Deck 9: Nontaxable Exchanges

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

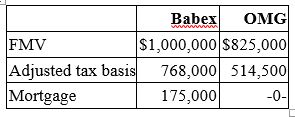

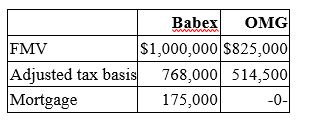

Babex Inc. and OMG Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute OMG's gain recognized on the exchange and its tax basis in the property received from Babex.

Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute OMG's gain recognized on the exchange and its tax basis in the property received from Babex.

A) $175,000 gain recognized; $514,500 basis in Babex property

B) No gain recognized; $689,500 basis in Babex property

C) No gain recognized; $514,500 basis in Babex property

D) None of the above.

Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute OMG's gain recognized on the exchange and its tax basis in the property received from Babex.A) $175,000 gain recognized; $514,500 basis in Babex property

B) No gain recognized; $689,500 basis in Babex property

C) No gain recognized; $514,500 basis in Babex property

D) None of the above.

Question

Question

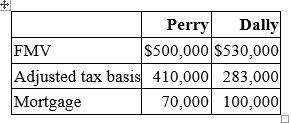

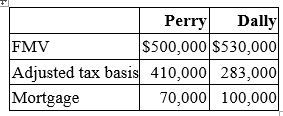

Perry Inc. and Dally Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Perry's gain recognized on the exchange and its tax basis in the property received from Dally.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Perry's gain recognized on the exchange and its tax basis in the property received from Dally.

A) No gain recognized; $410,000 basis in the Dally property

B) No gain recognized; $440,000 basis in the Dally property

C) $100,000 gain recognized; $410,000 basis in the Dally property

D) None of the above.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Perry's gain recognized on the exchange and its tax basis in the property received from Dally.A) No gain recognized; $410,000 basis in the Dally property

B) No gain recognized; $440,000 basis in the Dally property

C) $100,000 gain recognized; $410,000 basis in the Dally property

D) None of the above.

Question

Question

Question

Babex Inc. and OMG Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute Babex's gain recognized on the exchange and its tax basis in the property received from OMG.

Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute Babex's gain recognized on the exchange and its tax basis in the property received from OMG.

A) $175,000 gain recognized; $768,000 basis in OMG property

B) No gain recognized; $768,000 basis in OMG property

C) $175,000 gain recognized; $943,000 basis in OMG property

D) None of the above.

Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute Babex's gain recognized on the exchange and its tax basis in the property received from OMG.A) $175,000 gain recognized; $768,000 basis in OMG property

B) No gain recognized; $768,000 basis in OMG property

C) $175,000 gain recognized; $943,000 basis in OMG property

D) None of the above.

Question

Question

Question

Question

Question

Perry Inc. and Dally Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Dally's gain recognized on the exchange and its tax basis in the property received from Perry.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Dally's gain recognized on the exchange and its tax basis in the property received from Perry.

A) $30,000 gain recognized; $313,000 basis in the Perry property

B) 100,000 gain recognized; $383,000 basis in the Perry property

C) $30,000 gain recognized; $283,000 basis in the Perry property

D) None of the above.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Dally's gain recognized on the exchange and its tax basis in the property received from Perry.A) $30,000 gain recognized; $313,000 basis in the Perry property

B) 100,000 gain recognized; $383,000 basis in the Perry property

C) $30,000 gain recognized; $283,000 basis in the Perry property

D) None of the above.

Question

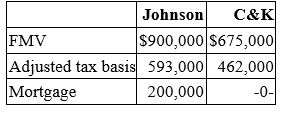

Johnson Inc. and C&K Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute C&K's gain recognized on the exchange and its tax basis in the property received from Johnson.

Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute C&K's gain recognized on the exchange and its tax basis in the property received from Johnson.

A) $200,000 gain recognized; $662,000 basis in Johnson property

B) No gain recognized; $462,000 basis in Johnson property

C) No gain recognized; $487,000 basis in Johnson property

D) None of the above.

Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute C&K's gain recognized on the exchange and its tax basis in the property received from Johnson.A) $200,000 gain recognized; $662,000 basis in Johnson property

B) No gain recognized; $462,000 basis in Johnson property

C) No gain recognized; $487,000 basis in Johnson property

D) None of the above.

Question

Question

Question

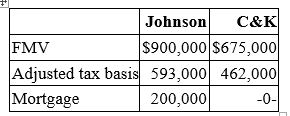

Johnson Inc. and C&K Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute Johnson's gain recognized on the exchange and its tax basis in the property received from C&K.

Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute Johnson's gain recognized on the exchange and its tax basis in the property received from C&K.

A) $25,000 gain recognized; $593,000 basis in C&K property

B) $25,000 gain recognized; $793,000 basis in C&K property

C) $225,000 gain recognized; $593,000 basis in C&K property

D) None of the above.

Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute Johnson's gain recognized on the exchange and its tax basis in the property received from C&K.A) $25,000 gain recognized; $593,000 basis in C&K property

B) $25,000 gain recognized; $793,000 basis in C&K property

C) $225,000 gain recognized; $593,000 basis in C&K property

D) None of the above.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/107

Play

Full screen (f)

Deck 9: Nontaxable Exchanges

1

Signo Inc.'s current year income statement includes a $21,000 gain realized on the exchange of an old business asset for a new business asset. If the exchange is nontaxable, Signo has a $21,000 favorable permanent book/tax difference.

False

2

The substituted basis rule results in permanent nonrecognition of gains and losses realized in a nontaxable exchange.

False

3

Gain realized on a property exchange that is not recognized is actually deferred rather than nontaxable.

True

4

A taxpayer who realizes a loss on the exchange of like-kind property can elect to recognize the loss.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

5

A taxpayer who receives boot in a nontaxable exchange must recognize gain equal to the lesser of the FMV of the boot or the gain realized.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

6

Qualifying property received in a nontaxable exchange has a cost basis for tax purposes.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

7

Muro Inc. exchanged an old inventory item for a new asset. If the new asset is also an inventory item, the exchange is nontaxable.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

8

Tarletto Inc.'s current year income statement includes a $229,000 gain realized on the exchange of an old business asset for a new business asset. If the exchange is nontaxable, Tarletto's book basis in the new asset is $229,000 greater than its tax basis.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

9

Yelano Inc. exchanged an old forklift used in its business for a new forklift. This like-kind exchange is nontaxable.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

10

Tax neutrality for asset exchanges is the exception rather than the rule.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

11

Mr. Lexon owns investment property with a $719,000 basis. If the property is worth only $500,000, Mr. Lexon would prefer a taxable disposition of the property over a like-kind exchange.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

12

When unrelated parties agree to an exchange of noncash properties, the economic presumption is that the properties have the same adjusted book basis.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

13

Tibco Inc. exchanged an equity interest in ABM Partnership for an equity interest in Jolla Partnership. This exchange is taxable.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

14

Nontaxable exchanges typically cause a temporary difference between book income and taxable income.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

15

Reiter Inc. exchanged an old forklift for new office furniture. This like-kind exchange is nontaxable.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

16

Mrs. Cooley exchanged 400 shares of stock for corporate bonds. If the stock and bonds were issued by the same corporation, they are like-kind properties, and the exchange is nontaxable.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

17

A taxpayer who receives or pays boot in a nontaxable exchange must recognize gain to the extent of the FMV of the boot.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

18

A taxpayer who pays boot in a nontaxable exchange includes the value of the boot in the basis of the qualifying property received.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

19

When unrelated parties agree to an exchange of noncash properties, the economic presumption is that the properties are of equal value.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

20

All types of business and investment real properties are like-kind.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

21

The goodwill of one business is never of a like-kind to the goodwill of a different business.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

22

A corporation's tax basis in property received in exchange for corporate stock depends on whether the exchange was taxable or nontaxable to the transferors of the property.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

23

A flood destroyed a business asset owned by Boochi Company. Boochi's adjusted tax basis in the asset was $87,100. Six months after the flood, Boochi used its $100,000 insurance settlement to replace the asset. Boochi can recognize a $12,900 gain or it can elect to defer gain recognition.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

24

Toffel Inc. exchanged investment land subject to a $240,000 mortgage for unencumbered farmland. If Toffel realized a $168,000 gain on the exchange, it must recognize the entire gain.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

25

Mr. Bentley exchanged investment land subject to a $300,000 mortgage for commercial real estate subject to a $188,000 mortgage. Mr. Bentley is treated as paying $112,000 boot in the exchange.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

26

Mrs. Volter exchanged residential real estate for a commercial office building. The residential real estate was subject to a $92,800 mortgage, which was assumed by the other party to the exchange. Mrs. Volter must treat the relief of the mortgage as $92,800 boot received.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

27

In a like-kind exchange in which both properties are subject to a mortgage, both parties to the exchange are treated as receiving boot equal to the relief of their respective mortgage.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following statements about the inclusion of boot in a nontaxable exchange is false?

A) The purpose of including boot in a nontaxable exchange is to equalize the adjusted tax bases of the properties exchanged.

B) The receipt of boot can trigger gain recognition but not loss recognition.

C) The party paying the boot includes the FMV of the boot in the tax basis of the property received.

D) None of the above is false.

A) The purpose of including boot in a nontaxable exchange is to equalize the adjusted tax bases of the properties exchanged.

B) The receipt of boot can trigger gain recognition but not loss recognition.

C) The party paying the boot includes the FMV of the boot in the tax basis of the property received.

D) None of the above is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

29

A taxpayer who realizes a loss on the sale of marketable securities and reacquires substantially the same securities within the 30 day period before the sale cannot recognize the loss.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

30

V&P Company exchanged unencumbered investment land for farmland subject to a $200,000 mortgage. If V&P realized a $168,000 gain on the exchange, it must recognize the entire gain.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

31

If a taxpayer elected to defer a $13,000 gain realized on an involuntary conversion, the tax basis of the taxpayer's replacement property equals the cost of the property less $13,000.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

32

Kimbo Inc. exchanged an old asset ($180,000 FMV and $145,000 adjusted basis) plus $10,000 cash for a new asset with a $190,000 FMV. What is Kimbo's basis in the new asset if the transaction qualifies as a like-kind exchange?

A) $145,000

B) $155,000

C) $135,000

D) $190,000

A) $145,000

B) $155,000

C) $135,000

D) $190,000

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

33

A partnership always takes a carryover basis in property received from a partner in exchange for an equity interest in the partnership.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

34

A taxpayer who exchanges property for an interest in a partnership never recognizes gain or loss on the exchange.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

35

Vandals destroyed a business asset owned by L&L Company. L&L's adjusted tax basis in the asset was $60,800, and the reimbursement from its property insurance company was $90,000. L&L must pay at least $60,800 for a replacement asset in order to defer gain recognition on the involuntary conversion.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

36

On July 2, 2015, a tornado destroyed an asset owned by Leigh Inc., a calendar year taxpayer. Leigh's adjusted tax basis in the asset was $22,700, and the reimbursement from its property insurance company was $35,000. If Leigh wants to defer recognizing its $12,300 realized gain, it must replace the asset no later than December 31, 2016.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

37

The wash sale rule can result in the nonrecognition of both gains and losses.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

38

A taxpayer who transfers property for corporate stock can defer gain recognition only if the taxpayer owns at least 50% of the corporation's outstanding stock immediately after the exchange.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

39

The tax basis in property received in a like-kind exchange in which no gain or loss is recognized is a:

A) FMV basis

B) Cost basis

C) Substituted basis

D) Carryover basis

A) FMV basis

B) Cost basis

C) Substituted basis

D) Carryover basis

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

40

Hank exchanged an old asset with a $12,000 adjusted basis for a new asset with a $32,000 FMV plus $2,000 cash. Compute Hank's realized and recognized gain if the new and old assets are like-kind properties.

A) $20,000 realized gain; $0 recognized gain

B) $22,000 realized gain; $0 recognized gain

C) $22,000 realized gain; $2,000 recognized gain

D) $2,000 realized gain; $2,000 recognized gain

A) $20,000 realized gain; $0 recognized gain

B) $22,000 realized gain; $0 recognized gain

C) $22,000 realized gain; $2,000 recognized gain

D) $2,000 realized gain; $2,000 recognized gain

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

41

Rydell Company exchanged business equipment (initial cost $55,250; accumulated depreciation $25,450) for like-kind equipment worth $44,000 and $2,000 cash. As a result, Rydell must recognize:

A) $2,000 ordinary gain

B) $2,000 Section 1231 gain

C) No gain or loss

D) None of the above.

A) $2,000 ordinary gain

B) $2,000 Section 1231 gain

C) No gain or loss

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

42

LiO Company transferred an old asset with a $13,600 adjusted tax basis in exchange for a new asset worth $11,000 and $1,500 cash. Which of the following statements is false?

A) If the exchange is taxable, LiO recognizes an $1,100 loss.

B) If the exchange is nontaxable, LiO recognizes no loss.

C) If the exchange is nontaxable, LiO's tax basis in the new asset is $12,100.

D) None of these statements is false.

A) If the exchange is taxable, LiO recognizes an $1,100 loss.

B) If the exchange is nontaxable, LiO recognizes no loss.

C) If the exchange is nontaxable, LiO's tax basis in the new asset is $12,100.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

43

Five years ago, Q&J Inc. transferred land with a $345,000 book and tax basis for a different parcel of land worth $472,000. Q&J included its $127,000 realized gain in book income, but the exchange was nontaxable. This year, Q&J sold the parcel of land received in the exchange for $533,000 cash. Compute Q&J's book and tax gain on sale.

A) $188,000 book and tax gain

B) $188,000 book gain and $61,000 tax gain

C) $61,000 book and tax gain

D) None of the above.

A) $188,000 book and tax gain

B) $188,000 book gain and $61,000 tax gain

C) $61,000 book and tax gain

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

44

Itak Company transferred an old asset with a $44,300 adjusted tax basis in exchange for a new asset worth $48,000 and $3,000 cash. Which of the following statements is false?

A) If the exchange is taxable, Itak recognizes a $6,700 gain.

B) If the exchange is nontaxable, Itak recognizes a $3,000 gain.

C) If the exchange is nontaxable, Itak's tax basis in the new asset is $44,300.

D) None of these statements is false.

A) If the exchange is taxable, Itak recognizes a $6,700 gain.

B) If the exchange is nontaxable, Itak recognizes a $3,000 gain.

C) If the exchange is nontaxable, Itak's tax basis in the new asset is $44,300.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

45

Luce Company exchanged the copyright on a software application for a copyright on a different software application. Luce's gain on the exchange was nontaxable (because the copyrights were like-kind) but was included in financial statement income. Which of the following statements is false?

A) Luce's book basis in the copyright received is the copyright's cost (FMV).

B) Luce's tax basis in the copyright received equals its tax basis in the copyright surrendered.

C) Luce's future amortization deductions with respect to its tax basis in the copyright will be different from future amortization expense for financial statement purposes.

D) None of these statements is false.

A) Luce's book basis in the copyright received is the copyright's cost (FMV).

B) Luce's tax basis in the copyright received equals its tax basis in the copyright surrendered.

C) Luce's future amortization deductions with respect to its tax basis in the copyright will be different from future amortization expense for financial statement purposes.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

46

YCM Inc. exchanged business equipment (initial cost $114,800; accumulated depreciation $63,400) for like-kind equipment worth $110,000 and $10,000 cash. As a result, Rydell must recognize:

A) No gain or loss

B) $10,000 Section 1231 gain

C) $10,000 ordinary gain

D) None of the above.

A) No gain or loss

B) $10,000 Section 1231 gain

C) $10,000 ordinary gain

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

47

Kornek Inc. transferred an old asset with a $200,000 adjusted tax basis plus $12,000 cash in exchange for a new asset worth $260,000. Which of the following statements is false?

A) If the exchange is taxable, Kornek recognizes a $48,000 gain.

B) If the exchange is nontaxable, Kornek recognizes a $12,000 gain.

C) If the exchange is nontaxable, Kornek's tax basis in the new asset is $212,000.

D) None of these statements is false.

A) If the exchange is taxable, Kornek recognizes a $48,000 gain.

B) If the exchange is nontaxable, Kornek recognizes a $12,000 gain.

C) If the exchange is nontaxable, Kornek's tax basis in the new asset is $212,000.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

48

Doppia Company transferred an old asset with a $68,750 adjusted tax basis in exchange for a new asset worth $90,000 and $10,000 cash. Which of the following statements is false?

A) The old asset's FMV is $100,000.

B) If the exchange is nontaxable, Doppia's recognized gain is $10,000.

C) If the exchange is nontaxable, Doppia's tax basis in the new asset is $78,750.

D) None of these statements is false.

A) The old asset's FMV is $100,000.

B) If the exchange is nontaxable, Doppia's recognized gain is $10,000.

C) If the exchange is nontaxable, Doppia's tax basis in the new asset is $78,750.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

49

Nagin Inc. transferred an old asset in exchange for a new asset worth $84,000 and $6,000 cash. The old asset and new asset were like-kind properties. Which of the following statements is true?

A) If Nagin's basis in the old asset was $95,000, Nagin can recognize a $5,000 loss.

B) If Nagin's basis in the old asset was $85,000, Nagin must recognize a $6,000 gain.

C) If Nagin's basis in the old asset was $79,200, Nagin must recognize a $6,000 gain.

D) None of the above is true.

A) If Nagin's basis in the old asset was $95,000, Nagin can recognize a $5,000 loss.

B) If Nagin's basis in the old asset was $85,000, Nagin must recognize a $6,000 gain.

C) If Nagin's basis in the old asset was $79,200, Nagin must recognize a $6,000 gain.

D) None of the above is true.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

50

Oxono Company realized a $74,900 gain on the exchange of one asset for another asset (no cash was included in the exchange). The assets were like-kind properties. Oxono reported the gain as revenue on its financial statements. Which of the following is true?

A) The exchange resulted in a favorable temporary book/tax difference.

B) The exchange resulted in a favorable permanent book/tax difference.

C) The exchange resulted in an unfavorable temporary book/tax difference.

D) The exchange resulted in an unfavorable permanent book/tax difference.

A) The exchange resulted in a favorable temporary book/tax difference.

B) The exchange resulted in a favorable permanent book/tax difference.

C) The exchange resulted in an unfavorable temporary book/tax difference.

D) The exchange resulted in an unfavorable permanent book/tax difference.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

51

Denali, Inc. exchanged equipment with a $230,000 adjusted basis for like-kind equipment with a $200,000 FMV and $5,000 cash. How much loss may Denali recognize?

A) $5,000

B) $25,000

C) $30,000

D) $0

A) $5,000

B) $25,000

C) $30,000

D) $0

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

52

Five years ago, Q&J Inc. transferred land with a $345,000 book and tax basis for a different parcel of land worth $472,000. Q&J included its $127,000 realized gain in book income, but the exchange was nontaxable. This year, Q&J sold the parcel of land received in the exchange for $533,000 cash. Which of the following statements is true?

A) The nontaxable exchange had no effect on Q&J's deferred tax accounts.

B) The nontaxable exchange resulted in a deferred tax liability that reversed this year.

C) The nontaxable exchange resulted in a deferred tax asset that reversed this year.

D) The sale of the parcel of land had no effect on Q&J's deferred tax accounts.

A) The nontaxable exchange had no effect on Q&J's deferred tax accounts.

B) The nontaxable exchange resulted in a deferred tax liability that reversed this year.

C) The nontaxable exchange resulted in a deferred tax asset that reversed this year.

D) The sale of the parcel of land had no effect on Q&J's deferred tax accounts.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

53

Berly Company transferred an old asset with a $12,300 adjusted tax basis in exchange for a new asset worth $20,000. Which of the following statements is false?

A) The old asset's FMV is $20,000.

B) If the exchange is nontaxable, Berly's tax basis in the new asset is $12,300.

C) If the exchange is taxable, Berly's recognized gain is $7,700.

D) None of these statements is false.

A) The old asset's FMV is $20,000.

B) If the exchange is nontaxable, Berly's tax basis in the new asset is $12,300.

C) If the exchange is taxable, Berly's recognized gain is $7,700.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following statements about boot included in a nontaxable exchange is false?

A) The purpose of boot is to equalize the values of the exchanged properties.

B) The payment of boot triggers recognition of realized gain to the payer.

C) The receipt of boot triggers recognition of realized gain to the recipient.

D) The receipt of boot does not trigger recognition of realized loss to the recipient.

A) The purpose of boot is to equalize the values of the exchanged properties.

B) The payment of boot triggers recognition of realized gain to the payer.

C) The receipt of boot triggers recognition of realized gain to the recipient.

D) The receipt of boot does not trigger recognition of realized loss to the recipient.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

55

Teco Inc. and MW Company exchanged like-kind production assets. Teco's asset had an $80,000 FMV and $53,900 adjusted tax basis, and MW's asset had an $87,500 FMV and a $28,100 adjusted tax basis. Teco paid $7,500 cash to MW as part of the exchange. Which of the following statements is false?

A) Teco's realized gain is $26,100 and recognized gain is -0-.

B) MW's realized gain is $59,400 and recognized gain is $7,500.

C) Teco's basis in its newly acquired asset is $61,400.

D) MW's basis in its newly acquired asset is $35,600.

A) Teco's realized gain is $26,100 and recognized gain is -0-.

B) MW's realized gain is $59,400 and recognized gain is $7,500.

C) Teco's basis in its newly acquired asset is $61,400.

D) MW's basis in its newly acquired asset is $35,600.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements about like-kind exchanges is false?

A) Like-kind property must be held for either business or investment use.

B) Businesses cannot engage in like-kind exchanges of inventory.

C) The definition of like-kind property for tangible personality is determined by the IRS.

D) Business cannot exchange undeveloped land for developed real estate.

A) Like-kind property must be held for either business or investment use.

B) Businesses cannot engage in like-kind exchanges of inventory.

C) The definition of like-kind property for tangible personality is determined by the IRS.

D) Business cannot exchange undeveloped land for developed real estate.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

57

Eliot Inc. transferred an old asset with a $53,100 adjusted tax basis plus $5,000 cash in exchange for a new asset worth $75,000. Which of the following statements is false?

A) The old asset's FMV is $70,000.

B) If the exchange is nontaxable, Eliot's recognized gain is $5,000.

C) If the exchange is nontaxable, Eliot's tax basis in the new asset is $58,100.

D) None of these statements is false.

A) The old asset's FMV is $70,000.

B) If the exchange is nontaxable, Eliot's recognized gain is $5,000.

C) If the exchange is nontaxable, Eliot's tax basis in the new asset is $58,100.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

58

Eight years ago, Prescott Inc. realized a $16,200 gain on the exchange of old equipment for new equipment. Prescott included the gain in book income, but the exchange was nontaxable. This year, Prescott sold the new equipment for $2,500. At date of sale, the equipment's book basis and tax basis had both been depreciated to zero. Which of the following statements is true?

A) The nontaxable exchange had no effect on Prescott's deferred tax accounts.

B) The nontaxable exchange resulted in a deferred tax asset.

C) The sale of the new equipment had no effect on Prescott's deferred tax accounts.

D) None of the above is true.

A) The nontaxable exchange had no effect on Prescott's deferred tax accounts.

B) The nontaxable exchange resulted in a deferred tax asset.

C) The sale of the new equipment had no effect on Prescott's deferred tax accounts.

D) None of the above is true.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following statements about nontaxable exchanges is true?

A) The parties to the exchange agree that the properties exchanged are of equal value.

B) The parties to the exchange both realize gain on the exchange.

C) No cash can change hands in a nontaxable exchange.

D) Any gain realized on the exchange is not included in financial statement income.

A) The parties to the exchange agree that the properties exchanged are of equal value.

B) The parties to the exchange both realize gain on the exchange.

C) No cash can change hands in a nontaxable exchange.

D) Any gain realized on the exchange is not included in financial statement income.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

60

G&G Inc. transferred an old asset with a $110,300 adjusted tax basis plus $20,000 cash in exchange for a new asset worth $150,000. Which of the following statements is false?

A) The old asset's FMV is $150,000.

B) If the exchange is nontaxable, G&G's recognized gain is -0-.

C) If the exchange is nontaxable, G&G's tax basis in the new asset is $130,300.

D) None of these statements is false.

A) The old asset's FMV is $150,000.

B) If the exchange is nontaxable, G&G's recognized gain is -0-.

C) If the exchange is nontaxable, G&G's tax basis in the new asset is $130,300.

D) None of these statements is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

61

In April, vandals completely destroyed outdoor signage owned by Renfru Inc. Renfru's adjusted tax basis in the signage was $31,300. Renfru received a $50,000 reimbursement from its property insurance company, and on August 8, it paid $60,000 to replace the signage. Compute Renfru's recognized gain or loss on the involuntary conversion and its tax basis in the new signage.

A) No recognized gain or loss; $50,000 basis in the signage

B) No recognized gain or loss; $60,000 basis in the signage

C) $18,700 recognized gain; $60,000 basis in the signage

D) None of the above.

A) No recognized gain or loss; $50,000 basis in the signage

B) No recognized gain or loss; $60,000 basis in the signage

C) $18,700 recognized gain; $60,000 basis in the signage

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

62

Thieves stole computer equipment used by Ms. James in her small business. Ms. James' tax basis in the equipment was zero. One month after the theft, she received a $17,600 reimbursement from her casualty insurance company and used $14,850 to replace the computer equipment. She used the $2,750 remaining reimbursement to purchase a new desk for her office. Which of the following statements is false?

A) Ms. James must recognize a $2,750 gain on the involuntary conversion.

B) Ms. James's basis in her new computer equipment is -0-.

C) Ms. James's basis in her new desk is $2,750.

D) None of the above is false.

A) Ms. James must recognize a $2,750 gain on the involuntary conversion.

B) Ms. James's basis in her new computer equipment is -0-.

C) Ms. James's basis in her new desk is $2,750.

D) None of the above is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

63

Grantly Seafood is a calendar year taxpayer. In 2015, a hurricane destroyed three of Grantly's fishing boats with a $784,500 aggregate adjusted tax basis. On October 12, 2015, Grantly received a $1.2 million reimbursement from its insurance company. What is the latest date that Grantly can replace the boats to avoid gain recognition from the involuntary conversion?

A) December 31, 2015

B) December 31, 2016

C) December 31, 2017

D) October 11, 2017

A) December 31, 2015

B) December 31, 2016

C) December 31, 2017

D) October 11, 2017

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

64

In March, a flood completely destroyed three delivery vans owned by Totle Inc. Totle's adjusted tax basis in the vans was $48,900. Totle received a $90,000 reimbursement from its property insurance company, and on September 8, it purchased one new delivery van for $70,000. Compute Totle's recognized gain or loss on the involuntary conversion and its tax basis in the new van.

A) No recognized gain or loss; $48,900 basis in the van

B) $20,000 recognized gain; $70,000 basis in the van

C) $20,000 recognized gain; $48,900 basis in the van

D) None of the above.

A) No recognized gain or loss; $48,900 basis in the van

B) $20,000 recognized gain; $70,000 basis in the van

C) $20,000 recognized gain; $48,900 basis in the van

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

65

Babex Inc. and OMG Company entered into an exchange of real property. Here is the information for the properties to be exchanged. Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute OMG's gain recognized on the exchange and its tax basis in the property received from Babex.

A) $175,000 gain recognized; $514,500 basis in Babex property

B) No gain recognized; $689,500 basis in Babex property

C) No gain recognized; $514,500 basis in Babex property

D) None of the above.

Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute OMG's gain recognized on the exchange and its tax basis in the property received from Babex.A) $175,000 gain recognized; $514,500 basis in Babex property

B) No gain recognized; $689,500 basis in Babex property

C) No gain recognized; $514,500 basis in Babex property

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

66

In June, a fire completely destroyed office furniture owned by W&S Inc. W&S's adjusted tax basis in the furniture was $17,040. W&S received a $15,000 reimbursement from its property insurance company, and on August 8, it paid $16,000 to replace the furniture. Compute W&S's recognized gain or loss on the involuntary conversion and its tax basis in the new furniture.

A) No recognized gain or loss; $18,040 basis in the furniture

B) $2,040 recognized loss; $16,000 basis in the furniture

C) No recognized gain or loss; $13,960 basis in the furniture

D) None of the above.

A) No recognized gain or loss; $18,040 basis in the furniture

B) $2,040 recognized loss; $16,000 basis in the furniture

C) No recognized gain or loss; $13,960 basis in the furniture

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

67

Perry Inc. and Dally Company entered into an exchange of real property. Here is the information for the properties to be exchanged. Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Perry's gain recognized on the exchange and its tax basis in the property received from Dally.

A) No gain recognized; $410,000 basis in the Dally property

B) No gain recognized; $440,000 basis in the Dally property

C) $100,000 gain recognized; $410,000 basis in the Dally property

D) None of the above.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Perry's gain recognized on the exchange and its tax basis in the property received from Dally.A) No gain recognized; $410,000 basis in the Dally property

B) No gain recognized; $440,000 basis in the Dally property

C) $100,000 gain recognized; $410,000 basis in the Dally property

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

68

Mr. Weller and the Olson Partnership entered into an exchange of investment real property. Mr. Weller's property was subject to a $428,000 mortgage, which Olson assumed. Olson's property was subject to a $235,000 mortgage, which Mr. Weller assumed. Which of the following statements is true?

A) Mr. Weller received $193,000 boot; Olson paid $193,000 boot.

B) Mr. Weller paid $193,000 boot; Olson received $193,000 boot.

C) Mr. Weller received $428,000 boot; Olson received $235,000 boot.

D) Mr. Weller paid $428,000 boot; Olson paid $235,000 boot.

A) Mr. Weller received $193,000 boot; Olson paid $193,000 boot.

B) Mr. Weller paid $193,000 boot; Olson received $193,000 boot.

C) Mr. Weller received $428,000 boot; Olson received $235,000 boot.

D) Mr. Weller paid $428,000 boot; Olson paid $235,000 boot.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

69

Tanner Inc. owns a fleet of passenger automobiles that it would like to dispose of in a nontaxable exchange. Which of the following would qualify as like-kind property?

A) Sports utility vehicles

B) Double decker buses

C) Dump trucks

D) Both a. and b. would qualify as like-kind.

A) Sports utility vehicles

B) Double decker buses

C) Dump trucks

D) Both a. and b. would qualify as like-kind.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

70

Babex Inc. and OMG Company entered into an exchange of real property. Here is the information for the properties to be exchanged. Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute Babex's gain recognized on the exchange and its tax basis in the property received from OMG.

A) $175,000 gain recognized; $768,000 basis in OMG property

B) No gain recognized; $768,000 basis in OMG property

C) $175,000 gain recognized; $943,000 basis in OMG property

D) None of the above.

Pursuant to the exchange, OMG assumed the mortgage on the Babex property. Compute Babex's gain recognized on the exchange and its tax basis in the property received from OMG.A) $175,000 gain recognized; $768,000 basis in OMG property

B) No gain recognized; $768,000 basis in OMG property

C) $175,000 gain recognized; $943,000 basis in OMG property

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

71

Carman wishes to exchange 10 acres of Iowa farm land in a like-kind exchange. Which of the following properties will qualify for like-kind exchange treatment?

A) New York office building

B) Tractor

C) 35 hogs raised for slaughter

D) Personal residence in Des Moines which Carman would use as her personal residence

A) New York office building

B) Tractor

C) 35 hogs raised for slaughter

D) Personal residence in Des Moines which Carman would use as her personal residence

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

72

Grantly Seafood is a calendar year taxpayer. In 2015, a hurricane destroyed three of Grantly's fishing boats with a $784,500 aggregate adjusted tax basis. On October 12, 2015, Grantly received a $1 million reimbursement from its insurance company. On May 19, 2016, Grantly purchased a new fishing boat for $750,000. Compute Grantly's recognized gain or loss on the involuntary conversion and its tax basis in the new boat.

A) $215,500 recognized gain; $750,000 basis in the boat

B) $250,000 recognized gain; $750,000 basis in the boat

C) $250,000 recognized gain; $784,500 basis in the boat

D) None of the above.

A) $215,500 recognized gain; $750,000 basis in the boat

B) $250,000 recognized gain; $750,000 basis in the boat

C) $250,000 recognized gain; $784,500 basis in the boat

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

73

Nixon Inc. transferred Asset A to an unrelated party in exchange for Asset Z and $15,750 cash. Nixon's tax basis in Asset A was $400,000, and Asset Z had a $510,000 appraised FMV. Which of the following statements is true?

A) If Asset A and Asset Z are like-kind property, Nixon recognizes a $15,750 gain and takes a $400,000 basis in Asset Z.

B) If Asset A and Asset Z are not like-kind property, Nixon recognizes a $110,000 gain and takes a $510,000 basis in Asset Z.

C) If Asset A and Asset Z are like-kind property, Nixon recognizes no gain and takes a $400,000 basis in Asset Z.

D) If Asset A and Asset Z are like-kind property, Nixon recognizes a $15,750 gain and takes a $415,750 basis in Asset Z.

A) If Asset A and Asset Z are like-kind property, Nixon recognizes a $15,750 gain and takes a $400,000 basis in Asset Z.

B) If Asset A and Asset Z are not like-kind property, Nixon recognizes a $110,000 gain and takes a $510,000 basis in Asset Z.

C) If Asset A and Asset Z are like-kind property, Nixon recognizes no gain and takes a $400,000 basis in Asset Z.

D) If Asset A and Asset Z are like-kind property, Nixon recognizes a $15,750 gain and takes a $415,750 basis in Asset Z.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

74

Tauber Inc. and J&I Company exchanged like-kind production assets. Tauber's asset had a $17,500 FMV and $3,000 adjusted tax basis, and J&I's asset had a $19,000 FMV and a $9,000 adjusted tax basis. Tauber paid $1,500 cash to J&I as part of the exchange. Which of the following statements is false?

A) Tauber's realized gain is $14,500 and recognized gain is -0-.

B) J&I's realized gain is $10,000 and recognized gain is -0-.

C) Tauber's basis in its newly acquired asset is $4,500.

D) J&I's basis in its newly acquired asset is $9,000.

A) Tauber's realized gain is $14,500 and recognized gain is -0-.

B) J&I's realized gain is $10,000 and recognized gain is -0-.

C) Tauber's basis in its newly acquired asset is $4,500.

D) J&I's basis in its newly acquired asset is $9,000.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

75

Perry Inc. and Dally Company entered into an exchange of real property. Here is the information for the properties to be exchanged. Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Dally's gain recognized on the exchange and its tax basis in the property received from Perry.

A) $30,000 gain recognized; $313,000 basis in the Perry property

B) 100,000 gain recognized; $383,000 basis in the Perry property

C) $30,000 gain recognized; $283,000 basis in the Perry property

D) None of the above.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Dally's gain recognized on the exchange and its tax basis in the property received from Perry.A) $30,000 gain recognized; $313,000 basis in the Perry property

B) 100,000 gain recognized; $383,000 basis in the Perry property

C) $30,000 gain recognized; $283,000 basis in the Perry property

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

76

Johnson Inc. and C&K Company entered into an exchange of real property. Here is the information for the properties to be exchanged. Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute C&K's gain recognized on the exchange and its tax basis in the property received from Johnson.

A) $200,000 gain recognized; $662,000 basis in Johnson property

B) No gain recognized; $462,000 basis in Johnson property

C) No gain recognized; $487,000 basis in Johnson property

D) None of the above.

Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute C&K's gain recognized on the exchange and its tax basis in the property received from Johnson.A) $200,000 gain recognized; $662,000 basis in Johnson property

B) No gain recognized; $462,000 basis in Johnson property

C) No gain recognized; $487,000 basis in Johnson property

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

77

Acme Inc. and Beamer Company exchanged like-kind production assets. Acme's asset had a $240,000 FMV and $117,300 adjusted tax basis, and Beamer's asset had a $225,000 FMV and a $168,200 adjusted tax basis. Beamer paid $15,000 cash to Acme as part of the exchange. Which of the following statements is true?

A) Acme's realized gain is $122,700 and recognized gain is -0-.

B) Beamer's realized gain is $56,800 and recognized gain is $15,000.

C) Acme's basis in its newly acquired asset is $117,300.

D) Beamer's basis in its newly acquired asset is $168,200.

A) Acme's realized gain is $122,700 and recognized gain is -0-.

B) Beamer's realized gain is $56,800 and recognized gain is $15,000.

C) Acme's basis in its newly acquired asset is $117,300.

D) Beamer's basis in its newly acquired asset is $168,200.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

78

Mr. and Mrs. Eyre own residential rental property that they would like to dispose of in a nontaxable exchange. Which of the following would not qualify as like-kind property?

A) Commercial office building

B) Undeveloped land

C) Warehouse used to store transportation equipment

D) All of the above qualify as like-kind property.

A) Commercial office building

B) Undeveloped land

C) Warehouse used to store transportation equipment

D) All of the above qualify as like-kind property.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

79

Johnson Inc. and C&K Company entered into an exchange of real property. Here is the information for the properties to be exchanged. Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute Johnson's gain recognized on the exchange and its tax basis in the property received from C&K.

A) $25,000 gain recognized; $593,000 basis in C&K property

B) $25,000 gain recognized; $793,000 basis in C&K property

C) $225,000 gain recognized; $593,000 basis in C&K property

D) None of the above.

Pursuant to the exchange, C&K paid $25,000 cash to Johnson and assumed the mortgage on the Johnson property. Compute Johnson's gain recognized on the exchange and its tax basis in the property received from C&K.A) $25,000 gain recognized; $593,000 basis in C&K property

B) $25,000 gain recognized; $793,000 basis in C&K property

C) $225,000 gain recognized; $593,000 basis in C&K property

D) None of the above.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following statements about the transfer of debt in a like-kind exchange is false?

A) The party relieved of debt treats the relief as boot received.

B) The party assuming debt treats the assumption as boot paid.

C) If both properties in the exchange are subject to debt, both parties will be treated as receiving boot.

D) None of the above is false.

A) The party relieved of debt treats the relief as boot received.

B) The party assuming debt treats the assumption as boot paid.

C) If both properties in the exchange are subject to debt, both parties will be treated as receiving boot.

D) None of the above is false.

Unlock Deck

Unlock for access to all 107 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 107 flashcards in this deck.