Deck 18: Capital Management and Adequacy

Full screen (f)

Question

Question

Question

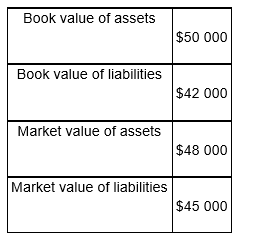

Assume you are presented with the following data regarding an FI's asset and liability values:  Which of the following statements is true?

Which of the following statements is true?

A) The net worth of the FI is $2000.

B) The net worth of the FI is -$3000.

C) The net worth of the FI is $3000.

D) The net worth of the FI is -$1000.

Which of the following statements is true?A) The net worth of the FI is $2000.

B) The net worth of the FI is -$3000.

C) The net worth of the FI is $3000.

D) The net worth of the FI is -$1000.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/66

Play

Full screen (f)

Deck 18: Capital Management and Adequacy

1

Which of the following elements is usually not included in the book value of capital?

A) the par value of shares

B) the FI's earnings

C) loan loss reserve

D) the surplus value of shares

A) the par value of shares

B) the FI's earnings

C) loan loss reserve

D) the surplus value of shares

B

2

Which of the following statements is true?

A) The par value of shares is the current market price of the common stock shares issued by the FI times the number of shares outstanding.

B) Retained earnings is the accumulated value of past profits not yet paid out in dividends to shareholders.

C) Loan loss reserve is a special reserve set aside out of retained earnings to meet unexpected losses on the portfolio.

D) All of the listed options are correct.

A) The par value of shares is the current market price of the common stock shares issued by the FI times the number of shares outstanding.

B) Retained earnings is the accumulated value of past profits not yet paid out in dividends to shareholders.

C) Loan loss reserve is a special reserve set aside out of retained earnings to meet unexpected losses on the portfolio.

D) All of the listed options are correct.

B

3

Assume you are presented with the following data regarding an FI's asset and liability values: Which of the following statements is true?

A) The net worth of the FI is $2000.

B) The net worth of the FI is -$3000.

C) The net worth of the FI is $3000.

D) The net worth of the FI is -$1000.

Which of the following statements is true?A) The net worth of the FI is $2000.

B) The net worth of the FI is -$3000.

C) The net worth of the FI is $3000.

D) The net worth of the FI is -$1000.

The net worth of the FI is $3000.

4

Which of the following statements is true?

A) Banks get a tax-shelter against the cost of write offs.

B) The cost of a write-off is increased by a tax shelter.

C) If losses exceed a bank's loan loss reserves, the bank is likely to use its liquidity holdings as its next line of defence.

D) All of the listed options are correct.

A) Banks get a tax-shelter against the cost of write offs.

B) The cost of a write-off is increased by a tax shelter.

C) If losses exceed a bank's loan loss reserves, the bank is likely to use its liquidity holdings as its next line of defence.

D) All of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

5

The term 'credit equivalent amount' refers to the:

A) nominal value of an on-balance-sheet item exposed to credit risk.

B) credit risk exposure of an on-balance-sheet item.

C) credit risk exposure of an off-balance-sheet item.

D) nominal value of an off-balance-sheet item exposed to credit risk.

A) nominal value of an on-balance-sheet item exposed to credit risk.

B) credit risk exposure of an on-balance-sheet item.

C) credit risk exposure of an off-balance-sheet item.

D) nominal value of an off-balance-sheet item exposed to credit risk.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is the correct way to calculate the historic value of an FI's equity per share?

A) The sum of the par value of equity divided by the number of shares.

B) The market value of ownership shares outstanding divided by the number of shares.

C) The sum of the par value of equity, the surplus value, retained earnings and loan reserves divided by the number of shares.

D) The sum of the par value of equity and retained earnings divided by the number of shares.

A) The sum of the par value of equity divided by the number of shares.

B) The market value of ownership shares outstanding divided by the number of shares.

C) The sum of the par value of equity, the surplus value, retained earnings and loan reserves divided by the number of shares.

D) The sum of the par value of equity and retained earnings divided by the number of shares.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

7

Assume an FI has $50 000 in assets and $45 000 in liabilities. Which of the following statements is true if interest rates on both assets and liabilities increase simultaneously?

A) As the interest rate for both assets and liabilities increase the value of the FI's net worth will remain constant.

B) As the interest rate for both assets and liabilities increase the value of the FI's assets and liabilities will both decrease.

C) As the interest rate for both assets and liabilities increase the value of the FI's assets and liabilities will both increase.

D) As the interest rate for both assets and liabilities increase the value of the FI's assets and liabilities will both increase, however as the FI has more assets than liabilities, the increase in the value of the FI's assets will be greater than the increase in the value of its liabilities.

A) As the interest rate for both assets and liabilities increase the value of the FI's net worth will remain constant.

B) As the interest rate for both assets and liabilities increase the value of the FI's assets and liabilities will both decrease.

C) As the interest rate for both assets and liabilities increase the value of the FI's assets and liabilities will both increase.

D) As the interest rate for both assets and liabilities increase the value of the FI's assets and liabilities will both increase, however as the FI has more assets than liabilities, the increase in the value of the FI's assets will be greater than the increase in the value of its liabilities.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements is true?

A) The Tier 1 capital ratio is the ratio of supplementary capital to the risk-adjusted assets of an FI.

B) The Tier 1 capital ratio is the ratio of core capital to the risk-adjusted assets of an FI.

C) The Tier 1 capital ratio is the ratio of supplementary capital to the assets of an FI.

D) The Tier 1 capital ratio is the ratio of core capital to the assets of an FI.

A) The Tier 1 capital ratio is the ratio of supplementary capital to the risk-adjusted assets of an FI.

B) The Tier 1 capital ratio is the ratio of core capital to the risk-adjusted assets of an FI.

C) The Tier 1 capital ratio is the ratio of supplementary capital to the assets of an FI.

D) The Tier 1 capital ratio is the ratio of core capital to the assets of an FI.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements is true?

A) The Basel Accord imposes minimum earnings ratios on banks in major industrialised countries.

B) The Basel Accord imposes maximum asset values on banks in major industrialised countries.

C) The Basel Accord imposes minimum liability values on banks in major industrialised countries.

D) The Basel Accord imposes risk-based capital ratios on banks in major industrialised countries.

A) The Basel Accord imposes minimum earnings ratios on banks in major industrialised countries.

B) The Basel Accord imposes maximum asset values on banks in major industrialised countries.

C) The Basel Accord imposes minimum liability values on banks in major industrialised countries.

D) The Basel Accord imposes risk-based capital ratios on banks in major industrialised countries.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is true?

A) Total capital is the sum of Tier I and Tier II capital less deductions.

B) Total capital must equal or exceed 8 per cent of risk-weighted assets.

C) The total of Tier II capital is limited to 100 per cent of Tier I capital.

D) All of the listed options are correct.

A) Total capital is the sum of Tier I and Tier II capital less deductions.

B) Total capital must equal or exceed 8 per cent of risk-weighted assets.

C) The total of Tier II capital is limited to 100 per cent of Tier I capital.

D) All of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is true?

A) The credit equivalent amount is calculated by multiplying the present value of an off-balance-sheet instrument by a conversion factor.

B) The credit equivalent amount is calculated by multiplying the present value of an on-balance-sheet instrument by a conversion factor.

C) The credit equivalent amount is calculated by multiplying the notional amount by a conversion factor.

D) The credit equivalent amount is calculated by multiplying the face value of an on-balance-sheet instrument by a conversion factor.

A) The credit equivalent amount is calculated by multiplying the present value of an off-balance-sheet instrument by a conversion factor.

B) The credit equivalent amount is calculated by multiplying the present value of an on-balance-sheet instrument by a conversion factor.

C) The credit equivalent amount is calculated by multiplying the notional amount by a conversion factor.

D) The credit equivalent amount is calculated by multiplying the face value of an on-balance-sheet instrument by a conversion factor.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following are arguments against market value accounting?

A) It introduces a higher degree of stability into an FI's earnings.

B) It is difficult to implement.

C) FI's would be less willing to accept investments in shorter term assets.

D) There are no arguments against market value accounting.

A) It introduces a higher degree of stability into an FI's earnings.

B) It is difficult to implement.

C) FI's would be less willing to accept investments in shorter term assets.

D) There are no arguments against market value accounting.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following statements is true for Basel II agreement?

A) The Basel capital framework consists of three mutually reinforcing pillars.

B) Pillar I deals with the calculation of regulatory capital against FI's credit risk only.

C) Pillar II deals with market discipline.

D) Pillar III deals with the supervisory review process.

A) The Basel capital framework consists of three mutually reinforcing pillars.

B) Pillar I deals with the calculation of regulatory capital against FI's credit risk only.

C) Pillar II deals with market discipline.

D) Pillar III deals with the supervisory review process.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements is true?

A) Potential exposure refers to the cost of replacing a derivative securities contract at today's prices.

B) Current exposure refers to the cost of replacing a derivative securities contract at today's prices.

C) Current exposure refers to the cost of replacing a derivative securities contract at the contract's maturity.

D) Potential exposure refers to the cost of replacing a derivative securities contract at the contract's maturity.

A) Potential exposure refers to the cost of replacing a derivative securities contract at today's prices.

B) Current exposure refers to the cost of replacing a derivative securities contract at today's prices.

C) Current exposure refers to the cost of replacing a derivative securities contract at the contract's maturity.

D) Potential exposure refers to the cost of replacing a derivative securities contract at the contract's maturity.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

15

The net worth is a measure of an FI's capital that is equal to the difference between the:

A) book value of its assets and the market value of its liabilities.

B) market value of its assets and the book value of its liabilities.

C) market value of its assets and the market value of its liabilities.

D) book value of its liabilities and the book value of its assets.

A) book value of its assets and the market value of its liabilities.

B) market value of its assets and the book value of its liabilities.

C) market value of its assets and the market value of its liabilities.

D) book value of its liabilities and the book value of its assets.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements is true?

A) Credit-risk adjusted assets are on-balance-sheet assets only whose values are adjusted for approximate credit risk.

B) Credit-risk adjusted assets are off-balance-sheet assets only whose values are adjusted for approximate credit risk.

C) Credit-risk adjusted assets are on- and off-balance-sheet assets whose values are adjusted for approximate credit risk.

D) Credit-risk adjusted assets are on- and off-balance-sheet assets whose values are adjusted for approximate credit risk of the FI.

A) Credit-risk adjusted assets are on-balance-sheet assets only whose values are adjusted for approximate credit risk.

B) Credit-risk adjusted assets are off-balance-sheet assets only whose values are adjusted for approximate credit risk.

C) Credit-risk adjusted assets are on- and off-balance-sheet assets whose values are adjusted for approximate credit risk.

D) Credit-risk adjusted assets are on- and off-balance-sheet assets whose values are adjusted for approximate credit risk of the FI.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following statements is true?

A) The market to book ratio shows the degree of discrepancy between the stock market value of an FI's equity and the book value of its equity.

B) The market to book ratio shows the degree of discrepancy between the stock market value of an FI's assets and the book value of its assets.

C) The market to book ratio shows the degree of discrepancy between the stock market value of an FI's liabilities and the book value of its liabilities.

D) None of the listed options are correct.

A) The market to book ratio shows the degree of discrepancy between the stock market value of an FI's equity and the book value of its equity.

B) The market to book ratio shows the degree of discrepancy between the stock market value of an FI's assets and the book value of its assets.

C) The market to book ratio shows the degree of discrepancy between the stock market value of an FI's liabilities and the book value of its liabilities.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following statements is true?

A) The first capital adequacy rules were implemented in Australia in 1987.

B) The first capital adequacy rules were implemented in Australia in 1988.

C) The first capital adequacy rules were implemented in Australia in 1989.

D) The first capital adequacy rules were implemented in Australia in 1990.

A) The first capital adequacy rules were implemented in Australia in 1987.

B) The first capital adequacy rules were implemented in Australia in 1988.

C) The first capital adequacy rules were implemented in Australia in 1989.

D) The first capital adequacy rules were implemented in Australia in 1990.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following are problems in using the leverage ratio as a measure of capital adequacy?

A) Even with a low leverage ratio, an FI could have a negative market value net worth.

B) The different types of risks, such as credit or interest rate risk are not captured.

C) Off-balance-sheet activities are not captured.

D) Even with a low leverage ratio, an FI could have a negative market value net worth, the different types of risks, such as credit or interest rate risk are not captured and off-balance-sheet activities are not captured.

A) Even with a low leverage ratio, an FI could have a negative market value net worth.

B) The different types of risks, such as credit or interest rate risk are not captured.

C) Off-balance-sheet activities are not captured.

D) Even with a low leverage ratio, an FI could have a negative market value net worth, the different types of risks, such as credit or interest rate risk are not captured and off-balance-sheet activities are not captured.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements is true?

A) The book value of a liability is the reported liability value reported according to its historical costs.

B) The market value concept is also referred to as marking to market.

C) Marking to market allows balance sheet values to reflect current rather than historical prices.

D) All of the listed options are correct.

A) The book value of a liability is the reported liability value reported according to its historical costs.

B) The market value concept is also referred to as marking to market.

C) Marking to market allows balance sheet values to reflect current rather than historical prices.

D) All of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

21

Market to book ratio is a ratio that shows the discrepancy between the:

A) stock market value of an FI's equity and the book value of its equity.

B) historic value of an FI's equity and the book value of its equity.

C) US dollar value of an FI's equity and the book value of its equity.

D) value of an FI's debt and the book value of its debt.

A) stock market value of an FI's equity and the book value of its equity.

B) historic value of an FI's equity and the book value of its equity.

C) US dollar value of an FI's equity and the book value of its equity.

D) value of an FI's debt and the book value of its debt.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

22

Loan loss reserve is:

A) the accumulated value of past profits not yet paid out in dividends to shareholders.

B) the face value of the ordinary shares issued by the FI.

C) a special reserve set aside out of retained earnings to meet expected and actual losses on the portfolio.

D) the difference between the price the public paid for common stock or shares when originally offered and their par values times the number of shares outstanding.

A) the accumulated value of past profits not yet paid out in dividends to shareholders.

B) the face value of the ordinary shares issued by the FI.

C) a special reserve set aside out of retained earnings to meet expected and actual losses on the portfolio.

D) the difference between the price the public paid for common stock or shares when originally offered and their par values times the number of shares outstanding.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

23

Consider an FI with the following off-balance-sheet items: A two-year loan commitment with a face value of $120 million, a standby letter of credit with a face value of $20 million and trade-related letters of credit with a face value of $70 million. All counterparties have a credit rating of BBB. What is the capital amount the FI needs to hold against these exposures?

A) $5.04 million

B) $7.52 million

C) $8.4 million

D) $24.8 million

A) $5.04 million

B) $7.52 million

C) $8.4 million

D) $24.8 million

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

24

Economic capital is:

A) the asset and liability values of an FI reported according to their historical costs.

B) the amount of capital that the DI's shareholders are prepared to contribute so that the business remains as a going concern.

C) a measure of an FI's capital that is equal to the difference between the market value of its assets and the market value of its liabilities.

D) allows balance sheet values to reflect current rather than historical prices.

A) the asset and liability values of an FI reported according to their historical costs.

B) the amount of capital that the DI's shareholders are prepared to contribute so that the business remains as a going concern.

C) a measure of an FI's capital that is equal to the difference between the market value of its assets and the market value of its liabilities.

D) allows balance sheet values to reflect current rather than historical prices.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following are criticisms of a risk-based capital ratio?

A) The risk-class categories might not adequately reflect riskiness.

B) The 8 per cent risk-based capital requirement has not created a level competitive playing field across banks.

C) Credit risk portfolio diversification opportunities are largely ignored.

D) All of the listed options are correct.

A) The risk-class categories might not adequately reflect riskiness.

B) The 8 per cent risk-based capital requirement has not created a level competitive playing field across banks.

C) Credit risk portfolio diversification opportunities are largely ignored.

D) All of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

26

Choose the correct statement:

A) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the standardised approach.

B) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the advanced approach.

C) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the combination approach.

D) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the IRB approach.

A) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the standardised approach.

B) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the advanced approach.

C) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the combination approach.

D) APRA's APS 112 Capital adequacy: standardised approach to credit risk (APS 112), sets out the methods to be used to calculate credit-risk-adjusted assets using the IRB approach.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

27

Consider an FI with the following off-balance-sheet items: A two-year loan commitment with a face value of $120 million, a standby letter of credit with a face value of $20m and trade-related letters of credit with a face value of $70 million. What is the total credit equivalent amount?

A) $63 million

B) $94 million

C) $105 million

D) $310 million

A) $63 million

B) $94 million

C) $105 million

D) $310 million

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

28

Choose the correct capital adequacy ratio(s):

A) Total capital (Tier 1 capital plus Tier 2 capital) must be at least 6.5 per cent of risk-weighted assets at all times.

B) Total Tier 1 capital must be at least 9 per cent of risk-weighted assets at all times.

C) Common equity Tier 1 must be at least 7.5 per cent of risk-weighted assets at all times.

D) None of the listed options are correct.

A) Total capital (Tier 1 capital plus Tier 2 capital) must be at least 6.5 per cent of risk-weighted assets at all times.

B) Total Tier 1 capital must be at least 9 per cent of risk-weighted assets at all times.

C) Common equity Tier 1 must be at least 7.5 per cent of risk-weighted assets at all times.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

29

Current credit exposure is the:

A) credit risk exposure of an off-balance-sheet item.

B) cost of replacing a derivative securities contract at today's prices.

C) risk that a counterparty to a derivative securities contract will default in the future.

D) potential loss on current loans.

A) credit risk exposure of an off-balance-sheet item.

B) cost of replacing a derivative securities contract at today's prices.

C) risk that a counterparty to a derivative securities contract will default in the future.

D) potential loss on current loans.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

30

Procyclicality refers to features or characteristics that:

A) serve to exacerbate or amplify the underlying cyclicality of economic activity.

B) are only apparent during the down cycle of an economy.

C) help the economy to recover from a down cycle.

D) None of the listed options are correct.

A) serve to exacerbate or amplify the underlying cyclicality of economic activity.

B) are only apparent during the down cycle of an economy.

C) help the economy to recover from a down cycle.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

31

Choose the correct statement:

A) Basel II provides a better alignment of risks to borrowers than Basel I and remains the basis of the current measurement of credit-risk-adjusted assets.

B) Basel I provides a better alignment of risks to borrowers than Basel II and remains the basis of the current measurement of credit-risk-adjusted assets.

C) Basel III provides a better alignment of risks to borrowers than Basel II and remains the basis of the current measurement of credit-risk-adjusted assets.

D) None of the listed options are correct.

A) Basel II provides a better alignment of risks to borrowers than Basel I and remains the basis of the current measurement of credit-risk-adjusted assets.

B) Basel I provides a better alignment of risks to borrowers than Basel II and remains the basis of the current measurement of credit-risk-adjusted assets.

C) Basel III provides a better alignment of risks to borrowers than Basel II and remains the basis of the current measurement of credit-risk-adjusted assets.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

32

Book value is:

A) the asset and liability values of an FI reported according to their historical costs.

B) the amount of capital that the DI's shareholders are prepared to contribute so that the business remains as a going concern.

C) a measure of an FI's capital that is equal to the difference between the market value of its assets and the market value of its liabilities.

D) allows balance sheet values to reflect current rather than historical prices.

A) the asset and liability values of an FI reported according to their historical costs.

B) the amount of capital that the DI's shareholders are prepared to contribute so that the business remains as a going concern.

C) a measure of an FI's capital that is equal to the difference between the market value of its assets and the market value of its liabilities.

D) allows balance sheet values to reflect current rather than historical prices.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

33

Total capital (Tier 1 capital plus Tier 2 capital) must be at least ______ of risk-weighted assets at all times:

A) 9 per cent

B) 7.5 per cent

C) 8 per cent

D) 4.5 per cent

A) 9 per cent

B) 7.5 per cent

C) 8 per cent

D) 4.5 per cent

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

34

Credit derivatives were included in the banking book with the introduction of:

A) Basel I.

B) Basel II.

C) Basel 2.5.

D) Basel III.

A) Basel I.

B) Basel II.

C) Basel 2.5.

D) Basel III.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements is true in the context of Basel II?

A) The standardised approach is the most basic approach to calculating operational risk capital.

B) FI's can choose whether or not to hold operational risk capital.

C) In the basic indicator approach, operational risk capital is calculated as a fixed percentage of an FI's gross income figure, whereby gross income is defined as gross interest income plus gross non-interest income.

D) None of the listed options are correct.

A) The standardised approach is the most basic approach to calculating operational risk capital.

B) FI's can choose whether or not to hold operational risk capital.

C) In the basic indicator approach, operational risk capital is calculated as a fixed percentage of an FI's gross income figure, whereby gross income is defined as gross interest income plus gross non-interest income.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

36

Choose the correct answer:

A) The purpose of Pillar 1 is to encourage market discipline through an information disclosure framework covering capital, capital adequacy, risk exposures and risk assessment processes.

B) The purpose of Pillar 2 is to encourage market discipline through an information disclosure framework covering capital, capital adequacy, risk exposures and risk assessment processes.

C) The purpose of Pillar 3 is to encourage market discipline through an information disclosure framework covering capital, capital adequacy, risk exposures and risk assessment processes.

D) None of the listed options are correct.

A) The purpose of Pillar 1 is to encourage market discipline through an information disclosure framework covering capital, capital adequacy, risk exposures and risk assessment processes.

B) The purpose of Pillar 2 is to encourage market discipline through an information disclosure framework covering capital, capital adequacy, risk exposures and risk assessment processes.

C) The purpose of Pillar 3 is to encourage market discipline through an information disclosure framework covering capital, capital adequacy, risk exposures and risk assessment processes.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

37

Choose the correct statement:

A) For DIs adopting advanced approaches to risk measurement, APRA requires the use of models that capture 'economic capital'.

B) For DIs adopting standardised approaches to risk measurement, APRA requires the use of models that capture 'economic capital'.

C) For DIs adopting combination approaches to risk measurement, APRA requires the use of models that capture 'economic capital'

D) None of the listed options are correct.

A) For DIs adopting advanced approaches to risk measurement, APRA requires the use of models that capture 'economic capital'.

B) For DIs adopting standardised approaches to risk measurement, APRA requires the use of models that capture 'economic capital'.

C) For DIs adopting combination approaches to risk measurement, APRA requires the use of models that capture 'economic capital'

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

38

Common equity Tier 1 is:

A) made up discretionary non-cumulative dividends or coupons that have neither a maturity date nor an incentive to redeem.

B) used to provide loss absorption on a going-concern basis and must be subordinated to depositors and general creditors and an original maturity of at least five years.

C) subordinated to all other types of funding, absorbs losses, has full flexibility of dividend payments and has no maturity date.

D) None of the listed options are correct.

A) made up discretionary non-cumulative dividends or coupons that have neither a maturity date nor an incentive to redeem.

B) used to provide loss absorption on a going-concern basis and must be subordinated to depositors and general creditors and an original maturity of at least five years.

C) subordinated to all other types of funding, absorbs losses, has full flexibility of dividend payments and has no maturity date.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

39

Retained earnings are:

A) the accumulated value of past profits not yet paid out in dividends to shareholders.

B) the face value of the ordinary shares issued by the FI.

C) a special reserve set aside out of retained earnings to meet expected and actual losses on the portfolio.

D) the difference between the price the public paid for common stock or shares when originally offered and their par values times the number of shares outstanding.

A) the accumulated value of past profits not yet paid out in dividends to shareholders.

B) the face value of the ordinary shares issued by the FI.

C) a special reserve set aside out of retained earnings to meet expected and actual losses on the portfolio.

D) the difference between the price the public paid for common stock or shares when originally offered and their par values times the number of shares outstanding.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

40

Market risk is made up of:

A) risk of companies on the stock exchange and political risk.

B) general market risk and specific market risk.

C) pure risk and speculative risk.

D) inflation risk and interest rate risk.

A) risk of companies on the stock exchange and political risk.

B) general market risk and specific market risk.

C) pure risk and speculative risk.

D) inflation risk and interest rate risk.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

41

Within the framework of Pillar I, which Basel Accord introduced two capital buffers: a capital conservation buffer and a countercyclical capital buffer?

A) Basel I.

B) Basel II.

C) Basel 2.5.

D) Basel III.

A) Basel I.

B) Basel II.

C) Basel 2.5.

D) Basel III.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

42

Tier 1 capital is used to provide loss absorption on a gone-concern basis and must be subordinated to depositors and general creditors and an original maturity of at least five years.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

43

The capital conservation buffer is _______ of risk-weighted assets, comprised of _______ only:

A) 2.5 per cent, common equity Tier 1 only.

B) 2.5 per cent, Tier 1 only.

C) 7.5 per cent, common equity Tier 1 only.

D) 7.5 per cent, Tier 1 only.

A) 2.5 per cent, common equity Tier 1 only.

B) 2.5 per cent, Tier 1 only.

C) 7.5 per cent, common equity Tier 1 only.

D) 7.5 per cent, Tier 1 only.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

44

Basel III's development and implementation has been driven by G20 countries following the global financial crisis and will include:

A) capital conservation buffers and pro-cyclical buffers.

B) increased capital requirements which can be met by holding more primary and secondary capital.

C) global liquidity and funding standards and higher quality of capital.

D) an increase in the maximum capital requirements.

A) capital conservation buffers and pro-cyclical buffers.

B) increased capital requirements which can be met by holding more primary and secondary capital.

C) global liquidity and funding standards and higher quality of capital.

D) an increase in the maximum capital requirements.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

45

The market risk capital charge is included in capital regulations as regulators recognise that changes in market value can impact on a FI's insolvency risk.

A) Market risk takes into account general market risk, specific market risk and operational risk.

B) FIs with APRA approval can use a combination approach with all risk categories and across all regions.

C) APRA can increase or decrease capital requirements from the internal model if it considers that it doesn't reflect fully the FI's market risk profile.

D) All of the listed options are correct.

A) Market risk takes into account general market risk, specific market risk and operational risk.

B) FIs with APRA approval can use a combination approach with all risk categories and across all regions.

C) APRA can increase or decrease capital requirements from the internal model if it considers that it doesn't reflect fully the FI's market risk profile.

D) All of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

46

Counterparty credit risk is the risk that the other side of a contract will default on payment obligation, whereby 'the other side' is always the FI.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

47

Pillar 3 of APRA's supervision framework is to encourage market discipline through an information disclosure framework. Pillar 3 requires:

A) qualitative disclosures for capital structure, capital adequacy and risk exposure.

B) quantitative disclosures for capital structure, capital adequacy and risk exposure.

C) comparison of the risk exposure, capital inadequacy and capital structure for FIs.

D) quantitative disclosures for risk management processes.

A) qualitative disclosures for capital structure, capital adequacy and risk exposure.

B) quantitative disclosures for capital structure, capital adequacy and risk exposure.

C) comparison of the risk exposure, capital inadequacy and capital structure for FIs.

D) quantitative disclosures for risk management processes.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

48

Under Basel II, all standard residential mortgages attract a risk weight of 35 per cent.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

49

Choose the correct statement:

A) Any Pillar 2 adjustment between the DI and APRA is made public to ensure investors are aware of the DI's current position.

B) Any Pillar 2 adjustment is confidential between the DI and APRA to avoid any adverse signalling effects.

C) Any Pillar 2 adjustment is confidential between the DI and APRA, only if the DI does not want to disclose the adjustment.

D) Any Pillar 2 adjustment between the DI and APRA is withheld for six weeks.

A) Any Pillar 2 adjustment between the DI and APRA is made public to ensure investors are aware of the DI's current position.

B) Any Pillar 2 adjustment is confidential between the DI and APRA to avoid any adverse signalling effects.

C) Any Pillar 2 adjustment is confidential between the DI and APRA, only if the DI does not want to disclose the adjustment.

D) Any Pillar 2 adjustment between the DI and APRA is withheld for six weeks.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

50

Choose the correct statement:

A) The countercyclical capital buffer has a microeconomic focus and aims to ensure that financial system capital requirements are sufficient given the political environment in which DIs operate.

B) The countercyclical capital buffer has a political focus and aims to ensure that financial system capital requirements are sufficient given the economic environment in which DIs operate.

C) The countercyclical capital buffer has a macroeconomic focus and aims to ensure that financial system capital requirements are sufficient given the macro-financial environment in which DIs operate.

D) None of the listed options are correct.

A) The countercyclical capital buffer has a microeconomic focus and aims to ensure that financial system capital requirements are sufficient given the political environment in which DIs operate.

B) The countercyclical capital buffer has a political focus and aims to ensure that financial system capital requirements are sufficient given the economic environment in which DIs operate.

C) The countercyclical capital buffer has a macroeconomic focus and aims to ensure that financial system capital requirements are sufficient given the macro-financial environment in which DIs operate.

D) None of the listed options are correct.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

51

The regulation required under Basel II is more costly than that required under Basel III, due to the higher liquid assets requirements and the higher levels of primary capital.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

52

In the standardised approach to operational risk capital, FI's are required to map their overall gross income into eight business lines that are pre-determined by the bank regulator.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

53

Which pillar of the Basel Accord requires quantitative disclosures for capital structure, capital adequacy and risk exposure so market participants are able to undertake a meaningful comparison of DIs and their risk-based performance?

A) Pillar 1

B) Pillar 2

C) Pillar 3

D) all pillars

A) Pillar 1

B) Pillar 2

C) Pillar 3

D) all pillars

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

54

The book value of an asset or liability is the value reported according to the historical cost of the asset or liability.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following statements is true?

A) Basel II broadened measures for measurement of capital and introduced the concept of two pillars to protect solvency of individual FIs whereas Basel III introduced liquidity and higher capital levels to protect the financial system in general.

B) APRA introduced an enhanced Basel II called Basel 2.5 with new provisions that were difficult for Australian FIs to meet in the short term.

C) Basel II set targets that were commensurate with the risk profile and environment in an endeavour to protect solvency of individual FIs whereas Basel III introduced liquidity and higher capital levels to protect the financial system in general.

D) Basel III changes to capital requirements requires higher secondary capital levels to be held by FIs.

A) Basel II broadened measures for measurement of capital and introduced the concept of two pillars to protect solvency of individual FIs whereas Basel III introduced liquidity and higher capital levels to protect the financial system in general.

B) APRA introduced an enhanced Basel II called Basel 2.5 with new provisions that were difficult for Australian FIs to meet in the short term.

C) Basel II set targets that were commensurate with the risk profile and environment in an endeavour to protect solvency of individual FIs whereas Basel III introduced liquidity and higher capital levels to protect the financial system in general.

D) Basel III changes to capital requirements requires higher secondary capital levels to be held by FIs.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

56

The leverage ratio is calculated as assets divided by core capital.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

57

Basel III introduced significant capital reforms including measures to raise the quality and minimum required levels of capital and establish a back-up leverage ratio.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

58

The calculation of the risk-adjusted asset values of OBS market contracts:

A) nearly always equals zero because the exchange over which the contract initially traded assumes all of the risk.

B) requires multiplication of the credit equivalent amounts by the appropriate risk weights and includes all OBS transactions.

C) requires the calculation of a conversion factor to create credit equivalent amounts for all OBS transactions.

D) requires multiplication of the credit equivalent amounts by the appropriate risk weights and the calculation of a conversion factor to create credit equivalent amounts

A) nearly always equals zero because the exchange over which the contract initially traded assumes all of the risk.

B) requires multiplication of the credit equivalent amounts by the appropriate risk weights and includes all OBS transactions.

C) requires the calculation of a conversion factor to create credit equivalent amounts for all OBS transactions.

D) requires multiplication of the credit equivalent amounts by the appropriate risk weights and the calculation of a conversion factor to create credit equivalent amounts

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

59

Basel III has introduced the first set of global liquidity regulations.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

60

To calculate the operational risk capital charge, the DI's activities are first divided into:

A) investment banking, commercial banking and 'all other activity'.

B) commercial lending, retail lending and 'all other activity'.

C) derivative trading, foreign exchange trading and 'all other activity'.

D) retail banking, commercial banking and 'all other activity'.

A) investment banking, commercial banking and 'all other activity'.

B) commercial lending, retail lending and 'all other activity'.

C) derivative trading, foreign exchange trading and 'all other activity'.

D) retail banking, commercial banking and 'all other activity'.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

61

Identify the main functions of an FI's capital and differentiate between Tier 1 and Tier 2 capital.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

62

Basel II established minimum capital requirements, procedures to ensure that sound internal process are used to assess capital adequacy and set targets that were commensurate with the risk profile and environment in an endeavour to protect solvency of individual FIs. Basel III introduced liquidity and higher capital levels to protect the financial system in general.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

63

Why is a regulatory capital charge against operational risk necessary?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

64

What are the major differences between the Basel I and the Basel II approaches to capital regulation?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

65

In determining the risk-adjusted value of the on-balance-sheet credit equivalent amounts of the contingent guaranty contracts, the risk weights are determined by the credit rating of the underlying counterparty of the off-balance-sheet activity.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

66

Credit-risk-adjusted assets are on- and off-balance-sheet assets whose values are adjusted for approximate credit risk.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 66 flashcards in this deck.