Deck 8: Analysis of Perfectly Competitive Markets

Full screen (f)

Question

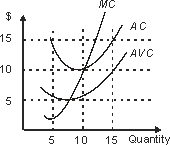

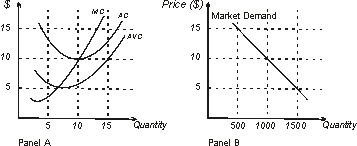

Suppose that all the firms in a given market can be characterized by the cost structure illustrated in the figure on the left.If market demand is as indicated in the figure on the right, the number of firms required to support long run equilibrium is:

A)90.

B)100.

C)110.

D)120.

E)some number greater than 50 that cannot be determined with the information provided.

A)90.

B)100.

C)110.

D)120.

E)some number greater than 50 that cannot be determined with the information provided.

Question

Question

Question

Question

Question

Question

Question

Question

Question

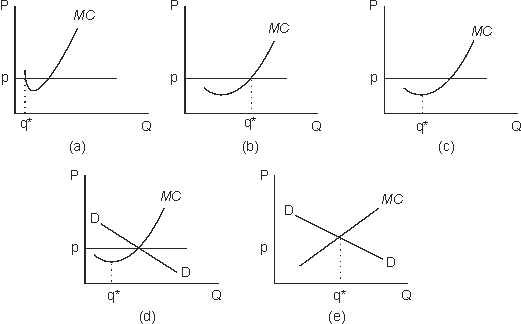

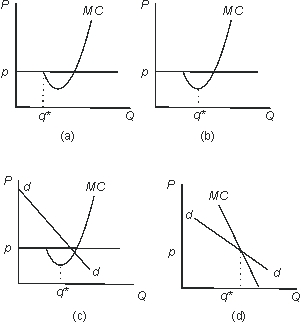

Which panel in the figure below most accurately indicates by q* the level of output which a single supplier in a perfectly competitive industry will produce, given it produces a positive amount?

A)a

B)b

C)c

D)d

E)e

A)a

B)b

C)c

D)d

E)e

Question

Question

Question

Question

Question

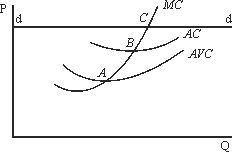

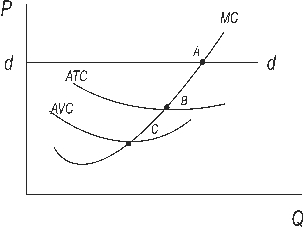

Which of the following statements is correct in reference to the figure below?

A)B is the shutdown point.

B)B is the profit-maximizing point.

C)C is the zero-profit point.

D)A is the shutdown point.

E)C is the shutdown point.

A)B is the shutdown point.

B)B is the profit-maximizing point.

C)C is the zero-profit point.

D)A is the shutdown point.

E)C is the shutdown point.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Which of the following statements is correct with reference to the figure below?

A)A is the shutdown point.

B)B is the zero-profit point.

C)C is the zero-profit point.

D)B is the shutdown point.

E)B is the profit-maximizing point.

A)A is the shutdown point.

B)B is the zero-profit point.

C)C is the zero-profit point.

D)B is the shutdown point.

E)B is the profit-maximizing point.

Question

Question

Question

Which of the panels in the figure below best indicates with q* the level of output that a supplier in a perfectly competitive industry will produce?

A)a

B)b

C)c

D)d

E)None of the above.

A)a

B)b

C)c

D)d

E)None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions :

Figure 8-1

In Figure 8-1, in the long-run the firm's economic profits will equal:

A)0.

B)$40.

C)$100.

D)$150.

E)none of the above.

Figure 8-1

In Figure 8-1, in the long-run the firm's economic profits will equal:

A)0.

B)$40.

C)$100.

D)$150.

E)none of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions :

Figure 8-1

If the market price increases to $15, the firm depicted in Figure 8-1 will:

A)shutdown.

B)earn economic profits.

C)produce more than 10 units of output.

D)produce less than 10 units of output.

E)both B and C are correct.

Figure 8-1

If the market price increases to $15, the firm depicted in Figure 8-1 will:

A)shutdown.

B)earn economic profits.

C)produce more than 10 units of output.

D)produce less than 10 units of output.

E)both B and C are correct.

Question

Question

Use the following to answer questions :

Figure 8-1

In Figure 8-1, the long run equilibrium competitive price is:

A)$5.

B)$7.

C)$10.

D)greater than $10.

E)some positive number that cannot be determined without seeing the market demand curve.

Figure 8-1

In Figure 8-1, the long run equilibrium competitive price is:

A)$5.

B)$7.

C)$10.

D)greater than $10.

E)some positive number that cannot be determined without seeing the market demand curve.

Question

Question

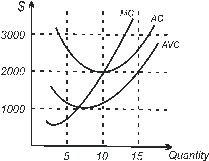

Use the following to answer questions :

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive level of output is 5.

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive level of output is 5.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions :

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive equilibrium price is $1000.

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive equilibrium price is $1000.

Question

Question

Question

Question

Question

Question

Question

Given the market demand drawn in Panel B of the figure below and the cost structure for the typical firms shown in Panel A of the figure below, the long-run total output of the industry is 900 units.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/80

Play

Full screen (f)

Deck 8: Analysis of Perfectly Competitive Markets

1

Suppose that all the firms in a given market can be characterized by the cost structure illustrated in the figure on the left.If market demand is as indicated in the figure on the right, the number of firms required to support long run equilibrium is:

A)90.

B)100.

C)110.

D)120.

E)some number greater than 50 that cannot be determined with the information provided.

A)90.

B)100.

C)110.

D)120.

E)some number greater than 50 that cannot be determined with the information provided.

100.

2

Which of the following is an important function of prices in a competitive market economy?

A)Ensuring an equal distribution of goods and services.

B)Ensuring that resources are used in the most efficient manner.

C)Ensuring that all industries will be perfectly competitive in the long run.

D)Equating the marginal utilities of all goods consumed.

E)Equating level of purchases with level of needs.

A)Ensuring an equal distribution of goods and services.

B)Ensuring that resources are used in the most efficient manner.

C)Ensuring that all industries will be perfectly competitive in the long run.

D)Equating the marginal utilities of all goods consumed.

E)Equating level of purchases with level of needs.

Ensuring that resources are used in the most efficient manner.

3

If four firms constituting a competitive industry have the supply schedules given below, then their combined market supply may be stated as: Ql s= 16 + 4P Q3 s= 32 + 8P

Q2 s= 5 + 5P Q4 s= 60 + 10P

A)Q = 113 - 27P.

B)Q = 113 + 27P.

C)Q = 51 + 4P.

D)Q = 92 + 18P.

E)none of the above.

Q2 s= 5 + 5P Q4 s= 60 + 10P

A)Q = 113 - 27P.

B)Q = 113 + 27P.

C)Q = 51 + 4P.

D)Q = 92 + 18P.

E)none of the above.

Q = 113 + 27P.

4

If prices rise in a perfectly competitive industry, then in the short run the firms in that industry will:

A)bid for more resources.

B)reduce marginal costs.

C)decrease production.

D)increase plant capacity.

E)none of the above.

A)bid for more resources.

B)reduce marginal costs.

C)decrease production.

D)increase plant capacity.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

5

What is the underlying reason that maximum profit comes at the level of output where marginal cost equals price?

A)there is additional profit as long as the price is greater than the marginal cost of the last unit.

B)there is additional profit when the marginal cost of a unit is higher than the price.

C)there is no more profit when the price is greater than the marginal cost of the last unit.

D)price is not important in determining profit.

E)none of the above.

A)there is additional profit as long as the price is greater than the marginal cost of the last unit.

B)there is additional profit when the marginal cost of a unit is higher than the price.

C)there is no more profit when the price is greater than the marginal cost of the last unit.

D)price is not important in determining profit.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

6

If you are a wheat farmer and you want to earn as much profit as you can, you should do which of the following:

A)try to produce and sell that quantity of output at which marginal cost has risen to equality with price.

B)try to produce and sell that quantity of output at which marginal cost is equal to average variable cost.

C)try to produce and sell that quantity of output at which marginal cost has reached its minimum possible level.

D)never let marginal cost reach equality with price, since this is the point at which profits become zero.

E)keep marginal cost above price.

A)try to produce and sell that quantity of output at which marginal cost has risen to equality with price.

B)try to produce and sell that quantity of output at which marginal cost is equal to average variable cost.

C)try to produce and sell that quantity of output at which marginal cost has reached its minimum possible level.

D)never let marginal cost reach equality with price, since this is the point at which profits become zero.

E)keep marginal cost above price.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

7

A supplier in a perfectly competitive market is characterized by all but which of the following?

A)It can influence the price of its product.

B)It produces such that marginal cost equals price.

C)It can sell all it wants to at the prevailing market price.

D)It produces a positive amount in the short run if it can recover variable costs.

E)None of the above are incorrect.

A)It can influence the price of its product.

B)It produces such that marginal cost equals price.

C)It can sell all it wants to at the prevailing market price.

D)It produces a positive amount in the short run if it can recover variable costs.

E)None of the above are incorrect.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

8

The zero-profit point for a perfectly competitive firm occurs where the price equals the minimum point of the:

A)AVC curve.

B)AC curve.

C)MC curve.

D)AFC curve.

E)none of the above.

A)AVC curve.

B)AC curve.

C)MC curve.

D)AFC curve.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

9

Profit maximization requires a firm to do which of the following:

A)manage internal operations efficiently.

B)prevent waste.

C)encourage worker morale.

D)choose efficient production processes.

E)all of the above.

A)manage internal operations efficiently.

B)prevent waste.

C)encourage worker morale.

D)choose efficient production processes.

E)all of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

10

Which panel in the figure below most accurately indicates by q* the level of output which a single supplier in a perfectly competitive industry will produce, given it produces a positive amount?

A)a

B)b

C)c

D)d

E)e

A)a

B)b

C)c

D)d

E)e

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

11

If all the firms in a perfectly competitive industry that is characterized by constant costs are charging a price equal to marginal cost, then an upward shift in demand will in the long run (if there are marginal firms which have not yet entered the industry):

A)cause each firm's marginal cost curve to move to the right.

B)cause the industry price to rise.

C)cause the industry price to fall.

D)have no effect on the industry price.

E)cause excess capacity.

A)cause each firm's marginal cost curve to move to the right.

B)cause the industry price to rise.

C)cause the industry price to fall.

D)have no effect on the industry price.

E)cause excess capacity.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

12

In long-run equilibrium, a firm in a perfectly competitive industry will produce at the point where:

A)marginal cost equals average total cost.

B)total revenue is maximized.

C)marginal cost equals average variable cost.

D)its opportunity cost is lowest.

E)price equals average fixed cost.

A)marginal cost equals average total cost.

B)total revenue is maximized.

C)marginal cost equals average variable cost.

D)its opportunity cost is lowest.

E)price equals average fixed cost.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

13

In a market economy, the short-run reaction to a shortage of a commodity after an increase in demand will be that:

A)price will fall, but profits will increase.

B)price will rise, but profits decrease.

C)price will rise, but profits remain unchanged.

D)price and profits will both rise.

E)output will fall, but price rises.

A)price will fall, but profits will increase.

B)price will rise, but profits decrease.

C)price will rise, but profits remain unchanged.

D)price and profits will both rise.

E)output will fall, but price rises.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

14

The shutdown point is that point at which

A)price equals marginal cost.

B)average fixed cost equals marginal cost.

C)average variable cost equals marginal cost.

D)average total cost equals marginal cost.

E)none of the above.

A)price equals marginal cost.

B)average fixed cost equals marginal cost.

C)average variable cost equals marginal cost.

D)average total cost equals marginal cost.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements is correct in reference to the figure below?

A)B is the shutdown point.

B)B is the profit-maximizing point.

C)C is the zero-profit point.

D)A is the shutdown point.

E)C is the shutdown point.

A)B is the shutdown point.

B)B is the profit-maximizing point.

C)C is the zero-profit point.

D)A is the shutdown point.

E)C is the shutdown point.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

16

"I'm losing money, but with my investment in equipment I can't afford to shut down at this time." If this entrepreneur is attempting to maximize profits, his behavior is:

A)rational if the firm is covering its variable costs.

B)rational if the firm is covering its fixed costs.

C)irrational since plant closing is necessary to eliminate losses.

D)irrational since fixed costs are eliminated if a firm shuts down.

E)none of the above.

A)rational if the firm is covering its variable costs.

B)rational if the firm is covering its fixed costs.

C)irrational since plant closing is necessary to eliminate losses.

D)irrational since fixed costs are eliminated if a firm shuts down.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

17

If you are losing money on your wheat farm, you should consider changing to another crop when which of the following is true:

A)when the price falls below average variable costs.

B)when the price equals costs.

C)when the price is above costs.

D)when the price equals zero profits.

E)none of the above.

A)when the price falls below average variable costs.

B)when the price equals costs.

C)when the price is above costs.

D)when the price equals zero profits.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

18

If a firm in circumstances of perfect competition finds that, at its best possible operating position, total revenue is not sufficient to cover total variable costs, it should:

A)plan to shut down, even in the short run.

B)plan to continue operating permanently.

C)continue to operate if, at this same level of output, price per unit is sufficient to cover average cost.

D)increase the price it is charging.

E)decrease the price it is charging.

A)plan to shut down, even in the short run.

B)plan to continue operating permanently.

C)continue to operate if, at this same level of output, price per unit is sufficient to cover average cost.

D)increase the price it is charging.

E)decrease the price it is charging.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is true at the quantity of output where average cost (AC)has reached its minimum level?

A)AVC = FC

B)MC = AVC

C)MC = AC

D)AC = AFC

E)P = AVC

A)AVC = FC

B)MC = AVC

C)MC = AC

D)AC = AFC

E)P = AVC

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

20

The long-run supply curve of an individual firm in perfect competition is the same thing as:

A)the rising segment of its marginal cost curve, above average cost.

B)the rising segment of its average cost curve.

C)its entire average cost curve.

D)that entire part of its total cost curve in which total cost rises or remains constant as output increases.

E)none of the above.

A)the rising segment of its marginal cost curve, above average cost.

B)the rising segment of its average cost curve.

C)its entire average cost curve.

D)that entire part of its total cost curve in which total cost rises or remains constant as output increases.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

21

In the long run, all firms in a perfectly competitive industry will operate at the point where:

A)marginal cost is minimized.

B)social welfare is compromised by overextended resources.

C)marginal cost equals average fixed costs.

D)marginal cost equals average total cost.

E)none of the above.

A)marginal cost is minimized.

B)social welfare is compromised by overextended resources.

C)marginal cost equals average fixed costs.

D)marginal cost equals average total cost.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

22

If, in long run equilibrium, the competitive price of some good is $16.67, then, for each and every firm in the industry,

A)marginal cost > average cost = $16.67.

B)marginal cost < average cost = $16.67.

C)$16.67 = marginal cost = average cost.

D)$16.67 = marginal cost > average cost.

E)$16.67 = marginal cost < average cost.

A)marginal cost > average cost = $16.67.

B)marginal cost < average cost = $16.67.

C)$16.67 = marginal cost = average cost.

D)$16.67 = marginal cost > average cost.

E)$16.67 = marginal cost < average cost.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following characterizes a supplier of a good in a perfectly competitive market?

A)It can influence the price of its product.

B)In the short run, it produces a positive amount only if price is greater than average total cost.

C)It chooses output such that marginal cost equals price.

D)In the long run, it will shut down if price exceeds average variable cost.

E)None of the above.

A)It can influence the price of its product.

B)In the short run, it produces a positive amount only if price is greater than average total cost.

C)It chooses output such that marginal cost equals price.

D)In the long run, it will shut down if price exceeds average variable cost.

E)None of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

24

Since you cannot add another corner in Times Square regardless of the rent you can charge, we call the payment for the corners in Times Square what?

A)pure economic rent.

B)pure economic wage.

C)fixed rent.

D)high demand rent.

E)none of the above.

A)pure economic rent.

B)pure economic wage.

C)fixed rent.

D)high demand rent.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

25

In a market economy, the short-run reaction to an excess supply of a commodity after a decrease in demand is that the price will:

A)rise, but profits fall.

B)fall and profits will fall.

C)fall, but profits will be unchanged.

D)fall, but profits will increase.

E)rise and profits will both increase.

A)rise, but profits fall.

B)fall and profits will fall.

C)fall, but profits will be unchanged.

D)fall, but profits will increase.

E)rise and profits will both increase.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

26

When there are only perfectly competitive producers in a market economy, there will be an efficient allocation of resources (ignoring externalities)because:

A)even though excess profits are earned in some industries, capital is prevented from moving into those industries.

B)even though excess profits are earned in some industries, there will be excess losses earned in other industries.

C)some firms will produce too little output and other firms will produce too much output.

D)the prices of goods will tend to reflect their marginal costs of production.

E)none of the above.

A)even though excess profits are earned in some industries, capital is prevented from moving into those industries.

B)even though excess profits are earned in some industries, there will be excess losses earned in other industries.

C)some firms will produce too little output and other firms will produce too much output.

D)the prices of goods will tend to reflect their marginal costs of production.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

27

If prices fall in a perfectly competitive industry, then the firms in that industry will in the short run:

A)not decrease in number unless price falls below ATC for some firms.

B)try to reduce production or shut down.

C)keep output at the same level but make losses.

D)advertise.

E)both A and B.

A)not decrease in number unless price falls below ATC for some firms.

B)try to reduce production or shut down.

C)keep output at the same level but make losses.

D)advertise.

E)both A and B.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

28

When an economy is in the position where no person can be made better off without making another person worse off, it:

A)income will be distributed equally.

B)exhibits allocative efficiency.

C)has maximized its social utility irrespective of any pollution.

D)has eliminated all opportunity costs.

E)has distributed all opportunity cost as equitably as possible.

A)income will be distributed equally.

B)exhibits allocative efficiency.

C)has maximized its social utility irrespective of any pollution.

D)has eliminated all opportunity costs.

E)has distributed all opportunity cost as equitably as possible.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

29

If a competitive firm must sell its output at the going price and wants to maximize profits, it should:

A)produce at its zero-profit point.

B)produce where average cost equals price.

C)produce where marginal cost equals price.

D)sell as much as it can produce.

E)none of the above.

A)produce at its zero-profit point.

B)produce where average cost equals price.

C)produce where marginal cost equals price.

D)sell as much as it can produce.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

30

In the long run, falling average cost curves over the relevant range of output lead to:

A)perfect competition.

B)zero total profit.

C)imperfect competition.

D)allocative efficiency.

E)any of the above.

A)perfect competition.

B)zero total profit.

C)imperfect competition.

D)allocative efficiency.

E)any of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

31

If all firms in an industry which is characterized by decreasing costs are charging a price equal to marginal cost, then an upward shift in demand in the long run will:

A)increase industry output and lower price.

B)decrease industry output and raise price.

C)alter neither industry output nor price.

D)result in much more competitive industry structure.

E)do none of the above.

A)increase industry output and lower price.

B)decrease industry output and raise price.

C)alter neither industry output nor price.

D)result in much more competitive industry structure.

E)do none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

32

The zero-profit price for a firm in perfect competition:

A)is a price just sufficient to cover fixed cost.

B)is at the point where total revenue from sales is at its minimum level.

C)occurs at the point where marginal and average cost are equal.

D)occurs at the point where marginal cost is at its minimum level.

E)is not correctly described by any of the above.

A)is a price just sufficient to cover fixed cost.

B)is at the point where total revenue from sales is at its minimum level.

C)occurs at the point where marginal and average cost are equal.

D)occurs at the point where marginal cost is at its minimum level.

E)is not correctly described by any of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

33

When dealing with the economics of the business firm, the short run is defined as a period long enough to:

A)gather cost data but not production data.

B)gather cost data and production data.

C)vary output but not plant capacity.

D)vary output and plant capacity.

E)vary plant capacity but not output.

A)gather cost data but not production data.

B)gather cost data and production data.

C)vary output but not plant capacity.

D)vary output and plant capacity.

E)vary plant capacity but not output.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

34

The short-run supply curve of a firm in perfect competition is the rising segment of its short-run:

A)marginal cost curve.

B)average fixed cost curve.

C)average variable cost curve.

D)marginal cost curve above its average variable cost curve.

E)average total cost curve.

A)marginal cost curve.

B)average fixed cost curve.

C)average variable cost curve.

D)marginal cost curve above its average variable cost curve.

E)average total cost curve.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements is correct with reference to the figure below?

A)A is the shutdown point.

B)B is the zero-profit point.

C)C is the zero-profit point.

D)B is the shutdown point.

E)B is the profit-maximizing point.

A)A is the shutdown point.

B)B is the zero-profit point.

C)C is the zero-profit point.

D)B is the shutdown point.

E)B is the profit-maximizing point.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

36

Pareto efficiency occurs:

A)when no possible reorganization of production or distribution can make anyone better off without making someone else worse off.

B)when everyone gets a fair share of the goods produced.

C)when reorganizing the production makes everyone better off.

D)when I am better off and everyone else stays the same.

E)none of the above.

A)when no possible reorganization of production or distribution can make anyone better off without making someone else worse off.

B)when everyone gets a fair share of the goods produced.

C)when reorganizing the production makes everyone better off.

D)when I am better off and everyone else stays the same.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

37

Allocative efficiency occurs when:

A)marginal social utility equals marginal social cost.

B)all industries are monopolized.

C)all externalities are eliminated.

D)marginal social cost equals the minimum of average social cost.

E)marginal social cost equals average social cost, though not necessarily at the minimum of average social cost.

A)marginal social utility equals marginal social cost.

B)all industries are monopolized.

C)all externalities are eliminated.

D)marginal social cost equals the minimum of average social cost.

E)marginal social cost equals average social cost, though not necessarily at the minimum of average social cost.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the panels in the figure below best indicates with q* the level of output that a supplier in a perfectly competitive industry will produce?

A)a

B)b

C)c

D)d

E)None of the above.

A)a

B)b

C)c

D)d

E)None of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

39

In a competitive market with a downward-sloping demand curve, a tax that increases the fixed cost of every firm will:

A)reduce the number of firms supporting long-run equilibrium.

B)increase the long-run equilibrium price.

C)not cause the number of firms supporting long-run equilibrium to change.

D)answers a and b.

E)answers b and c.

A)reduce the number of firms supporting long-run equilibrium.

B)increase the long-run equilibrium price.

C)not cause the number of firms supporting long-run equilibrium to change.

D)answers a and b.

E)answers b and c.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

40

In a market economy, if you double the inputs for a new branch of your textile company and produce double the output which term best describes your situation.

A)constant cost.

B)increasing cost diminishing returns.

C)decreasing cost diminishing returns.

D)both B and C.

E)none of the above.

A)constant cost.

B)increasing cost diminishing returns.

C)decreasing cost diminishing returns.

D)both B and C.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

41

Suppose that Michael Jordan, star basketball player, earns a pure economic rent.This means that:

A)the demand curve for his talent is perfectly elastic.

B)the supply curve for his talent is perfectly inelastic.

C)the demand curve for his talent is downward-sloping.

D)the supply curve for his talent is perfectly elastic.

E)market equilibrium will be undefined.

A)the demand curve for his talent is perfectly elastic.

B)the supply curve for his talent is perfectly inelastic.

C)the demand curve for his talent is downward-sloping.

D)the supply curve for his talent is perfectly elastic.

E)market equilibrium will be undefined.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following would occur if a single farm in perfect competition lowered its price below the long-run equilibrium market price?

A)All other farms would lower their prices, too.

B)It would not be maximizing profit.

C)It would get a larger share of the market, and this would be profitable for it.

D)Other farms would be driven out of the industry.

E)Other farms would enter the industry.

A)All other farms would lower their prices, too.

B)It would not be maximizing profit.

C)It would get a larger share of the market, and this would be profitable for it.

D)Other farms would be driven out of the industry.

E)Other farms would enter the industry.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

43

It will sometimes pay a firm to operate at a loss under perfect competition, so long as price covers:

A)average variable cost.

B)average cost.

C)marginal cost.

D)average fixed cost.

E)none of the above.

A)average variable cost.

B)average cost.

C)marginal cost.

D)average fixed cost.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

44

Marginal cost equals marginal utility in a well-running society, so they are essentially the same thing.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

45

The "demand rule" states that an increase in the demand for a commodity will raise the price of the commodity.This may not be the case when the supply curve is:

A)backward-bending.

B)perfectly inelastic.

C)upward-sloping.

D)all of the above.

E)none of the above.

A)backward-bending.

B)perfectly inelastic.

C)upward-sloping.

D)all of the above.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

46

All of the following qualify as market failure except:

A)imperfect competition.

B)externalities.

C)imperfect information.

D)pollution.

E)allocative efficiency.

A)imperfect competition.

B)externalities.

C)imperfect information.

D)pollution.

E)allocative efficiency.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

47

In a market economy, if you are only one of many wheat farmers you are considered a which of the following:

A)price-maker.

B)price-taker.

C)price manipulator.

D)price-neogiator.

E)none of the above.

A)price-maker.

B)price-taker.

C)price manipulator.

D)price-neogiator.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

48

Use the following to answer questions :

Figure 8-1

In Figure 8-1, in the long-run the firm's economic profits will equal:

A)0.

B)$40.

C)$100.

D)$150.

E)none of the above.

Figure 8-1

In Figure 8-1, in the long-run the firm's economic profits will equal:

A)0.

B)$40.

C)$100.

D)$150.

E)none of the above.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

49

When its variable costs are less than total revenue, a firm should shut down.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

50

In a purely competitive market, the maximum profit comes at that output where marginal cost equals price.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

51

Economic efficiency simply requires that all commodities be produced at minimum marginal cost.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

52

Allocative efficiency does not necessarily mean:

A)a socially desirable distribution of resources.

B)zero economic profits for firms.

C)price is equal to marginal cost.

D)price is equal to average costs.

E)there are many firms in the industry.

A)a socially desirable distribution of resources.

B)zero economic profits for firms.

C)price is equal to marginal cost.

D)price is equal to average costs.

E)there are many firms in the industry.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

53

An efficient allocation of resources calls for flexible prices.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

54

If all factors of production could be bought at existing prices and output were to show constant returns to scale, then long-run MC could be horizontal forever.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

55

A perfect competitor is defined as one who can sell all she wants at the prevailing market price.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

56

The total quantity brought to market at a given price will be the sum of the individual quantities that all firms supply at that price.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

57

The shutdown point comes where revenues just cover variable costs.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

58

Use the following to answer questions :

Figure 8-1

If the market price increases to $15, the firm depicted in Figure 8-1 will:

A)shutdown.

B)earn economic profits.

C)produce more than 10 units of output.

D)produce less than 10 units of output.

E)both B and C are correct.

Figure 8-1

If the market price increases to $15, the firm depicted in Figure 8-1 will:

A)shutdown.

B)earn economic profits.

C)produce more than 10 units of output.

D)produce less than 10 units of output.

E)both B and C are correct.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

59

If a firm is maximizing profit their marginal cost curve will also be their supply curve.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

60

Use the following to answer questions :

Figure 8-1

In Figure 8-1, the long run equilibrium competitive price is:

A)$5.

B)$7.

C)$10.

D)greater than $10.

E)some positive number that cannot be determined without seeing the market demand curve.

Figure 8-1

In Figure 8-1, the long run equilibrium competitive price is:

A)$5.

B)$7.

C)$10.

D)greater than $10.

E)some positive number that cannot be determined without seeing the market demand curve.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

61

In the long run, the industry's supply curve may reflect constant, increasing, or decreasing costs.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

62

Use the following to answer questions :

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive level of output is 5.

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive level of output is 5.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

63

Free (unrestricted)entry and exit of firms is not an essential feature for adjustments in industry output in response to price changes in a competitive market.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

64

The market demand curve is a reflection of society's marginal benefit schedule including the social costs of any production externalities.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

65

A perfect competitor is defined as one who can earn economic profits, even in the long run.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

66

A competitive price system equitably and even-handedly distributes income to compensate for the minor inefficiencies it must entail.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

67

If externalities are involved, there may be a divergence between social costs and private production costs.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

68

A profit maximizing competitive firm should produce at the point where marginal cost is lowest.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

69

There can be an efficient allocation of resources even if P does not equal MC for all commodities.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

70

We can add horizontally the supply curves of firms to get a market supply curve even for low prices, although in the short run some firms will close down if they cannot cover their variable costs.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

71

The fact that some large firms are earning positive profits while smaller firms in the same industry are losing money is not in itself an indication of monopoly power.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

72

Use the following to answer questions :

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive equilibrium price is $1000.

Figure 8-2

For the market whose typical firm is characterized in Figure 8-2, the long-run competitive equilibrium price is $1000.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

73

A tax on the emission of a pollutant from the firms of a competitive industry can be expected to cause the equilibrium quantity demanded and supplied to decline.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

74

A competitive firm in the long run must realize a price that covers its average cost.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

75

A firm will shut down if its MU exceeds its MC.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

76

A competitive firm always wants to produce at the point where average cost is lowest.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

77

Economic rents are earned by factors of production that are fixed in total supply so that the supply curve is perfectly elastic.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

78

Pure economic rent is the price paid to a factor of production that is fixed in total supply

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

79

Given the market demand drawn in Panel B of the figure below and the cost structure for the typical firms shown in Panel A of the figure below, the long-run total output of the industry is 900 units.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

80

If demand decreases in a constant cost industry, in the long-run firms will exit, industry output will fall, and the price of the product will fall.

Unlock Deck

Unlock for access to all 80 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 80 flashcards in this deck.