Deck 13: Investments

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

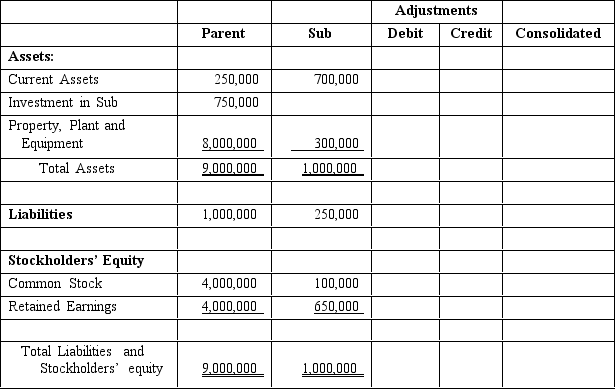

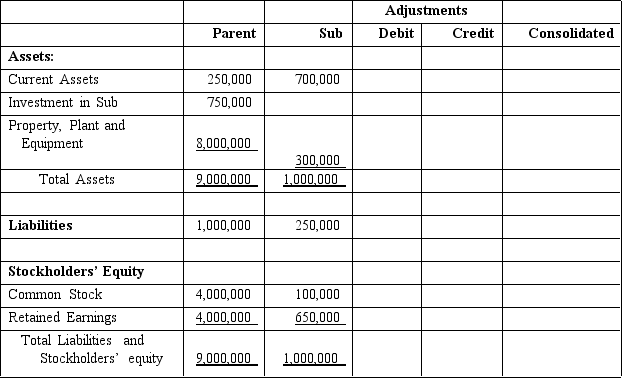

On January 1, 2012, Parent, Inc., purchased 80% of the outstanding common stock of Sub Corporation for $750,000. Since Parent has control over Sub, a consolidated balance sheet must be prepared from the individual balance sheets of both companies. Complete the following worksheet to prepare the consolidated balance sheet on January 1, 2012.

Question

Question

Trattoria, Inc. engaged in the following investment transactions during 2013:

At December 31, 2013, the market value of Tarbet's stock was $54.

At December 31, 2013, the market value of Tarbet's stock was $54.

At December 31, 2013, the market value of Tarbet's stock was $54. Question

Question

Question

Tail Winds Corporation acquired the following equity securities during 2013:

The company's investment in these two companies is passive and classified as available-for-sale. During 2013, TICO paid a dividend of $1.10 per share and Thankful paid a dividend of $1.75 per share. At December 31, 2013, the market value of these securities was $79 per share for TICO and $23 per share for Thankful.

The company's investment in these two companies is passive and classified as available-for-sale. During 2013, TICO paid a dividend of $1.10 per share and Thankful paid a dividend of $1.75 per share. At December 31, 2013, the market value of these securities was $79 per share for TICO and $23 per share for Thankful.

The company's investment in these two companies is passive and classified as available-for-sale. During 2013, TICO paid a dividend of $1.10 per share and Thankful paid a dividend of $1.75 per share. At December 31, 2013, the market value of these securities was $79 per share for TICO and $23 per share for Thankful. Question

Question

Tidewater Management, Inc. had no investments in short-term marketable securities prior to 2013. During 2013, the company engaged in the following investment transactions:

At the end of 2013, the Toucan Taxi stock had a market value of $15 per share.

At the end of 2013, the Toucan Taxi stock had a market value of $15 per share.

At the end of 2013, the Toucan Taxi stock had a market value of $15 per share. Question

On January 1, 2012, Parent, Inc., purchases all the outstanding common stock of Sub Corporation for $750,000. Since Parent has control over Sub, a consolidated balance sheet must be prepared from the individual balance sheets of both companies. Complete the following worksheet to prepare the consolidated balance sheet on January 1, 2012.

Question

Thomkin Enterprises purchased several investment securities on November 1, 2013. Various transactions and market activities occurred regarding these investments between acquisition and December 31st (the company's year-end), as shown below:

Additional information:

Additional information:

Prepare journal entries to record the purchase of the securities, the receipt of dividends and interest, the sale of the TRL stock, and the end-of-year mark-to-market adjustments. For the end-of-year entries, indicate how the resulting gains or losses should be recognized in Thomkin's year-end financial statements.

Prepare journal entries to record the purchase of the securities, the receipt of dividends and interest, the sale of the TRL stock, and the end-of-year mark-to-market adjustments. For the end-of-year entries, indicate how the resulting gains or losses should be recognized in Thomkin's year-end financial statements.

Additional information: Prepare journal entries to record the purchase of the securities, the receipt of dividends and interest, the sale of the TRL stock, and the end-of-year mark-to-market adjustments. For the end-of-year entries, indicate how the resulting gains or losses should be recognized in Thomkin's year-end financial statements. Question

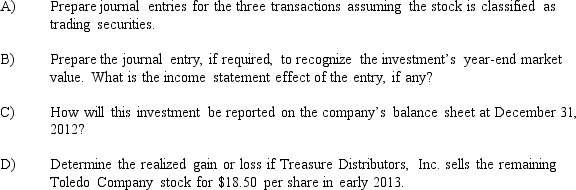

Treasure Distributors, Inc. had no investments in short-term marketable securities prior to 2012. During 2012, the company engaged in the following investment transactions:

At the end of 2012, the Toledo Company stock had a market value of $18 per share.

At the end of 2012, the Toledo Company stock had a market value of $18 per share.

At the end of 2012, the Toledo Company stock had a market value of $18 per share. Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/73

Play

Full screen (f)

Deck 13: Investments

1

The excess of acquisition cost over the current value of the investee's identifiable net assets, referred to as goodwill, may not be recorded by the investor under current generally accepted accounting principles.

False

2

____________________ securities, such as bonds, exist when another entity owes the security holder some combination of principal and interest.

Debt

3

If the investor holds enough common stock to control the investee (50% or more common stock ownership), then the two corporations are no longer separate accounting entities and therefore they no longer may maintain separate accounting records.

False

4

____________________ securities are debt investments that are accounted for on an amortized cost basis because management intends to hold the investment until the debt contract requires the borrower to completely repay the debt.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

5

Securities issued by a corporation as a form of ownership in the business, such as common stock and preferred stock, are called equity securities.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

6

A purchased company must be recorded at the value of the cash and other consideration given by the acquiring company.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

7

____________________ securities are equity or debt investments that are bought and sold frequently and are typically owned for less than one month.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

8

If the investor owns over 50% of the outstanding common stock, the investor is deemed to have control over the operating and financial policies of the investee.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

9

The equity method of accounting is used if the investor owns between 20-50% of another company and the investor is able to exert influence over the other company.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

10

An advantage of the equity method over the fair value method is that it prevents an investor from manipulating its own income by exerting influence over the amount and timing of investee dividends.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

11

The fair value method should be used to account for stock investments of less than 20% of the outstanding shares.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

12

When an investor is able to exert significant influence over another company, the ____________________ method of accounting is used for the investment.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

13

If the parent owns 90% of the subsidiary's stock, then 90% of the subsidiary's assets and liabilities are included in the consolidated balance sheet.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

14

A debt security exists when another entity owes the security holder some combination of interest and principal.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

15

Ownership in a corporation is represented by shares of common or preferred stock called ____________________ securities.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

16

Any transaction or set of transactions that brings together two or more previously separate entities to form a single accounting entity is called a business combination.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

17

Held-to-maturity securities are equity and debt investments that management intends to sell in the future, but not necessarily in the near term.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

18

If the acquisition cost exceeds the current value of the net assets (assets minus liabilities)acquired, the investor must also be purchasing an intangible asset arising from attributes that are not separable from the business-such as customer satisfaction, product quality, skilled employees, and business location.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

19

Minority (or noncontrolling)interest is disclosed when the parent owns more than 50%, but less than 100% of the outstanding common stock.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

20

If the investor holds 50% or more of the investee's outstanding common stock, then the investor is referred to as the parent and the investee is called the subsidiary.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

21

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Method of accounting for all investments in debt securities that are classified as held-to-maturity securities

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Method of accounting for all investments in debt securities that are classified as held-to-maturity securities

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

22

Business combinations can occur through either an asset or ____________________ acquisition.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

23

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Situation where the investor owns less than 20% of the common stock of another company and therefore is not attempting to exert influence over the operating and financial policies of the investee

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Situation where the investor owns less than 20% of the common stock of another company and therefore is not attempting to exert influence over the operating and financial policies of the investee

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

24

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Situation where the investor owns 20% to 50% of the outstanding common stock of the investee and is therefore assumed to possess significant influence over the operating and financial policies of the investee

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Situation where the investor owns 20% to 50% of the outstanding common stock of the investee and is therefore assumed to possess significant influence over the operating and financial policies of the investee

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

25

Any transaction or set of transactions that brings together two or more previously separate entities to form a single accounting entity is called a ____________________.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

26

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Any transaction or set of transactions that brings together two or more previously separate entities to form a single accounting entity

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Any transaction or set of transactions that brings together two or more previously separate entities to form a single accounting entity

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

27

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Represents an ownership interest in a corporation, usually common stock

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Represents an ownership interest in a corporation, usually common stock

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

28

If the investor holds 50% or more of the common stock of the investee, then the investor is referred to as the ____________________ and the investee is referred to as the ____________________.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

29

A business combination is recorded at the cost of acquisition, without regard to the seller's ____________________ value.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

30

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Name given to the investee when an investor owns over 50% of the investee's outstanding common stock

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Name given to the investee when an investor owns over 50% of the investee's outstanding common stock

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

31

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Exists when another entity owes the security holder some combination of interest and principal

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Exists when another entity owes the security holder some combination of interest and principal

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

32

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Equity and debt investments that management intends to sell in the future, but not necessarily in the near term

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Equity and debt investments that management intends to sell in the future, but not necessarily in the near term

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

33

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Any voting stock not held by the parent in situations where consolidation is required because the investor acquires between 50% and 100% of the investee's stock

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Any voting stock not held by the parent in situations where consolidation is required because the investor acquires between 50% and 100% of the investee's stock

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

34

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Equity or debt investments that management intends to sell in the near term, typically within a single month

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Equity or debt investments that management intends to sell in the near term, typically within a single month

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

35

If the investor holds 50% or more of the common stock of the investee, then the two corporations are no longer separate accounting entities and therefore must prepare ____________________ financial statements, which combine information about the two corporations as if they were a single company.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

36

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

An intangible asset arising from attributes that are not separable from the business-such as customer satisfaction, product quality, skilled employees, and business location

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

An intangible asset arising from attributes that are not separable from the business-such as customer satisfaction, product quality, skilled employees, and business location

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

37

Consolidation is required when a parent acquires between 50% and 100% of the subsidiary's stock. Any voting stock not held by the parent is called the ____________________.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

38

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Method of accounting required for all passive investments in which the investment is valued at the price for which the investor could sell the asset in an orderly transaction between market participants

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Method of accounting required for all passive investments in which the investment is valued at the price for which the investor could sell the asset in an orderly transaction between market participants

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

39

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Debt investments that management intends to hold until the debt contract requires the borrower to repay the debt in its entirety

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Debt investments that management intends to hold until the debt contract requires the borrower to repay the debt in its entirety

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

40

The excess of the investor's acquisition cost over the current value of the investee's identifiable net assets is recorded as an intangible asset called ____________________.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

41

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Result when the value of securities must be written up or down to fair market value at the balance sheet date, a process referred to as "marking to market"

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Result when the value of securities must be written up or down to fair market value at the balance sheet date, a process referred to as "marking to market"

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

42

On January 1, 2011, P Company purchased all of the outstanding common stock of S Company. The consolidation of the two balance sheets requires a

A)credit adjustment to eliminate P Company's "Investment in S Company" account.

B)debit adjustment to eliminate S Company's "Investment in P Company" account

C)debit adjustment to eliminate P Company's "Investment in S Company" account

D)credit adjustment to eliminate S Company's "Investment in P Company" account

A)credit adjustment to eliminate P Company's "Investment in S Company" account.

B)debit adjustment to eliminate S Company's "Investment in P Company" account

C)debit adjustment to eliminate P Company's "Investment in S Company" account

D)credit adjustment to eliminate S Company's "Investment in P Company" account

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

43

A company is referred to as a parent if it owns

A)33% of the debt securities of another company.

B)100% of the debt securities of another company.

C)15% of the stock of another company.

D)more than 50% of the stock of another company.

A)33% of the debt securities of another company.

B)100% of the debt securities of another company.

C)15% of the stock of another company.

D)more than 50% of the stock of another company.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

44

The equity method of accounting for an investment is used when a company purchases

A)more than 20% of the debt securities of another company.

B)100% of the debt securities of another company.

C)15% of the equity securities of another company.

D)between 20-50% of the equity securities of another company.

A)more than 20% of the debt securities of another company.

B)100% of the debt securities of another company.

C)15% of the equity securities of another company.

D)between 20-50% of the equity securities of another company.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

45

A transaction that brings together two or more previously separate entities to form a single legal entity is called

A)stock acquisition.

B)debt acquisition.

C)asset acquisition.

D)business acquisition.

A)stock acquisition.

B)debt acquisition.

C)asset acquisition.

D)business acquisition.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

46

On January 1, 2011, P Company purchased all of the outstanding common stock of S Company. Which of the following represents the worksheet entry needed to consolidate the balance sheets of the two companies?

A)Investment in S XXX Common stock XXX

Retained earnings XXX

B)Investment in S XXX Retained earnings XXX

C)Common stock XXX Retained earnings XXX

Investment in S XXX

D)Retained earnings XXX Investment in S XXX

A)Investment in S XXX Common stock XXX

Retained earnings XXX

B)Investment in S XXX Retained earnings XXX

C)Common stock XXX Retained earnings XXX

Investment in S XXX

D)Retained earnings XXX Investment in S XXX

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

47

A passive investment is one in which the owner

A)is not attempting to exert influence over the company.

B)owns between 15-25% of the company's outstanding stock.

C)uses the equity method of accounting for the investment.

D)is gradually attempting to gain control over the company.

A)is not attempting to exert influence over the company.

B)owns between 15-25% of the company's outstanding stock.

C)uses the equity method of accounting for the investment.

D)is gradually attempting to gain control over the company.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

48

When a company purchases less than 50% of the equity securities of another company, which of the following statements is true?

A)Both companies' financial statements must be combined in consolidation.

B)The equity method of accounting will be required if the company's investment is at least 20%.

C)The fair value method of accounting will be used only if the securities are classified as available-for-sale.

D)The fair value method of accounting will be used only if they are trading securities.

A)Both companies' financial statements must be combined in consolidation.

B)The equity method of accounting will be required if the company's investment is at least 20%.

C)The fair value method of accounting will be used only if the securities are classified as available-for-sale.

D)The fair value method of accounting will be used only if they are trading securities.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

49

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Device that facilitates combining the financial statements of the investor and investee companies

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Device that facilitates combining the financial statements of the investor and investee companies

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

50

P Company paid $500,000 for 100% of the net assets (assets less liabilities)of S Company. The current value of S Company's net assets was only $475,000. As a result of this acquisition, P Company must recognize

A)negative goodwill.

B)goodwill.

C)gain.

D)loss.

A)negative goodwill.

B)goodwill.

C)gain.

D)loss.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

51

Select the incorrect statement from the following:

A)The financial statements for a 100% asset acquisition will be different from the consolidated financial statements for a 100% stock acquisition.

B)Business combinations usually, but not always, transfer ownership of the acquired business entity from one stockholder group to another.

C)Purchased assets are recorded at their current value to the purchaser, without regard to their recorded value to the seller.

D)The excess of acquisition cost over the current value of the investee's identifiable net assets is recorded as goodwill.

A)The financial statements for a 100% asset acquisition will be different from the consolidated financial statements for a 100% stock acquisition.

B)Business combinations usually, but not always, transfer ownership of the acquired business entity from one stockholder group to another.

C)Purchased assets are recorded at their current value to the purchaser, without regard to their recorded value to the seller.

D)The excess of acquisition cost over the current value of the investee's identifiable net assets is recorded as goodwill.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

52

Select the incorrect statement from the following:

A)Adjustments are required to eliminate any transactions between Parent and Sub (e.g., selling or other transfer of assets).

B)Even when the parent owns less than 100% of the subsidiary's stock, 100% of the subsidiary's assets and liabilities are included in the consolidated balance sheet.

C)Any consolidated net income attributable to minority interest must be clearly identified and shown on the consolidated income statement.

D)Consolidated net income is equal to the sum of the parent's net income and the sub's net income.

A)Adjustments are required to eliminate any transactions between Parent and Sub (e.g., selling or other transfer of assets).

B)Even when the parent owns less than 100% of the subsidiary's stock, 100% of the subsidiary's assets and liabilities are included in the consolidated balance sheet.

C)Any consolidated net income attributable to minority interest must be clearly identified and shown on the consolidated income statement.

D)Consolidated net income is equal to the sum of the parent's net income and the sub's net income.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

53

What are the effects on the accounting equation from the purchase of a short-term investment?

A)Assets and stockholders' equity increase.

B)No effects; assets increase and decrease by the same amount.

C)Assets and liabilities decrease.

D)Stockholders' equity increases and liabilities decrease.

A)Assets and stockholders' equity increase.

B)No effects; assets increase and decrease by the same amount.

C)Assets and liabilities decrease.

D)Stockholders' equity increases and liabilities decrease.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

54

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Situation where the investor owns over 50% of the outstanding common stock and is therefore deemed to own the investee

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Situation where the investor owns over 50% of the outstanding common stock and is therefore deemed to own the investee

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

55

The practice of adjusting the market value of securities that are accounted for using the fair value method is referred to as

A)consolidation.

B)marking-to-market.

C)passive investing.

D)segregation of investments.

A)consolidation.

B)marking-to-market.

C)passive investing.

D)segregation of investments.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

56

What are the effects on the accounting equation from the recognition of an unrealized loss on trading securities?

A)Assets and stockholders' equity decrease.

B)No effects; unrealized gains and losses should not be recorded.

C)Assets and liabilities decrease.

D)Stockholders' equity decreases and liabilities increase.

A)Assets and stockholders' equity decrease.

B)No effects; unrealized gains and losses should not be recorded.

C)Assets and liabilities decrease.

D)Stockholders' equity decreases and liabilities increase.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

57

Select the correct statement from the following:

A)Consolidation worksheet adjustments are not entered on the accounting records of either Parent or Sub.

B)Consolidation worksheet adjustments are entered on the accounting records of the Parent but not the Sub.

C)Consolidation worksheet adjustments are entered on the accounting records of the Sub but not the Parent.

D)Consolidation worksheet adjustments are entered on the accounting records of both the Parent and the Sub.

A)Consolidation worksheet adjustments are not entered on the accounting records of either Parent or Sub.

B)Consolidation worksheet adjustments are entered on the accounting records of the Parent but not the Sub.

C)Consolidation worksheet adjustments are entered on the accounting records of the Sub but not the Parent.

D)Consolidation worksheet adjustments are entered on the accounting records of both the Parent and the Sub.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

58

Any transaction or set of transactions that brings together two or more previously separate entities to form a single accounting entity is called a

A)business plan.

B)business combination.

C)corporation.

D)joint venture.

A)business plan.

B)business combination.

C)corporation.

D)joint venture.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

59

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Method of accounting for investments where the investor possesses significant influence (20% to 50% common stock ownership)over the operating and financial policies of the investee

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Method of accounting for investments where the investor possesses significant influence (20% to 50% common stock ownership)over the operating and financial policies of the investee

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

60

Match the following terms to their correct definition:

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Name given to an investor who owns over 50% of the outstanding common stock of the investee

a.equity security

j.held-to-maturity securities

b.debt security

k.amortized cost method

c.passive

l.fair value method

d.significant influence

m.unrealized gains and losses

e.control

n.equity method

f.parent

o.consolidation worksheet

g.subsidiary

p.minority interest

h.trading securities

q.business combination

i.available-for-sale securities

r.goodwill

Name given to an investor who owns over 50% of the outstanding common stock of the investee

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

61

Which method of accounting for investments recognizes income when income is earned by the investee?

A)fair value method

B)amortized cost method

C)trading method

D)equity method

A)fair value method

B)amortized cost method

C)trading method

D)equity method

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

62

On January 1, 2012, Parent, Inc., purchased 80% of the outstanding common stock of Sub Corporation for $750,000. Since Parent has control over Sub, a consolidated balance sheet must be prepared from the individual balance sheets of both companies. Complete the following worksheet to prepare the consolidated balance sheet on January 1, 2012.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

63

On January 1, 2012, Teddy Bear Company purchased 25% of the common stock of one of its major suppliers-Fluff n' Stuff, for $1,000,000 cash. On November 1, 2012, Fluff n' Stuff declared and paid a cash dividend of $50,000. Further, for the year ended December 31, 2012, Fluff n' Stuff reported net income of $200,000.

A)Which method of accounting for investments should be used for the Fluff n' Stuff stock?

B)Record all of the necessary journal entries for this investment during 2012.

C)What will be the balance in the investment account at December 31, 2012?

A)Which method of accounting for investments should be used for the Fluff n' Stuff stock?

B)Record all of the necessary journal entries for this investment during 2012.

C)What will be the balance in the investment account at December 31, 2012?

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

64

Trattoria, Inc. engaged in the following investment transactions during 2013:

At December 31, 2013, the market value of Tarbet's stock was $54.

At December 31, 2013, the market value of Tarbet's stock was $54. Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

65

The journal entry required to record the receipt of dividends under the fair value method of accounting for investments includes a

A)credit to the investment account.

B)debit to the investment account.

C)credit to dividend income.

D)debit to retained earnings.

A)credit to the investment account.

B)debit to the investment account.

C)credit to dividend income.

D)debit to retained earnings.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

66

The Allowance to Adjust Trading Securities to Market account is

A)an asset account.

B)a contra asset account.

C)a liability account.

D)an unrealized gain or loss account.

A)an asset account.

B)a contra asset account.

C)a liability account.

D)an unrealized gain or loss account.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

67

Tail Winds Corporation acquired the following equity securities during 2013:

The company's investment in these two companies is passive and classified as available-for-sale. During 2013, TICO paid a dividend of $1.10 per share and Thankful paid a dividend of $1.75 per share. At December 31, 2013, the market value of these securities was $79 per share for TICO and $23 per share for Thankful.

The company's investment in these two companies is passive and classified as available-for-sale. During 2013, TICO paid a dividend of $1.10 per share and Thankful paid a dividend of $1.75 per share. At December 31, 2013, the market value of these securities was $79 per share for TICO and $23 per share for Thankful. Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

68

Which method of accounting for investments results in unrealized gains and losses because the investments must be marked to market?

A)equity method

B)amortized cost method

C)fair value method

D)trading method

A)equity method

B)amortized cost method

C)fair value method

D)trading method

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

69

Tidewater Management, Inc. had no investments in short-term marketable securities prior to 2013. During 2013, the company engaged in the following investment transactions:

At the end of 2013, the Toucan Taxi stock had a market value of $15 per share.

At the end of 2013, the Toucan Taxi stock had a market value of $15 per share. Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

70

On January 1, 2012, Parent, Inc., purchases all the outstanding common stock of Sub Corporation for $750,000. Since Parent has control over Sub, a consolidated balance sheet must be prepared from the individual balance sheets of both companies. Complete the following worksheet to prepare the consolidated balance sheet on January 1, 2012.

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

71

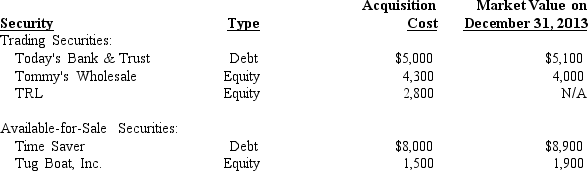

Thomkin Enterprises purchased several investment securities on November 1, 2013. Various transactions and market activities occurred regarding these investments between acquisition and December 31st (the company's year-end), as shown below:

Additional information:

Prepare journal entries to record the purchase of the securities, the receipt of dividends and interest, the sale of the TRL stock, and the end-of-year mark-to-market adjustments. For the end-of-year entries, indicate how the resulting gains or losses should be recognized in Thomkin's year-end financial statements.

Additional information: Prepare journal entries to record the purchase of the securities, the receipt of dividends and interest, the sale of the TRL stock, and the end-of-year mark-to-market adjustments. For the end-of-year entries, indicate how the resulting gains or losses should be recognized in Thomkin's year-end financial statements. Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

72

Treasure Distributors, Inc. had no investments in short-term marketable securities prior to 2012. During 2012, the company engaged in the following investment transactions:

At the end of 2012, the Toledo Company stock had a market value of $18 per share.

At the end of 2012, the Toledo Company stock had a market value of $18 per share. Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

73

An investor's available-for-sale securities had increased in market value from $50,000 to $55,000 as of the balance sheet date. Which of the following journal entries would be required?

A)Realized gain on investments 5,000 Allowance to adjust investments to market 5,000

B)Allowance to adjust investments to market 5,000 Realized gain on investments 5,000

C)Unrealized gain on investments 5,000 Allowance to adjust investments to market 5,000

D)Allowance to adjust investments to market 5,000 Unrealized gain on investments 5,000

A)Realized gain on investments 5,000 Allowance to adjust investments to market 5,000

B)Allowance to adjust investments to market 5,000 Realized gain on investments 5,000

C)Unrealized gain on investments 5,000 Allowance to adjust investments to market 5,000

D)Allowance to adjust investments to market 5,000 Unrealized gain on investments 5,000

Unlock Deck

Unlock for access to all 73 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 73 flashcards in this deck.