Deck 8: Property Dispositions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Irby Inc. was incorporated in 2005 and adopted a calendar year. Here is a schedule of Irby's net Section 1231 gains and (losses) reported on its tax returns through 2010.  In 2011, Irby recognized a $14,750 gain on the sale of business land. How is this gain characterized on Irby's tax return?

In 2011, Irby recognized a $14,750 gain on the sale of business land. How is this gain characterized on Irby's tax return?

A) $14,750 Section 1231 gain

B) $10,890 ordinary gain and $9,415 Section 1231 gain

C) $14,750 ordinary gain

D) None of the above

In 2011, Irby recognized a $14,750 gain on the sale of business land. How is this gain characterized on Irby's tax return?A) $14,750 Section 1231 gain

B) $10,890 ordinary gain and $9,415 Section 1231 gain

C) $14,750 ordinary gain

D) None of the above

Question

Question

Question

Question

Proctor Inc. was incorporated in 2004 and adopted a calendar year. Here is a schedule of Proctor's net Section 1231 gains and (losses) reported on its tax returns through 2009.  In 2010, Proctor recognized a $25,000 gain on the sale of business land. How is this gain characterized on Proctor's tax return?

In 2010, Proctor recognized a $25,000 gain on the sale of business land. How is this gain characterized on Proctor's tax return?

A) $25,000 Section 1231 gain

B) $19,700 ordinary gain and $5,300 Section 1231 gain

C) $15,900 ordinary gain and $9,100 Section 1231 gain

D) $25,000 ordinary gain

In 2010, Proctor recognized a $25,000 gain on the sale of business land. How is this gain characterized on Proctor's tax return?A) $25,000 Section 1231 gain

B) $19,700 ordinary gain and $5,300 Section 1231 gain

C) $15,900 ordinary gain and $9,100 Section 1231 gain

D) $25,000 ordinary gain

Question

Delour Inc. was incorporated in 2004 and adopted a calendar year. Here is a schedule of Delour's net Section 1231 gains and (losses) reported on its tax returns through 2009.  In 2010, Delour recognized a $50,000 gain on the sale of business land. How is this gain characterized on Delour's tax return?

In 2010, Delour recognized a $50,000 gain on the sale of business land. How is this gain characterized on Delour's tax return?

A) $50,000 Section 1231 gain

B) $12,000 ordinary gain and $38,000 Section 1231 gain

C) $16,900 ordinary gain and $33,100 Section 1231 gain

D) $50,000 ordinary gain

In 2010, Delour recognized a $50,000 gain on the sale of business land. How is this gain characterized on Delour's tax return?A) $50,000 Section 1231 gain

B) $12,000 ordinary gain and $38,000 Section 1231 gain

C) $16,900 ordinary gain and $33,100 Section 1231 gain

D) $50,000 ordinary gain

Question

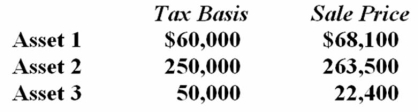

R&T Inc. made the following sales of capital assets this year.  What is the effect of the three sales on R&T's taxable income this year?

What is the effect of the three sales on R&T's taxable income this year?

A) $21,600 increase

B) $12,900 increase

C) No effect

D) None of the above

What is the effect of the three sales on R&T's taxable income this year?A) $21,600 increase

B) $12,900 increase

C) No effect

D) None of the above

Question

Question

Question

Question

Question

Question

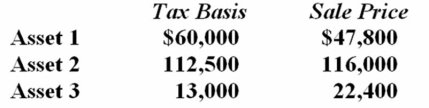

Gupta Company made the following sales of capital assets this year.  What is the effect of the three sales on Gupta's taxable income?

What is the effect of the three sales on Gupta's taxable income?

A) $700 increase

B) $12,900 increase

C) No effect

D) None of the above

What is the effect of the three sales on Gupta's taxable income?A) $700 increase

B) $12,900 increase

C) No effect

D) None of the above

Question

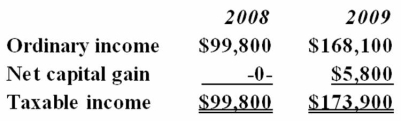

Fantino Inc. was incorporated in 2008 and adopted a calendar year for tax purposes. Here is a schedule of Fantino's taxable income for 2008 and 2009.  In 2010, Fantino generated $297,300 ordinary income and recognized a $14,000 net capital loss. Which of the following statements is true?

In 2010, Fantino generated $297,300 ordinary income and recognized a $14,000 net capital loss. Which of the following statements is true?

A) Fantino can deduct its $14,000 net capital loss only on a carryforward basis.

B) Fantino can carry the net capital loss back to 2008 and receive a $4,760 refund of 2008 tax.

C) Fantino can carry the net capital loss back to 2009 and receive a $5,460 refund of 2009 tax.

D) Fantino can carry the net capital loss back to 2009 and receive a $2,262 refund of 2009 tax.

In 2010, Fantino generated $297,300 ordinary income and recognized a $14,000 net capital loss. Which of the following statements is true?A) Fantino can deduct its $14,000 net capital loss only on a carryforward basis.

B) Fantino can carry the net capital loss back to 2008 and receive a $4,760 refund of 2008 tax.

C) Fantino can carry the net capital loss back to 2009 and receive a $5,460 refund of 2009 tax.

D) Fantino can carry the net capital loss back to 2009 and receive a $2,262 refund of 2009 tax.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/110

Play

Full screen (f)

Deck 8: Property Dispositions

1

A taxpayer that is using the installment sale method to recognize gain must recompute the gross profit percentage every year during the term of the installment note.

False

2

The use of the installment sale method can result in an unfavorable difference between book income and taxable income in the year of sale.

False

3

A corporation can use the installment sale method of accounting for both book and tax purposes.

False

4

Kopel Company transferred an inventory asset to Cassim LLC in exchange for Cassim's $230,000 interest-bearing note. Kopel's tax basis in the note is its $230,000 face value.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

5

Mr. and Mrs. Plame sold an investment asset to their grandson Leonard. Because Leonard is a related party, the Plames do not recognize any gain or loss realized on sale.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

6

The installment sale method of accounting is not applicable to realized losses.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

7

The characterization of income as ordinary or capital gain has no relevance for financial reporting purposes.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

8

Both corporate and individual taxpayers can carry back a net capital loss to the three prior taxable years.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

9

The same asset may be an ordinary asset in the hands of one taxpayer and a capital asset in the hands of a different taxpayer.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

10

Mr. Hickem sold an investment asset worth $20,000. The purchaser paid Mr. Hickem by giving him $12,500 cash and an oil painting worth $7,500. Mr. Hickem's amount realized on sale is $12,500.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

11

Sandy Cole realized a loss on sale of an investment asset to her mother, Lynne. If the facts and circumstances prove that the selling price was an arm's length market price, Sandy can recognize the loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

12

According to the realization principle, an increase in the value of an asset is not accounted for as income unless the amount of the increase can be accurately measured.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

13

The gain or loss recognized on any disposition of a capital asset is characterized as capital gain or loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

14

Four years ago, Mrs. Beights purchased marketable securities for $75,000 cash. At the end of 2011, the FMV of the securities had plummeted to $4,000. Mrs. Beights may elect to recognize her $71,000 loss in 2011, even though she still owns the securities.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

15

Both corporate and individual taxpayers can deduct capital losses to the extent of capital gains.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

16

Gain or loss realized on the disposition of property is recognized unless the tax law provides a nonrecognition exception.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

17

N&B Inc. sold land worth $385,000. The purchaser paid $80,000 cash and assumed N&B's $305,000 mortgage on the land. N&B's amount realized on sale is $385,000.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

18

Every gain or loss realized on the disposition of property is ultimately characterized as either ordinary or capital for tax purposes.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

19

Mrs. Lex realized a $78,400 gain on sale of investment land to S&T, which issued a 10-year note in full payment. Mrs. Lex must recognize the gain in the year of sale unless she elects to use the installment sale method to recognize gain over the term of the note.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

20

For tax purposes, every asset is a capital asset unless it falls into one of eight categories of noncapital assets.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

21

Mr. Jason realized a gain on sale of a residential apartment complex that he had placed in service in 1993. Accumulated MACRS depreciation on the complex was $311,800. The entire gain is characterized as Section 1231 gain.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

22

Ms. Cregg has a $43,790 basis in 2,460 shares of ABD Inc. common stock. ABD recently declared bankruptcy and announced that its common stock is worthless. As a result, Ms. Cregg can recognize a $43,790 ordinary loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

23

Netelli Inc. owned a tract of land with a $175,000 basis that was subject to a $228,500 nonrecourse mortgage. Netelli defaulted on the mortgage, and the creditor foreclosed on the land. Netelli must recognize a $53,500 gain on the disposition of the land.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

24

The general rule is that a net Section 1231 loss is treated as a capital loss and a net Section 1231 gain is treated as ordinary income.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

25

Milton Inc. recognized a $16,900 gain on sale of depreciable equipment held for three years. If Milton's accumulated MACRS depreciation on the equipment is $16,900 or more, the entire gain is ordinary income.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

26

Milton Inc. recognized a $1,300 net Section 1231 loss in 2011. If Milton recognizes a $5,000 net Section 1231 gain in 2012, it must characterize $1,300 as ordinary income.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

27

A fire destroyed business equipment that was worth $160,000 and had a $118,100 adjusted tax basis. The equipment was uninsured. The owner can recognize a $160,000 ordinary casualty loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

28

Verno Inc. purchased business equipment in March and sold it in November. Verno's gain or loss recognized on the sale is ordinary.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

29

Tullia Inc. recognized $500,000 ordinary income, $22,600 net Section 1231 gain, and $6,000 net capital loss this year. Tullia's taxable income is $522,600.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

30

Langtry Corporation recognized $798,000 ordinary income, $13,000 net Section 1231 loss, and $6,000 net capital loss this year. Langtry's taxable income is $785,000.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

31

Abada Inc. has a $925,000 basis in 100% of the stock of AbWest Inc., which derives all its income from a manufacturing activity. If Abada determines that the AbWest stock is worthless, it can recognize a $925,000 ordinary loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

32

JG Inc. recognized $690,000 ordinary income, $48,000 net Section 1231 gain, and $77,000 net capital loss this year. JG's taxable income is $690,000.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

33

The sale of business inventory always generates ordinary income or loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

34

CBM Inc. realized a $429,000 gain on sale of a commercial office building that the corporation placed in service in 1993. Accumulated MACRS depreciation on the complex was $311,800. The entire gain is characterized as Section 1231 gain.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

35

Both corporate and individual taxpayers may be taxed at a preferential rate on net capital gain.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

36

A fire destroyed business equipment that was worth $100,000 and had a $118,100 adjusted tax basis. The equipment was uninsured. The owner can recognize a $118,100 ordinary casualty loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

37

A taxpayer cannot compute its net Section 1231 gain or loss for a taxable year until the year closes.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

38

Because land is nondepreciable, it is always a capital asset.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

39

Stone Company recognized a $7,700 loss on sale of depreciable equipment held for three years. If Stone's accumulated MACRS depreciation on the equipment is $7,700 or more, the entire loss is ordinary.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

40

The abandonment of business equipment with a $6,019 adjusted basis results in a $6,019 Section 1231 loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

41

A casualty loss realized on the destruction of depreciable business property is characterized as a Section 1231 loss.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

42

Mr. Quick sold marketable securities with a $112,900 tax basis to his 100% owned corporation for $95,000 cash. Which of the following statements is true?

A) If Mr. Quick can offer evidence that the FMV of the securities is $95,000, he can recognize his $17,900 realized loss.

B) If Mr. Quick and his corporation negotiated the terms of the sale at arm's length, Mr. Quick can recognize his $17,900 realized loss.

C) The corporation's tax basis in the securities is $112,900.

D) None of the above is true.

A) If Mr. Quick can offer evidence that the FMV of the securities is $95,000, he can recognize his $17,900 realized loss.

B) If Mr. Quick and his corporation negotiated the terms of the sale at arm's length, Mr. Quick can recognize his $17,900 realized loss.

C) The corporation's tax basis in the securities is $112,900.

D) None of the above is true.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

43

In 2011, TPC Inc. sold investment land with a $388,000 book and tax basis for $523,000. The purchaser paid $60,000 in cash and gave TPC a note for the $463,000 balance of the price. In 2012, TPC received a $67,800 payment on the note ($40,000 principal + $27,800 interest). In 2012, TPC's use of the installment sale method results in a:

A) $10,325 favorable permanent book/tax difference

B) $17,496 unfavorable temporary difference

C) $17,496 favorable temporary difference

D) None of the above

A) $10,325 favorable permanent book/tax difference

B) $17,496 unfavorable temporary difference

C) $17,496 favorable temporary difference

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

44

Lenoci Inc. paid $310,000 for equipment three years ago. This year, it sold the equipment for $200,000. Through date of sale, accumulated book depreciation was $93,840 and accumulated tax depreciation was $147,327. Which of the following statements is true?

A) The sale results in a $53,487 favorable temporary book/tax difference.

B) The sale results in a $53,487 unfavorable temporary book/tax difference.

C) The sale results in a $53,487 unfavorable permanent book/tax difference.

D) None of the above is true.

A) The sale results in a $53,487 favorable temporary book/tax difference.

B) The sale results in a $53,487 unfavorable temporary book/tax difference.

C) The sale results in a $53,487 unfavorable permanent book/tax difference.

D) None of the above is true.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

45

Noble Inc. paid $310,000 for equipment three years ago. This year, it sold the equipment for $200,000. Through date of sale, accumulated book depreciation was $93,840 and accumulated tax depreciation was $147,327. Assuming a 35% tax rate, what is the effect of the sale on Noble's deferred tax accounts?

A) $18,720 increase in deferred tax assets

B) $18,720 increase in deferred tax liabilities

C) $18,720 decrease in deferred tax liabilities

D) No effect on deferred tax accounts

A) $18,720 increase in deferred tax assets

B) $18,720 increase in deferred tax liabilities

C) $18,720 decrease in deferred tax liabilities

D) No effect on deferred tax accounts

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

46

The installment sale method of accounting applies to which of the following?

A) $89,300 gain realized on sale of business inventory.

B) $798,600 gain realized on sale of common stock in a publicly held corporation.

C) $(41,500) loss realized on sale of land used in a trade or business.

D) None of the above

A) $89,300 gain realized on sale of business inventory.

B) $798,600 gain realized on sale of common stock in a publicly held corporation.

C) $(41,500) loss realized on sale of land used in a trade or business.

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

47

Winslow Company sold investment land to an unrelated purchaser. The purchaser paid $250,000 cash, assumed Winslow's $600,000 mortgage on the land, and gave Winslow its $580,000 ten-year, interest-bearing note. Compute Winslow's amount realized on sale.

A) $250,000

B) $830,000

C) $850,000

D) $1,430,000

A) $250,000

B) $830,000

C) $850,000

D) $1,430,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

48

Mrs. Beld sold marketable securities with a $79,600 tax basis to her daughter for $60,000 cash. Two years later, the daughter sold the securities through her broker for $93,000. Compute the daughter's gain recognized on sale.

A) $13,400

B) $19,600

C) $33,000

D) None of the above

A) $13,400

B) $19,600

C) $33,000

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

49

This year, Ms Lucas sold investment land for $125,000 cash plus the purchaser's assumption of a $50,000 mortgage on the land. Ms. Lucas's tax basis in the land was $93,000. If any recognized gain is taxed at 15 percent, compute the after-tax cash flow from the sale.

A) $62,300

B) $69,700

C) $112,700

D) $162,700

A) $62,300

B) $69,700

C) $112,700

D) $162,700

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

50

O&V sold a business asset with a $78,300 adjusted tax basis for $100,000. The purchaser paid $30,000 in cash and gave O&V a note for the $70,000 balance of the price. O&V will not receive a payment on the note until next year. Compute O&V's gain recognized under the installment sale method.

A) $7,690

B) $6,510

C) $4,920

D) None of the above

A) $7,690

B) $6,510

C) $4,920

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

51

Mr. Quick sold marketable securities with a $112,900 tax basis to his son for $95,000 cash. Two years later, the son sold the securities through his broker for $90,000. Compute the son's loss recognized on sale.

A) -0-

B) $5,000

C) $22,900

D) None of the above

A) -0-

B) $5,000

C) $22,900

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

52

Six years ago, Alejo Company purchased real property by paying $250,000 cash and giving the seller its $1 million note for the balance of the purchase price. This year, Alejo deducted $30,800 depreciation on the property and made a $125,000 principal payment on the note. Which of the following statements is false?

A) The depreciation deduction reduced Alejo's adjusted tax basis in the real property.

B) The principal payment increased Alejo's equity in the real property.

C) The principal payment reduced Alejo's tax basis in the real property and the balance due on the note.

D) None of the above statements is false.

A) The depreciation deduction reduced Alejo's adjusted tax basis in the real property.

B) The principal payment increased Alejo's equity in the real property.

C) The principal payment reduced Alejo's tax basis in the real property and the balance due on the note.

D) None of the above statements is false.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

53

Warsham Inc. sold land with a $300,000 basis to Sara Phillips for $117,000 cash. Sara owns 68 percent of Warsham's outstanding stock. Which of the following statements is true?

A) Warsham cannot recognize its $183,000 realized loss on sale on its current year tax return.

B) Warsham does not report the $183,000 realized loss on its current year financial statements.

C) The $183,000 loss is an unfavorable temporary difference between Warsham's book and tax income.

D) Both a. and c. are true.

A) Warsham cannot recognize its $183,000 realized loss on sale on its current year tax return.

B) Warsham does not report the $183,000 realized loss on its current year financial statements.

C) The $183,000 loss is an unfavorable temporary difference between Warsham's book and tax income.

D) Both a. and c. are true.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

54

The installment sale method of accounting does not apply to which of the following sales?

A) Sale of 12-acre tract of land held as inventory by a real estate developer

B) Sale of business equipment

C) Sale of U.S. Treasury notes

D) The method does not apply to a. and c.

A) Sale of 12-acre tract of land held as inventory by a real estate developer

B) Sale of business equipment

C) Sale of U.S. Treasury notes

D) The method does not apply to a. and c.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

55

Dolzer Inc. sold a business asset with a $474,000 adjusted book and tax basis for $775,000. The purchaser paid $100,000 in cash and gave Dolzer a note for the $675,000 balance of the price. Dolzer will not receive a payment on the note until next year. Assuming that Dolzer uses the installment sale method, compute Dolzer's book and tax gain in the year of sale.

A) Book gain $301,000; tax gain $100,000

B) Book and tax gain $38,839

C) Book gain $301,000; tax gain $38,839

D) None of the above

A) Book gain $301,000; tax gain $100,000

B) Book and tax gain $38,839

C) Book gain $301,000; tax gain $38,839

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

56

In 2007, ChaGo Inc. sold a business asset with a $39,400 adjusted tax basis for $130,000. The purchaser paid $50,000 cash and gave ChaGo a note for the $80,000 balance of the price. ChaGo is using the installment sale method to recognize its gain on sale. This year, ChaGo sold the note to a financial institution for the note's $55,000 face value (ChaGo had received a total of $25,000 principal payments on the note.) Compute ChaGo's gain recognized on sale of the installment note.

A) -0-

B) $38,332

C) $52,268

D) $55,000

A) -0-

B) $38,332

C) $52,268

D) $55,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

57

In 2011, TPC Inc. sold investment land with a $474,000 book and tax basis for $775,000. The purchaser paid $100,000 in cash and gave TPC a note for the $675,000 balance of the price. In 2012, TPC received a $105,500 payment on the note ($67,500 principal + $38,000 interest). Assuming that TPC is using the installment sale method, compute its gain recognized in 2011.

A) $26,216

B) $40,976

C) $67,500

D) None of the above

A) $26,216

B) $40,976

C) $67,500

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

58

Skeen Company paid $90,000 for tangible personalty three years ago and elected to expense and deduct the cost under Section 179. This year, Skeen sold the personalty for $52,700. Accumulated book depreciation through date of sale was $31,000. What is the effect of the sale on Skeen's book income and taxable income?

A) $6,300 book loss: $52,700 tax gain

B) $6,300 book loss; -0- tax gain

C) $6,300 book and tax gain

D) None of the above

A) $6,300 book loss: $52,700 tax gain

B) $6,300 book loss; -0- tax gain

C) $6,300 book and tax gain

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

59

Philp Inc. sold equipment with a $132,900 adjusted tax basis for $200,000. The purchaser paid $20,000 in cash and assumed Philp's $180,000 mortgage on the asset. Compute Philp's net cash flow from the sale assuming a 35% tax rate.

A) $23,485

B) $20,000

C) -0-

D) None of the above

A) $23,485

B) $20,000

C) -0-

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

60

O&V sold an asset with a $78,300 adjusted tax basis for $100,000. The purchaser paid $30,000 in cash and assumed O&V's $70,000 mortgage on the asset. Compute O&V's net cash flow from the sale assuming a 35% tax rate.

A) $22,405

B) $13,095

C) $14,105

D) None of the above

A) $22,405

B) $13,095

C) $14,105

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

61

"Tiny Dancer" is the name of a bronze figurine created by artist Diego Ossa. The owner recently recognized a $43,500 gain on sale of the figurine. Which of the following statements is false?

A) If Diego Ossa was the seller, the gain is ordinary.

B) If a commercial art gallery that had held Tiny Dancer in its inventory was the seller, the gain is ordinary.

C) If a private collector who purchased Tiny Dancer from an art gallery was the seller, the gain is capital gain.

D) None of the above is false.

A) If Diego Ossa was the seller, the gain is ordinary.

B) If a commercial art gallery that had held Tiny Dancer in its inventory was the seller, the gain is ordinary.

C) If a private collector who purchased Tiny Dancer from an art gallery was the seller, the gain is capital gain.

D) None of the above is false.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

62

Mr. and Mrs. Sykes operate a very profitable small business. This year, the Sykes recognized a $100,000 gain on sale of a trade name they had created and copyrighted for use in their business in 1994. Which of the following statements is true?

A) The $100,000 gain is capital gain eligible for a preferential tax rate.

B) The $100,000 gain is capital gain against which the Sykes can deduct any capital losses recognized this year.

C) The $100,000 gain is ordinary business income.

D) Statements a. and b. are true.

A) The $100,000 gain is capital gain eligible for a preferential tax rate.

B) The $100,000 gain is capital gain against which the Sykes can deduct any capital losses recognized this year.

C) The $100,000 gain is ordinary business income.

D) Statements a. and b. are true.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following assets is not a Section 1231 asset?

A) Business equipment held for four years

B) Office furniture held for eight months

C) Land used in a business and held for 16 years

D) All of the above are Section 1231 assets

A) Business equipment held for four years

B) Office furniture held for eight months

C) Land used in a business and held for 16 years

D) All of the above are Section 1231 assets

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is a capital asset?

A) Supplies used in a business

B) Business inventory

C) Land used in a business

D) None of the above

A) Supplies used in a business

B) Business inventory

C) Land used in a business

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

65

Irby Inc. was incorporated in 2005 and adopted a calendar year. Here is a schedule of Irby's net Section 1231 gains and (losses) reported on its tax returns through 2010. In 2011, Irby recognized a $14,750 gain on the sale of business land. How is this gain characterized on Irby's tax return?

A) $14,750 Section 1231 gain

B) $10,890 ordinary gain and $9,415 Section 1231 gain

C) $14,750 ordinary gain

D) None of the above

In 2011, Irby recognized a $14,750 gain on the sale of business land. How is this gain characterized on Irby's tax return?A) $14,750 Section 1231 gain

B) $10,890 ordinary gain and $9,415 Section 1231 gain

C) $14,750 ordinary gain

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

66

Benlow Company., a calendar year taxpayer, sold two operating assets this year. The first sale generated a $19,200 Section 1231 loss, and the second sale generated a $33,600 Section 1231 gain. As a result of these sales, Benlow should recognize:

A) $19,200 ordinary loss and $33,600 gain treated as capital gain.

B) $14,400 gain treated as capital gain.

C) $14,400 ordinary income.

D) None of the above

A) $19,200 ordinary loss and $33,600 gain treated as capital gain.

B) $14,400 gain treated as capital gain.

C) $14,400 ordinary income.

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

67

Schatz Corporation generated $8,083,000 ordinary business income and recognized a $73,900 net capital gain on the sale of assets. Which of the following statements is true?

A) Schatz must pay tax at the regular corporate rates on $8,156,900 taxable income.

B) Schatz must pay tax at the regular corporate rates on $8,083,000 taxable income. The $73,900 capital gain is eligible for a preferential tax rate.

C) Schatz's net capital gain results in a permanent book/tax difference.

D) None of the above is true.

A) Schatz must pay tax at the regular corporate rates on $8,156,900 taxable income.

B) Schatz must pay tax at the regular corporate rates on $8,083,000 taxable income. The $73,900 capital gain is eligible for a preferential tax rate.

C) Schatz's net capital gain results in a permanent book/tax difference.

D) None of the above is true.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following is a Section 1231 asset?

A) Business inventory

B) Business accounts receivable

C) Supplies used in a business

D) None of the above is a Section 1231 asset

A) Business inventory

B) Business accounts receivable

C) Supplies used in a business

D) None of the above is a Section 1231 asset

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

69

Proctor Inc. was incorporated in 2004 and adopted a calendar year. Here is a schedule of Proctor's net Section 1231 gains and (losses) reported on its tax returns through 2009. In 2010, Proctor recognized a $25,000 gain on the sale of business land. How is this gain characterized on Proctor's tax return?

A) $25,000 Section 1231 gain

B) $19,700 ordinary gain and $5,300 Section 1231 gain

C) $15,900 ordinary gain and $9,100 Section 1231 gain

D) $25,000 ordinary gain

In 2010, Proctor recognized a $25,000 gain on the sale of business land. How is this gain characterized on Proctor's tax return?A) $25,000 Section 1231 gain

B) $19,700 ordinary gain and $5,300 Section 1231 gain

C) $15,900 ordinary gain and $9,100 Section 1231 gain

D) $25,000 ordinary gain

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

70

Delour Inc. was incorporated in 2004 and adopted a calendar year. Here is a schedule of Delour's net Section 1231 gains and (losses) reported on its tax returns through 2009. In 2010, Delour recognized a $50,000 gain on the sale of business land. How is this gain characterized on Delour's tax return?

A) $50,000 Section 1231 gain

B) $12,000 ordinary gain and $38,000 Section 1231 gain

C) $16,900 ordinary gain and $33,100 Section 1231 gain

D) $50,000 ordinary gain

In 2010, Delour recognized a $50,000 gain on the sale of business land. How is this gain characterized on Delour's tax return?A) $50,000 Section 1231 gain

B) $12,000 ordinary gain and $38,000 Section 1231 gain

C) $16,900 ordinary gain and $33,100 Section 1231 gain

D) $50,000 ordinary gain

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

71

R&T Inc. made the following sales of capital assets this year. What is the effect of the three sales on R&T's taxable income this year?

A) $21,600 increase

B) $12,900 increase

C) No effect

D) None of the above

What is the effect of the three sales on R&T's taxable income this year?A) $21,600 increase

B) $12,900 increase

C) No effect

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

72

This year, Izard Company sold equipment purchased in 2008 at a cost of $48,500. Accumulated depreciation through date of sale was $18,900. Which of the following statements is false?

A) If the sale price was $25,000, Izard recognized $4,600 Section 1231 loss.

B) If the sale price was $42,500, Izard recognized $18,900 Section 1231 gain.

C) If the sale price was $50,000, Izard recognized $18,900 ordinary gain and $1,500 Section 1231 gain.

D) None of the above is false.

A) If the sale price was $25,000, Izard recognized $4,600 Section 1231 loss.

B) If the sale price was $42,500, Izard recognized $18,900 Section 1231 gain.

C) If the sale price was $50,000, Izard recognized $18,900 ordinary gain and $1,500 Section 1231 gain.

D) None of the above is false.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

73

Hugo Inc., a calendar year taxpayer, sold two operating assets this year. The first sale generated a $38,700 Section 1231 gain, and the second sale generated a $59,400 Section 1231 loss. As a result of these sales, Hugo should recognize:

A) $20,700 ordinary loss

B) $38,700 Section 1231 gain treated as capital gain and $59,400 ordinary loss

C) $20,700 capital loss

D) None of the above

A) $20,700 ordinary loss

B) $38,700 Section 1231 gain treated as capital gain and $59,400 ordinary loss

C) $20,700 capital loss

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

74

This year, Adula Company sold equipment purchased in 2008 at a cost of $117,200. Accumulated depreciation through date of sale was $33,000. Which of the following statements is false?

A) If the sale price was $90,000, Adula recognized $5,800 ordinary gain.

B) If the sale price was $120,000 Adula recognized $33,000 ordinary gain and $2,800 Section 1231 gain.

C) If the sale price was $80,000, Adula recognized $4,200 ordinary loss.

D) None of the above is false.

A) If the sale price was $90,000, Adula recognized $5,800 ordinary gain.

B) If the sale price was $120,000 Adula recognized $33,000 ordinary gain and $2,800 Section 1231 gain.

C) If the sale price was $80,000, Adula recognized $4,200 ordinary loss.

D) None of the above is false.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following is a capital asset?

A) Accounts receivable of an accrual basis business

B) Business equipment

C) Self-created goodwill

D) Purchased goodwill

A) Accounts receivable of an accrual basis business

B) Business equipment

C) Self-created goodwill

D) Purchased goodwill

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

76

Norbett Inc. generated $15,230,000 ordinary taxable income and realized a $238,000 net capital loss on the sale of marketable securities this year. Which of the following statements is false?

A) Norbett's net income per books includes the $238,000 net capital loss.

B) Norbett's taxable income is $15,230,000.

C) The $238,000 net capital loss is a favorable book/tax difference.

D) The $238,000 net capital loss is a temporary book/tax difference.

A) Norbett's net income per books includes the $238,000 net capital loss.

B) Norbett's taxable income is $15,230,000.

C) The $238,000 net capital loss is a favorable book/tax difference.

D) The $238,000 net capital loss is a temporary book/tax difference.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

77

Gupta Company made the following sales of capital assets this year. What is the effect of the three sales on Gupta's taxable income?

A) $700 increase

B) $12,900 increase

C) No effect

D) None of the above

What is the effect of the three sales on Gupta's taxable income?A) $700 increase

B) $12,900 increase

C) No effect

D) None of the above

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

78

Fantino Inc. was incorporated in 2008 and adopted a calendar year for tax purposes. Here is a schedule of Fantino's taxable income for 2008 and 2009. In 2010, Fantino generated $297,300 ordinary income and recognized a $14,000 net capital loss. Which of the following statements is true?

A) Fantino can deduct its $14,000 net capital loss only on a carryforward basis.

B) Fantino can carry the net capital loss back to 2008 and receive a $4,760 refund of 2008 tax.

C) Fantino can carry the net capital loss back to 2009 and receive a $5,460 refund of 2009 tax.

D) Fantino can carry the net capital loss back to 2009 and receive a $2,262 refund of 2009 tax.

In 2010, Fantino generated $297,300 ordinary income and recognized a $14,000 net capital loss. Which of the following statements is true?A) Fantino can deduct its $14,000 net capital loss only on a carryforward basis.

B) Fantino can carry the net capital loss back to 2008 and receive a $4,760 refund of 2008 tax.

C) Fantino can carry the net capital loss back to 2009 and receive a $5,460 refund of 2009 tax.

D) Fantino can carry the net capital loss back to 2009 and receive a $2,262 refund of 2009 tax.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

79

Rizzi Corporation sold a capital asset with a $692,000 book and tax basis for $650,000 cash. This was Rizzi's only asset sale during the year. The sale results in:

A) $42,000 unfavorable permanent book/tax difference

B) $42,000 unfavorable temporary book/tax difference

C) $42,000 favorable permanent book/tax difference

D) No book/tax difference

A) $42,000 unfavorable permanent book/tax difference

B) $42,000 unfavorable temporary book/tax difference

C) $42,000 favorable permanent book/tax difference

D) No book/tax difference

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

80

In its current tax year, PRS Corporation generated $300,000 ordinary income from the performance of consulting services for its clients. PRS sold two assets, recognizing a $20,000 gain on the first sale and a $31,000 loss on the second sale. Which of the following statements is false?

A) If the gain and loss were capital gain and loss, PRS's taxable income was $300,000.

B) If the gain was capital gain and the loss was ordinary, PRS's taxable income was $269,000.

C) If the gain and loss were ordinary, PRS's taxable income was $289,000.

D) If the gain was ordinary and the loss was a capital loss, PRS's taxable income was $320,000.

A) If the gain and loss were capital gain and loss, PRS's taxable income was $300,000.

B) If the gain was capital gain and the loss was ordinary, PRS's taxable income was $269,000.

C) If the gain and loss were ordinary, PRS's taxable income was $289,000.

D) If the gain was ordinary and the loss was a capital loss, PRS's taxable income was $320,000.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 110 flashcards in this deck.