Deck 12: Reports on Audited Financial Statements

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

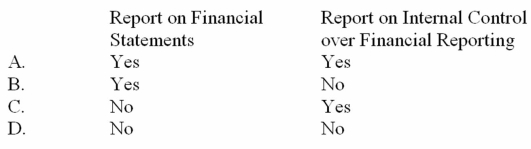

If the auditors decide to present separate reports on the entity's financial statements and internal control over financial reporting,which of the following reports should be modified to refer to the other report?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Question

Question

Question

Question

Question

Question

Question

Question

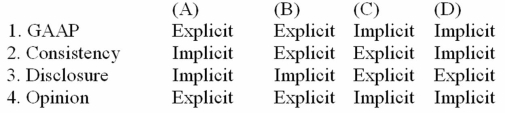

When reporting under GAAS,certain statements are required in all auditors' reports ("explicit")and others are required only under certain conditions ("implicit").Which combination that follows correctly describes the auditors' responsibilities for reporting?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/114

Play

Full screen (f)

Deck 12: Reports on Audited Financial Statements

1

If predecessor auditors had examined comparative financial statements,those auditors' reports must be presented along with the auditors' report.

False

2

The auditors' report should be dated as of the date of the client's financial statements.

False

3

The introductory paragraph of the auditors' report identifies management's responsibility for the financial statements.

True

4

When a division of responsibility is noted in the auditors' report on group financial statements,the introductory paragraph would be modified.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

5

Auditors are not responsible for determining whether there is a substantial doubt about an entity's ability to continue as a going concern.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

6

An adverse opinion indicates that the financial statements are not presented in conformity with GAAP.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

7

When there is a material departure from GAAP,auditors may issue either an adverse opinion or disclaimer of opinion on the entity's financial statements.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

8

Auditors would be more likely to issue a disclaimer of opinion when a scope limitation is client imposed as opposed to circumstance imposed.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

9

If separate reports on the entity's financial statements and internal control over financial reporting are presented,the auditors' report on the financial statements should reference the report on internal control over financial reporting.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

10

The scope paragraph of the auditors' report contains a general description of the audit work and reference to standards of the Public Company Accounting Oversight Board.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

11

If group auditors choose to rely on the work of component auditors,the group auditors must refer to the component auditors in their report by name.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

12

The auditors' report references the consistent application of accounting principles only when the entity has changed accounting principles.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

13

Rule 203 allows auditors to issue an unqualified opinion on the entity's financial statements even when these financial statements contain a departure from an FASB standard.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

14

If auditors cannot apply specific auditing procedures during the examination,the opinion paragraph in the report must be qualified.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

15

The first paragraph of the standard report on the entity's financial statements is referred to as the scope paragraph.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

16

The introductory paragraph of the auditors' report indicates that an audit has been conducted and identifies the financial statements the auditors examined.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

17

In all cases in which auditors are associated by name or participation with unaudited financial statements of public entities,the auditors must issue a disclaimer of opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

18

When the financial statements contain a departure from GAAP,the auditors must render an adverse opinion on the entity's financial statements.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

19

If a justified departure from GAAP exists,auditors would issue an unqualified opinion but would modify the scope paragraph to describe the departure and its monetary effects.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

20

If the audit scope is restricted in some specific respect,but sufficient appropriate evidence is gathered by performing other procedures,the standard scope paragraph of the report need not be modified.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

21

When auditors qualify their opinion on the entity's financial statements because of inadequate disclosure,the auditors should describe the nature of the omission in an additional paragraph and modify the

A) Introductory and scope paragraphs.

B) Introductory paragraph only.

C) Scope paragraph only.

D) Neither the introductory or scope paragraph.

A) Introductory and scope paragraphs.

B) Introductory paragraph only.

C) Scope paragraph only.

D) Neither the introductory or scope paragraph.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements is not included in the scope paragraph of the standard report on the entity's financial statements?

A) "Our responsibility is to express an opinion on those financial statements.…"

B) "Those standards require that we plan and perform the audit...."

C) "We believe that our audit provides a reasonable basis for our opinion."

D) "An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements."

A) "Our responsibility is to express an opinion on those financial statements.…"

B) "Those standards require that we plan and perform the audit...."

C) "We believe that our audit provides a reasonable basis for our opinion."

D) "An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements."

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

23

If financial statements contain a material but nonpervasive departure from generally accepted accounting principles,the auditors should render a(n)

A) Qualified opinion with reference to departure.

B) Adverse opinion with scope limitation reference.

C) Adverse opinion with reference to departure.

D) Disclaimer of opinion.

A) Qualified opinion with reference to departure.

B) Adverse opinion with scope limitation reference.

C) Adverse opinion with reference to departure.

D) Disclaimer of opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

24

Auditors should disclose the substantive reasons for expressing an adverse opinion on the entity's financial statements in an additional paragraph

A) Preceding the scope paragraph.

B) Preceding the opinion paragraph.

C) Following the opinion paragraph.

D) In the footnotes to the financial statements.

A) Preceding the scope paragraph.

B) Preceding the opinion paragraph.

C) Following the opinion paragraph.

D) In the footnotes to the financial statements.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

25

Auditors are required to reference consistency in their report when there are changes in

A) Accounting estimates.

B) The format of the statement of cash flows.

C) The classification of financial statement amounts.

D) Accounting principles.

A) Accounting estimates.

B) The format of the statement of cash flows.

C) The classification of financial statement amounts.

D) Accounting principles.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

26

When auditors are engaged to examine an entity's financial statements but decide to issue a disclaimer of opinion,the report would not

A) Identify management's responsibility for the financial statements.

B) Refer to any scope limitation in an additional paragraph.

C) Modify the scope paragraph to identify the basis for the disclaimer.

D) Indicate that the auditors were engaged to audit the financial statements.

A) Identify management's responsibility for the financial statements.

B) Refer to any scope limitation in an additional paragraph.

C) Modify the scope paragraph to identify the basis for the disclaimer.

D) Indicate that the auditors were engaged to audit the financial statements.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

27

In which of the following circumstances would a qualified opinion not be appropriate?

A) A scope limitation prevents the auditors from completing an important auditing procedure.

B) The entity has failed to properly disclose going-concern uncertainties.

C) An accounting principle at variance with generally accepted accounting principles is used.

D) The auditors lack independence with respect to the audited entity.

A) A scope limitation prevents the auditors from completing an important auditing procedure.

B) The entity has failed to properly disclose going-concern uncertainties.

C) An accounting principle at variance with generally accepted accounting principles is used.

D) The auditors lack independence with respect to the audited entity.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

28

The auditors' report on the entity's financial statements included an additional paragraph disclosing a difference of opinion between the auditors and the entity for which the auditors believed an adjustment to the financial statements should be made.The opinion paragraph of the auditors' report should express a(n)

A) Unqualified opinion.

B) Qualified opinion citing a departure from generally accepted accounting principles.

C) Qualified opinion citing a scope limitation and lack of specific evidence.

D) Disclaimer of opinion.

A) Unqualified opinion.

B) Qualified opinion citing a departure from generally accepted accounting principles.

C) Qualified opinion citing a scope limitation and lack of specific evidence.

D) Disclaimer of opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

29

Auditors will issue an adverse opinion when

A) A severe scope limitation has been imposed by the entity.

B) A violation of generally accepted accounting principles is sufficiently material and pervasive that a qualified opinion is not justified.

C) A qualified opinion cannot be rendered because the auditors lack independence.

D) The entity's ability to continue as a going concern is subject to substantial doubt.

A) A severe scope limitation has been imposed by the entity.

B) A violation of generally accepted accounting principles is sufficiently material and pervasive that a qualified opinion is not justified.

C) A qualified opinion cannot be rendered because the auditors lack independence.

D) The entity's ability to continue as a going concern is subject to substantial doubt.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

30

The issuance of a disclaimer of opinion generally indicates

A) The auditors cannot form an opinion on the fairness of presentation of the financial statements as a whole.

B) The auditors have some uncertainties, but these uncertainties are not so material that they cannot form an opinion on the fairness of presentation of the financial statements as a whole.

C) The auditors have observed a departure from generally accepted accounting principles but the departure is not of sufficient materiality to justify a qualified opinion.

D) The auditors have observed a departure from generally accepted accounting principles that is so material and pervasive that a qualified opinion is not justified.

A) The auditors cannot form an opinion on the fairness of presentation of the financial statements as a whole.

B) The auditors have some uncertainties, but these uncertainties are not so material that they cannot form an opinion on the fairness of presentation of the financial statements as a whole.

C) The auditors have observed a departure from generally accepted accounting principles but the departure is not of sufficient materiality to justify a qualified opinion.

D) The auditors have observed a departure from generally accepted accounting principles that is so material and pervasive that a qualified opinion is not justified.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

31

A report that acknowledges reliance on the reports of component auditors is a type of report modification known as a(n)

A) Qualification.

B) Division of responsibility.

C) Expansion of scope.

D) Scope limitation.

A) Qualification.

B) Division of responsibility.

C) Expansion of scope.

D) Scope limitation.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

32

When auditors lack independence,which of the following is true about the report on the entity's financial statements that should be issued?

A) The auditors should disclaim an opinion and should state specifically that they are not independent.

B) The auditors should disclaim an opinion but not mention that they are not independent.

C) The auditors should issue an unqualified opinion with an explanatory paragraph stating that they are not independent.

D) The auditors should issue a qualified opinion with an explanatory paragraph stating that they are not independent.

A) The auditors should disclaim an opinion and should state specifically that they are not independent.

B) The auditors should disclaim an opinion but not mention that they are not independent.

C) The auditors should issue an unqualified opinion with an explanatory paragraph stating that they are not independent.

D) The auditors should issue a qualified opinion with an explanatory paragraph stating that they are not independent.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

33

Restrictions imposed by an entity prohibited the auditors' observation of physical inventories,which accounted for 35% of total assets.Alternative auditing procedures were not feasible,although the auditors were able to examine satisfactory evidence for all other items in the financial statements.The auditors would most likely express

A) A qualified opinion on the entity's financial statements, referring to a departure from generally accepted accounting principles.

B) A disclaimer of opinion on the entity's financial statements.

C) An unqualified opinion on the entity's financial statements with a separate explanatory paragraph.

D) An unqualified opinion on the entity's financial statements with a modification of the scope paragraph.

A) A qualified opinion on the entity's financial statements, referring to a departure from generally accepted accounting principles.

B) A disclaimer of opinion on the entity's financial statements.

C) An unqualified opinion on the entity's financial statements with a separate explanatory paragraph.

D) An unqualified opinion on the entity's financial statements with a modification of the scope paragraph.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following scope limitations would ordinarily be of most concern to the auditors?

A) The inability to observe inventories because the auditors were appointed following the date of the financial statements.

B) Management's refusal to provide written representations to the auditors.

C) The inability to obtain confirmation of year-end balances from customers because of different billing dates.

D) The use of the work of component auditors in the audit of group financial statements.

A) The inability to observe inventories because the auditors were appointed following the date of the financial statements.

B) Management's refusal to provide written representations to the auditors.

C) The inability to obtain confirmation of year-end balances from customers because of different billing dates.

D) The use of the work of component auditors in the audit of group financial statements.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

35

The auditors conclude that there is a material inconsistency in the "other information" in an annual report to shareholders containing audited financial statements.If the auditors conclude that the financial statements do not require revision but the entity refuses to revise or eliminate the material inconsistency,the auditors may

A) Issue a qualified opinion on the entity's financial statements, citing a departure from generally accepted accounting principles.

B) Consider the matter closed because the other information is not included in the audited financial statements.

C) Issue an adverse opinion on the entity's financial statements due to inadequate disclosure.

D) Revise the report on the entity's financial statements to include a separate explanatory paragraph describing the material inconsistency.

A) Issue a qualified opinion on the entity's financial statements, citing a departure from generally accepted accounting principles.

B) Consider the matter closed because the other information is not included in the audited financial statements.

C) Issue an adverse opinion on the entity's financial statements due to inadequate disclosure.

D) Revise the report on the entity's financial statements to include a separate explanatory paragraph describing the material inconsistency.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

36

When an entity will not permit inquiry of outside legal counsel,the auditors' report on the entity's financial statements will ordinarily contain a(n)

A) Disclaimer of opinion.

B) Qualified opinion referencing a departure from generally accepted accounting principles.

C) Unqualified opinion with a separate explanatory paragraph.

D) Adverse opinion.

A) Disclaimer of opinion.

B) Qualified opinion referencing a departure from generally accepted accounting principles.

C) Unqualified opinion with a separate explanatory paragraph.

D) Adverse opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following situations would not result in auditors adding an additional paragraph to their report without modifying the introductory,scope,or opinion paragraphs of that report?

A) Reference to a change in the method of accounting mandated by the issuance of a new accounting standard.

B) Reference to a going-concern uncertainty facing the client.

C) Reference to a departure from GAAP that is material but not pervasive to the financial statements.

D) Reference to an acquisition made by the client during the most recent fiscal year.

A) Reference to a change in the method of accounting mandated by the issuance of a new accounting standard.

B) Reference to a going-concern uncertainty facing the client.

C) Reference to a departure from GAAP that is material but not pervasive to the financial statements.

D) Reference to an acquisition made by the client during the most recent fiscal year.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

38

The scope paragraph of the standard report on the entity's financial statements does not include the statement

A) "In conformity with accounting principles generally accepted in the United States of America…."

B) "We believe that our audits provide a reasonable basis for an opinion."

C) "An audit also includes assessing the accounting principles used and significant estimates made by management...."

D) "Those standards require that we plan and perform the audit to obtain reasonable assurance...."

A) "In conformity with accounting principles generally accepted in the United States of America…."

B) "We believe that our audits provide a reasonable basis for an opinion."

C) "An audit also includes assessing the accounting principles used and significant estimates made by management...."

D) "Those standards require that we plan and perform the audit to obtain reasonable assurance...."

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

39

"As described in Note 5 to the financial statements,General Express changed its statistical method of computing product warranty expense for the year ended December 31,2012" is an illustration of a

A) Consistency change requiring a qualified opinion.

B) Scope limitation.

C) Departure from generally accepted accounting principles

D) Report with a consistency modification.

A) Consistency change requiring a qualified opinion.

B) Scope limitation.

C) Departure from generally accepted accounting principles

D) Report with a consistency modification.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

40

In which of the following circumstances may auditors issue a standard report on the entity's financial statements?

A) The entity changed accounting principles having an immaterial effect on the entity's financial position, results of operations, and cash flows.

B) The auditors wish to emphasize a matter regarding the financial statements.

C) The financial statements are affected by a departure from a generally accepted accounting principle explained and justified by Rule 203 of the AICPA Code of Professional Conduct.

D) The auditors have not been able to audit a substantial portion of the balance sheet because of a circumstance-imposed scope limitation.

A) The entity changed accounting principles having an immaterial effect on the entity's financial position, results of operations, and cash flows.

B) The auditors wish to emphasize a matter regarding the financial statements.

C) The financial statements are affected by a departure from a generally accepted accounting principle explained and justified by Rule 203 of the AICPA Code of Professional Conduct.

D) The auditors have not been able to audit a substantial portion of the balance sheet because of a circumstance-imposed scope limitation.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

41

When audited financial statements are presented in a document containing other information,the auditors should

A) Perform inquiry and analytical procedures to ascertain whether the other information is reasonable.

B) Add an explanatory paragraph to the auditors' report without modifying the opinion on the financial statements.

C) Perform the appropriate substantive procedures to corroborate the other information.

D) Read the other information to determine that it is consistent with the audited financial statements.

A) Perform inquiry and analytical procedures to ascertain whether the other information is reasonable.

B) Add an explanatory paragraph to the auditors' report without modifying the opinion on the financial statements.

C) Perform the appropriate substantive procedures to corroborate the other information.

D) Read the other information to determine that it is consistent with the audited financial statements.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

42

Charlie Company's comparative financial statements include the financial statements of the prior year that were audited by predecessor auditors whose report on those financial statements is not presented.If the predecessor's report was qualified,the successor auditors should

A) Indicate in their report the substantive reasons for the qualification issued by the predecessor auditors.

B) Request the entity to reissue the predecessor's report on the prior-year statements.

C) Issue an updated comparative report on the entity's financial statements, indicating the division of responsibility.

D) Express an opinion only on the current-year financial statements and make no reference to the prior-year financial statements or opinion.

A) Indicate in their report the substantive reasons for the qualification issued by the predecessor auditors.

B) Request the entity to reissue the predecessor's report on the prior-year statements.

C) Issue an updated comparative report on the entity's financial statements, indicating the division of responsibility.

D) Express an opinion only on the current-year financial statements and make no reference to the prior-year financial statements or opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

43

In which of the following situations would auditors ordinarily choose between expressing a qualified opinion or an adverse opinion on the entity's financial statements?

A) The auditors did not observe the entity's physical inventory and are unable to become satisfied as to its balance by other auditing procedures.

B) The financial statements fail to disclose information that is required by generally accepted accounting principles.

C) The auditors are asked to report only on the entity's balance sheet but not on the other basic financial statements.

D) Events disclosed in the financial statements cause the auditors to have substantial doubt about the entity's ability to continue as a going concern.

A) The auditors did not observe the entity's physical inventory and are unable to become satisfied as to its balance by other auditing procedures.

B) The financial statements fail to disclose information that is required by generally accepted accounting principles.

C) The auditors are asked to report only on the entity's balance sheet but not on the other basic financial statements.

D) Events disclosed in the financial statements cause the auditors to have substantial doubt about the entity's ability to continue as a going concern.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following is an example of a material accounting change that requires recognition in an unqualified opinion on the entity's financial statements?

A) A change in the estimate of useful lives used to depreciate property, plant and equipment.

B) A change in the entity's form of reporting entity.

C) Management has changed from one generally accepted accounting principle to another but has not provided reasonable justification.

D) A change from an accounting principle that conforms with GAAP to one that does not.

A) A change in the estimate of useful lives used to depreciate property, plant and equipment.

B) A change in the entity's form of reporting entity.

C) Management has changed from one generally accepted accounting principle to another but has not provided reasonable justification.

D) A change from an accounting principle that conforms with GAAP to one that does not.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

45

In which of the following circumstances would auditors be most likely to express an adverse opinion?

A) The chief executive officer refuses to provide the auditors access to minutes of the board of directors' meetings.

B) Tests of controls show that the entity's internal control is so ineffective that it cannot be relied upon.

C) The financial statements are not in conformity with generally accepted accounting principles regarding the capitalization of leases.

D) Information comes to the auditors' attention that raises substantial doubt about the entity's ability to continue as a going concern.

A) The chief executive officer refuses to provide the auditors access to minutes of the board of directors' meetings.

B) Tests of controls show that the entity's internal control is so ineffective that it cannot be relied upon.

C) The financial statements are not in conformity with generally accepted accounting principles regarding the capitalization of leases.

D) Information comes to the auditors' attention that raises substantial doubt about the entity's ability to continue as a going concern.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

46

If management fails to provide adequate justification for a change from one generally accepted accounting principle to another,the auditors should

A) Add an additional paragraph and express a qualified or an adverse opinion on the entity's financial statements for lack of conformity with generally accepted accounting principles.

B) Disclaim an opinion on the entity's financial statements because of uncertainty.

C) Disclose the matter in a separate explanatory paragraph but not modify the opinion paragraph on the entity's financial statements.

D) Neither modify the opinion on the entity's financial statements nor disclose the matter because both principles are generally accepted accounting principles.

A) Add an additional paragraph and express a qualified or an adverse opinion on the entity's financial statements for lack of conformity with generally accepted accounting principles.

B) Disclaim an opinion on the entity's financial statements because of uncertainty.

C) Disclose the matter in a separate explanatory paragraph but not modify the opinion paragraph on the entity's financial statements.

D) Neither modify the opinion on the entity's financial statements nor disclose the matter because both principles are generally accepted accounting principles.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

47

When there has been a change in accounting principles but its effect on the comparability of the financial statements is not material,the auditors should

A) Refer to the change in an explanatory paragraph.

B) Explicitly concur that the change is preferred.

C) Not refer to consistency in the report.

D) Refer to the change in the opinion paragraph.

A) Refer to the change in an explanatory paragraph.

B) Explicitly concur that the change is preferred.

C) Not refer to consistency in the report.

D) Refer to the change in the opinion paragraph.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

48

In which of the following circumstances would auditors most likely add an explanatory paragraph to the standard report without affecting the unqualified opinion on the entity's financial statements?

A) The auditors are asked to report on the balance sheet but not on the other basic financial statements.

B) There is substantial doubt about the entity's ability to continue as a going concern.

C) Management's estimates of the effects of future events on the entity's financial condition, results of operations, and cash flows are unreasonable.

D) Certain transactions cannot be tested because of management's records retention policy.

A) The auditors are asked to report on the balance sheet but not on the other basic financial statements.

B) There is substantial doubt about the entity's ability to continue as a going concern.

C) Management's estimates of the effects of future events on the entity's financial condition, results of operations, and cash flows are unreasonable.

D) Certain transactions cannot be tested because of management's records retention policy.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

49

Reference in a group auditors' report to the fact that part of the audit of group financial statements was performed by component auditors most likely would be an indication of

A) Division of responsibility between the auditors who conducted the audits of the components of the group financial statements.

B) The portion of the group statements audited by the component auditors not being considered material.

C) Group auditors' recognition of the component auditors' competence, reputation, and professional certification.

D) Different opinions the auditors are expressing on the components of the financial statements that each audited.

A) Division of responsibility between the auditors who conducted the audits of the components of the group financial statements.

B) The portion of the group statements audited by the component auditors not being considered material.

C) Group auditors' recognition of the component auditors' competence, reputation, and professional certification.

D) Different opinions the auditors are expressing on the components of the financial statements that each audited.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

50

The auditors include a separate paragraph in an otherwise unmodified report on the entity's financial statements to emphasize that the entity being reported on had significant transactions with related parties.The inclusion of this separate paragraph

A) Is considered a qualification of the opinion.

B) Violates generally accepted auditing standards if this information is already disclosed in footnotes to the financial statements.

C) Necessitates a revision of the opinion paragraph to include the phrase "with the foregoing explanation."

D) Is appropriate and would not otherwise affect the unqualified opinion.

A) Is considered a qualification of the opinion.

B) Violates generally accepted auditing standards if this information is already disclosed in footnotes to the financial statements.

C) Necessitates a revision of the opinion paragraph to include the phrase "with the foregoing explanation."

D) Is appropriate and would not otherwise affect the unqualified opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

51

Auditors most likely would issue a disclaimer of opinion on the entity's financial statements because of

A) Inadequate disclosure of material information.

B) The omission of the statement of cash flows.

C) A material departure from generally accepted accounting principles.

D) Management's refusal to furnish written representations.

A) Inadequate disclosure of material information.

B) The omission of the statement of cash flows.

C) A material departure from generally accepted accounting principles.

D) Management's refusal to furnish written representations.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

52

The auditors conclude that an entity's illegal act,which has a material effect on the financial statements,has not been properly accounted for or disclosed.Depending on the overall materiality and pervasiveness of the effect of this illegal act on the financial statements,the auditors should express either a(n)

A) Adverse opinion or a disclaimer of opinion.

B) Qualified opinion or adverse opinion.

C) Disclaimer of opinion or an unqualified opinion with a separate explanatory paragraph.

D) Unqualified opinion with a separate explanatory paragraph or a qualified opinion.

A) Adverse opinion or a disclaimer of opinion.

B) Qualified opinion or adverse opinion.

C) Disclaimer of opinion or an unqualified opinion with a separate explanatory paragraph.

D) Unqualified opinion with a separate explanatory paragraph or a qualified opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

53

Independent auditors must consider whether the entity has the ability to continue as a going concern.If a substantial doubt exists but disclosure is adequate and no other basis exists for modifying the report,the auditors would normally

A) Disclaim an opinion.

B) Express an adverse opinion.

C) Qualify the opinion.

D) Express an unqualified opinion with an additional paragraph describing the going-concern uncertainty.

A) Disclaim an opinion.

B) Express an adverse opinion.

C) Qualify the opinion.

D) Express an unqualified opinion with an additional paragraph describing the going-concern uncertainty.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

54

Under which of the following circumstances would a disclaimer of opinion on the entity's financial statements not be appropriate?

A) The financial statements fail to contain adequate disclosure of related-party transactions.

B) The entity refuses to permit its attorney to furnish information requested in an attorney letter.

C) The auditors are engaged after the date of the financial statements and are unable to observe physical inventories or apply alternative procedures to verify their balances.

D) The auditors are unable to determine the amounts associated with illegal acts committed by the entity's management.

A) The financial statements fail to contain adequate disclosure of related-party transactions.

B) The entity refuses to permit its attorney to furnish information requested in an attorney letter.

C) The auditors are engaged after the date of the financial statements and are unable to observe physical inventories or apply alternative procedures to verify their balances.

D) The auditors are unable to determine the amounts associated with illegal acts committed by the entity's management.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

55

When disclaiming an opinion due to a client-imposed scope limitation,auditors should indicate in a separate paragraph why the audit did not comply with the standards of the PCAOB.The auditors should also omit

A) The opinion paragraph.

B) The scope and opinion paragraph.

C) Neither the scope or opinion paragraph

D) The scope paragraph.

A) The opinion paragraph.

B) The scope and opinion paragraph.

C) Neither the scope or opinion paragraph

D) The scope paragraph.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

56

C.Green,CPA,was engaged to audit the financial statements of Essex Co.after its fiscal year had ended.The timing of Green's appointment and the start of fieldwork made confirming accounts receivable by direct communication with the customers not feasible.However,Green applied other procedures and was satisfied as to the reasonableness of the account balances.Green's auditors' report most likely contained a(n)

A) Unqualified opinion.

B) Unqualified opinion with an explanatory paragraph.

C) Qualified opinion due to a scope limitation.

D) Qualified opinion due to a departure from generally accepted auditing standards.

A) Unqualified opinion.

B) Unqualified opinion with an explanatory paragraph.

C) Qualified opinion due to a scope limitation.

D) Qualified opinion due to a departure from generally accepted auditing standards.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following phrases would auditors most likely include in their report when expressing a qualified opinion on the entity's financial statements because of inadequate disclosure?

A) "Subject to the departure from generally accepted accounting principles, as described above."

B) "With the foregoing explanation of these omitted disclosures."

C) "Except for the omission of the information discussed in the preceding paragraph."

D) "Does not present fairly in all material respects."

A) "Subject to the departure from generally accepted accounting principles, as described above."

B) "With the foregoing explanation of these omitted disclosures."

C) "Except for the omission of the information discussed in the preceding paragraph."

D) "Does not present fairly in all material respects."

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

58

Auditors who are reporting on financial statements that contain a material departure from generally accepted accounting principles should include an additional paragraph and

A) Express a qualified or adverse opinion.

B) Not modify the opinion paragraph as long as the departure is adequately disclosed in a footnote.

C) Disclaim an opinion on the financial statements.

D) Express a qualified opinion or disclaimer of opinion.

A) Express a qualified or adverse opinion.

B) Not modify the opinion paragraph as long as the departure is adequately disclosed in a footnote.

C) Disclaim an opinion on the financial statements.

D) Express a qualified opinion or disclaimer of opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

59

Auditors would not normally issue a qualified opinion on the entity's financial statements when

A) An accounting principle at variance with generally accepted accounting principles is used.

B) The auditors lack independence with respect to the audited entity.

C) A scope limitation prevents the auditors from completing an important auditing procedure.

D) The entity has undertaken a change in accounting principle with which the auditor does not agree.

A) An accounting principle at variance with generally accepted accounting principles is used.

B) The auditors lack independence with respect to the audited entity.

C) A scope limitation prevents the auditors from completing an important auditing procedure.

D) The entity has undertaken a change in accounting principle with which the auditor does not agree.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

60

When financial statements contain a departure from GAAP because of unusual circumstances and the statements would otherwise be misleading,the auditors should explain the unusual circumstances in a separate paragraph and express an opinion that is

A) Unqualified.

B) Qualified.

C) Adverse.

D) Qualified or adverse, depending on the overall materiality and pervasiveness of the GAAP departure.

A) Unqualified.

B) Qualified.

C) Adverse.

D) Qualified or adverse, depending on the overall materiality and pervasiveness of the GAAP departure.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

61

R.Wolfe became the new auditor for Royal Corporation,succeeding

A) Only if Mason's opinion last year was qualified.

B) Describing the prior audit and the opinion but not naming Mason as the predecessor auditor.

C) Describing the audit but not revealing the type of opinion Mason gave.

C) Mason, who audited the financial statements last year. Wolfe needs to report on Royal's comparative financial statements and should disclose in the report an explanation about other auditors having audited the prior year

D) Describing the audit and the opinion and naming Mason as the predecessor auditor.

A) Only if Mason's opinion last year was qualified.

B) Describing the prior audit and the opinion but not naming Mason as the predecessor auditor.

C) Describing the audit but not revealing the type of opinion Mason gave.

C) Mason, who audited the financial statements last year. Wolfe needs to report on Royal's comparative financial statements and should disclose in the report an explanation about other auditors having audited the prior year

D) Describing the audit and the opinion and naming Mason as the predecessor auditor.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

62

How is the auditors' own responsibility for expressing the opinion on financial statements disclosed in the report?

A) Stated explicitly in the introductory paragraph of the standard report.

B) Unstated but understood in the introductory paragraph of the standard report.

C) Stated explicitly in the opinion paragraph of the standard report.

D) Stated explicitly in the scope paragraph of the standard report.

A) Stated explicitly in the introductory paragraph of the standard report.

B) Unstated but understood in the introductory paragraph of the standard report.

C) Stated explicitly in the opinion paragraph of the standard report.

D) Stated explicitly in the scope paragraph of the standard report.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

63

Auditors found that the entity has not capitalized a material amount of leases in the financial statements.When considering the overall materiality of this departure from GAAP,the auditors would choose which reporting options?

A) Unqualified opinion or disclaimer of opinion.

B) Unqualified opinion or qualified opinion.

C) Explanatory paragraph with unqualified opinion or an adverse opinion.

D) Qualified opinion or adverse opinion.

A) Unqualified opinion or disclaimer of opinion.

B) Unqualified opinion or qualified opinion.

C) Explanatory paragraph with unqualified opinion or an adverse opinion.

D) Qualified opinion or adverse opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is not included in the scope paragraph of the standard report on the entity's financial statements?

A) A conclusion that the financial statements are in conformity with U.S. GAAP.

B) A statement that the audit was conducted in accordance with the standards of the Public Company Accounting Oversight Board (United States).

C) The fact that an audit includes assessing the accounting principles used by the entity.

D) The fact that the auditors planned and performed the audit to obtain reasonable assurance that the financial statements are free of material misstatement.

A) A conclusion that the financial statements are in conformity with U.S. GAAP.

B) A statement that the audit was conducted in accordance with the standards of the Public Company Accounting Oversight Board (United States).

C) The fact that an audit includes assessing the accounting principles used by the entity.

D) The fact that the auditors planned and performed the audit to obtain reasonable assurance that the financial statements are free of material misstatement.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

65

When auditors render an adverse opinion on the entity's financial statements,the

A) Introductory and scope paragraph should not be modified.

B) Auditors do not possess all necessary evidence.

C) Departures do not need to be explained in the auditors' report.

D) Auditors require less evidence to support the opinion.

A) Introductory and scope paragraph should not be modified.

B) Auditors do not possess all necessary evidence.

C) Departures do not need to be explained in the auditors' report.

D) Auditors require less evidence to support the opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

66

When other independent auditors are involved in the current audit of parts of the entity's business,the group auditors may issue a report that

A) Mentions the component auditors, describes the extent of the component auditors' work, and expresses an unqualified opinion.

B) Does not consider or evaluate the component auditors' work, but expresses an unqualified opinion in a standard report.

C) Places primary responsibility for the reporting on the component auditors.

D) Names the component auditors, describes their work, and presents only the group auditors' report.

A) Mentions the component auditors, describes the extent of the component auditors' work, and expresses an unqualified opinion.

B) Does not consider or evaluate the component auditors' work, but expresses an unqualified opinion in a standard report.

C) Places primary responsibility for the reporting on the component auditors.

D) Names the component auditors, describes their work, and presents only the group auditors' report.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

67

Under which of the following conditions can a disclaimer of opinion never be issued?

A) The entity's going-concern problems are highly material and pervasive.

B) The entity does not allow the auditors access to evidence about important accounts.

C) The auditors own stock in the entity.

D) The auditors have determined that the entity uses the NIFO (next-in, first-out) inventory costing method.

A) The entity's going-concern problems are highly material and pervasive.

B) The entity does not allow the auditors access to evidence about important accounts.

C) The auditors own stock in the entity.

D) The auditors have determined that the entity uses the NIFO (next-in, first-out) inventory costing method.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following is not included in the introductory paragraph of the standard report on the entity's financial statements?

A) The names of the financial statements audited.

B) The auditors' responsibility to express an opinion on the entity's financial statements.

C) Management's responsibility for the financial statements.

D) The fact that an audit provides a reasonable basis for an opinion.

A) The names of the financial statements audited.

B) The auditors' responsibility to express an opinion on the entity's financial statements.

C) Management's responsibility for the financial statements.

D) The fact that an audit provides a reasonable basis for an opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

69

An entity accomplished an early extinguishment of debt and the auditors believe that literal application of GAAP would cause recognition of a loss that would materially distort the financial statements and cause them to be misleading.Given these facts,the auditors would probably choose which reporting option?

A) Explain the situation and issue an adverse opinion.

B) Explain the situation and issue a disclaimer of opinion.

C) Explain the situation and issue an unqualified opinion, relying on Rule 203 of the AICPA Code of Professional Conduct.

D) Issue the standard report.

A) Explain the situation and issue an adverse opinion.

B) Explain the situation and issue a disclaimer of opinion.

C) Explain the situation and issue an unqualified opinion, relying on Rule 203 of the AICPA Code of Professional Conduct.

D) Issue the standard report.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

70

If the auditors decide to present separate reports on the entity's financial statements and internal control over financial reporting,which of the following reports should be modified to refer to the other report?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

71

When reporting on comparative financial statements,auditors ordinarily should modify their previously expressed opinion on the prior-year financial statements if the

A) Prior-year financial statements are restated to conform with generally accepted accounting principles.

B) Auditors were predecessor auditors who have been requested by a former client to reissue the previous report.

C) The prior-year opinion was unqualified and the opinion on the current-year financial statements is modified due to a lack of consistency.

D) The prior-year financial statements are restated following an acquisition in the current year.

A) Prior-year financial statements are restated to conform with generally accepted accounting principles.

B) Auditors were predecessor auditors who have been requested by a former client to reissue the previous report.

C) The prior-year opinion was unqualified and the opinion on the current-year financial statements is modified due to a lack of consistency.

D) The prior-year financial statements are restated following an acquisition in the current year.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is not included in the standard report on the financial statements?

A) An identification of the financial statements that were audited.

B) A general description of an audit.

C) An opinion that the financial statements present financial position in conformity with GAAP.

D) An explanatory paragraph commenting on the effect of economic conditions on the entity.

A) An identification of the financial statements that were audited.

B) A general description of an audit.

C) An opinion that the financial statements present financial position in conformity with GAAP.

D) An explanatory paragraph commenting on the effect of economic conditions on the entity.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

73

How would the auditors' opinion on the entity's financial statements be affected if a material weakness in internal control over financial reporting is identified?

A) The auditors would need to disclaim an opinion on the entity's financial statements.

B) The auditors would need to issue either a qualified or an adverse opinion on the entity's financial statements, depending on the significance of the material weakness.

C) The auditors' opinion on the entity's financial statements would not be affected by the material weakness, assuming sufficient appropriate evidence has been obtained.

D) The auditors would need to withdraw from the engagement and would not issue an opinion or other form of assurance on the financial statements.

A) The auditors would need to disclaim an opinion on the entity's financial statements.

B) The auditors would need to issue either a qualified or an adverse opinion on the entity's financial statements, depending on the significance of the material weakness.

C) The auditors' opinion on the entity's financial statements would not be affected by the material weakness, assuming sufficient appropriate evidence has been obtained.

D) The auditors would need to withdraw from the engagement and would not issue an opinion or other form of assurance on the financial statements.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

74

The auditors determined that the entity is suffering financial difficulty and the going-concern status is seriously in doubt.Assuming the entity adequately disclosed this matter in the financial statements,the auditors must choose between which of the following auditors' report alternatives?

A) Unqualified opinion with a going-concern explanatory paragraph or disclaimer of opinion.

B) Standard report or a disclaimer of opinion.

C) Qualified opinion or adverse opinion.

D) Standard report or adverse opinion.

A) Unqualified opinion with a going-concern explanatory paragraph or disclaimer of opinion.

B) Standard report or a disclaimer of opinion.

C) Qualified opinion or adverse opinion.

D) Standard report or adverse opinion.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following would cause the auditors to issue a report on the entity's financial statements other than a standard report?

A) The financial statements present fairly the financial condition of the entity.

B) The entity omitted a necessary footnote from the financial statements.

C) There were no unusual issues related to the conduct of the audit.

D) The auditors do not need to highlight any entity transactions or events.

A) The financial statements present fairly the financial condition of the entity.

B) The entity omitted a necessary footnote from the financial statements.

C) There were no unusual issues related to the conduct of the audit.

D) The auditors do not need to highlight any entity transactions or events.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

76

When auditors wish to issue an unqualified opinion but highlight that the entity changed its method of accounting for software development costs,what type of report modification would be most appropriate?

A) Identify the change in accounting methods in the introductory paragraph.

B) Identify the change in accounting methods in the opinion paragraph.

C) Identify the change in accounting methods in an emphasis-of-matter paragraph.

D) Identify the change in accounting methods in an other-matter paragraph.

A) Identify the change in accounting methods in the introductory paragraph.

B) Identify the change in accounting methods in the opinion paragraph.

C) Identify the change in accounting methods in an emphasis-of-matter paragraph.

D) Identify the change in accounting methods in an other-matter paragraph.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

77

If the auditors obtain sufficient appropriate evidence on the entity's accounts receivable balance by using alternative procedures because it is impracticable to confirm accounts receivable,the opinion on the entity's financial statements should be unqualified and would

A) Disclose the fact that alternative procedures were used due to client-imposed scope limitation.

B) Disclose in the opinion paragraph that confirmation of accounts receivable was impracticable.

C) Not mention the alternative procedures.

D) Include an explanatory paragraph that discloses the performance of alternative procedures.

A) Disclose the fact that alternative procedures were used due to client-imposed scope limitation.

B) Disclose in the opinion paragraph that confirmation of accounts receivable was impracticable.

C) Not mention the alternative procedures.

D) Include an explanatory paragraph that discloses the performance of alternative procedures.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

78

When reporting under GAAS,certain statements are required in all auditors' reports ("explicit")and others are required only under certain conditions ("implicit").Which combination that follows correctly describes the auditors' responsibilities for reporting?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

79

In a standard report,which of the following paragraphs indicates that auditors conducted their audits in accordance with standards of the PCAOB?

A) Introductory paragraph.

B) Scope paragraph.

C) Opinion paragraph.

D) Additional paragraph.

A) Introductory paragraph.

B) Scope paragraph.

C) Opinion paragraph.

D) Additional paragraph.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

80

Which of these situations would require auditors to append an explanatory paragraph about consistency to an otherwise unqualified opinion?

A) Entity changed its estimated allowance for uncollectible accounts receivable.

B) Entity corrected a prior mistake in accounting for interest capitalization.

C) Entity sold one of its subsidiaries and consolidated six subsidiaries this year compared to seven last year.

D) Entity changed its inventory costing method from FIFO to LIFO.

A) Entity changed its estimated allowance for uncollectible accounts receivable.

B) Entity corrected a prior mistake in accounting for interest capitalization.

C) Entity sold one of its subsidiaries and consolidated six subsidiaries this year compared to seven last year.

D) Entity changed its inventory costing method from FIFO to LIFO.

Unlock Deck

Unlock for access to all 114 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 114 flashcards in this deck.