Deck 11: Decision Making With a Strategic Emphasis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

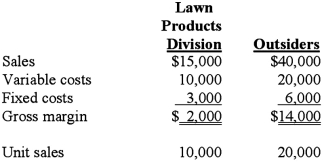

The Blade Division of Dana Company produces hardened steel blades.Approximately one-third of the Blade Division's output is sold to the Lawn Products Division of Dana; the remainder is sold to outside customers.The Blade Division's estimated sales and cost data for the year ending June 30 are as follows:  The Lawn Products Division has an opportunity to purchase 10,000 identical quality blades from an outside supplier at a cost of $1.25 per unit on a continual basis.Assume that the Blade Division cannot sell any additional products to outside customers.Based solely on short-term financial considerations, should Dana allow its Lawn Products Division to purchase the blades from the outside supplier, and why?

The Lawn Products Division has an opportunity to purchase 10,000 identical quality blades from an outside supplier at a cost of $1.25 per unit on a continual basis.Assume that the Blade Division cannot sell any additional products to outside customers.Based solely on short-term financial considerations, should Dana allow its Lawn Products Division to purchase the blades from the outside supplier, and why?

A)Yes, because buying the blades would save Dana Company $500.

B)No, because making the blades would save Dana Company $1,500.

C)Yes, because buying the blades would save Dana Company $2,500.

D)No, because making the blades would save Dana Company $2,500.

The Lawn Products Division has an opportunity to purchase 10,000 identical quality blades from an outside supplier at a cost of $1.25 per unit on a continual basis.Assume that the Blade Division cannot sell any additional products to outside customers.Based solely on short-term financial considerations, should Dana allow its Lawn Products Division to purchase the blades from the outside supplier, and why?A)Yes, because buying the blades would save Dana Company $500.

B)No, because making the blades would save Dana Company $1,500.

C)Yes, because buying the blades would save Dana Company $2,500.

D)No, because making the blades would save Dana Company $2,500.

Question

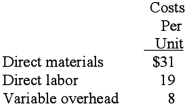

Quirch Inc.manufactures machine parts for aircraft engines.The CEO, Chucky Valters, was considering an offer from a subcontractor who would provide 2,400 units of product PQ107 for Valters for a price of $150,000.If Quirch does not purchase these parts from the subcontractor it must produce them in-house with the following costs:  In addition to the above costs, if Quirch produces part PQ107, it would also have a retooling and design cost of $9,800.The relevant costs of producing 2,400 units of product PQ107 are:

In addition to the above costs, if Quirch produces part PQ107, it would also have a retooling and design cost of $9,800.The relevant costs of producing 2,400 units of product PQ107 are:

A)$149,000.

B)$129,800.

C)$150,000.

D)$164,200.

E)$148,300.

In addition to the above costs, if Quirch produces part PQ107, it would also have a retooling and design cost of $9,800.The relevant costs of producing 2,400 units of product PQ107 are:A)$149,000.

B)$129,800.

C)$150,000.

D)$164,200.

E)$148,300.

Question

Question

Question

Question

Question

Question

Question

Question

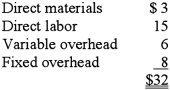

Plainfield Company manufactures part G for use in its production cycle.The costs per unit for 10,000 units of part G are as follows:  Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit.If Plainfield accepts Verona's offer, the released facilities could be used to save $45,000 in relevant costs in the manufacture of part H.In addition, $5 per unit of the fixed overhead applied to part G would be totally eliminated.What alternative is more desirable and by what amount?

Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit.If Plainfield accepts Verona's offer, the released facilities could be used to save $45,000 in relevant costs in the manufacture of part H.In addition, $5 per unit of the fixed overhead applied to part G would be totally eliminated.What alternative is more desirable and by what amount?

A)Option A

B)Option B

C)Option C

D)Option D

Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit.If Plainfield accepts Verona's offer, the released facilities could be used to save $45,000 in relevant costs in the manufacture of part H.In addition, $5 per unit of the fixed overhead applied to part G would be totally eliminated.What alternative is more desirable and by what amount? A)Option A

B)Option B

C)Option C

D)Option D

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

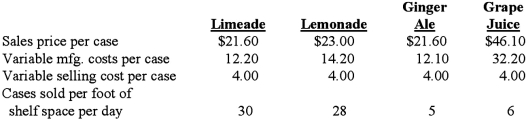

The Sand Cruiser is a takeout food store at a popular beachside resort.Teresa Texton, owner of the Sand Cruiser, was deciding how much refrigerator space to devote to four different beverages.Appropriate data on the four beverages follow:  Teresa had a maximum front shelf space of fourteen feet to devote to the four beverages.She wanted a minimum of two feet and a maximum of seven feet of front shelf for each beverage.The contribution margin per case for Limeade is:

Teresa had a maximum front shelf space of fourteen feet to devote to the four beverages.She wanted a minimum of two feet and a maximum of seven feet of front shelf for each beverage.The contribution margin per case for Limeade is:

A)$5.50.

B)$6.40.

C)$17.60.

D)$16.20.

E)$9.40.

Teresa had a maximum front shelf space of fourteen feet to devote to the four beverages.She wanted a minimum of two feet and a maximum of seven feet of front shelf for each beverage.The contribution margin per case for Limeade is:A)$5.50.

B)$6.40.

C)$17.60.

D)$16.20.

E)$9.40.

Question

Question

Question

Question

The Tee Box is a golf shop inside the clubhouse of a North Carolina golf course.Derek Dunlop, owner of the Tee Box, was deciding how much shelf space to devote to four different golf ball types.Derek had a maximum front shelf space of fifteen feet to devote to the four golf ball types.He wanted a minimum of three feet and a maximum of seven feet of front shelf for each golf ball type.Appropriate data on the four ball types follow:  The daily contribution per foot of front shelf space for Straight is calculated to be:

The daily contribution per foot of front shelf space for Straight is calculated to be:

A)$190.00

B)$140.00

C)$120.00

D)$130.00

E)$170.00

The daily contribution per foot of front shelf space for Straight is calculated to be:A)$190.00

B)$140.00

C)$120.00

D)$130.00

E)$170.00

Question

Question

Question

Question

Question

Question

Question

The Car Lot is a New York car dealership located in a highly visible area along a prominent highway.Fred Barns, owner of The Car Lot, was deciding how much front-row space along the highway to devote to four different car models.Fred had a maximum front-row space of 200 feet to devote to the four car models.He wanted a minimum of twenty feet and a maximum of eighty feet of front-row space for each car model.Appropriate data on the four car models follow:  The convertible model's monthly contribution per 10 feet of front-row space is calculated to be:

The convertible model's monthly contribution per 10 feet of front-row space is calculated to be:

A)$70,000.

B)$60,000.

C)$90,000.

D)$80,000.

E)$30,000.

The convertible model's monthly contribution per 10 feet of front-row space is calculated to be:A)$70,000.

B)$60,000.

C)$90,000.

D)$80,000.

E)$30,000.

Question

Question

Question

Under the assumption that the company would like to minimize total cost, what should the company do, and what are the total cost savings in the first year?

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/137

Play

Full screen (f)

Deck 11: Decision Making With a Strategic Emphasis

1

One of the behavioral problems with relevant cost analysis is the overemphasis on:

A)Short-term goals.

B)Unit fixed costs.

C)Opportunity costs.

D)Long-term strategic goals.

E)Goal congruency issues.

A)Short-term goals.

B)Unit fixed costs.

C)Opportunity costs.

D)Long-term strategic goals.

E)Goal congruency issues.

A

2

Which one of the following issues would least likely be addressed during the regular review of product profitability?

A)Which product managers should be rewarded?

B)Which products are most profitable?

C)Which products provide the greatest contribution margin per unit of the scarce resource?

D)Which products should be promoted and advertised most aggressively?

E)Are the products priced properly?

A)Which product managers should be rewarded?

B)Which products are most profitable?

C)Which products provide the greatest contribution margin per unit of the scarce resource?

D)Which products should be promoted and advertised most aggressively?

E)Are the products priced properly?

C

3

Depreciation expense is a relevant cost in a decision only in the context of:

A)Time value of money.

B)Amortized values.

C)Reducing the tax liability of the organization.

D)Determining sunk costs associated with the decision problem.

E)Financial accounting.

A)Time value of money.

B)Amortized values.

C)Reducing the tax liability of the organization.

D)Determining sunk costs associated with the decision problem.

E)Financial accounting.

C

4

Which one of the following is most descriptive of a strategic analysis conducted as part of a decision analysis?

A)Quantitative.

B)Customer focus.

C)Short-term orientation.

D)Individual product focus.

E)Differential costing.

A)Quantitative.

B)Customer focus.

C)Short-term orientation.

D)Individual product focus.

E)Differential costing.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

5

A special sales order is:

A)Typically expected.

B)A profitable opportunity to sell a specified quantity of a firm's product or service.

C)A one-time opportunity to sell a specified quantity of a product or service.

D)A particularly large customer order.

E)In most cases, a rush order.

A)Typically expected.

B)A profitable opportunity to sell a specified quantity of a firm's product or service.

C)A one-time opportunity to sell a specified quantity of a product or service.

D)A particularly large customer order.

E)In most cases, a rush order.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

6

All the following are characteristic of relevant costs except:

A)They are generally variable.

B)They are not committed.

C)They are different in amount for different options.

D)They are costs that will be incurred in the future.

E)They are inventory-related costs.

A)They are generally variable.

B)They are not committed.

C)They are different in amount for different options.

D)They are costs that will be incurred in the future.

E)They are inventory-related costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

7

The major problem with relevant cost determination is that it fails to recognize the:

A)Impact of variable costs in the long run.

B)Long-term nature of most product-related decisions.

C)"Sunk" nature of most fixed product costs.

D)Short-term nature of most product-related decisions.

E)Need to calculate costs more precisely.

A)Impact of variable costs in the long run.

B)Long-term nature of most product-related decisions.

C)"Sunk" nature of most fixed product costs.

D)Short-term nature of most product-related decisions.

E)Need to calculate costs more precisely.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

8

Which one of the following is correct for determining relevant costs for decision-making?

A)Differential.

B)Integrative.

C)Long-term focus.

D)Subjective.

E)Absorption.

A)Differential.

B)Integrative.

C)Long-term focus.

D)Subjective.

E)Absorption.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

9

The decision to keep or drop products or services involves strategic consideration of all the following except:

A)Potential impact on remaining products or services.

B)Impact on employee morale.

C)Impact on organizational effectiveness.

D)Growth potential of the firm.

E)The desired inventory levels of the product.

A)Potential impact on remaining products or services.

B)Impact on employee morale.

C)Impact on organizational effectiveness.

D)Growth potential of the firm.

E)The desired inventory levels of the product.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

10

A useful device for solving production problems involving multiple products and limited resources is:

A)Gross profit per unit of product.

B)Contribution per unit of scarce resource.

C)Value-stream costing.

D)Relevant cost pricing.

E)The contribution income statement.

A)Gross profit per unit of product.

B)Contribution per unit of scarce resource.

C)Value-stream costing.

D)Relevant cost pricing.

E)The contribution income statement.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

11

Determination of the optimum short-term product mix needs to include an analysis of:

A)Fully absorbed costs.

B)Production constraints.

C)Sales-mix costs.

D)Revenue forecasts.

E)Joint manufacturing costs.

A)Fully absorbed costs.

B)Production constraints.

C)Sales-mix costs.

D)Revenue forecasts.

E)Joint manufacturing costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

12

Operating at or near full capacity will require a firm considering a special sales order to potentially recognize the:

A)Opportunity cost from lost sales.

B)Value of full employment.

C)The use of operating leverage.

D)Need for good management.

E)Importance of facility-level cost drivers.

A)Opportunity cost from lost sales.

B)Value of full employment.

C)The use of operating leverage.

D)Need for good management.

E)Importance of facility-level cost drivers.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

13

The value chain analysis used in connection with the make-or-buy decision often leads a firm to make use of:

A)Activity-based costing (ABC).

B)Cost-volume profit (CVP) analysis.

C)Outsourcing options.

D)Relevant cost-based pricing.

E)Value stream accounting.

A)Activity-based costing (ABC).

B)Cost-volume profit (CVP) analysis.

C)Outsourcing options.

D)Relevant cost-based pricing.

E)Value stream accounting.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

14

Fixed costs will often be irrelevant for decision making because they:

A)Do not vary on a per-unit-of-output basis.

B)Are the same each time period.

C)Typically do not differ between and among decision alternatives.

D)Are not committed.

E)Cannot be estimated with precision.

A)Do not vary on a per-unit-of-output basis.

B)Are the same each time period.

C)Typically do not differ between and among decision alternatives.

D)Are not committed.

E)Cannot be estimated with precision.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

15

Special sales orders:

A)Are frequent.

B)Typically come directly from the customer rather than normal sales or distribution channels.

C)Commonly represent a large part of a firm's overall business.

D)Can never be profitable to a firm in the short run.

E)Generally speaking do not involve long-term pricing considerations.

A)Are frequent.

B)Typically come directly from the customer rather than normal sales or distribution channels.

C)Commonly represent a large part of a firm's overall business.

D)Can never be profitable to a firm in the short run.

E)Generally speaking do not involve long-term pricing considerations.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

16

A cost is not relevant for decision making if it:

A)Does not differ for each option available to the decision maker.

B)Changes from period to period.

C)Is a future cost.

D)Is a mixed cost.

E)Is a fixed cost.

A)Does not differ for each option available to the decision maker.

B)Changes from period to period.

C)Is a future cost.

D)Is a mixed cost.

E)Is a fixed cost.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

17

When using relevant cost analysis, it is a common mistake for untrained managers to include in their analysis all the following except:

A)Sunk costs.

B)Allocated fixed costs.

C)Average fixed costs.

D)Unit variable costs.

E)Total fixed costs.

A)Sunk costs.

B)Allocated fixed costs.

C)Average fixed costs.

D)Unit variable costs.

E)Total fixed costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

18

Committed or "sunk" costs are generally:

A)Not fixed.

B)Small in amount.

C)The result of prior bad decisions.

D)Those that have been incurred in the past.

E)Recoverable in trade.

A)Not fixed.

B)Small in amount.

C)The result of prior bad decisions.

D)Those that have been incurred in the past.

E)Recoverable in trade.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

19

Done on a regular basis, relevant cost pricing in special order decisions can erode normal pricing policies and lead to:

A)Overconfidence in decision-making.

B)A decrease in the firm's long-term profitability.

C)Goal congruence between management and sales personnel.

D)A cost leadership strategy.

E)Maximization of the value stream.

A)Overconfidence in decision-making.

B)A decrease in the firm's long-term profitability.

C)Goal congruence between management and sales personnel.

D)A cost leadership strategy.

E)Maximization of the value stream.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

20

Variable costs will generally be relevant for decision making because they:

A)Differ between options.

B)Are volume-based.

C)Have not been committed and differ between options.

D)Differ between options and have been committed.

E)Measure opportunity cost.

A)Differ between options.

B)Are volume-based.

C)Have not been committed and differ between options.

D)Differ between options and have been committed.

E)Measure opportunity cost.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

21

Product X's sales value at the split-off point is:

A)$306,000.

B)$135,000.

C)$340,000.

D)$150,000.

E)$233,000.

A)$306,000.

B)$135,000.

C)$340,000.

D)$150,000.

E)$233,000.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

22

In a joint production process, the allocation of joint (common) costs to the joint products is needed:

A)To meet external reporting requirements (i.e., for financial statement preparation purposes).

B)To determine whether the firm in question should produce at all.

C)To assess managerial performance.

D)To determine which products, if any, should be produced beyond the split-off point.

E)For short-term decision-making purposes.

A)To meet external reporting requirements (i.e., for financial statement preparation purposes).

B)To determine whether the firm in question should produce at all.

C)To assess managerial performance.

D)To determine which products, if any, should be produced beyond the split-off point.

E)For short-term decision-making purposes.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

23

The Blade Division of Dana Company produces hardened steel blades.Approximately one-third of the Blade Division's output is sold to the Lawn Products Division of Dana; the remainder is sold to outside customers.The Blade Division's estimated sales and cost data for the year ending June 30 are as follows: The Lawn Products Division has an opportunity to purchase 10,000 identical quality blades from an outside supplier at a cost of $1.25 per unit on a continual basis.Assume that the Blade Division cannot sell any additional products to outside customers.Based solely on short-term financial considerations, should Dana allow its Lawn Products Division to purchase the blades from the outside supplier, and why?

A)Yes, because buying the blades would save Dana Company $500.

B)No, because making the blades would save Dana Company $1,500.

C)Yes, because buying the blades would save Dana Company $2,500.

D)No, because making the blades would save Dana Company $2,500.

The Lawn Products Division has an opportunity to purchase 10,000 identical quality blades from an outside supplier at a cost of $1.25 per unit on a continual basis.Assume that the Blade Division cannot sell any additional products to outside customers.Based solely on short-term financial considerations, should Dana allow its Lawn Products Division to purchase the blades from the outside supplier, and why?A)Yes, because buying the blades would save Dana Company $500.

B)No, because making the blades would save Dana Company $1,500.

C)Yes, because buying the blades would save Dana Company $2,500.

D)No, because making the blades would save Dana Company $2,500.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

24

Quirch Inc.manufactures machine parts for aircraft engines.The CEO, Chucky Valters, was considering an offer from a subcontractor who would provide 2,400 units of product PQ107 for Valters for a price of $150,000.If Quirch does not purchase these parts from the subcontractor it must produce them in-house with the following costs: In addition to the above costs, if Quirch produces part PQ107, it would also have a retooling and design cost of $9,800.The relevant costs of producing 2,400 units of product PQ107 are:

A)$149,000.

B)$129,800.

C)$150,000.

D)$164,200.

E)$148,300.

In addition to the above costs, if Quirch produces part PQ107, it would also have a retooling and design cost of $9,800.The relevant costs of producing 2,400 units of product PQ107 are:A)$149,000.

B)$129,800.

C)$150,000.

D)$164,200.

E)$148,300.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

25

Based solely on a relevant cost analysis, which of the three products should be manufactured by Walman beyond the split-off point?

A)Only X

B)Only Y

C)Only Z

D)Only Y and Z

E)All three products: X, Y and Z

A)Only X

B)Only Y

C)Only Z

D)Only Y and Z

E)All three products: X, Y and Z

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

26

The contribution margin per unit for Clash is:

A)$53.

B)$35.

C)$47.

D)$42.

E)$23.

A)$53.

B)$35.

C)$47.

D)$42.

E)$23.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

27

Kingston Company, which needs 10,000 units of a certain part to be used in its production cycle, can make or buy the part.If Kingston buys the part from Utica Company, Kingston could not use the released facilities in another manufacturing activity within the coming year.60% of the fixed overhead applied will continue regardless of which decision is made.The following information is available: Cost to Kingston to make the part: In deciding whether to make or buy the part, Kingston's total relevant costs to make the part are:

A)$342,000.

B)$480,000

C)$530,000.

D)$570,000.

E)Some other amount.

A)$342,000.

B)$480,000

C)$530,000.

D)$570,000.

E)Some other amount.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

28

In a make-or-buy decision:

A)Only variable costs are relevant.

B)Fixed costs that can be avoided in the future are relevant.

C)Fixed costs that will continue regardless of the decision are relevant.

D)Only opportunity costs are relevant.

E)Opportunity costs are generally zero.

A)Only variable costs are relevant.

B)Fixed costs that can be avoided in the future are relevant.

C)Fixed costs that will continue regardless of the decision are relevant.

D)Only opportunity costs are relevant.

E)Opportunity costs are generally zero.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

29

To make a decision whether to accept or reject a special sales order, managers need critical information about all the following except:

A)Relevant costs.

B)Prior period operating costs.

C)Any opportunity costs.

D)The strategic, competitive environment of the firm.

A)Relevant costs.

B)Prior period operating costs.

C)Any opportunity costs.

D)The strategic, competitive environment of the firm.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

30

In a joint production process, joint product costs are:

A)Those costs incurred after the split-off point.

B)Allocated to outputs (products) to facilitate short-term decision making.

C)Not relevant to the decision whether to produce at all.

D)Those that are incurred before the point in the process when individual products arise.

E)Relatively small compared to costs incurred after the split-off point.

A)Those costs incurred after the split-off point.

B)Allocated to outputs (products) to facilitate short-term decision making.

C)Not relevant to the decision whether to produce at all.

D)Those that are incurred before the point in the process when individual products arise.

E)Relatively small compared to costs incurred after the split-off point.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements regarding a joint production process is NOT true?

A)The essential decision facing management is whether to sell products at the split-off point or to sell these products after further processing.

B)The allocation of joint (common) production costs to individual products helps management determine which products should be processed beyond the split-off point.

C)Costs incurred up to the split-off point are referred to as joint production costs.

D)The decision as to whether individual products should be sold "as is" or processed further is made on the basis of comparing incremental revenues and incremental costs.

E)For financial reporting purposes output (inventory) is valued at the sum of separable processing cost plus an allocated share of joint production costs.

A)The essential decision facing management is whether to sell products at the split-off point or to sell these products after further processing.

B)The allocation of joint (common) production costs to individual products helps management determine which products should be processed beyond the split-off point.

C)Costs incurred up to the split-off point are referred to as joint production costs.

D)The decision as to whether individual products should be sold "as is" or processed further is made on the basis of comparing incremental revenues and incremental costs.

E)For financial reporting purposes output (inventory) is valued at the sum of separable processing cost plus an allocated share of joint production costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

32

Plainfield Company manufactures part G for use in its production cycle.The costs per unit for 10,000 units of part G are as follows: Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit.If Plainfield accepts Verona's offer, the released facilities could be used to save $45,000 in relevant costs in the manufacture of part H.In addition, $5 per unit of the fixed overhead applied to part G would be totally eliminated.What alternative is more desirable and by what amount?

A)Option A

B)Option B

C)Option C

D)Option D

Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit.If Plainfield accepts Verona's offer, the released facilities could be used to save $45,000 in relevant costs in the manufacture of part H.In addition, $5 per unit of the fixed overhead applied to part G would be totally eliminated.What alternative is more desirable and by what amount? A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

33

Joint (common) costs in a joint production process are relevant for determining:

A)Whether to produce at all.

B)Which products should be produced up to the split-off point in the production process.

C)Which products should be produced internally and which products should be outsourced.

D)The set of products that should be subjected to additional processing.

E)The selling price of individual products produced as part of the joint production process.

A)Whether to produce at all.

B)Which products should be produced up to the split-off point in the production process.

C)Which products should be produced internally and which products should be outsourced.

D)The set of products that should be subjected to additional processing.

E)The selling price of individual products produced as part of the joint production process.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

34

Given a selling price per unit of $750, what is the contribution margin per unit sold?

A)$336.

B)$316.

C)$276.

D)$396.

E)$630.

A)$336.

B)$316.

C)$276.

D)$396.

E)$630.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

35

In deciding whether to manufacture a part or buy it from an outside vendor, a cost that is irrelevant to this short-run decision is:

A)Direct labor.

B)Variable overhead.

C)Fixed overhead that will be avoided if the part is bought from an outside vendor.

D)Fixed overhead that will continue even if the part is bought from an outside vendor.

E)Transportation-in charges assessed on external purchases.

A)Direct labor.

B)Variable overhead.

C)Fixed overhead that will be avoided if the part is bought from an outside vendor.

D)Fixed overhead that will continue even if the part is bought from an outside vendor.

E)Transportation-in charges assessed on external purchases.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

36

In view of the labor shortage, which of the two products is most profitable, and how much is the contribution margin, per direct labor hour?

A)Slash, $23.00.

B)Clash, $18.00.

C)Slash, $11.50.

D)Slash, $11.00.

E)Clash, $10.50.

A)Slash, $23.00.

B)Clash, $18.00.

C)Slash, $11.50.

D)Slash, $11.00.

E)Clash, $10.50.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

37

For the past 12 years, the Blue Company has produced the small electric motors that fit into its main product line of dental drilling equipment.As material costs have steadily increased, the controller of the company is reviewing the decision to continue to make the small motors and has identified the following facts: (1) The equipment used to manufacture the electric motors has a net book value (NBV) of $150,000.

(2) The space now occupied by the electric motor manufacturing department could be used to eliminate the need for storage space now being rented.

(3) Comparable units can be purchased from an outside supplier for $59.75.

(4) Four of those who work in the electric motor manufacturing department would be terminated and given eight weeks' severance pay.

(5) A $10,000 unsecured note is still outstanding on the equipment used in the manufacturing process.

Which of the items above are relevant to the controller's decision analysis?

A)1, 3, and 4.

B)2, 3, and 4.

C)2, 3, 4, and 5.

D)1, 2, 4, and 5.

E)4 and 5

(2) The space now occupied by the electric motor manufacturing department could be used to eliminate the need for storage space now being rented.

(3) Comparable units can be purchased from an outside supplier for $59.75.

(4) Four of those who work in the electric motor manufacturing department would be terminated and given eight weeks' severance pay.

(5) A $10,000 unsecured note is still outstanding on the equipment used in the manufacturing process.

Which of the items above are relevant to the controller's decision analysis?

A)1, 3, and 4.

B)2, 3, and 4.

C)2, 3, 4, and 5.

D)1, 2, 4, and 5.

E)4 and 5

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

38

Assume that the Violin Division was evaluating whether or not it would accept a special sales order for ten violins at $390 per unit.For this purpose, total relevant cost per unit (given the costs stated above) is:

A)$330.

B)$342.

C)$390.

D)$366.

E)$354.

A)$330.

B)$342.

C)$390.

D)$366.

E)$354.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

39

A boat, costing $108,000 and uninsured, was wrecked the very first day it was used.It can either be disposed of for $11,000 cash and be replaced with a similar boat costing $110,000, or rebuilt for $98,000 and be brand new as far as operating characteristics and looks are concerned.A relevant cost analysis of the decision to replace the boat shows:

A)A cost equivalence between the two decision options.

B)An $11,000 net advantage associated with the decision to fix the old boat.

C)A $1,000 cost advantage associated with the decision to fix the old boat.

D)A $21,000 cost advantage associated with the decision to fix the old boat.

E)A $2,000 cost advantage associated with the decision to purchase a new boat.

A)A cost equivalence between the two decision options.

B)An $11,000 net advantage associated with the decision to fix the old boat.

C)A $1,000 cost advantage associated with the decision to fix the old boat.

D)A $21,000 cost advantage associated with the decision to fix the old boat.

E)A $2,000 cost advantage associated with the decision to purchase a new boat.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following statements regarding "opportunity costs" is TRUE?

A)These costs are recorded routinely by cost accounting systems.

B)These costs relate to the benefit lost or foregone when a chosen option (course of action) precludes the benefits from an alternative option.

C)These costs are generally deductible for federal income tax purposes.

D)In terms of most short-run decisions, they are irrelevant.

E)They are usually considered a sunk cost associated with one or more decision alternatives.

A)These costs are recorded routinely by cost accounting systems.

B)These costs relate to the benefit lost or foregone when a chosen option (course of action) precludes the benefits from an alternative option.

C)These costs are generally deductible for federal income tax purposes.

D)In terms of most short-run decisions, they are irrelevant.

E)They are usually considered a sunk cost associated with one or more decision alternatives.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

41

The contribution margin per case for Lemonade is:

A)$5.50.

B)$6.40.

C)$5.40.

D)$4.80.

E)$9.90.

A)$5.50.

B)$6.40.

C)$5.40.

D)$4.80.

E)$9.90.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

42

When deciding to purchase a new cutting machine or continue using the existing machine, the following costs are all relevant EXCEPT the:

A)$60,000 cost of the old machine.

B)$30,000 cost of the new machine.

C)$15,000 disposal (salvage) value of the old machine.

D)$4,000 annual savings in operating costs if the new machine is purchased.

E)Maintenance costs, which are expected to be less under the new machine.

A)$60,000 cost of the old machine.

B)$30,000 cost of the new machine.

C)$15,000 disposal (salvage) value of the old machine.

D)$4,000 annual savings in operating costs if the new machine is purchased.

E)Maintenance costs, which are expected to be less under the new machine.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

43

When deciding whether to discontinue a segment of a business, managers should focus on:

A)The amount of operating income per unit produced by the segment.

B)The amount of contribution margin per direct labor hour in the segment.

C)How corporate-level administrative costs would be redistributed if the segment were eliminated.

D)Equipment from the segment that could go idle if the segment were discontinued.

E)The total contribution margin generated by the segment relative to any traceable (avoidable) fixed costs associated with the segment.

A)The amount of operating income per unit produced by the segment.

B)The amount of contribution margin per direct labor hour in the segment.

C)How corporate-level administrative costs would be redistributed if the segment were eliminated.

D)Equipment from the segment that could go idle if the segment were discontinued.

E)The total contribution margin generated by the segment relative to any traceable (avoidable) fixed costs associated with the segment.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

44

Opportunity costs:

A)Result in a cash outlay.

B)Unless zero are always relevant for decision making.

C)Should be maximized for the best decision.

D)Are recorded in the accounting records.

E)Are the result of a completed event or transaction.

A)Result in a cash outlay.

B)Unless zero are always relevant for decision making.

C)Should be maximized for the best decision.

D)Are recorded in the accounting records.

E)Are the result of a completed event or transaction.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

45

The contribution per foot of front shelf space per day for Limeade is:

A)$165.00.

B)$162.00.

C)$154.00.

D)$134.40.

E)$153.90.

A)$165.00.

B)$162.00.

C)$154.00.

D)$134.40.

E)$153.90.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

46

In the situation where a firm produces multiple products and the firm has a single resource constraint (e.g., machine hours), the most profitable use of available capacity (machine hours) requires that we assess:

A)Total demand for each product.

B)The selling price per unit for each product.

C)Non production-related costs (e.g., selling costs) associated with each product.

D)The contribution margin of each product per machine hour.

E)The gross profit per unit of each product.

A)Total demand for each product.

B)The selling price per unit for each product.

C)Non production-related costs (e.g., selling costs) associated with each product.

D)The contribution margin of each product per machine hour.

E)The gross profit per unit of each product.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

47

In deciding whether to accept or a reject a special sales order, which of the following costs are likely relevant to the decision?

A)Depreciation expense on manufacturing equipment.

B)A portion of facilities-level costs.

C)A portion of batch-level costs.

D)Total batch-level costs.

E)An allocated share of fixed manufacturing support costs.

A)Depreciation expense on manufacturing equipment.

B)A portion of facilities-level costs.

C)A portion of batch-level costs.

D)Total batch-level costs.

E)An allocated share of fixed manufacturing support costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

48

When there is limited capacity, the minimum acceptable price for a special sales order will equal the _______________ from the product that is sacrificed plus the variable costs of the ordered product.

A)Selling price.

B)Full cost.

C)Variable cost.

D)Contribution margin.

A)Selling price.

B)Full cost.

C)Variable cost.

D)Contribution margin.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

49

The opportunity cost of making a component part in a factory with excess capacity for which there is no alternative use is:

A)The variable manufacturing cost of the component.

B)The total manufacturing cost of the component.

C)The total variable cost of the component.

D)The fixed manufacturing cost of the component.

E)Zero.

A)The variable manufacturing cost of the component.

B)The total manufacturing cost of the component.

C)The total variable cost of the component.

D)The fixed manufacturing cost of the component.

E)Zero.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

50

When a firm has surplus capacity as opposed to constrained capacity (i.e., resource constraints), relevant costs for decision-making (e.g., determining short-term product mix) will be:

A)Lower.

B)The same.

C)Greater.

D)It varies-that is, it is impossible to tell without further information.

A)Lower.

B)The same.

C)Greater.

D)It varies-that is, it is impossible to tell without further information.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

51

Lyman Company has the opportunity to increase annual credit sales $100,000 by selling to a new, riskier group of customers.The expenses of collecting credit sales are expected to be 15 percent of credit sales.The company's manufacturing and selling expenses are 70% of sales, and its effective tax rate is 40%.If Lyman should accept this opportunity, the company's after-tax profits would increase by:

A)$9,000.

B)$10,000.

C)$10,200.

D)$14,400.

E)Some amount other than those given above.

A)$9,000.

B)$10,000.

C)$10,200.

D)$14,400.

E)Some amount other than those given above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

52

A company owns equipment that is used to manufacture important parts for its production process.Because the equipment is repeatedly breaking down, the company plans to sell the equipment for $10,000 and to select one of the following alternatives: (1) acquire new equipment for $80,000 and continue to manufacture the part at the same variable cost, or (2) purchase the parts from an outside company at $4 per part.In the short run the company should quantitatively analyze the alternatives by comparing the variable cost of manufacturing the parts:

A)Plus $80,000, to the cost of buying the parts.

B)To the cost of buying the parts less $10,000.

C)Less $10,000 to the cost of buying the parts.

D)To the cost of buying the parts.

E)Plus $70,000, to the cost of buying the parts.

A)Plus $80,000, to the cost of buying the parts.

B)To the cost of buying the parts less $10,000.

C)Less $10,000 to the cost of buying the parts.

D)To the cost of buying the parts.

E)Plus $70,000, to the cost of buying the parts.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

53

The costs described in situations 1 and 4 above are:

A)Prime costs.

B)Sunk costs.

C)Discretionary costs.

D)Relevant costs.

E)Fully-absorbed costs.

A)Prime costs.

B)Sunk costs.

C)Discretionary costs.

D)Relevant costs.

E)Fully-absorbed costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

54

The contribution margin per machine hour is calculated as:

A)Full cost per unit ÷ number of machine-hours per unit.

B)Number of machine-hours per unit ÷ full-cost per unit.

C)Selling price per unit less variable manufacturing cost per unit.

D)Selling price per unit less variable manufacturing cost per unit less variable selling cost per machine-hour.

E)Selling price per unit less total variable cost per unit, divided by number of machine-hours per unit.

A)Full cost per unit ÷ number of machine-hours per unit.

B)Number of machine-hours per unit ÷ full-cost per unit.

C)Selling price per unit less variable manufacturing cost per unit.

D)Selling price per unit less variable manufacturing cost per unit less variable selling cost per machine-hour.

E)Selling price per unit less total variable cost per unit, divided by number of machine-hours per unit.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

55

The practice of setting prices below average variable cost and plans to raise prices later to recover the losses from the lower prices, is referred to as:

A)Marginal cost pricing.

B)Activity-based pricing.

C)Menu-based pricing.

D)Cost-plus pricing.

E)Predatory pricing.

A)Marginal cost pricing.

B)Activity-based pricing.

C)Menu-based pricing.

D)Cost-plus pricing.

E)Predatory pricing.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

56

The costs described in situations 2, 3, and 5 above are:

A)Prime costs.

B)Sunk costs.

C)Discretionary costs.

D)Relevant costs.

E)Differential costs.

A)Prime costs.

B)Sunk costs.

C)Discretionary costs.

D)Relevant costs.

E)Differential costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

57

The Sand Cruiser is a takeout food store at a popular beachside resort.Teresa Texton, owner of the Sand Cruiser, was deciding how much refrigerator space to devote to four different beverages.Appropriate data on the four beverages follow: Teresa had a maximum front shelf space of fourteen feet to devote to the four beverages.She wanted a minimum of two feet and a maximum of seven feet of front shelf for each beverage.The contribution margin per case for Limeade is:

A)$5.50.

B)$6.40.

C)$17.60.

D)$16.20.

E)$9.40.

Teresa had a maximum front shelf space of fourteen feet to devote to the four beverages.She wanted a minimum of two feet and a maximum of seven feet of front shelf for each beverage.The contribution margin per case for Limeade is:A)$5.50.

B)$6.40.

C)$17.60.

D)$16.20.

E)$9.40.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

58

For short-run product-mix decisions, relevant costs (for the seller) include short-run _________ costs plus any ____________ costs.

A)direct material; direct labor.

B)variable; opportunity.

C)fixed; differential.

D)support; distribution.

E)capital; opportunity.

A)direct material; direct labor.

B)variable; opportunity.

C)fixed; differential.

D)support; distribution.

E)capital; opportunity.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

59

The opportunity cost of making a component part in a factory with no excess capacity is the:

A)Variable manufacturing cost of the component.

B)Fixed manufacturing cost of the component.

C)Total manufacturing cost of the component.

D)Cost of the production given up in order to manufacture the component.

E)Net benefit foregone from the best alternative use of the capacity required.

A)Variable manufacturing cost of the component.

B)Fixed manufacturing cost of the component.

C)Total manufacturing cost of the component.

D)Cost of the production given up in order to manufacture the component.

E)Net benefit foregone from the best alternative use of the capacity required.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

60

Relevant costs for a make-or-buy decision for a component part include all of the following EXCEPT:

A)Fixed salaries that will not be incurred if the part is outsourced.

B)Payroll tax (unemployment insurance cost), because of outsourcing.

C)Material-handling costs that can be eliminated if the part is outsourced.

D)Special machinery for the part that has no resale value.

E)Current direct material costs for the part.

A)Fixed salaries that will not be incurred if the part is outsourced.

B)Payroll tax (unemployment insurance cost), because of outsourcing.

C)Material-handling costs that can be eliminated if the part is outsourced.

D)Special machinery for the part that has no resale value.

E)Current direct material costs for the part.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

61

The Tee Box is a golf shop inside the clubhouse of a North Carolina golf course.Derek Dunlop, owner of the Tee Box, was deciding how much shelf space to devote to four different golf ball types.Derek had a maximum front shelf space of fifteen feet to devote to the four golf ball types.He wanted a minimum of three feet and a maximum of seven feet of front shelf for each golf ball type.Appropriate data on the four ball types follow: The daily contribution per foot of front shelf space for Straight is calculated to be:

A)$190.00

B)$140.00

C)$120.00

D)$130.00

E)$170.00

The daily contribution per foot of front shelf space for Straight is calculated to be:A)$190.00

B)$140.00

C)$120.00

D)$130.00

E)$170.00

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

62

In deciding between alternative choices for a given situation, managers usually employ a five-step process.Which of the following is not a step in the decision-making process?

A)Evaluate performance.

B)Specify the criteria and identify the alternative actions.

C)Select and implement the best course of action.

D)Perform relevant and strategic cost analysis.

E)Review the audit report.

A)Evaluate performance.

B)Specify the criteria and identify the alternative actions.

C)Select and implement the best course of action.

D)Perform relevant and strategic cost analysis.

E)Review the audit report.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

63

Assuming that Product Line C is discontinued and the manufacturing space formerly devoted to this line is rented for $6,000 per year, operating income for the company will:

A)Be unchanged-the two effects cancel each other out.

B)Increase by $3,300.

C)Increase by $4,500.

D)Increase by $7,200.

E)Increase by some other amount.

A)Be unchanged-the two effects cancel each other out.

B)Increase by $3,300.

C)Increase by $4,500.

D)Increase by $7,200.

E)Increase by some other amount.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

64

Relevant costs in a make-vs.-buy decision of a part include:

A)Corporate headquarter costs that will be allocated differently depending on the decision option chosen.

B)Setup overhead costs for the manufacture of the product using the outsourced part.

C)Currently used manufacturing capacity that has alternative uses if the part is outsourced.

D)Factory-related insurance cost.

E)Corporate (i.e., headquarter) salaries.

A)Corporate headquarter costs that will be allocated differently depending on the decision option chosen.

B)Setup overhead costs for the manufacture of the product using the outsourced part.

C)Currently used manufacturing capacity that has alternative uses if the part is outsourced.

D)Factory-related insurance cost.

E)Corporate (i.e., headquarter) salaries.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

65

The Robinson-Patman Act, administered by the U.S.Federal Trade Commission, addresses pricing that could substantially damage the competition in an industry.This pricing is called:

A)Competitive pricing.

B)Predatory pricing.

C)Cost-benefit pricing.

D)Variable pricing.

E)Incentive pricing.

A)Competitive pricing.

B)Predatory pricing.

C)Cost-benefit pricing.

D)Variable pricing.

E)Incentive pricing.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

66

The maximum price that Preston should be willing to pay the outside vendor for each unit of QX100 is:

A)$10.00

B)$11.00

C)$15.00

D)$15.80

E)$16.00

A)$10.00

B)$11.00

C)$15.00

D)$15.80

E)$16.00

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

67

The cost(s) NOT relevant for this asset-replacement decision is/are:

A)The acquisition cost of the used fork lift.

B)The acquisition cost of the existing fork lift.

C)The repairs cost for the existing fork lift.

D)The annual operating costs for the existing fork lift.

E)The annual operating costs for the used fork lift.

A)The acquisition cost of the used fork lift.

B)The acquisition cost of the existing fork lift.

C)The repairs cost for the existing fork lift.

D)The annual operating costs for the existing fork lift.

E)The annual operating costs for the used fork lift.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

68

The Car Lot is a New York car dealership located in a highly visible area along a prominent highway.Fred Barns, owner of The Car Lot, was deciding how much front-row space along the highway to devote to four different car models.Fred had a maximum front-row space of 200 feet to devote to the four car models.He wanted a minimum of twenty feet and a maximum of eighty feet of front-row space for each car model.Appropriate data on the four car models follow: The convertible model's monthly contribution per 10 feet of front-row space is calculated to be:

A)$70,000.

B)$60,000.

C)$90,000.

D)$80,000.

E)$30,000.

The convertible model's monthly contribution per 10 feet of front-row space is calculated to be:A)$70,000.

B)$60,000.

C)$90,000.

D)$80,000.

E)$30,000.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

69

Calculate the expected surplus or deficit from operations given the above information.

A)$28,000 surplus.

B)$10,000 surplus.

C)$17,000 deficit.

D)$18,000 deficit.

A)$28,000 surplus.

B)$10,000 surplus.

C)$17,000 deficit.

D)$18,000 deficit.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

70

Diamond is thinking of dropping Product Line C because it is reporting an operating loss.Assuming the company drops Product Line C and does not replace it, operating income for the firm will:

A)Be unchanged

B)Increase by $1,200

C)Increase by $1,500

D)Decrease by $1,500

E)Decrease by $2,700

A)Be unchanged

B)Increase by $1,200

C)Increase by $1,500

D)Decrease by $1,500

E)Decrease by $2,700

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

71

Under the assumption that the company would like to minimize total cost, what should the company do, and what are the total cost savings in the first year?

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

72

Employee morale and social responsibility represent two examples of:

A)Qualitative decision factors.

B)Differential factors.

C)Opportunity costs.

D)Sunk cost expenditures.

E)Relevant costs.

A)Qualitative decision factors.

B)Differential factors.

C)Opportunity costs.

D)Sunk cost expenditures.

E)Relevant costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following items does NOT have to be considered when evaluating a make-or-buy decision?

A)The reliability of the supplier's delivery schedule.

B)Quality of the supplier's product.

C)Net book value of the production equipment used to make the item in question.

D)Contribution margin generated by an alternative use of the production equipment.

E)Financial stability of the supplier.

A)The reliability of the supplier's delivery schedule.

B)Quality of the supplier's product.

C)Net book value of the production equipment used to make the item in question.

D)Contribution margin generated by an alternative use of the production equipment.

E)Financial stability of the supplier.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

74

Value streams are useful in decision-making because:

A)They identify all value-added products and services.

B)They help to highlight the improved efficiency in the plant.

C)Special orders can be evaluated within the context of the value stream.

D)Irrelevant costs are identified.

E)Lean thinking produces better decision making.

A)They identify all value-added products and services.

B)They help to highlight the improved efficiency in the plant.

C)Special orders can be evaluated within the context of the value stream.

D)Irrelevant costs are identified.

E)Lean thinking produces better decision making.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

75

If the company accepts the offer from the outside supplier, the monthly avoidable costs (costs that would no longer be incurred) would be:

A)$32,000

B)$82,000

C)$158,000

D)$190,000

E)$110,000

A)$32,000

B)$82,000

C)$158,000

D)$190,000

E)$110,000

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

76

One of the key management functions is to perform a regular review of product profitability.Which question(s) below would not be asked when performing the analysis?

A)Are the products priced properly?

B)Which products are the most profitable?

C)Which products should be advertised more aggressively?

D)Should any product manager be rewarded?

E)What was the product manager paid last year?

A)Are the products priced properly?

B)Which products are the most profitable?

C)Which products should be advertised more aggressively?

D)Should any product manager be rewarded?

E)What was the product manager paid last year?

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

77

Orange Computer Co.is quickly becoming a major player in the personal computer market.The company currently has multiple companies producing products that go into an Orange computer.This practice of having an outside firm provide a function for Orange Computer Co.is called:

A)Outsourcing.

B)Opportunity costing.

C)Profitability maximization.

D)Strategic positioning.

E)Multivariate sourcing.

A)Outsourcing.

B)Opportunity costing.

C)Profitability maximization.

D)Strategic positioning.

E)Multivariate sourcing.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

78

Smith Co., maker of high-quality eyewear, incurs fixed costs of $18 and variable costs of $36 in making one unit of its matrix line of sunglasses.Smith Co.'s major supplier has offered to make all 100,000 matrix sunglasses for $44 each.If Smith accepts the offer of the supplier, Smith will save $4 per unit in fixed costs.Based on this information, should Smith Co.make or buy the sunglasses and how much will be saved?

A)Smith Co.should buy the sunglasses in order to save $200,000.

B)Smith Co.should buy the sunglasses in order to save $500,000.

C)Smith Co.should make the sunglasses in order to save $400,000.

D)Smith Co.should make the sunglasses in order to save $300,000.

A)Smith Co.should buy the sunglasses in order to save $200,000.

B)Smith Co.should buy the sunglasses in order to save $500,000.

C)Smith Co.should make the sunglasses in order to save $400,000.

D)Smith Co.should make the sunglasses in order to save $300,000.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

79

In deciding whether to drop or keep a product line, all of the following are relevant to the decision EXCEPT:

A)The level of unavoidable fixed costs.

B)The segment margin generated by the product line.

C)Demand interdependencies across product lines of the company.

D)Effect of the decision on overall company morale.

E)Whether dropping the product line today would eliminate future options for growth and expansion.

A)The level of unavoidable fixed costs.

B)The segment margin generated by the product line.

C)Demand interdependencies across product lines of the company.

D)Effect of the decision on overall company morale.

E)Whether dropping the product line today would eliminate future options for growth and expansion.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

80

Zippy Company has a product which it currently sells in the market for $50 per unit.Zippy has developed a new feature which, if added to the existing product, will allow Zippy to receive a price of $65 per unit.The cost of adding this new feature is $26,000 and Zippy expects to sell 1,600 units over the next year.What is the effect on operating income of adding the feature to the product?

A)$2,000 increase in operating income.

B)$3,000 decrease in operating income.

C)$3,500 increase in operating income.

D)$4,000 decrease in operating income.

E)$2,000 decrease in operating incomE.Net effect on operating income = incremental revenue - incremental costs = [($65 - $50)/unit × 1,600 units] - $26,000 = $24,000 - $26,000 = $2,000 decrease in operating income.

A)$2,000 increase in operating income.

B)$3,000 decrease in operating income.

C)$3,500 increase in operating income.

D)$4,000 decrease in operating income.

E)$2,000 decrease in operating incomE.Net effect on operating income = incremental revenue - incremental costs = [($65 - $50)/unit × 1,600 units] - $26,000 = $24,000 - $26,000 = $2,000 decrease in operating income.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 137 flashcards in this deck.