Deck 11: Understanding Financing and Payout Decisions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

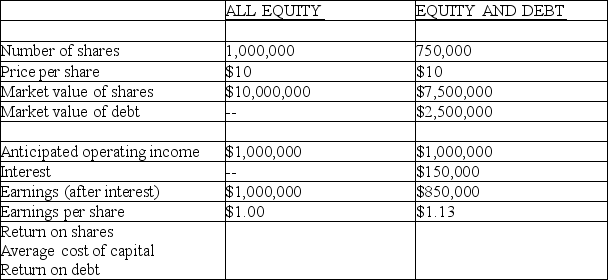

Use the information for Silicon Solutions found in Figure 11.1 and assume perfect capital markets (PCM)to determine the average cost of capital for the unlevered firm.Then determine the return on shares,the return on debt,and the average cost of capital for the levered firm.What do you think will happen to the return on equity,return on debt,and the average cost of capital for the levered firm if the ratio of debt to equity is increased?

Silicon Solutions pays all of its operating income to shareholders as a dividend,which represents the return to the shareholders.Estimates for the firm's operating income next year,and in all subsequent years,is anticipated to be $1.0 million.Note that this is not a guaranteed amount,but simply the best guess of what the operating income will be.Because the firm does not expect the operating income to grow,and because all operating income is paid in dividends,the return to all shareholders will be the dividend yield they receive: $1.0 million relative to the $10 million market value of equity.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/71

Play

Full screen (f)

Deck 11: Understanding Financing and Payout Decisions

1

A firm's capital structure combines all forms of financing on which the firm relies including:

A)preferred shares.

B)common equity.

C)long-term debt.

D)All of the above.

A)preferred shares.

B)common equity.

C)long-term debt.

D)All of the above.

D

2

A firm's capital structure combines all forms of long-term financing on which the firm relies EXCEPT:

A)long-term debt.

B)common equity.

C)inventory.

D)preferred shares.

A)long-term debt.

B)common equity.

C)inventory.

D)preferred shares.

C

3

Modigliani and Miller (M&M)Proposition II states:

A)the cost of equity does not change when a firm takes on a greater proportion of debt.

B)the cost of equity increases when a firm takes on a greater proportion of debt.

C)the cost of debt increases when a firm takes on a greater proportion of equity.

D)the cost of equity decreases when a firm takes on a greater proportion of debt.

A)the cost of equity does not change when a firm takes on a greater proportion of debt.

B)the cost of equity increases when a firm takes on a greater proportion of debt.

C)the cost of debt increases when a firm takes on a greater proportion of equity.

D)the cost of equity decreases when a firm takes on a greater proportion of debt.

B

4

Flyover Airlines Inc.has a cost of equity equal to 24.67%.If the firm is financed with 40% debt and 60% equity and has an average cost of capital of 18%,what is the cost of debt? Assume perfect capital markets.

A)8.00%

B)6.67%

C)10.00%

D)12.33%

A)8.00%

B)6.67%

C)10.00%

D)12.33%

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is NOT one of M&M's perfect capital market assumptions?

A)Bankruptcy is costless.

B)Shareholders have more information than bondholders.

C)Individuals and firms can borrow and lend at the same rates.

D)There are no taxes.

A)Bankruptcy is costless.

B)Shareholders have more information than bondholders.

C)Individuals and firms can borrow and lend at the same rates.

D)There are no taxes.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

6

According to data assembled for U.S.firms,the average level of debt as a percentage of capital is approximately equal across industries.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

7

Capital structure is important,but it CANNOT impact the overall value of a firm.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

8

Spectronix Inc.operates in a world of perfect capital markets,has no debt,and has a required rate of return on equity of 10%.An executive manager has suggested that borrowing money to buy back outstanding stock is a good idea because it would replace equity financing with less expensive debt financing,thus increasing the value of the firm.Assume the firm issues new debt with a required return of of 5% to repurchase 30% of the outstanding stock.What is the cost of equity at the conclusion of this transaction?

A)21.67%

B)12.14%

C)16.43%

D)45.00%

A)21.67%

B)12.14%

C)16.43%

D)45.00%

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

9

________ refers to the difficulties experienced by firms as they attempt to meet financial commitments to their creditors.

A)Financial distress

B)Capital structure

C)Capital budgeting

D)Working capital management

A)Financial distress

B)Capital structure

C)Capital budgeting

D)Working capital management

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

10

PrintQuik Inc.has a cost of equity of 14% and a cost of debt of 6%.If the firm is financed with 70% equity and 30% debt,and they operate under the conditions of a perfect capital market,what is the firm's average cost of capital?

A)9.80%

B)10.50%

C)11.60%

D)10.00%

A)9.80%

B)10.50%

C)11.60%

D)10.00%

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

11

According to a recent study,CFOs estimated they were able to add about THIRTY percent of the overall value of the firm through financial management.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

12

A leveraged buyout (LBO)is when we tend to find firms at their lowest debt levels.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

13

Capital budgeting is the mix of debt and common equity (as well as preferred equity)of a firm.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

14

A firm's risk level will fluctuate as its ________ changes.

A)financial leverage

B)debt-to-equity

C)degree of financial leverage

D)All of the above.

A)financial leverage

B)debt-to-equity

C)degree of financial leverage

D)All of the above.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

15

Modigliani and Miller each won a Nobel prize in economics in at least in part because of their work with capital structure.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is NOT a reason why banks are more willing to lend to some firms than to others?

A)Banks prefer to lend to firms with more stable cash flows.

B)Banks prefer to lend to firms with more physical as opposed to intellectual assets.

C)Banks prefer to lend to firms that remain in a specific geographical region.

D)All of the above are preferences for banks.

A)Banks prefer to lend to firms with more stable cash flows.

B)Banks prefer to lend to firms with more physical as opposed to intellectual assets.

C)Banks prefer to lend to firms that remain in a specific geographical region.

D)All of the above are preferences for banks.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is NOT one of M&M's perfect capital market assumptions?

A)No taxes

B)Individuals can borrow or lend at the same rate

C)Every party has equal access to information

D)Bankruptcy costs are reasonably low

A)No taxes

B)Individuals can borrow or lend at the same rate

C)Every party has equal access to information

D)Bankruptcy costs are reasonably low

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

18

In M&M Proposition II the cost of equity changes with changes in the amount of debt financing.Which of the following is the correct formula for Proposition II?

A)Ke = Ku + (Ku - Kd)/ ( )

B)Ke = Ku + (Ku - Kd)( )

C)Ke = Ku + (Ku + Kd)( )

D)Ke = Ku + (Ku + Kd)/ ( )

A)Ke = Ku + (Ku - Kd)/ ( )

B)Ke = Ku + (Ku - Kd)( )

C)Ke = Ku + (Ku + Kd)( )

D)Ke = Ku + (Ku + Kd)/ ( )

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

19

Modigliani and Miller (M&M)Proposition I states:

A)overall market value of the firm = market value of equity - market value of debt.

B)overall market value of equity = market value of the firm+ market value of debt.

C)overall market value of the firm = market value of equity + market value of debt.

D)overall market value of debt = market value of equity + market value of the firm.

A)overall market value of the firm = market value of equity - market value of debt.

B)overall market value of equity = market value of the firm+ market value of debt.

C)overall market value of the firm = market value of equity + market value of debt.

D)overall market value of debt = market value of equity + market value of the firm.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

20

Under conditions of perfect capital markets,M&M suggest that the average cost of capital for the firm will ________ with the ________ of debt.

A)decrease; addition

B)remain the same; addition

C)increase; reduction

D)increase; addition

A)decrease; addition

B)remain the same; addition

C)increase; reduction

D)increase; addition

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

21

-What is the combined debt and equity income (interest plus earnings after tax)for the Equity and Debt firm?

A)$700,000

B)$760,000

C)$560,000

D)$300,000

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements is NOT correct? Under conditions of perfect capital markets:

A)investors do not pay taxes,but firms do.

B)firms do not pay taxes,but investors do.

C)capital structure matters because it can change the value of the firm.

D)capital structure does not matter because it cannot change the value of the firm.

A)investors do not pay taxes,but firms do.

B)firms do not pay taxes,but investors do.

C)capital structure matters because it can change the value of the firm.

D)capital structure does not matter because it cannot change the value of the firm.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

23

Under conditions of perfect capital markets,M&M insist that the value of the levered firm is greater than the value of the unlevered firm.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

24

The major real-world benefit of debt is that interest payments are:

A)made after tax considerations.

B)a tax-deductible expense.

C)always less than 10% of the firm's profit.

D)smaller than the dividend payments.

A)made after tax considerations.

B)a tax-deductible expense.

C)always less than 10% of the firm's profit.

D)smaller than the dividend payments.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

25

Under terms of the U.S.federal bankruptcy code,chapter ________ call for a ________ procedure.

A)7; reorganization

B)11; liquidation

C)11; reorganization

D)None of the above

A)7; reorganization

B)11; liquidation

C)11; reorganization

D)None of the above

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

26

Due primarily to concerns about financial distress,we tend to see very few firms financed with ________ or more of their capital structure as debt.

A)20%

B)35%

C)55%

D)70%

A)20%

B)35%

C)55%

D)70%

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

27

-The interest tax shield is equal to:

A)$0

B)(EBIT - I )* (1-the tax rate).

C)(equity + debt)* (1-the tax rate)

D)the tax rate multiplied by the amount of interest.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following is NOT one of M&M's perfect capital market assumptions?

A)There are no taxes.

B)Individuals must borrow (or lend)at the same rate at which a firm can borrow.

C)There is no asymmetric information in the market place.

D)There are no costs of bankruptcy.

A)There are no taxes.

B)Individuals must borrow (or lend)at the same rate at which a firm can borrow.

C)There is no asymmetric information in the market place.

D)There are no costs of bankruptcy.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

29

Modigliani and Miller (M&M)proposed a model in which,given certain restrictive assumptions,the capital structure of a firm does not impact the value of the firm.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

30

-In a world with taxes,M&M's second proposition defines the expected return on equity as:

A)Ke = Ku + (Ku - Kd)(1 - t)( )

B)Ke = Ku + (Ku + Kd)(1 - t)( )

C)Ke = Ku + (Ku - Kd)(1 + t)( )

D)Ke = Ku - (Ku - Kd)(1 - t)( )

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

31

The beauty of the Modigliani and Miller model is that if you relax the restrictive assumptions,it still demonstrates that capital structure does not impact the value of the firm.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

32

Under conditions of perfect capital markets,M&M suggest that the average cost of capital for the firm will increase with the addition of debt.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

33

Use the information for Silicon Solutions found in Figure 11.1 and assume perfect capital markets (PCM)to determine the average cost of capital for the unlevered firm.Then determine the return on shares,the return on debt,and the average cost of capital for the levered firm.What do you think will happen to the return on equity,return on debt,and the average cost of capital for the levered firm if the ratio of debt to equity is increased?

Silicon Solutions pays all of its operating income to shareholders as a dividend,which represents the return to the shareholders.Estimates for the firm's operating income next year,and in all subsequent years,is anticipated to be $1.0 million.Note that this is not a guaranteed amount,but simply the best guess of what the operating income will be.Because the firm does not expect the operating income to grow,and because all operating income is paid in dividends,the return to all shareholders will be the dividend yield they receive: $1.0 million relative to the $10 million market value of equity.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

34

Assume an M&M world with taxes where the corporate tax rate is 25%,the before tax required return on debt is 8%,the required return on the unlevered firm is 12%,and the firm is financed 20% with debt and 80% with equity.What is the required return on equity?

A)12.75%

B)15.00%

C)13.25%

D)11.25%

A)12.75%

B)15.00%

C)13.25%

D)11.25%

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

35

According to Modigliani and Miller (M&M),in a world of perfect capital markets,what will be the expected equity return (or cost of equity)for a firm that has a cost of capital of 14 percent,a cost of debt of 8 percent,debt valued at $3.0 million,and equity valued at $4.0 million? What would happen to the cost of equity as the amount of debt increased? What would happen to the cost of debt if the amount of debt was increased?

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

36

-What are taxes payable for the Equity and Debt firm?

A)$240,000

B)$560,000

C)$300,000

D)$0

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

37

-In an M&M world with taxes,as a firm takes on ________ debt,the cost of equity ________.

A)more; decreases.

B)more; increases.

C)less; increases.

D)less; remains the same.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

38

-What are the Earnings after tax for the Equity and Debt firm?

A)$240,000

B)$300,000

C)$560,000

D)$0

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

39

-In the Modigliani and Miller world where we now assume that taxes exist,and that interest payments are tax deductible for firms,then which of the following statements is true?

A)VL = VU - Dt

B)VU = VL + Dt

C)VL = VU + Dt

D)VU = VL - Dt

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

40

________ describes a legal state whereby a firm cannot pay its creditors

A)Capital distress

B)Bankruptcy

C)Liquification

D)Capital structure

A)Capital distress

B)Bankruptcy

C)Liquification

D)Capital structure

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

41

Which type of firm described is likely to have a high dividend payout ratio policy?

A)A younger firm with uncertain income but significant growth opportunities.

B)An older firm with steady earnings but few growth opportunities..

C)An older firm with irregular income and significant growth opportunities.

D)A younger firm with significant income and super normal positive growth opportunities.

A)A younger firm with uncertain income but significant growth opportunities.

B)An older firm with steady earnings but few growth opportunities..

C)An older firm with irregular income and significant growth opportunities.

D)A younger firm with significant income and super normal positive growth opportunities.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

42

Under U.S.Bankruptcy code,claims against the firm are prioritized along the lines of secured creditors followed in order by:

A)preferred stock holders,common stock holders,and then unsecured creditors after all others have been compensated.

B)unsecured creditors,preferred stock holders,and then common stock holders after all others have been compensated.

C)preferred stock holders,unsecured creditors,and then common stock holders after all others have been compensated.

D)common stock holders,preferred stock holders,and then unsecured creditors after all others have been compensated.

A)preferred stock holders,common stock holders,and then unsecured creditors after all others have been compensated.

B)unsecured creditors,preferred stock holders,and then common stock holders after all others have been compensated.

C)preferred stock holders,unsecured creditors,and then common stock holders after all others have been compensated.

D)common stock holders,preferred stock holders,and then unsecured creditors after all others have been compensated.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

43

In a world of both personal and corporate taxes,individual investors may not be able to get the full advantage of debt by borrowing personally.Corporate borrowing rates,personal borrowing rates,and tax rates may differ.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following statements is most accurate in the M&M world including taxes and financial distress?

A)Overall market value of the firm = market value of all-equity firm - value of interest tax shield - costs of financial distress

B)Overall market value of the firm = market value of all-equity firm + value of interest tax shield - costs of financial distress

C)Overall market value of the firm = market value of all-equity firm - value of interest tax shield + costs of financial distress

D)Overall market value of the firm = market value of all-equity firm + value of interest tax shield + costs of financial distress

A)Overall market value of the firm = market value of all-equity firm - value of interest tax shield - costs of financial distress

B)Overall market value of the firm = market value of all-equity firm + value of interest tax shield - costs of financial distress

C)Overall market value of the firm = market value of all-equity firm - value of interest tax shield + costs of financial distress

D)Overall market value of the firm = market value of all-equity firm + value of interest tax shield + costs of financial distress

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

45

Under conditions of asymmetric information,when a firm issues debt this is more likely to be a negative signal,rather than a positive signal regarding the firm's future prospects.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

46

As we waive the conditions of perfect capital markets and include taxes,M&M suggest that the average cost of capital for the firm will remain unchanged with the addition of debt.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

47

The major real-world benefit of debt is that interest payments are a tax-deductible expense.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

48

We can interpret the optimal level of debt as the firm's ________,or the highest amount the firm can borrow before the value of the firm begins to decline.

A)equity capacity

B)equity multiplier

C)debt capacity

D)interest tax shield

A)equity capacity

B)equity multiplier

C)debt capacity

D)interest tax shield

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

49

The pecking-order model of capital structure suggests the order in which firms prefer to raise capital is:

A)debt,then retained earnings,then external equity.

B)retained earnings,then debt,then external equity.

C)preferred stock,then debt,then external equity.

D)debt,then external equity,then retained earnings.

A)debt,then retained earnings,then external equity.

B)retained earnings,then debt,then external equity.

C)preferred stock,then debt,then external equity.

D)debt,then external equity,then retained earnings.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

50

According to Modigliani and Miller (M&M),in a world of perfect capital markets,except that interest on debt is tax deductible,what will be the expected equity return (or cost of equity)for a firm that has a cost of capital of 14 percent,a cost of debt of 8 percent,a tax rate of 30%,debt valued at $3.0 million,and equity valued at $4.0 million? What would happen to the cost of equity as the amount of debt increased? What would happen to the cost of debt if the amount of debt was increased?

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

51

Your author identifies the ________ model of capital structure as one that describes the order in which firms typically raise capital.

A)step

B)internal-external

C)queuing

D)pecking-order

A)step

B)internal-external

C)queuing

D)pecking-order

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

52

A publicly traded firm just announced that its issuing debt to finance a new project.Which of the following scenarios is most likely true in a market with asymmetric information?

A)The firm's future prospects look good and they are sending a costly signal that indicates they will be able to meet higher debt obligations.

B)The firm has a questionable project and are attempting to increase the attractiveness of the project by raising the WACC via an increase in the level of debt financing.

C)The firm has a poor project but they know debt financing provides an effective tax shield.

D)None of these signals are viable explanations.

A)The firm's future prospects look good and they are sending a costly signal that indicates they will be able to meet higher debt obligations.

B)The firm has a questionable project and are attempting to increase the attractiveness of the project by raising the WACC via an increase in the level of debt financing.

C)The firm has a poor project but they know debt financing provides an effective tax shield.

D)None of these signals are viable explanations.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

53

According to data presented by the author,corporate tax rates in the United States are among the lowest across major economies.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

54

The interest tax shield represents the value of the reduction in taxes that results from allowable deductions from taxable income.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

55

Longneck Brewery Inc.has net income of $3.00 per share and a dividend payout ratio of 35%.How large is the firm's per share dividend payment?

A)$1.05

B)$1.95

C)$1.50

D)$0.35

A)$1.05

B)$1.95

C)$1.50

D)$0.35

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

56

Direct forms of bankruptcy costs include legal and administrative costs associated with the actual bankruptcy proceedings,as well as the money paid to lawyers.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

57

-The combined debt plus equity income is equal to the equity income + (Interest * the tax rate).

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

58

Assume perfect capital markets except that taxes DO exist.Why does the value of the interest tax shield accrue entirely to the shareholders and none of the value goes to the bondholders?

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

59

When two groups have different access to information,there is then symmetric information for these two groups.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

60

Under terms of the U.S.federal bankruptcy code,chapter ________ call for a ________ pr.

A)11; liquidation

B)7; reorganization

C)7; liquidation

D)None of the above

A)11; liquidation

B)7; reorganization

C)7; liquidation

D)None of the above

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following is NOT generally considered to be a dividend clientele?

A)Clients who are middle-aged and just entering the market.

B)Clients in low tax brackets who desire high dividends.

C)Clients in high tax brackets who desire low or no dividends.

D)Clients who prefer high and reliable streams of investment cash flow.

A)Clients who are middle-aged and just entering the market.

B)Clients in low tax brackets who desire high dividends.

C)Clients in high tax brackets who desire low or no dividends.

D)Clients who prefer high and reliable streams of investment cash flow.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

62

________ occurs when a firm buys back some of its own common shares.

A)A leveraged buyout

B)An IPO

C)A share repurchase

D)Secondary offering

A)A leveraged buyout

B)An IPO

C)A share repurchase

D)Secondary offering

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

63

Dividend payments and share repurchases are conceptually equivalent.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

64

Miller and Modigliani also studied dividend policy and determined that in their world of perfect capital markets (no taxes,no bankruptcy costs,no asymmetric information)that dividend policy DOES matter.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

65

The author cites a global study by Servaes and Tufano from 2006 which shows ________ as the dividend policy preferred by the vast majority (76%)of the firms surveyed.

A)a specific percentage amount

B)a specific target amount

C)a specific growth amount

D)no specific policy

A)a specific percentage amount

B)a specific target amount

C)a specific growth amount

D)no specific policy

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following statements regarding a share repurchase is NOT true?

A)Share repurchases occur most commonly as open market repurchases.

B)The firm typically buys its shares just like any investor would purchase stocks listed on a stock exchange.

C)A firm often announces its intention to repurchase a certain number of its shares,say over the upcoming year.

D)In most cases,a firm may agree to repurchase shares from a major shareholder at a negotiated price.

A)Share repurchases occur most commonly as open market repurchases.

B)The firm typically buys its shares just like any investor would purchase stocks listed on a stock exchange.

C)A firm often announces its intention to repurchase a certain number of its shares,say over the upcoming year.

D)In most cases,a firm may agree to repurchase shares from a major shareholder at a negotiated price.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

67

In what manner are share repurchases and dividend payments related to each other? Why would a firm choose to engage in a share repurchase?

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

68

All else equal,an individual investor would prefer ________ even if rates on both are equal,since ________ can be deferred.

A)dividends to capital gains; dividends

B)dividends to capital gains; capital gains

C)capital gains to dividends; capital gains

D)Investors are indifferent to capital gains vs dividends.

A)dividends to capital gains; dividends

B)dividends to capital gains; capital gains

C)capital gains to dividends; capital gains

D)Investors are indifferent to capital gains vs dividends.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

69

Dividend policy can be interpreted as either (1)the cash amount of dividends a firm decides to pay to its shareholders or (2)the percentage of earnings the firm decides to pay as dividends,also known as the dividend payout ratio.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

70

When a firm is young and growing,managers tend to have high dividend payout ratios in an attempt to encourage investors to buy the stock.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

71

The majority of firms view cutting dividends as a way to send a POSITIVE signal to the market as an indication that they have increased opportunities to invest earnings.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 71 flashcards in this deck.