatives:A)The returns are independent and identically distributed over time.

B)The returns are independent over time.

C)The returns are normally distributed.

D)None of the above.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements is most valid for the recursive programming of a binomial tree for pricing options?

A)The recursive program requires more lines of code than a non-recursive loop-driven program.

B)The recursive program requires less computer memory than a non-recursive loop-driven program.

C)The recursive program runs slower than a non-recursive loop-driven program.

D)The recursive program runs in polynomial time whereas a non-recursive loop-driven program runs in exponential time.

A)The recursive program requires more lines of code than a non-recursive loop-driven program.

B)The recursive program requires less computer memory than a non-recursive loop-driven program.

C)The recursive program runs slower than a non-recursive loop-driven program.

D)The recursive program runs in polynomial time whereas a non-recursive loop-driven program runs in exponential time.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

10

If is normally distributed with mean and variance ,then is

A)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

is normally distributed with mean and variance ,then isA)Normally distributed.

B)Lognormally distributed.

C)Exponentially distributed.

D)None of the above.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

11

Consider a binomial tree in which the stock moves up by a factor and down by a factor ,respectively with probabilities and .The variance of log-returns per time step is given by the following formula:

(a)

(b)

(c)

(d)

and down by a factor ,respectively with probabilities and .The variance of log-returns per time step is given by the following formula:(a)

(b)

(c)

(d)

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

12

In the Cox-Ross-Rubinstein (CRR)binomial model,the volatility is given as .The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?

A)0.45

B)0.50

C)0.55

D)0.60

.The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?A)0.45

B)0.50

C)0.55

D)0.60

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

13

As the number of steps in the CRR binomial tree increases (keeping maturity fixed),the solution "converges" to a limit result.Which of the following statements characterizes this convergence best?

A)The solution results in the Black-Scholes formula.

B)The convergence may be oscillatory for even and odd number of steps in the tree.

C)The convergence may be monotonic for even and odd number of steps in the tree.

D)All of the above.

A)The solution results in the Black-Scholes formula.

B)The convergence may be oscillatory for even and odd number of steps in the tree.

C)The convergence may be monotonic for even and odd number of steps in the tree.

D)All of the above.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

14

Suppose you are modeling the price evolution of a stock on a tree using a general version of the CRR model.The stock price is stochastic (lognormal),but the rate of interest each time step may not be the same,and the time step itself may be different across periods.The following is sufficient for a binomial tree representation of the stock price process to be recombining:

A)The volatility of the stock is constant each period,and the time step and interest rate are different each period.

B)The volatility of the stock is constant each period,the time step on the tree is the same each period,and the interest rate may be different each period.

C)The volatility of the stock is constant,the time step on the tree is the different each period,and the up and down probabilities are equal.

D)The volatility of the stock is different each period,the time step on the tree is the same each period,and the interest rate is the same each period.

A)The volatility of the stock is constant each period,and the time step and interest rate are different each period.

B)The volatility of the stock is constant each period,the time step on the tree is the same each period,and the interest rate may be different each period.

C)The volatility of the stock is constant,the time step on the tree is the different each period,and the up and down probabilities are equal.

D)The volatility of the stock is different each period,the time step on the tree is the same each period,and the interest rate is the same each period.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

15

In the Jarrow-Rudd (JR)binomial model,the volatility is given as .The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?

A)0.45

B)0.50

C)0.55

D)0.60

.The risk-free rate of interest is 2%.What is the risk-neutral probability of an up move on a binomial tree with a time step of one month?A)0.45

B)0.50

C)0.55

D)0.60

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

16

Suppose returns on a stock are lognormally distributed with expected (annualized)mean of of 0.10 and standard deviation of 0.20.What is the expected continuously compounded return on the stock for one month?

A)0.100%

B)0.333%

C)0.833%

D)1.667%

A)0.100%

B)0.333%

C)0.833%

D)1.667%

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 16 flashcards in this deck.