Deck 23: Further Consolidation Issues III: Accounting for Indirect Ownership Interest

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

The following diagram represents the ownership of issued share capital of the companies in a group.What is the ownership interest of A Ltd in D Ltd?

A)50%

B)96.5%

C)68%

D)80%

A)50%

B)96.5%

C)68%

D)80%

Question

Question

Question

Question

Question

Question

Question

The following diagram represents the ownership of issued share capital of the companies in a group.What is the ownership interest of A Ltd in D Ltd?

A)83.4%

B)76.6%

C)100%

D)86%

A)83.4%

B)76.6%

C)100%

D)86%

Question

Question

The following diagram represents the ownership of issued share capital of the companies in a group.What is the total outside equity interest in D Ltd?

A)20%

B)33.6%

C)60%

D)24.8%

A)20%

B)33.6%

C)60%

D)24.8%

Question

Question

Question

The following diagram represents the ownership of issued share capital of the companies in a group.What is the total outside equity interest in D Ltd?

A)14%

B)10%

C)30%

D)22%

A)14%

B)10%

C)30%

D)22%

Question

Question

Question

Question

Question

Question

Question

Question

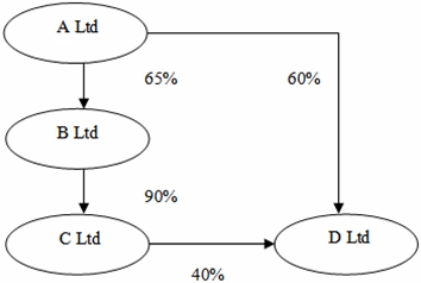

The following diagram represents the ownership of issued share capital of the companies in a group.  What is the direct parent entity interest and direct non-controlling interest in D Ltd,respectively?

What is the direct parent entity interest and direct non-controlling interest in D Ltd,respectively?

A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; zero

What is the direct parent entity interest and direct non-controlling interest in D Ltd,respectively?A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; zero

Question

Question

Question

Question

Question

Question

The following diagram represents the ownership of issued share capital of the companies in a group.  What is the indirect parent entity interest and indirect non-controlling interest in D Ltd,respectively?

What is the indirect parent entity interest and indirect non-controlling interest in D Ltd,respectively?

A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; 40%

What is the indirect parent entity interest and indirect non-controlling interest in D Ltd,respectively?A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; 40%

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/46

Play

Full screen (f)

Deck 23: Further Consolidation Issues III: Accounting for Indirect Ownership Interest

1

A Plc owns 80% of the issued capital of B Plc and B Plc owns 60% of the issued capital of C Plc.What is A's interest in C Plc?

A)32%

B)48%

C)60%

D)16%

A)32%

B)48%

C)60%

D)16%

B

2

The order of acquisition of subsidiaries (i.e.sequential or non-sequential)is of no consequence when it comes to calculating non-controlling interests; they are calculated the same way regardless of the order.

False

3

Control means the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

True

4

In calculating indirect non-controlling interests,intragroup transactions need not be eliminated.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

5

An ultimate parent entity may obtain a controlling indirect interest in another entity as a result of holding a controlling interest in the immediate parent entity of that other entity.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

6

The elimination of the parent entity's investment in a subsidiary will be done by eliminating the investment against the parent entity's direct and indirect ownership interest in pre-acquisition share capital and reserves.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

7

It is possible for aggregated direct and indirect non-controlling interests in an entity to be a greater percentage of ownership than the parent's aggregated direct and indirect ownership interests.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

8

The following diagram represents the ownership of issued share capital of the companies in a group.What is the ownership interest of A Ltd in D Ltd?

A)50%

B)96.5%

C)68%

D)80%

A)50%

B)96.5%

C)68%

D)80%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

9

Non-controlling indirect interests are entitled to receive dividends in a subsidiary.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

10

The non-controlling interest in post-acquisition movement in reserves and post-acquisition profits is based on the combined sum of both direct non-controlling interest and indirect non-controlling interest.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

11

When a parent acquires its interest in an intermediate subsidiary after the intermediate subsidiary acquires an interest its own subsidiary,this is referred to as a non-sequential acquisition.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

12

The non-controlling interest in post-acquisition capital and reserves will be based on direct non-controlling interest.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

13

A Plc owns 85% of the issued capital of B Plc and B Plc owns 90% of the issued capital of C Plc.What is the total outside equity interest in C Plc?

A)23.5%

B)10%

C)13.5%

D)15%

A)23.5%

B)10%

C)13.5%

D)15%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

14

A Plc owns 60 per cent of the issued capital of B Plc,B Plc owns 80 per cent of the issued capital of C Plc,and B Plc owns 70 per cent of the issued capital of D Plc.The ultimate parent entity is B Plc.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

15

The following diagram represents the ownership of issued share capital of the companies in a group.What is the ownership interest of A Ltd in D Ltd?

A)83.4%

B)76.6%

C)100%

D)86%

A)83.4%

B)76.6%

C)100%

D)86%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

16

A Plc owns 60% of the issued capital of B Plc and B Plc owns 55% of the issued capital of C Plc.What is A's interest in C Plc?

A)55%

B)24%

C)30%

D)33%

A)55%

B)24%

C)30%

D)33%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

17

The following diagram represents the ownership of issued share capital of the companies in a group.What is the total outside equity interest in D Ltd?

A)20%

B)33.6%

C)60%

D)24.8%

A)20%

B)33.6%

C)60%

D)24.8%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

18

A Plc owns 75% of the issued capital of B Plc and B Plc owns 65% of the issued capital of C Plc.What is the total outside equity interest in C Plc?

A)48.75%

B)35%

C)25.75%

D)51.25%

A)48.75%

B)35%

C)25.75%

D)51.25%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

19

It is not possible for one entity to control another entity without any direct ownership interest.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

20

The following diagram represents the ownership of issued share capital of the companies in a group.What is the total outside equity interest in D Ltd?

A)14%

B)10%

C)30%

D)22%

A)14%

B)10%

C)30%

D)22%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

21

The following is an extract from the non-controlling interest memorandum,used to calculate non-controlling interests.Both subsidiaries became members of the economic entity at the same time at the start of this current period. What is the parent's indirect equity (percentage)interest in Barbie Limited?

A)0%

B)10%

C)25%

D)40%

A)0%

B)10%

C)25%

D)40%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

22

X Plc owns 90% of the issued capital of Y Plc and Y Plc owns 70% of the issued capital of Z Plc.What is the total outside equity interest in C Plc?

A)37%

B)87.15%

C)12.85%

D)63%

A)37%

B)87.15%

C)12.85%

D)63%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

23

Jabba Ltd acquired a 70 per cent interest in Han Ltd on 30 June 2012 for €2 000 000.On the same date,Han Ltd acquired a 60 per cent interest in Leia Ltd for a cash consideration of €1 600 000.The purchase price represents the fair value of consideration transferred for both investments.The share capital and retained earnings at the date of acquisition are as follows: What is the non-controlling interest in Han Ltd and Leai Ltd,respectively on the date of acquisition using the partial goodwill method (round to the nearest dollar)?

A)€780 000; €960 000

B)€857 143; €1 066 667

C)€1 820 000; €1 440 000

D)€2 000 000; €1 600 000

A)€780 000; €960 000

B)€857 143; €1 066 667

C)€1 820 000; €1 440 000

D)€2 000 000; €1 600 000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

24

A Plc owns 85% of the issued capital of B Plc and B Plc owns 95% of the issued capital of C Plc.What is the total outside equity interest in C Plc?

A)23.5%

B)10.5%

C)19.25%

D)15%

A)23.5%

B)10.5%

C)19.25%

D)15%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

25

Jabba Ltd acquired a 70 per cent interest in Han Ltd on 30 June 2012 for €2 000 000.On the same date,Han Ltd acquired a 60 per cent interest in Leia Ltd for a cash consideration of €1 600 000.The purchase price represents the fair value of consideration transferred for both investments.The share capital and retained earnings at the date of acquisition are as follows: What is the non-controlling interest in Han Ltd and Leai Ltd,respectively on the date of acquisition using the full goodwill method (round to the nearest dollar)?

A)€780 000; €960 000

B)€857 143; €1 066 667

C)€1 820 000; €1 440 000

D)€2 857 143; €2 666 667

A)€780 000; €960 000

B)€857 143; €1 066 667

C)€1 820 000; €1 440 000

D)€2 857 143; €2 666 667

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

26

Jabba Ltd acquired a 70 per cent interest in Han Ltd on 30 June 2012 for €2 000 000.On the same date,Han Ltd acquired a 60 per cent interest in Leia Ltd for a cash consideration of €1 600 000.The purchase price represents the fair value of consideration transferred for both investments.The following information is available: No dividends have been declared since acquisition and there were no intragroup transactions during the year. What is the non-controlling interest in Han Ltd and Leai Ltd as at 30 June 2013,respectively using the partial goodwill method (round to the nearest dollar)?

A)€780 000; €960 000

B)€857 143; €1 066 667

C)€900 000; €1 134 000

D)€977 143; €1 240 667

A)€780 000; €960 000

B)€857 143; €1 066 667

C)€900 000; €1 134 000

D)€977 143; €1 240 667

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

27

Rose Ltd acquired a 75 per cent interest in Daisy Ltd on 1 July 2014 for a cash consideration of €758 000.On the same date,Daisy Ltd acquired a 56 per cent interest in Tulip Ltd for a cash consideration of €534 000.The fair value of the net assets of each of the companies at acquisition is as follows: Goodwill has been determined not to have been impaired.Information for the period ended 30 June 2015 for Daisy and Tulip is as follows: Neither dividend had been paid at the end of the period.There were no other intragroup transactions during the period.What is the non-controlling interest in Daisy and Tulip as at 30 June 2015?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

28

The following diagram represents the ownership of issued share capital of the companies in a group. What is the direct parent entity interest and direct non-controlling interest in D Ltd,respectively?

A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; zero

What is the direct parent entity interest and direct non-controlling interest in D Ltd,respectively?A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; zero

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

29

Pudding Ltd acquired a 90 per cent interest in Peaches Ltd on 1 July 2013 for a cash consideration of €2 300 000.On the same date,Peaches Ltd acquired a 70 per cent interest in Cream Ltd for a cash consideration of €1 100 000.The fair value of the net assets of each of the companies at acquisition is as follows: Goodwill has been determined not to have been impaired.What would the analysis of direct and indirect interests in the subsidiaries and the elimination entries be for the consolidation for the period ended 30 June 2014?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

30

Vader Ltd acquired a 75 per cent interest in Luke Ltd on 30 June 2012 for a cash consideration of €900 000.On the same date,Luke Ltd acquired a 60 per cent interest in Leia Ltd for a cash consideration of €600 000.The fair value of the net assets of each of the companies at acquisition is as follows: Goodwill has been determined not to have been impaired.Using the multiple entity consolidation approach,what would the analysis of direct and indirect interests in the subsidiaries and the elimination entries be for the consolidation for 30 June 2012?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

31

The following is an extract from the non-controlling interest memorandum,used to calculate non-controlling interests.Both subsidiaries became members of the economic entity at the same time at the start of this current period. The line item 'Dividend received from entity within the group' is an adjustment made:

A)to prevent double-counting as the indirect non-controlling interest of Barbie Ltd is in fact the same interest as the direct non-controlling interest in Ken Ltd and would have already received a share of the dividend as part of the share of profit in Ken Ltd.

B)to recognise, and eliminate, the dividend paid by Barbie Ltd directly to the parent entity.

C)to prevent double-counting as the indirect non-controlling interest of Ken Ltd is in fact the same interest as the direct non-controlling interest in Barbie Ltd and would have already received a share of the dividend as part of the share of profit in Ken Ltd

D)to recognise, and eliminate, the dividend paid by Ken Ltd directly to the parent entity.

A)to prevent double-counting as the indirect non-controlling interest of Barbie Ltd is in fact the same interest as the direct non-controlling interest in Ken Ltd and would have already received a share of the dividend as part of the share of profit in Ken Ltd.

B)to recognise, and eliminate, the dividend paid by Barbie Ltd directly to the parent entity.

C)to prevent double-counting as the indirect non-controlling interest of Ken Ltd is in fact the same interest as the direct non-controlling interest in Barbie Ltd and would have already received a share of the dividend as part of the share of profit in Ken Ltd

D)to recognise, and eliminate, the dividend paid by Ken Ltd directly to the parent entity.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

32

The following acquisition analysis relates to a non-sequential acquisition,at the time that Ginger Ltd acquires a controlling interest (acquiring 60 per cent)in Posh Ltd.Posh Ltd had previously acquitted 75 per cent of Scary Ltd. What are the figures represented by (a)and (b)in the table above?

A)(a) €210 000; (b) €93 000

B)(a) €168 000; (b) €74,400

C)(a) €126 000; (b) €55,800

D)(a) €280 000; (b) €124 000

A)(a) €210 000; (b) €93 000

B)(a) €168 000; (b) €74,400

C)(a) €126 000; (b) €55,800

D)(a) €280 000; (b) €124 000

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

33

The following is an extract from the non-controlling interest memorandum,used to calculate non-controlling interests.Both subsidiaries became members of the economic entity at the same time at the start of this current period. What is the parent's direct equity (percentage)interest in Barbie Limited?

A)0%

B)10%

C)25%

D)40%

A)0%

B)10%

C)25%

D)40%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

34

The following diagram represents the ownership of issued share capital of the companies in a group. What is the indirect parent entity interest and indirect non-controlling interest in D Ltd,respectively?

A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; 40%

What is the indirect parent entity interest and indirect non-controlling interest in D Ltd,respectively?A)12.6%; 23.4%

B)23.4%; 12.6%

C)40%; 60%

D)60%; 40%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

35

Summarise the calculations for recognising non-controlling interests,where both direct and indirect interests exist,in relation to:

(a)pre-acquisition share capital and reserves; (b)post-acquisition profits; and (c)post-acquisition movements in reserves.

(a)pre-acquisition share capital and reserves; (b)post-acquisition profits; and (c)post-acquisition movements in reserves.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

36

Pudding Ltd acquired a 90 per cent interest in Peaches Ltd on 1 July 2013 for a cash consideration of $2 300 000.On the same date,Peaches Ltd acquired a 70 per cent interest in Cream Ltd for a cash consideration of $1 100 000.The fair value of the net assets of each of the companies at acquisition is as follows: Goodwill has been determined not to have been impaired.Information for the period ended 30 June 2014 for Peaches Ltd and Cream Ltd is as follows: Neither dividend had been paid at the end of the period.There were no other intragroup transactions during the period.What is the non-controlling interest in Peaches Ltd and Cream Ltd as at 30 June 2014?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

37

The following acquisition analysis relates to a non-sequential acquisition,at the time that Ginger Ltd acquires a controlling interest (acquiring 60 per cent)in Posh Ltd.Posh Ltd had previously acquitted 75 per cent of Scary Ltd.

What are the figures represented by (c)and (d)in the table above?

A)(a) €176 000; (b) €54 000

B)(a) €150 000; (b) €67 500

C)(a) €146 000; (b) €54 000

D)(a) €146 000; (b) €67 500

What are the figures represented by (c)and (d)in the table above?

A)(a) €176 000; (b) €54 000

B)(a) €150 000; (b) €67 500

C)(a) €146 000; (b) €54 000

D)(a) €146 000; (b) €67 500

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

38

The following is an extract from the non-controlling interest memorandum,used to calculate non-controlling interests.Both subsidiaries became members of the economic entity at the same time at the start of this current period. What is the non-controlling indirect equity (percentage)interest in Ken Limited?

A)0%

B)22%

C)33%

D)40%

A)0%

B)22%

C)33%

D)40%

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

39

Pasta Ltd acquired an 80 per cent interest in Sauce Ltd on 1 July 2014 for a cash consideration of $3 193 000.On the same date,Sauce Ltd acquired a 60 per cent interest in Cheese Ltd for a cash consideration of $1 340 000.The fair value of the net assets of each of the companies at acquisition is as follows: Goodwill has been determined not to have been impaired.Information for the period ended 30 June 2015 for Sauce Ltd and Cheese Ltd is as follows: Neither dividend had been paid at the end of the period.There were no other intragroup transactions during the period.What is the non-controlling interest in Sauce Ltd and Cheese Ltd as at 30 June 2015?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

40

Rose Ltd acquired a 75 per cent interest in Daisy Ltd on 1 July 2014 for a cash consideration of €758 000.On the same date,Daisy Ltd acquired a 56 per cent interest in Tulip Ltd for a cash consideration of €534 000.The fair value of the net assets of each of the companies at acquisition is as follows: Goodwill has been determined not to have been impaired.Using the multiple entity consolidation approach,what would the analysis of direct and indirect interests in the subsidiaries and the elimination entries be for the consolidation for 30 June 2015?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

41

Discuss how it is possible for one entity to control another entity without any direct ownership interest.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

42

Discuss why it is necessary to differentiate between direct and indirect non-controlling interests in a group.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

43

A acquires a controlling interest of less than 100% ownership in B,who in turn acquires a controlling interest of less than 100% ownership in C,on the same day.The acquisition by B of C results in the recognition of goodwill on acquisition.Explain why there is a need to adjust for the impairment of goodwill when calculating the non-controlling interest for

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

44

Describe a non-sequential acquisition and explain the process of consolidation for this type of business combination.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

45

Describe the two multiple subsidiary acquisition types,based on the order of acquisition.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

46

Illustrate with the use of a diagram with hypothetical ownership interests,a structure where a parent entity has indirect ownership in a subsidiary.Demonstrate using the hypothetical percentages in proposed diagram,how direct and indirect ownership of parent and non-controlling interests are calculated.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 46 flashcards in this deck.