Deck 11: Share Capital, Reserves and Share Options Employee Bonus Schemes

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Sundowner Plc called for subscriptions for 2 million shares.The issue price per share is £6.00 to be paid in three parts: the first payment of $3.00 is to be made on application,£2.00 is to be paid within 1 month of allotment and the remaining £1.00 is to be paid within 6 months of allotment.At the end of July,when applications close,applications for 5 million shares have been received.Two million share applicants were unsuccessful,while the remaining 3 million applicants were allotted shares on 1 August on a pro rata basis with the excess application money to be applied against the amount due on allotment.The first and final call on the shares is made on 1October.Assume all amounts on allotment and call are paid by the due date.What are the accounting entries to record these events?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/62

Play

Full screen (f)

Deck 11: Share Capital, Reserves and Share Options Employee Bonus Schemes

1

Where new investors are offered the opportunity to buy new shares this will have the effect of diluting the existing shareholders' interest in the company.

True

2

As a residual interest,equity ranks after liabilities in terms of a claim against the assets of a reporting entity.

True

3

A public issue of shares involves:

A)compiling and then issuing a prospectus that outlines the details of the share issue so those interested can make an informed decision.

B)making the general public aware that shares are available for sale at a set price.

C)only issuing a limited number of shares to ensure there is sufficient demand for a full subscription.

D)issuing ordinary shares to all members of the public who are interested.

A)compiling and then issuing a prospectus that outlines the details of the share issue so those interested can make an informed decision.

B)making the general public aware that shares are available for sale at a set price.

C)only issuing a limited number of shares to ensure there is sufficient demand for a full subscription.

D)issuing ordinary shares to all members of the public who are interested.

A

4

A share split is usually funded through retained earnings.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

5

Flag Plc has received applications for 4 million shares during July 2014.The shares are to be issued at a price of £2.75 per share.The 4 million shares are allotted on 15 August 2014.What are the accounting entries required to record these events?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

6

The process for issuing shares is that:

A)They are offered for sale, allotments are received and an assignment made.Monies received on allotment must be held in trust until the assignment is made.

B)They are offered for sale, applications are received and an allotment made.Monies received on application must be held in trust until the allotment is made.

C)Applications are received for the issue of shares and an offer of shares is made.Applicants contribute capital that is returned to them if their application is unsuccessful when the shares are assigned.

D)A notice of intention to purchase shares is registered with the stock exchange, which the company receives.The company then offers shares.The applicant may then be allotted shares and at that point must make the cash contribution.

A)They are offered for sale, allotments are received and an assignment made.Monies received on allotment must be held in trust until the assignment is made.

B)They are offered for sale, applications are received and an allotment made.Monies received on application must be held in trust until the allotment is made.

C)Applications are received for the issue of shares and an offer of shares is made.Applicants contribute capital that is returned to them if their application is unsuccessful when the shares are assigned.

D)A notice of intention to purchase shares is registered with the stock exchange, which the company receives.The company then offers shares.The applicant may then be allotted shares and at that point must make the cash contribution.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

7

Double entry accounting requires that:

A)the claims held by external parties equal the claims held by the owners.

B)the total assets of an entity equal the total of the claims held by external parties plus those claims held by the owners.

C)the liabilities of the entity equal its total assets plus the claims held by the owners.

D)the recognition of the claims held by owners will match the entity's total assets.

A)the claims held by external parties equal the claims held by the owners.

B)the total assets of an entity equal the total of the claims held by external parties plus those claims held by the owners.

C)the liabilities of the entity equal its total assets plus the claims held by the owners.

D)the recognition of the claims held by owners will match the entity's total assets.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

8

If an entity performs a share split on a partly paid share,the split must be done in such a way as to divide the uncalled portion equally among the shares issued.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

9

In a public issue of shares,the procedure to be adopted in the case of an oversubscription is normally specified in the prospectus.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

10

In the case of a share issue being oversubscribed,the common approaches include:

A)Issue additional shares to meet the excess demand.

B)Allocate the shares on a pro rata basis.

C)Increase the issue price of the shares.

D)Issue additional shares to meet the excess demand and increase the issue price of the shares.

A)Issue additional shares to meet the excess demand.

B)Allocate the shares on a pro rata basis.

C)Increase the issue price of the shares.

D)Issue additional shares to meet the excess demand and increase the issue price of the shares.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

11

Ordinary shares receive low dividends because they do not perform very well.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

12

The owners' equity of an organisation is the same as the shareholders' funds of a company.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

13

Company law usually requires that where a company redeems preference shares it must do so out of profits that would otherwise be available for dividends or out of the proceeds of a fresh issue of shares made for the purpose of the redemption.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

14

It used to be normal practice to issue shares at below par value.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

15

Accounts that make up owners' equity may include:

A)preference shares.

B)debentures.

C)general reserves.

D)preference shares and general reserves.

A)preference shares.

B)debentures.

C)general reserves.

D)preference shares and general reserves.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

16

An individual's views on measurement techniques for assets and liabilities will have a direct impact on the amount recorded in shareholders' funds.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

17

If a company is listed in the London Stock Exchange and shareholders fail to pay the amount due on allotment,the shares forfeited must be refunded in full to defaulting investors.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

18

A company may elect to issues its shares at any price,which will depend on:

A)the last sales price for the company's shares before the new issue.

B)the market demand.

C)the minimum price that has been paid for the shares over the last reporting period..

D)the amount specified in legislation at which all companies were required to issue shares.

A)the last sales price for the company's shares before the new issue.

B)the market demand.

C)the minimum price that has been paid for the shares over the last reporting period..

D)the amount specified in legislation at which all companies were required to issue shares.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

19

IAS 1 Presentation of Financial Statements requires an entity to disclose a description of the nature and purpose of each reserve within equity.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

20

Share capital:

A)relates to one class of shares, with the remaining equity recorded as reserves or retained profits.

B)represents the amount shareholders are guaranteed to receive if the company is wound up.

C)may relate to one or several classes of shares.

D)may be calculated by subtracting liabilities from assets.

A)relates to one class of shares, with the remaining equity recorded as reserves or retained profits.

B)represents the amount shareholders are guaranteed to receive if the company is wound up.

C)may relate to one or several classes of shares.

D)may be calculated by subtracting liabilities from assets.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

21

The statement of changes in equity:

A)presents, either on the face of the statement or in the notes, the amounts of dividends recognised as distributions to owners during the period and the related amount per share.

B)is identical to the statement of recognised income and expense.

C)is the same as that required under the former UK 'Reconciliation of Shareholders Funds' statement.

D)provides a reconciliation between the expenses outstanding at the start of the period and those outstanding at the end of the period.

A)presents, either on the face of the statement or in the notes, the amounts of dividends recognised as distributions to owners during the period and the related amount per share.

B)is identical to the statement of recognised income and expense.

C)is the same as that required under the former UK 'Reconciliation of Shareholders Funds' statement.

D)provides a reconciliation between the expenses outstanding at the start of the period and those outstanding at the end of the period.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

22

In the case of a share issue being oversubscribed,excess application monies:

A)will always be refunded to applicants.

B)may be used to reduce future amounts owing on allotment if the shares are issued on a pro rata basis.

C)must be recorded as revenue in the current financial period.

D)must be placed in a trust account until a refund is requested by applicants.

A)will always be refunded to applicants.

B)may be used to reduce future amounts owing on allotment if the shares are issued on a pro rata basis.

C)must be recorded as revenue in the current financial period.

D)must be placed in a trust account until a refund is requested by applicants.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

23

Giggles Plc has 2 million shares issued.The directors have elected,with the support of a resolution passed at a general meeting,to undertake a 1: 2 share split so that there will be 4 million issued shares.The shares were originally issued at a price of €2 each.What is the summary entry to record the share split?

A)

B)

C)

D)None of the given answers are correct.

A)

B)

C)

D)None of the given answers are correct.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

24

Motion Plc issued €5 million in redeemable preference shares in a private placement on 1 July 2012.The shares are redeemable on 30 June 2016,have no voting rights and offer a fixed rate of return to the holder.The shares are redeemed as expected with a fresh issue of shares.What are the accounting entries and note disclosures to record the transactions on 1 July 2012 and 30 June 2016?

A)

Note disclosure: redeemable preference shares have characteristics different to ordinary shares and so have been disclosed separately in the shareholders' funds section of the statement of financial position.

B)

Note disclosure: redeemable preference shares have characteristics different to ordinary shares and so have been disclosed separately in the shareholders' funds section of the statement of financial position.

C)

Note disclosure: redeemable preference shares have the characteristics of debt and so have been classified as liabilities in the statement of financial position.

D)

Note disclosure: redeemable preference shares are to be redeemed on 30 June 2008.

A)

Note disclosure: redeemable preference shares have characteristics different to ordinary shares and so have been disclosed separately in the shareholders' funds section of the statement of financial position.

B)

Note disclosure: redeemable preference shares have characteristics different to ordinary shares and so have been disclosed separately in the shareholders' funds section of the statement of financial position.

C)

Note disclosure: redeemable preference shares have the characteristics of debt and so have been classified as liabilities in the statement of financial position.

D)

Note disclosure: redeemable preference shares are to be redeemed on 30 June 2008.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

25

A statement of changes in equity:

A)is identical to a statement of comprehensive income.

B)is required to include only the components listed in paragraph 106 of IAS 1.

C)includes the effects of changes in accounting policies recognised in accordance with IAS 8.

D)is required to include only the components listed in paragraph 106 of IAS 1 and includes the effects of changes in accounting policies recognised in accordance with IAS 8.

A)is identical to a statement of comprehensive income.

B)is required to include only the components listed in paragraph 106 of IAS 1.

C)includes the effects of changes in accounting policies recognised in accordance with IAS 8.

D)is required to include only the components listed in paragraph 106 of IAS 1 and includes the effects of changes in accounting policies recognised in accordance with IAS 8.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

26

Semaphore Plc called for subscriptions for 15 million shares.The issue price per share is €2.50 to be paid in two parts: the first payment of €1.00 is to be made on application and the remaining €1.50 is to be paid within 1 month of allotment.At the end of September,when applications close,applications for 19 million shares have been received.The shares are allotted on 1 October on a pro rata basis with the excess application money to be applied against the amount due on allotment.All amounts on allotment are paid by the due date.What are the accounting entries to record these events?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

27

When a rights issue is tradeable it is often referred to as:

A)reducable.

B)rightful.

C)redeemable.

D)renounceable.

A)reducable.

B)rightful.

C)redeemable.

D)renounceable.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

28

The effect of a bonus issue to all shareholders on (a)net asset backing per share,(b)each shareholder's share of net assets and (c)market capitalisation is:

A)(a) The net asset backing per share will decrease; (b) each shareholder's share of net assets will remain the same; (c) evidence suggests that on average the market capitalisation will increase.

B)(a) The net asset backing per share will increase; (b) each shareholder's share of net assets will increase; (c) evidence suggests that on average the market capitalisation will remain the same.

C)(a) The net asset backing per share will decrease; (b) each shareholder's share of net assets will decrease; (c) evidence suggests that on average the market capitalisation will remain the same.

D)(a) The net asset backing per share will remain the same; (b) each shareholder's share of net assets will decrease; (c) evidence suggests that on average the market capitalisation will decrease.

A)(a) The net asset backing per share will decrease; (b) each shareholder's share of net assets will remain the same; (c) evidence suggests that on average the market capitalisation will increase.

B)(a) The net asset backing per share will increase; (b) each shareholder's share of net assets will increase; (c) evidence suggests that on average the market capitalisation will remain the same.

C)(a) The net asset backing per share will decrease; (b) each shareholder's share of net assets will decrease; (c) evidence suggests that on average the market capitalisation will remain the same.

D)(a) The net asset backing per share will remain the same; (b) each shareholder's share of net assets will decrease; (c) evidence suggests that on average the market capitalisation will decrease.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

29

Reserves recorded in the equity section of the statement of financial position:

A)represent an amount of cash put aside for future projects.

B)are created from excess profits that are not available for distribution as dividends.

C)may be established by transferring amounts from retained profits.

D)will not have an impact on the total equity reported in the equity section of the statement of financial position when created.

A)represent an amount of cash put aside for future projects.

B)are created from excess profits that are not available for distribution as dividends.

C)may be established by transferring amounts from retained profits.

D)will not have an impact on the total equity reported in the equity section of the statement of financial position when created.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

30

When a company redeems preference shares:

A)It must ensure it has sufficient cash reserves to do so.

B)It must do so out of profits other than those available for the issuing of dividends.

C)It must issue fresh shares to fund the redemption.

D)None of the given answers are correct.

A)It must ensure it has sufficient cash reserves to do so.

B)It must do so out of profits other than those available for the issuing of dividends.

C)It must issue fresh shares to fund the redemption.

D)None of the given answers are correct.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

31

An effect of a bonus issue to all shareholders is to:

A)increase the total amount of shareholders' funds.

B)make the amount that was previously recorded as retained earnings no longer available for the payment of cash dividends.

C)alter the current shareholders' proportionate share of the company's net assets.

D)increase the total assets of the company.

A)increase the total amount of shareholders' funds.

B)make the amount that was previously recorded as retained earnings no longer available for the payment of cash dividends.

C)alter the current shareholders' proportionate share of the company's net assets.

D)increase the total assets of the company.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

32

When shares are allotted,or a call made on them,allotment and call accounts are created respectively.What is the nature of these accounts and how are they to be disclosed in the financial statements?

A)The accounts are similar in nature to an account receivable and are to be disclosed in the statement of financial position as a current asset.

B)The accounts are similar to a future income benefit and are to be separately disclosed as assets in the statement of financial position.

C)The accounts are similar to an account receivable and are disclosed in the statement of financial position as a reduction against share capital.

D)The accounts are in the nature of a deferred income and are disclosed as a provision for future cash inflows in the statement of financial position.

A)The accounts are similar in nature to an account receivable and are to be disclosed in the statement of financial position as a current asset.

B)The accounts are similar to a future income benefit and are to be separately disclosed as assets in the statement of financial position.

C)The accounts are similar to an account receivable and are disclosed in the statement of financial position as a reduction against share capital.

D)The accounts are in the nature of a deferred income and are disclosed as a provision for future cash inflows in the statement of financial position.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

33

Signal Plc called for subscriptions for 8 million shares.The issue price per share is €3.50 to be paid in three parts: the first payment of €1.00 is to be made on application,€1.50 is to be paid within 1 month of allotment and the remaining €1.00 is to be paid within 3 months of allotment.At the end of July,when applications close,applications for 10 million shares have been received.The shares are allotted on 1 August on a pro rata basis with the excess application money to be applied against the amount due on allotment.The first and final call on the shares is made on 1 October.Assume all amounts on allotment and call are paid by the due date.What are the accounting entries to record these events?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

34

A statement of changes in equity includes:

A)each item of income and expense for the period that, as required by other International Financial Reporting Standards, is recognised directly in equity.

B)profit or loss for the period.

C)total income and expense for the period showing separately the total amounts attributable to equity holders of the parent and to minority interest.

D)each item of income and expense for the period that, as required by other International Financial Reporting Standards, is recognised directly in equity, profit or loss for the period, and total income and expense for the period showing separately the total amounts attributable to equity holders of the parent and to minority interest.

A)each item of income and expense for the period that, as required by other International Financial Reporting Standards, is recognised directly in equity.

B)profit or loss for the period.

C)total income and expense for the period showing separately the total amounts attributable to equity holders of the parent and to minority interest.

D)each item of income and expense for the period that, as required by other International Financial Reporting Standards, is recognised directly in equity, profit or loss for the period, and total income and expense for the period showing separately the total amounts attributable to equity holders of the parent and to minority interest.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

35

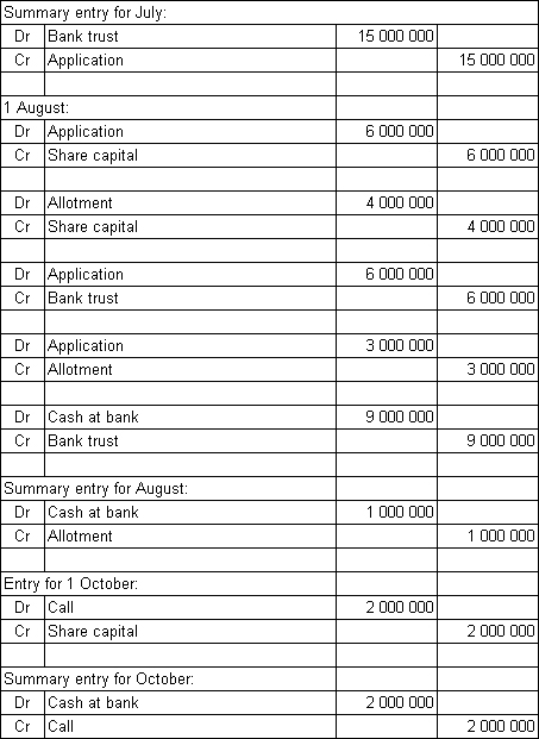

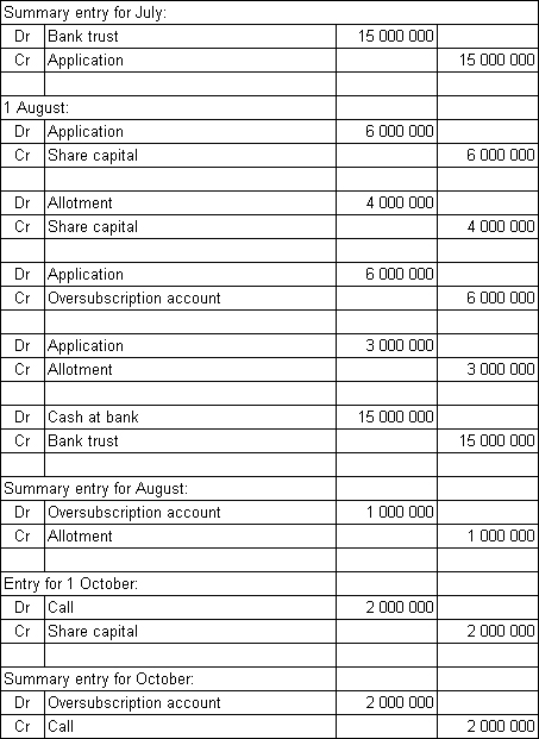

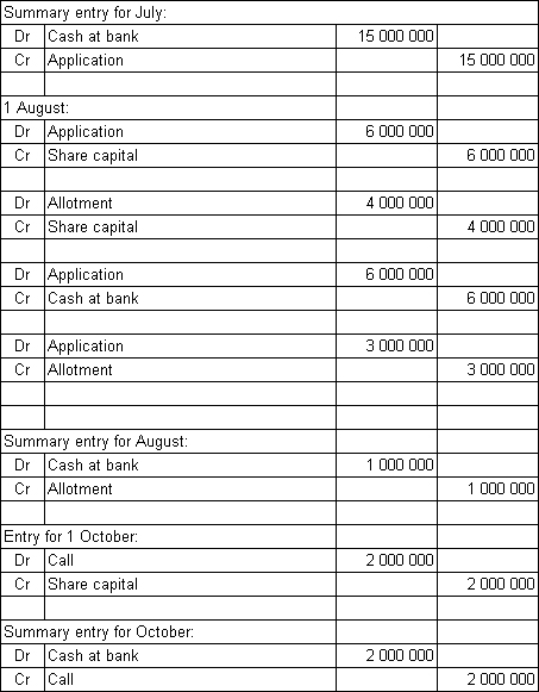

Sundowner Plc called for subscriptions for 2 million shares.The issue price per share is £6.00 to be paid in three parts: the first payment of $3.00 is to be made on application,£2.00 is to be paid within 1 month of allotment and the remaining £1.00 is to be paid within 6 months of allotment.At the end of July,when applications close,applications for 5 million shares have been received.Two million share applicants were unsuccessful,while the remaining 3 million applicants were allotted shares on 1 August on a pro rata basis with the excess application money to be applied against the amount due on allotment.The first and final call on the shares is made on 1October.Assume all amounts on allotment and call are paid by the due date.What are the accounting entries to record these events?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

36

Share splits are conducted because it is believed that:

A)Excess capital leads to reduced return ratios, which the market does not view favourably.

B)Increasing the number of shares issued makes the company appear larger and more stable.

C)Decreasing the price per share makes them more marketable.

D)Investors view this as a bonus because they now have more shares than they previously held.

A)Excess capital leads to reduced return ratios, which the market does not view favourably.

B)Increasing the number of shares issued makes the company appear larger and more stable.

C)Decreasing the price per share makes them more marketable.

D)Investors view this as a bonus because they now have more shares than they previously held.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

37

Normal features of ordinary shares include:

A)They entitle the holder to receive his/her proportion of any ordinary dividends declared.

B)They ensure the holder has priority over unsecured creditors in the case of the company going into liquidation.

C)They confer voting rights.

D)They entitle the holder to receive his/her proportion of any ordinary dividends declared and they confer voting rights.

A)They entitle the holder to receive his/her proportion of any ordinary dividends declared.

B)They ensure the holder has priority over unsecured creditors in the case of the company going into liquidation.

C)They confer voting rights.

D)They entitle the holder to receive his/her proportion of any ordinary dividends declared and they confer voting rights.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

38

The total market capitalisation of a company after a bonus issue is likely to:

A)be lower than it was before the bonus issue.

B)be greater than it was before the bonus issue.

C)be less than it was before the bonus issue.

D)There will be no change.

A)be lower than it was before the bonus issue.

B)be greater than it was before the bonus issue.

C)be less than it was before the bonus issue.

D)There will be no change.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

39

Cartoon Plc is listed on the London Stock Exchange.It has 3 million shares issued at a price of £5.50 per share.The investors were required to pay £2.00 on application and £1.00 on allotment.Both these amounts were paid in full.A first and final call of £2.50 was made and was due on 30 August 2013.At the end of November the directors of the company elect to forfeit 50 000 shares on which the holders have failed to pay the call.Cartoon Plc reissues the shares fully paid up for a price of £4.75 and incurred costs of £1500.What are the entries required to forfeit the shares,reissue the shares,and make a refund if appropriate?

A)

B)

Refund the shares:

No entry required

C)

D)

Refund the shares:

None to be made

A)

B)

Refund the shares:

No entry required

C)

D)

Refund the shares:

None to be made

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

40

Holders of ordinary shares:

A)are assured of dividends each year.

B)may not receive a cash dividend each year but the dividend will accrue and eventually be paid.

C)will always receive a dividend if the company has made a profit in that financial year.

D)receive dividends at the discretion of the board.

A)are assured of dividends each year.

B)may not receive a cash dividend each year but the dividend will accrue and eventually be paid.

C)will always receive a dividend if the company has made a profit in that financial year.

D)receive dividends at the discretion of the board.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

41

Shares may be issued for consideration other than cash including:

A)promissory notes.

B)contracts for future services.

C)real or personal property.

D)all of the given answers.

A)promissory notes.

B)contracts for future services.

C)real or personal property.

D)all of the given answers.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

42

What is the effect of a share split on earnings per share and the number of shares outstanding,respectively?

A)increase; decrease

B)decrease; increase

C)increase; increase

D)no effect; increase

A)increase; decrease

B)decrease; increase

C)increase; increase

D)no effect; increase

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

43

Explain the options available for a company when an investor fails to pay the amounts due on subsequent calls.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

44

IAS 10 Events After the Reporting Period specifically prohibits the recognition of dividends as a liability at the end of the reporting period if:

A)the dividends have been declared before the end of the reporting period.

B)the dividends have been declared after the end of the reporting period.

C)the dividends have been declared during the reporting period.

D)the dividends have not been declared after the end of the reporting period.

A)the dividends have been declared before the end of the reporting period.

B)the dividends have been declared after the end of the reporting period.

C)the dividends have been declared during the reporting period.

D)the dividends have not been declared after the end of the reporting period.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

45

Discuss,with examples,how the recognition criteria for assets and liabilities provide the criteria for the recognition of equity.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

46

For each class of share capital,an entity shall disclose either on the face of the statement of financial position or in the notes:

A)shares in the entity held by the entity or its subsidiaries or associates.

B)the number of shares authorised.

C)the number of shares issued but not fully paid.

D)all of the given answers.

A)shares in the entity held by the entity or its subsidiaries or associates.

B)the number of shares authorised.

C)the number of shares issued but not fully paid.

D)all of the given answers.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

47

Explain how an entity could handle excess monies in a share issue that is oversubscribed.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

48

Where there is a redemption of preference shares 'out of profit':

A)The redemption is recorded in the appropriations section of the statement of comprehensive income.

B)The redemption is recorded as an expense.

C)The redemption is recorded as a liability and is amortised over a maximum of five years.

D)The redemption is not recorded in the current period.

A)The redemption is recorded in the appropriations section of the statement of comprehensive income.

B)The redemption is recorded as an expense.

C)The redemption is recorded as a liability and is amortised over a maximum of five years.

D)The redemption is not recorded in the current period.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

49

Discuss the primary role of the statement of changes in equity,and what is included in such a statement.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

50

The forfeited shares account is used to make up any shortfall:

A)to the forfeiting shareholder.

B)the forfeited share reserve.

C)on the issue of the shares.

D)on the cash at bank account .

A)to the forfeiting shareholder.

B)the forfeited share reserve.

C)on the issue of the shares.

D)on the cash at bank account .

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

51

Explain the various possible outcomes when there is a forfeiture of shares,due to non-payment of amounts owing when a call is made.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

52

The term 'reserves' in the statement of financial position is used to identify:

A)a decline in the fair value of a non-current asset.

B)an amount of retained earnings that is allocated for a specific purpose.

C)the allowance for uncollectible receivables.

D)an amount that is being accumulated to reduce the financial effect of a litigation lawsuit.

A)a decline in the fair value of a non-current asset.

B)an amount of retained earnings that is allocated for a specific purpose.

C)the allowance for uncollectible receivables.

D)an amount that is being accumulated to reduce the financial effect of a litigation lawsuit.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

53

Share capital is also referred to as:

A)equity

B)contributed equity

C)owners contribution

D)shareholder equity

A)equity

B)contributed equity

C)owners contribution

D)shareholder equity

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following statements correctly describes this journal entry:

A)The issue of options, costing $3.50 each.

B)The issue of options, costing $30 each.

C)The exercise of options, with a current market value per share of $3.50.

D)The exercise of options, initially costing $3 500 000 to issue and with an exercise price for each option of $30.

A)The issue of options, costing $3.50 each.

B)The issue of options, costing $30 each.

C)The exercise of options, with a current market value per share of $3.50.

D)The exercise of options, initially costing $3 500 000 to issue and with an exercise price for each option of $30.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

55

Fraser Plc issued 10 million shares at a price of €3 on 1 July 2012.The subscribers are required to pay €1 on application,€1 on allotment and the balance on call to be announced at a later date.The share issue was oversubscribed by 2 million shares.On 1 August 2012 the shares were allotted to all subscribers on a pro rata basis.What is the balance of the 'allotment account' and 'share capital' for this share issue on 1 August 2012,respectively?

A)€8 million; €20 million

B)€8 million; €30 million

C)€10 million; €20 million

D)€10 million; €30 million

A)€8 million; €20 million

B)€8 million; €30 million

C)€10 million; €20 million

D)€10 million; €30 million

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is ? not a required disclosure to be made in relation to each class of share capital?

A)number of shares authorised

B)number of shares issued and fully paid and issued but not fully paid

C)par value per share or that the shares have no par value

D)None of the given answers are correct.

A)number of shares authorised

B)number of shares issued and fully paid and issued but not fully paid

C)par value per share or that the shares have no par value

D)None of the given answers are correct.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

57

What is meant by an oversubscription of a share offer?

Explain the two approaches that could be adopted in the case of an oversubscription.

Explain the two approaches that could be adopted in the case of an oversubscription.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following would not apply to a preference shares?

A)higher order of ranking in relation to asset distributions on the winding up of the company

B)redeemable at a set date in the future

C)can be classified as an expense

D)can be converted to ordinary shares

A)higher order of ranking in relation to asset distributions on the winding up of the company

B)redeemable at a set date in the future

C)can be classified as an expense

D)can be converted to ordinary shares

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following share issue costs does not qualify as a deduction from share capital?

A)advertising of share issue

B)costs of prospectus issue

C)administration overheads

D)audit expenses associated with the issue of a prospectus

A)advertising of share issue

B)costs of prospectus issue

C)administration overheads

D)audit expenses associated with the issue of a prospectus

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

60

Preference shares may be classified as a liability,an equity item,or have features of both.Explain with examples,how to determine such a classification.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

61

Explain the differences between a rights issue and share options.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

62

When a company sells shares,various costs are incurred.Discuss why these costs are classified as equity and the circumstance that would allow these costs to be expensed.

Unlock Deck

Unlock for access to all 62 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 62 flashcards in this deck.