Deck 16: Revenue Recognition Issues

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

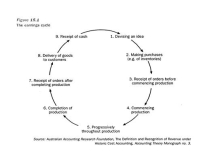

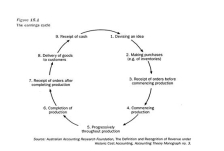

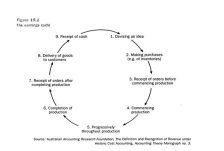

The following is a diagram of the earnings cycle as presented by Coombes and Martin (1982). Products such as precious metals,or agricultural products,recognise revenue at which point in the earnings cycle shown above?

A) Point 1.

B) Point 4.

C) Point 6.

D) Point 7.

E) None of the given answers.

A) Point 1.

B) Point 4.

C) Point 6.

D) Point 7.

E) None of the given answers.

Question

Question

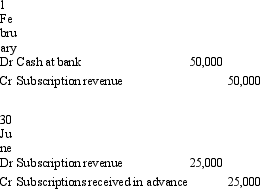

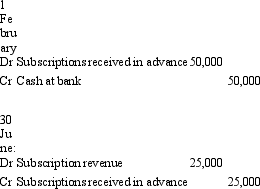

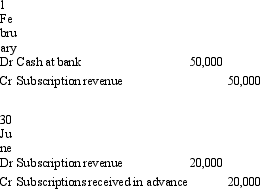

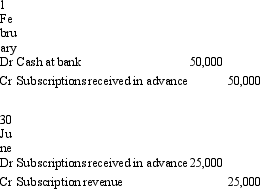

Magazines Galore receives subscription money in advance,and has received $50,000 from customers on 1 February to cover the next ten issues of Wheels Galore.There are ten issues a year - one at the end of each month except for January and December.What are the appropriate accounting entries to record the receipt of the subscription money and (assuming no monthly entries have been made)the adjusting entry at 30 June (after June's issue has been mailed to subscribers)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

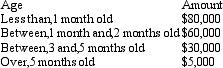

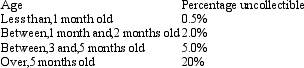

Vettori Ltd has the following information from an aged debtors listing for the current period.  Based on experience in the industry,Vettori Ltd uses the following basis for estimating uncollectible amounts:

Based on experience in the industry,Vettori Ltd uses the following basis for estimating uncollectible amounts:

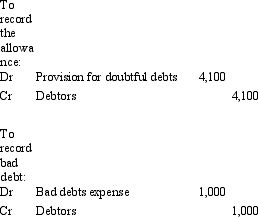

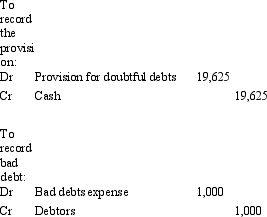

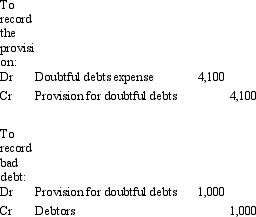

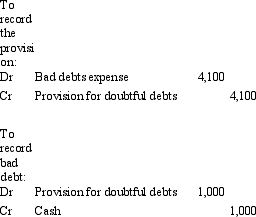

Assuming that the current balance in the provision for doubtful debts is zero,what is the entry to record the provision for this period? What is the entry to record the writing off of a bad debt of $1,000 when a debtor goes bankrupt?

Assuming that the current balance in the provision for doubtful debts is zero,what is the entry to record the provision for this period? What is the entry to record the writing off of a bad debt of $1,000 when a debtor goes bankrupt?

A)

B)

C)

D)

E) None of the given answers.

Based on experience in the industry,Vettori Ltd uses the following basis for estimating uncollectible amounts: Assuming that the current balance in the provision for doubtful debts is zero,what is the entry to record the provision for this period? What is the entry to record the writing off of a bad debt of $1,000 when a debtor goes bankrupt?A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

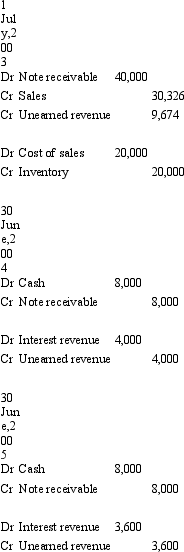

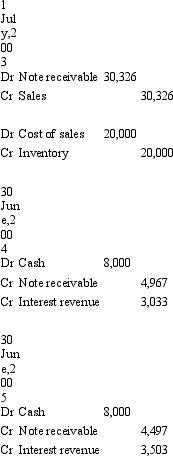

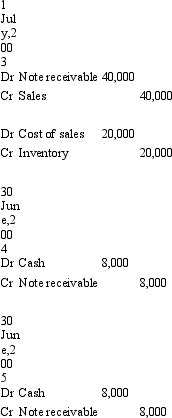

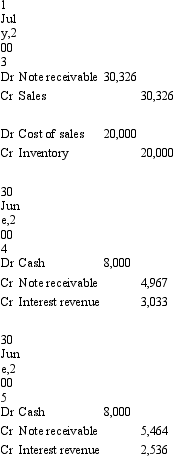

On 1 July 2003 Bigwell Ltd sells a machine to Archer Ltd in exchange for a promissory note which requires Archer Ltd to make five payments of $8,000,the first to be made on 30 June 2004.The machine cost Bigwell Ltd $20,000 to manufacture.Bigwell Ltd would normally sell this type of machine for $30,326 for cash or short-term credit.The implicit interest rate in the agreement is 10 per cent.What are the appropriate journal entries to record the sale agreement and the first two instalments using the gross method?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

The following is a diagram of the earnings cycle as presented by Coombes and Martin (1982). In the traditional historical-cost accounting model,at what point has revenue been recognised for long-term construction contracts in the building industry?

A) Point 8.

B) Point 4.

C) Point 6.

D) Point 5.

E) None of the given answers.

A) Point 8.

B) Point 4.

C) Point 6.

D) Point 5.

E) None of the given answers.

Question

Question

Question

Question

Question

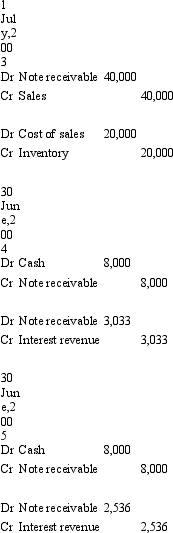

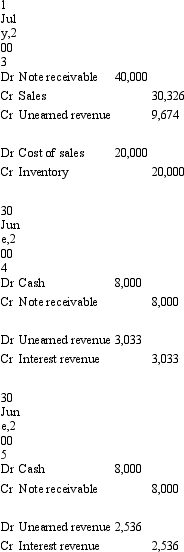

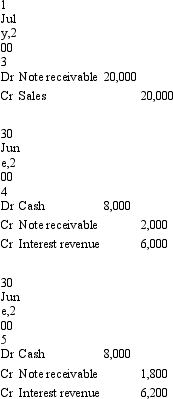

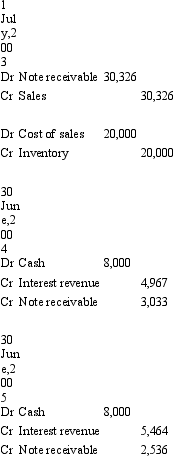

On 1 July,2003 Bryson Ltd sells a machine to Adams Ltd in exchange for a promissory note which requires Adams Ltd to make five payments of $8,000,the first to be made on 30 June,2004.The machine cost Bryson Ltd $20,000 to manufacture.Bryson Ltd would normally sell this type of machine for $30,326 for cash or short-term credit.The implicit interest rate in the agreement is 10 per cent.What are the appropriate journal entries to record the sale agreement and the first two instalments using the net-interest method?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

The following is a diagram of the earnings cycle as presented by Coombes and Martin (1982). Because of uncertainty and depending on which measurement model is being applied,revenue recognition will take place at a limited number of points in the earnings cycle.In traditional historical-cost accounting,in most cases,at which point in the cycle above have revenues been recognised?

A) Point 5.

B) Point 8.

C) Point 7.

D) Point 9.

E) None of the given answers.

A) Point 5.

B) Point 8.

C) Point 7.

D) Point 9.

E) None of the given answers.

Question

Question

Question

Question

Question

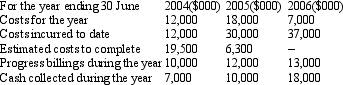

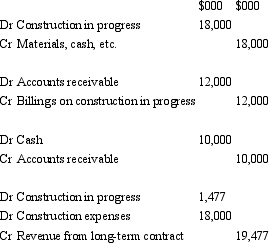

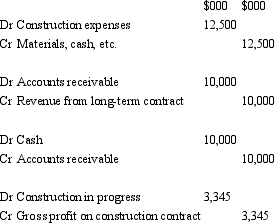

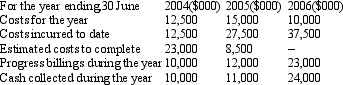

Russell Ltd commenced the construction of a bridge on 1July 2003.It has a fixed-price contract for total revenues of $35million.The expected completion date is 30 June 2006.The expected total cost to Russell Ltd at the beginning of the project is $29 million.The following information relates only to the construction of the bridge:  Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Question

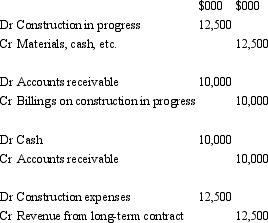

Russell Ltd commenced the construction of a bridge on 1July 2003.It has a fixed-price contract for total revenues of $35million.The expected completion date is 30 June 2006.The expected total cost to Russell Ltd at the beginning of the project is $29 million.The following information relates only to the construction of the bridge:  Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.Assuming that 2004's entries have been made,what are the journal entries for the year ended 30June 2005 (rounded to the nearest $000)?

Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.Assuming that 2004's entries have been made,what are the journal entries for the year ended 30June 2005 (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.Assuming that 2004's entries have been made,what are the journal entries for the year ended 30June 2005 (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Question

Question

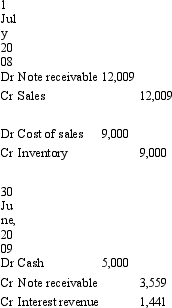

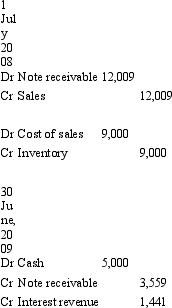

The following journal entries were recorded by a vendor who sold goods and received promissory notes on 1 July 2008 in exchange.  Assuming that the issuer of the promissory notes intends to make three equal payments of $5,000 at the end of each of the three years,30 June 2009,30 June 2010 and,30 June 2011; what is the amount of interest revenue recorded by the vendor at,30 June,2011?

Assuming that the issuer of the promissory notes intends to make three equal payments of $5,000 at the end of each of the three years,30 June 2009,30 June 2010 and,30 June 2011; what is the amount of interest revenue recorded by the vendor at,30 June,2011?

A) Nil.

B) $536

C) $1,014

D) $1,441

E) $4,464

Assuming that the issuer of the promissory notes intends to make three equal payments of $5,000 at the end of each of the three years,30 June 2009,30 June 2010 and,30 June 2011; what is the amount of interest revenue recorded by the vendor at,30 June,2011?A) Nil.

B) $536

C) $1,014

D) $1,441

E) $4,464

Question

Question

Question

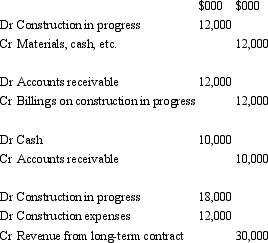

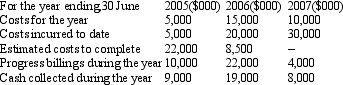

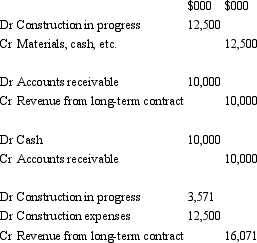

Undersea Construction Ltd commenced the construction of a tunnel under a major river for public transport on 1 July 2004.It has a fixed-price contract for total revenues of $36 million.The expected completion date is 30 June 2007.The expected total cost to Undersea Construction at the beginning of the project is $28 million.The following information relates only to the construction of the tunnel:  Undersea Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

Undersea Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Undersea Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Question

Question

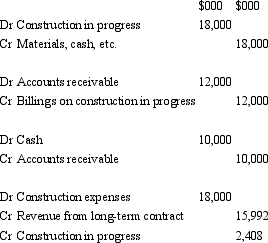

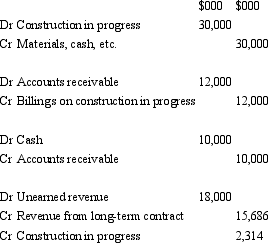

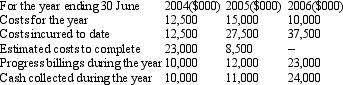

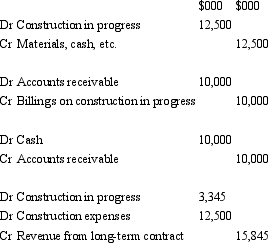

Hillier Construction Ltd commenced the construction of a building on 1 July 2003.It has a fixed-price contract for total revenues of $45 million.The expected completion date is 30 June 2006.The expected total cost to Hillier Construction at the beginning of the project is $35 million.The following information relates only to the construction of this building:  Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What are the journal entries for the year ended 30 June 2004 (rounded to the nearest $000)?

Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What are the journal entries for the year ended 30 June 2004 (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What are the journal entries for the year ended 30 June 2004 (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Question

Hillier Construction Ltd commenced the construction of a building on 1 July 2003.It has a fixed-price contract for total revenues of $45 million.The expected completion date is 30 June 2006.The expected total cost to Hillier Construction at the beginning of the project is $35 million.The following information relates only to the construction of this building:  Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Question

Question

The following journal entries were recorded by a vendor who sold goods and received promissory notes on 1 July 2008 in exchange.  What is the interest rate implicit in the arrangement?

What is the interest rate implicit in the arrangement?

A) 29.6 per cent.

B) 16 per cent.

C) Cannot determine on the basis of the information provided.

D) 10 per cent.

E) 12 per cent.

What is the interest rate implicit in the arrangement?A) 29.6 per cent.

B) 16 per cent.

C) Cannot determine on the basis of the information provided.

D) 10 per cent.

E) 12 per cent.

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/64

Play

Full screen (f)

Deck 16: Revenue Recognition Issues

1

When it is probable that total contract costs will exceed total contract revenue,the expected loss should not be recognised as an expense until the future economic sacrifice eventuates.

False

2

In most cases dividend revenue should not be recognised until the dividend proposed has been ratified by the shareholders at the annual general meeting:

False

3

Where the percentage of completion method is based on costs,costs that relate to the contract activity generally and are not normally related to specific contracts,such as finance costs,should be allocated across the projects currently in progress:

False

4

With the 'percentage-of-completion' method of accounting for construction contracts,profit is recognised in proportion to the work performed in each reporting perioD.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

5

Gains must be reported net of related expenses:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

6

If the borrower prepays interest,the inflow of future economic benefits represented by the prepayment would not constitute an item of revenue to the lender because the lender has a present obligation to the borrower to provide finance for the period to which the prepayment relates.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

7

Revenues may be generated by:

A) Holding and disposing of inventory in the normal course of business.

B) Having a liability forgiven.

C) Receiving a donation.

D) The ordinary activities of the entity only.

E) All of the given answers.

A) Holding and disposing of inventory in the normal course of business.

B) Having a liability forgiven.

C) Receiving a donation.

D) The ordinary activities of the entity only.

E) All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

8

Construction costs plus gross profit earned to date from a construction contract are accumulated in the construction in progress account less progress billings and these are disclosed in the liability section of the statement of financial position.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

9

When the gross method is used to record the interest inherent in a sales transaction,it is typical for the accrued interest to be offset against the note receivable:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

10

Gains never arise from the ordinary activities of an entity:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

11

When making a provision for doubtful debts,debtors' subsidiary ledgers are not adjusted,as the provision is made in anticipation of likely unrecoverability of amounts owing,although the identity of who will not pay is unknown:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

12

AASB 118 requires revenues to be measured in terms of historical cost to improve reliability:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

13

The AASB Framework now divides revenues into 'income' and 'gains':

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

14

Unearned revenues are assets treated as liabilities,as these are received by a business for services to be performed at a future date.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

15

Accounting standards require that the provision for doubtful debts should be shown as a deduction from the class of assets to which it relates.The net expense in relation to bad and doubtful debts must also be disclosed

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

16

An entry to an asset revaluation reserve is an example of the general rule that indicates that holding gains are not typically included as income:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

17

Transactions that result in an inflow of economic benefits such as the purchase of assets can be classified as a gain:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

18

Under the AASB Framework a saving in an outflow through the reduction of a liability that is not a contribution by equity participants,and results in an increase in equity during the reporting period,was income:

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

19

When the outcome of a construction contract can be estimated reliably,contract revenue and contract costs associated with the construction contract shall be recognised as revenue and expenses respectively by reference to the stage of completion of the contract activity at the reporting date.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

20

If a company sells its product but gives the buyer the right to return the product,AASB 118 requires revenue from the sales transaction to be recognised at the time of sale.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

21

Daniel Ltd sells one of its properties to a financing company with an attached call option,which allows Daniel Ltd to reacquire the property at a future date for $400,000.The current market value at the time of the sale is $300,000,but the financing company pays $350,000 for it.It is expected that the market value of the property will exceed $400,000 before the option expires.What is the appropriate treatment of this sale?

A) Record the revenue and make appropriate note disclosures about the call option and its associated risks.

B) Set-off the call option and the building - reporting changes in the difference between their current values as revenues or expenses as appropriate.

C) No entry would be required as the call option is off balance sheet and the building has not effectively been sold.

D) Record the inflow of cash and a liability.

E) None of the given answers.

A) Record the revenue and make appropriate note disclosures about the call option and its associated risks.

B) Set-off the call option and the building - reporting changes in the difference between their current values as revenues or expenses as appropriate.

C) No entry would be required as the call option is off balance sheet and the building has not effectively been sold.

D) Record the inflow of cash and a liability.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

22

When goods are sold 'free on board' (f.o.b)shipping point the revenue should be recognised when:

A) The goods are completed and ready to be transported.

B) The goods are received by the purchaser.

C) The goods are received by the common carrier.

D) There is no revenue involved for goods sold on terms 'free on board'.

E) None of the given answers.

A) The goods are completed and ready to be transported.

B) The goods are received by the purchaser.

C) The goods are received by the common carrier.

D) There is no revenue involved for goods sold on terms 'free on board'.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

23

In the situation that a debtor becomes unable to pay and the amount has not been anticipated through an provision for doubtful debts,what is the entry to record the bad debt?

A) Dr Debtors; Cr Provision for doubtful debts.

B) Dr Provision for doubtful debts; Cr Debtors.

C) Dr Bad debts expense; Cr Cash.

D) Dr Bad debts expense; Cr Debtors.

E) None of the given answers.

A) Dr Debtors; Cr Provision for doubtful debts.

B) Dr Provision for doubtful debts; Cr Debtors.

C) Dr Bad debts expense; Cr Cash.

D) Dr Bad debts expense; Cr Debtors.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

24

The following is a diagram of the earnings cycle as presented by Coombes and Martin (1982). Products such as precious metals,or agricultural products,recognise revenue at which point in the earnings cycle shown above?

A) Point 1.

B) Point 4.

C) Point 6.

D) Point 7.

E) None of the given answers.

A) Point 1.

B) Point 4.

C) Point 6.

D) Point 7.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

25

SAC 4 previously outlined tests that may have been useful in determining if it is probable that an inflow of future economic benefits that is capable of measurement has occurred.These tests included.

A) That cash has been received.

B) That an order has been placed or it is possible to reliably estimate the collectability of debts.

C) That all acts of performance necessary to establish a valid claim against the external party have been completed.

D) That cash has been received and that all acts of performance necessary to establish a valid claim against the external party have been completed.

E) None of the given answers.

A) That cash has been received.

B) That an order has been placed or it is possible to reliably estimate the collectability of debts.

C) That all acts of performance necessary to establish a valid claim against the external party have been completed.

D) That cash has been received and that all acts of performance necessary to establish a valid claim against the external party have been completed.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

26

Magazines Galore receives subscription money in advance,and has received $50,000 from customers on 1 February to cover the next ten issues of Wheels Galore.There are ten issues a year - one at the end of each month except for January and December.What are the appropriate accounting entries to record the receipt of the subscription money and (assuming no monthly entries have been made)the adjusting entry at 30 June (after June's issue has been mailed to subscribers)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

27

Vettori Ltd has the following information from an aged debtors listing for the current period. Based on experience in the industry,Vettori Ltd uses the following basis for estimating uncollectible amounts:

Assuming that the current balance in the provision for doubtful debts is zero,what is the entry to record the provision for this period? What is the entry to record the writing off of a bad debt of $1,000 when a debtor goes bankrupt?

A)

B)

C)

D)

E) None of the given answers.

Based on experience in the industry,Vettori Ltd uses the following basis for estimating uncollectible amounts: Assuming that the current balance in the provision for doubtful debts is zero,what is the entry to record the provision for this period? What is the entry to record the writing off of a bad debt of $1,000 when a debtor goes bankrupt?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

28

The general rule under modified historical-cost accounting is that holding gains on non-current assets should be:

A) Treated as revenue in the period that the fair value of the asset changes.

B) Deferred and amortised over the life of the asset (effectively decreasing depreciation expense).

C) Taken to an asset revaluation reserve unless it is the reversal of a previous devaluation that was expensed. In that case it can be recognised as income to the extent the devaluation was recognised as an expense.

D) Never recognised.

E) None of the given answers.

A) Treated as revenue in the period that the fair value of the asset changes.

B) Deferred and amortised over the life of the asset (effectively decreasing depreciation expense).

C) Taken to an asset revaluation reserve unless it is the reversal of a previous devaluation that was expensed. In that case it can be recognised as income to the extent the devaluation was recognised as an expense.

D) Never recognised.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

29

There are various appropriate accounting treatments when a sale is made subject to a right of return.These methods include:

A) Recording the sale and accounting for the returns as they occur in future periods.

B) Recording the cash received as held in trust until all return privileges have expired.

C) Recording the sale but reducing sales by an estimate of the future returns.

D) Recording the sale and accounting for the returns as they occur in future periods and recording the sale but reducing sales by an estimate of the future returns.

E) All of the given answers.

A) Recording the sale and accounting for the returns as they occur in future periods.

B) Recording the cash received as held in trust until all return privileges have expired.

C) Recording the sale but reducing sales by an estimate of the future returns.

D) Recording the sale and accounting for the returns as they occur in future periods and recording the sale but reducing sales by an estimate of the future returns.

E) All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

30

On 1 July 2003 Bigwell Ltd sells a machine to Archer Ltd in exchange for a promissory note which requires Archer Ltd to make five payments of $8,000,the first to be made on 30 June 2004.The machine cost Bigwell Ltd $20,000 to manufacture.Bigwell Ltd would normally sell this type of machine for $30,326 for cash or short-term credit.The implicit interest rate in the agreement is 10 per cent.What are the appropriate journal entries to record the sale agreement and the first two instalments using the gross method?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

31

The following is a diagram of the earnings cycle as presented by Coombes and Martin (1982). In the traditional historical-cost accounting model,at what point has revenue been recognised for long-term construction contracts in the building industry?

A) Point 8.

B) Point 4.

C) Point 6.

D) Point 5.

E) None of the given answers.

A) Point 8.

B) Point 4.

C) Point 6.

D) Point 5.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

32

The 'percentage of completion' that may be used to account for construction contracts can be justified on the basis that:

A) The contractor will be continuously working and therefore earning revenue.

B) In most long-term construction projects, payments are made periodically throughout the life of the contract allowing revenue to be recognised.

C) It is unreasonable to expect a contractor to record revenue only when construction is completed.

D) The contracting firm may be considered to be in a continuous sales transaction.

E) All of the given answers.

A) The contractor will be continuously working and therefore earning revenue.

B) In most long-term construction projects, payments are made periodically throughout the life of the contract allowing revenue to be recognised.

C) It is unreasonable to expect a contractor to record revenue only when construction is completed.

D) The contracting firm may be considered to be in a continuous sales transaction.

E) All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

33

Revenue recognition under AASB 18 requires that:

A) The entity has transferred to the buyer the significant risks and rewards of ownership.

B) The entity retains neither continuing managerial involvement to the degree normally associated with ownership nor effective control over the goods.

C) The costs incurred or to be incurred can be measured reliably.

D) The amount of revenue can be measured reliably.

E) All of the given answers.

A) The entity has transferred to the buyer the significant risks and rewards of ownership.

B) The entity retains neither continuing managerial involvement to the degree normally associated with ownership nor effective control over the goods.

C) The costs incurred or to be incurred can be measured reliably.

D) The amount of revenue can be measured reliably.

E) All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

34

When goods are sold on extended credit there is an implicit financing arrangement contained in the sale agreement.In order to separate the financing element from the sale,it is necessary to calculate the interest rate inherent in the agreement.What advice does AASB 118 provide about this?

A) The implicit rate of interest is the more clearly determinable of either: (a) the prevailing rate of a similar instrument of an issuer with a similar credit rating; or (b) a rate of interest that discounts the nominal amount of the instrument to the current cash sales price of the goods or services.

B) The implicit rate of interest is the internal rate of return implicit in the contract such that the sales price is equal to the fair market value of the asset.

C) The implicit rate of interest is the more reliably determinable of either: (a) the prevailing rate of a debt instrument of an issuer adjusted to the organisation-specific, risk adjusted rate of the issuer; or (b) a rate of interest that discounts the sales price to the fair market value of the goods or services.

D) The implicit rate of interest is the internal rate of return implicit in the contract such that the sales price is equal to the fair market value of the asset. This rate may have to be adjusted to take account of the risk of the issuer if it is significantly different to the market-determined interest rate for similar entities.

E) None of the given answers.

A) The implicit rate of interest is the more clearly determinable of either: (a) the prevailing rate of a similar instrument of an issuer with a similar credit rating; or (b) a rate of interest that discounts the nominal amount of the instrument to the current cash sales price of the goods or services.

B) The implicit rate of interest is the internal rate of return implicit in the contract such that the sales price is equal to the fair market value of the asset.

C) The implicit rate of interest is the more reliably determinable of either: (a) the prevailing rate of a debt instrument of an issuer adjusted to the organisation-specific, risk adjusted rate of the issuer; or (b) a rate of interest that discounts the sales price to the fair market value of the goods or services.

D) The implicit rate of interest is the internal rate of return implicit in the contract such that the sales price is equal to the fair market value of the asset. This rate may have to be adjusted to take account of the risk of the issuer if it is significantly different to the market-determined interest rate for similar entities.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

35

When the collectability of an amount that has been recorded as revenue becomes uncertain,the appropriate accounting treatment is to:

A) Recognise as an expense the amount in respect of which recovery has ceased to be probable.

B) Calculate the discounted present value of the amount expected to be received and adjust the recorded revenue accordingly.

C) Adjust the amount of revenue originally recognised.

D) Make no adjustment as the amount and timing of the uncollectible amount is uncertain.

E) None of the given answers.

A) Recognise as an expense the amount in respect of which recovery has ceased to be probable.

B) Calculate the discounted present value of the amount expected to be received and adjust the recorded revenue accordingly.

C) Adjust the amount of revenue originally recognised.

D) Make no adjustment as the amount and timing of the uncollectible amount is uncertain.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

36

On 1 July,2003 Bryson Ltd sells a machine to Adams Ltd in exchange for a promissory note which requires Adams Ltd to make five payments of $8,000,the first to be made on 30 June,2004.The machine cost Bryson Ltd $20,000 to manufacture.Bryson Ltd would normally sell this type of machine for $30,326 for cash or short-term credit.The implicit interest rate in the agreement is 10 per cent.What are the appropriate journal entries to record the sale agreement and the first two instalments using the net-interest method?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

37

Kringle Company has agreed to provide services to North to South Ltd in exchange for a piece of equipment and a cash payment.The equipment is currently recorded in North to South's books at $73,000 but independent assessors have set the fair value at $65,000.The cash payment of $20,000 will be received 12 months after completion of the services.Kringle should record revenue as:

A) $85,000.

B) $65,000 in the current period, $20,000 next period.

C) $93,000.

D) $85,000 but this figure must be discounted to allow for the 12 months until payment of the cash component.

E) $65,000 plus the present value of the $20,000 cash component.

A) $85,000.

B) $65,000 in the current period, $20,000 next period.

C) $93,000.

D) $85,000 but this figure must be discounted to allow for the 12 months until payment of the cash component.

E) $65,000 plus the present value of the $20,000 cash component.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

38

The following is a diagram of the earnings cycle as presented by Coombes and Martin (1982). Because of uncertainty and depending on which measurement model is being applied,revenue recognition will take place at a limited number of points in the earnings cycle.In traditional historical-cost accounting,in most cases,at which point in the cycle above have revenues been recognised?

A) Point 5.

B) Point 8.

C) Point 7.

D) Point 9.

E) None of the given answers.

A) Point 5.

B) Point 8.

C) Point 7.

D) Point 9.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

39

In the case of a fixed price contract,AASB 111 specifies four conditions that must all be met in order for the percentage of completion method to be applied.These conditions include:

A) Costs related to the contract can be clearly identified and measured reliably.

B) It is probable that the economic benefits arising from the contract will flow to the contractor.

C) The entity commissioning the work has a good credit rating and is able to pay its debts.

D) Costs related to the contract can be clearly identified and measured reliably and it is probable that the economic benefits arising from the contract will flow to the contractor.

E) All of the given answers.

A) Costs related to the contract can be clearly identified and measured reliably.

B) It is probable that the economic benefits arising from the contract will flow to the contractor.

C) The entity commissioning the work has a good credit rating and is able to pay its debts.

D) Costs related to the contract can be clearly identified and measured reliably and it is probable that the economic benefits arising from the contract will flow to the contractor.

E) All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

40

Under the AASB Framework income is now subdivided into:

A) Revenues, which only include sales, fees, interest, dividends, royalties and rent; Gains, which are no different in nature to revenue.

B) Gains, which are regarded as constituting a separate element in the Framework; Revenues, which may only arise in the course of the ordinary activities of the entity.

C) Revenues, which arise in the course of the ordinary activities of the entity; Gains, which may or may not arise in the course of the ordinary activities of the entity.

D) Increases in equity referred to as Gains; reductions in liabilities which are classified as Revenues.

E) None of the given answers.

A) Revenues, which only include sales, fees, interest, dividends, royalties and rent; Gains, which are no different in nature to revenue.

B) Gains, which are regarded as constituting a separate element in the Framework; Revenues, which may only arise in the course of the ordinary activities of the entity.

C) Revenues, which arise in the course of the ordinary activities of the entity; Gains, which may or may not arise in the course of the ordinary activities of the entity.

D) Increases in equity referred to as Gains; reductions in liabilities which are classified as Revenues.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

41

Biological assets are:

A) recognised as income when sold.

B) to be valued at market value, with any increase being capitalised and amortised over the period until the asset is sold.

C) to be valued at market value, with any increase being treated as income.

D) to be valued at fair value, with any increase being treated as income.

E) to be valued at fair value, with any increase being capitalised and amortised over the period until the asset is sold.

A) recognised as income when sold.

B) to be valued at market value, with any increase being capitalised and amortised over the period until the asset is sold.

C) to be valued at market value, with any increase being treated as income.

D) to be valued at fair value, with any increase being treated as income.

E) to be valued at fair value, with any increase being capitalised and amortised over the period until the asset is sold.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

42

When the cost basis is used to calculate the percentage of completion,cost items that may need adjustment include:

A) Discounts for the bulk purchase of construction materials.

B) Gains and losses on foreign currency translation.

C) Materials delivered and paid for, but not yet used.

D) Interest charges on late payments for materials and other items used in the construction project.

E) None of the given answers.

A) Discounts for the bulk purchase of construction materials.

B) Gains and losses on foreign currency translation.

C) Materials delivered and paid for, but not yet used.

D) Interest charges on late payments for materials and other items used in the construction project.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

43

Russell Ltd commenced the construction of a bridge on 1July 2003.It has a fixed-price contract for total revenues of $35million.The expected completion date is 30 June 2006.The expected total cost to Russell Ltd at the beginning of the project is $29 million.The following information relates only to the construction of the bridge: Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

44

Russell Ltd commenced the construction of a bridge on 1July 2003.It has a fixed-price contract for total revenues of $35million.The expected completion date is 30 June 2006.The expected total cost to Russell Ltd at the beginning of the project is $29 million.The following information relates only to the construction of the bridge: Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.Assuming that 2004's entries have been made,what are the journal entries for the year ended 30June 2005 (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Russell Ltd uses the percentage of completion method based on cost to account for its construction contracts.Assuming that 2004's entries have been made,what are the journal entries for the year ended 30June 2005 (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

45

In considering whether to recognise revenue when there are associated options:

A) The probability of the exercise of the options must be considered.

B) The probability of the exercise of the options must not be considered.

C) Put options will always give rise to revenue, whereas call options will not.

D) Call options will always give rise to revenue, whereas put options will not.

E) None of the given answers.

A) The probability of the exercise of the options must be considered.

B) The probability of the exercise of the options must not be considered.

C) Put options will always give rise to revenue, whereas call options will not.

D) Call options will always give rise to revenue, whereas put options will not.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

46

The following journal entries were recorded by a vendor who sold goods and received promissory notes on 1 July 2008 in exchange. Assuming that the issuer of the promissory notes intends to make three equal payments of $5,000 at the end of each of the three years,30 June 2009,30 June 2010 and,30 June 2011; what is the amount of interest revenue recorded by the vendor at,30 June,2011?

A) Nil.

B) $536

C) $1,014

D) $1,441

E) $4,464

Assuming that the issuer of the promissory notes intends to make three equal payments of $5,000 at the end of each of the three years,30 June 2009,30 June 2010 and,30 June 2011; what is the amount of interest revenue recorded by the vendor at,30 June,2011?A) Nil.

B) $536

C) $1,014

D) $1,441

E) $4,464

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

47

Transactions such as the purchase of assets or the issuance of debt are not considered income because:

A) they involve external parties.

B) they necessarily involve cash.

C) they do not result in an increase in equity.

D) they both result in an increase of the asset or liability concerned.

E) they both result in a reduction of leverage.

A) they involve external parties.

B) they necessarily involve cash.

C) they do not result in an increase in equity.

D) they both result in an increase of the asset or liability concerned.

E) they both result in a reduction of leverage.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

48

AASB 111 specifies the accounting treatment in the case that the outcome of a construction contract cannot be reliably estimated.The treatment specified is:

A) (a) Contract costs must be deferred and matched against revenues in the financial year in which they are recognised where it is not probable that the costs will be recovered in the current period; and (b) where it is probable that the costs will be recovered in the current period, revenue must be recognised only to the extent of the costs incurred.

B) (a) Construction costs must be recognised as a contra asset in the financial year in which they are incurred and set-off against the receivable recorded on the contract; and (b) where the receivable is less than the accrued costs, the difference must be written off as an expense in the period.

C) (a) Contract costs must be recognised as an expense in the financial year in which they are incurred; and (b) where it is probable that the costs will be recovered, revenue must be recognised only to the extent of the costs incurred.

D) (a) Construction costs must be accrued and reported as a deferred asset to the extent that it is considered probable that the costs will be recovered; and (b) revenue may be recognised only to the extent of the costs incurred.

E) None of the given answers.

A) (a) Contract costs must be deferred and matched against revenues in the financial year in which they are recognised where it is not probable that the costs will be recovered in the current period; and (b) where it is probable that the costs will be recovered in the current period, revenue must be recognised only to the extent of the costs incurred.

B) (a) Construction costs must be recognised as a contra asset in the financial year in which they are incurred and set-off against the receivable recorded on the contract; and (b) where the receivable is less than the accrued costs, the difference must be written off as an expense in the period.

C) (a) Contract costs must be recognised as an expense in the financial year in which they are incurred; and (b) where it is probable that the costs will be recovered, revenue must be recognised only to the extent of the costs incurred.

D) (a) Construction costs must be accrued and reported as a deferred asset to the extent that it is considered probable that the costs will be recovered; and (b) revenue may be recognised only to the extent of the costs incurred.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

49

Undersea Construction Ltd commenced the construction of a tunnel under a major river for public transport on 1 July 2004.It has a fixed-price contract for total revenues of $36 million.The expected completion date is 30 June 2007.The expected total cost to Undersea Construction at the beginning of the project is $28 million.The following information relates only to the construction of the tunnel: Undersea Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Undersea Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

50

In relation to the expense associated with the creation of an allowance for doubtful debts,the Australian Taxation Office:

A) Never allows a deduction for taxation purposes for that amount.

B) Allows a deduction for taxation purposes for that amount when it is recognised as an expense.

C) Allows a deduction for taxation purposes immediately.

D) Allows a deduction for taxation purposes only when there is a bad debt written off against a debtors account.

E) Allows a deduction for taxation purposes if the probability of the debt not being repaid is greater than 50 per cent.

A) Never allows a deduction for taxation purposes for that amount.

B) Allows a deduction for taxation purposes for that amount when it is recognised as an expense.

C) Allows a deduction for taxation purposes immediately.

D) Allows a deduction for taxation purposes only when there is a bad debt written off against a debtors account.

E) Allows a deduction for taxation purposes if the probability of the debt not being repaid is greater than 50 per cent.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

51

Hillier Construction Ltd commenced the construction of a building on 1 July 2003.It has a fixed-price contract for total revenues of $45 million.The expected completion date is 30 June 2006.The expected total cost to Hillier Construction at the beginning of the project is $35 million.The following information relates only to the construction of this building: Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What are the journal entries for the year ended 30 June 2004 (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What are the journal entries for the year ended 30 June 2004 (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following statements is not in accordance with AAS 118 "Revenue" with respect to revenue recognition?

A) Revenue is measured at the fair value of the consideration received or receivable taking into account the amount of any trade discounts and volume rebates allowed by the entity.

B) When goods are sold or services are rendered in exchange for dissimilar goods or services, the exchange is regarded as a transaction which generates revenue.

C) The amount of revenue arising on a transaction is usually determined by agreement between the entity and the buyer or user of the asset.

D) When goods or services are exchanged or swapped for goods or services which are of a similar nature and value, the exchange is not regarded as a transaction which generates revenue.

E) E: None of the given answers.

A) Revenue is measured at the fair value of the consideration received or receivable taking into account the amount of any trade discounts and volume rebates allowed by the entity.

B) When goods are sold or services are rendered in exchange for dissimilar goods or services, the exchange is regarded as a transaction which generates revenue.

C) The amount of revenue arising on a transaction is usually determined by agreement between the entity and the buyer or user of the asset.

D) When goods or services are exchanged or swapped for goods or services which are of a similar nature and value, the exchange is not regarded as a transaction which generates revenue.

E) E: None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following statements is not in accordance with AAS 118 "Revenue" with respect to revenue recognition?

A) When the selling price of a product includes an identifiable amount for subsequent servicing, that amount is deferred and recognised as revenue over the period during which the service is performed.

B) When the arrangement effectively constitutes a financing transaction, the fair value of the consideration is determined by discounting all future receipts using an imputed rate of interest.

C) When an entity sells goods and at the same time enter into a separate agreement to repurchase the goods at a later date, the two transactions are dealt with separately.

D) When goods or services are exchanged or swapped for goods or services, the revenue is measured at the fair value of the goods or services received, adjusted by the amount of any cash or cash equivalents transferred.

E) E: When goods or services are exchanged or swapped for goods or services and the fair value of the goods or services received cannot be measured reliably, the revenue is measured at the fair value of the goods or services given up, adjusted by the amount of any cash or cash equivalents transferred.

A) When the selling price of a product includes an identifiable amount for subsequent servicing, that amount is deferred and recognised as revenue over the period during which the service is performed.

B) When the arrangement effectively constitutes a financing transaction, the fair value of the consideration is determined by discounting all future receipts using an imputed rate of interest.

C) When an entity sells goods and at the same time enter into a separate agreement to repurchase the goods at a later date, the two transactions are dealt with separately.

D) When goods or services are exchanged or swapped for goods or services, the revenue is measured at the fair value of the goods or services received, adjusted by the amount of any cash or cash equivalents transferred.

E) E: When goods or services are exchanged or swapped for goods or services and the fair value of the goods or services received cannot be measured reliably, the revenue is measured at the fair value of the goods or services given up, adjusted by the amount of any cash or cash equivalents transferred.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following is not an example of a situation in which an entity retains the risks and rewards of ownership?

A) When the entity retains an obligation for unsatisfactory performance not covered by normal warranty provisions.

B) When the entity provides a normal warranty for the goods sold.

C) When the buyer has the right to rescind the purchase for a reason specified in the sales contract and the entity is uncertain about the probability of return.

D) When the goods that are shipped subject to installation and the installation is a significant part of the contract which has not yet been completed by the entity.

E) When the receipt of revenue form a particular sale is contingent upon the derivation of revenue by the buyer from its sales of goods.

A) When the entity retains an obligation for unsatisfactory performance not covered by normal warranty provisions.

B) When the entity provides a normal warranty for the goods sold.

C) When the buyer has the right to rescind the purchase for a reason specified in the sales contract and the entity is uncertain about the probability of return.

D) When the goods that are shipped subject to installation and the installation is a significant part of the contract which has not yet been completed by the entity.

E) When the receipt of revenue form a particular sale is contingent upon the derivation of revenue by the buyer from its sales of goods.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

55

Hillier Construction Ltd commenced the construction of a building on 1 July 2003.It has a fixed-price contract for total revenues of $45 million.The expected completion date is 30 June 2006.The expected total cost to Hillier Construction at the beginning of the project is $35 million.The following information relates only to the construction of this building: Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?

A)

B)

C)

D)

E) None of the given answers.

Hillier Construction uses the percentage of completion method based on cost to account for its construction contracts.What is the gross profit to be recognised in each of the 3 years (rounded to the nearest $000)?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

56

Using the cost method to calculate the percentage of completion,the formula for the amount of revenue and gross profit to be recognised is:

A) Costs incurred to the end of the current period divided by most recent estimate of total costs.

B) Estimated total revenue or gross profit from the contract multiplied by (costs incurred to the end of the current period divided by most recent estimate of total costs) less (total revenue or gross profit recognised in prior periods).

C) Costs incurred to the end of the current period divided by most recent estimate of total costs multiplied by (total revenue or gross profit recognised in prior periods).

D) Estimated total revenue or gross profit from the contract divided by (costs incurred to the end of the current period multiplied by most recent estimate of total costs) less (total revenue or gross profit recognised in prior periods).

E) None of the given answers.

A) Costs incurred to the end of the current period divided by most recent estimate of total costs.

B) Estimated total revenue or gross profit from the contract multiplied by (costs incurred to the end of the current period divided by most recent estimate of total costs) less (total revenue or gross profit recognised in prior periods).

C) Costs incurred to the end of the current period divided by most recent estimate of total costs multiplied by (total revenue or gross profit recognised in prior periods).

D) Estimated total revenue or gross profit from the contract divided by (costs incurred to the end of the current period multiplied by most recent estimate of total costs) less (total revenue or gross profit recognised in prior periods).

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

57

The following journal entries were recorded by a vendor who sold goods and received promissory notes on 1 July 2008 in exchange. What is the interest rate implicit in the arrangement?

A) 29.6 per cent.

B) 16 per cent.

C) Cannot determine on the basis of the information provided.

D) 10 per cent.

E) 12 per cent.

What is the interest rate implicit in the arrangement?A) 29.6 per cent.

B) 16 per cent.

C) Cannot determine on the basis of the information provided.

D) 10 per cent.

E) 12 per cent.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

58

According to AASB 111 a group of contracts shall be treated as a single contract:

A) Only when they involve one customer.

B) Only when the contracts are performed concurrently.

C) When the group of contracts is negotiated as a single package.

D) All of the given answers.

E) None of the given answers.

A) Only when they involve one customer.

B) Only when the contracts are performed concurrently.

C) When the group of contracts is negotiated as a single package.

D) All of the given answers.

E) None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following is not a disclosure requirement of AASB 111?

A) The amount of contract revenue recognised as revenue must be disclosed either on the face of the income statement or in the accompanying notes.

B) Contract costs incurred must be disclosed either on the face of the income statement or in the accompanying notes.

C) A liability being the gross amount due to customers for contract work.

D) The gross amount of work progress must be disclosed in the balance sheet.

E) For contracts in progress, the amount of advances received, must be disclosed either on the face of the income statement or in the accompanying notes.

A) The amount of contract revenue recognised as revenue must be disclosed either on the face of the income statement or in the accompanying notes.

B) Contract costs incurred must be disclosed either on the face of the income statement or in the accompanying notes.

C) A liability being the gross amount due to customers for contract work.

D) The gross amount of work progress must be disclosed in the balance sheet.

E) For contracts in progress, the amount of advances received, must be disclosed either on the face of the income statement or in the accompanying notes.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

60

The percentage of completion can be measured in a number of ways,including:

A) Physical estimates or surveys of the work performed to date.

B) The work plan basis, which uses the project management plan to calculate the percentage of the construction completed.

C) The billings basis, using the proportion that progress billings to date bear to the total estimated billings for the contract.

D) Physical estimates or surveys of the work performed to date and the billings basis, using the proportion that progress billings to date bear to the total estimated billings for the contract.

E) All of the given answers.

A) Physical estimates or surveys of the work performed to date.

B) The work plan basis, which uses the project management plan to calculate the percentage of the construction completed.

C) The billings basis, using the proportion that progress billings to date bear to the total estimated billings for the contract.

D) Physical estimates or surveys of the work performed to date and the billings basis, using the proportion that progress billings to date bear to the total estimated billings for the contract.

E) All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following statements is incorrect with respect to revenue recognition of construction contracts?

A) The percentage-of-completion method is to be applied for fixed price contracts if the recognition criteria are satisfied.

B) AASB 111 requires individual construction contracts to be accounted for separately and the requirements of the standard to be applied separately to each contract.

C) The percentage-of-completion method should be used, provided certain conditions are met that enable the outcome of the contract to be reliably estimated.

D) Percentage-of-completion method requires contract revenue to be matched with progress billings, resulting in the reporting of revenue, expenses and profit which can be attributed to the amount billed to customers.

E) E: All of the given answers.

A) The percentage-of-completion method is to be applied for fixed price contracts if the recognition criteria are satisfied.

B) AASB 111 requires individual construction contracts to be accounted for separately and the requirements of the standard to be applied separately to each contract.

C) The percentage-of-completion method should be used, provided certain conditions are met that enable the outcome of the contract to be reliably estimated.

D) Percentage-of-completion method requires contract revenue to be matched with progress billings, resulting in the reporting of revenue, expenses and profit which can be attributed to the amount billed to customers.

E) E: All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

62

Lonsdale Ltd sells mobile phones and provides a one-year warranty.Lonsdale is able to recognise revenue at point-of-sale in accordance with AASB 118 because:

A) this is industry practice;

B) repairs are unlikely within a year of sale;

C) cost of repairs can be estimated based on experience and this is recognised as warranty expense in the year of sale;

D) cost of repairs can be estimated based on experience and this is recognised as sales returns;

E) E: None of the given answers.

A) this is industry practice;

B) repairs are unlikely within a year of sale;

C) cost of repairs can be estimated based on experience and this is recognised as warranty expense in the year of sale;

D) cost of repairs can be estimated based on experience and this is recognised as sales returns;

E) E: None of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

63

Werribee Direct Ltd is a mail order company that allows its customers to order on-line and return the goods without obligations.Werribee Direct Ltd had experienced a high ratio of returned merchandise from on-line sales.What is the appropriate accounting treatment for this sale that is in accordance with AASB 118 "Revenue"?

A) Record the sale only when the option to return has expired;

B) Record the sale and reduce this by an estimate of future returns;

C) Record the sale and account for returns as they occur;

D) Record the sale as deferred revenue and recognise revenue progressively until expiry of the privileges;

E) E: All of the given answers.

A) Record the sale only when the option to return has expired;

B) Record the sale and reduce this by an estimate of future returns;

C) Record the sale and account for returns as they occur;

D) Record the sale as deferred revenue and recognise revenue progressively until expiry of the privileges;

E) E: All of the given answers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

64

Bellarine Ltd is publisher of Mode magazine and its customers usually sign a three-year subscription with an advance payment of $500.Mode magazine has 12 issues in a year.What is the appropriate accounting treatment for this sale on the date of signing that is in accordance with AASB 118 "Revenue"?

A) Recognise revenue in full as this is an immaterial amount;

B) Recognise as a provision;

C) Recognise as unearned revenue;

D) Disclose in the notes as a contingent item;

E) E: None of the given answers

A) Recognise revenue in full as this is an immaterial amount;

B) Recognise as a provision;

C) Recognise as unearned revenue;

D) Disclose in the notes as a contingent item;

E) E: None of the given answers

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 64 flashcards in this deck.