Deck 2: A: Consolidation of Financial Information

Full screen (f)

Question

Question

Question

Direct combination costs and amounts incurred to register and issue stock in connection with a business combination.How should those costs be accounted for in a pre-2009 business combination?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

In an acquisition where 100% control is acquired, how would the land accounts of the parent and the land accounts of the subsidiary be reported on consolidated financial statements?

Question

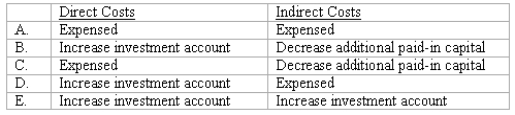

How are direct and indirect costs accounted for when applying the acquisition method for a business combination?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/116

Play

Full screen (f)

Deck 2: A: Consolidation of Financial Information

1

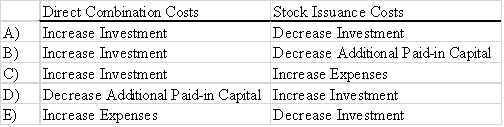

In a business combination where a subsidiary retains its incorporation and which is accounted for under the acquisition method, how should stock issuance costs and direct combination costs be treated?

A) Stock issuance costs and direct combination costs are expensed as incurred.

B) Direct combination costs are ignored, and the stock issuance costs result in a reduction to additional paid-in capital.

C) Direct combination costs are expensed as incurred and stock issuance costs result in a reduction to additional paid-in capital.

D) Both are treated as part of the acquisition consideration transferred.

E) Both reduce additional paid-in capital.

A) Stock issuance costs and direct combination costs are expensed as incurred.

B) Direct combination costs are ignored, and the stock issuance costs result in a reduction to additional paid-in capital.

C) Direct combination costs are expensed as incurred and stock issuance costs result in a reduction to additional paid-in capital.

D) Both are treated as part of the acquisition consideration transferred.

E) Both reduce additional paid-in capital.

C

2

What is the primary difference between: (i) accounting for a business combination when the subsidiary is dissolved; and (ii) accounting for a business combination when the subsidiary retains its incorporation?

A) If the subsidiary is dissolved, it will not be operated as a separate division.

B) If the subsidiary is dissolved, assets and liabilities are consolidated at their book values.

C) If the subsidiary retains its incorporation, there will be no goodwill associated with the acquisition.

D) If the subsidiary retains its incorporation, assets and liabilities are consolidated at their book values.

E) If the subsidiary retains its incorporation, the consolidation is not formally recorded in the accounting records of the acquiring company.

A) If the subsidiary is dissolved, it will not be operated as a separate division.

B) If the subsidiary is dissolved, assets and liabilities are consolidated at their book values.

C) If the subsidiary retains its incorporation, there will be no goodwill associated with the acquisition.

D) If the subsidiary retains its incorporation, assets and liabilities are consolidated at their book values.

E) If the subsidiary retains its incorporation, the consolidation is not formally recorded in the accounting records of the acquiring company.

E

3

Direct combination costs and amounts incurred to register and issue stock in connection with a business combination.How should those costs be accounted for in a pre-2009 business combination?

B

4

Using the acquisition method for a business combination, goodwill is generally calculated as the:

A) Cost of the investment less the subsidiary's book value at the beginning of the year.

B) Cost of the investment less the subsidiary's book value at the acquisition date.

C) Cost of the investment less the subsidiary's fair value at the beginning of the year.

D) Cost of the investment less the subsidiary's fair value at acquisition date.

E) Zero, it is no longer allowed under federal law.

A) Cost of the investment less the subsidiary's book value at the beginning of the year.

B) Cost of the investment less the subsidiary's book value at the acquisition date.

C) Cost of the investment less the subsidiary's fair value at the beginning of the year.

D) Cost of the investment less the subsidiary's fair value at acquisition date.

E) Zero, it is no longer allowed under federal law.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

5

Lisa Co.paid cash for all of the voting common stock of Victoria Corp.Victoria will continue to exist as a separate corporation.Entries for the consolidation of Lisa and Victoria would be recorded in

A) A worksheet.

B) Lisa's general journal.

C) Victoria's general journal.

D) Victoria's secret consolidation journal.

E) The general journals of both companies.

A) A worksheet.

B) Lisa's general journal.

C) Victoria's general journal.

D) Victoria's secret consolidation journal.

E) The general journals of both companies.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

6

With respect to recognizing and measuring the fair value of a business combination in accordance with the acquisition method of accounting, which of the following should the acquirer consider when determining fair value?

A) Only assets received by the acquirer.

B) Only consideration transferred by the acquirer.

C) The consideration transferred by the acquirer plus the fair value of assets received less liabilities assumed.

D) The par value of stock transferred by the acquirer, and the book value of identifiable assets transferred by the entity acquired.

E) The book value of identifiable assets transferred to the acquirer as part of the business combination less any liabilities assumed.

A) Only assets received by the acquirer.

B) Only consideration transferred by the acquirer.

C) The consideration transferred by the acquirer plus the fair value of assets received less liabilities assumed.

D) The par value of stock transferred by the acquirer, and the book value of identifiable assets transferred by the entity acquired.

E) The book value of identifiable assets transferred to the acquirer as part of the business combination less any liabilities assumed.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

7

At the date of an acquisition which is not a bargain purchase, the acquisition method

A) Consolidates the subsidiary's assets at fair value and the liabilities at book value.

B) Consolidates all subsidiary assets and liabilities at book value.

C) Consolidates all subsidiary assets and liabilities at fair value.

D) Consolidates current assets and liabilities at book value, and long-term assets and liabilities at fair value.

E) Consolidates the subsidiary's assets at book value and the liabilities at fair value.

A) Consolidates the subsidiary's assets at fair value and the liabilities at book value.

B) Consolidates all subsidiary assets and liabilities at book value.

C) Consolidates all subsidiary assets and liabilities at fair value.

D) Consolidates current assets and liabilities at book value, and long-term assets and liabilities at fair value.

E) Consolidates the subsidiary's assets at book value and the liabilities at fair value.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

8

Assume that Bullen paid a total of $480,000 in cash for all of the shares of Vicker.In addition, Bullen paid $35,000 for secretarial and management time allocated to the acquisition transaction.What will be the balance in consolidated goodwill?

A) $ 0.

B) $20,000.

C) $35,000.

D) $55,000.

E) $65,000.

A) $ 0.

B) $20,000.

C) $35,000.

D) $55,000.

E) $65,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

9

Assume that Bullen issued 12,000 shares of common stock with a $5 par value and a $47 fair value for all of the outstanding shares of Vicker.What will be the consolidated Additional Paid-In Capital and Retained Earnings (January 1, 2018 balances) as a result of this acquisition transaction?

A) $60,000 and $490,000.

B) $60,000 and $250,000.

C) $380,000 and $250,000.

D) $524,000 and $250,000.

E) $524,000 and $420,000.

A) $60,000 and $490,000.

B) $60,000 and $250,000.

C) $380,000 and $250,000.

D) $524,000 and $250,000.

E) $524,000 and $420,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

10

A statutory merger is a(n)

A) Business combination in which only one of the two companies continues to exist as a legal corporation.

B) Business combination in which both companies continue to exist.

C) Acquisition of a competitor.

D) Acquisition of a supplier or a customer.

E) Legal proposal to acquire outstanding shares of the target's stock.

A) Business combination in which only one of the two companies continues to exist as a legal corporation.

B) Business combination in which both companies continue to exist.

C) Acquisition of a competitor.

D) Acquisition of a supplier or a customer.

E) Legal proposal to acquire outstanding shares of the target's stock.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

11

Assume that Bullen issued 12,000 shares of common stock, with a $5 par value and a $47 fair value, to obtain all of Vicker's outstanding stock.In this acquisition transaction, how much goodwill should be recognized?

A) $144,000.

B) $104,000.

C) $ 64,000.

D) $ 60,000.

E) $ 0.

A) $144,000.

B) $104,000.

C) $ 64,000.

D) $ 60,000.

E) $ 0.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

12

Assume that Bullen issued preferred stock with a par value of $240,000 and a fair value of $500,000 for all of the outstanding shares of Vicker in an acquisition business combination.What will be the balance in the consolidated Inventory and Land accounts?

A) $440,000, $496,000.

B) $440,000, $520,000.

C) $425,000, $505,000.

D) $400,000, $500,000.

E) $427,000, $510,000.

A) $440,000, $496,000.

B) $440,000, $520,000.

C) $425,000, $505,000.

D) $400,000, $500,000.

E) $427,000, $510,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

13

Acquired in-process research and development is considered as

A) A definite-lived asset subject to amortization.

B) A definite-lived asset subject to testing for impairment.

C) An indefinite-lived asset subject to amortization.

D) An indefinite-lived asset subject to testing for impairment.

E) A research and development expense at the date of acquisition.

A) A definite-lived asset subject to amortization.

B) A definite-lived asset subject to testing for impairment.

C) An indefinite-lived asset subject to amortization.

D) An indefinite-lived asset subject to testing for impairment.

E) A research and development expense at the date of acquisition.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following examples accurately describes a difference in the types of business combinations?

A) A statutory merger can only be effected through an asset acquisition while a statutory consolidation can only be effected through a capital stock acquisition.

B) A statutory merger can only be effected through a capital stock acquisition while a statutory consolidation can only be effected through an asset acquisition.

C) A statutory merger requires the dissolution of the acquired company while a statutory consolidation requires dissolution of the companies involved in the combination following the transfer of assets or stock to a newly formed entity.

D) A statutory consolidation requires dissolution of the acquired company while a statutory merger does not require dissolution.

E) Both a statutory merger and a statutory consolidation can only be effected through an asset acquisition but only a statutory consolidation requires dissolution of the acquired company.

A) A statutory merger can only be effected through an asset acquisition while a statutory consolidation can only be effected through a capital stock acquisition.

B) A statutory merger can only be effected through a capital stock acquisition while a statutory consolidation can only be effected through an asset acquisition.

C) A statutory merger requires the dissolution of the acquired company while a statutory consolidation requires dissolution of the companies involved in the combination following the transfer of assets or stock to a newly formed entity.

D) A statutory consolidation requires dissolution of the acquired company while a statutory merger does not require dissolution.

E) Both a statutory merger and a statutory consolidation can only be effected through an asset acquisition but only a statutory consolidation requires dissolution of the acquired company.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

15

According to GAAP, which of the following is true with respect to the pooling of interest method of accounting for business combinations?

A) It was the only method used prior to 2002.

B) It must be used for all new acquisitions.

C) GAAP allowed its use prior to 2002.

D) It, or the acquisition method, may be used at the acquirer's discretion.

E) GAAP requires it to be used instead of the acquisition method for business combinations for which $50 billion or more in consideration is transferred.

A) It was the only method used prior to 2002.

B) It must be used for all new acquisitions.

C) GAAP allowed its use prior to 2002.

D) It, or the acquisition method, may be used at the acquirer's discretion.

E) GAAP requires it to be used instead of the acquisition method for business combinations for which $50 billion or more in consideration is transferred.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

16

Assume that Botkins acquired Volkerson on January 1, 2017 and that Volkerson maintains a separate corporate existence.At what amount did Botkins record the investment in Volkerson?

A) $ 56,000.

B) $182,000.

C) $209,000.

D) $261,000.

E) $312,000.

A) $ 56,000.

B) $182,000.

C) $209,000.

D) $261,000.

E) $312,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following statements is true regarding the acquisition method of accounting for a business combination?

A) The combination must involve the exchange of equity securities only.

B) The transaction establishes an acquisition fair value basis for the company being acquired.

C) The two companies may be about the same size, and it is difficult to determine the acquired company and the acquiring company.

D) The transaction may be considered to be the uniting of the ownership interests of the companies involved.

E) The acquired subsidiary must be smaller in size than the acquiring parent.

A) The combination must involve the exchange of equity securities only.

B) The transaction establishes an acquisition fair value basis for the company being acquired.

C) The two companies may be about the same size, and it is difficult to determine the acquired company and the acquiring company.

D) The transaction may be considered to be the uniting of the ownership interests of the companies involved.

E) The acquired subsidiary must be smaller in size than the acquiring parent.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

18

In an acquisition where 100% control is acquired, how would the land accounts of the parent and the land accounts of the subsidiary be reported on consolidated financial statements?

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

19

How are direct and indirect costs accounted for when applying the acquisition method for a business combination?

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

20

Assume that Bullen issued 12,000 shares of common stock with a $5 par value and a $47 fair value for all of the outstanding stock of Vicker.What is the consolidated balance for Land as a result of this acquisition transaction?

A) $460,000.

B) $510,000.

C) $500,000.

D) $520,000.

E) $490,000.

A) $460,000.

B) $510,000.

C) $500,000.

D) $520,000.

E) $490,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is a not a reason for a business combination to take place?

A) Cost savings through elimination of duplicate facilities.

B) Quick entry for new and existing products into domestic and foreign markets.

C) Diversification of business risk.

D) Vertical integration.

E) Increase in stock price of the acquired company.

A) Cost savings through elimination of duplicate facilities.

B) Quick entry for new and existing products into domestic and foreign markets.

C) Diversification of business risk.

D) Vertical integration.

E) Increase in stock price of the acquired company.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

22

Compute the consideration transferred for this acquisition at December 31, 2018.

A) $ 900.

B) $1,165.

C) $1,200.

D) $1,765.

E) $1,800.

A) $ 900.

B) $1,165.

C) $1,200.

D) $1,765.

E) $1,800.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

23

In this acquisition business combination, what total amount of common stock and additional paid-in capital should Goodwin recognize on its consolidated financial statements?

A) $ 265.

B) $1,165.

C) $1,200.

D) $1,235.

E) $1,765.

A) $ 265.

B) $1,165.

C) $1,200.

D) $1,235.

E) $1,765.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

24

In a transaction accounted for using the acquisition method where consideration transferred exceeds book value of the acquired company, which statement is true for the acquiring company with regard to its investment?

A) Net assets of the acquired company are revalued to their fair values and any excess of consideration transferred over fair value of net assets acquired is allocated to goodwill.

B) Net assets of the acquired company are maintained at book value and any excess of consideration transferred over book value of net assets acquired is allocated to goodwill.

C) Acquired assets are revalued to their fair values. Acquired liabilities are maintained at book values. Any excess is allocated to goodwill.

D) Acquired long-term assets are revalued to their fair values. Any excess is allocated to goodwill.

A) Net assets of the acquired company are revalued to their fair values and any excess of consideration transferred over fair value of net assets acquired is allocated to goodwill.

B) Net assets of the acquired company are maintained at book value and any excess of consideration transferred over book value of net assets acquired is allocated to goodwill.

C) Acquired assets are revalued to their fair values. Acquired liabilities are maintained at book values. Any excess is allocated to goodwill.

D) Acquired long-term assets are revalued to their fair values. Any excess is allocated to goodwill.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

25

Compute the goodwill arising from this acquisition at December 31, 2018.

A) $ 0.

B) $100.

C) $125.

D) $160.

E) $ 45.

A) $ 0.

B) $100.

C) $125.

D) $160.

E) $ 45.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following statements is true regarding the acquisition method of accounting for a business combination?

A) Net assets of the acquired company are reported at their fair values.

B) Net assets of the acquired company are reported at their book values.

C) Any goodwill associated with the acquisition is reported as a development cost.

D) The acquisition can only be effected by a mutual exchange of voting common stock.

E) Indirect costs of the combination reduce additional paid-in capital.

A) Net assets of the acquired company are reported at their fair values.

B) Net assets of the acquired company are reported at their book values.

C) Any goodwill associated with the acquisition is reported as a development cost.

D) The acquisition can only be effected by a mutual exchange of voting common stock.

E) Indirect costs of the combination reduce additional paid-in capital.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

27

Compute the consolidated buildings (net) account at December 31, 2018.

A) $2,700.

B) $3,370.

C) $3,300.

D) $3,260.

E) $3,340.

A) $2,700.

B) $3,370.

C) $3,300.

D) $3,260.

E) $3,340.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following statements is true?

A) The pooling of interests for business combinations is an alternative to the acquisition method.

B) The purchase method for business combinations is an alternative to the acquisition method.

C) Neither the purchase method nor the pooling of interests method is allowed for new business combinations.

D) Any previous business combination originally accounted for under purchase or pooling of interests accounting method will now be accounted for under the acquisition method of accounting for business combinations.

E) Companies previously using the purchase or pooling of interests accounting method must report a change in accounting principle when consolidating those subsidiaries with new acquisition combinations.

A) The pooling of interests for business combinations is an alternative to the acquisition method.

B) The purchase method for business combinations is an alternative to the acquisition method.

C) Neither the purchase method nor the pooling of interests method is allowed for new business combinations.

D) Any previous business combination originally accounted for under purchase or pooling of interests accounting method will now be accounted for under the acquisition method of accounting for business combinations.

E) Companies previously using the purchase or pooling of interests accounting method must report a change in accounting principle when consolidating those subsidiaries with new acquisition combinations.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

29

Compute the consolidated revenues for 2018.

A) $2,700.

B) $ 720.

C) $ 920.

D) $3,300.

E) $1,540.

A) $2,700.

B) $ 720.

C) $ 920.

D) $3,300.

E) $1,540.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

30

Assuming that Corr retains a separate corporate existence after this acquisition, at what amount is the investment recorded on Goodwin's books?

A) $1,540.

B) $1,800.

C) $1,860.

D) $1,825.

E) $1,625.

A) $1,540.

B) $1,800.

C) $1,860.

D) $1,825.

E) $1,625.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements is true regarding a statutory merger?

A) The original companies dissolve while remaining as separate divisions of a newly created company.

B) Both companies remain in existence as legal corporations with one corporation now a subsidiary of the acquiring company.

C) The acquired company dissolves as a separate corporation and becomes a division of the acquiring company.

D) The acquiring company acquires the stock of the acquired company as an investment.

E) A statutory merger is no longer a legal option.

A) The original companies dissolve while remaining as separate divisions of a newly created company.

B) Both companies remain in existence as legal corporations with one corporation now a subsidiary of the acquiring company.

C) The acquired company dissolves as a separate corporation and becomes a division of the acquiring company.

D) The acquiring company acquires the stock of the acquired company as an investment.

E) A statutory merger is no longer a legal option.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

32

In a transaction accounted for using the acquisition method where consideration transferred is less than fair value of net assets acquired, which statement is true?

A) Negative goodwill is recorded.

B) A deferred credit is recorded.

C) A gain on bargain purchase is recorded.

D) Long-term assets of the acquired company are reduced in proportion to their fair values. Any excess is recorded as a deferred credit.

E) Long-term assets and liabilities of the acquired company are reduced in proportion to their fair values. Any excess is recorded as gain.

A) Negative goodwill is recorded.

B) A deferred credit is recorded.

C) A gain on bargain purchase is recorded.

D) Long-term assets of the acquired company are reduced in proportion to their fair values. Any excess is recorded as a deferred credit.

E) Long-term assets and liabilities of the acquired company are reduced in proportion to their fair values. Any excess is recorded as gain.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

33

Compute the consolidated receivables and inventory for 2018.

A) $1,200.

B) $1,515.

C) $1,540.

D) $1,800.

E) $2,140.

A) $1,200.

B) $1,515.

C) $1,540.

D) $1,800.

E) $2,140.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

34

Compute the consolidated common stock account at December 31, 2018.

A) $1,080.

B) $1,480.

C) $1,380.

D) $2,280.

E) $2,680.

A) $1,080.

B) $1,480.

C) $1,380.

D) $2,280.

E) $2,680.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

35

Assume that Botkins acquired Volkerson on January 1, 2017.Immediately afterwards, what is the value of the consolidated Common Stock?

A) $456,000.

B) $402,000.

C) $274,000.

D) $276,000.

E) $330,000.

A) $456,000.

B) $402,000.

C) $274,000.

D) $276,000.

E) $330,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

36

Compute the consolidated equipment (net) account at December 31, 2018.

A) $2,100.

B) $3,500.

C) $3,300.

D) $3,000.

E) $3,200.

A) $2,100.

B) $3,500.

C) $3,300.

D) $3,000.

E) $3,200.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

37

Compute the consolidated cash account at December 31, 2018.

A) $460.

B) $425.

C) $400.

D) $435.

E) $240.

A) $460.

B) $425.

C) $400.

D) $435.

E) $240.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements is true regarding a statutory consolidation?

A) The original companies dissolve while remaining as separate divisions of a newly created company.

B) Both companies remain in existence as legal corporations with one corporation now a subsidiary of the acquiring company.

C) The acquired company dissolves as a separate corporation and becomes a division of the acquiring company.

D) The acquiring company acquires the stock of the acquired company as an investment.

E) A statutory consolidation is no longer a legal option.

A) The original companies dissolve while remaining as separate divisions of a newly created company.

B) Both companies remain in existence as legal corporations with one corporation now a subsidiary of the acquiring company.

C) The acquired company dissolves as a separate corporation and becomes a division of the acquiring company.

D) The acquiring company acquires the stock of the acquired company as an investment.

E) A statutory consolidation is no longer a legal option.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

39

Compute the consolidated expenses for 2018.

A) $1,980.

B) $2,005.

C) $2,040.

D) $2,380.

E) $2,405.

A) $1,980.

B) $2,005.

C) $2,040.

D) $2,380.

E) $2,405.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

40

Chapel Hill Company had common stock of $350,000 and retained earnings of $490,000.Blue Town Inc.had common stock of $700,000 and retained earnings of $980,000.On January 1, 2018, Blue Town issued 34,000 shares of common stock with a $12 par value and a $35 fair value for all of Chapel Hill Company's outstanding common stock.This combination was accounted for using the acquisition method.Immediately after the combination, what was the amount of total consolidated net assets?

A) $2,520,000.

B) $1,190,000.

C) $1,680,000.

D) $2,870,000.

E) $2,030,000.

A) $2,520,000.

B) $1,190,000.

C) $1,680,000.

D) $2,870,000.

E) $2,030,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

41

Compute consolidated land at the date of the acquisition.

A) $2,060.

B) $1,800.

C) $ 260.

D) $2,050.

E) $2,070.

A) $2,060.

B) $1,800.

C) $ 260.

D) $2,050.

E) $2,070.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

42

What will the consolidated common stock account be as a result of this acquisition?

A) $ 300,000.

B) $ 990,000.

C) $1,000,000.

D) $1,590,000.

E) $1,600,000.

A) $ 300,000.

B) $ 990,000.

C) $1,000,000.

D) $1,590,000.

E) $1,600,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

43

Compute the amount of consolidated buildings (net) at date of acquisition.

A) $1,700.

B) $1,760.

C) $1,640.

D) $1,320.

E) $ 500.

A) $1,700.

B) $1,760.

C) $1,640.

D) $1,320.

E) $ 500.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

44

Compute the consolidated retained earnings at December 31, 2018.

A) $2,800.

B) $2,825.

C) $2,850.

D) $3,425.

E) $3,450.

A) $2,800.

B) $2,825.

C) $2,850.

D) $3,425.

E) $3,450.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

45

What will be the consolidated additional paid-in capital as a result of this acquisition?

A) $440,000.

B) $740,000.

C) $750,000.

D) $940,000.

E) $950,000.

A) $440,000.

B) $740,000.

C) $750,000.

D) $940,000.

E) $950,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

46

Compute the amount of consolidated cash after recording the acquisition transaction.

A) $220.

B) $185.

C) $200.

D) $205.

E) $215.

A) $220.

B) $185.

C) $200.

D) $205.

E) $215.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

47

If Osorio retains a separate corporate existence, what amount was recorded as the investment in Osorio?

A) $930.

B) $820.

C) $800.

D) $835.

E) $815.

A) $930.

B) $820.

C) $800.

D) $835.

E) $815.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

48

Compute the consolidated additional paid-in capital at December 31, 2018.

A) $ 810.

B) $1,350.

C) $1,675.

D) $1,910.

E) $1,875.

A) $ 810.

B) $1,350.

C) $1,675.

D) $1,910.

E) $1,875.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

49

Compute the consolidated liabilities at December 31, 2018.

A) $1,500.

B) $2,100.

C) $2,320.

D) $2,920.

E) $2,885.

A) $1,500.

B) $2,100.

C) $2,320.

D) $2,920.

E) $2,885.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

50

Compute the amount of consolidated additional paid-in capital at date of acquisition.

A) $1,080.

B) $1,420.

C) $1,065.

D) $1,425.

E) $1,440.

A) $1,080.

B) $1,420.

C) $1,065.

D) $1,425.

E) $1,440.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

51

Compute the amount of the consideration transferred by Atwood to acquire Franz.

A) $1,750.

B) $1,760.

C) $1,775.

D) $1,300.

E) $1,120.

A) $1,750.

B) $1,760.

C) $1,775.

D) $1,300.

E) $1,120.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

52

On December 31, 2017, assuming that Cames will retain its separate corporate existence, what value is assigned to Riley's investment account?

A) $ 150,000.

B) $ 300,000.

C) $ 750,000.

D) $ 760,000.

E) $1,350,000.

A) $ 150,000.

B) $ 300,000.

C) $ 750,000.

D) $ 760,000.

E) $1,350,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

53

Compute the amount of consolidated land at date of acquisition.

A) $1,000.

B) $ 960.

C) $ 920.

D) $ 400.

E) $ 320.

A) $1,000.

B) $ 960.

C) $ 920.

D) $ 400.

E) $ 320.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

54

Compute the amount of consolidated inventories at date of acquisition.

A) $1,080.

B) $1,350.

C) $1,360.

D) $1,370.

E) $ 290.

A) $1,080.

B) $1,350.

C) $1,360.

D) $1,370.

E) $ 290.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

55

Compute the amount of consolidated equipment at date of acquisition.

A) $480.

B) $580.

C) $559.

D) $570.

E) $560.

A) $480.

B) $580.

C) $559.

D) $570.

E) $560.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

56

At the date of acquisition, by how much does Riley's additional paid-in capital increase or decrease?

A) $ 0.

B) $440,000 increase.

C) $450,000 increase.

D) $640,000 increase.

E) $650,000 decrease.

A) $ 0.

B) $440,000 increase.

C) $450,000 increase.

D) $640,000 increase.

E) $650,000 decrease.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

57

Compute consolidated inventory at the date of the acquisition.

A) $1,650.

B) $1,810.

C) $1,230.

D) $ 580.

E) $1,830.

A) $1,650.

B) $1,810.

C) $1,230.

D) $ 580.

E) $1,830.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

58

What is the amount of goodwill arising from this acquisition?

A) $230.

B) $120.

C) $520.

D) None. There is a gain on bargain purchase of $230.

E) None. There is a gain on bargain purchase of $265.

A) $230.

B) $120.

C) $520.

D) None. There is a gain on bargain purchase of $230.

E) None. There is a gain on bargain purchase of $265.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

59

Compute the amount of consolidated common stock at date of acquisition.

A) $370.

B) $570.

C) $610.

D) $330.

E) $530.

A) $370.

B) $570.

C) $610.

D) $330.

E) $530.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

60

Compute the consolidated common stock at the date of acquisition.

A) $1,000.

B) $2,980.

C) $2,400.

D) $3,400.

E) $3,730.

A) $1,000.

B) $2,980.

C) $2,400.

D) $3,400.

E) $3,730.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

61

Compute consolidated equipment immediately following the acquisition.

A) $ 400.

B) $ 660.

C) $1,060.

D) $1,040.

E) $1,050.

A) $ 400.

B) $ 660.

C) $1,060.

D) $1,040.

E) $1,050.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

62

Compute consolidated expenses immediately following the acquisition.

A) $2,760.

B) $2,770.

C) $2,785.

D) $3,380.

E) $3,390.

A) $2,760.

B) $2,770.

C) $2,785.

D) $3,380.

E) $3,390.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

63

Compute consolidated revenues immediately following the acquisition.

A) $3,540.

B) $2,880.

C) $1,170.

D) $1,650.

E) $4,050.

A) $3,540.

B) $2,880.

C) $1,170.

D) $1,650.

E) $4,050.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

64

Compute consolidated goodwill at the date of the acquisition.

A) $360.

B) $450.

C) $460.

D) $440.

E) $475.

A) $360.

B) $450.

C) $460.

D) $440.

E) $475.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

65

Compute consolidated revenues immediately following the acquisition.

A) $3,540.

B) $2,880.

C) $1,170.

D) $1,650.

E) $4,050.

A) $3,540.

B) $2,880.

C) $1,170.

D) $1,650.

E) $4,050.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

66

Compute the investment to be recorded at the date of acquisition.

A) $1,750.

B) $1,755.

C) $1,725.

D) $1,760.

E) $1,765.

A) $1,750.

B) $1,755.

C) $1,725.

D) $1,760.

E) $1,765.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

67

Compute consolidated equipment (net) at the date of the acquisition.

A) $ 400.

B) $ 660.

C) $1,060.

D) $1,040.

E) $1,050.

A) $ 400.

B) $ 660.

C) $1,060.

D) $1,040.

E) $1,050.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

68

Compute consolidated land immediately following the acquisition.

A) $2,060.

B) $1,800.

C) $ 260.

D) $2,050.

E) $2,070.

A) $2,060.

B) $1,800.

C) $ 260.

D) $2,050.

E) $2,070.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

69

Compute consolidated goodwill immediately following the acquisition.

A) $440.

B) $442.

C) $450.

D) $455.

E) $452.

A) $440.

B) $442.

C) $450.

D) $455.

E) $452.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

70

Compute consolidated inventory immediately following the acquisition.

A) $1,650.

B) $1,810.

C) $1,230.

D) $ 580.

E) $1,830.

A) $1,650.

B) $1,810.

C) $1,230.

D) $ 580.

E) $1,830.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

71

Compute consolidated buildings (net) immediately following the acquisition.

A) $2,450.

B) $2,340.

C) $1,800.

D) $ 650.

E) $1,690.

A) $2,450.

B) $2,340.

C) $1,800.

D) $ 650.

E) $1,690.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

72

Compute the consolidated cash upon completion of the acquisition.

A) $1,350.

B) $1,110.

C) $1,080.

D) $1,085.

E) $ 635.

A) $1,350.

B) $1,110.

C) $1,080.

D) $1,085.

E) $ 635.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

73

Compute consolidated retained earnings as a result of this acquisition.

A) $1,160.

B) $1,170.

C) $1,265.

D) $1,280.

E) $1,650.

A) $1,160.

B) $1,170.

C) $1,265.

D) $1,280.

E) $1,650.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

74

Compute consolidated expenses immediately following the acquisition.

A) $2,735.

B) $2,760.

C) $2,770.

D) $2,785.

E) $3,380.

A) $2,735.

B) $2,760.

C) $2,770.

D) $2,785.

E) $3,380.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

75

By how much will Flynn's additional paid-in capital increase as a result of this acquisition?

A) $150,000.

B) $160,000.

C) $230,000.

D) $350,000.

E) $360,000.

A) $150,000.

B) $160,000.

C) $230,000.

D) $350,000.

E) $360,000.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

76

Compute consolidated long-term liabilities at the date of the acquisition.

A) $2,600.

B) $2,700.

C) $2,800.

D) $3,720.

E) $3,820.

A) $2,600.

B) $2,700.

C) $2,800.

D) $3,720.

E) $3,820.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

77

Compute consolidated retained earnings at the date of the acquisition.

A) $1,160.

B) $1,170.

C) $1,280.

D) $1,290.

E) $1,640.

A) $1,160.

B) $1,170.

C) $1,280.

D) $1,290.

E) $1,640.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

78

Compute consolidated buildings (net) at the date of the acquisition.

A) $2,450.

B) $2,340.

C) $1,800.

D) $ 650.

E) $1,690.

A) $2,450.

B) $2,340.

C) $1,800.

D) $ 650.

E) $1,690.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

79

Compute consolidated cash at the completion of the acquisition.

A) $1,350.

B) $1,085.

C) $1,110.

D) $ 870.

E) $ 845.

A) $1,350.

B) $1,085.

C) $1,110.

D) $ 870.

E) $ 845.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

80

Compute fair value of the net assets acquired at the date of the acquisition.

A) $1,300.

B) $1,340.

C) $1,500.

D) $1,750.

E) $2,480.

A) $1,300.

B) $1,340.

C) $1,500.

D) $1,750.

E) $2,480.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 116 flashcards in this deck.