Deck 13: Perfect Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

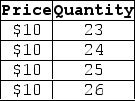

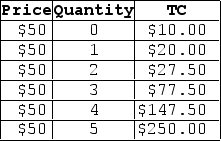

This table shows price and quantity produced for a single firm in a perfectly competitive market.  Given the information in the table shown,what is the market price?

Given the information in the table shown,what is the market price?

A) $20

B) $10

C) $2

D) $260

Given the information in the table shown,what is the market price?A) $20

B) $10

C) $2

D) $260

Question

Question

Question

Question

Question

Question

Question

Question

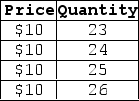

This table shows price and quantity produced for a single firm in a perfectly competitive market.  Given the information in the table shown,what is the total revenue when 23 units are produced?

Given the information in the table shown,what is the total revenue when 23 units are produced?

A) $230

B) $10

C) $23

D) $2.30

Given the information in the table shown,what is the total revenue when 23 units are produced?A) $230

B) $10

C) $23

D) $2.30

Question

Question

Question

Question

Question

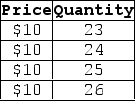

This table shows price and quantity produced for a single firm in a perfectly competitive market.  Given the information in the table shown,what is the average revenue when 24 units are produced?

Given the information in the table shown,what is the average revenue when 24 units are produced?

A) $240

B) $10

C) $24

D) $2.40

Given the information in the table shown,what is the average revenue when 24 units are produced?A) $240

B) $10

C) $24

D) $2.40

Question

Question

Question

Question

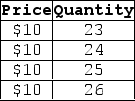

This table shows price and quantity produced for a single firm in a perfectly competitive market.  Given the information in the table shown,what is the marginal revenue when 25 units are produced?

Given the information in the table shown,what is the marginal revenue when 25 units are produced?

A) $250

B) $25

C) $10

D) $20

Given the information in the table shown,what is the marginal revenue when 25 units are produced?A) $250

B) $25

C) $10

D) $20

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

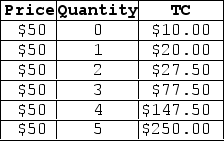

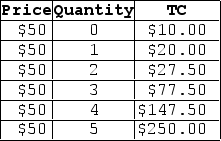

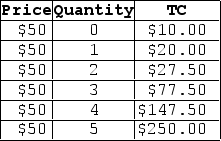

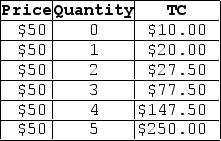

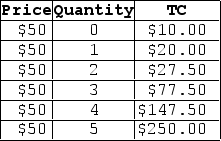

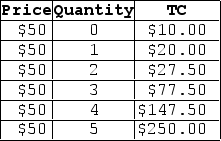

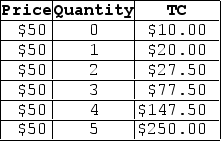

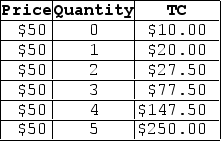

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,what is the market price?

According to the table shown,what is the market price?

A) $500

B) $150

C) $50

D) $27.50

According to the table shown,what is the market price?A) $500

B) $150

C) $50

D) $27.50

Question

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,what is the firm's total revenue when 4 units are produced?

According to the table shown,what is the firm's total revenue when 4 units are produced?

A) $160

B) $50

C) $200

D) $40

According to the table shown,what is the firm's total revenue when 4 units are produced?A) $160

B) $50

C) $200

D) $40

Question

Question

Question

Question

Question

Question

Question

Question

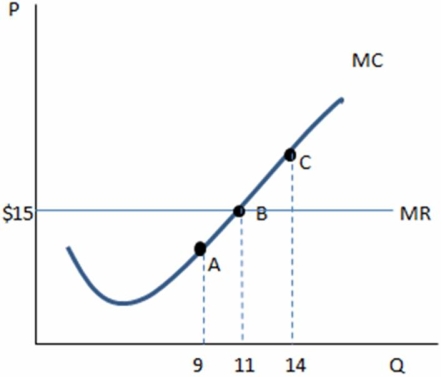

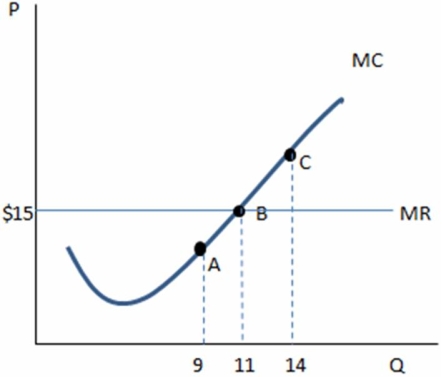

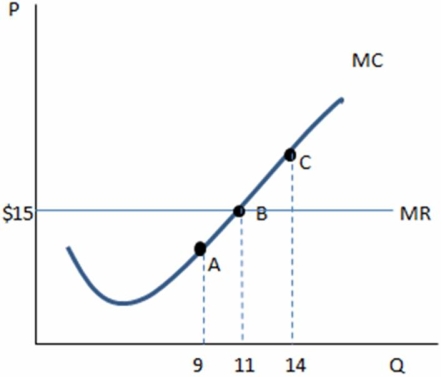

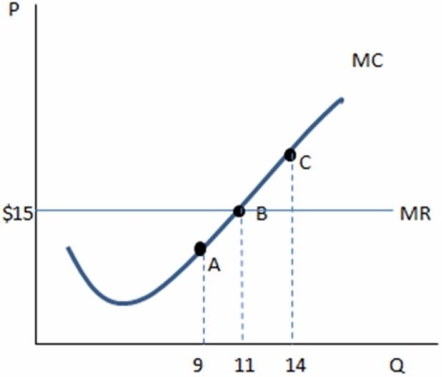

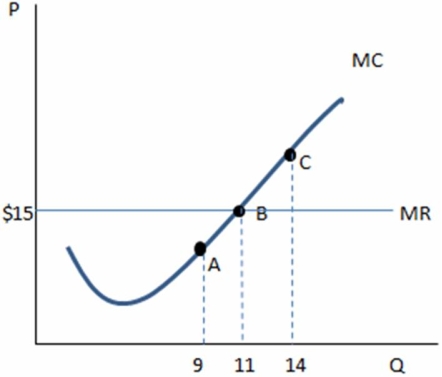

According to the graph shown,the profits at point A are:

According to the graph shown,the profits at point A are:A)higher than those at point B.

B)lower than those at point B.

C)the same as those at point B.

D)higher than those at point C.

Question

Question

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,fixed costs must be:

According to the table shown,fixed costs must be:

A) $10.

B) $200.

C) $60.

D) Fixed costs cannot be determined by the information in the table.

According to the table shown,fixed costs must be:A) $10.

B) $200.

C) $60.

D) Fixed costs cannot be determined by the information in the table.

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,the firm's marginal revenue:

According to the table shown,the firm's marginal revenue:

A) is constant.

B) increases as output increases.

C) decreases as output increases.

D) increases until the 3rd unit, then decreases.

According to the table shown,the firm's marginal revenue:A) is constant.

B) increases as output increases.

C) decreases as output increases.

D) increases until the 3rd unit, then decreases.

Question

According to the graph shown,producing 9 units earns profits that are:

According to the graph shown,producing 9 units earns profits that are:A) lower than output of 11 units, and the firm should increase production.

B) higher than output of 11 units, and the firm should decrease production.

C) higher than output of 11 units, and the firm should increase production.

D) lower than output of 11 units, and the firm should decrease production.

Question

Question

According to the graph shown,producing 14 units:

According to the graph shown,producing 14 units:A) is not as profitable as producing 11 units.

B) will earn negative profits.

C) will earn more profits than producing 9 or 11 units.

D) will earn zero profit.

Question

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,what is the firm's marginal revenue from the 3rd unit produced?

According to the table shown,what is the firm's marginal revenue from the 3rd unit produced?

A) $50

B) $90

C) $150

D) $60

According to the table shown,what is the firm's marginal revenue from the 3rd unit produced?A) $50

B) $90

C) $150

D) $60

Question

According to the graph shown,at point C the firm is earning:

According to the graph shown,at point C the firm is earning:A) higher profits than at point B, and they should produce more.

B) fewer profits than at point B, and they should produce more.

C) fewer profits than at point B, and they should produce less.

D) higher profits than at point B, and they should produce less.

Question

Question

Question

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,when 1 unit is produced:

According to the table shown,when 1 unit is produced:

A) marginal costs exceed marginal revenue, and the firm should produce more.

B) marginal revenue exceeds marginal costs, and the firm should produce more.

C) marginal revenue exceeds marginal costs, and the firm should produce less.

D) marginal costs exceed marginal revenue, and the firm should produce less.

According to the table shown,when 1 unit is produced:A) marginal costs exceed marginal revenue, and the firm should produce more.

B) marginal revenue exceeds marginal costs, and the firm should produce more.

C) marginal revenue exceeds marginal costs, and the firm should produce less.

D) marginal costs exceed marginal revenue, and the firm should produce less.

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,when 5 units are produced:

According to the table shown,when 5 units are produced:

A) profits are maximized.

B) profits are positive.

C) the firm is producing less than the profit-maximizing amount.

D) the firm is producing more than the profit-maximizing amount.

According to the table shown,when 5 units are produced:A) profits are maximized.

B) profits are positive.

C) the firm is producing less than the profit-maximizing amount.

D) the firm is producing more than the profit-maximizing amount.

Question

According to the graph shown,the market price is:

According to the graph shown,the market price is:A) $15

B) $9

C) $11

D) $20

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,what is the firm's marginal cost from producing the 2nd unit?

According to the table shown,what is the firm's marginal cost from producing the 2nd unit?

A) $10.00

B) $7.50

C) $27.50

D) $20.00

According to the table shown,what is the firm's marginal cost from producing the 2nd unit?A) $10.00

B) $7.50

C) $27.50

D) $20.00

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,the firm's profit is:

According to the table shown,the firm's profit is:

A) maximized at 3 units of output.

B) maximized at 4 units of output.

C) maximized at 5 units of output.

D) not maximized at any level of output given.

According to the table shown,the firm's profit is:A) maximized at 3 units of output.

B) maximized at 4 units of output.

C) maximized at 5 units of output.

D) not maximized at any level of output given.

Question

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market.  According to the table shown,the firm's marginal costs:

According to the table shown,the firm's marginal costs:

A) are constant.

B) increase as output increases.

C) decrease until the 2nd unit, then increase.

D) increase until the 4th unit, then decrease.

According to the table shown,the firm's marginal costs:A) are constant.

B) increase as output increases.

C) decrease until the 2nd unit, then increase.

D) increase until the 4th unit, then decrease.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/156

Play

Full screen (f)

Deck 13: Perfect Competition

1

Commodities:

A) are a special type of standardized good.

B) have no product differentiation.

C) are identical regardless of who produced them.

D) All of these are true.

A) are a special type of standardized good.

B) have no product differentiation.

C) are identical regardless of who produced them.

D) All of these are true.

D

2

One implication of goods being standardized in a market is:

A) the government regulations must promote competition and lower prices to be efficient.

B) there are no information asymmetries.

C) the similarity in products may be real or perceived.

D) the market has a low degree of competition.

A) the government regulations must promote competition and lower prices to be efficient.

B) there are no information asymmetries.

C) the similarity in products may be real or perceived.

D) the market has a low degree of competition.

B

3

The definition of a price taker is:

A) having market power.

B) having no control over the market price.

C) being competitive.

D) having government determine what you sell goods and services for.

A) having market power.

B) having no control over the market price.

C) being competitive.

D) having government determine what you sell goods and services for.

B

4

An example of a standardized good is:

A) grain.

B) granola cereal.

C) hamburgers.

D) digital cameras.

A) grain.

B) granola cereal.

C) hamburgers.

D) digital cameras.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

5

An essential characteristic of a perfectly competitive market is:

A) buyers and sellers share market power.

B) sellers are price makers.

C) goods are standardized.

D) goods are unique.

A) buyers and sellers share market power.

B) sellers are price makers.

C) goods are standardized.

D) goods are unique.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

6

Which is not an essential characteristic of a perfectly competitive market?

A) Goods are standardized.

B) Buyers have perfect information.

C) Goods from one seller cannot be distinguished from another's.

D) Firms have limited market power.

A) Goods are standardized.

B) Buyers have perfect information.

C) Goods from one seller cannot be distinguished from another's.

D) Firms have limited market power.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

7

Standardized goods are:

A) goods which are regulated by government quality standards.

B) goods which are easily substitutable and not distinguishable.

C) the most common type of good produced.

D) those sold in markets with regulated price systems.

A) goods which are regulated by government quality standards.

B) goods which are easily substitutable and not distinguishable.

C) the most common type of good produced.

D) those sold in markets with regulated price systems.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

8

When firms have market power,it means that they:

A) can noticeably affect the market price.

B) have no control over the market price.

C) can noticeably affect the market quantity available for sale.

D) do not noticeably affect the market quantity offered for sale.

A) can noticeably affect the market price.

B) have no control over the market price.

C) can noticeably affect the market quantity available for sale.

D) do not noticeably affect the market quantity offered for sale.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

9

Standardized goods and services refers to those that:

A) are interchangeable.

B) have close substitutes.

C) are unique.

D) are regulated by the government.

A) are interchangeable.

B) have close substitutes.

C) are unique.

D) are regulated by the government.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

10

Most markets in the United States:

A) have some degree of competitiveness, but are not perfectly competitive.

B) have very few competitive features and so are regulated by the government.

C) are monopolies.

D) are perfectly competitive.

A) have some degree of competitiveness, but are not perfectly competitive.

B) have very few competitive features and so are regulated by the government.

C) are monopolies.

D) are perfectly competitive.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

11

An example of a standardized good is:

A) cereal.

B) iron.

C) soda.

D) pizza.

A) cereal.

B) iron.

C) soda.

D) pizza.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

12

Transactions costs are defined to be the:

A) costs a buyer or seller incurs to make a transaction take place.

B) taxes they pay when purchasing a good or service.

C) fees they are charged if they purchase a good or service on credit.

D) costs a buyer faces if they re-sell a good or service.

A) costs a buyer or seller incurs to make a transaction take place.

B) taxes they pay when purchasing a good or service.

C) fees they are charged if they purchase a good or service on credit.

D) costs a buyer faces if they re-sell a good or service.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

13

A price taker is a buyer or seller who:

A) has complete control over setting the market price.

B) can influence the market price.

C) has no control over setting the market price.

D) has the goal of maximizing market share, not profits.

A) has complete control over setting the market price.

B) can influence the market price.

C) has no control over setting the market price.

D) has the goal of maximizing market share, not profits.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

14

In a perfectly competitive market price takers exist because there are:

A) few sellers and many buyers.

B) few buyers and many sellers.

C) many buyers and sellers.

D) few sellers and buyers.

A) few sellers and many buyers.

B) few buyers and many sellers.

C) many buyers and sellers.

D) few sellers and buyers.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

15

An essential characteristic of a perfectly competitive market is:

A) buyers and sellers have no control over the market price.

B) sellers are selling unique products.

C) buyers have complete control over the market price and sellers have none.

D) sellers have complete control over the market price and buyers have none.

A) buyers and sellers have no control over the market price.

B) sellers are selling unique products.

C) buyers have complete control over the market price and sellers have none.

D) sellers have complete control over the market price and buyers have none.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

16

When firms have market power,it means that they:

A) are a price taker.

B) can noticeably affect the market price.

C) do not affect the market quantity offered for sale.

D) can earn as much profit as they want.

A) are a price taker.

B) can noticeably affect the market price.

C) do not affect the market quantity offered for sale.

D) can earn as much profit as they want.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

17

An essential characteristic of a perfectly competitive market is that buyers and sellers have:

A) no competition and so must set the market price on their own.

B) so much competition that they must work together perfectly to set a market price.

C) so much competition that they have no ability set their own price.

D) no control over the price they set because it is determined by government.

A) no competition and so must set the market price on their own.

B) so much competition that they must work together perfectly to set a market price.

C) so much competition that they have no ability set their own price.

D) no control over the price they set because it is determined by government.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

18

A competitive market is one in which:

A) fully informed price-taking buyers and sellers easily trade a standardized good.

B) few large sellers compete for a majority of the market share.

C) government oversees its operation.

D) individual sellers and buyers have a lot of influence over market price.

A) fully informed price-taking buyers and sellers easily trade a standardized good.

B) few large sellers compete for a majority of the market share.

C) government oversees its operation.

D) individual sellers and buyers have a lot of influence over market price.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

19

A good that is perfectly standardized is:

A) likely to be interchangeable with others in the market.

B) indistinguishable to others in the market.

C) fairly close to others in the market.

D) determined to be the same by government.

A) likely to be interchangeable with others in the market.

B) indistinguishable to others in the market.

C) fairly close to others in the market.

D) determined to be the same by government.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

20

Perfectly competitive markets:

A) are more of an idealized model economists use than a real-life occurrence.

B) are the most common type of market in the United States.

C) tend to have relatively few buyers.

D) tend to have relatively few sellers.

A) are more of an idealized model economists use than a real-life occurrence.

B) are the most common type of market in the United States.

C) tend to have relatively few buyers.

D) tend to have relatively few sellers.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

21

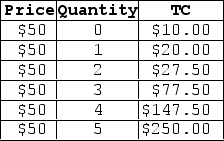

This table shows price and quantity produced for a single firm in a perfectly competitive market. Given the information in the table shown,what is the market price?

A) $20

B) $10

C) $2

D) $260

Given the information in the table shown,what is the market price?A) $20

B) $10

C) $2

D) $260

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

22

A characteristic that is important,but not essential to defining a perfectly competitive market is:

A) goods are standardized.

B) buyers and sellers are price takers.

C) firms can freely enter and exit the market.

D) All of these are necessary to define a perfectly competitive market.

A) goods are standardized.

B) buyers and sellers are price takers.

C) firms can freely enter and exit the market.

D) All of these are necessary to define a perfectly competitive market.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

23

For firms that sell one product in a perfectly competitive market,average revenue is:

A) calculated by total revenue divided by total output.

B) equal to marginal revenue.

C) equal to the market price.

D) All of these are true.

A) calculated by total revenue divided by total output.

B) equal to marginal revenue.

C) equal to the market price.

D) All of these are true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

24

Collusion is:

A) more likely when the threat of market entry is missing.

B) more likely in perfectly competitive markets.

C) less likely when the threat of market entry is missing.

D) not affected by firm's ability to enter a market.

A) more likely when the threat of market entry is missing.

B) more likely in perfectly competitive markets.

C) less likely when the threat of market entry is missing.

D) not affected by firm's ability to enter a market.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

25

For firms that sell one product in a perfectly competitive market,marginal revenue is always:

A) greater than market price.

B) less than market price.

C) the same as market price.

D) equal to average total cost.

A) greater than market price.

B) less than market price.

C) the same as market price.

D) equal to average total cost.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

26

If a firm in a perfectly competitive market faces a market price of $5,and it decides to produce 400 units,the firm's total revenue will be:

A) $5.

B) $400.

C) $2,000.

D) $405.

A) $5.

B) $400.

C) $2,000.

D) $405.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

27

For firms that sell one product in a perfectly competitive market,the market price:

A) can be influenced by one firm's output decision.

B) is equal to the average total cost of a firm.

C) is taken as a constant by individual firms.

D) is higher than the marginal revenue of a firm

A) can be influenced by one firm's output decision.

B) is equal to the average total cost of a firm.

C) is taken as a constant by individual firms.

D) is higher than the marginal revenue of a firm

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

28

For firms that sell one product in a perfectly competitive market,average revenue is:

A) calculated by total output divided by total revenue.

B) equal to marginal cost.

C) equal to the market price.

D) greater than market price.

A) calculated by total output divided by total revenue.

B) equal to marginal cost.

C) equal to the market price.

D) greater than market price.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

29

This table shows price and quantity produced for a single firm in a perfectly competitive market. Given the information in the table shown,what is the total revenue when 23 units are produced?

A) $230

B) $10

C) $23

D) $2.30

Given the information in the table shown,what is the total revenue when 23 units are produced?A) $230

B) $10

C) $23

D) $2.30

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

30

If a perfectly competitive firm faces a market price of $3 per unit,and it decides to produce 30,000 units,the market price will likely:

A) increase.

B) decrease.

C) stay the same.

D) increase initially and then decrease.

A) increase.

B) decrease.

C) stay the same.

D) increase initially and then decrease.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

31

For firms that sell one product in a perfectly competitive market,average revenue will:

A) increase if marginal revenue is greater than it.

B) decrease if marginal revenue is greater than it.

C) always be the same as marginal revenue.

D) always be greater than average total cost.

A) increase if marginal revenue is greater than it.

B) decrease if marginal revenue is greater than it.

C) always be the same as marginal revenue.

D) always be greater than average total cost.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

32

For firms that sell one product in a perfectly competitive market,the market price:

A) will remain constant regardless of an individual firm's output decision.

B) is equal to the average total cost of a firm.

C) is equal to the marginal cost of a firm.

D) All of these are true.

A) will remain constant regardless of an individual firm's output decision.

B) is equal to the average total cost of a firm.

C) is equal to the marginal cost of a firm.

D) All of these are true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

33

Having free entry and exit in a market can help drive:

A) innovation.

B) cost-cutting.

C) quality improvements.

D) All of these occur more often with free entry and exit.

A) innovation.

B) cost-cutting.

C) quality improvements.

D) All of these occur more often with free entry and exit.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

34

This table shows price and quantity produced for a single firm in a perfectly competitive market. Given the information in the table shown,what is the average revenue when 24 units are produced?

A) $240

B) $10

C) $24

D) $2.40

Given the information in the table shown,what is the average revenue when 24 units are produced?A) $240

B) $10

C) $24

D) $2.40

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

35

In a perfectly competitive market,producers:

A) are able to sell as much as they want without affecting the market price.

B) can influence the price upward by restricting output.

C) often undercut the competition's price and force firms to leave the market.

D) None of these is true of perfectly competitive markets.

A) are able to sell as much as they want without affecting the market price.

B) can influence the price upward by restricting output.

C) often undercut the competition's price and force firms to leave the market.

D) None of these is true of perfectly competitive markets.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

36

In perfectly competitive markets,transactions costs are:

A) generally quite high.

B) a natural byproduct of making the transaction.

C) low or nearly zero.

D) seen as a nuisance and generally ignored when making a transaction.

A) generally quite high.

B) a natural byproduct of making the transaction.

C) low or nearly zero.

D) seen as a nuisance and generally ignored when making a transaction.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

37

In a perfectly competitive market,total revenue:

A) measures how much revenue the firm takes in from all sales less any costs they incur.

B) is equal to price multiplied by quantity sold.

C) varies due to changes in price, since quantity is constant.

D) should vary across firms.

A) measures how much revenue the firm takes in from all sales less any costs they incur.

B) is equal to price multiplied by quantity sold.

C) varies due to changes in price, since quantity is constant.

D) should vary across firms.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

38

This table shows price and quantity produced for a single firm in a perfectly competitive market. Given the information in the table shown,what is the marginal revenue when 25 units are produced?

A) $250

B) $25

C) $10

D) $20

Given the information in the table shown,what is the marginal revenue when 25 units are produced?A) $250

B) $25

C) $10

D) $20

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

39

For firms that sell one product in a perfectly competitive market,the market price is:

A) constant, regardless of quantity sold.

B) equal to average revenue for a firm.

C) equal to marginal revenue for a firm.

D) All of these are true.

A) constant, regardless of quantity sold.

B) equal to average revenue for a firm.

C) equal to marginal revenue for a firm.

D) All of these are true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

40

For firms that sell one product in a perfectly competitive market,marginal revenue is:

A) the additional revenue gained from selling one more unit.

B) equal to average revenue.

C) equal to market price.

D) All of these are true.

A) the additional revenue gained from selling one more unit.

B) equal to average revenue.

C) equal to market price.

D) All of these are true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

41

Firms in perfectly competitive markets typically have:

A) one profit-maximizing level of output.

B) several profit-maximizing levels of output to choose from.

C) two profit-maximizing levels of output to choose from.

D) no chance of maximizing profits, since they have no control over market price.

A) one profit-maximizing level of output.

B) several profit-maximizing levels of output to choose from.

C) two profit-maximizing levels of output to choose from.

D) no chance of maximizing profits, since they have no control over market price.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

42

If a firm in a perfectly competitive market faces a market price of $4,and it decides to produce 700 units,the firm's average revenue will be:

A) $4.

B) $2,800.

C) $175.

D) $700.

A) $4.

B) $2,800.

C) $175.

D) $700.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

43

If a firm in a perfectly competitive market is producing at a level of output where marginal costs are less than marginal revenue,its profit:

A) must be positive.

B) are maximized.

C) will increase if it produces less.

D) will increase if it produces more.

A) must be positive.

B) are maximized.

C) will increase if it produces less.

D) will increase if it produces more.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

44

If a firm in a perfectly competitive market faces a market price of $2,and it decides to increase its production from 2,000 units to 4,000 units,the firm's marginal revenue:

A) will increase from $4,000 to $8,000.

B) will decrease from $8,000 to $4,000.

C) will stay the same.

D) None of these is true.

A) will increase from $4,000 to $8,000.

B) will decrease from $8,000 to $4,000.

C) will stay the same.

D) None of these is true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

45

Firms in perfectly competitive markets who wish to maximize profits should produce:

A) more as long as marginal cost is greater than marginal revenue.

B) less as long as marginal cost is less than marginal revenue.

C) at the level where marginal cost equals marginal revenue.

D) All of these are true.

A) more as long as marginal cost is greater than marginal revenue.

B) less as long as marginal cost is less than marginal revenue.

C) at the level where marginal cost equals marginal revenue.

D) All of these are true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

46

If a firm in a perfectly competitive market faces a market price of $7,and it decides to increase its production from 4,000 to 12,000 units,the firm's marginal revenue will:

A) diminish once diminishing marginal product sets in.

B) rise once diminishing marginal product sets in.

C) stay the same.

D) increase from $28,000 to $84,000.

A) diminish once diminishing marginal product sets in.

B) rise once diminishing marginal product sets in.

C) stay the same.

D) increase from $28,000 to $84,000.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

47

Because firms in perfectly competitive markets can sell any quantity without driving down prices,they should:

A) produce as much as possible to maximize profits.

B) produce at the lowest cost per unit to maximize profits.

C) try to flood the market.

D) increase quantity until the additional profit it earns on its last unit sold is zero.

A) produce as much as possible to maximize profits.

B) produce at the lowest cost per unit to maximize profits.

C) try to flood the market.

D) increase quantity until the additional profit it earns on its last unit sold is zero.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

48

For a firm in a perfectly competitive market,if it produces where marginal cost exceeds marginal revenue it:

A) should cut back production to increase profits.

B) should increase production to increase profits.

C) is producing a profit-maximizing quantity.

D) is impossible to tell if it is actually maximizing profits.

A) should cut back production to increase profits.

B) should increase production to increase profits.

C) is producing a profit-maximizing quantity.

D) is impossible to tell if it is actually maximizing profits.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

49

The profit-maximizing level of output for any firm in a perfectly competitive market is to produce where:

A) MC = MR.

B) MC > MR.

C) MC < MR.

D) MR = P*.

A) MC = MR.

B) MC > MR.

C) MC < MR.

D) MR = P*.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

50

Firms in perfectly competitive markets who wish to maximize profits should produce where:

A) marginal revenue and marginal cost are equal.

B) marginal revenue and market price are equal.

C) marginal revenue and average revenue are equal.

D) marginal cost and average cost are equal.

A) marginal revenue and marginal cost are equal.

B) marginal revenue and market price are equal.

C) marginal revenue and average revenue are equal.

D) marginal cost and average cost are equal.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

51

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,what is the market price?

A) $500

B) $150

C) $50

D) $27.50

According to the table shown,what is the market price?A) $500

B) $150

C) $50

D) $27.50

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

52

For a firm in a perfectly competitive market,if it is producing at a level of output where marginal costs are equal to marginal revenue it:

A) should cut back production to increase profits.

B) should increase production to increase profits.

C) is producing a profit-maximizing quantity.

D) is impossible to tell how quantity should be changed without more information.

A) should cut back production to increase profits.

B) should increase production to increase profits.

C) is producing a profit-maximizing quantity.

D) is impossible to tell how quantity should be changed without more information.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

53

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,what is the firm's total revenue when 4 units are produced?

A) $160

B) $50

C) $200

D) $40

According to the table shown,what is the firm's total revenue when 4 units are produced?A) $160

B) $50

C) $200

D) $40

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

54

If a firm in a perfectly competitive market faces a market price of $8,and it decides to increase its production from 300 units to 550 units,the firm's total revenue will:

A) increase from $2,400 to $4,400.

B) decrease from $4,400 to $2,400.

C) stay the same at $8.

D) likely rise, but it cannot be determined by how much.

A) increase from $2,400 to $4,400.

B) decrease from $4,400 to $2,400.

C) stay the same at $8.

D) likely rise, but it cannot be determined by how much.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

55

For a firm in a perfectly competitive market,if it is producing at a level of output where marginal costs are less than marginal revenue it:

A) should cut back production to increase profits.

B) should increase production to increase profits.

C) is producing a profit-maximizing quantity.

D) should invest more in advertising in order to raise revenues.

A) should cut back production to increase profits.

B) should increase production to increase profits.

C) is producing a profit-maximizing quantity.

D) should invest more in advertising in order to raise revenues.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

56

Firms in perfectly competitive markets who wish to maximize profits ought to produce:

A) where marginal revenue equals market price.

B) as many units as their scale allows.

C) at capacity and plan to expand in the long run.

D) where total profit is the greatest.

A) where marginal revenue equals market price.

B) as many units as their scale allows.

C) at capacity and plan to expand in the long run.

D) where total profit is the greatest.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

57

A firm in a perfectly competitive market can maximize its profits by producing:

A) the level of output where marginal cost equals marginal revenue.

B) any level below where marginal cost equals marginal revenue.

C) any level beyond where marginal cost equals marginal revenue.

D) slightly below its maximal capacity.

A) the level of output where marginal cost equals marginal revenue.

B) any level below where marginal cost equals marginal revenue.

C) any level beyond where marginal cost equals marginal revenue.

D) slightly below its maximal capacity.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

58

If a firm in a perfectly competitive market is producing at a level of output where marginal costs exceed marginal revenue,its profits:

A) must be negative.

B) are maximized.

C) will increase if it produces less.

D) cannot be determined.

A) must be negative.

B) are maximized.

C) will increase if it produces less.

D) cannot be determined.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

59

When a firm faces a perfectly competitive market and buys its inputs from perfectly competitive markets,the only choice the firm has to affect its profits is to:

A) increase its selling price.

B) change the quantity it produces.

C) decrease the selling price.

D) decrease its cost of production lower than other firms.

A) increase its selling price.

B) change the quantity it produces.

C) decrease the selling price.

D) decrease its cost of production lower than other firms.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

60

Firms in perfectly competitive markets who wish to maximize profits should:

A) keep producing more as long as marginal cost is less than marginal revenue.

B) produce less as long as marginal cost is greater than marginal revenue.

C) produce where marginal cost and marginal revenue are equal.

D) All of these are true.

A) keep producing more as long as marginal cost is less than marginal revenue.

B) produce less as long as marginal cost is greater than marginal revenue.

C) produce where marginal cost and marginal revenue are equal.

D) All of these are true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

61

According to the graph shown,the profits at point A are:A)higher than those at point B.

B)lower than those at point B.

C)the same as those at point B.

D)higher than those at point C.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

62

The MC of a firm:

A) crosses TC at its minimum.

B) crosses AVC and ATC at its minimum.

C) crosses MR at the above the profit-maximizing level of output.

D) is a horizontal line indicating that costs are constant in perfect competition.

A) crosses TC at its minimum.

B) crosses AVC and ATC at its minimum.

C) crosses MR at the above the profit-maximizing level of output.

D) is a horizontal line indicating that costs are constant in perfect competition.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

63

If the market price falls below the bottom of the firm's ATC curve:

A) there is no level of output at which the firm can make a profit.

B) the firm is earning profits.

C) the market price must be lower than the firm's AVC.

D) Total revenue must be higher than total cost.

A) there is no level of output at which the firm can make a profit.

B) the firm is earning profits.

C) the market price must be lower than the firm's AVC.

D) Total revenue must be higher than total cost.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

64

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,fixed costs must be:

A) $10.

B) $200.

C) $60.

D) Fixed costs cannot be determined by the information in the table.

According to the table shown,fixed costs must be:A) $10.

B) $200.

C) $60.

D) Fixed costs cannot be determined by the information in the table.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

65

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,the firm's marginal revenue:

A) is constant.

B) increases as output increases.

C) decreases as output increases.

D) increases until the 3rd unit, then decreases.

According to the table shown,the firm's marginal revenue:A) is constant.

B) increases as output increases.

C) decreases as output increases.

D) increases until the 3rd unit, then decreases.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

66

According to the graph shown,producing 9 units earns profits that are:A) lower than output of 11 units, and the firm should increase production.

B) higher than output of 11 units, and the firm should decrease production.

C) higher than output of 11 units, and the firm should increase production.

D) lower than output of 11 units, and the firm should decrease production.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

67

As long as average revenue remains above average total cost:

A) total revenue will be higher than total cost.

B) the firm will be making profits.

C) price will be greater than average total cost.

D) All of these are true.

A) total revenue will be higher than total cost.

B) the firm will be making profits.

C) price will be greater than average total cost.

D) All of these are true.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

68

According to the graph shown,producing 14 units:A) is not as profitable as producing 11 units.

B) will earn negative profits.

C) will earn more profits than producing 9 or 11 units.

D) will earn zero profit.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

69

As long as market price remains above the average total cost,and the firm chooses the profit-maximizing level of output,it will:

A) make profits.

B) earn zero profits.

C) make a loss.

D) Any of these is possible.

A) make profits.

B) earn zero profits.

C) make a loss.

D) Any of these is possible.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

70

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,what is the firm's marginal revenue from the 3rd unit produced?

A) $50

B) $90

C) $150

D) $60

According to the table shown,what is the firm's marginal revenue from the 3rd unit produced?A) $50

B) $90

C) $150

D) $60

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

71

According to the graph shown,at point C the firm is earning:A) higher profits than at point B, and they should produce more.

B) fewer profits than at point B, and they should produce more.

C) fewer profits than at point B, and they should produce less.

D) higher profits than at point B, and they should produce less.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

72

If a firm is earning a profit,then:

A) the ATC must be higher than the market price.

B) total revenue must be higher than total cost.

C) the ATC must be higher than AR.

D) MR is equal to MC.

A) the ATC must be higher than the market price.

B) total revenue must be higher than total cost.

C) the ATC must be higher than AR.

D) MR is equal to MC.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

73

For a firm in a perfectly competitive market,a price decrease:

A) increases the profit-maximizing quantity.

B) lowers the profit-maximizing quantity.

C) is unrelated to the profit-maximizing quantity.

D) signifies the firm should leave the market.

A) increases the profit-maximizing quantity.

B) lowers the profit-maximizing quantity.

C) is unrelated to the profit-maximizing quantity.

D) signifies the firm should leave the market.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

74

If the market price falls below a firm's minimum average total cost,the firm should:

A) definitely stop production.

B) definitely continue to operate at a loss.

C) consider how to minimize its losses.

D) pay only fixed costs.

A) definitely stop production.

B) definitely continue to operate at a loss.

C) consider how to minimize its losses.

D) pay only fixed costs.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

75

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,when 1 unit is produced:

A) marginal costs exceed marginal revenue, and the firm should produce more.

B) marginal revenue exceeds marginal costs, and the firm should produce more.

C) marginal revenue exceeds marginal costs, and the firm should produce less.

D) marginal costs exceed marginal revenue, and the firm should produce less.

According to the table shown,when 1 unit is produced:A) marginal costs exceed marginal revenue, and the firm should produce more.

B) marginal revenue exceeds marginal costs, and the firm should produce more.

C) marginal revenue exceeds marginal costs, and the firm should produce less.

D) marginal costs exceed marginal revenue, and the firm should produce less.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

76

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,when 5 units are produced:

A) profits are maximized.

B) profits are positive.

C) the firm is producing less than the profit-maximizing amount.

D) the firm is producing more than the profit-maximizing amount.

According to the table shown,when 5 units are produced:A) profits are maximized.

B) profits are positive.

C) the firm is producing less than the profit-maximizing amount.

D) the firm is producing more than the profit-maximizing amount.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

77

According to the graph shown,the market price is:A) $15

B) $9

C) $11

D) $20

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

78

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,what is the firm's marginal cost from producing the 2nd unit?

A) $10.00

B) $7.50

C) $27.50

D) $20.00

According to the table shown,what is the firm's marginal cost from producing the 2nd unit?A) $10.00

B) $7.50

C) $27.50

D) $20.00

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

79

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,the firm's profit is:

A) maximized at 3 units of output.

B) maximized at 4 units of output.

C) maximized at 5 units of output.

D) not maximized at any level of output given.

According to the table shown,the firm's profit is:A) maximized at 3 units of output.

B) maximized at 4 units of output.

C) maximized at 5 units of output.

D) not maximized at any level of output given.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

80

This table shows the total costs for various levels of output for a firm operating in a perfectly competitive market. According to the table shown,the firm's marginal costs:

A) are constant.

B) increase as output increases.

C) decrease until the 2nd unit, then increase.

D) increase until the 4th unit, then decrease.

According to the table shown,the firm's marginal costs:A) are constant.

B) increase as output increases.

C) decrease until the 2nd unit, then increase.

D) increase until the 4th unit, then decrease.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 156 flashcards in this deck.