Deck 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

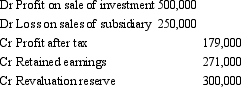

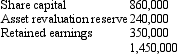

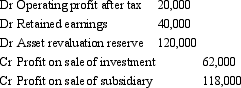

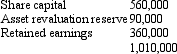

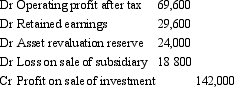

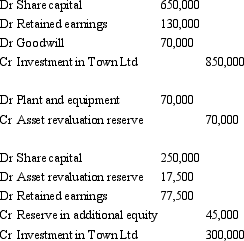

The following consolidation adjusting journal entries appeared at the end of a period in which the parent sold all of its shareholding in a subsidiary.It received $1,200,000 for the shares.  At the time of the sale of the shares,the parent was holding the investment in subsidiary at what amount,in its own books?

At the time of the sale of the shares,the parent was holding the investment in subsidiary at what amount,in its own books?

A) $450,000.

B) $700,000.

C) $950,000.

D) $1,450,000.

E) Cannot be determined from the information given.

At the time of the sale of the shares,the parent was holding the investment in subsidiary at what amount,in its own books?A) $450,000.

B) $700,000.

C) $950,000.

D) $1,450,000.

E) Cannot be determined from the information given.

Question

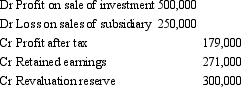

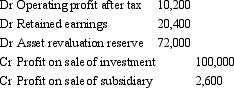

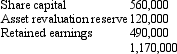

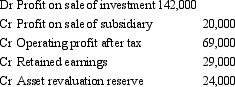

The following consolidation adjusting journal entries appeared at the end of a period in which the parent sold all of its shareholding in a subsidiary.It received $1,200,000 for the shares.  The amount of the share of post-acquisition profits and movements in equity balances,contributed to the group by the subsidiary,and attributable to the parent,is:

The amount of the share of post-acquisition profits and movements in equity balances,contributed to the group by the subsidiary,and attributable to the parent,is:

A) ($250,000).

B) $350,000.

C) $750,000.

D) $1,200,000.

E) Cannot be determined from the information given.

The amount of the share of post-acquisition profits and movements in equity balances,contributed to the group by the subsidiary,and attributable to the parent,is:A) ($250,000).

B) $350,000.

C) $750,000.

D) $1,200,000.

E) Cannot be determined from the information given.

Question

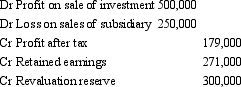

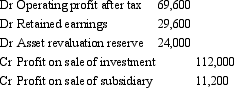

The following consolidation adjusting journal entries appeared at the end of a period in which the parent sold all of its shareholding in a subsidiary.It received $1,200,000 for the shares.  The 'Cr Profit after tax' entry above represents:

The 'Cr Profit after tax' entry above represents:

A) the profit made by the parent on the sale of the shares.

B) the profit made by the economic entity on the sale of the shares.

C) the amount accruing to the minority interest of the subsidiary.

D) the share of profits derived by the subsidiary for the entire current period.

E) the share of profits derived by the subsidiary in the current period, up to the time of divestment.

The 'Cr Profit after tax' entry above represents:A) the profit made by the parent on the sale of the shares.

B) the profit made by the economic entity on the sale of the shares.

C) the amount accruing to the minority interest of the subsidiary.

D) the share of profits derived by the subsidiary for the entire current period.

E) the share of profits derived by the subsidiary in the current period, up to the time of divestment.

Question

Question

Question

Question

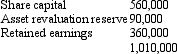

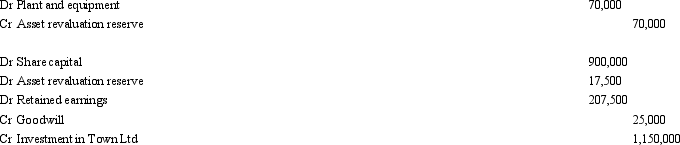

Fan Ltd acquired a 60 per cent interest in Dance Ltd on 1 July 2002 for a cash consideration of $780,000.At that date the fair value of the net assets of Dance Ltd was represented by:  On 30 June 2005 Fan Ltd sold all its shares in Dance Ltd for $880,000.At this date the fair value of the net assets of Dance Ltd was represented by:

On 30 June 2005 Fan Ltd sold all its shares in Dance Ltd for $880,000.At this date the fair value of the net assets of Dance Ltd was represented by:

The retained earnings of $350,000 include operating profit after tax of $20,000 from the current period.Impairment of goodwill was assessed at $5,400,the impairment having been incurred evenly across the last three years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

The retained earnings of $350,000 include operating profit after tax of $20,000 from the current period.Impairment of goodwill was assessed at $5,400,the impairment having been incurred evenly across the last three years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

A)

B)

C)

D)

E) None of the given answers.

On 30 June 2005 Fan Ltd sold all its shares in Dance Ltd for $880,000.At this date the fair value of the net assets of Dance Ltd was represented by: The retained earnings of $350,000 include operating profit after tax of $20,000 from the current period.Impairment of goodwill was assessed at $5,400,the impairment having been incurred evenly across the last three years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?A)

B)

C)

D)

E) None of the given answers.

Question

Question

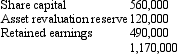

Fish Ltd acquired an 80 per cent interest in Chips Ltd on 1 July 2003 for a cash consideration of $838,000.At that date the fair value of the net assets of Chips Ltd was represented by:  On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by:

On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by:

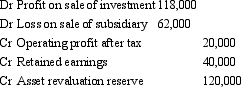

The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000.The investment has not been marked to market during the period that the shares were held.What is the amount of profit or loss on the sale of the shares recognised in the books of Fish Ltd during the period ended 30 June 2005?

The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000.The investment has not been marked to market during the period that the shares were held.What is the amount of profit or loss on the sale of the shares recognised in the books of Fish Ltd during the period ended 30 June 2005?

A) $14,000

B) $112,000

C) $20,000

D) $118,000

E) None of the given answers.

On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by: The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000.The investment has not been marked to market during the period that the shares were held.What is the amount of profit or loss on the sale of the shares recognised in the books of Fish Ltd during the period ended 30 June 2005?A) $14,000

B) $112,000

C) $20,000

D) $118,000

E) None of the given answers.

Question

Star Trek Ltd acquires shares in Vulcan Ltd at various stages summarised as follows:  Which of the following statements is not? in accordance with AASB 127 "Consolidated Financial Statements"?

Which of the following statements is not? in accordance with AASB 127 "Consolidated Financial Statements"?

A) Recognise goodwill (bargain gain on purchase) on the acquisition of shares purchased in 2010 and 2011 on consolidation of financial statements for the year 2010 and 2011, respectively, when Star Trek Ltd has control of Vulcan Ltd.

B) Recognise goodwill (bargain gain on purchase) on acquisition of shares made in 2010, when Star Trek Ltd ultimately gained control of the equity of Vulcan Ltd.

C) Difference between purchase consideration and net identifiable assets of Vulcan Ltd for share interests acquired in 2011 is taken to equity.

D) Star Trek Ltd should recognize goodwill using single-date method.

E) None of the given answers.

Which of the following statements is not? in accordance with AASB 127 "Consolidated Financial Statements"?A) Recognise goodwill (bargain gain on purchase) on the acquisition of shares purchased in 2010 and 2011 on consolidation of financial statements for the year 2010 and 2011, respectively, when Star Trek Ltd has control of Vulcan Ltd.

B) Recognise goodwill (bargain gain on purchase) on acquisition of shares made in 2010, when Star Trek Ltd ultimately gained control of the equity of Vulcan Ltd.

C) Difference between purchase consideration and net identifiable assets of Vulcan Ltd for share interests acquired in 2011 is taken to equity.

D) Star Trek Ltd should recognize goodwill using single-date method.

E) None of the given answers.

Question

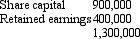

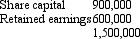

Hill Ltd acquired an 80 per cent interest in Dale Ltd on 1 July 2004 for a cash consideration of $1,200,000.At that date the shareholders' funds of Dale Ltd were:  The assets of Dale Ltd were recorded at fair value at the time of the purchase.

The assets of Dale Ltd were recorded at fair value at the time of the purchase.

On 1 July 2005 Hill Ltd purchased the remaining 20 per cent of the issued capital of Dale Ltd for a cash consideration of $336,000.At this date the fair value of the net assets of Dale Ltd were represented by:

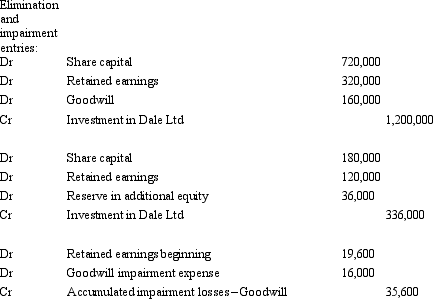

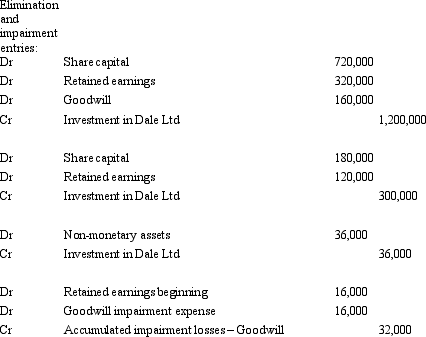

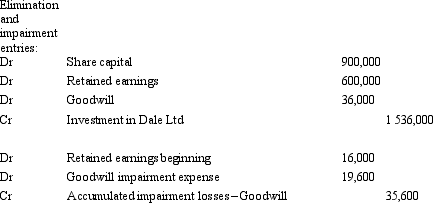

Impairment of goodwill amounted to $35,600; $16,000 of which related to the year ended 30 June 2006.There were no inter-company transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?

Impairment of goodwill amounted to $35,600; $16,000 of which related to the year ended 30 June 2006.There were no inter-company transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

The assets of Dale Ltd were recorded at fair value at the time of the purchase.On 1 July 2005 Hill Ltd purchased the remaining 20 per cent of the issued capital of Dale Ltd for a cash consideration of $336,000.At this date the fair value of the net assets of Dale Ltd were represented by:

Impairment of goodwill amounted to $35,600; $16,000 of which related to the year ended 30 June 2006.There were no inter-company transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Question

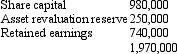

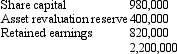

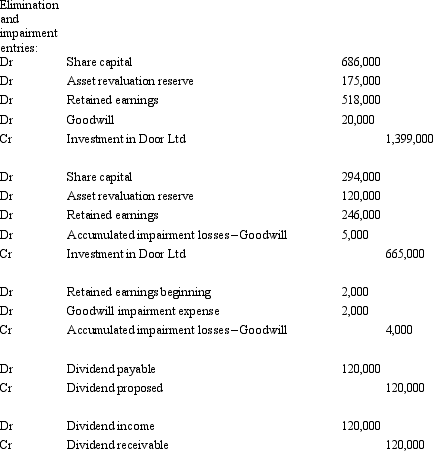

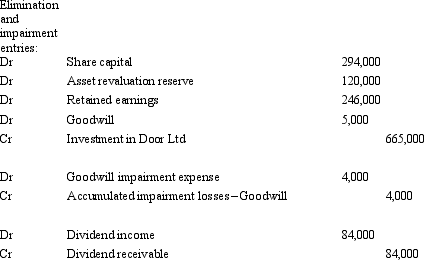

Window Ltd acquired a 70 per cent interest in Door Ltd on 1 July 2003 for a cash consideration of $1,399,000.At that date fair value of the net assets of Door Ltd were represented by:  On 1 July 2004 Window Ltd purchased a further 30 per cent of the issued capital of Door Ltd for cash consideration of $665,000.At this date the fair value of the net assets of Door Ltd were represented by:

On 1 July 2004 Window Ltd purchased a further 30 per cent of the issued capital of Door Ltd for cash consideration of $665,000.At this date the fair value of the net assets of Door Ltd were represented by:

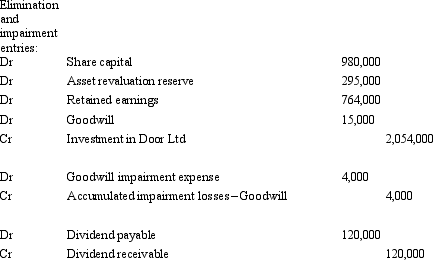

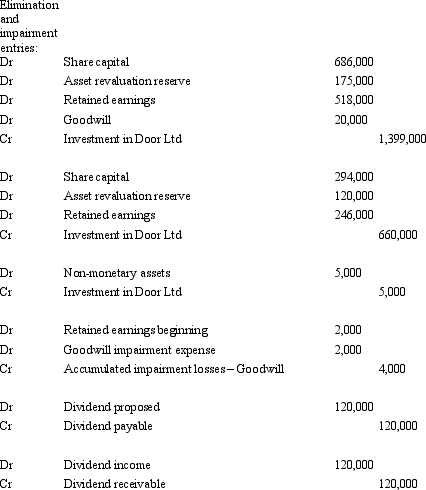

Impairment of goodwill was assessed at $4,000; relating evenly across each of the last two years.During the period ended 30 June 2005,Door Ltd proposed a dividend of $120,000.The dividend has not been paid at the end of the period,but Window Ltd has a policy of accruing the dividends of subsidiaries when they are proposed.There were no other intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary,account for goodwill and eliminate the dividends for the period ended 30 June 2005?

Impairment of goodwill was assessed at $4,000; relating evenly across each of the last two years.During the period ended 30 June 2005,Door Ltd proposed a dividend of $120,000.The dividend has not been paid at the end of the period,but Window Ltd has a policy of accruing the dividends of subsidiaries when they are proposed.There were no other intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary,account for goodwill and eliminate the dividends for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

On 1 July 2004 Window Ltd purchased a further 30 per cent of the issued capital of Door Ltd for cash consideration of $665,000.At this date the fair value of the net assets of Door Ltd were represented by: Impairment of goodwill was assessed at $4,000; relating evenly across each of the last two years.During the period ended 30 June 2005,Door Ltd proposed a dividend of $120,000.The dividend has not been paid at the end of the period,but Window Ltd has a policy of accruing the dividends of subsidiaries when they are proposed.There were no other intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary,account for goodwill and eliminate the dividends for the period ended 30 June 2005?A)

B)

C)

D)

E) None of the given answers.

Question

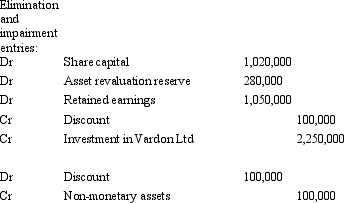

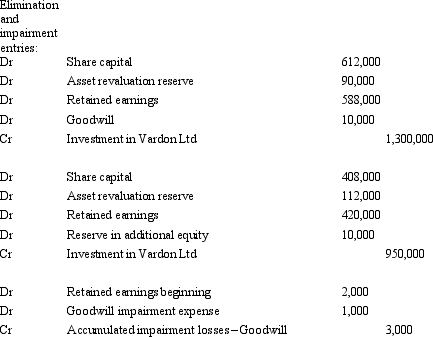

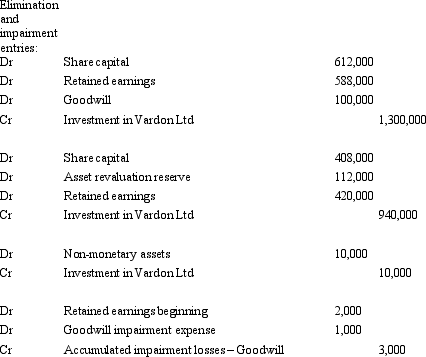

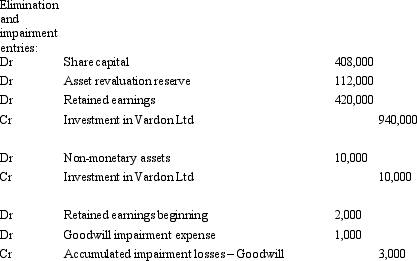

Dolly Ltd acquired a 60 per cent interest in Vardon Ltd on 1 July 2002 for a cash consideration of $1,300,000.At that date fair value of the net assets of Vardon Ltd were represented by:  On 1 July 2004 Dolly Ltd purchased the final 40 per cent of the issued capital of Vardon Ltd for cash consideration of $950,000.At this date the fair value of the net assets of Vardon Ltd were represented by:

On 1 July 2004 Dolly Ltd purchased the final 40 per cent of the issued capital of Vardon Ltd for cash consideration of $950,000.At this date the fair value of the net assets of Vardon Ltd were represented by:

Impairment of goodwill was assessed at $3,000; of which $2,000 related to the year ended 30 June 2005.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and amortise goodwill for the period ended 30 June 2006?

Impairment of goodwill was assessed at $3,000; of which $2,000 related to the year ended 30 June 2005.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and amortise goodwill for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

On 1 July 2004 Dolly Ltd purchased the final 40 per cent of the issued capital of Vardon Ltd for cash consideration of $950,000.At this date the fair value of the net assets of Vardon Ltd were represented by: Impairment of goodwill was assessed at $3,000; of which $2,000 related to the year ended 30 June 2005.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and amortise goodwill for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Fish Ltd acquired an 80 per cent interest in Chips Ltd on 1 July 2003 for a cash consideration of $838,000.At that date the fair value of the net assets of Chips Ltd was represented by:  On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by:

On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by:

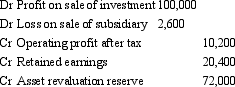

The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000,the impairment having been incurred evenly across the last two years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000,the impairment having been incurred evenly across the last two years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

A)

B)

C)

D)

E) None of the given answers.

On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by: The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000,the impairment having been incurred evenly across the last two years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?A)

B)

C)

D)

E) None of the given answers.

Question

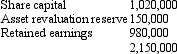

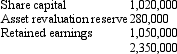

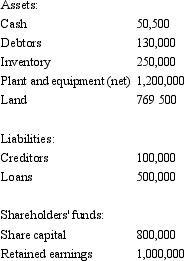

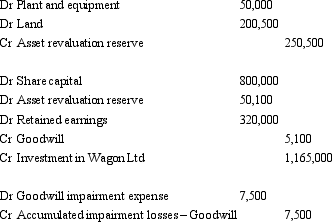

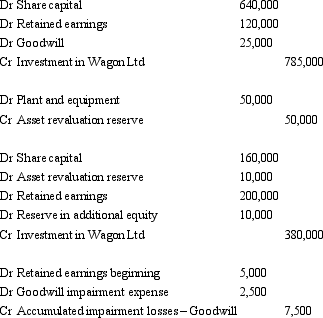

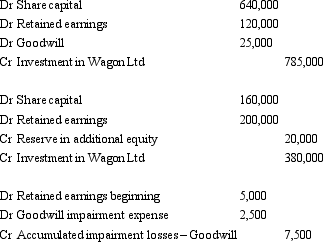

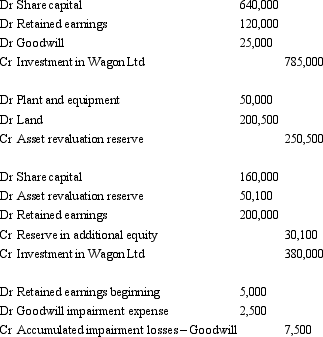

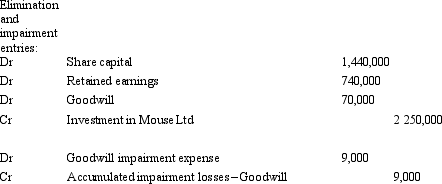

On 1 July 2004,Horse Ltd acquired 80 per cent of the issued capital of Wagon Ltd for $785,000 when the fair value of the net assets of Wagon Ltd was $950,000 (share capital $800,000 and retained earnings $150,000).On 30 June 2007 Horse Ltd purchased the final 20 per cent of Wagon's issued capital for $380,000.The net assets of Wagon Ltd were not stated at fair value in the accounts,which are summarised as follows:  The fair value of the plant and equipment is $1,250,000 and the land was valued at $970,000 at year end.Impairment of goodwill was assessed at $7,500,the impairment having been incurred evenly across the last three years.There were no intragroup transactions during the period.

The fair value of the plant and equipment is $1,250,000 and the land was valued at $970,000 at year end.Impairment of goodwill was assessed at $7,500,the impairment having been incurred evenly across the last three years.There were no intragroup transactions during the period.

What are the consolidation journal entries required for the period ended 30 June 2007? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

The fair value of the plant and equipment is $1,250,000 and the land was valued at $970,000 at year end.Impairment of goodwill was assessed at $7,500,the impairment having been incurred evenly across the last three years.There were no intragroup transactions during the period.What are the consolidation journal entries required for the period ended 30 June 2007? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

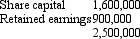

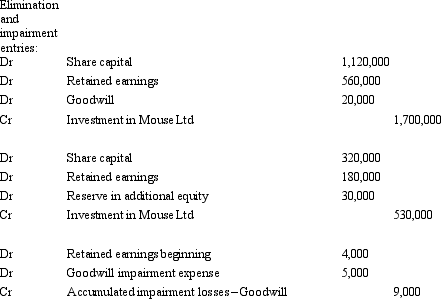

Mickey Ltd acquired a 70 per cent interest in Mouse Ltd on 1 July 2003 for a cash consideration of $1,700,000.At that date the shareholders' funds of Mouse Ltd were:  The assets of Mouse Ltd were recorded at fair value at the time of the purchase.

The assets of Mouse Ltd were recorded at fair value at the time of the purchase.

On 1 July 2005 Mickey Ltd purchased a further 20 per cent of the issued capital of Mouse Ltd for a cash consideration of $530,000.At this date the fair value of the net assets of Mouse Ltd were represented by:

Impairment of goodwill was assessed at $9,000; of which $5,000 relates to the current period.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?

Impairment of goodwill was assessed at $9,000; of which $5,000 relates to the current period.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

The assets of Mouse Ltd were recorded at fair value at the time of the purchase.On 1 July 2005 Mickey Ltd purchased a further 20 per cent of the issued capital of Mouse Ltd for a cash consideration of $530,000.At this date the fair value of the net assets of Mouse Ltd were represented by:

Impairment of goodwill was assessed at $9,000; of which $5,000 relates to the current period.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Question

Question

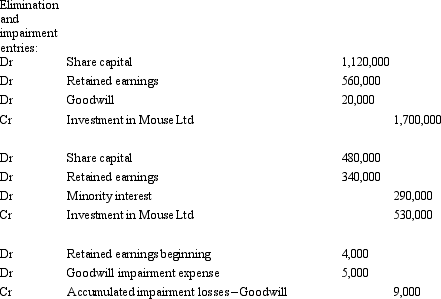

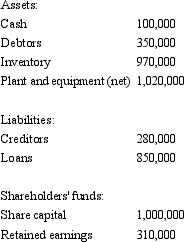

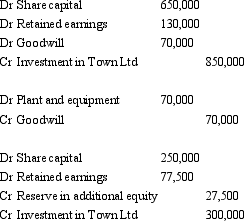

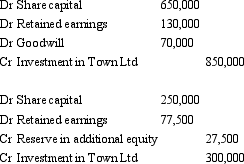

On 1 July 2002,City Ltd acquired 65 per cent of the issued capital of Town Ltd for $850,000 when the fair value of the net assets of Town Ltd was $1.2 million (share capital $1 million and retained earnings $0.2 million).On 30 June 2005 City Ltd purchased a further 25 per cent of Town's issued capital for $300,000.The net assets of Town Ltd were not stated at fair value in the accounts,which are summarised as follows:  The fair value of the plant and equipment is $1,090,000 at year end.Goodwill has been deemed not to have been impaired.There were no inter-company transactions during the period.

The fair value of the plant and equipment is $1,090,000 at year end.Goodwill has been deemed not to have been impaired.There were no inter-company transactions during the period.

What are the consolidation journal entries required for the period ended 30 June 2005? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

The fair value of the plant and equipment is $1,090,000 at year end.Goodwill has been deemed not to have been impaired.There were no inter-company transactions during the period.What are the consolidation journal entries required for the period ended 30 June 2005? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

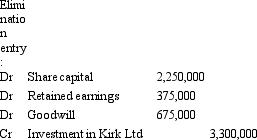

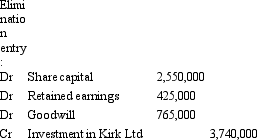

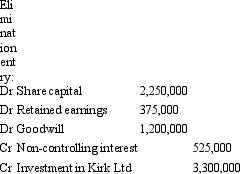

Spock Ltd acquired a 10 per cent holding in Kirk Ltd on 1 July 2011 for $350,000 cash,being the fair value of consideration transferred. On 30 June 2012,Spock Ltd acquired a further 75 per cent of the contributed capital of Kirk Ltd for $3,300,000,which represents the fair value of consideration transferred.After the latest acquisition,Spock Ltd gained control of Kirk Ltd.The fair value of the net assets acquired and the liabilities assumed of Kirk Ltd at the acquisition date of 30 June 2012 was $3,500,000 and all assets were recorded at far value in the financial statements of Kirk Ltd.

At that date fair value of the net assets of Kirk Ltd were represented by:

Goodwill is also attributed to the non-controlling interest.

Goodwill is also attributed to the non-controlling interest.

What is the consolidation entry to eliminate the investment in Kirk Ltd on consolidation for the financial year ended 30 June 2012?

A)

B)

C)

D)

E) None of the given answers.

At that date fair value of the net assets of Kirk Ltd were represented by:

Goodwill is also attributed to the non-controlling interest.What is the consolidation entry to eliminate the investment in Kirk Ltd on consolidation for the financial year ended 30 June 2012?

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/39

Play

Full screen (f)

Deck 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg

1

When a parent sells its interest in a subsidiary,any profit or loss generated by the subsidiary:

A) is transferred to the parent's investment in subsidiary account, and used to calculate the amount of profit or loss on the sale of the shares.

B) is immediately transferred to the equity section of the consolidated accounts, and is then available from distribution to shareholders.

C) is set off against any remaining balance in the goodwill on acquisition account, with any remaining amount distributed as dividends to the new owners.

D) is to be recorded in the consolidated financial statements for the period of the year that the parent had control of the subsidiary.

E) is to be recorded in the parent's financial statements for the period of the year that the parent had control of the subsidiary.

A) is transferred to the parent's investment in subsidiary account, and used to calculate the amount of profit or loss on the sale of the shares.

B) is immediately transferred to the equity section of the consolidated accounts, and is then available from distribution to shareholders.

C) is set off against any remaining balance in the goodwill on acquisition account, with any remaining amount distributed as dividends to the new owners.

D) is to be recorded in the consolidated financial statements for the period of the year that the parent had control of the subsidiary.

E) is to be recorded in the parent's financial statements for the period of the year that the parent had control of the subsidiary.

D

2

AASB 127 "Consolidated and Separate Financial Statements" prescribes that changes in the parent's ownership interest in a subsidiary that do not result in a loss of control are accounted for as equity transactions.

True

3

Under the step-by-step method,the need to revalue the subsidiary's assets,liabilities and contingent liabilities to fair value at each acquisition date,is not an indication that the acquirer has elected to apply the revaluation method for measuring assets,such as that prescribed by AASB 116:

True

4

Additional purchases of shares in a subsidiary should be accounted for by the combined tranche method,according to AASB 3:

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

5

Under the single-date method,goodwill would be recognised.

A) at the point in time when the parent entity ultimately gains control of the subsidiary.

B) at the time when each additional acquisition of shares is made.

C) as part of equity in the parent's books.

D) at the point in time when the subsidiary shareholders acknowledge that they will sell their shareholdings to the parent entity.

E) None of the given answers.

A) at the point in time when the parent entity ultimately gains control of the subsidiary.

B) at the time when each additional acquisition of shares is made.

C) as part of equity in the parent's books.

D) at the point in time when the subsidiary shareholders acknowledge that they will sell their shareholdings to the parent entity.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

6

Under the step-by-step method,the aggregate costs of the investments would be eliminated against the parent's share of capital and reserves at the date control of the subsidiary has been ultimately established and only one amount of goodwill (or bargain gain on purchase)is calculated.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

7

Control over a subsidiary may be lost without a change in absolute or relative ownership levels.An example of this is loss of control to a court administrator as a result of bankruptcy.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

8

The profit or loss on the sale of shares in a controlled entity will be the same in the parent entity's legal books as it is in the consolidated accounts:

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

9

The required method (according to AASB 3)of accounting for the acquisition of additional shares in a subsidiary is the single-date method.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

10

The consolidated balance sheet at year-end,in a period when the parent sold its interests in a subsidiary:

A) includes the assets and liabilities of the former subsidiary, to ensure that the opening balances reconcile.

B) does not include the assets and liabilities of the former subsidiary, if the subsidiary is no longer controlled by the parent.

C) reports the investment account at cost less proceeds of the sale.

D) includes the assets and liabilities of the former subsidiary, proportionately adjusted for the proceeds of sale.

E) None of the given answers.

A) includes the assets and liabilities of the former subsidiary, to ensure that the opening balances reconcile.

B) does not include the assets and liabilities of the former subsidiary, if the subsidiary is no longer controlled by the parent.

C) reports the investment account at cost less proceeds of the sale.

D) includes the assets and liabilities of the former subsidiary, proportionately adjusted for the proceeds of sale.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

11

In calculating the profit or loss on the sale of shares in a controlled entity that is to be included in the group accounts,consideration should be given to the share of post-acquisition profits and movements in reserves that have been recognised.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

12

Where a parent entity with a controlling interest in a subsidiary obtains additional equity,the carrying amounts of the controlling and non-controlling interests should be adjusted to reflect the changes in their relative interests in the subsidiary.Any difference between the fair value paid and the carrying amount of the additional interest acquired is recognised directly in profit or loss of the parent entity.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

13

Two common approaches to accounting for acquisition of additional shares in a subsidiary include:

A) The combined tranche method and the single-date method.

B) The step-by-step method and the combined tranche method.

C) The step-by-step method and the single-date method.

D) The step-by-step method and the equity method.

E) The equity method and the single-date method.

A) The combined tranche method and the single-date method.

B) The step-by-step method and the combined tranche method.

C) The step-by-step method and the single-date method.

D) The step-by-step method and the equity method.

E) The equity method and the single-date method.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

14

In a business combination achieved in stages,the acquirer shall re-measure its previously held equity interest in the acquiree at its acquisition-date fair value and recognise the resulting gain or loss,if any,in equity.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

15

The following consolidation adjusting journal entries appeared at the end of a period in which the parent sold all of its shareholding in a subsidiary.It received $1,200,000 for the shares. At the time of the sale of the shares,the parent was holding the investment in subsidiary at what amount,in its own books?

A) $450,000.

B) $700,000.

C) $950,000.

D) $1,450,000.

E) Cannot be determined from the information given.

At the time of the sale of the shares,the parent was holding the investment in subsidiary at what amount,in its own books?A) $450,000.

B) $700,000.

C) $950,000.

D) $1,450,000.

E) Cannot be determined from the information given.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

16

The following consolidation adjusting journal entries appeared at the end of a period in which the parent sold all of its shareholding in a subsidiary.It received $1,200,000 for the shares. The amount of the share of post-acquisition profits and movements in equity balances,contributed to the group by the subsidiary,and attributable to the parent,is:

A) ($250,000).

B) $350,000.

C) $750,000.

D) $1,200,000.

E) Cannot be determined from the information given.

The amount of the share of post-acquisition profits and movements in equity balances,contributed to the group by the subsidiary,and attributable to the parent,is:A) ($250,000).

B) $350,000.

C) $750,000.

D) $1,200,000.

E) Cannot be determined from the information given.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

17

The following consolidation adjusting journal entries appeared at the end of a period in which the parent sold all of its shareholding in a subsidiary.It received $1,200,000 for the shares. The 'Cr Profit after tax' entry above represents:

A) the profit made by the parent on the sale of the shares.

B) the profit made by the economic entity on the sale of the shares.

C) the amount accruing to the minority interest of the subsidiary.

D) the share of profits derived by the subsidiary for the entire current period.

E) the share of profits derived by the subsidiary in the current period, up to the time of divestment.

The 'Cr Profit after tax' entry above represents:A) the profit made by the parent on the sale of the shares.

B) the profit made by the economic entity on the sale of the shares.

C) the amount accruing to the minority interest of the subsidiary.

D) the share of profits derived by the subsidiary for the entire current period.

E) the share of profits derived by the subsidiary in the current period, up to the time of divestment.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

18

When shares in a subsidiary are sold during a period,any income and expenses recorded in the consolidated accounts that relate to the subsidiary,are eliminated.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

19

When additional shares in a subsidiary are acquired,AASB 3 requires each acquisition to be accounted for separately:

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

20

Once control over a subsidiary has been lost,the parent entity must derecognise the individual assets,liabilities and equity including any non-controlling interest relating to that subsidiary.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

21

Fan Ltd acquired a 60 per cent interest in Dance Ltd on 1 July 2002 for a cash consideration of $780,000.At that date the fair value of the net assets of Dance Ltd was represented by: On 30 June 2005 Fan Ltd sold all its shares in Dance Ltd for $880,000.At this date the fair value of the net assets of Dance Ltd was represented by:

The retained earnings of $350,000 include operating profit after tax of $20,000 from the current period.Impairment of goodwill was assessed at $5,400,the impairment having been incurred evenly across the last three years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

A)

B)

C)

D)

E) None of the given answers.

On 30 June 2005 Fan Ltd sold all its shares in Dance Ltd for $880,000.At this date the fair value of the net assets of Dance Ltd was represented by: The retained earnings of $350,000 include operating profit after tax of $20,000 from the current period.Impairment of goodwill was assessed at $5,400,the impairment having been incurred evenly across the last three years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

22

AASB 3 specifies that where a parent entity purchases additional shares in a subsidiary over time:

A) No further goodwill on purchase may be recognised. Any excess payment over the fair value of the additional net assets purchased is to be written off in the period of the purchase.

B) Each purchase of shares is to be treated as part of a single, combined purchase so that the amount of goodwill reported in the consolidated financial statements cannot be increased at the discretion of the controlling entity.

C) Goodwill would be recognised by a single consolidation journal entry at that point in time when the parent entity ultimately gains control of the subsidiary.

D) The parent entity may choose between treating the purchases separately or combining them into a single transaction.

E) None of the given answers.

A) No further goodwill on purchase may be recognised. Any excess payment over the fair value of the additional net assets purchased is to be written off in the period of the purchase.

B) Each purchase of shares is to be treated as part of a single, combined purchase so that the amount of goodwill reported in the consolidated financial statements cannot be increased at the discretion of the controlling entity.

C) Goodwill would be recognised by a single consolidation journal entry at that point in time when the parent entity ultimately gains control of the subsidiary.

D) The parent entity may choose between treating the purchases separately or combining them into a single transaction.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

23

Fish Ltd acquired an 80 per cent interest in Chips Ltd on 1 July 2003 for a cash consideration of $838,000.At that date the fair value of the net assets of Chips Ltd was represented by: On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by:

The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000.The investment has not been marked to market during the period that the shares were held.What is the amount of profit or loss on the sale of the shares recognised in the books of Fish Ltd during the period ended 30 June 2005?

A) $14,000

B) $112,000

C) $20,000

D) $118,000

E) None of the given answers.

On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by: The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000.The investment has not been marked to market during the period that the shares were held.What is the amount of profit or loss on the sale of the shares recognised in the books of Fish Ltd during the period ended 30 June 2005?A) $14,000

B) $112,000

C) $20,000

D) $118,000

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

24

Star Trek Ltd acquires shares in Vulcan Ltd at various stages summarised as follows: Which of the following statements is not? in accordance with AASB 127 "Consolidated Financial Statements"?

A) Recognise goodwill (bargain gain on purchase) on the acquisition of shares purchased in 2010 and 2011 on consolidation of financial statements for the year 2010 and 2011, respectively, when Star Trek Ltd has control of Vulcan Ltd.

B) Recognise goodwill (bargain gain on purchase) on acquisition of shares made in 2010, when Star Trek Ltd ultimately gained control of the equity of Vulcan Ltd.

C) Difference between purchase consideration and net identifiable assets of Vulcan Ltd for share interests acquired in 2011 is taken to equity.

D) Star Trek Ltd should recognize goodwill using single-date method.

E) None of the given answers.

Which of the following statements is not? in accordance with AASB 127 "Consolidated Financial Statements"?A) Recognise goodwill (bargain gain on purchase) on the acquisition of shares purchased in 2010 and 2011 on consolidation of financial statements for the year 2010 and 2011, respectively, when Star Trek Ltd has control of Vulcan Ltd.

B) Recognise goodwill (bargain gain on purchase) on acquisition of shares made in 2010, when Star Trek Ltd ultimately gained control of the equity of Vulcan Ltd.

C) Difference between purchase consideration and net identifiable assets of Vulcan Ltd for share interests acquired in 2011 is taken to equity.

D) Star Trek Ltd should recognize goodwill using single-date method.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

25

Hill Ltd acquired an 80 per cent interest in Dale Ltd on 1 July 2004 for a cash consideration of $1,200,000.At that date the shareholders' funds of Dale Ltd were: The assets of Dale Ltd were recorded at fair value at the time of the purchase.

On 1 July 2005 Hill Ltd purchased the remaining 20 per cent of the issued capital of Dale Ltd for a cash consideration of $336,000.At this date the fair value of the net assets of Dale Ltd were represented by:

Impairment of goodwill amounted to $35,600; $16,000 of which related to the year ended 30 June 2006.There were no inter-company transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

The assets of Dale Ltd were recorded at fair value at the time of the purchase.On 1 July 2005 Hill Ltd purchased the remaining 20 per cent of the issued capital of Dale Ltd for a cash consideration of $336,000.At this date the fair value of the net assets of Dale Ltd were represented by:

Impairment of goodwill amounted to $35,600; $16,000 of which related to the year ended 30 June 2006.There were no inter-company transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

26

Window Ltd acquired a 70 per cent interest in Door Ltd on 1 July 2003 for a cash consideration of $1,399,000.At that date fair value of the net assets of Door Ltd were represented by: On 1 July 2004 Window Ltd purchased a further 30 per cent of the issued capital of Door Ltd for cash consideration of $665,000.At this date the fair value of the net assets of Door Ltd were represented by:

Impairment of goodwill was assessed at $4,000; relating evenly across each of the last two years.During the period ended 30 June 2005,Door Ltd proposed a dividend of $120,000.The dividend has not been paid at the end of the period,but Window Ltd has a policy of accruing the dividends of subsidiaries when they are proposed.There were no other intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary,account for goodwill and eliminate the dividends for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

On 1 July 2004 Window Ltd purchased a further 30 per cent of the issued capital of Door Ltd for cash consideration of $665,000.At this date the fair value of the net assets of Door Ltd were represented by: Impairment of goodwill was assessed at $4,000; relating evenly across each of the last two years.During the period ended 30 June 2005,Door Ltd proposed a dividend of $120,000.The dividend has not been paid at the end of the period,but Window Ltd has a policy of accruing the dividends of subsidiaries when they are proposed.There were no other intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary,account for goodwill and eliminate the dividends for the period ended 30 June 2005?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

27

Dolly Ltd acquired a 60 per cent interest in Vardon Ltd on 1 July 2002 for a cash consideration of $1,300,000.At that date fair value of the net assets of Vardon Ltd were represented by: On 1 July 2004 Dolly Ltd purchased the final 40 per cent of the issued capital of Vardon Ltd for cash consideration of $950,000.At this date the fair value of the net assets of Vardon Ltd were represented by:

Impairment of goodwill was assessed at $3,000; of which $2,000 related to the year ended 30 June 2005.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and amortise goodwill for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

On 1 July 2004 Dolly Ltd purchased the final 40 per cent of the issued capital of Vardon Ltd for cash consideration of $950,000.At this date the fair value of the net assets of Vardon Ltd were represented by: Impairment of goodwill was assessed at $3,000; of which $2,000 related to the year ended 30 June 2005.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and amortise goodwill for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

28

An immediate parent entity may purchase shares in its subsidiary in separate transactions with long periods of time between transactions.It is possible that one transaction may give rise to goodwill on consolidation and another to an excess.How would the excess on consolidation be calculated and treated in the consolidated accounts?

A) The difference between the fair value of the total consideration paid in all transactions to date should be compared to the proportion of the fair value of the net assets of the subsidiary as at the last purchase date. An excess arises where the consideration is less than the share of the fair value of the net assets purchased. The excess should be eliminated pro-rata against the subsidiary's monetary items. Where the excess is greater than the amount of non-monetary items the balance should be eliminated against the non-monetary assets of the subsidiary.

B) The difference between the fair value of the consideration paid for the shares and the fair value of the proportion of net assets acquired in each transaction should be calculated separately. An excess arises where the consideration is less than the share of the fair value of the net assets purchased. The excess should be recognised as revenue.

C) The difference between the value of the total consideration paid in all transactions to date should be compared to the proportion of the book value of the net assets of the subsidiary as at the last purchase date. An excess arises where the consideration is less than the share of the fair value of the net assets purchased. The excess should be amortised over a period of not greater than 10 years.

D) The difference between the fair value of the consideration paid for the shares and the fair value of the proportion of net assets acquired in each transaction should be calculated. While the Standard does not permit goodwill to be recognised on a purchase of further shares after control has been achieved, an excess will be recognised if the consideration is less than the share of the fair value of the net assets purchased. The excess should be eliminated pro-rata against the subsidiary's monetary items. The excess should be amortised over a period of not greater than 10 years.

E) None of the given answers.

A) The difference between the fair value of the total consideration paid in all transactions to date should be compared to the proportion of the fair value of the net assets of the subsidiary as at the last purchase date. An excess arises where the consideration is less than the share of the fair value of the net assets purchased. The excess should be eliminated pro-rata against the subsidiary's monetary items. Where the excess is greater than the amount of non-monetary items the balance should be eliminated against the non-monetary assets of the subsidiary.

B) The difference between the fair value of the consideration paid for the shares and the fair value of the proportion of net assets acquired in each transaction should be calculated separately. An excess arises where the consideration is less than the share of the fair value of the net assets purchased. The excess should be recognised as revenue.

C) The difference between the value of the total consideration paid in all transactions to date should be compared to the proportion of the book value of the net assets of the subsidiary as at the last purchase date. An excess arises where the consideration is less than the share of the fair value of the net assets purchased. The excess should be amortised over a period of not greater than 10 years.

D) The difference between the fair value of the consideration paid for the shares and the fair value of the proportion of net assets acquired in each transaction should be calculated. While the Standard does not permit goodwill to be recognised on a purchase of further shares after control has been achieved, an excess will be recognised if the consideration is less than the share of the fair value of the net assets purchased. The excess should be eliminated pro-rata against the subsidiary's monetary items. The excess should be amortised over a period of not greater than 10 years.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following statements is in accordance with AASB 127 "Consolidated Financial Statements" with respect to multiple acquisitions?

A) Each individual investment in the subsidiary is accounted for separately and separate consolidation worksheet entries are made to eliminate each investment on consolidation.

B) Once control of the subsidiary is established, consolidation worksheet entries will eliminate the parent entity's respective share of the subsidiary's net identifiable assets as at each of the respective investment dates (at fair value).

C) The aggregate costs of the investments would be eliminated against the parent's share of capital and reserves at the date when control is ultimately established and only one amount of goodwill (or bargain gain on purchase) is calculated.

D) Because eliminations of each investment are made at the various investment dates, there is a need to calculate a separate amount of goodwill (bargain gain on purchase) for each investment date.

E) All of the given answers.

A) Each individual investment in the subsidiary is accounted for separately and separate consolidation worksheet entries are made to eliminate each investment on consolidation.

B) Once control of the subsidiary is established, consolidation worksheet entries will eliminate the parent entity's respective share of the subsidiary's net identifiable assets as at each of the respective investment dates (at fair value).

C) The aggregate costs of the investments would be eliminated against the parent's share of capital and reserves at the date when control is ultimately established and only one amount of goodwill (or bargain gain on purchase) is calculated.

D) Because eliminations of each investment are made at the various investment dates, there is a need to calculate a separate amount of goodwill (bargain gain on purchase) for each investment date.

E) All of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

30

Fish Ltd acquired an 80 per cent interest in Chips Ltd on 1 July 2003 for a cash consideration of $838,000.At that date the fair value of the net assets of Chips Ltd was represented by: On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by:

The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000,the impairment having been incurred evenly across the last two years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

A)

B)

C)

D)

E) None of the given answers.

On 30 June 2005 Fish Ltd sold all its shares in Chips Ltd for $950,000.At this date the fair value of the net assets of Chips Ltd was represented by: The retained earnings of $490,000 includes operating profit after tax of $90,000 from the current period.Impairment of goodwill was assessed at $6,000,the impairment having been incurred evenly across the last two years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

31

On 1 July 2004,Horse Ltd acquired 80 per cent of the issued capital of Wagon Ltd for $785,000 when the fair value of the net assets of Wagon Ltd was $950,000 (share capital $800,000 and retained earnings $150,000).On 30 June 2007 Horse Ltd purchased the final 20 per cent of Wagon's issued capital for $380,000.The net assets of Wagon Ltd were not stated at fair value in the accounts,which are summarised as follows: The fair value of the plant and equipment is $1,250,000 and the land was valued at $970,000 at year end.Impairment of goodwill was assessed at $7,500,the impairment having been incurred evenly across the last three years.There were no intragroup transactions during the period.

What are the consolidation journal entries required for the period ended 30 June 2007? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

The fair value of the plant and equipment is $1,250,000 and the land was valued at $970,000 at year end.Impairment of goodwill was assessed at $7,500,the impairment having been incurred evenly across the last three years.There were no intragroup transactions during the period.What are the consolidation journal entries required for the period ended 30 June 2007? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is not a reason for a parent to lose control of a subsidiary?

A) Where the subsidiary issues additional shares to parties other than the parent.

B) Where the subsidiary issues bonus shares on a pro-rata basis.

C) When the parent makes a decision to sell its controlling interest in the subsidiary to another party.

D) Where the subsidiary issues additional shares to parties other than the parent.

E) The subsidiary becoming subject to the control of a government regulator.

A) Where the subsidiary issues additional shares to parties other than the parent.

B) Where the subsidiary issues bonus shares on a pro-rata basis.

C) When the parent makes a decision to sell its controlling interest in the subsidiary to another party.

D) Where the subsidiary issues additional shares to parties other than the parent.

E) The subsidiary becoming subject to the control of a government regulator.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

33

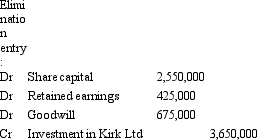

Spock Ltd acquired a 10 per cent holding in Kirk Ltd on 1 July 2011 for $350,000 cash,being the fair value of consideration transferred. On 30 June 2012,Spock Ltd acquired a further 75 per cent of the contributed capital of Kirk Ltd for $3,300,000,which represents the fair value of consideration transferred.After the latest acquisition,Spock Ltd gained control of Kirk Ltd.The fair value of the net assets acquired and the liabilities assumed of Kirk Ltd at the acquisition date of 30 June 2012 was $3,500,000 and all assets were recorded at far value in the financial statements of Kirk Ltd.

Goodwill is also attributed to the non-controlling interest.

Based on the above information,which of the following accounting treatments is not in accordance with AASB 127?

A) Goodwill on acquisition of Kirk Ltd to be eliminated on consolidation is $765,000.

B) Gain on acquisition of additional investment in Kirk Ltd to be recognised in 2012 is $90,000.

C) Non-controlling interest in Kirk Ltd on 30 June 2012 is $660,000.

D) Investment in Kirk Ltd to be eliminated on 30 June 2012 is $3,740,000.

E) None of the given answers.

Goodwill is also attributed to the non-controlling interest.

Based on the above information,which of the following accounting treatments is not in accordance with AASB 127?

A) Goodwill on acquisition of Kirk Ltd to be eliminated on consolidation is $765,000.

B) Gain on acquisition of additional investment in Kirk Ltd to be recognised in 2012 is $90,000.

C) Non-controlling interest in Kirk Ltd on 30 June 2012 is $660,000.

D) Investment in Kirk Ltd to be eliminated on 30 June 2012 is $3,740,000.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

34

Mickey Ltd acquired a 70 per cent interest in Mouse Ltd on 1 July 2003 for a cash consideration of $1,700,000.At that date the shareholders' funds of Mouse Ltd were: The assets of Mouse Ltd were recorded at fair value at the time of the purchase.

On 1 July 2005 Mickey Ltd purchased a further 20 per cent of the issued capital of Mouse Ltd for a cash consideration of $530,000.At this date the fair value of the net assets of Mouse Ltd were represented by:

Impairment of goodwill was assessed at $9,000; of which $5,000 relates to the current period.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

The assets of Mouse Ltd were recorded at fair value at the time of the purchase.On 1 July 2005 Mickey Ltd purchased a further 20 per cent of the issued capital of Mouse Ltd for a cash consideration of $530,000.At this date the fair value of the net assets of Mouse Ltd were represented by:

Impairment of goodwill was assessed at $9,000; of which $5,000 relates to the current period.There were no intragroup transactions.What are the consolidation entries to eliminate the investment in the subsidiary and account for goodwill for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

35

The profit or loss on the sale of shares in a subsidiary will be reported in both the books of the parent legal entity and the consolidated accounts.The method of calculating the profit or loss in the parent's individual legal entity books is to:

A) Revalue the investment in the subsidiary by adjusting that amount for operating profits recognised in the group accounts over the life of the holding of the shares. The adjusted amount is then compared to the consideration received for the shares and the profit or loss calculated as the difference.

B) The investment in the subsidiary may be recognised in the accounts at either cost or fair value. If it is at cost the amount should be revalued by reference to the last quoted price on the stock exchange. A revaluation difference will be taken to an asset revaluation reserve if it is an increase in value, or written off in the income statement if it is a decrease in value. Any remaining difference between the consideration received and the revalued investment is recognised as a profit or loss in the period of the sale.

C) The profit or loss recognised in the income statement is calculated as the difference between the consideration received and the book value of the investment at the time of sale. The book value may have been fair value or it may be at cost.

D) The investment recorded in the books of the parent entity is first adjusted for any amount of purchased goodwill amortised over the period that the shares have been held, by netting the accumulated amortisation against the investment. The adjusted amount is compared to the consideration received for the shares and where the amount received is greater than the adjusted investment a profit is recognised in the income statement. A loss is recognised in the alternative case, where the consideration is less than the adjusted investment.

E) None of the given answers.

A) Revalue the investment in the subsidiary by adjusting that amount for operating profits recognised in the group accounts over the life of the holding of the shares. The adjusted amount is then compared to the consideration received for the shares and the profit or loss calculated as the difference.

B) The investment in the subsidiary may be recognised in the accounts at either cost or fair value. If it is at cost the amount should be revalued by reference to the last quoted price on the stock exchange. A revaluation difference will be taken to an asset revaluation reserve if it is an increase in value, or written off in the income statement if it is a decrease in value. Any remaining difference between the consideration received and the revalued investment is recognised as a profit or loss in the period of the sale.

C) The profit or loss recognised in the income statement is calculated as the difference between the consideration received and the book value of the investment at the time of sale. The book value may have been fair value or it may be at cost.

D) The investment recorded in the books of the parent entity is first adjusted for any amount of purchased goodwill amortised over the period that the shares have been held, by netting the accumulated amortisation against the investment. The adjusted amount is compared to the consideration received for the shares and where the amount received is greater than the adjusted investment a profit is recognised in the income statement. A loss is recognised in the alternative case, where the consideration is less than the adjusted investment.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

36

On 1 July 2002,City Ltd acquired 65 per cent of the issued capital of Town Ltd for $850,000 when the fair value of the net assets of Town Ltd was $1.2 million (share capital $1 million and retained earnings $0.2 million).On 30 June 2005 City Ltd purchased a further 25 per cent of Town's issued capital for $300,000.The net assets of Town Ltd were not stated at fair value in the accounts,which are summarised as follows: The fair value of the plant and equipment is $1,090,000 at year end.Goodwill has been deemed not to have been impaired.There were no inter-company transactions during the period.

What are the consolidation journal entries required for the period ended 30 June 2005? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

The fair value of the plant and equipment is $1,090,000 at year end.Goodwill has been deemed not to have been impaired.There were no inter-company transactions during the period.What are the consolidation journal entries required for the period ended 30 June 2005? (Ignore the tax effect of the revaluation)

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

37

The profit or loss on the sale of shares in a subsidiary will be reported in the books of both the parent legal entity and the consolidated accounts.The method of calculating the profit or loss in the consolidated accounts is to:

A) Deduct the remaining balance of goodwill (after accumulated amortisation) from the investment balance and the difference between that and the consideration received is the profit or loss as recognised by the group. The profit or loss is recognised as part of an elimination entry that removes the investment, balance of goodwill and the investment.

B) Adjust the amount of the cost of the investment in the subsidiary by adding the parent's share of post-acquisition movements in retained earnings and reserves, and subtracting accumulated goodwill impairment. This figure is then subtracted from the consideration received.

C) Calculate, from the perspective of the group, the profit or loss on sale of the shares in a controlled company as the difference between the investment and the consideration received. This will only require an elimination entry when the parent entity has revalued the investment in its own books. In this case the revaluation should be reversed in the elimination entry and the profit or loss recognised by crediting the investment and debiting the assets contributed as payment in consideration for the shares.

D) Adjust the investment held in the subsidiary by deducting any asset revaluation reserves and then calculating the difference between the adjusted investment and the consideration received. The elimination entry will remove the equity items of the subsidiary against the investment and recognise the profit or loss by debiting the consideration received against the fair value of the net assets of the subsidiary at the time of sale.

E) None of the given answers.

A) Deduct the remaining balance of goodwill (after accumulated amortisation) from the investment balance and the difference between that and the consideration received is the profit or loss as recognised by the group. The profit or loss is recognised as part of an elimination entry that removes the investment, balance of goodwill and the investment.

B) Adjust the amount of the cost of the investment in the subsidiary by adding the parent's share of post-acquisition movements in retained earnings and reserves, and subtracting accumulated goodwill impairment. This figure is then subtracted from the consideration received.

C) Calculate, from the perspective of the group, the profit or loss on sale of the shares in a controlled company as the difference between the investment and the consideration received. This will only require an elimination entry when the parent entity has revalued the investment in its own books. In this case the revaluation should be reversed in the elimination entry and the profit or loss recognised by crediting the investment and debiting the assets contributed as payment in consideration for the shares.

D) Adjust the investment held in the subsidiary by deducting any asset revaluation reserves and then calculating the difference between the adjusted investment and the consideration received. The elimination entry will remove the equity items of the subsidiary against the investment and recognise the profit or loss by debiting the consideration received against the fair value of the net assets of the subsidiary at the time of sale.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is not a reason for a parent to lose control of a subsidiary?

A) When the parent makes a decision to sell its controlling interest in the subsidiary to another party.

B) Where the subsidiary issues additional shares to parties other than the parent.

C) The expiry of a contractual agreement that previously permitted the parent entity to control a subsidiary.

D) The subsidiary becoming subject to the control of a voluntary administrator due to bankruptcy.

E) None of the given answers.

A) When the parent makes a decision to sell its controlling interest in the subsidiary to another party.

B) Where the subsidiary issues additional shares to parties other than the parent.

C) The expiry of a contractual agreement that previously permitted the parent entity to control a subsidiary.

D) The subsidiary becoming subject to the control of a voluntary administrator due to bankruptcy.

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

39

Spock Ltd acquired a 10 per cent holding in Kirk Ltd on 1 July 2011 for $350,000 cash,being the fair value of consideration transferred. On 30 June 2012,Spock Ltd acquired a further 75 per cent of the contributed capital of Kirk Ltd for $3,300,000,which represents the fair value of consideration transferred.After the latest acquisition,Spock Ltd gained control of Kirk Ltd.The fair value of the net assets acquired and the liabilities assumed of Kirk Ltd at the acquisition date of 30 June 2012 was $3,500,000 and all assets were recorded at far value in the financial statements of Kirk Ltd.

At that date fair value of the net assets of Kirk Ltd were represented by:

Goodwill is also attributed to the non-controlling interest.

What is the consolidation entry to eliminate the investment in Kirk Ltd on consolidation for the financial year ended 30 June 2012?

A)

B)

C)

D)

E) None of the given answers.

At that date fair value of the net assets of Kirk Ltd were represented by:

Goodwill is also attributed to the non-controlling interest.What is the consolidation entry to eliminate the investment in Kirk Ltd on consolidation for the financial year ended 30 June 2012?

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 39 flashcards in this deck.