Deck 32: Accounting for Foreign Currency Transactions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

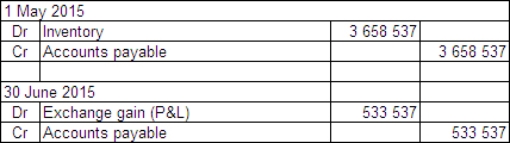

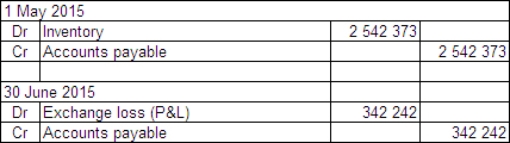

Question

Question

Question

Question

Question

Question

Question

Question

Question

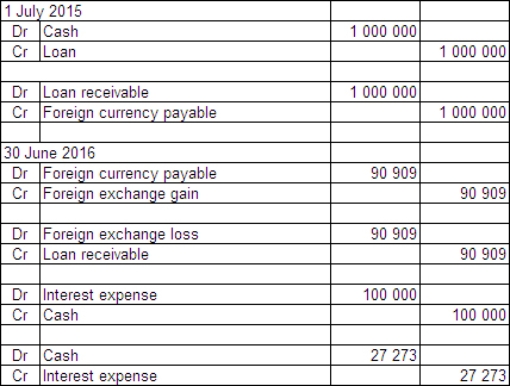

On 1 July 2016 McGrath Ltd enters into an arrangement with a Hong Kong bank to borrow $HK1 500 000.The term of the loan is 3 years with interest payable annually in arrears on 30 June at the rate of 7 per cent.The exchange rate information is: What journal entries are required in McGrath Ltd's books for 1 July 2016 and 30 June 2017 and 30 June 2018 in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

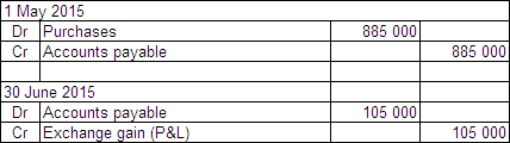

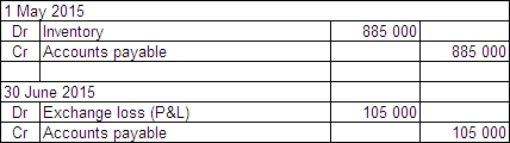

On 1 May 2015 Harry's Plastics Ltd acquires goods from a supplier in the US.The goods are shipped f.o.b.from the United States on 1 May 2015.The cost of the goods is US$1 500 000.The amount has not been paid at period end,30 June 2015.Exchange rates are as follows: Harry's Plastics Ltd uses a perpetual inventory system.

What entries are required at transaction date and reporting date (rounded to the nearest whole A$)?

A)

B)

C)

D)

What entries are required at transaction date and reporting date (rounded to the nearest whole A$)?

A)

B)

C)

D)

Question

Question

Question

Question

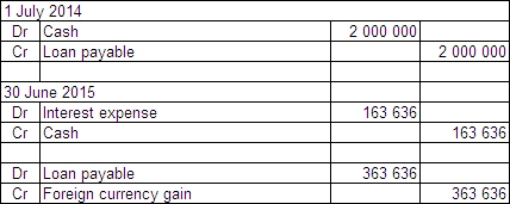

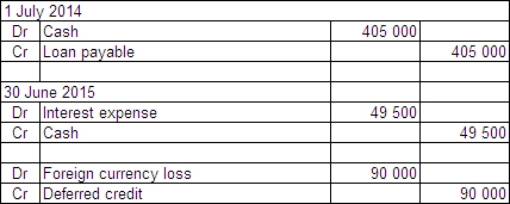

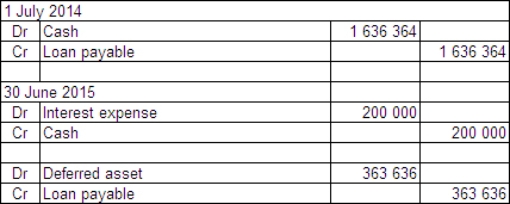

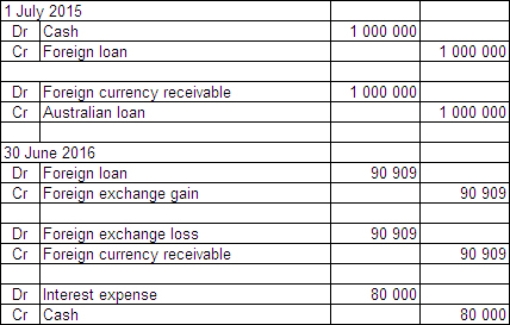

On 1 July 2014 Waugh Ltd enters into an arrangement with a US bank-Big Bank-to borrow US$900 000.The term of the loan is 3 years with interest payable annually in arrears on 30 June at the rate of 10 per cent.The exchange rate information is: What journal entries are required in Waugh Ltd's books for 1 July 2014 and 30 June 2015 in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

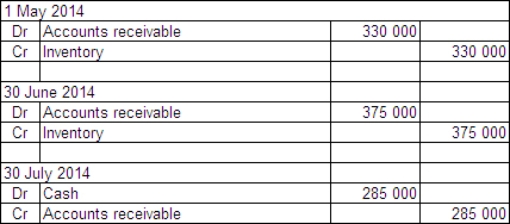

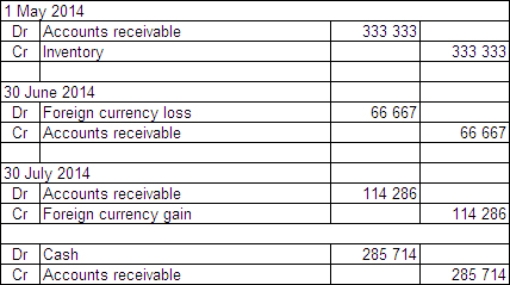

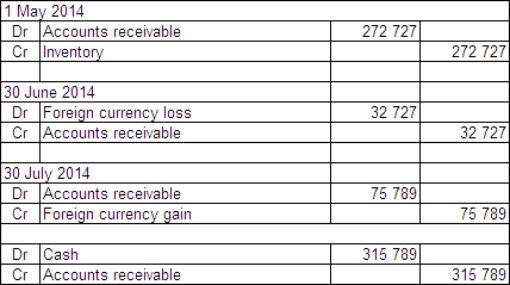

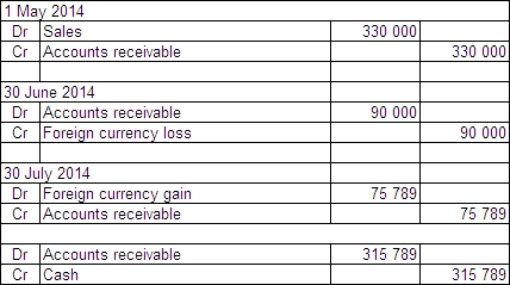

On 1 May 2014 Moorooba Exporters Ltd sells inventory to a customer in Singapore.The inventory is sold for $S300 000 and payment is not due until 30 July 2014.The reporting date for Moorooba Exporters Ltd is 30 June.The exchange rate information is: Moorooba Exporters uses a perpetual inventory system.What journal entries are required in Moorooba Exporters Ltd's books to record the transaction,adjustments at the end of the period and settlement in accordance with AASB 121 (rounded to the nearest whole A$)?

What is the realised gain/loss on the monetary item?

A)

Realised loss $45 000

Realised loss $45 000

B)

Realised loss $66 667

Realised loss $66 667

C)

Realised gain $43 062

Realised gain $43 062

D)

Realised gain $90 000

Realised gain $90 000

What is the realised gain/loss on the monetary item?

A)

Realised loss $45 000B)

Realised loss $66 667C)

Realised gain $43 062D)

Realised gain $90 000 Question

Question

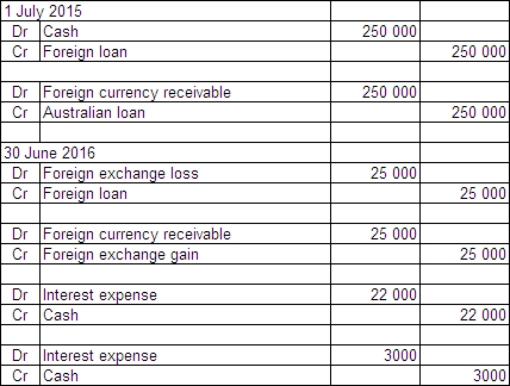

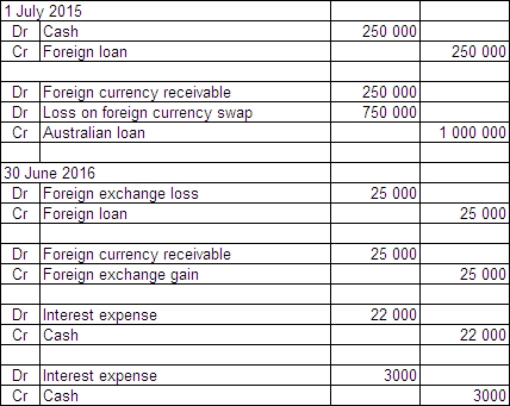

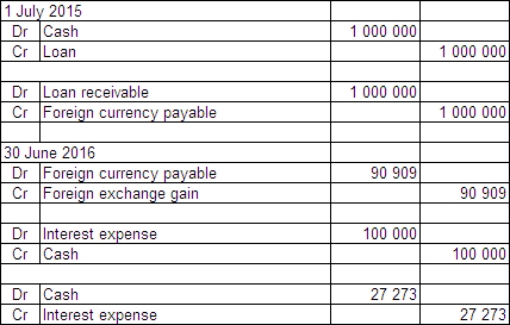

On 1 July 2015 Jarrets Ltd borrows £500 000 from a British bank at an interest rate of 8 per cent,repayable in pounds sterling (£)and with interest due on 30 June each year.The term of the loan is 3 years.On the same date Fitners Ltd borrows A$1 million from an Australian bank at an interest rate of 10 per cent.The term of the loan is 3 years.Jarrets and Fitners decide to swap their interest and principal obligations on 1 July 2015.Exchange rate information is as follows: Both Jarrets and Fitners are Australian companies.What are the journal entries to record the swap for the period ended 30 June 2016 in Jarrets Ltd's books (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

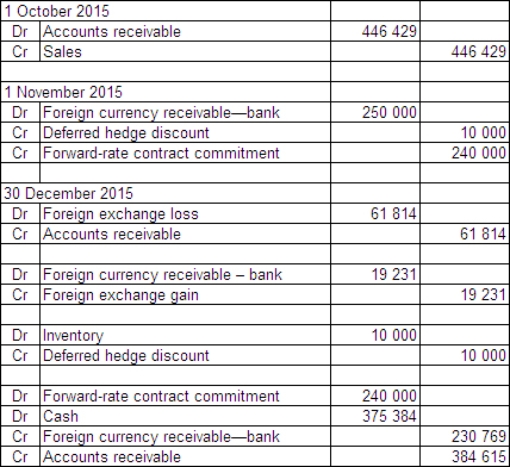

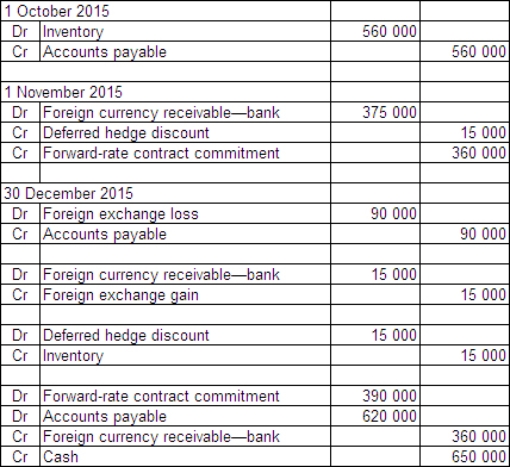

Emu Exports Ltd sold products to a New Zealand company.The sales contract was denominated in $NZ.On 1 October 2015,$NZ500 000 worth of products were sold with the terms f.o.b.shipping point and payment due 30 December 2015.A forward-exchange contract in which the bank agrees to purchase $NZ300 000 from Emu Exports on 30 December 2015 is entered into on 1 November 2015.The forward-exchange rate is A$1 = $NZ1.25.Other exchange rates are as follows: What are the journal entries to record the above transactions from 1 October through to 30 December 2015 in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

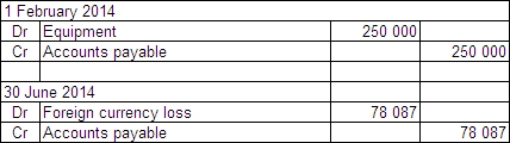

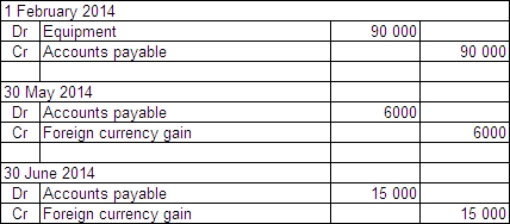

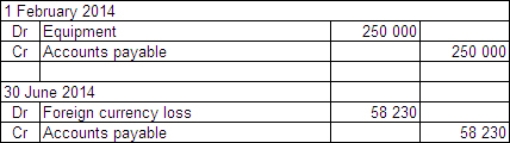

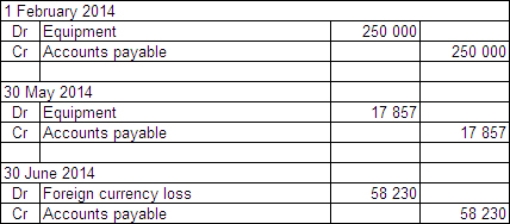

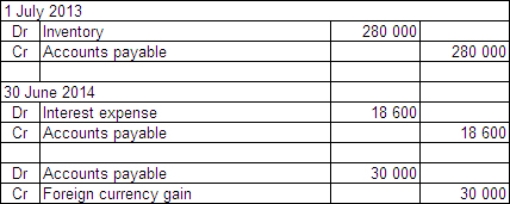

On 1 February 2014,Morinda Ltd completes a binding agreement to purchase a hydraulic lift from a manufacturer located in Germany.The cost of the equipment is €150 000.The construction of the lift is completed on 30 May 2014,and it is considered to be a qualifying asset according to AASB 123.The amount owing has not been paid by reporting date 30 June 2014.The following is information about the exchange rates: What entries are required to record the transaction and subsequent events in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

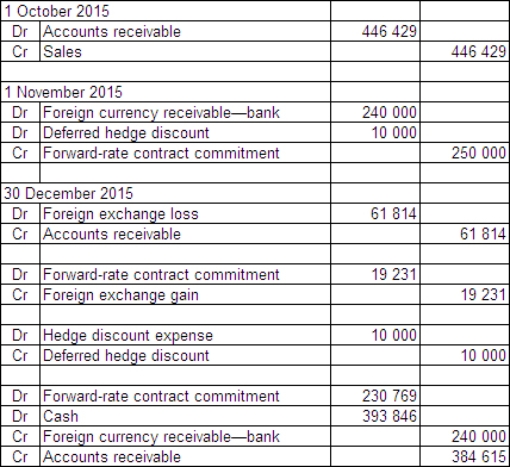

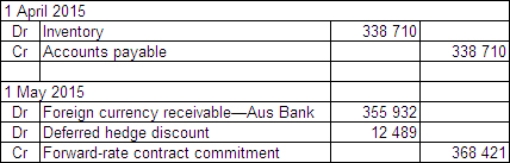

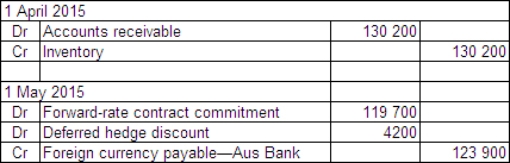

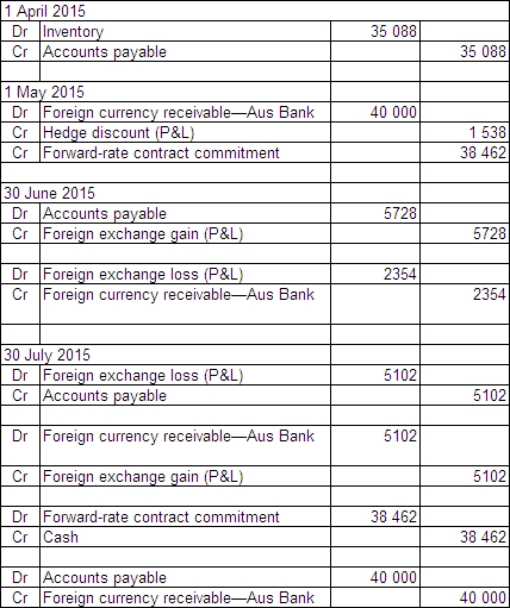

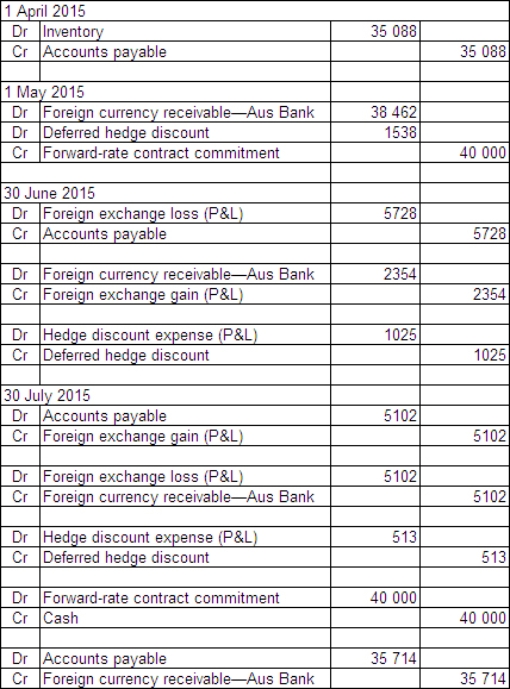

Sure Ltd purchased goods for £210 000 from a British supplier on 1 April 2015.The amount owing on the purchase is payable on 30 July 2015.On 1 May 2015 a forward-exchange contract for the delivery of £210 000 on 30 July 2015 is taken out with Aus Bank.Exchange rates are as follows:  What entries are required to record the initial transaction and the forward-exchange contract in accordance with AASB 121 and AASB 139 (rounded to the nearest whole A$)?

What entries are required to record the initial transaction and the forward-exchange contract in accordance with AASB 121 and AASB 139 (rounded to the nearest whole A$)?

A)

B)

C)

D)

What entries are required to record the initial transaction and the forward-exchange contract in accordance with AASB 121 and AASB 139 (rounded to the nearest whole A$)?A)

B)

C)

D)

Question

Question

Question

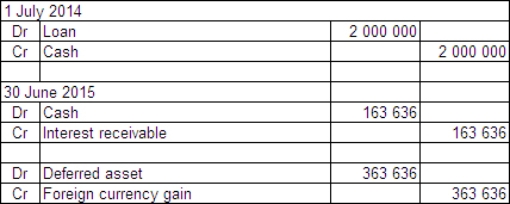

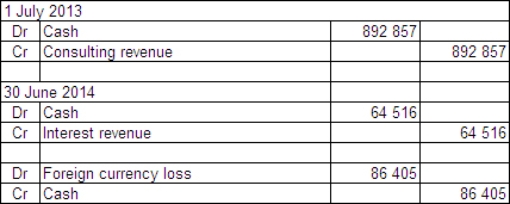

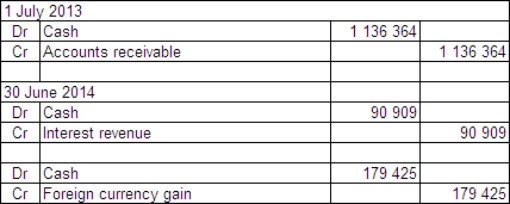

On 1 July 2013 Kanga Consultants Ltd completes a contract to provide advice on the installation of a networked computer system to a company in the US.The client pays the fee of US$500 000 into Kanga Consultants' US bank account on that date.The bank pays interest of 8 per cent annually on 30 June.The exchange rate information is: What journal entries are required in Kanga Consultants Ltd's books for 1 July 2013 and 30 June 2014 in accordance with AASB 1012 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

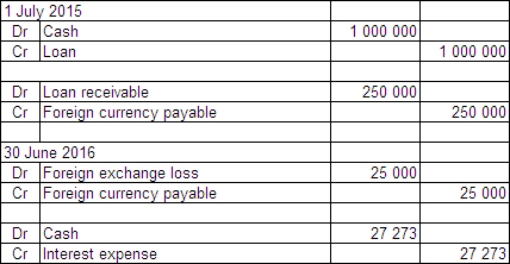

On 1 July 2015 Jarrets Ltd borrows £500 000 from a British bank at an interest rate of 8 per cent,repayable in pounds sterling (£)and with interest due on 30 June each year.The term of the loan is 3 years.On the same date Fitners Ltd borrows A$1 million from an Australian bank at an interest rate of 10 per cent.The term of the loan is 3 years.Jarrets and Fitners decide to swap their interest and principal obligations on 1 July 2015.Exchange rate information is as follows: Both Jarrets and Fitners are Australian companies.What are the journal entries to record the swap for the period ended 30 June 2016 in Fitners Ltd's books (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

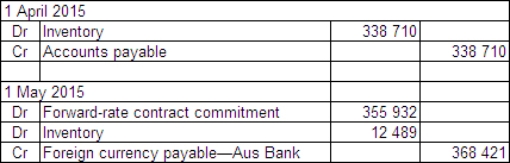

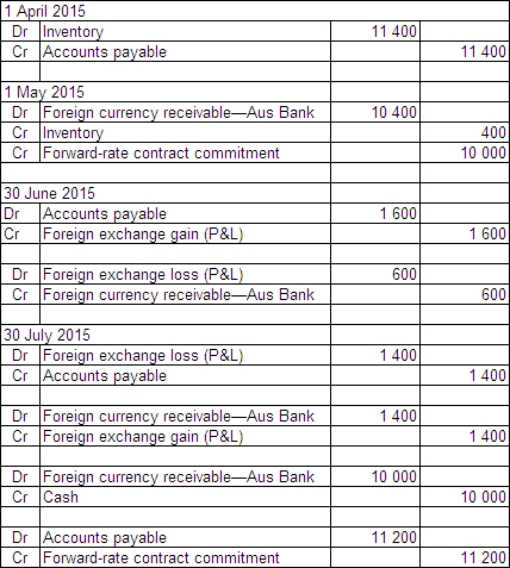

Safety Ltd purchased goods for £20 000 from a British supplier on 1 April 2015.The amount owing on the purchase is payable on 30 July 2015.On 1 May 2015 a forward-exchange contract for the delivery of £20 000 on 30 July 2015 is taken out with Aus Bank.Safety Ltd's reporting date is 30 June.Exchange rates are as follows:  What entries are required to report these transactions in accordance with AASB 121 (rounded to the nearest whole A$)?

What entries are required to report these transactions in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

What entries are required to report these transactions in accordance with AASB 121 (rounded to the nearest whole A$)?A)

B)

C)

D)

Question

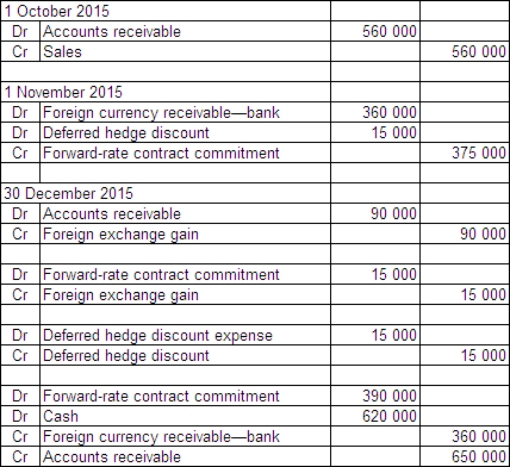

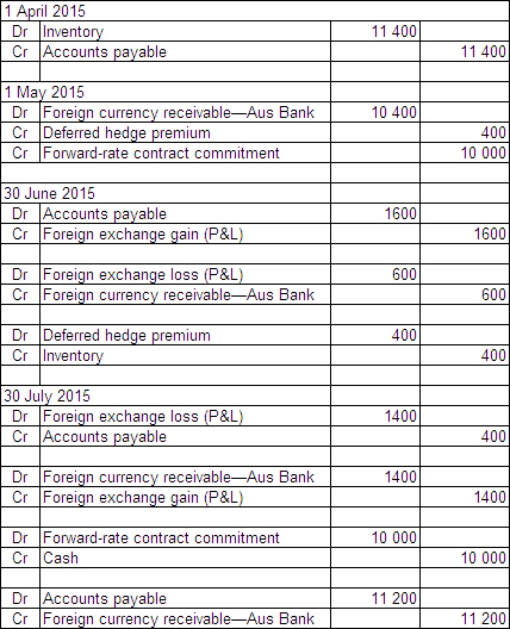

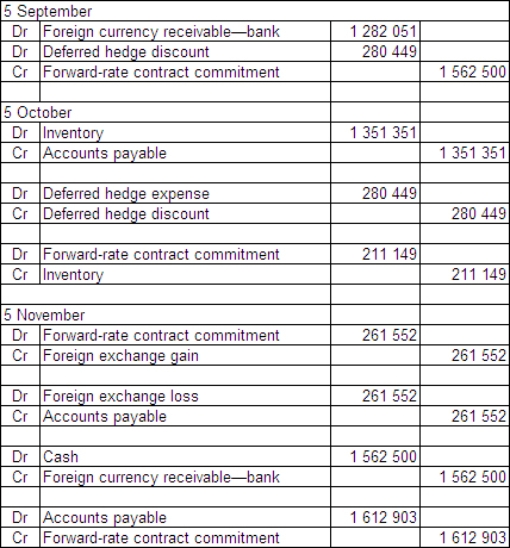

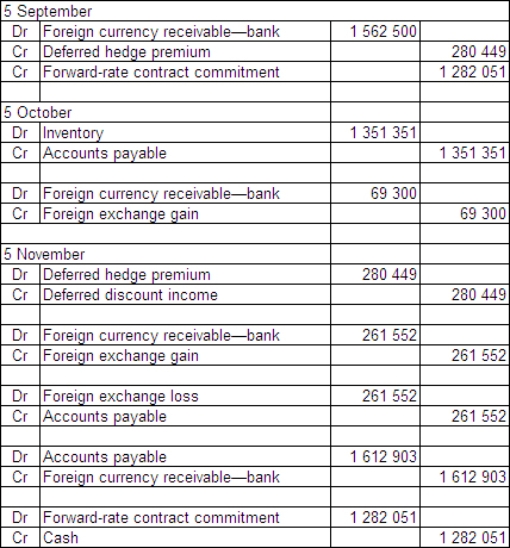

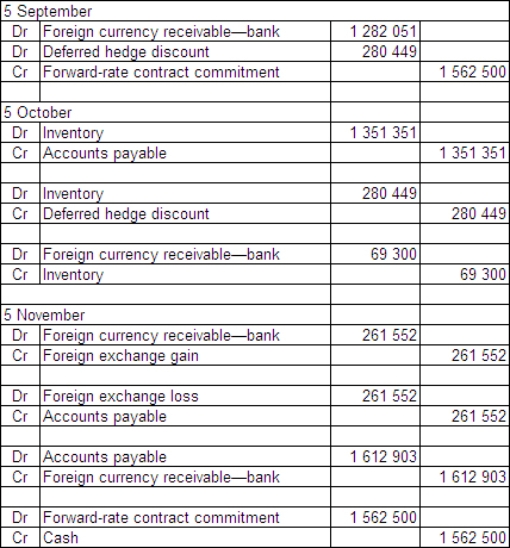

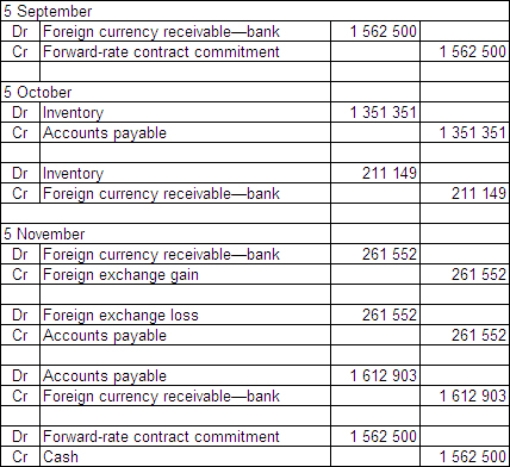

On 5 September 2014 Russell Ltd places an order for €500 000 of inventory from a Swedish supplier.The terms for the purchase of the goods are that they are f.o.b.shipping point and they are to be paid for on 5 November.The financial controller of Russell Ltd enters into a forward-exchange contract on 5 September and designates it as a hedge for the purchase.The forward-exchange contract is for €500 000 to be supplied by the bank on 5 November 2014.The goods are shipped on 5 October 2014 and are paid for on 5 November.  What are the journal entries to record the above transactions from 5 September through to 5 November in accordance with AASB 121 (rounded to the nearest whole A$)?

What are the journal entries to record the above transactions from 5 September through to 5 November in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

What are the journal entries to record the above transactions from 5 September through to 5 November in accordance with AASB 121 (rounded to the nearest whole A$)?A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/78

Play

Full screen (f)

Deck 32: Accounting for Foreign Currency Transactions

1

Monetary items are units of currency held and assets and liabilities to be received or paid in a fixed or determinable number of units of currency.

True

2

Issues in relation to foreign currency arise when a reporting entity based in Australia has transactions with an overseas entity and the transaction is denominated in Australian currency.

False

3

AASB 121 requires foreign currency monetary items that are expected to be settled in the short term to be translated at the spot rate at reporting date,but does not require this treatment for long-term monetary items denominated in foreign currencies.

False

4

The functional currency of an entity is the currency of the prime economic environment in which the entity operates.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

5

AASB 121 defines an exchange rate as a ratio for the exchange of two currencies at a particular time.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

6

The essential feature of a non-monetary item is the absence of a right to receive (or an obligation to deliver)a fixed or determinable number of units of currency.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

7

To classify an arrangement as a hedge,and therefore to apply 'hedge accounting',AASB 132 requires a set of strict conditions be met.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

8

In selecting the appropriate foreign currency exchange rates to apply in translating foreign currency transactions,the accountant exercises an important element of judgment about whether the rates are overvaluing or undervaluing the reporting currency.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

9

According to AASB 123 a qualifying asset is one that necessarily takes a substantial period of time to get ready for its intended use or sale.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

10

The purpose of 'hedge accounting' is to recognise the offsetting effects on profit or loss of changes in the nominal values of the financial instrument and the hedging instrument.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

11

An entity may change its functional currency when there is a change in the underlying transactions,events and conditions.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

12

If the foreign currency exchange rate between Australia and the US was A$1.00 = US$0.55 on 1 October 2014 and moved to be A$1.00 = US$0.60 one month later,the Australian dollar has decreased relative to the foreign currency.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

13

Inventory is an example of a monetary item.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

14

Hedges cannot be designated and/or documented on a retrospective basis.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

15

It seems pointless to distinguish between different types of hedges,as the accounting treatment is the same for all hedging,that is,all changes in fair values of hedging instruments are recognised in profit or loss.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

16

An example of a foreign currency swap is when a loan denominated in one currency is swapped for a loan denominated in another currency.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

17

Exchange gains or losses on a qualifying asset that arise before it ceases to be a qualifying asset are to be deferred and amortised over the life of the asset according to AASB 123.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

18

Management may exercise its judgment to determine the functional currency that most faithfully represents the economic effects of the underlying transactions,events and conditions.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

19

AASB 121 requires foreign currency transactions to be recorded,on initial recognition in the presentation currency,by applying to the foreign currency amount the spot exchange rate between the presentation currency and the foreign currency at the date of the transaction.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

20

A hedge is defined by AASB 139 as an action taken,whether by entering into a foreign currency contract or otherwise,with the objective of maximising the possible positive effects of movements in exchange rates.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

21

On 1 May 2015 Harriet's Importers Ltd acquires goods from a supplier in Britain.The goods are shipped f.o.b.from England on 1 May 2015.The cost of the goods is £200 000.The amount has not been paid at period end 30 June 2015.Exchange rates are as follows: Harriet's Importers Ltd uses a perpetual inventory system.

What entries are required at transaction date and reporting date (rounded to the nearest whole A$)?

A)

B)

C)

D)

What entries are required at transaction date and reporting date (rounded to the nearest whole A$)?

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

22

There are two broad categories of foreign currency issues that arise in financial reporting.They are:

A) reporting purchase price parity and reporting foreign interest rate adjustments.

B) accounting for foreign currency debt and offshore financing.

C) accounting for foreign currency transactions and translating the accounts of foreign subsidiaries.

D) accounting for foreign currencies using the forex buy rate and the forex sell rate.

A) reporting purchase price parity and reporting foreign interest rate adjustments.

B) accounting for foreign currency debt and offshore financing.

C) accounting for foreign currency transactions and translating the accounts of foreign subsidiaries.

D) accounting for foreign currencies using the forex buy rate and the forex sell rate.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

23

On 1 September 2015 Antique Furniture Importers acquires furniture from a supplier in Europe.The furniture is shipped f.o.b.from Brussels on 1 September 2015.The cost of the furniture is €500 000.The amount has not been paid at 30 September 2015.Exchange rates are as follows: What is the amount payable at 1 September and 30 September 2015in Australian dollars (rounded to the nearest whole A$)?

Did the Australian dollar strengthen or weaken?

A)

The Australian dollar weakened.

B)

The Australian dollar strengthened.

C)

The Australian dollar strengthened.

D)

The Australian dollar weakened.

Did the Australian dollar strengthen or weaken?

A)

The Australian dollar weakened.

B)

The Australian dollar strengthened.

C)

The Australian dollar strengthened.

D)

The Australian dollar weakened.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

24

The exchange rate for a currency depends on many factors including:

A) the price of McDonald's hamburgers in each country.

B) the rate at which the Australian currency is pegged at relative to the other currency of interest.

C) the price of options on futures of the foreign currency.

D) the demand for and supply of the currency in the market.

A) the price of McDonald's hamburgers in each country.

B) the rate at which the Australian currency is pegged at relative to the other currency of interest.

C) the price of options on futures of the foreign currency.

D) the demand for and supply of the currency in the market.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

25

If an organisation enters a foreign currency swap it will effectively insulate itself against the effects of changes in the spot rates.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

26

The effect of an increase in the exchange rate for Australian dollars relative to other major world currencies would include:

A) Offshore debt would become more expensive.

B) The cost of importing goods from overseas would increase.

C) People buying goods overseas with Australian dollars would find the goods relatively cheaper than before.

D) The cost of Australian exports for overseas buyers would decrease.

A) Offshore debt would become more expensive.

B) The cost of importing goods from overseas would increase.

C) People buying goods overseas with Australian dollars would find the goods relatively cheaper than before.

D) The cost of Australian exports for overseas buyers would decrease.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

27

A foreign currency transaction shall be recorded on initial recognition in the:

A) presentation currency.

B) local currency.

C) foreign currency.

D) functional currency.

A) presentation currency.

B) local currency.

C) foreign currency.

D) functional currency.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

28

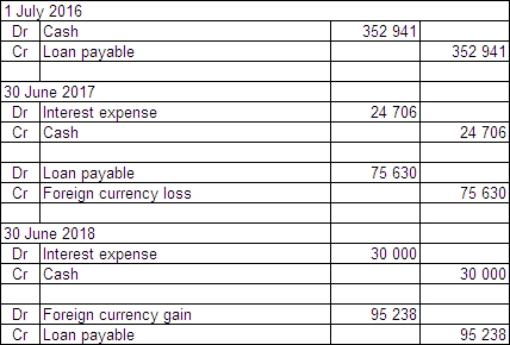

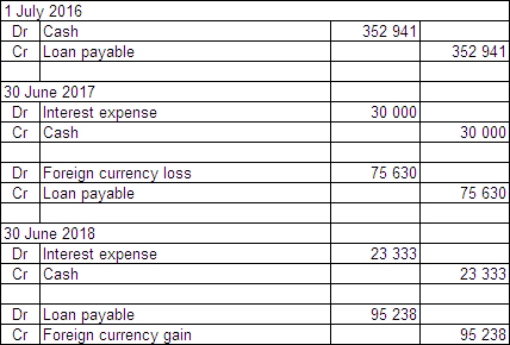

On 1 July 2016 McGrath Ltd enters into an arrangement with a Hong Kong bank to borrow $HK1 500 000.The term of the loan is 3 years with interest payable annually in arrears on 30 June at the rate of 7 per cent.The exchange rate information is: What journal entries are required in McGrath Ltd's books for 1 July 2016 and 30 June 2017 and 30 June 2018 in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

29

The spot rate is defined in AASB 121 as:

A) the rate at which the currency to be exchanged is currently selling against a bundle of currencies of major trading partners.

B) the exchange rate for immediate delivery of currencies to be exchanged.

C) one identified exchange rate for the relevant currencies from the period on or around the date of the transaction.

D) the current exchange rate as implied by forward-exchange contracts in place at the time of the transaction.

A) the rate at which the currency to be exchanged is currently selling against a bundle of currencies of major trading partners.

B) the exchange rate for immediate delivery of currencies to be exchanged.

C) one identified exchange rate for the relevant currencies from the period on or around the date of the transaction.

D) the current exchange rate as implied by forward-exchange contracts in place at the time of the transaction.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

30

The Big Mac index is:

A) an indicator of the economic wealth of a country, applied to a capacity to purchase Big Macs with the average wage.

B) a measure of interest rate parity such that the exchange rates between countries can be compared to assess whether or not interest rates are too high or low in a particular country relative to other major currencies in the world.

C) a measure of purchasing power parity applied to a 'real' product that is essentially identical and available around the world.

D) a measure of interest rate parity such that the exchange rates between countries can be compared to assess whether or not interest rates are too high or low in a particular country relative to other major currencies in the world and a measure of purchasing power parity applied to a 'real' product that is essentially identical and available around the world.

A) an indicator of the economic wealth of a country, applied to a capacity to purchase Big Macs with the average wage.

B) a measure of interest rate parity such that the exchange rates between countries can be compared to assess whether or not interest rates are too high or low in a particular country relative to other major currencies in the world.

C) a measure of purchasing power parity applied to a 'real' product that is essentially identical and available around the world.

D) a measure of interest rate parity such that the exchange rates between countries can be compared to assess whether or not interest rates are too high or low in a particular country relative to other major currencies in the world and a measure of purchasing power parity applied to a 'real' product that is essentially identical and available around the world.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

31

What is the required treatment for long-term monetary items denominated in a foreign currency according to AASB 121 and what is a concern that has been raised about the treatment?

A) Long-term foreign currency monetary items are not required to be re-translated at reporting date. The concern raised is that the failure to reflect the affect of changes in the exchange rate on items that are exposed to forex risk does not provide useful information for decision making about the risk exposure of the reporting entity.

B) Long-term foreign currency monetary items are required to be re-translated at the spot exchange rate at reporting date and the difference is deferred to be recognised/amortised over the life of the monetary item. The concern that has been raised is that the deferred items are not assets or liabilities in terms of the conceptual framework and are therefore meaningless in the statement of financial position and misleading for users of the financial statements.

C) Long-term foreign currency monetary items are not required to be re-translated at reporting date, but the exchange rates, maturity dates and applicable forward rates are required note disclosures. The concern raised about this treatment is that the need to reflect the risk exposure in foreign currency denominated monetary items is not addressed through measurement, but only through disclosure, leaving the burden of assessing the impact on the financial position and performance of the entity up to the user.

D) Long-term foreign currency monetary items are required to be re-translated at the spot rate at reporting date and any differences treated as gains or losses in the statement of comprehensive income. The concern raised about this treatment is that the amounts of profit and loss recognised in the statement of comprehensive income are actually unrealised and there is considerable doubt about whether or not they would ever be realised as a result of the fluctuating nature of exchange rates.

A) Long-term foreign currency monetary items are not required to be re-translated at reporting date. The concern raised is that the failure to reflect the affect of changes in the exchange rate on items that are exposed to forex risk does not provide useful information for decision making about the risk exposure of the reporting entity.

B) Long-term foreign currency monetary items are required to be re-translated at the spot exchange rate at reporting date and the difference is deferred to be recognised/amortised over the life of the monetary item. The concern that has been raised is that the deferred items are not assets or liabilities in terms of the conceptual framework and are therefore meaningless in the statement of financial position and misleading for users of the financial statements.

C) Long-term foreign currency monetary items are not required to be re-translated at reporting date, but the exchange rates, maturity dates and applicable forward rates are required note disclosures. The concern raised about this treatment is that the need to reflect the risk exposure in foreign currency denominated monetary items is not addressed through measurement, but only through disclosure, leaving the burden of assessing the impact on the financial position and performance of the entity up to the user.

D) Long-term foreign currency monetary items are required to be re-translated at the spot rate at reporting date and any differences treated as gains or losses in the statement of comprehensive income. The concern raised about this treatment is that the amounts of profit and loss recognised in the statement of comprehensive income are actually unrealised and there is considerable doubt about whether or not they would ever be realised as a result of the fluctuating nature of exchange rates.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

32

An exception to the requirement that foreign currency monetary items should be re-translated at the reporting date is:

A) when the foreign exchange rate is considered to be undervalued.

B) when the foreign currency exchange rate is fixed for a particular transaction according to a contractual arrangement.

C) when exchange rates are expected to move in the opposite direction shortly after reporting date.

D) when the foreign exchange rate is considered to be overvalued.

A) when the foreign exchange rate is considered to be undervalued.

B) when the foreign currency exchange rate is fixed for a particular transaction according to a contractual arrangement.

C) when exchange rates are expected to move in the opposite direction shortly after reporting date.

D) when the foreign exchange rate is considered to be overvalued.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

33

On 1 May 2015 Harry's Plastics Ltd acquires goods from a supplier in the US.The goods are shipped f.o.b.from the United States on 1 May 2015.The cost of the goods is US$1 500 000.The amount has not been paid at period end,30 June 2015.Exchange rates are as follows: Harry's Plastics Ltd uses a perpetual inventory system.

What entries are required at transaction date and reporting date (rounded to the nearest whole A$)?

A)

B)

C)

D)

What entries are required at transaction date and reporting date (rounded to the nearest whole A$)?

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

34

AASB 121 requires that the initial recognition of a foreign currency transaction be:

A) in the amount of the foreign currency.

B) at the closing rate at balance date.

C) at the rate the currency is expected to be exchanged at on the settlement date for the monetary asset or liability based on the current market price of futures contracts for the relevant foreign currency.

D) at the spot rate at the date of the transaction.

A) in the amount of the foreign currency.

B) at the closing rate at balance date.

C) at the rate the currency is expected to be exchanged at on the settlement date for the monetary asset or liability based on the current market price of futures contracts for the relevant foreign currency.

D) at the spot rate at the date of the transaction.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

35

The effect of a fall in the exchange rate for Australian dollars relative to other major world currencies would include:

A) People buying goods overseas with Australian dollars would find the goods relatively cheaper than before.

B) The cost of importing goods from overseas would increase.

C) The cost of offshore debt would increase.

D) The cost of importing goods from overseas would increase and the cost of offshore debt would increase.

A) People buying goods overseas with Australian dollars would find the goods relatively cheaper than before.

B) The cost of importing goods from overseas would increase.

C) The cost of offshore debt would increase.

D) The cost of importing goods from overseas would increase and the cost of offshore debt would increase.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

36

Apart from some limited exceptions,AASB 121 requires that exchange differences on monetary items shall be:

A) deferred and recognised when the associated asset or liability is realised or settled.

B) treated as a reserve or provision against the associated monetary item.

C) not recognised in the accounts until the monetary asset is received or monetary liability settled.

D) recognised as income or an expense in the reporting period in which the exchange rates change.

A) deferred and recognised when the associated asset or liability is realised or settled.

B) treated as a reserve or provision against the associated monetary item.

C) not recognised in the accounts until the monetary asset is received or monetary liability settled.

D) recognised as income or an expense in the reporting period in which the exchange rates change.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

37

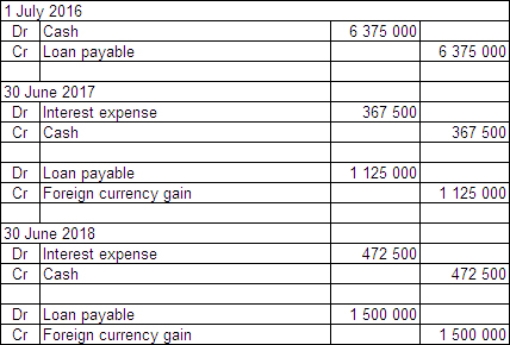

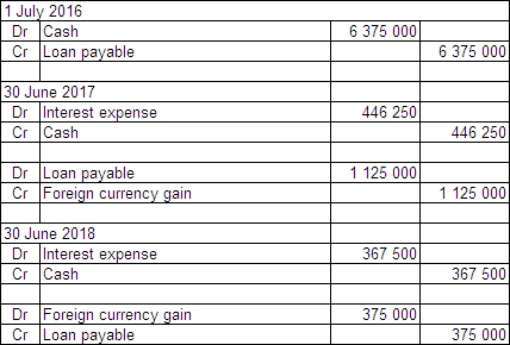

On 1 July 2014 Waugh Ltd enters into an arrangement with a US bank-Big Bank-to borrow US$900 000.The term of the loan is 3 years with interest payable annually in arrears on 30 June at the rate of 10 per cent.The exchange rate information is: What journal entries are required in Waugh Ltd's books for 1 July 2014 and 30 June 2015 in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

38

Examples of monetary items that may be denominated in foreign currencies include:

A) accounts payable and receivable, inventory, bank overdrafts.

B) interest receivable and payable, loans, accounts payable.

C) inventory, interest receivable, supplies, accounts payable.

D) prepayments, loans, accounts payable, debentures payable.

A) accounts payable and receivable, inventory, bank overdrafts.

B) interest receivable and payable, loans, accounts payable.

C) inventory, interest receivable, supplies, accounts payable.

D) prepayments, loans, accounts payable, debentures payable.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

39

AASB 121 requires that foreign currency monetary items outstanding at reporting date must be:

A) translated at the spot rate at the transaction date.

B) reported at the forward-exchange rate based on the 90-day bank bill rate at that date.

C) translated at the spot rate at reporting date.

D) translated at the spot rate at settlement date.

A) translated at the spot rate at the transaction date.

B) reported at the forward-exchange rate based on the 90-day bank bill rate at that date.

C) translated at the spot rate at reporting date.

D) translated at the spot rate at settlement date.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

40

On 1 January 2014 Antique Furniture Importers acquires furniture from a supplier in Europe.The furniture is shipped f.o.b.from Brussels on 1 January 2014.The cost of the furniture is €600 000.The amount has not been paid at 31 January 2014.Exchange rates are as follows: What is the amount payable at 1 January and 31 January 2014 in Australian dollars (rounded to the nearest whole A$)?

Did the Australian dollar strengthen or weaken?

A)

The Australian dollar weakened.

B)

The Australian dollar strengthened.

C)

The Australian dollar weakened.

D)

The Australian dollar strengthened.

Did the Australian dollar strengthen or weaken?

A)

The Australian dollar weakened.

B)

The Australian dollar strengthened.

C)

The Australian dollar weakened.

D)

The Australian dollar strengthened.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

41

The functional currency of an entity:

A) never changes once determined.

B) must be assessed and changed annually.

C) can change if there is a change in underlying transactions, events and conditions which determine the functional currency.

D) can change as a consequence of the foreign currency transactions that are undertaken by the parent entity.

A) never changes once determined.

B) must be assessed and changed annually.

C) can change if there is a change in underlying transactions, events and conditions which determine the functional currency.

D) can change as a consequence of the foreign currency transactions that are undertaken by the parent entity.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

42

On 1 May 2014 Moorooba Exporters Ltd sells inventory to a customer in Singapore.The inventory is sold for $S300 000 and payment is not due until 30 July 2014.The reporting date for Moorooba Exporters Ltd is 30 June.The exchange rate information is: Moorooba Exporters uses a perpetual inventory system.What journal entries are required in Moorooba Exporters Ltd's books to record the transaction,adjustments at the end of the period and settlement in accordance with AASB 121 (rounded to the nearest whole A$)?

What is the realised gain/loss on the monetary item?

A)

Realised loss $45 000

B)

Realised loss $66 667

C)

Realised gain $43 062

D)

Realised gain $90 000

What is the realised gain/loss on the monetary item?

A)

Realised loss $45 000B)

Realised loss $66 667C)

Realised gain $43 062D)

Realised gain $90 000 Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

43

The following data is provided for the fair value of a share portfolio,and the fair value of a forward contract taken out on 1 July 2014 to 'hedge' movements in the fair value of the shares.Assume the hedge was highly effective at inception of the hedge. Which of the following statements is true?

A) It is not an effective hedge as there was a difference of $10 000 000 between the fair values of the shares and the forward contract at inception.

B) It is not an effective hedge as a forward contract cannot be used as a hedging instrument.

C) It is an effective hedge as the movement in the fair value of the hedging instrument between 1 July 2014 and 30 June 2017offset movements in fair value of the shares in the same period, which is within the 80-125 per cent hedge effectiveness range.

D) It is not an effective hedge as the movements in the fair value of the hedging instrument failed to offset movements in the fair value of the shares and stay within the 80-125 per cent hedge effectiveness range throughout the period to 30 June 2017.

A) It is not an effective hedge as there was a difference of $10 000 000 between the fair values of the shares and the forward contract at inception.

B) It is not an effective hedge as a forward contract cannot be used as a hedging instrument.

C) It is an effective hedge as the movement in the fair value of the hedging instrument between 1 July 2014 and 30 June 2017offset movements in fair value of the shares in the same period, which is within the 80-125 per cent hedge effectiveness range.

D) It is not an effective hedge as the movements in the fair value of the hedging instrument failed to offset movements in the fair value of the shares and stay within the 80-125 per cent hedge effectiveness range throughout the period to 30 June 2017.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

44

On 1 July 2015 Jarrets Ltd borrows £500 000 from a British bank at an interest rate of 8 per cent,repayable in pounds sterling (£)and with interest due on 30 June each year.The term of the loan is 3 years.On the same date Fitners Ltd borrows A$1 million from an Australian bank at an interest rate of 10 per cent.The term of the loan is 3 years.Jarrets and Fitners decide to swap their interest and principal obligations on 1 July 2015.Exchange rate information is as follows: Both Jarrets and Fitners are Australian companies.What are the journal entries to record the swap for the period ended 30 June 2016 in Jarrets Ltd's books (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

45

Emu Exports Ltd sold products to a New Zealand company.The sales contract was denominated in $NZ.On 1 October 2015,$NZ500 000 worth of products were sold with the terms f.o.b.shipping point and payment due 30 December 2015.A forward-exchange contract in which the bank agrees to purchase $NZ300 000 from Emu Exports on 30 December 2015 is entered into on 1 November 2015.The forward-exchange rate is A$1 = $NZ1.25.Other exchange rates are as follows: What are the journal entries to record the above transactions from 1 October through to 30 December 2015 in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following statements is correct with respect to AASB 121 The Effects of Changes in Foreign Exchange Rates?

A) Foreign currency transactions are recorded, on initial recognition in the presentation currency, by applying to the foreign currency amount the spot exchange rate between the presentation currency and the foreign currency at the date of the transaction.

B) At each end of the reporting period, foreign currency monetary items shall be translated using the closing rate.

C) At each end of the reporting period non-monetary items that are measured in terms of historical cost in a foreign currency shall be translated using the exchange rate at the date of the transaction.

D) At each end of the reporting period, non-monetary items that are measured at fair value in a foreign currency shall be translated using closing rate.

A) Foreign currency transactions are recorded, on initial recognition in the presentation currency, by applying to the foreign currency amount the spot exchange rate between the presentation currency and the foreign currency at the date of the transaction.

B) At each end of the reporting period, foreign currency monetary items shall be translated using the closing rate.

C) At each end of the reporting period non-monetary items that are measured in terms of historical cost in a foreign currency shall be translated using the exchange rate at the date of the transaction.

D) At each end of the reporting period, non-monetary items that are measured at fair value in a foreign currency shall be translated using closing rate.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

47

For a cash flow hedge relating to the purchase of a particular asset,foreign exchange gains and losses made on the hedging instrument:

A) are all passed to profit or loss.

B) are passed to equity accounts up to the time of the underlying transaction, at which time they are then included as part of the cost of the asset. After this date, they are passed directly to profit or loss.

C) are all passed to the cost of the asset.

D) are passed to equity accounts up to the time of the expiration of the hedging instrument, at which time they are then included as part of the cost of the asset.

E) are passed directly to profit or loss up to the time of the underlying transaction. After this date, they are passed to equity accounts, up to the time of the expiration of the hedging instrument, at which time they are then included as part of the cost of the asset.

A) are all passed to profit or loss.

B) are passed to equity accounts up to the time of the underlying transaction, at which time they are then included as part of the cost of the asset. After this date, they are passed directly to profit or loss.

C) are all passed to the cost of the asset.

D) are passed to equity accounts up to the time of the expiration of the hedging instrument, at which time they are then included as part of the cost of the asset.

E) are passed directly to profit or loss up to the time of the underlying transaction. After this date, they are passed to equity accounts, up to the time of the expiration of the hedging instrument, at which time they are then included as part of the cost of the asset.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

48

On 1 February 2014,Morinda Ltd completes a binding agreement to purchase a hydraulic lift from a manufacturer located in Germany.The cost of the equipment is €150 000.The construction of the lift is completed on 30 May 2014,and it is considered to be a qualifying asset according to AASB 123.The amount owing has not been paid by reporting date 30 June 2014.The following is information about the exchange rates: What entries are required to record the transaction and subsequent events in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

49

Sure Ltd purchased goods for £210 000 from a British supplier on 1 April 2015.The amount owing on the purchase is payable on 30 July 2015.On 1 May 2015 a forward-exchange contract for the delivery of £210 000 on 30 July 2015 is taken out with Aus Bank.Exchange rates are as follows: What entries are required to record the initial transaction and the forward-exchange contract in accordance with AASB 121 and AASB 139 (rounded to the nearest whole A$)?

A)

B)

C)

D)

What entries are required to record the initial transaction and the forward-exchange contract in accordance with AASB 121 and AASB 139 (rounded to the nearest whole A$)?A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

50

The three principal types of hedges referred to in AASB 139 are:

A) fair-value hedges; market value hedges, cash-flow hedges.

B) fair-value hedges; natural hedges, cash-flow hedges.

C) fair-value hedges; hedges of net investments in a foreign operation, cash-flow hedges.

D) hedges of net investments in a foreign operation; market value hedges, cash-flow hedges.

A) fair-value hedges; market value hedges, cash-flow hedges.

B) fair-value hedges; natural hedges, cash-flow hedges.

C) fair-value hedges; hedges of net investments in a foreign operation, cash-flow hedges.

D) hedges of net investments in a foreign operation; market value hedges, cash-flow hedges.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

51

Exchange differences recognised as borrowing costs and included in the cost of an asset,are not recognised:

A) until the asset is ready for its intended use or sale, provided the capitalisation of costs does not mean that the cost of the asset exceeds recoverable amount.

B) until such time as they are deemed to be income and expenses by a resolution of the board of management.

C) until such time as income is derived, at which time they are passed directly to profit or loss.

D) until after the asset is ready for its intended use or sale, provided the capitalisation of costs does not mean that the cost of the asset exceeds recoverable amount.

A) until the asset is ready for its intended use or sale, provided the capitalisation of costs does not mean that the cost of the asset exceeds recoverable amount.

B) until such time as they are deemed to be income and expenses by a resolution of the board of management.

C) until such time as income is derived, at which time they are passed directly to profit or loss.

D) until after the asset is ready for its intended use or sale, provided the capitalisation of costs does not mean that the cost of the asset exceeds recoverable amount.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

52

On 1 July 2013 Kanga Consultants Ltd completes a contract to provide advice on the installation of a networked computer system to a company in the US.The client pays the fee of US$500 000 into Kanga Consultants' US bank account on that date.The bank pays interest of 8 per cent annually on 30 June.The exchange rate information is: What journal entries are required in Kanga Consultants Ltd's books for 1 July 2013 and 30 June 2014 in accordance with AASB 1012 (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

53

AASB 123 Borrowing Costs defines a qualifying asset as an asset that:

A) takes a period of greater than 12 months to get ready for its intended use or sale.

B) takes a substantial period of time to get ready for its intended use or sale.

C) takes a period of greater than 12 months to complete.

D) takes a substantial period of time to complete.

A) takes a period of greater than 12 months to get ready for its intended use or sale.

B) takes a substantial period of time to get ready for its intended use or sale.

C) takes a period of greater than 12 months to complete.

D) takes a substantial period of time to complete.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

54

On 1 July 2015 Jarrets Ltd borrows £500 000 from a British bank at an interest rate of 8 per cent,repayable in pounds sterling (£)and with interest due on 30 June each year.The term of the loan is 3 years.On the same date Fitners Ltd borrows A$1 million from an Australian bank at an interest rate of 10 per cent.The term of the loan is 3 years.Jarrets and Fitners decide to swap their interest and principal obligations on 1 July 2015.Exchange rate information is as follows: Both Jarrets and Fitners are Australian companies.What are the journal entries to record the swap for the period ended 30 June 2016 in Fitners Ltd's books (rounded to the nearest whole A$)?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

55

In terms of retrospectively assessing hedge effectiveness,which of the following situations does not meet the criteria for effectiveness?

A) Fair value of shares increased by $12 750; fair value of hedging instrument increased by $11 200

B) Fair value of shares increased by $12 800; fair value of hedging instrument decreased by $10 255

C) Fair value of shares decreased by $12 316; fair value of hedging instrument increased by $15 325

D) Fair value of shares decreased by $11 999; fair value of hedging instrument increased by $13 225

A) Fair value of shares increased by $12 750; fair value of hedging instrument increased by $11 200

B) Fair value of shares increased by $12 800; fair value of hedging instrument decreased by $10 255

C) Fair value of shares decreased by $12 316; fair value of hedging instrument increased by $15 325

D) Fair value of shares decreased by $11 999; fair value of hedging instrument increased by $13 225

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

56

Common examples of qualifying assets are assets that result from development and construction activities in:

A) agriculture; power generation facilities; investment property.

B) extractive industries; general insurance; investment property.

C) agriculture; general insurance; investment property.

D) extractive industries; power generation facilities; investment property.

A) agriculture; power generation facilities; investment property.

B) extractive industries; general insurance; investment property.

C) agriculture; general insurance; investment property.

D) extractive industries; power generation facilities; investment property.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following is not a condition that must be met,according to AASB 139,before a relationship qualifies for hedge accounting?

A) At the inception of the hedge, there is formal designation and documentation of the hedging relationship.

B) At the inception of the hedge, there is formal designation and documentation of the entity's risk management objective and strategy for undertaking the hedge.

C) The hedge is expected to be highly effective.

D) For fair-value hedges, a forecast transaction that is subject to the hedge must be highly probable.

A) At the inception of the hedge, there is formal designation and documentation of the hedging relationship.

B) At the inception of the hedge, there is formal designation and documentation of the entity's risk management objective and strategy for undertaking the hedge.

C) The hedge is expected to be highly effective.

D) For fair-value hedges, a forecast transaction that is subject to the hedge must be highly probable.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

58

The hedge effectiveness criteria prescribed in AASB 139 have made which type of financial instrument much less effective as a potential hedging instrument?

A) forward-foreign-exchange contract

B) option

C) futures contract

D) swap

A) forward-foreign-exchange contract

B) option

C) futures contract

D) swap

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

59

Safety Ltd purchased goods for £20 000 from a British supplier on 1 April 2015.The amount owing on the purchase is payable on 30 July 2015.On 1 May 2015 a forward-exchange contract for the delivery of £20 000 on 30 July 2015 is taken out with Aus Bank.Safety Ltd's reporting date is 30 June.Exchange rates are as follows: What entries are required to report these transactions in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

What entries are required to report these transactions in accordance with AASB 121 (rounded to the nearest whole A$)?A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

60

On 5 September 2014 Russell Ltd places an order for €500 000 of inventory from a Swedish supplier.The terms for the purchase of the goods are that they are f.o.b.shipping point and they are to be paid for on 5 November.The financial controller of Russell Ltd enters into a forward-exchange contract on 5 September and designates it as a hedge for the purchase.The forward-exchange contract is for €500 000 to be supplied by the bank on 5 November 2014.The goods are shipped on 5 October 2014 and are paid for on 5 November. What are the journal entries to record the above transactions from 5 September through to 5 November in accordance with AASB 121 (rounded to the nearest whole A$)?

A)

B)

C)

D)

What are the journal entries to record the above transactions from 5 September through to 5 November in accordance with AASB 121 (rounded to the nearest whole A$)?A)

B)

C)

D)

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

61

The following items are in the financial statements of Pirie Ltd as at 30 June 2015. Which of the following combinations identify all items required to be translated at spot rate on 30 June 2015 as prescribed in AASB 121 The Effects of Changes in Foreign Exchange Rates?

A) I and II

B) II and III

C) II and IV

D) III and IV

A) I and II

B) II and III

C) II and IV

D) III and IV

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

62

Discuss the accounting treatment required under AASB 121 The Effects of Changes in Foreign Exchange Rates when a reporting entity has a foreign currency monetary items at the reporting date.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following items is not within the scope of AASB 121 The Effects of Changes in Foreign Exchange Rates?

A) foreign currency denominated loans

B) bank deposits in foreign currency

C) investments in foreign operations

D) foreign currency derivatives

A) foreign currency denominated loans

B) bank deposits in foreign currency

C) investments in foreign operations

D) foreign currency derivatives

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

64

Describe,with examples,the reasons why organisations would want to swap a loan denominated in one currency for another.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

65

Explain why some opponents of the accounting prescribed in AASB 121 object to the requirement that long-term receivables and payables be translated using the reporting date spot rates.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

66

Discuss the situations in which the discontinuation of fair-value hedge accounting is to be done as provided for in AASB 139.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

67

What is a forward rate agreement?

Explain,with an example,how such an agreement can be used as a hedging instrument.

Explain,with an example,how such an agreement can be used as a hedging instrument.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following items is within the scope of AASB 121 The Effects of Changes in Foreign Exchange Rates?

A) translation of cash flows from foreign operations

B) presentation in a statement of cash flows of the cash flows arising from transactions in a foreign currency

C) hedge accounting for hedging a net investment in a foreign operation

D) presentation of an entity's financial statements in a foreign currency

A) translation of cash flows from foreign operations

B) presentation in a statement of cash flows of the cash flows arising from transactions in a foreign currency

C) hedge accounting for hedging a net investment in a foreign operation

D) presentation of an entity's financial statements in a foreign currency

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

69

Describe,with examples,the two tests of hedge effectiveness.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

70

According to AASB 139,what are the five conditions that must be met in order to apply 'hedge accounting'?

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

71

What are presentation and functional currencies?

How do they differ?

How do they differ?

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following items is a commonly used swap?

A) foreign currency swaps

B) options swap

C) investments in foreign operations swaps

D) foreign currency derivatives swaps

A) foreign currency swaps

B) options swap

C) investments in foreign operations swaps

D) foreign currency derivatives swaps

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

73

Explain the terms hedging instrument and hedged item,and how hedge accounting brings these two together.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following statements is correct with respect to AASB 121 The Effects of Changes in Foreign Exchange Rates?

A) When there is a change in an entity's functional currency, the entity shall apply the translation procedures applicable to the new functional currency prospectively from the date of the change.

B) When there is a change in an entity's functional currency, the entity shall apply the translation procedures applicable to the new functional currency retrospectively from the date of the change.

C) Exchange differences arising from the translation of long-term monetary items are recognised in profit or loss on settlement.

D) Exchange differences arising from long-term monetary items are deferred and amortised into operating profit or loss over the term of the long-term monetary asset or liability.

A) When there is a change in an entity's functional currency, the entity shall apply the translation procedures applicable to the new functional currency prospectively from the date of the change.

B) When there is a change in an entity's functional currency, the entity shall apply the translation procedures applicable to the new functional currency retrospectively from the date of the change.

C) Exchange differences arising from the translation of long-term monetary items are recognised in profit or loss on settlement.

D) Exchange differences arising from long-term monetary items are deferred and amortised into operating profit or loss over the term of the long-term monetary asset or liability.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

75

Where the hedge arrangement completely eliminates the consequences of adverse exchange-rate fluctuations,the purchase or sales arrangement is considered to be:

A) partially hedged.

B) positively hedged.

C) perfectly hedged.

D) negatively hedged.

A) partially hedged.

B) positively hedged.

C) perfectly hedged.

D) negatively hedged.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

76

Which of the following items is not a required condition for applying hedge accounting?

A) The hedge is expected to be highly effective.

B) The forecast transaction does not affect profit or loss.

C) The effectiveness of the hedge can be reliably measured.

D) The hedge is assessed on an ongoing basis.

A) The hedge is expected to be highly effective.

B) The forecast transaction does not affect profit or loss.

C) The effectiveness of the hedge can be reliably measured.

D) The hedge is assessed on an ongoing basis.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

77

How does the accounting treatment for qualifying monetary items differ from other foreign currency monetary items as prescribed under AASB 121 The Effects of Changes in Foreign Exchange Rates?

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

78

What is a qualifying asset,and what are the accounting implications in respect to accounting for foreign exchange differences when acquiring such an asset?

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 78 flashcards in this deck.