Deck 22: Managing Interest Rate Risk and Insolvency Risk on the Balance Sheet

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

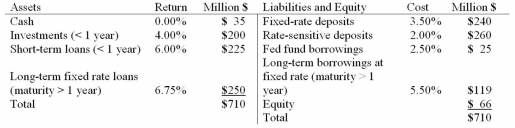

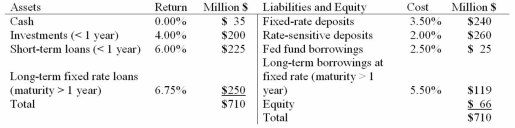

A bank has the following balance sheet:  The bank's one-year repricing gap is (Million $)

The bank's one-year repricing gap is (Million $)

A)$425.

B)$285.

C)$74.

D)$140.

E)$66.

The bank's one-year repricing gap is (Million $)A)$425.

B)$285.

C)$74.

D)$140.

E)$66.

Question

Question

Question

A bank has the following balance sheet:  If the spread effect is zero and all interest rates decline 50 basis points,the bank's NII will change by ________________ over the year.

If the spread effect is zero and all interest rates decline 50 basis points,the bank's NII will change by ________________ over the year.

A)$0

B)$400,000

C)-$400,000

D)$700,000

E)-$700,000

If the spread effect is zero and all interest rates decline 50 basis points,the bank's NII will change by ________________ over the year.A)$0

B)$400,000

C)-$400,000

D)$700,000

E)-$700,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/54

Play

Full screen (f)

Deck 22: Managing Interest Rate Risk and Insolvency Risk on the Balance Sheet

1

Due to convexity problems,banks are actually better off using the simpler repricing model to manage interest rate risk rather than the duration model.

False

2

A bond's price changes 2 percent when interest rates drop. The duration model would predict a price increase of more than 2 percent.

False

3

Insolvency occurs when an institution's duration gap becomes negative.

False

4

A bank has a negative repricing gap using a six-month maturity bucket. Which one of the following statements is most correct if MMDAs are rate-sensitive liabilities?

A)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from two-year CDs at current rates to three-month CDs.

B)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from MMDAs to two-year CDs at current rates.

C)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from three-month CDs to two-year CDs at current rates.

D)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from two-year CDs at current rates to MMDAs.

E)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from MMDAs to two-year CDs at current rates.

A)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from two-year CDs at current rates to three-month CDs.

B)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from MMDAs to two-year CDs at current rates.

C)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from three-month CDs to two-year CDs at current rates.

D)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from two-year CDs at current rates to MMDAs.

E)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail deposit customers to switch from MMDAs to two-year CDs at current rates.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

5

The "runoff" of fixed income contracts is itself rate-sensitive.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

6

If a bank wishes to have a positive balance sheet repricing gap and a negative balance sheet duration gap,then the bank should predominantly have short-term rate-sensitive assets funded by long-term fixed-rate liabilities.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

7

The duration gap model is a more complete measure of interest rate risk than the repricing model.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

8

The cash flow from the interest a bank receives on a long-term loan that is normally reinvested is called the runoff from the loan.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

9

A bank has a positive repricing gap using a six-month maturity bucket. Which one of the following statements is most correct?

A)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from one-year adjustable rate loans to fed funds loans.

B)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from one-month reset floating rate loans to three-year fixed-rate loans at current rates.

C)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from fixed-rate mortgages to adjustable rate mortgages.

D)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from three-year to five-year auto loans.

E)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from their bank to another bank.

A)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from one-year adjustable rate loans to fed funds loans.

B)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from one-month reset floating rate loans to three-year fixed-rate loans at current rates.

C)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from fixed-rate mortgages to adjustable rate mortgages.

D)If all interest rates are projected to increase,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from three-year to five-year auto loans.

E)If all interest rates are projected to decrease,to limit a profit decline when this occurs,the bank could encourage its retail loan customers to switch from their bank to another bank.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

10

A bank is facing a forecast of rising interest rates. How should it set the repricing and duration gap?

A)Positive repricing gap and negative duration gap

B)Negative repricing gap and positive duration gap

C)Positive repricing gap and positive duration gap

D)Negative repricing gap and negative duration gap

A)Positive repricing gap and negative duration gap

B)Negative repricing gap and positive duration gap

C)Positive repricing gap and positive duration gap

D)Negative repricing gap and negative duration gap

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

11

A bank has a negative duration gap. Which one of the following statements is most correct?

A)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase the amount of short-term loans on the balance sheet.

B)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase the amount of short-term bonds issued by the bank.

C)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase the amount of long-term loans on the balance sheet.

D)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase the amount of long-term bonds issued by the bank.

A)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase the amount of short-term loans on the balance sheet.

B)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase the amount of short-term bonds issued by the bank.

C)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase the amount of long-term loans on the balance sheet.

D)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase the amount of long-term bonds issued by the bank.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

12

The repricing gap fails to consider how the value of fixed income accounts will change when rates change.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

13

If a bank has a negative repricing gap,falling interest rates increase profitability.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

14

A rate-sensitive asset is one that either matures within the maturity bucket or one that will have a payment change within the maturity bucket if interest rates change.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

15

Convexity arises because a fixed income's price is a nonlinear function of interest rates.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

16

For a one-year maturity bucket,the repricing model assumes that a nine-month loan is as equally rate-sensitive as a three-month loan.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

17

In a bank's three-month maturity bucket,a 30-year ARM with a rate reset in six months would be considered a fixed-rate asset,but in its one-year maturity bucket,this ARM would be considered a rate-sensitive asset.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

18

The repricing gap is the most comprehensive measure of interest rate risk used by financial intermediaries.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

19

If DA > kDL,then falling interest rates will cause the market value of equity to rise.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

20

The structure of a bank's balance sheet as evidenced by its repricing gap and its duration gap affects a bank's sensitivity to interest rate changes. Which one of the following statements about the two types of gaps is true?

A)The repricing gap immunizes the present value of all future cash flows,whereas managing the duration gap can stabilize future cash flows,but not their present value.

B)The duration gap considers all cash flows up to and including maturity,whereas the repricing gap really only considers how cash flows will change within the maturity bucket.

C)If a bank could only manage one type of gap,the bank would limit its interest rate risk the most by managing its repricing gap instead of its duration gap.

D)The repricing gap is superior to the duration gap since the repricing gap has a well-defined maturity bucket.

E)It is virtually impossible for an institution to have both a positive duration gap and a negative repricing gap at the same time.

A)The repricing gap immunizes the present value of all future cash flows,whereas managing the duration gap can stabilize future cash flows,but not their present value.

B)The duration gap considers all cash flows up to and including maturity,whereas the repricing gap really only considers how cash flows will change within the maturity bucket.

C)If a bank could only manage one type of gap,the bank would limit its interest rate risk the most by managing its repricing gap instead of its duration gap.

D)The repricing gap is superior to the duration gap since the repricing gap has a well-defined maturity bucket.

E)It is virtually impossible for an institution to have both a positive duration gap and a negative repricing gap at the same time.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

21

A bank has the following balance sheet: The bank's one-year repricing gap is (Million $)

A)$425.

B)$285.

C)$74.

D)$140.

E)$66.

The bank's one-year repricing gap is (Million $)A)$425.

B)$285.

C)$74.

D)$140.

E)$66.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

22

For large interest rate declines,duration ___________ the increases in the bond's price,and for large interest rate increases,it ____________ the decline in the bond's price.

A)underpredicts; overpredicts

B)overpredicts; underpredicts

C)underpredicts; underpredicts

D)overpredicts; overpredicts

A)underpredicts; overpredicts

B)overpredicts; underpredicts

C)underpredicts; underpredicts

D)overpredicts; overpredicts

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

23

After interest rate and yield curve changes,a bank's market value of assets increased $4 million and the market value of its liabilities fell $6 million. The book value of equity _____________ and the market value of equity ____________.

A)increased $2 million; was unchanged

B)fell $2 million; was unchanged

C)was unchanged; fell $2 million

D)was unchanged; fell $10 million

E)was unchanged; increased $10 million

A)increased $2 million; was unchanged

B)fell $2 million; was unchanged

C)was unchanged; fell $2 million

D)was unchanged; fell $10 million

E)was unchanged; increased $10 million

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

24

A bank has the following balance sheet: If the spread effect is zero and all interest rates decline 50 basis points,the bank's NII will change by ________________ over the year.

A)$0

B)$400,000

C)-$400,000

D)$700,000

E)-$700,000

If the spread effect is zero and all interest rates decline 50 basis points,the bank's NII will change by ________________ over the year.A)$0

B)$400,000

C)-$400,000

D)$700,000

E)-$700,000

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

25

For a nine-month maturity bucket,the bank has _________________ in fixed-rate assets and _________________ in fixed-rate liabilities.

A)$425; $285

B)$285; $425

C)$285; $359

D)$359; $285

E)$250; $66

A)$425; $285

B)$285; $425

C)$285; $359

D)$359; $285

E)$250; $66

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

26

A bank has DA = 2.4 years and DL= 0.9 years. The bank has total equity of $82 million and total assets of $850 million. Interest rates are at 6 percent. If interest rates increase 100 basis points the predicted dollar change in equity value will equal

A)$10,171,698.

B)-$10,171,698.

C)$12,724,528.

D)-$12,724,528.

E)$4,928,756.

A)$10,171,698.

B)-$10,171,698.

C)$12,724,528.

D)-$12,724,528.

E)$4,928,756.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

27

A bank has a negative repricing gap and estimates that the spread between RSAs and RSLs will move inversely with interest rates. If interest rates increase,NII will

A)rise.

B)fall.

C)be unchanged.

D)rise or fall depending on the size of the spread effect relative to the size of the CGAP effect.

A)rise.

B)fall.

C)be unchanged.

D)rise or fall depending on the size of the spread effect relative to the size of the CGAP effect.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

28

A bank has three assets. It has $75 million invested in consumer loans with a three-year duration,$39 million invested in T-bonds with a 16-year duration,and $39 million in six-month maturity T-bills. What is the duration of the bank's asset portfolio in years?

A)3.95 years

B)4.83 years

C)6.50 years

D)7.38 years

E)11.51 years

A)3.95 years

B)4.83 years

C)6.50 years

D)7.38 years

E)11.51 years

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

29

A bank has a positive duration gap. Which one of the following statements is most correct?

A)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase long-term loans and decrease short-term loans.

B)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase long-term loans and decrease short-term loans.

C)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase short-term loans and decrease long-term loans.

D)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase long-term bonds issued by the bank and decrease short-term bonds.

A)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase long-term loans and decrease short-term loans.

B)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase long-term loans and decrease short-term loans.

C)If all interest rates are projected to increase,to limit a net value decline before rates rise,the bank should increase short-term loans and decrease long-term loans.

D)If all interest rates are projected to decrease,to limit a net value decline before rates fall,the bank should increase long-term bonds issued by the bank and decrease short-term bonds.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

30

Weaknesses of the repricing model include the fact that

I) it ignores changes in present values caused by changes in interest rates.

II) it ignores different cash flow sensitivities within a maturity bucket.

III) it fails to account for runoffs and prepayments.

A)I only

B)I and II only

C)I and III only

D)II and III only

E)I,II,and III

I) it ignores changes in present values caused by changes in interest rates.

II) it ignores different cash flow sensitivities within a maturity bucket.

III) it fails to account for runoffs and prepayments.

A)I only

B)I and II only

C)I and III only

D)II and III only

E)I,II,and III

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

31

For a bank with a positive duration gap,an increase in interest rates will

A)increase the likelihood of insolvency.

B)decrease the likelihood of insolvency.

C)not affect the likelihood of insolvency.

D)result in increased loan trading.

A)increase the likelihood of insolvency.

B)decrease the likelihood of insolvency.

C)not affect the likelihood of insolvency.

D)result in increased loan trading.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

32

A bank has DA = 2.4 years and DL= 0.9 years. The bank has total equity of $82 million and total assets of $850 million. Interest rates are at 6 percent. To get DE to equal zero to protect the equity value in the event of an interest rate change,the bank could

A)reduce DA to 1.21 years.

B)increase DL to 2.44 years.

C)increase DL to 3.10 years.

D)reduce DA to zero.

E)increase DL to 2.76 years.

A)reduce DA to 1.21 years.

B)increase DL to 2.44 years.

C)increase DL to 3.10 years.

D)reduce DA to zero.

E)increase DL to 2.76 years.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

33

A bank's balance sheet is characterized by long-term fixed-rate assets funded by short-term variable-rate liabilities. Most likely the bank has a

A)positive repricing gap and a positive duration gap.

B)positive repricing gap and a negative duration gap.

C)negative repricing gap and a positive duration gap.

D)negative repricing gap and a negative duration gap.

A)positive repricing gap and a positive duration gap.

B)positive repricing gap and a negative duration gap.

C)negative repricing gap and a positive duration gap.

D)negative repricing gap and a negative duration gap.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

34

A bank has DA = 2.4 years and DL= 0.9 years. The bank has total equity of $82 million and total assets of $850 million. Interest rates are at 6 percent. What is the bank's duration gap in years?

A)1.5325

B)1.5868

C)1.2685

D)1.4563

E)1.6222

A)1.5325

B)1.5868

C)1.2685

D)1.4563

E)1.6222

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

35

A bank has a negative repricing gap. This implies that

A)some RSAs are financed by fixed-rate liabilities.

B)some RSLs are financing fixed-rate assets.

C)some RSAs are financing equity.

D)the bank has no fixed-rate assets.

A)some RSAs are financed by fixed-rate liabilities.

B)some RSLs are financing fixed-rate assets.

C)some RSAs are financing equity.

D)the bank has no fixed-rate assets.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

36

An FI's balance sheet is characterized by long-term fixed-rate assets funded by short-term variable-rate securities. Most likely the bank has a

A)positive repricing gap and a positive duration gap.

B)positive repricing gap and a negative duration gap.

C)negative repricing gap and a positive duration gap.

D)negative repricing gap and a negative duration gap.

A)positive repricing gap and a positive duration gap.

B)positive repricing gap and a negative duration gap.

C)negative repricing gap and a positive duration gap.

D)negative repricing gap and a negative duration gap.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

37

A bank has a negative duration gap. Interest rates decline. Which one of the following best describes the effects of the interest rate change?

A)The bank's market value of equity is unchanged since the market value of its assets and liabilities moves in the same direction.

B)The bank's market value of equity goes up because the market value of its assets goes up by more than the market value of its liabilities goes down.

C)The bank's market value of equity goes down because the market value of its assets goes up by more than the market value of its liabilities goes down.

D)The bank's market value of equity goes down because the market value of its assets goes down by more than the market value of its liabilities goes down.

E)The bank's market value of equity goes down because the market value of its liabilities increases by more than the market value of its assets increases.

A)The bank's market value of equity is unchanged since the market value of its assets and liabilities moves in the same direction.

B)The bank's market value of equity goes up because the market value of its assets goes up by more than the market value of its liabilities goes down.

C)The bank's market value of equity goes down because the market value of its assets goes up by more than the market value of its liabilities goes down.

D)The bank's market value of equity goes down because the market value of its assets goes down by more than the market value of its liabilities goes down.

E)The bank's market value of equity goes down because the market value of its liabilities increases by more than the market value of its assets increases.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

38

With a six-month maturity bucket,a nine-month fixed-rate loan would be considered a ________________ asset and a 30-year mortgage with a rate adjustment in three months would be classified as a _______________ asset.

A)rate-sensitive; fixed-rate

B)rate-sensitive; rate-sensitive

C)fixed-rate; fixed-rate

D)fixed-rate; rate-sensitive

E)fixed-rate; nonearning

A)rate-sensitive; fixed-rate

B)rate-sensitive; rate-sensitive

C)fixed-rate; fixed-rate

D)fixed-rate; rate-sensitive

E)fixed-rate; nonearning

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

39

A bank has a positive repricing gap and estimates that the spread between RSAs and RSLs will move directly with interest rates. If interest rates fall,the bank's overall NII will

A)rise.

B)fall.

C)be unchanged.

D)rise or fall depending on the size of the spread effect relative to the size of the CGAP effect.

A)rise.

B)fall.

C)be unchanged.

D)rise or fall depending on the size of the spread effect relative to the size of the CGAP effect.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

40

A bank has a positive repricing gap. This implies that

A)some RSAs are financed by fixed-rate liabilities.

B)some RSLs are financing fixed-rate assets.

C)some RSAs are financing equity.

D)the bank has no fixed-rate assets.

A)some RSAs are financed by fixed-rate liabilities.

B)some RSLs are financing fixed-rate assets.

C)some RSAs are financing equity.

D)the bank has no fixed-rate assets.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

41

A thrift has an annual CGAP of -$25 million. A credit union has an annual CGAP of +$5 million. The thrift has total assets of $500 million and net income of $7.5 million,and the credit union has total assets of $40 million and net income of $0.7 million.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

42

What are arguments for and against requiring banks to mark all assets and liabilities to market continuously?

Relate your arguments to managing credit risk and interest rate risk.

Relate your arguments to managing credit risk and interest rate risk.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

43

Convexity in bond prices is caused by the

A)coupon changes on a bond.

B)change in default probability associated with a yield change.

C)CGAP effect.

D)curvature around the bond price yield relationship.

E)mismatch between the duration of the assets and liabilities.

A)coupon changes on a bond.

B)change in default probability associated with a yield change.

C)CGAP effect.

D)curvature around the bond price yield relationship.

E)mismatch between the duration of the assets and liabilities.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

44

A bank has book value of assets equal to $800 million and market value of assets equal to $1,100 million. The bank has book value of liabilities of $700 million and market value of liabilities equal to $850 million. The bank's market-to-book ratio is

A)2.5.

B)2.0.

C)1.5.

D)1.0.

E)0.67.

A)2.5.

B)2.0.

C)1.5.

D)1.0.

E)0.67.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

45

Weaknesses of the duration gap immunization model include all but which of the following?

A)Continuously matching the duration of assets and liabilities can be time-consuming and costly.

B)Duration-based predictions are always incorrect due to convexity.

C)Duration measurement and management are more complex than the repricing model.

D)Duration-based immunization strategies require continuous rebalancing of asset and liability durations.

E)Duration measures only how cash flows change,not the present value of those changes.

A)Continuously matching the duration of assets and liabilities can be time-consuming and costly.

B)Duration-based predictions are always incorrect due to convexity.

C)Duration measurement and management are more complex than the repricing model.

D)Duration-based immunization strategies require continuous rebalancing of asset and liability durations.

E)Duration measures only how cash flows change,not the present value of those changes.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

46

A thrift has an annual CGAP of -$25 million. A credit union has an annual CGAP of +$5 million. The thrift has total assets of $500 million and net income of $7.5 million,and the credit union has total assets of $40 million and net income of $0.7 million. Assuming a zero spread effect,if all interest rates decrease 50 basis points,what is the change in NII for the thrift?

For the credit union?

For the credit union?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

47

What are three major weaknesses of the repricing model?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

48

A bank has DA = 2.5 years,DL= 0.80 years,and k = 92%. Assets are equal to $1,200 million. According to the duration gap model,what size interest rate change would make the institution insolvent if rates are currently 5 percent?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

49

A bank has an average asset duration of 2.25 years,the average duration of the liabilities is 1.25 years,and the bank has total assets of $2 billion and $200 million in equity. The bank has an ROE of 9.00 percent. If all interest rates decrease 50 basis points,the predicted change in the bank's market value of equity is ___________.

A)-2.85 percent

B)-3.55 percent

C)3.55 percent

D)2.85 percent

E)5.16 percent

A)-2.85 percent

B)-3.55 percent

C)3.55 percent

D)2.85 percent

E)5.16 percent

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

50

Explain how interest rate risk could change at banks,thrifts,and other institutions that originate and sell fixed-rate mortgages but are funded with deposits if these institutions lose the ability to securitize and sell mortgages. What could be the effect on the economy?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

51

What factors can cause a bank's book value of equity to differ from its market value?

What widely available ratio is typically used to measure the difference between the two?

What widely available ratio is typically used to measure the difference between the two?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

52

In each of the following cases indicate whether the change in profits due to the spread effect was (i)greater than (ii)less than,or (iii)equal to the change in profitability due to the repricing GAP. In some cases you may not be able to tell; indicate which ones.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

53

Explain how an FI's capital protects against credit risk and interest rate risk.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

54

The effect of an interest rate change on the market value of an FI's equity is a function of three things. What are they and how do they affect the equity value change?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 54 flashcards in this deck.