Deck 12: Structuring the Deal: Tax and Accounting Considerations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Case Study Short Essay Examination Questions

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

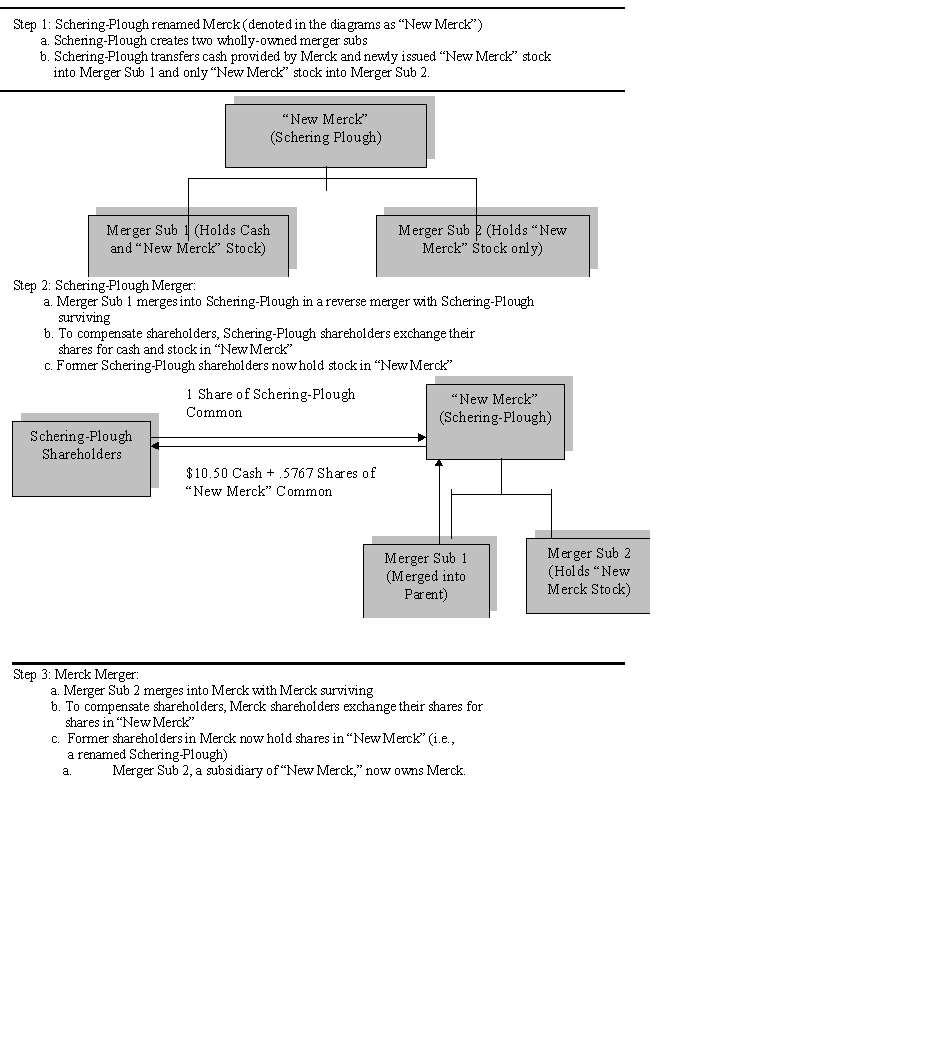

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently. Concluding Comments

Concluding Comments

In reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

Do you agree with the argument that the courts should focus on the form or structure of an agreement and not try to interpret the actual intent of the parties to the transaction? Explain your answer.

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently.

Concluding CommentsIn reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

Do you agree with the argument that the courts should focus on the form or structure of an agreement and not try to interpret the actual intent of the parties to the transaction? Explain your answer.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Case Study Short Essay Examination Questions

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently. Concluding Comments

In reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

How might allowing the form of a transaction to override the actual spirit or intent of the deal impact the cost of doing business for the parties involved in the distribution agreement? Be specific.

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently.

Concluding CommentsIn reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

How might allowing the form of a transaction to override the actual spirit or intent of the deal impact the cost of doing business for the parties involved in the distribution agreement? Be specific.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/97

Play

Full screen (f)

Deck 12: Structuring the Deal: Tax and Accounting Considerations

1

If a transaction involves a cash purchase of target stock,the target company's tax cost or basis in the acquired stock or assets is increased or "stepped up" automatically to their fair market value (FMV),which is equal to the purchase price paid by the acquirer.

False

2

In a triangular cash merger,the target firm may either be merged into an acquirer's operating or shell acquisition subsidiary with the subsidiary surviving or the acquirer's subsidiary is merged into the target firm with the target surviving.

True

3

The form of payment does not affect whether a transaction is taxable to the seller's shareholders.

False

4

According to Section 338 of the U.S.tax code,a purchaser of 80% or more of the assets of the target may elect to treat the acquisition as if it were an acquisition of the target's assets for tax purposes.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

5

The sale of stock,rather than assets,is generally preferable to the target firm shareholders to avoid double taxation,if the target firm is structured as a limited liability company.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

6

Empirical studies generally show that the tax shelter resulting from the ability of the acquiring firm to increase the value of acquired assets to their FMV is a highly important motivating factor for a takeover.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

7

Taxes are an important consideration in almost any transaction,and they are often the primary motivation for an acquisition.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

8

A transaction is usually taxable to the target firm's shareholders,if the acquirer's stock is used to purchase at least 30% of the target firm's stock or assets.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

9

Purchase accounting affects only the cash flow of the combined firms but not the reported net income.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

10

It is seldom important that the buyer and seller agree on the allocation of the sales price among the assets being sold,since the allocation will determine the potential tax liability that would be incurred by the seller but that could by passed on to the buyer through to terms of the sales contract.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

11

As a general rule,a transaction is taxable to the target company shareholders if they receive the acquiring firm's stock and non-taxable if they receive cash.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

12

Taxable transactions usually involve the purchase of the target's voting stock,because the purchase of assets automatically will trigger a taxable gain for the target if the fair market value of the acquired assets exceeds the target firm's tax basis in the assets.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

13

From the viewpoint of the seller or target company shareholder,transactions may be tax-free or entirely or partially taxable.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

14

A transaction generally will be considered non-taxable to the seller or target firm's shareholder if it involves the purchase of the target's stock or assets for substantially all cash,notes,or some other nonequity consideration.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

15

In a cash purchase of assets.the target's shareholders could be taxed twice,once when the firm pays taxes on any gains and a second time when the proceeds from the sale are paid to the shareholders either as a dividend or distribution following liquidation of the corporation.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

16

The major advantages of using a triangular structure are limitations of the voting rights of acquiring shareholders and that the acquirer gains control of the target through a subsidiary without being directly responsible for the target's known and unknown liabilities.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

17

In a taxable purchase of target stock with cash,the target firm does not restate (i.e.,revalue)its assets and liabilities for tax purposes to reflect the amount that the acquirer paid for the shares of common stock.Rather,the tax basis (i.e.,their value on the target's financial statements)of assets and liabilities of the target before the acquisition carries over to the acquirer after the acquisition.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

18

The IRS generally views forward triangular cash mergers as a purchase of target stock followed by a liquidation of the target for which target shareholders will recognize a taxable gain or loss as if they had sold their shares.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

19

Under purchase price accounting,the excess of the purchase price paid over the book value of equity of the target firm is assigned only to the tangible assets up to their fair market value or to goodwill.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

20

Under purchase accounting,the difference between the combined firm's shareholders' equity immediately following closing and the acquiring firm's shareholders' equity equals the purchase price paid for the target firm.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

21

Nontaxable transactions also are called tax-free reorganizations.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

22

In a statutory merger,the buyer retains the target's tax attributes.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

23

Acquirers and targets planning to enter into a tax-free transaction seldom seek to get an advance ruling from the IRS to determine its tax-free status.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

24

In a purchase of assets,the buyer retains the target's tax attributes.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

25

Tax-free reorganizations require that substantially all of the consideration received by the target's shareholders be paid in cash.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

26

The tax-free structure is generally not suitable for the acquisition of a division within a corporation..

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

27

With the purchase of target stock,the acquirer retains the target's tax attributes,but there is no step up in the basis of the acquired assets unless the acquirer adopts a 338 election.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

28

If the transaction is tax-free,the acquiring company is able to transfer or carry over the target's tax basis to its own financial statements.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

29

In a reverse triangular merger,the acquirer retains the target's tax attributes.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

30

To demonstrate continuity of interests (COI),target shareholders must continue to own a substantial part of the value of the combined target and acquiring firms.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

31

Tax benefits that result from an acquisition should always be considered as among the most important justification for paying a very high premium for the target firm.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

32

In a forward triangular merger,the target firm's tax attributes in the form of any tax loss carry forwards or carrybacks or investment tax credits carry over to the acquirer because the target ceases to exist.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

33

A buyer may divest a significant portion of the acquired company immediately following closing without jeopardizing the tax-free status of the transaction.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

34

In a tax-free reorganization,the buyer is never required to get shareholder approval.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

35

Tax free reorganizations generally require that all or substantially all of the target company's assets or shares be acquired in order to ensure that the acquiring firm has a continuing ownership interest in the combined firms.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

36

Tax-free reorganizations generally require that all or substantially all of the target company's assets or shares be acquired.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

37

The IRS treats the reverse triangular cash merger as a purchase of target shares,with the target firm,including its assets,liabilities,and tax attributes,ceasing to exist.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

38

As a result of a 338 election,the IRS treats the purchase of target shares as a taxable purchase of assets which can be stepped up to fair market value.Only the buyer has to agree to the 338 election.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

39

If the acquirer invokes a 338 election no taxes will have to be paid on any gains on assets written up to their fair market value.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

40

Transactions may be partially taxable if the target shareholders receive some nonequity consideration,such as cash or debt,in addition to the acquirer's stock.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

41

The disadvantages of the forward triangular merger may include the requirement of the buyer to get shareholder approval.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

42

For tax purposes,goodwill created after July 1993 may be amortized up to 15 years and is tax deductible.Goodwill booked before July 1993 is also tax deductible.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

43

Asset sales by the target firm just prior to the transaction may threaten the tax-free status of the deal.Moreover,tax-free deals are disallowed within ten-years of a spin-off.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

44

So-called Morris Trust transactions tax code rules restrict how certain types of corporate deals can be structured to avoid taxes.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

45

A type C reorganization is a stock-for-assets reorganization with the requirement that at least 50% of the FMV of the target's assets,as well as the assumption of certain specified liabilities,are acquired solely in exchange for voting stock.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following is not true about mergers and acquisitions and taxes?

A) Tax considerations and strategies are likely to have an important impact on how a deal is structured by affecting the amount, timing, and composition of the price offered to a target firm.

B) None of the above

B) Tax factors are likely to affect how the combined firms are organized following closing, as the tax ramifications of a corporate structure are quite different from those of a limited liability company or partnership.

C) Potential tax savings are often the primary motivation for an acquisition or merger.

D) Transactions may be either partly or entirely taxable to the target firm's shareholders or tax-free.

A) Tax considerations and strategies are likely to have an important impact on how a deal is structured by affecting the amount, timing, and composition of the price offered to a target firm.

B) None of the above

B) Tax factors are likely to affect how the combined firms are organized following closing, as the tax ramifications of a corporate structure are quite different from those of a limited liability company or partnership.

C) Potential tax savings are often the primary motivation for an acquisition or merger.

D) Transactions may be either partly or entirely taxable to the target firm's shareholders or tax-free.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

47

The acquirer must be careful that not too large a proportion of the purchase price be composed of cash,because this might not meet the IRS's requirement for continuity of interests of the target shareholders and disqualify the transaction as a Type A reorganization.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

48

The Type C reorganization is used when it is essential for the acquirer not to assume any undisclosed liabilities.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

49

Goodwill no longer has to be amortized over its projected life,but it must be written off if it is deemed to have been impaired.Impairment reviews are to be taken annually or whenever the firm has experienced an event which materially affects the value of its assets.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

50

Although NOLs represent a potential source of value,their use must be monitored carefully to realize the full value resulting from the potential for deferring income taxes.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

51

To qualify for a 1031 exchange,the property must be an investment property or one that is used in a trade or business (e.g.,a warehouse,store,or commercial office building).

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

52

Type A reorganizations are generally viewed as the least flexible of the various types of tax-free reorganizations.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

53

Tax-free reorganizations require that substantially all of the consideration received by the target's shareholders be paid in common or preferred stock.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

54

In a type B stock-for-stock reorganization,the acquirer must purchase an amount of voting stock that comprises at least 50% of the voting power of all of the target's voting stock outstanding.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

55

To qualify for a Type A reorganization,the transaction must be either a merger or a consolidation.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

56

Since the IRS requires that target shareholders continue to hold a substantial equity interest in the acquiring company,the tax code defines what constitutes a substantial equity interest.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

57

Subchapter S Corporation shareholders,and LLC members,are taxed at their personal tax rates.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

58

A forward triangular merger is the most commonly used form of reorganization for tax-free stock acquisitions in which the form of payment is acquirer stock.It involves three parties: the acquiring firm,the target firm,and a shell subsidiary of the target firm.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

59

Triangular mergers are rarely used for tax-free transactions.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

60

A section of the U.S.tax code known as 1031 forbids investors to make a "like kind" exchange of investment properties.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following is not true of a taxable purchase of stock?

A) Taxable transactions usually involve the purchase of the target's voting stock with acquirer stock.

B) Taxable transactions usually involve the purchase of the target's voting stock, because the purchase of assets automatically will trigger a taxable gain for the target if the fair market value of the acquired assets exceeds the target firm's tax basis in the assets.

C) All stockholders are affected equally in a taxable purchase of assets.

D) The target firm does not pay any taxes on the transaction.

E) The effect of the tax liability will vary depending on the individual shareholder's tax basis.

A) Taxable transactions usually involve the purchase of the target's voting stock with acquirer stock.

B) Taxable transactions usually involve the purchase of the target's voting stock, because the purchase of assets automatically will trigger a taxable gain for the target if the fair market value of the acquired assets exceeds the target firm's tax basis in the assets.

C) All stockholders are affected equally in a taxable purchase of assets.

D) The target firm does not pay any taxes on the transaction.

E) The effect of the tax liability will vary depending on the individual shareholder's tax basis.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following are non-taxable transactions?

A) Statutory stock merger or consolidation

B) Stock for stock merger

C) Stock for assets merger

D) Triangular reverse stock merger

E) All of the above

A) Statutory stock merger or consolidation

B) Stock for stock merger

C) Stock for assets merger

D) Triangular reverse stock merger

E) All of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following represent taxable transactions?

A) Purchase of assets with cash

B) Purchase of stock with cash

C) Purchase of stock or assets with cash

D) Statutory cash merger or consolidation

E) All of the above

A) Purchase of assets with cash

B) Purchase of stock with cash

C) Purchase of stock or assets with cash

D) Statutory cash merger or consolidation

E) All of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is not true of taxable asset purchases?

A) Net operating losses carry over to the acquiring firm

B) The acquiring firm may step up its basis in the acquired assets.

C) The target firm is subject to recapture of tax credits and excess depreciation

D) Target firm shareholders' are subject to a potential immediate tax liability

E) Target firm net operating losses and tax credits cannot be transferred to the acquiring firm

A) Net operating losses carry over to the acquiring firm

B) The acquiring firm may step up its basis in the acquired assets.

C) The target firm is subject to recapture of tax credits and excess depreciation

D) Target firm shareholders' are subject to a potential immediate tax liability

E) Target firm net operating losses and tax credits cannot be transferred to the acquiring firm

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

65

Which one of the following statements is true?

A) Target firm shareholders may accept cash or acquirer stock in exchange for their shares for the transaction to be considered tax free

B) To be tax free, the target firm shareholders must receive acquirer firm shares for all of the target firm's shares outstanding

C) At least one-half of the assets of the target firm are recorded on the balance sheet of the acquirer at their book rather than market value in a tax free transaction

D) If the assets of a firm are written up to fair market value as part of the transaction, the increase in value is considered a taxable gain

E) Target firm shareholders are required by law to pay taxes on any writeup of the firm's assets to fair market value

A) Target firm shareholders may accept cash or acquirer stock in exchange for their shares for the transaction to be considered tax free

B) To be tax free, the target firm shareholders must receive acquirer firm shares for all of the target firm's shares outstanding

C) At least one-half of the assets of the target firm are recorded on the balance sheet of the acquirer at their book rather than market value in a tax free transaction

D) If the assets of a firm are written up to fair market value as part of the transaction, the increase in value is considered a taxable gain

E) Target firm shareholders are required by law to pay taxes on any writeup of the firm's assets to fair market value

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following is not true about goodwill ?

A) Goodwill must be written off over 20 years.

B) Goodwill must be checked for impairment at least annually.

C) The loss of key customers could impair the value of goodwill.

D) Goodwill does not have to be amortized.

E) Goodwill is shown as an asset on the balance sheet.

A) Goodwill must be written off over 20 years.

B) Goodwill must be checked for impairment at least annually.

C) The loss of key customers could impair the value of goodwill.

D) Goodwill does not have to be amortized.

E) Goodwill is shown as an asset on the balance sheet.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

67

For financial reporting purposes,goodwill resulting from an acquisition

A) Must equal the fair market value of the target firm's assets

B) Immediately impacts the acquirer's profits

C) Is expensed over 20 years

D) Is reviewed annually or whenever there is reason to believe it has lost value and amortized to the extent its value has declined

E) Never affects the profits of the acquirer

A) Must equal the fair market value of the target firm's assets

B) Immediately impacts the acquirer's profits

C) Is expensed over 20 years

D) Is reviewed annually or whenever there is reason to believe it has lost value and amortized to the extent its value has declined

E) Never affects the profits of the acquirer

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

68

Case Study Short Essay Examination Questions

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently. Concluding Comments

In reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

Do you agree with the argument that the courts should focus on the form or structure of an agreement and not try to interpret the actual intent of the parties to the transaction? Explain your answer.

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently.

Concluding CommentsIn reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

Do you agree with the argument that the courts should focus on the form or structure of an agreement and not try to interpret the actual intent of the parties to the transaction? Explain your answer.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

69

Which of the following are not true of net operating loss carrybacks and carryforwards?

A) Net operating loss carrybacks enable firms to recover previous taxes paid.

B) Net operating loss carryforwards enable firms to shelter future taxable income.

C) Net operating loss carryforwards may be applied to income up to 5 years into the future..

D) Loss corporations" cannot use a net operating loss carry forward unless they remain viable and in essentially the same business for at least 2 years following the closing of the acquisition.

E) None of the above

A) Net operating loss carrybacks enable firms to recover previous taxes paid.

B) Net operating loss carryforwards enable firms to shelter future taxable income.

C) Net operating loss carryforwards may be applied to income up to 5 years into the future..

D) Loss corporations" cannot use a net operating loss carry forward unless they remain viable and in essentially the same business for at least 2 years following the closing of the acquisition.

E) None of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

70

The tax status of the transaction may influence the purchase price by

A) Raising the price demanded by the seller to offset potential tax liabilities

B) Reducing the price demanded by the seller to offset potential tax liabilities

C) Causing the buyer to reduce the purchase price if the transaction is taxable to the target firm's shareholders

D) Forcing the seller to agree to defer a portion of the purchase price

E) Forcing the buyer to agree to defer a portion of the purchase price

A) Raising the price demanded by the seller to offset potential tax liabilities

B) Reducing the price demanded by the seller to offset potential tax liabilities

C) Causing the buyer to reduce the purchase price if the transaction is taxable to the target firm's shareholders

D) Forcing the seller to agree to defer a portion of the purchase price

E) Forcing the buyer to agree to defer a portion of the purchase price

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following is not considered a tax-free reorganization?

A) Type A transactions

B) Type B transactions

C) Type C Transactions

D) Forward triangular merger

E) Cash purchase of assets

A) Type A transactions

B) Type B transactions

C) Type C Transactions

D) Forward triangular merger

E) Cash purchase of assets

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is not true of a 338 election ?

A) It applies to asset purchases only.

B) It applies to stock purchases only.

C) It allows a purchase of stock to be treated as an asset purchase for tax purposes.

D) The buyer must adopt the 338 election.

E) The seller must agree with the adoption of the 338 election.

A) It applies to asset purchases only.

B) It applies to stock purchases only.

C) It allows a purchase of stock to be treated as an asset purchase for tax purposes.

D) The buyer must adopt the 338 election.

E) The seller must agree with the adoption of the 338 election.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following is not true of a forward triangular cash merger?

A) It is considered by the IRS as a purchase of target assets.

B) It is generally followed by a liquidation of the target firm.

C) Target shareholders must recognize a gain or loss as if they had sold their shares.

D) The target's tax attributes carry over to the buyer.

E) Taxes are paid by the target firm on any gain on the sale of its assets and again by shareholders who receive a liquidating dividend.

A) It is considered by the IRS as a purchase of target assets.

B) It is generally followed by a liquidation of the target firm.

C) Target shareholders must recognize a gain or loss as if they had sold their shares.

D) The target's tax attributes carry over to the buyer.

E) Taxes are paid by the target firm on any gain on the sale of its assets and again by shareholders who receive a liquidating dividend.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following are required for an acquisition to be considered tax-free?

A) Continuity of interest

B) A legitimate business purpose other than tax avoidance

C) The use of predominately acquirer shares to buy the target's shares

D) An all cash acquisition of the target firm's shares

E) A, B, and C only

A) Continuity of interest

B) A legitimate business purpose other than tax avoidance

C) The use of predominately acquirer shares to buy the target's shares

D) An all cash acquisition of the target firm's shares

E) A, B, and C only

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

75

Purchase accounting requires that

A) The excess amount paid for the target firm be recorded as an intangible asset on the books of the acquirer and immediately written off

B) Target firm assets must be recorded on the acquirer's balance sheet at their fair market value

C) The excess of the purchase price of the purchase price of the target firm must be recorded as asset and expensed over a period of 10 years

D) Goodwill once established is never written off

E) Target firm liabilities are recorded on the balance sheet of the acquirer at their book value

A) The excess amount paid for the target firm be recorded as an intangible asset on the books of the acquirer and immediately written off

B) Target firm assets must be recorded on the acquirer's balance sheet at their fair market value

C) The excess of the purchase price of the purchase price of the target firm must be recorded as asset and expensed over a period of 10 years

D) Goodwill once established is never written off

E) Target firm liabilities are recorded on the balance sheet of the acquirer at their book value

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

76

Which of the following is true about purchase accounting?

A) Cash and accounts receivable, reduced for bad debt and returns, are valued at their values on the books of the target before the acquisition..

B) Marketable securities are valued at their realizable value after transactions costs.

C) Property, plant and equipment are valued at fair market value.

D) Intangible assets are booked at their appraised values.

E) All of the above.

A) Cash and accounts receivable, reduced for bad debt and returns, are valued at their values on the books of the target before the acquisition..

B) Marketable securities are valued at their realizable value after transactions costs.

C) Property, plant and equipment are valued at fair market value.

D) Intangible assets are booked at their appraised values.

E) All of the above.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

77

Which of the following is not true about purchase accounting?

A) For financial reporting purposes, all M&As must be recorded using the purchase method of accounting.

B) Under the purchase method of accounting, the excess of the purchase price over the target's net asset value is treated as goodwill on the combined firm's balance sheet.

C) Goodwill may be amortized up to 40 years.

D) If the fair value of the target's net assets later falls below its carrying value, the acquirer must record a loss equal to the difference.

E) None of the above

A) For financial reporting purposes, all M&As must be recorded using the purchase method of accounting.

B) Under the purchase method of accounting, the excess of the purchase price over the target's net asset value is treated as goodwill on the combined firm's balance sheet.

C) Goodwill may be amortized up to 40 years.

D) If the fair value of the target's net assets later falls below its carrying value, the acquirer must record a loss equal to the difference.

E) None of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

78

Case Study Short Essay Examination Questions

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently. Concluding Comments

In reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.

How might allowing the form of a transaction to override the actual spirit or intent of the deal impact the cost of doing business for the parties involved in the distribution agreement? Be specific.

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009 transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company ("Merck") and Schering-Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering-Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms. Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent, respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs under development at Schering-Plough. Furthermore, the deal increases Merck's international presence, since 70 percent of Schering-Plough's revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries . In reality, Merck acquired Schering-Plough.

Former shareholders of Schering-Plough and Merck become shareholders in the new Merck. The "New Merck" is simply Schering-Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering-Plough's 2008 revenues and about 70 percent of the firm's international revenues. Consequently, retaining these revenues following the merger was important to both Merck and Schering-Plough.

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these actions occur concurrently.

Concluding CommentsIn reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck's chairman and CEO, will run the newly combined firm when Fred Hassan, Schering-Plough's CEO, steps down. The new firm has been renamed Merck to reflect its broader brand recognition. Three-fourths of the new firm's board consists of former Merck directors, with the remainder coming from Schering-Plough's board. These factors would give Merck effective control of the combined Merck and Schering-Plough operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011. Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell Remicade overseas but providing for more royalties to J&J.