Deck 3: Statements of Income and Comprehensive Income

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

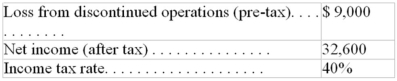

A company reported the following results of its operations for 2006:  Income from continuing operations was:

Income from continuing operations was:

A)$32,600

B)$27,200

C)$41,600

D)$38,000

Income from continuing operations was:A)$32,600

B)$27,200

C)$41,600

D)$38,000

Question

Question

Question

Question

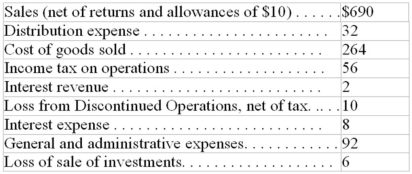

Given the following amounts from an income statement:  The amount shown on a multiple-step format income statement for operating income from continuing operations would be:

The amount shown on a multiple-step format income statement for operating income from continuing operations would be:

A)$232

B)$246

C)$290

D)$302

The amount shown on a multiple-step format income statement for operating income from continuing operations would be:A)$232

B)$246

C)$290

D)$302

Question

Question

Question

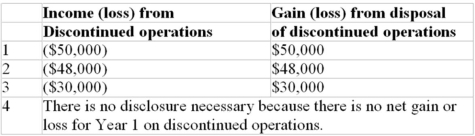

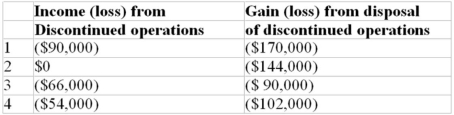

Jacks Corporation decided to sell its playing card business segment for $600,000,on September 1,Year 1.The disposal date is November 1,Year 1.The book value of the segment's net assets is $550,000.The pre-tax income for the segment for the period January 1 - September 1,Year 1,was a loss of $80,000; the pre-tax income for the segment for September and October was $30,000.Assuming a tax rate of 40%,choose the correct reporting for discontinued operations in the income statement of Jacks Corporation,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Question

Question

Question

Question

Question

Question

Question

Given the following amounts from an income statement:  The amount shown on a single-step format income statement for income from continuing operations items would be:

The amount shown on a single-step format income statement for income from continuing operations items would be:

A)$46

B)$41

C)$40

D)$35

The amount shown on a single-step format income statement for income from continuing operations items would be:A)$46

B)$41

C)$40

D)$35

Question

Question

A company which lost part of its accounting system in a fire is having trouble determining what its net income is for the current year.The following correct adjusted balances and additional information for the current year are available:  Additional information for the year:

Additional information for the year:  Other than earnings and the events listed above,no other events or transactions affected owners' Equity in the current year.What was net income for the current year?

Other than earnings and the events listed above,no other events or transactions affected owners' Equity in the current year.What was net income for the current year?

A)$12,000

B)$22,000

C)$17,000

D)$16,000

Additional information for the year: Other than earnings and the events listed above,no other events or transactions affected owners' Equity in the current year.What was net income for the current year?A)$12,000

B)$22,000

C)$17,000

D)$16,000

Question

Ace Corporation decided to sell its medical supplies business segment for $500,000,on September 1,Year 1.The disposal date is November 1,Year 1.The book value of the segment's net assets is $650,000.The pre-tax income for the segment for the period January 1 - September 1,Year 1,was a loss of $90,000; the pre-tax income for the segment for September and October was a loss of $20,000.Assuming a tax rate of 40%,choose the correct reporting for discontinued operations in the income statement of Ace Corporation,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/130

Play

Full screen (f)

Deck 3: Statements of Income and Comprehensive Income

1

A natural disaster,such as a flood,will always be considered unusual or infrequent.

False

2

Other comprehensive income includes unrealized gains on losses of foreign exchange hedges.

True

3

Under IFRS,The statement of comprehensive income includes net income and other comprehensive income.

True

4

Under ASPE,Assets held for sale may be current OR non-current.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

5

Gross Profit must always be shown on the face of a single-step income statement

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

6

Both extraordinary items and unusual or infrequent items must be reported net of income taxes.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

7

When reporting net income for a fiscal year,companies must use a 12-month period.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

8

Finance costs must always be shown on the face of the income statement under IFRS.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

9

An event is considered to occur infrequently if it would not reasonably be expected to recur in the foreseeable future,taking into account the entity's operating environment.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

10

The presentation of both net income and other comprehensive income is required under both IFRS and ASPE.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

11

Unusual or infrequent items should be reported separately,but not net of income tax,and not as an extraordinary item.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

12

Other comprehensive income generally includes unrealized gains or losses which bypass the income statement.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

13

Depreciation is not taken on assets that are temporarily idle but have not been abandoned.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

14

Under IFRS,an expense item must be both presented and disclosed by nature and function.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

15

Under IFRS,depreciation expense and employee benefits expense may be shown on the face of the income statement OR may be disclosed separately in the notes to the financial statements.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

16

Earnings per share represent the portion of the income for a period attributable to a share of voting capital of an enterprise.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

17

The operating losses and gain or loss from a discontinued operation must be shown net of tax in a distinct section on the statement of income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

18

Under IFRS,any Assets Held for Sale arising from the discontinuation of a business segment must be classified as current.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

19

Extraordinary items no longer exist under IFRS.The terms infrequent or unusual are sometimes used instead.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

20

The financial results of a discontinued segment must be reported separately on the income statement.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

21

Once any unrealized gains or losses included in Other Comprehensive Income are realized,they are transferred to the income statement.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

22

Once an asset has been abandoned,amortization stops and it is written down to its recoverable value.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

23

Basic and diluted Earnings per share figures must be disclosed under both ASPE and IFRS.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

24

Total Comprehensive income must be allocated to both the parent and the non-controlling interest (NCI) shareholder groups.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

25

Interperiod tax allocation refers to the deferral and allocation of income tax expense to future periods while intraperiod tax allocation refers to the process of splitting up income tax expense across the different income statement categories.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

26

A disposal group may include both current and non-current assets.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

27

An income statement showing depreciation expense a line item is showing its expenses by nature.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

28

Once an asset has been designated as held for sale,this classification is irrevocable.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

29

Correction of prior years' errors and changes in accounting principles are not recorded net of any income tax effects.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

30

Correction of prior years' errors and changes in accounting principles are never reported on the statement of income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

31

If an abandoned asset's recoverable value increases subsequent to abandonment,the asset may be written up to a maximum of the asset's original carrying value.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

32

Only non-current assets may be reclassified as Assets Held for Sale.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

33

Under IFRS,the parent company's share of any profits or losses arising from joint ventures must be included on the face of Statement of Comprehensive Income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

34

Once an asset has been designated as held for sale it must be re measured to the lower of its carrying value and its fair value less costs to sell.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

35

After an asset held for sale has been written down,it must written back if its fair value less costs to sell subsequently increases under IFRS.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

36

Under both ASPE and IFRS,a discontinued operation must be a reportable segment.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

37

Under ASPE,assets and liabilities forming part of a disposal group must be classified as current assets.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

38

Other comprehensive income includes unrealized gains and losses on Available-for-sale securities.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

39

Losses and provisions for losses with respect to bad debts and inventories should not be reported as unusual or infrequent.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

40

The concept of intra-period tax allocation is based on the going concern principle.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

41

All elements of OCI must eventually be recycled to the income statement.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

42

During the current period,Canada Revenue Agency assessed a firm a nonrecurring income tax amount (but not a penalty) as a result of a Tax Court case involving a disputed deduction from a prior year (the firm lost the case).This amount should be reported by the firm as a (n):

A)Correction of period years' errors.

B)Extraordinary loss.

C)Expense or loss of the current period.

D)Direct adjustment to owner's equity.

A)Correction of period years' errors.

B)Extraordinary loss.

C)Expense or loss of the current period.

D)Direct adjustment to owner's equity.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

43

The date on which a gain or loss from the disposal of a segment of a business is measured is the:

A)date that operations cease (if disposal is by abandonment).

B)last day of the fiscal year in which the decision to dispose is made plan.

C)date that the assets are sold.

D)date that the entity makes a formal commitment to disposal.

A)date that operations cease (if disposal is by abandonment).

B)last day of the fiscal year in which the decision to dispose is made plan.

C)date that the assets are sold.

D)date that the entity makes a formal commitment to disposal.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

44

In the current year,a firm has decided to dispose of a segment.Disposal will take place in the next (subsequent) year.Use the following symbols to answer this question on reporting for discontinued operations: P = income on discontinued segment from beginning of current year to date of disposal decision

Q = income on discontinued segment from date of disposal decision to end of current year

R = estimated loss of discontinued segment sale of assets in subsequent year to date of disposal of segment

When determining the amount to disclose as the gain or loss on disposal of the segment for the current period,which of the following should be considered:

A)P, Q and R

B)P and Q only

C)Q and R only

D)None of P, Q or R

Q = income on discontinued segment from date of disposal decision to end of current year

R = estimated loss of discontinued segment sale of assets in subsequent year to date of disposal of segment

When determining the amount to disclose as the gain or loss on disposal of the segment for the current period,which of the following should be considered:

A)P, Q and R

B)P and Q only

C)Q and R only

D)None of P, Q or R

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

45

Economic income excludes accounting income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

46

The realization of a previously unrealized gain or loss during a given period has no effect on the company's total shareholder equity.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

47

Accounting income is a concept in which:

A)Income is measured as the amount of "real wealth" that an entity could consume during a period and be as well off at the end of that period as it was at the beginning.

B)Market values adjusted for the effects of inflation or deflation are used to calculate real wealth.

C)The transactions approach is used to record revenues, expenses, gains and losses throughout the reporting period.

D)Income equals the change in market value of the firm's outstanding common stock for the period.

A)Income is measured as the amount of "real wealth" that an entity could consume during a period and be as well off at the end of that period as it was at the beginning.

B)Market values adjusted for the effects of inflation or deflation are used to calculate real wealth.

C)The transactions approach is used to record revenues, expenses, gains and losses throughout the reporting period.

D)Income equals the change in market value of the firm's outstanding common stock for the period.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

48

Increases in the recoverable value of a total disposal group are:

A)Recorded in net income.

B)Recorded in net income but are limited to the carrying value of the disposal group on the date it was designated as held-for-sale.

C)Ignored.

D)Credited to Retained Earnings.

A)Recorded in net income.

B)Recorded in net income but are limited to the carrying value of the disposal group on the date it was designated as held-for-sale.

C)Ignored.

D)Credited to Retained Earnings.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

49

When a segment of a business has been discontinued during the year and is sold at the end of that same year,the income or loss from the discontinued operations,one of the three amounts typically reported in the income statement,would not include:

A)the income or loss from operating the segment the entire year

B)the income or loss from operating the segment from the beginning of the year to the date the decision was made to dispose of the segment

C)the income or loss from operating the segment from the date the decision was made to dispose of the segment to the end of the year

D)the difference between the sales price of the segment and the segment's book value

A)the income or loss from operating the segment the entire year

B)the income or loss from operating the segment from the beginning of the year to the date the decision was made to dispose of the segment

C)the income or loss from operating the segment from the date the decision was made to dispose of the segment to the end of the year

D)the difference between the sales price of the segment and the segment's book value

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

50

Interperiod income tax allocation:

A)Involves the allocation of income taxes on certain taxable items of the same period.

B)Generally has no effect on the balance sheet.

C)Arises because certain revenues and expenses appear in the financial statements either before or after they are included on the income tax return.

D)Involves only items appearing below income from continuing operations in the income statement.

A)Involves the allocation of income taxes on certain taxable items of the same period.

B)Generally has no effect on the balance sheet.

C)Arises because certain revenues and expenses appear in the financial statements either before or after they are included on the income tax return.

D)Involves only items appearing below income from continuing operations in the income statement.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

51

Earnings per share reporting:

A)is mandatory for corporations following IFRS and requires two presentations (basic and fully diluted EPS) when a firm has a complex capital structure.

B)is required for all corporations with common stock outstanding.

C)Reveals the relationship between retained earnings available to holders of common stock and the number of shares of common stock outstanding.

D)Shows the maximum dividend which may be paid.

A)is mandatory for corporations following IFRS and requires two presentations (basic and fully diluted EPS) when a firm has a complex capital structure.

B)is required for all corporations with common stock outstanding.

C)Reveals the relationship between retained earnings available to holders of common stock and the number of shares of common stock outstanding.

D)Shows the maximum dividend which may be paid.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

52

Accounting income is a less complete measurement of wealth than is economic income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

53

Historical cost is more useful for measuring economic income than fair values.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

54

When individual assets and liabilities within a disposal group change in value,these changes are:

A)Ignored, since the disposal group will be sold as a whole.

B)Charged to Retained Earnings.

C)Charged to Other Comprehensive Income.

D)Reflected on the income statement.

A)Ignored, since the disposal group will be sold as a whole.

B)Charged to Retained Earnings.

C)Charged to Other Comprehensive Income.

D)Reflected on the income statement.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

55

Intraperiod income tax allocation:

A)Involves the allocation of income taxes between current and future periods.

B)Arises because items included in the determination of taxable income may be presented in different parts of the financial statements.

C)Arises because certain revenues and expenses appear on the financial statements either before or after they are included on the income tax return.

D)Involves items appearing above income from continuing operations in the income statement.

A)Involves the allocation of income taxes between current and future periods.

B)Arises because items included in the determination of taxable income may be presented in different parts of the financial statements.

C)Arises because certain revenues and expenses appear on the financial statements either before or after they are included on the income tax return.

D)Involves items appearing above income from continuing operations in the income statement.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements is/are correct?

A)Each asset and liability forming part of a disposal group must be remeasured individually.

B)All assets and liabilities forming part of a disposal group are remeasured as a whole.

C)Assets held for sale must be shown distinctly from Liabilities held for sale on the balance sheet.Both of these would be classified as non-current assets.

D)Assets and Liabilities held for sale may be netted against each other.

A)Each asset and liability forming part of a disposal group must be remeasured individually.

B)All assets and liabilities forming part of a disposal group are remeasured as a whole.

C)Assets held for sale must be shown distinctly from Liabilities held for sale on the balance sheet.Both of these would be classified as non-current assets.

D)Assets and Liabilities held for sale may be netted against each other.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

57

The issuance of new common shares and retirement of outstanding shares would be reported in comprehensive income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

58

Correction of prior years' errors directly affect the:

A)retained earnings account.

B)extraordinary gains and losses of the period when the correction of prior years' error is made.

C)net income of the period

D)retained earnings account through the period's net income.

A)retained earnings account.

B)extraordinary gains and losses of the period when the correction of prior years' error is made.

C)net income of the period

D)retained earnings account through the period's net income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following may form part of a disposal group?

A)Accounts receivable which are expected to be sold to a factoring company.

B)A discontinued operating segment.

C)Stand-alone assets and liabilities that form a distinct group within part of an operating segment.

D)Both B and C are correct.

A)Accounts receivable which are expected to be sold to a factoring company.

B)A discontinued operating segment.

C)Stand-alone assets and liabilities that form a distinct group within part of an operating segment.

D)Both B and C are correct.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

60

Other comprehensive income includes only unrealized gains and losses.When a previously unrecognized gain or loss is recognized later,this gain or loss will always be included in the company's net income in the year recognized.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

61

Munitions Inc.committed to sell its trade magazine division for $700,000 on October 1,Year 1.The book value of the division's net assets was $800,000.The disposal date is expected to be April 1,Year 2.Year 1 income of the division to October 1,Year 1 was a $30,000 loss,and income for the remainder of the year was $10,000.However,Munitions estimates that the division will lose $25,000 during the remainder of the phase-out period in Year 2.Ignoring taxes choose the correct reporting for discontinued operations in the income statement of Munitions,Inc.,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

62

A review of the December 31,2006,financial statements of a corporation revealed that under the caption "Exceptional and infrequent losses," a total of $130,000 was reported.Further analysis revealed that the $130,000 in losses was comprised of the following items: (1) A loss of $25,000 incurred in the abandonment of equipment formerly used in the business.

(2) An unusual and infrequent occurrence,a loss of $37,500 was sustained as a result of damage to a warehouse by a falling meteorite.

(3) During 2001,several factories were shut down during a major strike by employees.Shutdown expenses totalled $60,000.

(4) Uncollectible accounts receivable of $7,500 were written off as uncollectible.

(5) Foreign exchange - translation gains: $10,000

(6) Decline in market value of Available-for-sale securities: $15,000

Ignoring income taxes,what amount would be shown as Other Comprehensive Income (Loss) on the statement of Comprehensive Income?

A)($5,000)

B)$10,000

C)$15,000

D)$130,000

(2) An unusual and infrequent occurrence,a loss of $37,500 was sustained as a result of damage to a warehouse by a falling meteorite.

(3) During 2001,several factories were shut down during a major strike by employees.Shutdown expenses totalled $60,000.

(4) Uncollectible accounts receivable of $7,500 were written off as uncollectible.

(5) Foreign exchange - translation gains: $10,000

(6) Decline in market value of Available-for-sale securities: $15,000

Ignoring income taxes,what amount would be shown as Other Comprehensive Income (Loss) on the statement of Comprehensive Income?

A)($5,000)

B)$10,000

C)$15,000

D)$130,000

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

63

A company reported the following results of its operations for 2006: Income from continuing operations was:

A)$32,600

B)$27,200

C)$41,600

D)$38,000

Income from continuing operations was:A)$32,600

B)$27,200

C)$41,600

D)$38,000

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

64

A company started business on January 1,2006.At the end of 2006,the accounting records provided the following unadjusted and pre-tax amounts: Sales revenue (cash),$186,000; cost of goods sold,$100,000; expenses (cash),$40,000; accrued wages,$6,000; accrued rent revenue,$2,000; and a 40 percent average income tax rate. What was the net income on accrual basis?

A)$22,800

B)$25,200

C)$27,600

D)$30,000

A)$22,800

B)$25,200

C)$27,600

D)$30,000

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

65

Under IFRS,a discontinued operation must be a:

A)Product line.

B)Geographic segment.

C)Product line or Geographic segment.

D)Cash Generating Unit (CGU).

A)Product line.

B)Geographic segment.

C)Product line or Geographic segment.

D)Cash Generating Unit (CGU).

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

66

Sierra Inc.committed to sell its mountaineering division for $700,000 on October 1,Year 1.The book value of the division's net assets was $800,000.The disposal date is expected to be April 1,Year 2.Year 1 income of the division to October 1,Year 1 was a $30,000 loss,and income for the remainder of the year was a $10,000 loss.Sierra estimates that the division will lose another $25,000 during the remainder of the phase-out period in Year 2.Ignoring taxes choose the correct reporting for discontinued operations in the income statement of Sierra,Inc.,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

67

Given the following amounts from an income statement: The amount shown on a multiple-step format income statement for operating income from continuing operations would be:

A)$232

B)$246

C)$290

D)$302

The amount shown on a multiple-step format income statement for operating income from continuing operations would be:A)$232

B)$246

C)$290

D)$302

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

68

Basic and fully-diluted earnings per share under IFRS must be shown for:

A)Net Income only

B)Total Comprehensive Income

C)Income from continuing operations only

D)Income from continuing operations and net earnings

A)Net Income only

B)Total Comprehensive Income

C)Income from continuing operations only

D)Income from continuing operations and net earnings

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

69

King Corporation decided to sell its sporting goods business segment for $900,000,on September 1,Year 1,which is also the disposal date.The book value of the segment's net assets is $700,000 on this date.The pre-tax income for the segment for the period January 1 - September 1,Year 1,was $20,000.Assuming a tax rate of 40%,choose the correct reporting for discontinued operations in the income statement of King Corporation,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

70

Jacks Corporation decided to sell its playing card business segment for $600,000,on September 1,Year 1.The disposal date is November 1,Year 1.The book value of the segment's net assets is $550,000.The pre-tax income for the segment for the period January 1 - September 1,Year 1,was a loss of $80,000; the pre-tax income for the segment for September and October was $30,000.Assuming a tax rate of 40%,choose the correct reporting for discontinued operations in the income statement of Jacks Corporation,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

71

Under ASPE,foreign exchange translation gains or losses are charged to:

A)Net earnings

B)Retained earnings

C)Other comprehensive Income

D)A separate component of Shareholder equity entitled "Cumulative Translations Gains and Losses"

A)Net earnings

B)Retained earnings

C)Other comprehensive Income

D)A separate component of Shareholder equity entitled "Cumulative Translations Gains and Losses"

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

72

IFRS 5 defines a discontinued operation as an operating segment of a company that:

A)has been sold.

B)is held for sale.

C)has been sold or is held for -sale.

D)is no longer under management control.

A)has been sold.

B)is held for sale.

C)has been sold or is held for -sale.

D)is no longer under management control.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

73

Constructive obligations:

A)Arise from a reasonable expectation that a company will honour certain obligations based on past practices or events.

B)May result from legal requirements.

C)May or may not be legally enforceable.

D)Arise from a reasonable expectation that a company will honour certain obligations based on past practices or events and may or may not be legally enforceable.

A)Arise from a reasonable expectation that a company will honour certain obligations based on past practices or events.

B)May result from legal requirements.

C)May or may not be legally enforceable.

D)Arise from a reasonable expectation that a company will honour certain obligations based on past practices or events and may or may not be legally enforceable.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

74

Future costs associated with a restructuring can only be recognized if they:

A)will lead to a constructive obligation in the future.

B)will lead to a legal obligation in the future.

C)will lead to a constructive and legal obligation in the future.

D)will lead to a provision for restructuring cost.

A)will lead to a constructive obligation in the future.

B)will lead to a legal obligation in the future.

C)will lead to a constructive and legal obligation in the future.

D)will lead to a provision for restructuring cost.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

75

The results from operation of a discontinued segment under IFRS and any gain or loss on disposal or adjustment to fair value of the disposed segment should appear:

A)In one line on the statement of comprehensive income.

B)In two lines on the statement of comprehensive income.

C)in one or two lines on the statement of comprehensive income.

D)shown as part of other comprehensive income.

A)In one line on the statement of comprehensive income.

B)In two lines on the statement of comprehensive income.

C)in one or two lines on the statement of comprehensive income.

D)shown as part of other comprehensive income.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

76

Under IFRS,to qualify as a discontinued operation or disposal group,the proceeds of a sale must:

A)be recovered through a sale transaction.

B)be recovered through continuing use.

C)be recovered through a sale transaction or through continuing use.

D)be made in cash.

A)be recovered through a sale transaction.

B)be recovered through continuing use.

C)be recovered through a sale transaction or through continuing use.

D)be made in cash.

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

77

Given the following amounts from an income statement: The amount shown on a single-step format income statement for income from continuing operations items would be:

A)$46

B)$41

C)$40

D)$35

The amount shown on a single-step format income statement for income from continuing operations items would be:A)$46

B)$41

C)$40

D)$35

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

78

Queen Corporation decided to sell its furniture business segment for $400,000,on September 1,Year 1,which is also the disposal date.The book value of the segment's net assets is $500,000 on this date.The pre-tax income for the segment for the period January 1 - September 1,Year 1,was $150,000.Assuming a tax rate of 40%,choose the correct reporting for discontinued operations in the income statement of Queen Corporation,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

79

A company which lost part of its accounting system in a fire is having trouble determining what its net income is for the current year.The following correct adjusted balances and additional information for the current year are available: Additional information for the year: Other than earnings and the events listed above,no other events or transactions affected owners' Equity in the current year.What was net income for the current year?

A)$12,000

B)$22,000

C)$17,000

D)$16,000

Additional information for the year: Other than earnings and the events listed above,no other events or transactions affected owners' Equity in the current year.What was net income for the current year?A)$12,000

B)$22,000

C)$17,000

D)$16,000

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

80

Ace Corporation decided to sell its medical supplies business segment for $500,000,on September 1,Year 1.The disposal date is November 1,Year 1.The book value of the segment's net assets is $650,000.The pre-tax income for the segment for the period January 1 - September 1,Year 1,was a loss of $90,000; the pre-tax income for the segment for September and October was a loss of $20,000.Assuming a tax rate of 40%,choose the correct reporting for discontinued operations in the income statement of Ace Corporation,for the year ended December 31,Year 1.

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

A)Choice 1

B)Choice 2

C)Choice 3

D)Choice 4

Unlock Deck

Unlock for access to all 130 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 130 flashcards in this deck.