Deck 18: Attributes Sampling

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Which of the following sampling risks does the audit team control in an attributes sampling application (ROO = risk of overreliance,ROU = risk of underreliance)?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Question

Question

Question

Question

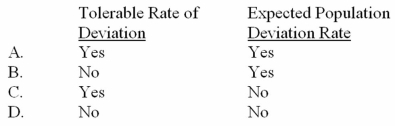

Which of the following factors has a direct relationship with sample size in an attributes sampling application?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/137

Play

Full screen (f)

Deck 18: Attributes Sampling

1

As the risk of overreliance decreases,the upper limit rate of deviation increases,holding all other factors constant.

True

2

The risk of underreliance occurs when the auditor's estimate of the deviation rate exceeds the tolerable rate of deviation.

True

3

In addition to the quantitative measure of deviations,the auditor should also consider qualitative measures,such as the pervasiveness and source of the deviations.

True

4

The tolerable rate of deviation has an inverse relationship with control risk; that is,as the acceptable level of control risk decreases,the appropriate tolerable rate of deviation increases.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

5

To measure sample items in an attributes sampling application,the auditor performs the appropriate test of controls.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

6

The risk of overreliance exposes the auditor to an effectiveness loss.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

7

Discovery sampling is ordinarily used when deviations from control procedures occur at a relatively low rate and are extremely important in the audit examination.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

8

Lower levels of control risk are typically associated with lower levels of the risk of overreliance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

9

If the upper limit rate of deviation exceeds the tolerable rate of deviation,the auditor may decide to increase the assessment of control risk.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

10

The upper limit rate of deviation is equal to the sample rate of deviation minus the allowance for sampling risk.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

11

The expected population deviation rate has an inverse relationship with the sample size.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

12

The sample rate of deviation is determined by dividing the number of deviations by the size of the population.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

13

When verifying the completeness assertion for sales transactions,the auditor would define the population as a shipping document for purposes of performing tests of controls.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

14

Of the two sampling risks associated with attributes sampling,auditors are more concerned with the risk of underreliance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

15

The auditor's sample size increases proportionally with increases in the population size.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

16

The upper limit rate of deviation has a (risk of overreliance)probability of being less than the true population deviation rate.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

17

After defining the deviations,the auditor would next identify the key controls to examine.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

18

The auditor determines the expected population deviation rate based on either prior audit experience or a pilot sample from the current year.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

19

Attributes sampling is most closely associated with the auditor's substantive procedures.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

20

The auditor's sample results must yield higher upper limit rate of deviation in order to support lower levels of control risk.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

21

In performing tests of controls over authorization of cash disbursements,which of the following statistical sampling methods would be most appropriate?

A) Variables.

B) Stratified.

C) Ratio.

D) Attributes.

A) Variables.

B) Stratified.

C) Ratio.

D) Attributes.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

22

The following are steps in attributes sampling: 1 = Define the population

2 = Determine the objective of sampling

3 = Determine the sample size

4 = Select the sample

What is the general order in which the steps are performed?

A) 1, 2, 3, 4.

B) 2, 1, 3, 4.

C) 1, 2, 4, 3.

D) 2, 1, 4, 3.

2 = Determine the objective of sampling

3 = Determine the sample size

4 = Select the sample

What is the general order in which the steps are performed?

A) 1, 2, 3, 4.

B) 2, 1, 3, 4.

C) 1, 2, 4, 3.

D) 2, 1, 4, 3.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

23

An auditor interested in ensuring that all sales have been recorded would define the population as:

A) Entries in the cash receipts journal.

B) Entries in the general journal.

C) Remittance advices.

D) Shipping documents.

A) Entries in the cash receipts journal.

B) Entries in the general journal.

C) Remittance advices.

D) Shipping documents.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following statements is correct concerning statistical sampling in tests of controls?

A) As the population increases, the sample size should increase proportionally.

B) The expected population deviation rate can either be based on prior audits or a small sample of controls examined in the current year.

C) There is an inverse relationship between the expected population deviation rate and sample size.

D) In determining the tolerable rate of deviation, an auditor considers detection risk and the sample size.

A) As the population increases, the sample size should increase proportionally.

B) The expected population deviation rate can either be based on prior audits or a small sample of controls examined in the current year.

C) There is an inverse relationship between the expected population deviation rate and sample size.

D) In determining the tolerable rate of deviation, an auditor considers detection risk and the sample size.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

25

For which of the following audit tests would an auditor most likely use attributes sampling?

A) Making an independent estimate of the amount of a LIFO inventory.

B) Examining invoices in support of the valuation of fixed asset additions.

C) Selecting accounts receivable for confirmation of account balances.

D) Inspecting employee time cards for proper approval by supervisors.

A) Making an independent estimate of the amount of a LIFO inventory.

B) Examining invoices in support of the valuation of fixed asset additions.

C) Selecting accounts receivable for confirmation of account balances.

D) Inspecting employee time cards for proper approval by supervisors.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

26

The risk of underreliance is the probability that the evidence in the sample indicates

A) Low control risk when the actual operating effectiveness of the control does not justify a low control risk assessment.

B) Low control risk when the actual operating effectiveness of the control would justify a low control risk assessment.

C) High control risk when the actual operating effectiveness of the control would justify a lower control risk assessment.

D) High control risk when the actual operating effectiveness of the control would justify a higher control risk assessment.

A) Low control risk when the actual operating effectiveness of the control does not justify a low control risk assessment.

B) Low control risk when the actual operating effectiveness of the control would justify a low control risk assessment.

C) High control risk when the actual operating effectiveness of the control would justify a lower control risk assessment.

D) High control risk when the actual operating effectiveness of the control would justify a higher control risk assessment.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

27

As a result of sampling procedures applied as tests of controls,an auditor incorrectly assesses control risk lower than appropriate.The most likely explanation for this situation is that

A) The deviation rates of both the auditor's sample and the population exceed the tolerable rate of deviation.

B) The deviation rates of both the auditor's sample and the population are less than the tolerable rate of deviation.

C) The deviation rate in the auditor's sample is less than the tolerable rate of deviation, but the deviation rate in the population exceeds the tolerable rate of deviation.

D) The deviation rate in the auditor's sample exceeds the tolerable rate of deviation, but the deviation rate in the population is less than the tolerable rate of deviation.

A) The deviation rates of both the auditor's sample and the population exceed the tolerable rate of deviation.

B) The deviation rates of both the auditor's sample and the population are less than the tolerable rate of deviation.

C) The deviation rate in the auditor's sample is less than the tolerable rate of deviation, but the deviation rate in the population exceeds the tolerable rate of deviation.

D) The deviation rate in the auditor's sample exceeds the tolerable rate of deviation, but the deviation rate in the population is less than the tolerable rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

28

The ultimate purpose of control risk assessment is to:

A) Estimate the overall risk of failing to detect material misstatements.

B) Decide the nature, timing, and extent of substantive procedures.

C) Determine the risk of incorrect acceptance.

D) Determine the probability that errors entered the accounts.

A) Estimate the overall risk of failing to detect material misstatements.

B) Decide the nature, timing, and extent of substantive procedures.

C) Determine the risk of incorrect acceptance.

D) Determine the probability that errors entered the accounts.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

29

As part of the assessment of control risk,the auditor decided to use audit sampling.After specifying the audit objectives,what would the auditor most likely do next?

A) Determine the sample size.

B) Select the sample.

C) Perform tests of control procedures.

D) Define the deviation conditions.

A) Determine the sample size.

B) Select the sample.

C) Perform tests of control procedures.

D) Define the deviation conditions.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following sampling risks is associated with the use of attributes sampling?

A) Risk of underreliance, yes; risk of incorrect rejection, yes.

B) Risk of underreliance, yes; risk of incorrect rejection, no.

C) Risk of underreliance, no; risk of incorrect rejection, yes.

D) Risk of underreliance, no; risk of incorrect rejection, no.

A) Risk of underreliance, yes; risk of incorrect rejection, yes.

B) Risk of underreliance, yes; risk of incorrect rejection, no.

C) Risk of underreliance, no; risk of incorrect rejection, yes.

D) Risk of underreliance, no; risk of incorrect rejection, no.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

31

The purpose of tests of controls is to determine that:

A) Internal control policies and procedures are functioning as prescribed.

B) Substantive procedures can be kept to a minimum.

C) Errors and irregularities are prevented or detected in a timely manner.

D) The auditor has an understanding of internal control.

A) Internal control policies and procedures are functioning as prescribed.

B) Substantive procedures can be kept to a minimum.

C) Errors and irregularities are prevented or detected in a timely manner.

D) The auditor has an understanding of internal control.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following would not be an example of nonsampling risk in an attributes sampling application?

A) Failure to perform the appropriate type of test of controls procedure.

B) Failure to notice a deviation from prescribed control procedures.

C) Incorrect estimation of the expected population deviation rate.

D) Incorrect accumulation of the number of deviations.

A) Failure to perform the appropriate type of test of controls procedure.

B) Failure to notice a deviation from prescribed control procedures.

C) Incorrect estimation of the expected population deviation rate.

D) Incorrect accumulation of the number of deviations.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

33

An auditor who concludes that a control is functioning properly when,in fact,it is not has committed the

A) Risk of underreliance.

B) Risk of overreliance.

C) Risk of incorrect acceptance.

D) Risk of incorrect rejection.

A) Risk of underreliance.

B) Risk of overreliance.

C) Risk of incorrect acceptance.

D) Risk of incorrect rejection.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

34

An erroneous decision to assess control risk too high can have an adverse effect on

A) The efficiency of an audit engagement.

B) The effectiveness of an audit engagement.

C) The validity of an audit.

D) The type of report the auditor decides to render.

A) The efficiency of an audit engagement.

B) The effectiveness of an audit engagement.

C) The validity of an audit.

D) The type of report the auditor decides to render.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

35

The auditor tested a sample of recorded sales invoices for evidence of credit approval.Based on the results of the sample,the auditor concluded that there was a satisfactory rate of approvals.Unknown to the auditor,credit approvals in the population were not satisfactory.This would be an example of the risk of

A) Overreliance.

B) Underreliance.

C) Incorrect acceptance.

D) Incorrect rejection.

A) Overreliance.

B) Underreliance.

C) Incorrect acceptance.

D) Incorrect rejection.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following components of the audit risk model is most closely associated with attributes sampling?

A) Audit risk.

B) Control risk.

C) Detection risk.

D) Inherent risk.

A) Audit risk.

B) Control risk.

C) Detection risk.

D) Inherent risk.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

37

Why is the auditor more concerned with the risk of overreliance rather than the risk of underreliance?

A) The risk of underreliance is not a type of sampling risk.

B) The risk of overreliance exposes the auditor to an efficiency loss.

C) The risk of overreliance may result in the auditor's failing to perform sufficient substantive procedures.

D) The risk of overreliance cannot be controlled by the auditor during the sampling process.

A) The risk of underreliance is not a type of sampling risk.

B) The risk of overreliance exposes the auditor to an efficiency loss.

C) The risk of overreliance may result in the auditor's failing to perform sufficient substantive procedures.

D) The risk of overreliance cannot be controlled by the auditor during the sampling process.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

38

Samples to test internal control procedures are intended to provide a basis for an auditor to conclude whether

A) The control procedures are operating effectively.

B) The financial statements are materially misstated.

C) The risk of incorrect acceptance is too high.

D) Overall materiality for planning purposes is at a sufficiently low level.

A) The control procedures are operating effectively.

B) The financial statements are materially misstated.

C) The risk of incorrect acceptance is too high.

D) Overall materiality for planning purposes is at a sufficiently low level.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

39

As a result of tests of controls,an auditor assessed control risk too low and decreased the number of substantive procedures performed.This assessment occurred because the true deviation rate in the population was

A) More than the risk of overreliance based on the auditor's sample.

B) More than the deviation rate in the auditor's sample.

C) Less than the risk of overreliance based on the auditor's sample.

D) Less than the deviation rate in the auditor's sample.

A) More than the risk of overreliance based on the auditor's sample.

B) More than the deviation rate in the auditor's sample.

C) Less than the risk of overreliance based on the auditor's sample.

D) Less than the deviation rate in the auditor's sample.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

40

The likelihood of assessing control risk too high is the risk that the sample selected to test controls

A) Does not support the auditor's planned level of control risk when the true operating effectiveness of the control justifies such an assessment.

B) Contains misstatements that could be material to the financial statements when aggregated with misstatements in other account balances or transaction classes.

C) Contains proportionally fewer monetary errors or deviations from prescribed control procedures than exist in the balance or class as a whole.

D) Does not support the tolerable misstatement for some or all of management's assertions.

A) Does not support the auditor's planned level of control risk when the true operating effectiveness of the control justifies such an assessment.

B) Contains misstatements that could be material to the financial statements when aggregated with misstatements in other account balances or transaction classes.

C) Contains proportionally fewer monetary errors or deviations from prescribed control procedures than exist in the balance or class as a whole.

D) Does not support the tolerable misstatement for some or all of management's assertions.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

41

An auditor who tested 50 transactions and found two deviations from an important control activity could conclude that

A) The tolerable rate is 4%.

B) The critical rate of occurrence is 4%.

C) The sample rate of deviation is 4%.

D) The expected population deviation rate is 4%.

A) The tolerable rate is 4%.

B) The critical rate of occurrence is 4%.

C) The sample rate of deviation is 4%.

D) The expected population deviation rate is 4%.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

42

In determining the number of documents to select for a test to obtain assurance that all sales returns have been properly authorized,an auditor should consider the tolerable rate of deviation from the control activity.The auditor should also consider: (1)Likely rate of deviations

(2)Allowable risk of underreliance.

A) (1) only.

B) (2) only.

C) Both (1) and (2).

D) Either (1) or (2).

(2)Allowable risk of underreliance.

A) (1) only.

B) (2) only.

C) Both (1) and (2).

D) Either (1) or (2).

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

43

In order for the auditor to decide to perform tests of controls,which of the following relationships should exist?

A) The sampling risk should be less than 5 percent.

B) The tolerable rate of deviation should exceed the expected population deviation rate.

C) The expected population deviation rate should exceed the risk of overreliance.

D) The expected population deviation rate should exceed the tolerable rate of deviation.

A) The sampling risk should be less than 5 percent.

B) The tolerable rate of deviation should exceed the expected population deviation rate.

C) The expected population deviation rate should exceed the risk of overreliance.

D) The expected population deviation rate should exceed the tolerable rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

44

In performing attributes sampling,the auditor will conclude that the control is functioning as intended if the _____________ is less than or equal to ____________.

A) expected population deviation rate, tolerable rate of deviation.

B) upper limit rate of deviation, tolerable rate of deviation.

C) tolerable rate of deviation, expected population deviation rate.

D) tolerable rate of deviation, upper limit rate of deviation.

A) expected population deviation rate, tolerable rate of deviation.

B) upper limit rate of deviation, tolerable rate of deviation.

C) tolerable rate of deviation, expected population deviation rate.

D) tolerable rate of deviation, upper limit rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following does not have a direct relationship with sample size?

A) Expected population deviation rate.

B) Population size.

C) Risk of overreliance.

D) All of the above have a direct relationship with sample size.

A) Expected population deviation rate.

B) Population size.

C) Risk of overreliance.

D) All of the above have a direct relationship with sample size.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

46

If an auditor calculated an upper limit rate of deviation of 5 percent when the tolerable rate of deviation was 4 percent,the auditor would conclude that

A) The population deviation rate is low enough to rely on internal control as planned.

B) The population deviation rate may be higher than that necessary to rely on internal control as planned.

C) The control risk can be assessed at planned levels.

D) The control risk should be assessed at lower levels.

A) The population deviation rate is low enough to rely on internal control as planned.

B) The population deviation rate may be higher than that necessary to rely on internal control as planned.

C) The control risk can be assessed at planned levels.

D) The control risk should be assessed at lower levels.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

47

An auditor is testing control procedures that are evidenced on an entity's vouchers by matching random numbers with voucher numbers.If a random number matches the number of a voided voucher,that voucher ordinarily should be replaced by another voucher in the random sample if the voucher

A) Constitutes a deviation.

B) Has been properly voided.

C) Cannot be located.

D) Represents an immaterial dollar amount.

A) Constitutes a deviation.

B) Has been properly voided.

C) Cannot be located.

D) Represents an immaterial dollar amount.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

48

Judgments about the frequency of control deviations that identify a particular control risk level are related to

A) Sample rate of deviation.

B) Tolerable rate of deviation.

C) Upper limit rate of deviations.

D) Expected population deviation rate.

A) Sample rate of deviation.

B) Tolerable rate of deviation.

C) Upper limit rate of deviations.

D) Expected population deviation rate.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

49

On the basis of attributes sampling,an auditor decided to increase the assessed level of control risk from the level originally planned.To achieve an overall audit risk level that is substantially the same as the original planned level of audit risk,the auditor would

A) Increase inherent risk.

B) Increase overall materiality levels.

C) Decrease substantive procedures.

D) Decrease detection risk.

A) Increase inherent risk.

B) Increase overall materiality levels.

C) Decrease substantive procedures.

D) Decrease detection risk.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

50

The procedures for statistical evaluation of tests of controls with the AICPA evaluation tables would not include which of the following steps?

A) Identify the population deviation rate.

B) Identify the sample size in the left margin.

C) Identify the number of actual deviations for the sample size.

D) Identify the upper limit rate of deviation given the sample size and number of deviations.

A) Identify the population deviation rate.

B) Identify the sample size in the left margin.

C) Identify the number of actual deviations for the sample size.

D) Identify the upper limit rate of deviation given the sample size and number of deviations.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

51

The sample size for a test of controls varies inversely with

A) Expected population deviation rate, yes; tolerable rate of deviation, yes.

B) Expected population deviation rate, no; tolerable rate of deviation, no.

C) Expected population deviation rate, yes; tolerable rate of deviation, no.

D) Expected population deviation rate, no; tolerable rate of deviation, yes.

A) Expected population deviation rate, yes; tolerable rate of deviation, yes.

B) Expected population deviation rate, no; tolerable rate of deviation, no.

C) Expected population deviation rate, yes; tolerable rate of deviation, no.

D) Expected population deviation rate, no; tolerable rate of deviation, yes.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

52

If the upper limit rate of deviation exceeds the tolerable rate of deviation,the auditor would most likely

A) Accept the account balance as being fairly stated.

B) Reject the account balance as being fairly stated.

C) Increase the planned effectiveness of substantive procedures.

D) Not increase the planned effectiveness of substantive procedures.

A) Accept the account balance as being fairly stated.

B) Reject the account balance as being fairly stated.

C) Increase the planned effectiveness of substantive procedures.

D) Not increase the planned effectiveness of substantive procedures.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following statements is correct concerning statistical sampling in tests of controls?

A) Deviations from control procedures at a given rate usually result in misstatements at a higher rate.

B) As the population size doubles, the sample size should also double.

C) The auditor does not consider qualitative aspects of deviations.

D) There is an inverse relationship between the sample size and the tolerable rate of deviation.

A) Deviations from control procedures at a given rate usually result in misstatements at a higher rate.

B) As the population size doubles, the sample size should also double.

C) The auditor does not consider qualitative aspects of deviations.

D) There is an inverse relationship between the sample size and the tolerable rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

54

In planning a statistical sample for a test of controls,an auditor increased the expected population deviation rate from the rates observed in prior audits because of the results of prior tests of controls and the overall control environment.The auditor most likely would then increase the planned

A) Tolerable rate of deviation.

B) Allowance for sampling risk.

C) Risk of overreliance.

D) Sample size.

A) Tolerable rate of deviation.

B) Allowance for sampling risk.

C) Risk of overreliance.

D) Sample size.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

55

The upper limit rate of deviation in attributes sampling is

A) The actual deviation rate in the population.

B) Always less than the tolerable rate of deviation.

C) Always more than the tolerable rate of deviation.

D) A statistical calculation that considers sampling risk.

A) The actual deviation rate in the population.

B) Always less than the tolerable rate of deviation.

C) Always more than the tolerable rate of deviation.

D) A statistical calculation that considers sampling risk.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

56

After examining sample items and classifying items as deviations,the auditor can divide the number of deviations by the sample size and calculate the

A) Expected population deviation rate.

B) Risk of underreliance.

C) Sample rate of deviation.

D) Tolerable rate of deviation.

A) Expected population deviation rate.

B) Risk of underreliance.

C) Sample rate of deviation.

D) Tolerable rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

57

To statistically evaluate an attributes sampling application,the auditor would not need to know

A) The acceptable risk of overreliance.

B) The actual deviations in the sample.

C) The actual population size.

D) The upper limit rate of deviation.

A) The acceptable risk of overreliance.

B) The actual deviations in the sample.

C) The actual population size.

D) The upper limit rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following is not true with regard to the relationship among control risk,the risk of overreliance,and the tolerable rate of deviation?

A) Lower levels of control risk result in a higher level of the risk of overreliance.

B) Lower levels of the risk of overreliance result in lower tolerable rate of deviations.

C) Lower levels of control risk result in lower tolerable rate of deviations.

D) All of the above are true.

A) Lower levels of control risk result in a higher level of the risk of overreliance.

B) Lower levels of the risk of overreliance result in lower tolerable rate of deviations.

C) Lower levels of control risk result in lower tolerable rate of deviations.

D) All of the above are true.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

59

In the study of internal control,the auditor uses sampling to compare the _____________ to the ____________.

A) error, overall materiality level.

B) sampling risk, precision.

C) deviation rate, tolerable rate of deviation.

D) precision interval, upper limit on misstatement.

A) error, overall materiality level.

B) sampling risk, precision.

C) deviation rate, tolerable rate of deviation.

D) precision interval, upper limit on misstatement.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following is not a judgment or estimate that auditors must make when performing attributes sampling?

A) Tolerable rate of deviation.

B) Expected population deviation rate.

C) Sample rate of deviation.

D) Risk of overreliance.

A) Tolerable rate of deviation.

B) Expected population deviation rate.

C) Sample rate of deviation.

D) Risk of overreliance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following would not result in the audit team's selecting a larger sample of controls for examination?

A) A reduction in the risk of overreliance from 10 percent to 5 percent.

B) An increase in the tolerable rate of deviation from 3 percent to 6 percent.

C) An increase in the expected population deviation rate from 2 percent to 4 percent.

D) All of the above would result in a larger sample of controls.

A) A reduction in the risk of overreliance from 10 percent to 5 percent.

B) An increase in the tolerable rate of deviation from 3 percent to 6 percent.

C) An increase in the expected population deviation rate from 2 percent to 4 percent.

D) All of the above would result in a larger sample of controls.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

62

Lincoln,CPA,selected a sample of 100 items by dividing the population of 100,000 sales invoices by 100.With a random start,she then selected every 1,000th invoice.This selection process is referred to as

A) Unrestricted random selection.

B) Nonstatistical selection.

C) Systematic random selection.

D) Judgmental selection.

A) Unrestricted random selection.

B) Nonstatistical selection.

C) Systematic random selection.

D) Judgmental selection.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

63

As a result of tests of controls,an auditor assessed control risk too low and decreased the effectiveness of her substantive procedures.This assessment occurred because the true deviation rate in the population was

A) Less than the risk of overreliance based on the auditor's sample.

B) Less than the deviation rate in the auditor's sample.

C) More than the risk of overreliance based on the auditor's sample.

D) More than the deviation rate in the auditor's sample.

A) Less than the risk of overreliance based on the auditor's sample.

B) Less than the deviation rate in the auditor's sample.

C) More than the risk of overreliance based on the auditor's sample.

D) More than the deviation rate in the auditor's sample.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

64

An auditor wanted to test credit approval on 10,000 sales invoices processed during the year.The auditor designed a statistical sample that would provide a 1% risk of overreliance (99% confidence)that not more than 7% of the sales invoices lacked approval.The auditor estimated from previous experience that about 2½% of the sales invoices lacked approval.A sample of 200 invoices was examined,and 7 of them were lacking approval.The auditor then determined the upper limit rate of deviation to be 8%. The allowance for sampling risk was

A) 5½%.

B) 4½%.

C) 3½%.

D) 1%.

A) 5½%.

B) 4½%.

C) 3½%.

D) 1%.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

65

An auditor is examining an important internal control in his audit of ABC Company.Because the account balance affected by this control is highly susceptible to fraud,he will reject the sample if even one deviation is discovered.What type of sampling plan should he use?

A) Attributes sampling.

B) Discovery sampling.

C) Sequential sampling.

D) Statistical sampling.

A) Attributes sampling.

B) Discovery sampling.

C) Sequential sampling.

D) Statistical sampling.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

66

An auditor who uses statistical sampling for attributes in testing internal controls should reduce the planned reliance on a prescribed control when the

A) Sample rate of deviation plus the allowance for sampling risk equals the tolerable rate of deviation.

B) Sample rate of deviation is less than the expected rate of deviation used in planning the sample.

C) Tolerable rate less the allowance for sampling risk exceeds the sample rate of deviation.

D) Sample rate of deviation plus the allowance for sampling risk exceeds the tolerable rate of deviation.

A) Sample rate of deviation plus the allowance for sampling risk equals the tolerable rate of deviation.

B) Sample rate of deviation is less than the expected rate of deviation used in planning the sample.

C) Tolerable rate less the allowance for sampling risk exceeds the sample rate of deviation.

D) Sample rate of deviation plus the allowance for sampling risk exceeds the tolerable rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following sampling risks does the audit team control in an attributes sampling application (ROO = risk of overreliance,ROU = risk of underreliance)?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following steps in attributes sampling is most closely related to identifying key controls corresponding to the relevant management assertions?

A) Determine the objective of sampling.

B) Define the deviation condition.

C) Define the population.

D) Determine the sample size.

A) Determine the objective of sampling.

B) Define the deviation condition.

C) Define the population.

D) Determine the sample size.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

69

A sampling plan for nonstatistical sampling is the same as statistical sampling except for which of the following steps?

A) Define the characteristic of interest.

B) Define the population.

C) Measure the sample items.

D) Evaluate the sample results.

A) Define the characteristic of interest.

B) Define the population.

C) Measure the sample items.

D) Evaluate the sample results.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

70

In discovery sampling,the desired probability of one occurrence is defined as

A) 1 minus the risk of underreliance.

B) 1 minus the risk of overreliance.

C) The critical rate of occurrence.

D) The population deviation rate.

A) 1 minus the risk of underreliance.

B) 1 minus the risk of overreliance.

C) The critical rate of occurrence.

D) The population deviation rate.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following factors has a direct relationship with sample size in an attributes sampling application?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is not true about using nonstatistical sampling?

A) It generally results in a smaller sample size.

B) It is allowed by auditing standards.

C) It is simple to use.

D) All of the above are true.

A) It generally results in a smaller sample size.

B) It is allowed by auditing standards.

C) It is simple to use.

D) All of the above are true.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

73

Why is the audit team more concerned with controlling the exposure to the risk of overreliance than with the risk of underreliance?

A) Only the risk of overreliance results in an incorrect audit decision.

B) The risk of underreliance is not related to the audit team's study and evaluation of internal control.

C) The risk of overreliance can ultimately result in the audit team's failing to reduce audit risk to acceptable levels.

D) The risk of underreliance can be controlled by performing tests of controls during the interim period.

A) Only the risk of overreliance results in an incorrect audit decision.

B) The risk of underreliance is not related to the audit team's study and evaluation of internal control.

C) The risk of overreliance can ultimately result in the audit team's failing to reduce audit risk to acceptable levels.

D) The risk of underreliance can be controlled by performing tests of controls during the interim period.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following major stages of the audit is most closely related to attributes sampling?

A) Determining preliminary levels of materiality.

B) Performing tests of controls.

C) Performing substantive procedures.

D) Searching for the possible occurrence of subsequent events.

A) Determining preliminary levels of materiality.

B) Performing tests of controls.

C) Performing substantive procedures.

D) Searching for the possible occurrence of subsequent events.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

75

A sampling plan in which an initial sample is selected and the audit team draws a final conclusion or selects additional items before drawing a final conclusion is called

A) Attributes sampling.

B) Discovery sampling.

C) Sequential sampling.

D) Statistical sampling.

A) Attributes sampling.

B) Discovery sampling.

C) Sequential sampling.

D) Statistical sampling.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

76

An auditor who increases the assessed level of control risk because certain control procedures were determined to be ineffective would most likely increase the

A) Extent of tests of controls.

B) Level of detection risk.

C) Extent of substantive procedures.

D) Level of inherent risk.

A) Extent of tests of controls.

B) Level of detection risk.

C) Extent of substantive procedures.

D) Level of inherent risk.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

77

An auditor wanted to test credit approval on 10,000 sales invoices processed during the year.The auditor designed a statistical sample that would provide a 1% risk of overreliance (99% confidence)that not more than 7% of the sales invoices lacked approval.The auditor estimated from previous experience that about 2½% of the sales invoices lacked approval.A sample of 200 invoices was examined,and 7 of them were lacking approval.The auditor then determined the upper limit rate of deviation to be 8%. In the evaluation of this sample,the auditor decided to increase the level of the preliminary assessment of control risk because the

A) Tolerable rate of deviation (7%) was less than the upper limit rate of deviation (8%).

B) Expected population deviation rate (7%) was more than the percentage of errors in the sample (3½%).

C) Expected population deviation rate (2½%) was less than the tolerable rate of deviation.

D) Upper limit rate of deviation (8%) was more than the percentage of errors in the sample (3½%).

A) Tolerable rate of deviation (7%) was less than the upper limit rate of deviation (8%).

B) Expected population deviation rate (7%) was more than the percentage of errors in the sample (3½%).

C) Expected population deviation rate (2½%) was less than the tolerable rate of deviation.

D) Upper limit rate of deviation (8%) was more than the percentage of errors in the sample (3½%).

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

78

An auditor wants to perform a test of controls for a sensitive control.If she discovers even one deviation,she will reject the control as unacceptable.She is especially concerned about finding a deviation rate of more than 1 percent.Using discovery sampling and the sample evaluation table for 5 percent risk of overreliance,what sample size should she use?

A) 20.

B) 150.

C) 300.

D) 500.

A) 20.

B) 150.

C) 300.

D) 500.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

79

What is an auditor's evaluation of a statistical sample for attributes when a test of 100 documents results in four deviations if the tolerable rate of deviation is 5%,the expected population deviation rate is 3%,and the allowance for sampling risk is 2%?

A) Accept the sample results as support for planned reliance on the control because the tolerable rate of deviation less then allowance for sampling risk equals the expected population deviation rate.

B) Modify planned reliance on the control because the sample rate of deviation plus the allowance for sampling risk exceeds the tolerable rate of deviation.

C) Modify planned reliance on the control because the tolerable rate of deviation plus the allowance for sampling risk exceeds the expected population deviation rate.

D) Accept the sample results as support for planned reliance on the control because the sample rate of deviation plus the allowance for sampling risk exceeds the tolerable rate of deviation.

A) Accept the sample results as support for planned reliance on the control because the tolerable rate of deviation less then allowance for sampling risk equals the expected population deviation rate.

B) Modify planned reliance on the control because the sample rate of deviation plus the allowance for sampling risk exceeds the tolerable rate of deviation.

C) Modify planned reliance on the control because the tolerable rate of deviation plus the allowance for sampling risk exceeds the expected population deviation rate.

D) Accept the sample results as support for planned reliance on the control because the sample rate of deviation plus the allowance for sampling risk exceeds the tolerable rate of deviation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

80

Mary Todd is auditing White House furniture.In selecting a sample of purchases,she finds that a purchase order is missing.She should

A) Select another purchase to test.

B) Have the client recreate the purchase order.

C) Consider the sample item a deviation.

D) Ask the client whether the purchase was authorized.

A) Select another purchase to test.

B) Have the client recreate the purchase order.

C) Consider the sample item a deviation.

D) Ask the client whether the purchase was authorized.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 137 flashcards in this deck.