Deck 30: Further Consolidation Issues II: Accounting for Minority Interests

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

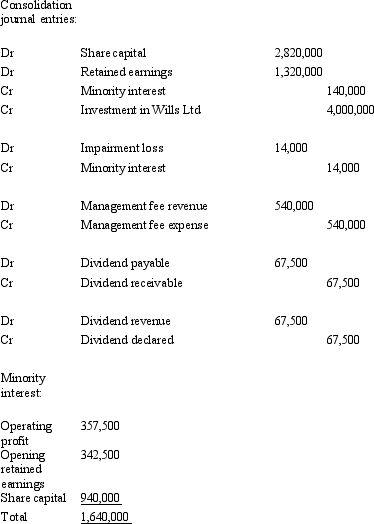

Finger Ltd purchased 75 per cent of the issued capital and in the process gained control over Nail Ltd on 1 July 2003.The fair value of the net assets of Nail Ltd at purchase was represented by:  Finger Ltd paid cash consideration of $4,000,000 for Nail Ltd.During the period ended 30 June 2005,Nail Ltd paid management fees of $540,000 to Finger Ltd and Nails had an operating profit of $980,000.Nails' opening retained earnings at the beginning of the period were $1,460,000.At the end of the period Nail Ltd declared a dividend of $90,000.There were no other inter-company transactions.Goodwill was determined to have been impaired by $19,000 during the period.Companies in the group accrue dividends when they are declared by subsidiaries.

Finger Ltd paid cash consideration of $4,000,000 for Nail Ltd.During the period ended 30 June 2005,Nail Ltd paid management fees of $540,000 to Finger Ltd and Nails had an operating profit of $980,000.Nails' opening retained earnings at the beginning of the period were $1,460,000.At the end of the period Nail Ltd declared a dividend of $90,000.There were no other inter-company transactions.Goodwill was determined to have been impaired by $19,000 during the period.Companies in the group accrue dividends when they are declared by subsidiaries.

For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Finger Ltd paid cash consideration of $4,000,000 for Nail Ltd.During the period ended 30 June 2005,Nail Ltd paid management fees of $540,000 to Finger Ltd and Nails had an operating profit of $980,000.Nails' opening retained earnings at the beginning of the period were $1,460,000.At the end of the period Nail Ltd declared a dividend of $90,000.There were no other inter-company transactions.Goodwill was determined to have been impaired by $19,000 during the period.Companies in the group accrue dividends when they are declared by subsidiaries.For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

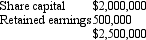

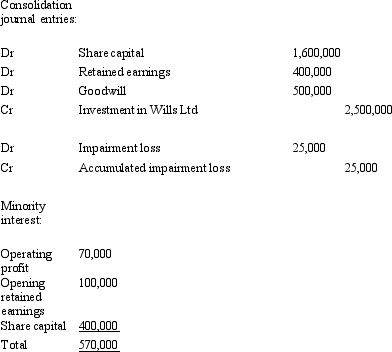

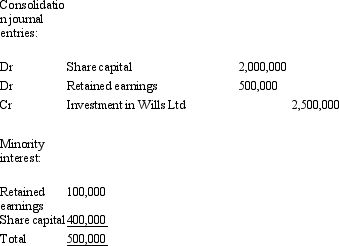

On 1 July 2005 Harry Ltd purchased 80 per cent of the issued share capital of Wills Ltd and has control of Wills.The fair value of the net assets of Wills Ltd on that date was represented as follows:  Harry Ltd paid cash consideration of $2,500,000 for Wills.Wills Ltd made an operating profit of $350,000,there were no intragroup transactions during the period ended 30 June 2006.Goodwill had been determined to have been impaired during the year by $25,000.What consolidation journal entries are required for the period and what is the minority interest in equity as at 30 June 2006?

Harry Ltd paid cash consideration of $2,500,000 for Wills.Wills Ltd made an operating profit of $350,000,there were no intragroup transactions during the period ended 30 June 2006.Goodwill had been determined to have been impaired during the year by $25,000.What consolidation journal entries are required for the period and what is the minority interest in equity as at 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

Harry Ltd paid cash consideration of $2,500,000 for Wills.Wills Ltd made an operating profit of $350,000,there were no intragroup transactions during the period ended 30 June 2006.Goodwill had been determined to have been impaired during the year by $25,000.What consolidation journal entries are required for the period and what is the minority interest in equity as at 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Question

Question

Question

Question

Question

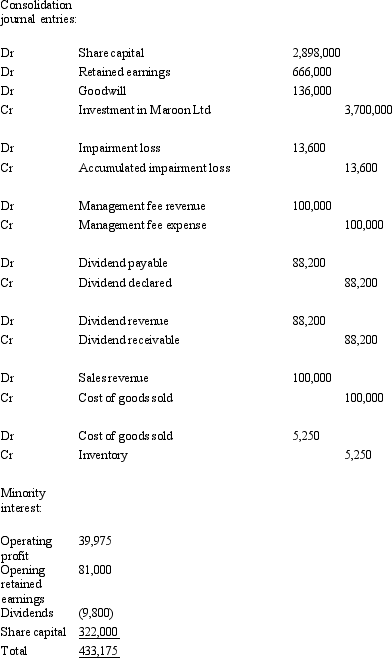

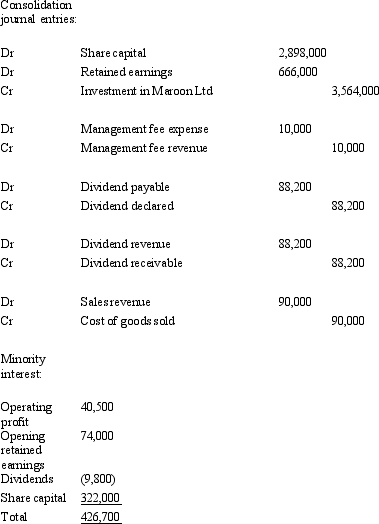

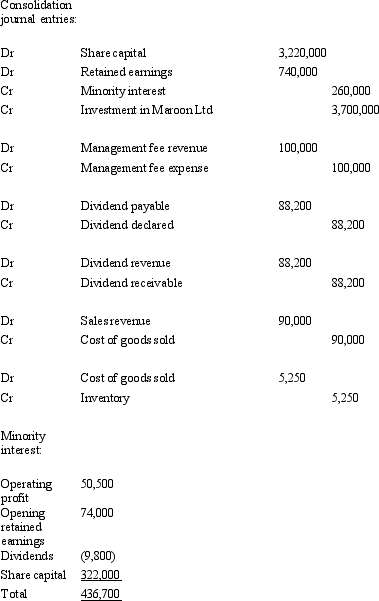

Green Ltd purchased 90 per cent of the issued capital and in the process gained control over Maroon Ltd on 1 July 2005.The fair value of the net assets of Maroon Ltd at purchase was represented by:  Green Ltd paid cash consideration of $3,700,000 for Maroon Ltd.During the period ended 30 June 2007,Maroon Ltd paid management fees of $100,000 to Green Ltd and Maroon had an operating profit of $405,000.Maroon Ltd declared a dividend of $98,000 during the period.Green purchased inventory from Maroon during the period ended 30 June 2007 for $100,000.The inventory cost Maroon Ltd $85,000 and at the end of the period Green had 35 per cent of that inventory still on hand.Maroon's opening retained earnings for the period ended 30 June 2007 was $810,000.Goodwill has been determined to have been impaired by $13,600.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.There were no other inter-company transactions.Ignore tax implications.

Green Ltd paid cash consideration of $3,700,000 for Maroon Ltd.During the period ended 30 June 2007,Maroon Ltd paid management fees of $100,000 to Green Ltd and Maroon had an operating profit of $405,000.Maroon Ltd declared a dividend of $98,000 during the period.Green purchased inventory from Maroon during the period ended 30 June 2007 for $100,000.The inventory cost Maroon Ltd $85,000 and at the end of the period Green had 35 per cent of that inventory still on hand.Maroon's opening retained earnings for the period ended 30 June 2007 was $810,000.Goodwill has been determined to have been impaired by $13,600.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.There were no other inter-company transactions.Ignore tax implications.

For the period ended 30 June 2007,what consolidation journal entries are required and what is the outside equity interest?

A)

B)

C)

D)

E) None of the given answers.

Green Ltd paid cash consideration of $3,700,000 for Maroon Ltd.During the period ended 30 June 2007,Maroon Ltd paid management fees of $100,000 to Green Ltd and Maroon had an operating profit of $405,000.Maroon Ltd declared a dividend of $98,000 during the period.Green purchased inventory from Maroon during the period ended 30 June 2007 for $100,000.The inventory cost Maroon Ltd $85,000 and at the end of the period Green had 35 per cent of that inventory still on hand.Maroon's opening retained earnings for the period ended 30 June 2007 was $810,000.Goodwill has been determined to have been impaired by $13,600.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.There were no other inter-company transactions.Ignore tax implications.For the period ended 30 June 2007,what consolidation journal entries are required and what is the outside equity interest?

A)

B)

C)

D)

E) None of the given answers.

Question

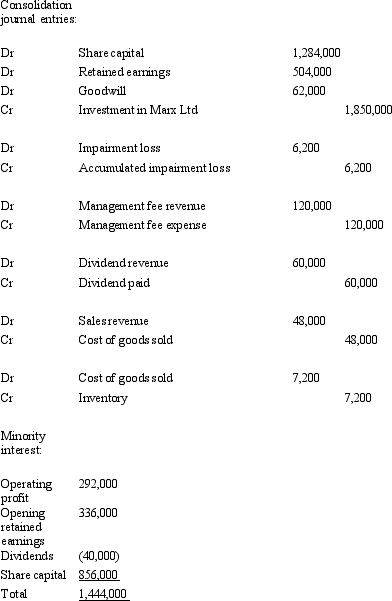

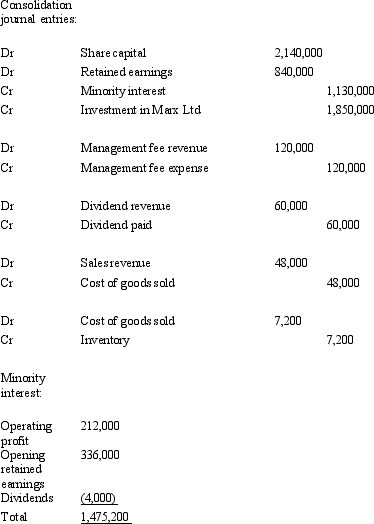

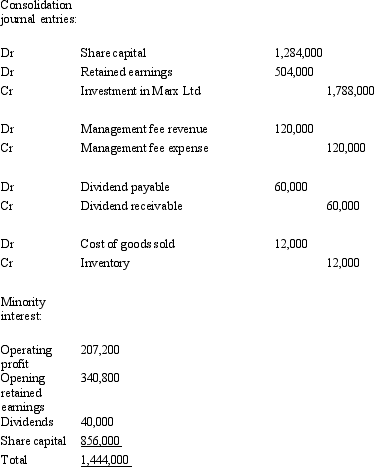

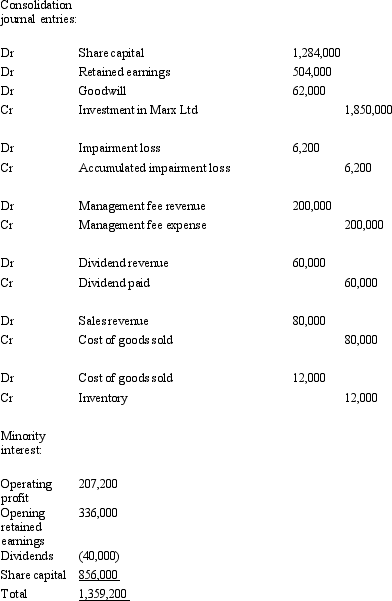

Groucho Ltd purchased 60 per cent of the issued capital and in the process gained control over Marx Ltd on 1 July 2004.The fair value of the net assets of Marx Ltd at purchase was represented by:  Groucho Ltd paid cash consideration of $1,850,000 for Marx Ltd.During the period ended 30 June 2005,Marx Ltd paid management fees of $200,000 to Groucho Ltd and Marx had an operating profit of $530,000.Marx Ltd paid a dividend of $100,000 during the period.Groucho purchased inventory from Marx during the period for $80,000.The inventory cost Marx Ltd $56,000 and at the end of the period Groucho had 50 per cent of that inventory still on hand.Goodwill has been determined to have been impaired by $6,200 during the period.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.Ignore tax implications.

Groucho Ltd paid cash consideration of $1,850,000 for Marx Ltd.During the period ended 30 June 2005,Marx Ltd paid management fees of $200,000 to Groucho Ltd and Marx had an operating profit of $530,000.Marx Ltd paid a dividend of $100,000 during the period.Groucho purchased inventory from Marx during the period for $80,000.The inventory cost Marx Ltd $56,000 and at the end of the period Groucho had 50 per cent of that inventory still on hand.Goodwill has been determined to have been impaired by $6,200 during the period.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.Ignore tax implications.

For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Groucho Ltd paid cash consideration of $1,850,000 for Marx Ltd.During the period ended 30 June 2005,Marx Ltd paid management fees of $200,000 to Groucho Ltd and Marx had an operating profit of $530,000.Marx Ltd paid a dividend of $100,000 during the period.Groucho purchased inventory from Marx during the period for $80,000.The inventory cost Marx Ltd $56,000 and at the end of the period Groucho had 50 per cent of that inventory still on hand.Goodwill has been determined to have been impaired by $6,200 during the period.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.Ignore tax implications.For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/34

Play

Full screen (f)

Deck 30: Further Consolidation Issues II: Accounting for Minority Interests

1

In calculating the proportion of a subsidiary's profit that is attributable to owners who are not part of the group,all adjustments to the group's profit should be treated as affecting the calculation for the outside owners:

False

2

AASB 127 "Consolidated and Separate Financial Statements" prescribes that non-controlling interests be presented in the consolidated statement of financial position as a liability.

False

3

Minority interests are 'identified' and eliminated as part of the consolidation process:

False

4

Buster Ltd owns 85 per cent of the issued capital of Rhymes Ltd.During the period ended 30 June 2006 the operating profit of Rhymes Ltd was $680,000.Buster Ltd bought goods for $540,000 from Rhymes.The goods cost Rhymes $400,000 and at the end of the period none of this inventory was still on hand.Rhymes paid Buster a management fee of $100,000 during the period.Goodwill on consolidation was impaired by $30,000.Rhymes paid a dividend of $40,000 at the end of the period. What is the minority interest in the operating profit of Rhymes Ltd?

A) $87,000

B) $112,500

C) $102,000

D) $101 969

E) None of the given answers.

A) $87,000

B) $112,500

C) $102,000

D) $101 969

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

5

Where the parent entity holds less than 100 per cent interest in a subsidiary,AASB 127 requires the remaining shareholders' interests in what items to be disclosed?

A) The subsidiary's share capital and reserves.

B) The subsidiary's profit or loss.

C) The subsidiary's current and non-current assets.

D) The subsidiary's share capital and reserves and the subsidiary's profit or loss.

E) All of the given answers.

A) The subsidiary's share capital and reserves.

B) The subsidiary's profit or loss.

C) The subsidiary's current and non-current assets.

D) The subsidiary's share capital and reserves and the subsidiary's profit or loss.

E) All of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

6

Parties who are not part of the ownership of the parent entity in a group and who own capital in a company that is a controlled entity in that group are called outside financing interests:

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

7

Total comprehensive income is attributed to the owners of the parent and to the non-controlling interests even if this results in the non-controlling interests having a deficit balance.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

8

In preparing consolidated financial statements minority interests are allocated on a 'line-by-line' basis:

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

9

Finger Ltd purchased 75 per cent of the issued capital and in the process gained control over Nail Ltd on 1 July 2003.The fair value of the net assets of Nail Ltd at purchase was represented by: Finger Ltd paid cash consideration of $4,000,000 for Nail Ltd.During the period ended 30 June 2005,Nail Ltd paid management fees of $540,000 to Finger Ltd and Nails had an operating profit of $980,000.Nails' opening retained earnings at the beginning of the period were $1,460,000.At the end of the period Nail Ltd declared a dividend of $90,000.There were no other inter-company transactions.Goodwill was determined to have been impaired by $19,000 during the period.Companies in the group accrue dividends when they are declared by subsidiaries.

For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Finger Ltd paid cash consideration of $4,000,000 for Nail Ltd.During the period ended 30 June 2005,Nail Ltd paid management fees of $540,000 to Finger Ltd and Nails had an operating profit of $980,000.Nails' opening retained earnings at the beginning of the period were $1,460,000.At the end of the period Nail Ltd declared a dividend of $90,000.There were no other inter-company transactions.Goodwill was determined to have been impaired by $19,000 during the period.Companies in the group accrue dividends when they are declared by subsidiaries.For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

10

Calculating goodwill for a subsidiary that has a minority interest involves:

A) Taking the parent entity's share of the fair value of the identifiable net assets of the subsidiary and deducting it from the fair value of the consideration paid.

B) Dividing the fair value of the consideration paid for the subsidiary by the percentage ownership of the parent entity and deducting the fair value of the identifiable net assets of the subsidiary from that amount.

C) Taking the book value of equity of the subsidiary and deducting the fair value of the consideration paid for the subsidiary.

D) Dividing the fair value of the identifiable net assets of the subsidiary by the percentage ownership of the parent entity and deducting this amount from the fair value of the consideration paid.

E) None of the given answers.

A) Taking the parent entity's share of the fair value of the identifiable net assets of the subsidiary and deducting it from the fair value of the consideration paid.

B) Dividing the fair value of the consideration paid for the subsidiary by the percentage ownership of the parent entity and deducting the fair value of the identifiable net assets of the subsidiary from that amount.

C) Taking the book value of equity of the subsidiary and deducting the fair value of the consideration paid for the subsidiary.

D) Dividing the fair value of the identifiable net assets of the subsidiary by the percentage ownership of the parent entity and deducting this amount from the fair value of the consideration paid.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

11

Minority interests are shown as equity: that is,as contributors of equity capital to the economic entity:

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

12

When a subsidiary company that has a minority interest (MI)declares a dividend,the treatment in the consolidated balance sheet of dividends not paid is:

A) The minority interest portion of the dividend owing should be eliminated along with the parent entity's share, leaving a zero balance in dividends payable.

B) The MI's portion should be deducted from the minority interest's share in equity. There should be no dividend amounts remaining in the consolidated balance sheet, but the amount owed to the MI should be disclosed separately.

C) The amount owing to MI as a dividend payable should be included in the consolidated balance sheet as a current liability.

D) The amount of dividends payable to both the parent entity and the MI will be reflected in the consolidated balance sheet.

E) None of the given answers.

A) The minority interest portion of the dividend owing should be eliminated along with the parent entity's share, leaving a zero balance in dividends payable.

B) The MI's portion should be deducted from the minority interest's share in equity. There should be no dividend amounts remaining in the consolidated balance sheet, but the amount owed to the MI should be disclosed separately.

C) The amount owing to MI as a dividend payable should be included in the consolidated balance sheet as a current liability.

D) The amount of dividends payable to both the parent entity and the MI will be reflected in the consolidated balance sheet.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

13

Minority interests arise when:

A) The parent entity does not control a subsidiary in the group.

B) The parent entity raises capital through preference shares that have the characteristics of debt to fund the subsidiary.

C) The subsidiary has owners of equity who are not owners through their ownership interest in the controlling parent entity.

D) The subsidiary has invested in other entities in which it does not have a controlling interest.

E) None of the given answers.

A) The parent entity does not control a subsidiary in the group.

B) The parent entity raises capital through preference shares that have the characteristics of debt to fund the subsidiary.

C) The subsidiary has owners of equity who are not owners through their ownership interest in the controlling parent entity.

D) The subsidiary has invested in other entities in which it does not have a controlling interest.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

14

AASB 101 "Presentation of Financial Statements" requires a separate line item on the face of the statement of financial position showing the non-controlling interest in equity.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

15

AASB 101 "Presentation of Financial Statements" requires an entity to disclose separately in the statement of comprehensive income,profit or loss for the period attributable to non-controlling interest and owners of the parent.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

16

Minority interests are allocated on a 'line-by-line' basis throughout the income statement:

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

17

Under the proprietary concept of consolidation,minority interests are shown as a liability:

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

18

One of the steps in preparing consolidated financial statements is working out the amounts to be attributed to non-controlling interests to determine the amount to be eliminated in the consolidation process.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

19

Using full goodwill method,share of goodwill attributable to the non-controlling interests is recognized in the statement of financial position as part of non-controlling interest in equity.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

20

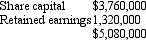

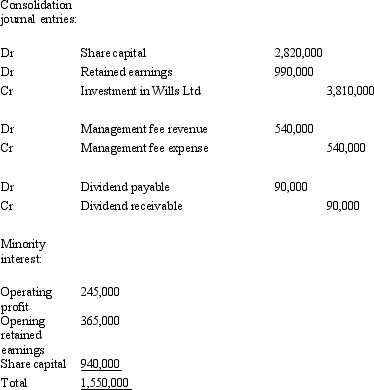

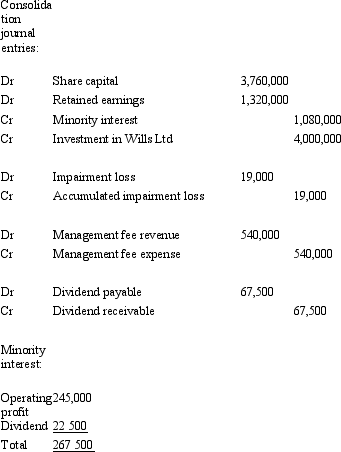

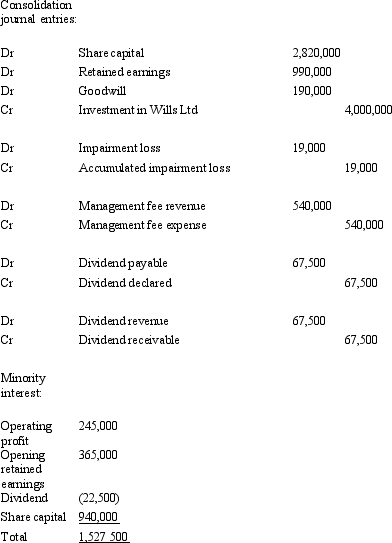

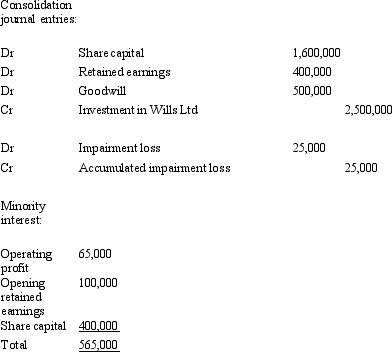

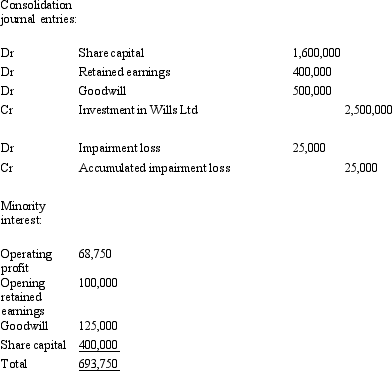

On 1 July 2005 Harry Ltd purchased 80 per cent of the issued share capital of Wills Ltd and has control of Wills.The fair value of the net assets of Wills Ltd on that date was represented as follows: Harry Ltd paid cash consideration of $2,500,000 for Wills.Wills Ltd made an operating profit of $350,000,there were no intragroup transactions during the period ended 30 June 2006.Goodwill had been determined to have been impaired during the year by $25,000.What consolidation journal entries are required for the period and what is the minority interest in equity as at 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

Harry Ltd paid cash consideration of $2,500,000 for Wills.Wills Ltd made an operating profit of $350,000,there were no intragroup transactions during the period ended 30 June 2006.Goodwill had been determined to have been impaired during the year by $25,000.What consolidation journal entries are required for the period and what is the minority interest in equity as at 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

21

On 1 July 2012,Han Solo Ltd acquired 80 per cent of the share capital of Chewbacca Ltd for $500,000,which represented the fair value of the consideration paid,when the share capital and reserves of Chewbacca Ltd were: Share capital $300,000

Revaluation surplus $100,000

Retained earnings $100,000

$500,000

All assets of Chewbacca Ltd were recorded at fair value at acquisition date,except for machinery that had a fair value $20,000 greater than its carrying amount.The cost of the equipment was $40,000 and it had accumulated depreciation of $10,000.The tax rate is 30 per cent?

Under the full goodwill method,what is the amount of fair value adjustment and goodwill,respectively,on 1 July 2012 for non-controlling interests in Chewbacca Ltd?

A) $ 2 800; Zero;

B) $11 200; Zero;

C) $ 2 800; $22 200;

D) $11 200; $88 800

E) $20 000; $88 800;

Revaluation surplus $100,000

Retained earnings $100,000

$500,000

All assets of Chewbacca Ltd were recorded at fair value at acquisition date,except for machinery that had a fair value $20,000 greater than its carrying amount.The cost of the equipment was $40,000 and it had accumulated depreciation of $10,000.The tax rate is 30 per cent?

Under the full goodwill method,what is the amount of fair value adjustment and goodwill,respectively,on 1 July 2012 for non-controlling interests in Chewbacca Ltd?

A) $ 2 800; Zero;

B) $11 200; Zero;

C) $ 2 800; $22 200;

D) $11 200; $88 800

E) $20 000; $88 800;

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is not one of the stages used to determine minority interests?

A) The minority interest in the current period's profit or loss.

B) The minority interest in share capital at the date of acquisition of the subsidiary by the parent entity.

C) The minority interest in the goodwill at acquisition.

D) The minority interest in reserves at the date of acquisition of the subsidiary by the parent entity.

E) The minority interest in post-acquisition changes in reserves.

A) The minority interest in the current period's profit or loss.

B) The minority interest in share capital at the date of acquisition of the subsidiary by the parent entity.

C) The minority interest in the goodwill at acquisition.

D) The minority interest in reserves at the date of acquisition of the subsidiary by the parent entity.

E) The minority interest in post-acquisition changes in reserves.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following statements is incorrect in regards to non-controlling interests in subsidiaries?

A) A non-controlling interest is defined as equity in a subsidiary not attributable, directly or indirectly, to a parent.

B) Under the entity concept, if subsidiaries are partly owned by the parent entity, both the parent entity and the non-controlling interests will have an ownership interest in the subsidiary's profits, dividend payments, and share capital and reserves.

C) Under the entity concept, non-controlling interests will be shown as a liability.

D) Under the proprietary concept, non-controlling interests will be shown as a liability.

E) None of the given answers.

A) A non-controlling interest is defined as equity in a subsidiary not attributable, directly or indirectly, to a parent.

B) Under the entity concept, if subsidiaries are partly owned by the parent entity, both the parent entity and the non-controlling interests will have an ownership interest in the subsidiary's profits, dividend payments, and share capital and reserves.

C) Under the entity concept, non-controlling interests will be shown as a liability.

D) Under the proprietary concept, non-controlling interests will be shown as a liability.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

24

After eliminating the dividend payable to the parent,the balance of the dividend payable to the minority interest:

A) will be eliminated as well.

B) will be included within the consolidated financial statements.

C) will be added recognised as an expense in the consolidated financial statements.

D) will be transferred into a minority interest reserve account.

E) None of the given answers.

A) will be eliminated as well.

B) will be included within the consolidated financial statements.

C) will be added recognised as an expense in the consolidated financial statements.

D) will be transferred into a minority interest reserve account.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

25

On 1 July 2012,Han Solo Ltd acquired 80 per cent of the share capital of Chewbacca Ltd for $400,000,which represented the fair value of the consideration paid,when the share capital and reserves of Subsidiary Ltd were: Share capital $300,000

Revaluation surplus $100,000

Retained earnings $100,000

$500,000

All assets of Chewbacca Ltd were recorded at fair value at acquisition date,except for equipment that had a fair value $20,000 greater than its carrying amount.The cost of the equipment was $40,000 and it had accumulated depreciation of $10,000.The tax rate is 30 per cent?

Using the partial goodwill method,what is the amount of fair value adjustment and goodwill,respectively,on 1 July 2012 for non-controlling interests in Chewbacca Ltd?

A) $ 2,800; Zero;

B) $11,200; 22,200

C) $ 2,800; $22,200;

D) $11,200; $88,800

E) $20,000; $88,800;

Revaluation surplus $100,000

Retained earnings $100,000

$500,000

All assets of Chewbacca Ltd were recorded at fair value at acquisition date,except for equipment that had a fair value $20,000 greater than its carrying amount.The cost of the equipment was $40,000 and it had accumulated depreciation of $10,000.The tax rate is 30 per cent?

Using the partial goodwill method,what is the amount of fair value adjustment and goodwill,respectively,on 1 July 2012 for non-controlling interests in Chewbacca Ltd?

A) $ 2,800; Zero;

B) $11,200; 22,200

C) $ 2,800; $22,200;

D) $11,200; $88,800

E) $20,000; $88,800;

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

26

The disclosure of minority interests in thE.(a)income statement; and (b)balance sheet; is as follows:

A) (a) profit or loss attributable to minority interest in the notes; (b) minority interest in equity as a separate line item.

B) (a) profit or loss attributable to minority interest on the face; (b) minority interest in equity as part of share capital.

C) (a) profit or loss attributable to minority interest in the notes; (b) minority interest in equity as part of share capital.

D) (a) profit or loss attributable to minority interest on the face; (b) minority interest in equity as a separate line item.

E) (a) profit or loss attributable to minority interest on the face; (b) minority interest as a liability, as a separate line item.

A) (a) profit or loss attributable to minority interest in the notes; (b) minority interest in equity as a separate line item.

B) (a) profit or loss attributable to minority interest on the face; (b) minority interest in equity as part of share capital.

C) (a) profit or loss attributable to minority interest in the notes; (b) minority interest in equity as part of share capital.

D) (a) profit or loss attributable to minority interest on the face; (b) minority interest in equity as a separate line item.

E) (a) profit or loss attributable to minority interest on the face; (b) minority interest as a liability, as a separate line item.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following situations,involving eliminations as part of the consolidation process,would not have implications for the calculation of minority interests?

A) The sale of a non-current asset by the subsidiary to the parent.

B) The payment of a management fee by the subsidiary to the parent.

C) The sale of inventory by the parent to the subsidiary.

D) The payment of a management fee by the subsidiary to the parent and the sale of inventory by the parent to the subsidiary.

E) The sale of a non-current asset by the subsidiary to the parent and the sale of inventory by the parent to the subsidiary

A) The sale of a non-current asset by the subsidiary to the parent.

B) The payment of a management fee by the subsidiary to the parent.

C) The sale of inventory by the parent to the subsidiary.

D) The payment of a management fee by the subsidiary to the parent and the sale of inventory by the parent to the subsidiary.

E) The sale of a non-current asset by the subsidiary to the parent and the sale of inventory by the parent to the subsidiary

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

28

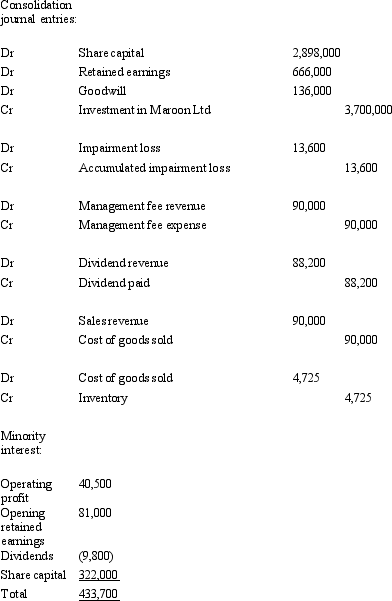

Green Ltd purchased 90 per cent of the issued capital and in the process gained control over Maroon Ltd on 1 July 2005.The fair value of the net assets of Maroon Ltd at purchase was represented by: Green Ltd paid cash consideration of $3,700,000 for Maroon Ltd.During the period ended 30 June 2007,Maroon Ltd paid management fees of $100,000 to Green Ltd and Maroon had an operating profit of $405,000.Maroon Ltd declared a dividend of $98,000 during the period.Green purchased inventory from Maroon during the period ended 30 June 2007 for $100,000.The inventory cost Maroon Ltd $85,000 and at the end of the period Green had 35 per cent of that inventory still on hand.Maroon's opening retained earnings for the period ended 30 June 2007 was $810,000.Goodwill has been determined to have been impaired by $13,600.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.There were no other inter-company transactions.Ignore tax implications.

For the period ended 30 June 2007,what consolidation journal entries are required and what is the outside equity interest?

A)

B)

C)

D)

E) None of the given answers.

Green Ltd paid cash consideration of $3,700,000 for Maroon Ltd.During the period ended 30 June 2007,Maroon Ltd paid management fees of $100,000 to Green Ltd and Maroon had an operating profit of $405,000.Maroon Ltd declared a dividend of $98,000 during the period.Green purchased inventory from Maroon during the period ended 30 June 2007 for $100,000.The inventory cost Maroon Ltd $85,000 and at the end of the period Green had 35 per cent of that inventory still on hand.Maroon's opening retained earnings for the period ended 30 June 2007 was $810,000.Goodwill has been determined to have been impaired by $13,600.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.There were no other inter-company transactions.Ignore tax implications.For the period ended 30 June 2007,what consolidation journal entries are required and what is the outside equity interest?

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

29

Groucho Ltd purchased 60 per cent of the issued capital and in the process gained control over Marx Ltd on 1 July 2004.The fair value of the net assets of Marx Ltd at purchase was represented by: Groucho Ltd paid cash consideration of $1,850,000 for Marx Ltd.During the period ended 30 June 2005,Marx Ltd paid management fees of $200,000 to Groucho Ltd and Marx had an operating profit of $530,000.Marx Ltd paid a dividend of $100,000 during the period.Groucho purchased inventory from Marx during the period for $80,000.The inventory cost Marx Ltd $56,000 and at the end of the period Groucho had 50 per cent of that inventory still on hand.Goodwill has been determined to have been impaired by $6,200 during the period.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.Ignore tax implications.

For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Groucho Ltd paid cash consideration of $1,850,000 for Marx Ltd.During the period ended 30 June 2005,Marx Ltd paid management fees of $200,000 to Groucho Ltd and Marx had an operating profit of $530,000.Marx Ltd paid a dividend of $100,000 during the period.Groucho purchased inventory from Marx during the period for $80,000.The inventory cost Marx Ltd $56,000 and at the end of the period Groucho had 50 per cent of that inventory still on hand.Goodwill has been determined to have been impaired by $6,200 during the period.Companies in the group use perpetual inventory systems and accrue dividends when they are declared by subsidiaries.Ignore tax implications.For the period ended 30 June 2005,what consolidation journal entries are required and what is the minority interest?

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

30

As prescribed in AASB 127,which of the following statements is incorrect in regards to non-controlling interests in subsidiaries?

A) Non-controlling interests are presented in the consolidated statement of financial position within equity, separately from the equity of the owners of the parent.

B) Profit or loss and each component of other comprehensive income are attributed to the owners of the parent and to the non-controlling interests.

C) Total comprehensive income is attributed to the owners of the parent and to the non-controlling interests even if this results in the non-controlling interests having a deficit balance.

D) Non-controlling interests is classified as equity because non-controlling interests does not meet the definition of a liability in the AASB Framework.

E) None of the given answers.

A) Non-controlling interests are presented in the consolidated statement of financial position within equity, separately from the equity of the owners of the parent.

B) Profit or loss and each component of other comprehensive income are attributed to the owners of the parent and to the non-controlling interests.

C) Total comprehensive income is attributed to the owners of the parent and to the non-controlling interests even if this results in the non-controlling interests having a deficit balance.

D) Non-controlling interests is classified as equity because non-controlling interests does not meet the definition of a liability in the AASB Framework.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

31

Acquirer Limited purchased 75 per cent of Subby Limited for $45,000.The fair value of identifiable assets was $95,000,and the fair value of liabilities and contingent liabilities amounted to $47,000.According to ED 139,what would be the amount of 'goodwill allocated to non-controlling interests of Subby Limited'?

A) $3,000.

B) $9,000.

C) $12,000.

D) ($3,000).

E) Cannot determine from the information given.

A) $3,000.

B) $9,000.

C) $12,000.

D) ($3,000).

E) Cannot determine from the information given.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

32

There is no adjustment for things such as management fees when determining minority interests,because:

A) they are not a material item.

B) they do not involve minority interests.

C) they are considered to be realised.

D) they relate only to the parent entity.

E) None of the given answers.

A) they are not a material item.

B) they do not involve minority interests.

C) they are considered to be realised.

D) they relate only to the parent entity.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following statements is incorrect in regards to non-controlling interests in subsidiaries?

A) The requirement to eliminate the effects of intragroup transactions holds whether or not there are non-controlling interests.

B) The non-controlling interest's share in the dividends paid or proposed by the subsidiary is eliminated on consolidation.

C) The non-controlling interest's share of the profits of the subsidiary is calculated after adjustments to eliminate income and expenses of the subsidiary that are unrealised from the economic entity's perspective.

D) Management fees paid in an intragroup transaction is considered realised when determining non-controlling interests in a subsidiary.

E) None of the given answers.

A) The requirement to eliminate the effects of intragroup transactions holds whether or not there are non-controlling interests.

B) The non-controlling interest's share in the dividends paid or proposed by the subsidiary is eliminated on consolidation.

C) The non-controlling interest's share of the profits of the subsidiary is calculated after adjustments to eliminate income and expenses of the subsidiary that are unrealised from the economic entity's perspective.

D) Management fees paid in an intragroup transaction is considered realised when determining non-controlling interests in a subsidiary.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

34

Calculating the minority interest (MI)in the operating profit and opening retained earnings of a subsidiary is done by:

A) Taking the operating profit and opening retained earnings figures of the subsidiary and multiplying them by the percentage ownership held by the MI.

B) Adjusting the operating profit and opening retained earnings of the subsidiary for any intragroup transactions and multiplying them by the percentage ownership held by the MI.

C) Adjusting the operating profit of the subsidiary for any unrealised profit or expense of the subsidiary as a result of any intragroup transactions and multiplying both this and the opening retained earnings by the percentage ownership held by the MI.

D) Adjusting the opening retained earnings and the operating profit for any unrealised profit or expense of the subsidiary as a result of intragroup transactions and multiplying this by the percentage ownership held by the MI.

E) None of the given answers.

A) Taking the operating profit and opening retained earnings figures of the subsidiary and multiplying them by the percentage ownership held by the MI.

B) Adjusting the operating profit and opening retained earnings of the subsidiary for any intragroup transactions and multiplying them by the percentage ownership held by the MI.

C) Adjusting the operating profit of the subsidiary for any unrealised profit or expense of the subsidiary as a result of any intragroup transactions and multiplying both this and the opening retained earnings by the percentage ownership held by the MI.

D) Adjusting the opening retained earnings and the operating profit for any unrealised profit or expense of the subsidiary as a result of intragroup transactions and multiplying this by the percentage ownership held by the MI.

E) None of the given answers.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 34 flashcards in this deck.