Deck 15: Auditing the Financing Investing Process: Long-Term Liabilities Stockholders Equity and Income Statement Accounts

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

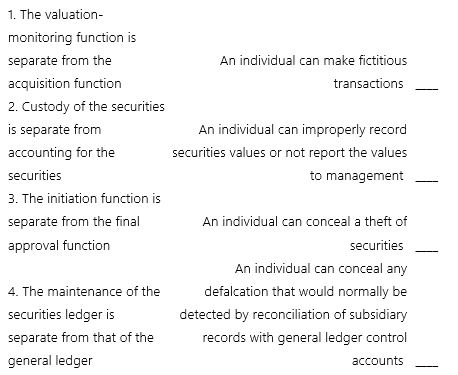

Match each of the following controls with the assertion for long-term debt that it supports.

Question

Match the balance sheet account with the income statement account that is typically audited at the same time.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 15: Auditing the Financing Investing Process: Long-Term Liabilities Stockholders Equity and Income Statement Accounts

1

The repurchase of stock includes the reacquisition of stock (treasury stock), but not the retirement of stock.

False

2

The auditor can best verify an entity's bond sinking fund transactions and year-end balance by

A) Recomputation of interest expense, interest payable, and amortization of bond discount or premium.

B) Confirmation with individual holders of retired bonds.

C) Confirmation with the bond trustee.

D) Examination and count of the bonds retired during the year.

A) Recomputation of interest expense, interest payable, and amortization of bond discount or premium.

B) Confirmation with individual holders of retired bonds.

C) Confirmation with the bond trustee.

D) Examination and count of the bonds retired during the year.

C

3

When auditing capital stock accounts, the cutoff assertion is the most important to consider.

False

4

The primary reason for preparing a reconciliation between interest-bearing obligations outstanding during the year and interest expense presented in the financial statements is to

A) Evaluate internal control over securities.

B) Determine the validity of prepaid interest expense.

C) Ascertain the reasonableness of imputed interest.

D) Detect unrecorded liabilities.

A) Evaluate internal control over securities.

B) Determine the validity of prepaid interest expense.

C) Ascertain the reasonableness of imputed interest.

D) Detect unrecorded liabilities.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

One major issue associated with long-term debt is the classification of the short-term portion of long-term debt that is due in the next year.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

The occurrence assertion is being tested when the auditor vouches stock repurchases to the canceled stock certificates.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

The auditor's program for the examination of long-term debt should include steps that require the

A) Verification of the existence of the bond holders.

B) Examination of any bond agreement.

C) Inspection of the accounts payable subsidiary ledger.

D) Investigation of credits to the bond interest income account.

A) Verification of the existence of the bond holders.

B) Examination of any bond agreement.

C) Inspection of the accounts payable subsidiary ledger.

D) Investigation of credits to the bond interest income account.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

The registrar is responsible for preparing stock certificates and maintaining adequate stockholders' records.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

Income statement accounts must be accounted for in accordance with GAAP.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

The auditor typically begins an audit of retained earnings by obtaining a schedule of account activity for the period.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

Generally, all dividends that are declared and paid will be audited.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

Long-term borrowing should be properly authorized.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

The dividend-disbursing agent prepares and mails dividends checks to the stockholders as of the date of declaration.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

There are typically only a couple of disclosure items that need to be considered for stockholders' equity.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

Notes receivable is a common type of long-term financing.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

A control which ensures that long-term borrowing is properly initiated by appropriate individuals addresses the control assertion of

A) Occurrence.

B) Authorization.

C) Completeness.

D) Valuation.

A) Occurrence.

B) Authorization.

C) Completeness.

D) Valuation.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

For most companies, stockholders' equity includes the following three accounts: preferred stock, paid-in capital, and retained earnings.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

Three types of transactions usually occur in stockholders' equity: issuance of stock, repurchase of stock, and payment of dividends.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

Several years ago, Conway, Inc., secured a conventional real estate mortgage loan. Which of the following audit procedures would least likely be performed by an auditor examining the mortgage balance?

A) Examine the current year's canceled checks.

B) Review the mortgage amortization schedule.

C) Inspect public records of lien balances.

D) Recompute mortgage interest expense.

A) Examine the current year's canceled checks.

B) Review the mortgage amortization schedule.

C) Inspect public records of lien balances.

D) Recompute mortgage interest expense.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

Substantive analytical procedures can be used extensively to test revenue and expense accounts.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

During an audit, Wicks learns that the entity was granted a 3-month waiver of the repayment of principal on the installment loan with Blank Bank without an extension of the maturity date, which is one year in the future. With respect to this loan, the audit program used by Wicks is least likely to include a verification of the

A) Interest expense for the year.

B) Balloon payment.

C) Total liability at year-end.

D) Installment loan payments.

A) Interest expense for the year.

B) Balloon payment.

C) Total liability at year-end.

D) Installment loan payments.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

Valuation and allocation is most likely an issue for long-term debt if

A) Bonds are sold on the open market.

B) Bonds are issued at a discount or premium.

C) The loans are from banks.

D) The company has many short-term leases.

A) Bonds are sold on the open market.

B) Bonds are issued at a discount or premium.

C) The loans are from banks.

D) The company has many short-term leases.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

In the audit of a medium-sized manufacturing concern, which one of the following areas can be expected to require the least amount of audit time?

A) Retained earnings.

B) Revenue.

C) Assets.

D) Liabilities.

A) Retained earnings.

B) Revenue.

C) Assets.

D) Liabilities.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

An auditor compares revenues and expenses reported for the year being audited (current year) with those of the prior year and investigates all changes exceeding 10%. By this procedure, the auditor would be most likely to learn that

A) An increase in property tax rates has not been recognized in the entity's accrual.

B) The current year provision for uncollectible accounts is inadequate, because of worsening economic conditions.

C) Fourth quarter payroll taxes were not paid.

D) The entity changed its capitalization policy for small tools in the current year.

A) An increase in property tax rates has not been recognized in the entity's accrual.

B) The current year provision for uncollectible accounts is inadequate, because of worsening economic conditions.

C) Fourth quarter payroll taxes were not paid.

D) The entity changed its capitalization policy for small tools in the current year.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

Reviewing interest expense to examine payments to debt holders not listed on the debt analysis schedule is a procedure that can be used to test the audit assertion of

A) Occurrence.

B) Completeness.

C) Cutoff.

D) Accuracy.

A) Occurrence.

B) Completeness.

C) Cutoff.

D) Accuracy.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

During the year under audit, a company has completed a private placement of a substantial amount of bonds. Which of the following is the most important step in the auditor's program for the audit of bonds payable?

A) Confirming the interest rate with the bond trustee.

B) Tracing the cash received from the issue to the accounting records.

C) Examining the bond agreement for a sinking fund provision.

D) Recomputing the annual interest cost and the effective yield.

A) Confirming the interest rate with the bond trustee.

B) Tracing the cash received from the issue to the accounting records.

C) Examining the bond agreement for a sinking fund provision.

D) Recomputing the annual interest cost and the effective yield.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

An auditor usually obtains evidence of stockholders' equity transactions by reviewing the entity's

A) Minutes of the board of directors' meetings.

B) Transfer agent's records.

C) Canceled stock certificates.

D) Treasury stock certificate book.

A) Minutes of the board of directors' meetings.

B) Transfer agent's records.

C) Canceled stock certificates.

D) Treasury stock certificate book.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

During an examination of a public company, the auditor should obtain written confirmation regarding bond transactions from the

A) Bond broker.

B) Entity's attorney.

C) Internal auditors.

D) Trustee.

A) Bond broker.

B) Entity's attorney.

C) Internal auditors.

D) Trustee.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

A company issued bonds for cash during the year under audit. To ascertain that this transaction was properly recorded, the auditor's best course of action is to

A) Request a statement from the bond trustee as to the amount of the bonds issued and outstanding.

B) Confirm the results of the issuance with the underwriter or investment banker.

C) Trace the cash received from the issuance to the accounting records.

D) Verify that the net cash received is credited to an account entitled "Bonds Payable."

A) Request a statement from the bond trustee as to the amount of the bonds issued and outstanding.

B) Confirm the results of the issuance with the underwriter or investment banker.

C) Trace the cash received from the issuance to the accounting records.

D) Verify that the net cash received is credited to an account entitled "Bonds Payable."

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

All corporate capital stock transactions should ultimately be traced to the

A) Minutes of the board of directors.

B) Cash receipts journal.

C) Cash disbursements journal.

D) Numbered stock certificates.

A) Minutes of the board of directors.

B) Cash receipts journal.

C) Cash disbursements journal.

D) Numbered stock certificates.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

If recorded interest expense is higher than the auditor's expectation calculated using recorded debt, all of the following are potential explanations except that

A) The entity failed to record debt.

B) Debt was recorded as equity.

C) The entity used the face interest rate to calculate interest expense on a bond issued at a discount.

D) The entity used the face interest rate to calculate interest expense on a bond issued at a premium.

A) The entity failed to record debt.

B) Debt was recorded as equity.

C) The entity used the face interest rate to calculate interest expense on a bond issued at a discount.

D) The entity used the face interest rate to calculate interest expense on a bond issued at a premium.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

Reviewing notes paid or renewed after the balance sheet date to determine if there are unrecorded liabilities at year-end can be used to test the assertion of

A) Existence.

B) Completeness.

C) Rights and obligations.

D) Valuation and allocation.

A) Existence.

B) Completeness.

C) Rights and obligations.

D) Valuation and allocation.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

In auditing long-term bonds payable, an auditor most likely would

A) Perform analytical procedures on the bond premium and discount accounts.

B) Examine documentation of assets purchased with bond proceeds for liens.

C) Compare interest expense with the bonds payable amount for reasonableness.

D) Confirm the existence of individual bond holders at year-end.

A) Perform analytical procedures on the bond premium and discount accounts.

B) Examine documentation of assets purchased with bond proceeds for liens.

C) Compare interest expense with the bonds payable amount for reasonableness.

D) Confirm the existence of individual bond holders at year-end.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

Which audit procedure is most closely related to management's assertion regarding presentation and disclosure of liabilities?

A) Tracing cash received from a bond issue to the accounting records.

B) Confirmation with the bond trustee of amounts owed on a private placement of bonds.

C) Reviewing the renewal of a note payable immediately after the balance sheet.

D) Inspection of public records of lien balances.

A) Tracing cash received from a bond issue to the accounting records.

B) Confirmation with the bond trustee of amounts owed on a private placement of bonds.

C) Reviewing the renewal of a note payable immediately after the balance sheet.

D) Inspection of public records of lien balances.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

During its fiscal year, a company issued, at a discount, a substantial amount of bonds. When performing audit work in connection with the bond issue, the independent auditor should

A) Confirm the existence of the bond holders.

B) Review the board of directors' minutes for authorization.

C) Trace the net cash received from the issuance to the bond payable account.

D) Inspect the records maintained by the bond trustee.

A) Confirm the existence of the bond holders.

B) Review the board of directors' minutes for authorization.

C) Trace the net cash received from the issuance to the bond payable account.

D) Inspect the records maintained by the bond trustee.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

The auditor is concerned with establishing that dividends are paid to stockholders of the entity owning stock as of the

A) Issue date.

B) Declaration date.

C) Record date.

D) Payment date.

A) Issue date.

B) Declaration date.

C) Record date.

D) Payment date.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

During the course of an audit, a CPA's substantive analytical procedure provides an expected interest expense that is significantly higher than the amount recorded in the entity's accounting records. This observation would most likely lead the auditor to suspect that

A) The entity failed to record all debt.

B) Discount on Bonds is misstated.

C) Interest income is overstated.

D) The entity failed to record all interest expense.

A) The entity failed to record all debt.

B) Discount on Bonds is misstated.

C) Interest income is overstated.

D) The entity failed to record all interest expense.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

In connection with the examination of bonds payable, an auditor would expect to find in a bond agreement

A) The issue date and maturity date of the bond.

B) The names of the original subscribers to the bond issue.

C) The yield to maturity of the bonds issued.

D) The company's debt-to-equity ratio at the time of issuance.

A) The issue date and maturity date of the bond.

B) The names of the original subscribers to the bond issue.

C) The yield to maturity of the bonds issued.

D) The company's debt-to-equity ratio at the time of issuance.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

A substantive strategy is typically used to audit stockholders' equity because

A) The number of transactions is small.

B) Controls over stockholders' equity transactions typically are weak.

C) A reliance strategy is most efficient.

D) A substantive strategy likely was used in prior years.

A) The number of transactions is small.

B) Controls over stockholders' equity transactions typically are weak.

C) A reliance strategy is most efficient.

D) A substantive strategy likely was used in prior years.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

The auditor gathers evidence about dividends that are declared and paid primarily because of

A) Concerns with violations of corporate bylaws or debt covenants.

B) The large dollar value of the transactions.

C) The ease with which the transactions can be audited.

D) Fraud concerns.

A) Concerns with violations of corporate bylaws or debt covenants.

B) The large dollar value of the transactions.

C) The ease with which the transactions can be audited.

D) Fraud concerns.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

Before expressing an opinion concerning the results of operations, the auditor would most likely proceed with the examination of the income statement by

A) Applying a rigid measurement standard designed to test for understatement of net income.

B) Analyzing the beginning and ending balance sheet inventory amounts.

C) Making net income comparisons to published industry trends and ratios.

D) Examining income statement accounts concurrently with the related balance sheet accounts.

A) Applying a rigid measurement standard designed to test for understatement of net income.

B) Analyzing the beginning and ending balance sheet inventory amounts.

C) Making net income comparisons to published industry trends and ratios.

D) Examining income statement accounts concurrently with the related balance sheet accounts.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following is the most important consideration of an auditor when examining the stockholders' equity section of an entity's balance sheet?

A) Changes in the capital stock account are verified by an independent stock transfer agent.

B) Stock dividends and/or stock splits during the year under audit were approved by the stockholders.

C) Stock dividends are capitalized at par or stated value on the dividend declaration date.

D) Entries in the capital stock account can be traced to a resolution in the minutes of the board of directors' meetings.

A) Changes in the capital stock account are verified by an independent stock transfer agent.

B) Stock dividends and/or stock splits during the year under audit were approved by the stockholders.

C) Stock dividends are capitalized at par or stated value on the dividend declaration date.

D) Entries in the capital stock account can be traced to a resolution in the minutes of the board of directors' meetings.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

During the course of an audit, a CPA observes that the recorded interest expense seems to be excessive in relation to the balance in the long-term debt account. This observation could lead the auditor to suspect that

A) Long-term debt is understated.

B) Discount on bonds payable is overstated.

C) Long-term debt is overstated.

D) Premium on bonds payable is understated.

A) Long-term debt is understated.

B) Discount on bonds payable is overstated.

C) Long-term debt is overstated.

D) Premium on bonds payable is understated.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following transactions is an auditor most likely to examine when auditing the retained earnings account?

A) Changing from one method of depreciation to another.

B) Adjusting the percentage used to estimate the allowance for doubtful accounts.

C) Changing from the FIFO to LIFO method of inventory valuation.

D) Correcting an error in depreciation in a prior year.

A) Changing from one method of depreciation to another.

B) Adjusting the percentage used to estimate the allowance for doubtful accounts.

C) Changing from the FIFO to LIFO method of inventory valuation.

D) Correcting an error in depreciation in a prior year.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

Which audit procedure is most closely related to management's assertions about the presentation and disclosure of stockholders' equity?

A) Determining whether restrictions have been imposed on retained earnings.

B) Counting treasury stock certificates.

C) Inspecting minutes of the board of directors to verify that cash dividends were declared.

D) Establishing that treasury stock is valued at cost.

A) Determining whether restrictions have been imposed on retained earnings.

B) Counting treasury stock certificates.

C) Inspecting minutes of the board of directors to verify that cash dividends were declared.

D) Establishing that treasury stock is valued at cost.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

Two months before year-end, the bookkeeper erroneously recorded the receipt of a long-term bank loan by a debit to cash and a credit to sales. Which of the following is the most effective procedure for detecting this type of error?

A) Analysis of the notes payable journal.

B) Analysis of bank confirmation information.

C) Preparation of a year-end bank reconciliation.

D) Preparation of a year-end bank transfer schedule.

A) Analysis of the notes payable journal.

B) Analysis of bank confirmation information.

C) Preparation of a year-end bank reconciliation.

D) Preparation of a year-end bank transfer schedule.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

Give an example of how the audit of income statement accounts could be affected by results of audit work done in other areas of the audit.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

Examining cancelled stock certificates addresses the assertion of

A) Occurrence.

B) Disclosures.

C) Valuation.

D) Completeness.

A) Occurrence.

B) Disclosures.

C) Valuation.

D) Completeness.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

Erik Rekdahl, senior-in-charge, is auditing Koonce Katfood, Inc.'s, long-term debt for the year ended December 31. Long-term debt is composed of two bond issues, which are due in 10 and 15 years, respectively. The debt is held by two insurance companies. Rekdahl has examined the bond agreements for each issue. The agreements provide that if Koonce fails to comply with the covenants of the contract, the debt becomes payable immediately. Rekdahl identified the following covenants when reviewing the bond agreements:

"The debtor company shall endeavor to maintain a working capital ratio of 2 to 1 at all times, and in any fiscal year following a failure to maintain said ratio, the company shall restrict compensation of officers to a total of $650,000. Officers include the chairperson of the board and the president."

"The debtor company shall keep all property that is security for these debt agreements insured against loss by fire to the extent of 100 percent of its actual value. Policies of insurance comprising this protection shall be filed with the trustee."

"The company is required to restrict 40 percent of retained earnings from availability for paying dividends."

"A sinking fund shall be established with the First Morgan Bank of Austin, and semiannual payments of $500,000 shall be deposited in the fund. The bank may, at its discretion, purchase bonds from either issue."

a. Provide any audit steps that Rekdahl should conduct to determine if the company is in compliance with the bond indentures.

b. List any reporting requirements that the financial statements or footnotes should include.

"The debtor company shall endeavor to maintain a working capital ratio of 2 to 1 at all times, and in any fiscal year following a failure to maintain said ratio, the company shall restrict compensation of officers to a total of $650,000. Officers include the chairperson of the board and the president."

"The debtor company shall keep all property that is security for these debt agreements insured against loss by fire to the extent of 100 percent of its actual value. Policies of insurance comprising this protection shall be filed with the trustee."

"The company is required to restrict 40 percent of retained earnings from availability for paying dividends."

"A sinking fund shall be established with the First Morgan Bank of Austin, and semiannual payments of $500,000 shall be deposited in the fund. The bank may, at its discretion, purchase bonds from either issue."

a. Provide any audit steps that Rekdahl should conduct to determine if the company is in compliance with the bond indentures.

b. List any reporting requirements that the financial statements or footnotes should include.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

Identify the three major types of transactions that occur in stockholders' equity.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

Overall analysis of income statement accounts may bring to light errors, omissions, and inconsistencies not disclosed in the overall analysis of balance sheet accounts. The income statement analysis can best be accomplished by comparing monthly

A) Income statement ratios to balance sheet ratios.

B) Revenue and expense account balances to the monthly reported net income.

C) Income statement ratios to published industry averages.

D) Revenue and expense account totals to the corresponding figures of the preceding years.

A) Income statement ratios to balance sheet ratios.

B) Revenue and expense account balances to the monthly reported net income.

C) Income statement ratios to published industry averages.

D) Revenue and expense account totals to the corresponding figures of the preceding years.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

You have been assigned the duty of auditing long-term debt and retained earnings for Keys, Inc. Describe the tests you would use to support management's assertions regarding disclosure for these accounts.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

An audit program for the examination of the retained earnings account should include a step that requires verification of the

A) Gain or loss resulting from disposition of treasury shares.

B) Market value used to charge retained earnings to account for a two-for-one stock split.

C) Authorization for both cash and stock dividends.

D) Approval of the adjustment to the beginning balance as a result of a write-down of an account receivable.

A) Gain or loss resulting from disposition of treasury shares.

B) Market value used to charge retained earnings to account for a two-for-one stock split.

C) Authorization for both cash and stock dividends.

D) Approval of the adjustment to the beginning balance as a result of a write-down of an account receivable.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

For each of the following substantive procedures, first note whether it is a test of details of transactions or a test of details of account balances. Then decide for which assertion the test provides the best evidence.

1. Trace large cash receipts and payments to the source documents and the general ledger.

2. Examine copies of note and bond agreements.

3. Recompute accrued interest payable.

4. Review debt activity for a few days before and after year-end to determine whether transactions are included in the proper period.

5. Examine due dates on notes and bonds for proper classification between current and long term debt.

1. Trace large cash receipts and payments to the source documents and the general ledger.

2. Examine copies of note and bond agreements.

3. Recompute accrued interest payable.

4. Review debt activity for a few days before and after year-end to determine whether transactions are included in the proper period.

5. Examine due dates on notes and bonds for proper classification between current and long term debt.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

Many of Granada Corporation's convertible bond holders have converted their bonds into stock during the year under examination. The independent auditor should review Granada Corporation's statement of cash flows to ascertain that it shows

A) Only cash used to reduce convertible debt.

B) Only cash provided by issuance of stock.

C) Cash provided by the issuance of stock and used to reduce convertible debt.

D) Nothing relating to the conversion because it does not affect cash.

A) Only cash used to reduce convertible debt.

B) Only cash provided by issuance of stock.

C) Cash provided by the issuance of stock and used to reduce convertible debt.

D) Nothing relating to the conversion because it does not affect cash.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

In performing tests concerning the granting of stock options, an auditor should

A) Confirm the transaction with the Secretary of State in the state of incorporation.

B) Verify the existence of option holders in the entity's payroll records or stock ledgers.

C) Determine that sufficient treasury stock is available to cover any new stock issued.

D) Trace the authorization for the transaction to a vote of the board of directors.

A) Confirm the transaction with the Secretary of State in the state of incorporation.

B) Verify the existence of option holders in the entity's payroll records or stock ledgers.

C) Determine that sufficient treasury stock is available to cover any new stock issued.

D) Trace the authorization for the transaction to a vote of the board of directors.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

Where no independent stock transfer agents are employed and the corporation issues its own stocks and maintains stock records, canceled stock certificates should

A) Be defaced to prevent reissuance and attached to their corresponding stubs.

B) Not be defaced, but segregated from other stock certificates and retained in a canceled certificates file.

C) Be destroyed to prevent fraudulent reissuance.

D) Be defaced and sent to the Secretary of State.

A) Be defaced to prevent reissuance and attached to their corresponding stubs.

B) Not be defaced, but segregated from other stock certificates and retained in a canceled certificates file.

C) Be destroyed to prevent fraudulent reissuance.

D) Be defaced and sent to the Secretary of State.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

Identify the four major assertions made regarding stockholders' equity and describe one control activity for each.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

Of the following, which is the most important procedure that an auditor should use when making an overall review of the income statement?

A) Select sales and expense items and trace amounts to related supporting documents.

B) Compare actual revenues and expenses with the corresponding figures of the previous year and investigate significant differences.

C) Obtain, from the proper entity representative, inventory certificates for the beginning and ending inventory amounts that were used to determine cost of sales.

D) Ascertain that the net income amount in the statement of cash flows agrees with the net income amount in the income statement.

A) Select sales and expense items and trace amounts to related supporting documents.

B) Compare actual revenues and expenses with the corresponding figures of the previous year and investigate significant differences.

C) Obtain, from the proper entity representative, inventory certificates for the beginning and ending inventory amounts that were used to determine cost of sales.

D) Ascertain that the net income amount in the statement of cash flows agrees with the net income amount in the income statement.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

An audit of stockholders' equity ordinarily should include

A) Tracing individual dividend payments to the capital stock records.

B) Reviewing minutes of board meetings to determine the number of shares outstanding.

C) Confirming shares outstanding with state officials.

D) Determining that dividend declarations comply with debt agreements.

A) Tracing individual dividend payments to the capital stock records.

B) Reviewing minutes of board meetings to determine the number of shares outstanding.

C) Confirming shares outstanding with state officials.

D) Determining that dividend declarations comply with debt agreements.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

Match each of the following controls with the assertion for long-term debt that it supports.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

Match the balance sheet account with the income statement account that is typically audited at the same time.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

What kind of information would typically be found on an income statement account analysis working paper? What kind of tests can an auditor perform using this information? Why would an auditor conduct additional analysis on an income statement account?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.