Deck 17: The Banking Sector

Full screen (f)

Question

Question

Question

Question

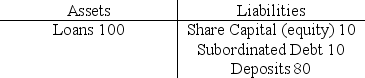

The following questions apply to the following simplified bank balance sheet

Shareholders in the bank above are offered the following deal.The bank will gamble the whole loan book on a double or nothing coin toss (i.e.50% chance loan book doubles in value,50% chance it has zero value).From the shareholders point of view,this deal

A) gives them a 50% chance of losing 10 and a 50% chance of gaining 10

B) gives them a 50% chance of losing 10 and a 50% chance of gaining 20

C) gives them a 50% chance of losing 10 and a 50% chance of gaining 100

D) gives them a 50% chance of losing 100 and a 50% chance of gaining 100

E) gives them a 50% chance of losing 100 and a 50% chance of gaining 200

Shareholders in the bank above are offered the following deal.The bank will gamble the whole loan book on a double or nothing coin toss (i.e.50% chance loan book doubles in value,50% chance it has zero value).From the shareholders point of view,this deal

A) gives them a 50% chance of losing 10 and a 50% chance of gaining 10

B) gives them a 50% chance of losing 10 and a 50% chance of gaining 20

C) gives them a 50% chance of losing 10 and a 50% chance of gaining 100

D) gives them a 50% chance of losing 100 and a 50% chance of gaining 100

E) gives them a 50% chance of losing 100 and a 50% chance of gaining 200

Question

The following questions apply to the following simplified bank balance sheet

The Bank above suffers a 50% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

The Bank above suffers a 50% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

Question

The following questions apply to the following simplified bank balance sheet

The Bank above suffers a 15% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

The Bank above suffers a 15% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

Question

Question

Question

Question

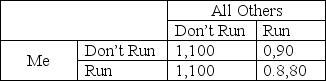

Given the payoff matrix for a Bank Run below (where the first number in each box is the payoff to me).What is the full set of possible Nash equilbria?

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) all the outcomes

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) all the outcomes

Question

Question

Question

Question

The following questions apply to the following simplified bank balance sheet

The Bank above suffers a 5% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

The Bank above suffers a 5% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

Question

Question

Question

Question

Given the payoff matrix for a Bank Run below (where the first number in each box is the payoff to me).What is the full set of possible Nash equilbria?

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) All the outcomes

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) All the outcomes

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/26

Play

Full screen (f)

Deck 17: The Banking Sector

1

Shareholders in a bank may encourage excessive risk taking by the bank because

A) shareholders are generally risk neutral

B) shareholders are generally risk averse

C) shareholders are generally risk loving

D) limited liability means that shareholder losses are limited

E) limited liability means that shareholder gains are limited

A) shareholders are generally risk neutral

B) shareholders are generally risk averse

C) shareholders are generally risk loving

D) limited liability means that shareholder losses are limited

E) limited liability means that shareholder gains are limited

limited liability means that shareholder losses are limited

2

Capital adequacy regulations are designed to

A) ensure banks' capital expenditure is adequate

B) ensure deposit insurance is sufficient

C) ensure that banks have sufficient equity and subordinated debt to absorb losses

D) ensure that banks are regularly inspected by bank regulators

E) ensure that the Bank's share capital is not concentrated in the hands of just a few shareholders

A) ensure banks' capital expenditure is adequate

B) ensure deposit insurance is sufficient

C) ensure that banks have sufficient equity and subordinated debt to absorb losses

D) ensure that banks are regularly inspected by bank regulators

E) ensure that the Bank's share capital is not concentrated in the hands of just a few shareholders

ensure that banks have sufficient equity and subordinated debt to absorb losses

3

A bus breaks down outside a small bank causing a big crowd.Passing bank customers think the crowd is caused by a queue of depositors withdrawing their money and so take their money out and warn their friends.You are also a depositor at the bank but realize that the run on the bank has been caused by a misconception.Your rational response is to

A) ignore the run since it is based on a misconception

B) withdraw your money also even though there is no risk of the bank failing

C) withdraw your money as there is now a risk of the bank failing

D) put more money in the bank as a show of confidence

E) ignore the run even though the bank is now at risk of failing

A) ignore the run since it is based on a misconception

B) withdraw your money also even though there is no risk of the bank failing

C) withdraw your money as there is now a risk of the bank failing

D) put more money in the bank as a show of confidence

E) ignore the run even though the bank is now at risk of failing

withdraw your money as there is now a risk of the bank failing

4

The following questions apply to the following simplified bank balance sheet

Shareholders in the bank above are offered the following deal.The bank will gamble the whole loan book on a double or nothing coin toss (i.e.50% chance loan book doubles in value,50% chance it has zero value).From the shareholders point of view,this deal

A) gives them a 50% chance of losing 10 and a 50% chance of gaining 10

B) gives them a 50% chance of losing 10 and a 50% chance of gaining 20

C) gives them a 50% chance of losing 10 and a 50% chance of gaining 100

D) gives them a 50% chance of losing 100 and a 50% chance of gaining 100

E) gives them a 50% chance of losing 100 and a 50% chance of gaining 200

Shareholders in the bank above are offered the following deal.The bank will gamble the whole loan book on a double or nothing coin toss (i.e.50% chance loan book doubles in value,50% chance it has zero value).From the shareholders point of view,this deal

A) gives them a 50% chance of losing 10 and a 50% chance of gaining 10

B) gives them a 50% chance of losing 10 and a 50% chance of gaining 20

C) gives them a 50% chance of losing 10 and a 50% chance of gaining 100

D) gives them a 50% chance of losing 100 and a 50% chance of gaining 100

E) gives them a 50% chance of losing 100 and a 50% chance of gaining 200

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

5

The following questions apply to the following simplified bank balance sheet

The Bank above suffers a 50% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

The Bank above suffers a 50% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

6

The following questions apply to the following simplified bank balance sheet

The Bank above suffers a 15% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

The Bank above suffers a 15% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

7

Generally Speaking,bank deposits

A) average over 100% of GDP and are a larger share of GDP in developed countries than in developing.

B) average less than 100% of GDP and are a larger share of GDP in developed countries than in developing

C) average over 100% of GDP and are a larger share of GDP in developing countries than in developed

D) average less than 100% of GDP and are a larger share of GDP in developing countries than in developed

E) average less than 100% of GDP and are a similar share of GDP in developed countries and developing

A) average over 100% of GDP and are a larger share of GDP in developed countries than in developing.

B) average less than 100% of GDP and are a larger share of GDP in developed countries than in developing

C) average over 100% of GDP and are a larger share of GDP in developing countries than in developed

D) average less than 100% of GDP and are a larger share of GDP in developing countries than in developed

E) average less than 100% of GDP and are a similar share of GDP in developed countries and developing

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

8

The key argument for a government-backed deposit insurance scheme is

A) to protect depositors against badly run banks

B) reduce the likelihood of bank runs

C) avoid moral hazard

D) to avoid depositors losing money in any type of bank failure

E) to make bank too big to fail

A) to protect depositors against badly run banks

B) reduce the likelihood of bank runs

C) avoid moral hazard

D) to avoid depositors losing money in any type of bank failure

E) to make bank too big to fail

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

9

Generally speaking,bank deposits

A) are a larger share of GDP in developing countries (relative to developed countries) but a smaller share of total financial assets

B) are smaller larger share of GDP in developing countries (relative to developed countries) and a smaller share of total financial assets

C) are a larger share of GDP in developing countries (relative to developed countries) and a larger share of total financial assets

D) are a smaller share of GDP in developing countries (relative to developed countries) but a larger share of total financial assets

E) are a similar share of GDP and financial assets in both developed and developing countries

A) are a larger share of GDP in developing countries (relative to developed countries) but a smaller share of total financial assets

B) are smaller larger share of GDP in developing countries (relative to developed countries) and a smaller share of total financial assets

C) are a larger share of GDP in developing countries (relative to developed countries) and a larger share of total financial assets

D) are a smaller share of GDP in developing countries (relative to developed countries) but a larger share of total financial assets

E) are a similar share of GDP and financial assets in both developed and developing countries

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

10

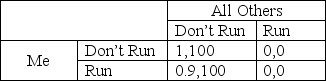

Given the payoff matrix for a Bank Run below (where the first number in each box is the payoff to me).What is the full set of possible Nash equilbria?

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) all the outcomes

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) all the outcomes

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

11

If a Bank is characterized by economies of scale,this means that the average cost,per unit,of providing its services

A) increases as the quantity of services provided increases

B) decreases as the quantity of services provided increases

C) increases as the number of banks decrease

D) decreases as the number of banks increase

E) is unrelated to bank size or number

A) increases as the quantity of services provided increases

B) decreases as the quantity of services provided increases

C) increases as the number of banks decrease

D) decreases as the number of banks increase

E) is unrelated to bank size or number

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

12

The tendency for a bank run at one bank to increase the likelihood at another is called

A) economies of scale

B) effective monitoring

C) contagion

D) moral hazard

E) Nash Equilibrium

A) economies of scale

B) effective monitoring

C) contagion

D) moral hazard

E) Nash Equilibrium

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

13

A company wishes to borrow $10,000 but to efficiently monitor that loan each lender will incur costs of $100.What is the difference in monitoring costs per lender (as a percentage of loan value) between the firm borrowing all the money from one lender and splitting the loan between ten lenders

A) 0%

B) 1%

C) 5%

D) 9%

E) 10%

A) 0%

B) 1%

C) 5%

D) 9%

E) 10%

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

14

The following questions apply to the following simplified bank balance sheet

The Bank above suffers a 5% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

The Bank above suffers a 5% fall in the value of its loans.It is now

A) in a position where none of its creditors will get any of their money back

B) effectively bankrupt and depositors stand to lose money

C) effectively bankrupt but depositors can be paid off

D) effectively bankrupt but depositors and subordinated debt holders can be paid off

E) still a viable enterprise but with dramatically reduced capital

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

15

A key difference between a Commercial and an Investment Bank is

A) Investment Banks focus on lending for investment rather the consumption

B) Commercial Banks tend to act as intermediaries in financial markets

C) Investment Banks focus on mortgages and loans to firms

D) Investment Banks may engage in proprietary trading

E) Commercial Banks often advise firms on how to raise funds in financial markets

A) Investment Banks focus on lending for investment rather the consumption

B) Commercial Banks tend to act as intermediaries in financial markets

C) Investment Banks focus on mortgages and loans to firms

D) Investment Banks may engage in proprietary trading

E) Commercial Banks often advise firms on how to raise funds in financial markets

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is not a key function of the banking system

A) offering access to an efficient payments system

B) economies of scale in pooling the savings of many small depositors

C) allowing the efficient operation of financial markets

D) more effective monitoring of small and medium size borrowers relative to financial markets

E) maturity transformation of instant access deposits into longer term loans

A) offering access to an efficient payments system

B) economies of scale in pooling the savings of many small depositors

C) allowing the efficient operation of financial markets

D) more effective monitoring of small and medium size borrowers relative to financial markets

E) maturity transformation of instant access deposits into longer term loans

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

17

A bank is termed 'too big to fail' when

A) it is of such economic importance that the government cannot allow it to fail

B) it is so large and profitable that failure is very unlikely

C) it is spread across so many countries, it cannot fail in any one country

D) it has enough money to pay off all its debts

E) all of the above

A) it is of such economic importance that the government cannot allow it to fail

B) it is so large and profitable that failure is very unlikely

C) it is spread across so many countries, it cannot fail in any one country

D) it has enough money to pay off all its debts

E) all of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

18

Given the payoff matrix for a Bank Run below (where the first number in each box is the payoff to me).What is the full set of possible Nash equilbria?

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) All the outcomes

A) I Don't Run and all others don't Run

B) I Don't Run and all others don't Run + I run and all others run

C) I run and all others run

D) I Don't Run and all others don't Run + I run and all others don't run

E) All the outcomes

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

19

The key source of finance for small and medium size firms in most countries is

A) Venture capital companies

B) Private financing companies

C) Financial markets

D) Public institutions

E) Banks

A) Venture capital companies

B) Private financing companies

C) Financial markets

D) Public institutions

E) Banks

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

20

Generally speaking the maturity mismatch of banks is due to

A) having short term liabilities and long term assets

B) having long term liabilities and short term assets

C) liabilities that pay a fixed rate of interest and assets that pay a variable rate

D) depositors that are willing to keep their money in the bank for many years whilst loans are often short term

E) all of the above

A) having short term liabilities and long term assets

B) having long term liabilities and short term assets

C) liabilities that pay a fixed rate of interest and assets that pay a variable rate

D) depositors that are willing to keep their money in the bank for many years whilst loans are often short term

E) all of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

21

A Credit Crunch is when

A) Central Banks tighten credit conditions too much

B) interest rate are too high

C) borrowers find it hard to access credit due to restricted supply by lenders

D) Central Banks dramatically increase the supply of money

E) several banks fail at once

A) Central Banks tighten credit conditions too much

B) interest rate are too high

C) borrowers find it hard to access credit due to restricted supply by lenders

D) Central Banks dramatically increase the supply of money

E) several banks fail at once

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

22

The bank lending channel of a credit crunch is when

A) bank restrict credit and so all firms find it hard to borrow

B) banks restrict credit and so small and medium size firms in particular find it hard to borrow

C) banks continue to lend, but borrowing through financial markets is restricted

D) borrowing is restricted though falling collateral values

E) Central Banks tighten credit conditions too much

A) bank restrict credit and so all firms find it hard to borrow

B) banks restrict credit and so small and medium size firms in particular find it hard to borrow

C) banks continue to lend, but borrowing through financial markets is restricted

D) borrowing is restricted though falling collateral values

E) Central Banks tighten credit conditions too much

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

23

Real Estate is important to banks because

A) real estate lending is a large part of total bank lending

B) real estate is often used as collateral for loans

C) banks tend to own a lot of property

D) of both a and b

E) of a,b and c

A) real estate lending is a large part of total bank lending

B) real estate is often used as collateral for loans

C) banks tend to own a lot of property

D) of both a and b

E) of a,b and c

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

24

The broad credit channel of a credit crunch is when

A) all banks restrict credit to borrowers

B) banks restrict lending to small and medium size firms

C) even large firms find it hard to borrow due to reduced collateral values

D) both firms and households find it hard to borrow

E) Central Banks tighten credit conditions too much

A) all banks restrict credit to borrowers

B) banks restrict lending to small and medium size firms

C) even large firms find it hard to borrow due to reduced collateral values

D) both firms and households find it hard to borrow

E) Central Banks tighten credit conditions too much

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

25

Recessions involving a credit crunch tend to be

A) more severe but shorter than other recessions

B) less severe but longer than other recessions

C) less severe and shorter than other recessions

D) more severe and longer than other recessions

E) the same as other recessions

A) more severe but shorter than other recessions

B) less severe but longer than other recessions

C) less severe and shorter than other recessions

D) more severe and longer than other recessions

E) the same as other recessions

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

26

A bank is said to be highly leveraged if

A) it has made a large number of risky loans

B) it is highly dependent on the interbank market for funding

C) its assets are very large in relation to its equity

D) its assets are very large in relation to its deposits

E) it liabilities are very large

A) it has made a large number of risky loans

B) it is highly dependent on the interbank market for funding

C) its assets are very large in relation to its equity

D) its assets are very large in relation to its deposits

E) it liabilities are very large

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 26 flashcards in this deck.