Deck 11: Accounting for Lease

Full screen (f)

Question

Question

Question

Question

Question

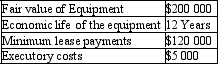

Alpine Ltd signed a 10-year non-cancellable lease with Mt Buller Ltd for the use of high-tech equipment.No bargain purchase option is provided in the lease contract. The following information is available.

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?

A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

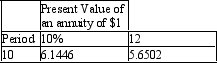

On 1 January 2012 Dobel Ltd signed a ten-year non-cancellable lease that requires a payment of $100 000 at the end of each year.Ownership of the leased asset remains with the lessor at expiry of the lease.The incremental borrowing rate of Dobel Ltd is 12% while the implicit rate of the lessor known to Dobel Ltd is 10%. The following information is also available:

At what amount should the leased property be recorded in the books of Dobel Ltd?

At what amount should the leased property be recorded in the books of Dobel Ltd?

A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

At what amount should the leased property be recorded in the books of Dobel Ltd?A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

Question

Question

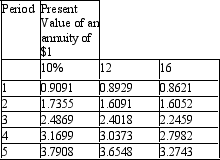

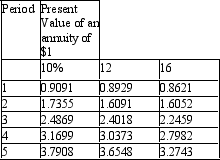

Kingslake Ltd signed a non-cancellable lease contract on 1 January 2012 for a machine that requires 5 annual payments of $200 000 at the start of each year.On the last annual payment,ownership will transfer from the lessor to Kingslake Ltd.The fair value of the asset if paid in cash is $75,964. The following information is also available:

What is the implicit rate of this lease arrangement in accordance with AASB 117?

What is the implicit rate of this lease arrangement in accordance with AASB 117?

A: 10%

B: 12%

C: 16%

D: Between 10% and 12%

E)Between 12% and 16%

What is the implicit rate of this lease arrangement in accordance with AASB 117?A: 10%

B: 12%

C: 16%

D: Between 10% and 12%

E)Between 12% and 16%

Question

Question

Question

Johnson Ltd enters into a lease agreement with Peterson Ltd under the following conditions:  The lease may be cancelled only with the permission of the lessor.If the rate of interest implicit in the lease is 10 per cent,what is the fair value of the asset at the inception of the lease,and is the lease a finance or operating lease?

The lease may be cancelled only with the permission of the lessor.If the rate of interest implicit in the lease is 10 per cent,what is the fair value of the asset at the inception of the lease,and is the lease a finance or operating lease?

A) $56,745, finance lease.

B) $52,596, operating lease.

C) $56,745, operating lease.

D) $52,596, finance lease.

E) None of the given answers.

The lease may be cancelled only with the permission of the lessor.If the rate of interest implicit in the lease is 10 per cent,what is the fair value of the asset at the inception of the lease,and is the lease a finance or operating lease?A) $56,745, finance lease.

B) $52,596, operating lease.

C) $56,745, operating lease.

D) $52,596, finance lease.

E) None of the given answers.

Question

Kensington Ltd decides to lease some equipment from Piccadilly Ltd on the following terms:  If the interest rate implicit in the lease is 8 per cent,what is the fair value of the equipment at the inception of the lease (rounded to the nearest dollar)?

If the interest rate implicit in the lease is 8 per cent,what is the fair value of the equipment at the inception of the lease (rounded to the nearest dollar)?

A) $44 518

B) $46 094

C) $40 094

D) $48 399

E) None of the given answers.

If the interest rate implicit in the lease is 8 per cent,what is the fair value of the equipment at the inception of the lease (rounded to the nearest dollar)?A) $44 518

B) $46 094

C) $40 094

D) $48 399

E) None of the given answers.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

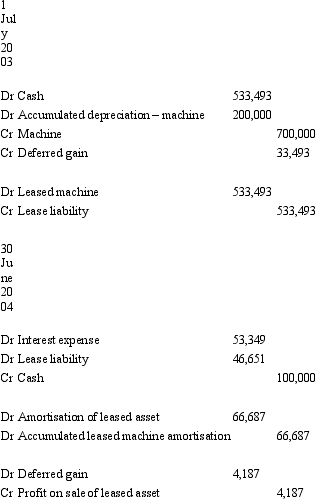

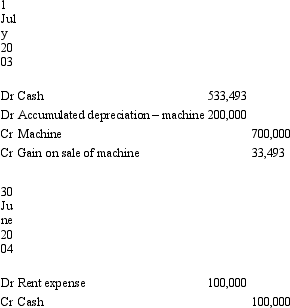

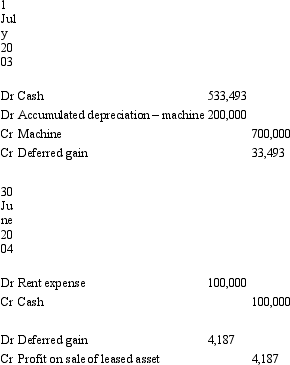

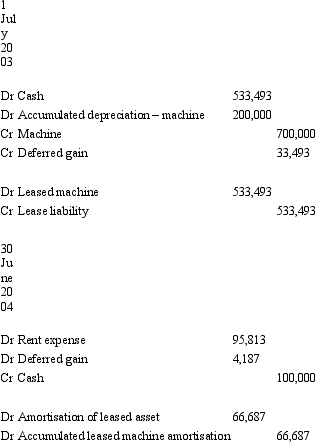

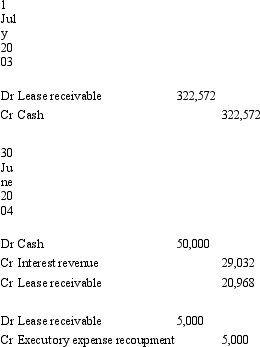

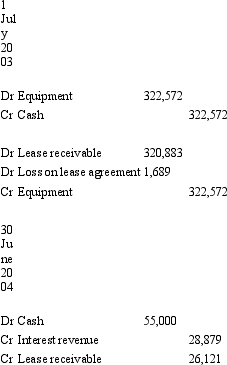

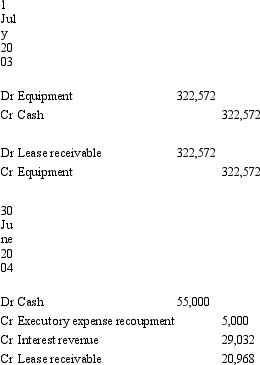

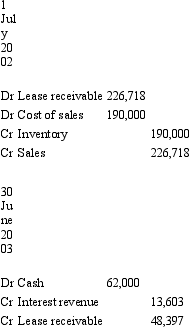

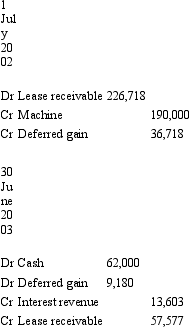

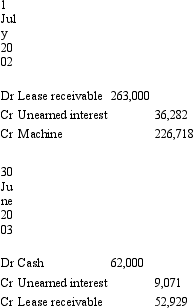

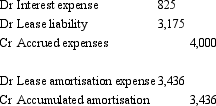

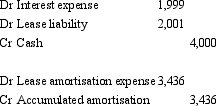

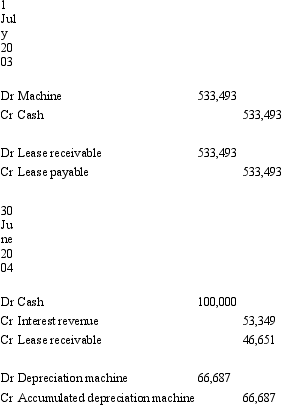

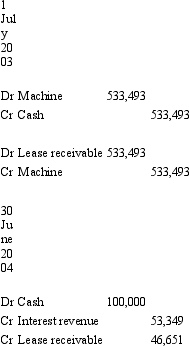

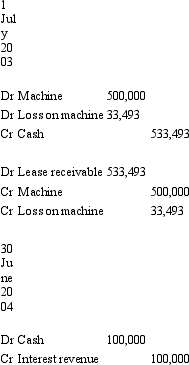

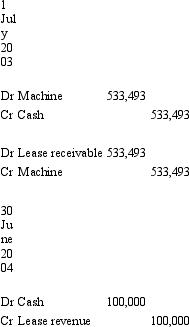

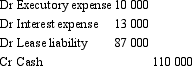

Cobalt Ltd owns an item of machinery that has a cost of $700,000 and accumulated depreciation of $200,000 as at 1 July 2003.On that date the machine is sold to Blue Ltd for $533,493,and then leased back over 8 years (the remaining life of the machine).The lease is non-cancellable.The lease payments are $100,000 per annum,payable in arrears on 30 June each year.The interest rate implicit in the lease is 10 per cent and the economic benefits of the asset are expected to be realised evenly over its life.What are the entries to record the transactions in Cobalt's books on 1 July 2003 and 30 June 2004 (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

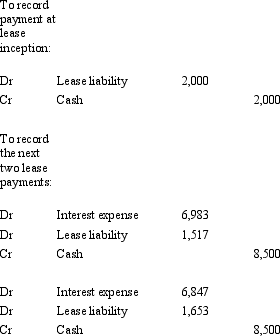

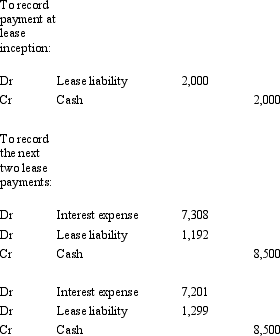

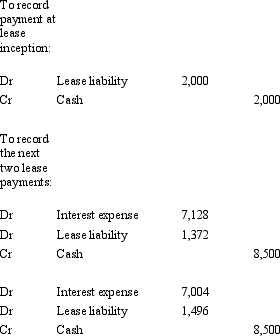

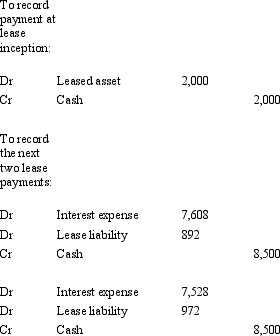

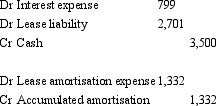

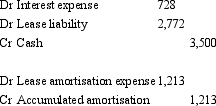

Fresco Ltd enters into a non-cancellable lease agreement with Meola Ltd to lease some equipment under the following conditions:  The interest rate implicit in the lease is 9 per cent and the fair value of the asset at the inception of the lease is $81,199.What are the journal entries to record the lease payment at inception of the lease,and the next two lease payments,in the books of the lessee (rounded to the nearest dollar)?

The interest rate implicit in the lease is 9 per cent and the fair value of the asset at the inception of the lease is $81,199.What are the journal entries to record the lease payment at inception of the lease,and the next two lease payments,in the books of the lessee (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 9 per cent and the fair value of the asset at the inception of the lease is $81,199.What are the journal entries to record the lease payment at inception of the lease,and the next two lease payments,in the books of the lessee (rounded to the nearest dollar)?A)

B)

C)

D)

E) None of the given answers.

Question

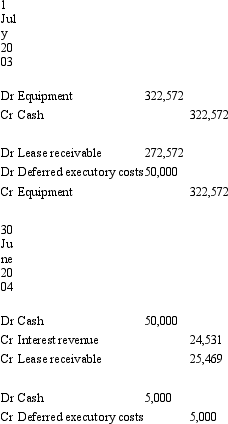

Medusa Ltd enters into a non-cancellable 10-year lease with Lennox Ltd on 1 July 2003.The lease is for an item of equipment that at the inception of the lease has a fair value of $322,572 (the amount that Medusa paid for the asset on 1 July 2003).The equipment is expected to have a useful life of 12 years and the lease term is for 10 years.The lease contract includes a bargain purchase option of $4,000 that Lennox Ltd will be able to exercise at the end of the 10-year lease.The lease payments will be made on 30 June each year,beginning 30 June 2004.The payments are to be $55,000 each year with $5,000 of this being for executory costs to cover maintenance of the equipment.The maintenance will be carried out annually.The interest rate implicit in the lease is 9 per cent.What are the entries in the books of Medusa Ltd for 1 July 2003 and 30 June 2004 (round amounts to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

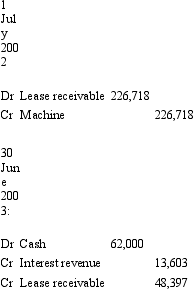

Gerbert Ltd enters into a finance lease with Hokiman Ltd on 1 July 2002 for an item of machinery that has a fair value at that date of $226,718.The lease is for a period of 4 years,with annual lease payments of $62,000 due on 30 June each year,the first payment to be made in 2003.There is a bargain purchase option of $15,000 available for Hokiman to exercise at the end of the lease period.The rate of interest implicit in the lease is 6 per cent.It cost Gerbert Ltd $190,000 to manufacture the machine.What are the entries in the books of Gerbert Ltd for 1 July 2002 and 30 June 2003 (round amounts to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Quaid Ltd entered into a lease agreement on 1 July 2002 to lease equipment on the following terms:  The interest rate implicit in the lease is 8 per cent and the fair value of the leased asset is $24,987.The lease is cancellable if the lessee immediately enters into a further lease for the same or equivalent asset.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.The lease payment has not been made on 30 June before the adjusting entries are made for the year end.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2003?

The interest rate implicit in the lease is 8 per cent and the fair value of the leased asset is $24,987.The lease is cancellable if the lessee immediately enters into a further lease for the same or equivalent asset.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.The lease payment has not been made on 30 June before the adjusting entries are made for the year end.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2003?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 8 per cent and the fair value of the leased asset is $24,987.The lease is cancellable if the lessee immediately enters into a further lease for the same or equivalent asset.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.The lease payment has not been made on 30 June before the adjusting entries are made for the year end.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2003?A)

B)

C)

D)

E) None of the given answers.

Question

Question

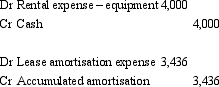

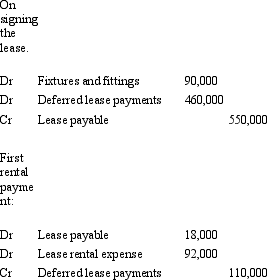

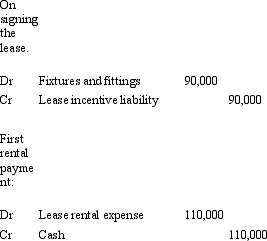

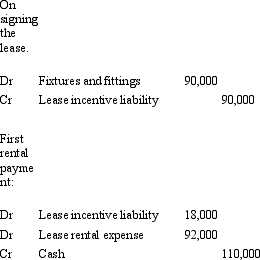

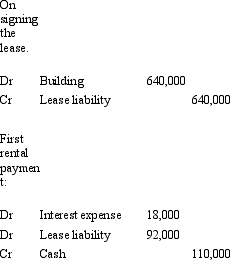

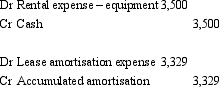

Schwann Ltd enters into a non-cancellable 5-year lease for office space in Bigtown's central business district.The building has an expected remaining life of 40 years.Schwann Ltd has been offered a free fit-out of the office as an incentive to take up the lease.The fit-out would have cost Schwann Ltd $90,000 to do itself.The benefits of the fit-out are to be recognised on a straight-line basis.The rental payments are $110,000 per annum.How would the signing of the lease and the first rental payment be recorded by Schwann Ltd in accordance with UIG Abstract 3?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Cobalt Ltd owns an item of machinery that has a cost of $700,000 and accumulated depreciation of $200,000 as at 1 July 2003.On that date the machine is sold to Blue Ltd for $533,493,and then leased back over 8 years (the remaining life of the machine).The lease is non-cancellable.The lease payments are $100,000 per annum,payable in arrears on 30 June each year.The interest rate implicit in the lease is 10 per cent and the economic benefits of the asset are expected to be realised evenly over its life.What are the entries to record the transactions in Blue's books on 1 July 2003 and 30 June 2004 (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Mitchum Ltd entered into a lease agreement on 1 July 2003 to lease equipment on the following terms:  The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset is $13,316.The lease is cancellable at the option of the lessee.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2004?

The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset is $13,316.The lease is cancellable at the option of the lessee.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2004?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset is $13,316.The lease is cancellable at the option of the lessee.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2004?A)

B)

C)

D)

E) None of the given answers.

Question

Question

Joplin Ltd entered into a lease agreement on 1 July 2002 with Thomas Ltd.The terms of the lease are as follows:  The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset at the inception of the lease is $20,517.The lease is non-cancellable and at the end of the lease the asset is returned to the lessor.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What is the value of the lease asset and lease liability in the books of the lessee after adjusting entries made on 30 June 2003?

The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset at the inception of the lease is $20,517.The lease is non-cancellable and at the end of the lease the asset is returned to the lessor.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What is the value of the lease asset and lease liability in the books of the lessee after adjusting entries made on 30 June 2003?

A) Lease asset: $17,908 Lease liability: $18,064

B) Lease asset: $21,352 Lease liability: $21,954

C) Lease asset: $18,465 Lease liability: $18,188

D) Lease asset: $17,460 Lease liability: $17,004

E) None of the given answers.

The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset at the inception of the lease is $20,517.The lease is non-cancellable and at the end of the lease the asset is returned to the lessor.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What is the value of the lease asset and lease liability in the books of the lessee after adjusting entries made on 30 June 2003?A) Lease asset: $17,908 Lease liability: $18,064

B) Lease asset: $21,352 Lease liability: $21,954

C) Lease asset: $18,465 Lease liability: $18,188

D) Lease asset: $17,460 Lease liability: $17,004

E) None of the given answers.

Question

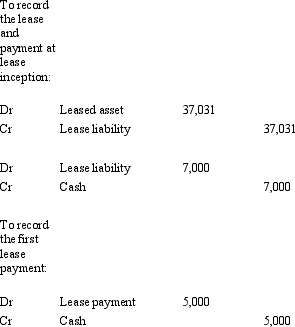

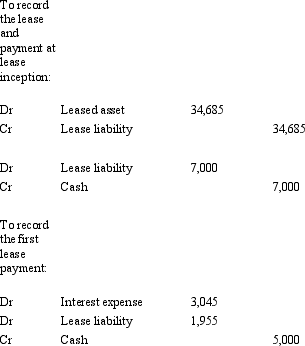

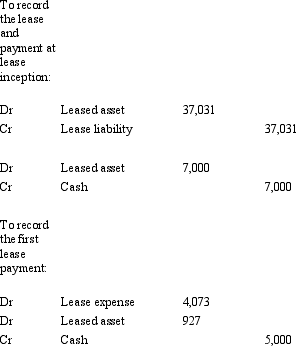

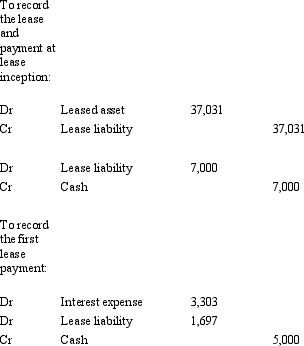

Hoof & Tail Ltd enters into a non-cancellable lease agreement with Equine Industries to lease some equipment under the following conditions:  The interest rate implicit in the lease is 11 per cent and the fair value of the asset at the inception of the lease is $37 031.What are the journal entries to record the lease,the payment at lease inception and the first lease payment in the books of the lessee (rounded to the nearest dollar)?

The interest rate implicit in the lease is 11 per cent and the fair value of the asset at the inception of the lease is $37 031.What are the journal entries to record the lease,the payment at lease inception and the first lease payment in the books of the lessee (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 11 per cent and the fair value of the asset at the inception of the lease is $37 031.What are the journal entries to record the lease,the payment at lease inception and the first lease payment in the books of the lessee (rounded to the nearest dollar)?A)

B)

C)

D)

E) None of the given answers.

Question

Question

The following journal entry,in the books of Lessee Pty Limited,records the lease payment made at 30 June 2010.The actual lease payment,the present value of which was included in the calculation of minimum lease payments at the inception of the lease,is: 30 June 2010

A) 87,000.

B) 93,000.

C) 97,000.

D) 100,000.

E) 110,000

A) 87,000.

B) 93,000.

C) 97,000.

D) 100,000.

E) 110,000

Question

The following is an extract from a lease payment schedule for Lessee Pty Limited.What is the present value of the lease liability at 30 June 2010?

A) 18,006.

B) 19,355.

C) 25,006.

D) 23,657

E) 20,157.

A) 18,006.

B) 19,355.

C) 25,006.

D) 23,657

E) 20,157.

Question

On 1 January 2012 Dobel Ltd signed a ten-year non-cancellable lease that requires a payment of $100 000 at the end of each year.Ownership of the leased asset remains with the lessor at expiry of the lease.The incremental borrowing rate of Dobel Ltd is 12% while the implicit rate of the lessor known to Dobel Ltd is 10%. The following information is also available:

At what amount should the leased property be recorded in the books of Dobel Ltd?

At what amount should the leased property be recorded in the books of Dobel Ltd?

A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

At what amount should the leased property be recorded in the books of Dobel Ltd?A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

Question

Alpine Ltd signed a 10-year non-cancellable lease with Mt Buller Ltd for the use of high-tech equipment.No bargain purchase option is provided in the lease contract. The following information is available.

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?

A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

Question

Question

Question

Question

Question

Question

The following is an extract from a lease payment schedule for Lessee Pty Limited.Assuming Lessee Pty Limited uses the current/non-current dichotomy to disclose liabilities,what are the amounts of (a)current liabilities; and (b)non-current liabilities,relating to this lease,disclosed by Lessee Pty Limited at 30 June 2012?

A) (a) current 2,601; (b) non-current 26,012.

B) (a) current 1,976; (b) non-current 13,268.

C) (a) current 1,796; (b) non-current 15,243.

D) (a) current 1,633; (b) non-current 17,039.

E) Cannot determine from the information provided above.

A) (a) current 2,601; (b) non-current 26,012.

B) (a) current 1,976; (b) non-current 13,268.

C) (a) current 1,796; (b) non-current 15,243.

D) (a) current 1,633; (b) non-current 17,039.

E) Cannot determine from the information provided above.

Question

Question

Question

Question

Question

The following journal entry,in the books of Lessee Pty Limited,records the entry for the depreciation expense at 30 June 2010.The lease term is of 5 years duration.Which of the following statements is correct? 30 June 2010

![<strong>The following journal entry,in the books of Lessee Pty Limited,records the entry for the depreciation expense at 30 June 2010.The lease term is of 5 years duration.Which of the following statements is correct? 30 June 2010 (to record depreciation expense [(739,648 - 120,000)/6]</strong> A) The economic life of the asset is 6 years. B) It is reasonably certain that the lessee will obtain ownership of the asset at the end of the lease term. C) It is reasonably certain that the lessee will not obtain ownership of the asset at the end of the lease term. D) The economic life of the asset is 6 years; and it is reasonably certain that the lessee will obtain ownership of the asset at the end of the lease term. E) The economic life of the asset is 6 years; and it is reasonably certain that the lessee will not obtain ownership of the asset at the end of the lease term. <div style=padding-top: 35px>](https://storage.examlex.com/TB3456/11ea7ef8_b350_6117_b9ea_dd6581e1a068_TB3456_00.jpg) (to record depreciation expense [(739,648 - 120,000)/6]

(to record depreciation expense [(739,648 - 120,000)/6]

A) The economic life of the asset is 6 years.

B) It is reasonably certain that the lessee will obtain ownership of the asset at the end of the lease term.

C) It is reasonably certain that the lessee will not obtain ownership of the asset at the end of the lease term.

D) The economic life of the asset is 6 years; and it is reasonably certain that the lessee will obtain ownership of the asset at the end of the lease term.

E) The economic life of the asset is 6 years; and it is reasonably certain that the lessee will not obtain ownership of the asset at the end of the lease term.

(to record depreciation expense [(739,648 - 120,000)/6]A) The economic life of the asset is 6 years.

B) It is reasonably certain that the lessee will obtain ownership of the asset at the end of the lease term.

C) It is reasonably certain that the lessee will not obtain ownership of the asset at the end of the lease term.

D) The economic life of the asset is 6 years; and it is reasonably certain that the lessee will obtain ownership of the asset at the end of the lease term.

E) The economic life of the asset is 6 years; and it is reasonably certain that the lessee will not obtain ownership of the asset at the end of the lease term.

Question

Kingslake Ltd signed a non-cancellable lease contract on 1 January 2012 for a machine that requires 5 annual payments of $200 000 at the start of each year.On the last annual payment,ownership will transfer from the lessor to Kingslake Ltd.The fair value of the asset if paid in cash is $75,964. The following information is also available:

What is the implicit rate of this lease arrangement in accordance with AASB 117?

What is the implicit rate of this lease arrangement in accordance with AASB 117?

A: 10%

B: 12%

C: 16%

D: Between 10% and 12%

E)Between 12% and 16%

What is the implicit rate of this lease arrangement in accordance with AASB 117?A: 10%

B: 12%

C: 16%

D: Between 10% and 12%

E)Between 12% and 16%

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/78

Play

Full screen (f)

Deck 11: Accounting for Lease

1

In a lease arrangement that is classified by the lessee as an operating the lease payment should be: A: allocated between depreciation expense and interest expense.

B: allocated between the reduction of liability for leased assets and interest expense

C: recognised as rental expense.

D: recognised as interest expense.

E) recognised as depreciation expense.

B: allocated between the reduction of liability for leased assets and interest expense

C: recognised as rental expense.

D: recognised as interest expense.

E) recognised as depreciation expense.

C

2

AASB 117 applies to accounting for leases,including those that relate to lease arrangements to explore for or use natural resources:

False

3

Explain what is meant by a 'direct finance' lease,and how such leases should be accounted under AASB 117.

A direct finance lease is a type of lease where the lessor (the company or individual who owns the asset) transfers substantially all the risks and rewards incidental to ownership of the asset to the lessee (the company or individual who is leasing the asset) without transferring the legal title of the asset. In other words, the lessee is responsible for the maintenance, insurance, and other costs associated with the asset as if they were the owner.

Under AASB 117, a direct finance lease should be accounted for as a finance lease. This means that the lessee should recognize the leased asset as an asset on their balance sheet and recognize a liability for the present value of the lease payments. The lease payments should be apportioned between the finance charge and the reduction of the outstanding liability. The finance charge should be allocated over the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability.

Additionally, the leased asset should be depreciated over its useful life, and the interest portion of the lease payments should be recognized as an expense in the income statement. This accounting treatment reflects the economic reality of the lease, where the lessee effectively has control and use of the asset for the majority of its useful life.

Under AASB 117, a direct finance lease should be accounted for as a finance lease. This means that the lessee should recognize the leased asset as an asset on their balance sheet and recognize a liability for the present value of the lease payments. The lease payments should be apportioned between the finance charge and the reduction of the outstanding liability. The finance charge should be allocated over the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability.

Additionally, the leased asset should be depreciated over its useful life, and the interest portion of the lease payments should be recognized as an expense in the income statement. This accounting treatment reflects the economic reality of the lease, where the lessee effectively has control and use of the asset for the majority of its useful life.

4

At inception of the lease,what is the cost basis of an asset acquired from a lease arrangement when the lease is classified as a finance lease? A: The net realisable value of the asset plus present value of the minimum lease payments.

B: The fair value of the leased asset.

C: The lower of fair value of the leased asset or present value of the minimum lease payments.

D: The lower of fair value of the leased asset or present value of the minimum lease payments plus any initial indirect costs.

E) The sum of the future minimum lease payments.

B: The fair value of the leased asset.

C: The lower of fair value of the leased asset or present value of the minimum lease payments.

D: The lower of fair value of the leased asset or present value of the minimum lease payments plus any initial indirect costs.

E) The sum of the future minimum lease payments.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

5

Alpine Ltd signed a 10-year non-cancellable lease with Mt Buller Ltd for the use of high-tech equipment.No bargain purchase option is provided in the lease contract. The following information is available.

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?

A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

6

If there is reasonable assurance at the inception of the lease that the lessee will obtain ownership of the assets at the end of the lease term,then the leased asset should be depreciated over the lease term.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

7

In a sale and leaseback transaction,if the risks and rewards incidental to ownership effectively pass to the lessor,this arrangement is classified as a finance lease.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

8

Discuss how entities with debt to asset constraints are impacted by the classification of leases as either finance or operating leases.What are the implications for lease accounting?

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

9

Under a lease agreement,the lessee may have control of an asset even if the lessee does not have legal ownership.According to the AASB Framework this is not a sufficient basis for recording an asset:

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

10

If the lease arrangement contains a bargain purchase option,it is reasonable to assume that the risks and rewards of ownership are transferred to the lessee.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

11

A leased asset classified as a finance lease is not subject to depreciation or amortisation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

12

Discuss the issues raised by the IASB and the US FASB on the accounting treatment for operating leases and how this arrangement gives rise to an asset and a liability to the lessee at inception of the lease.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

13

Explain the accounting treatment for a lease arrangement involving both land and building.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

14

The discount rate to be used in calculating the present value of the minimum lease payments is the interest rate implicit to the lease,or if this is not practicable to do so,the lessor's incremental borrowing rate.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

15

Snowy River Ltd is a lessee to two lease arrangements.Lease A is non-cancellable,contains a bargain purchase option and the lease term is equal to 75 per cent of the economic life of the asset.Lease B is non-cancellable,lease term is less than 60% of the economic life of the asset and the minimum lease payment represents 75% of the fair value of the leased asset. How should Snowy River Ltd classify Lease A and Lease B,respectively?

A: Operating lease; Operating lease;

B: Operating lease; Finance lease

C: Finance lease; Finance lease;

D: Finance lease; Operating lease;

E) None of the given answers.

A: Operating lease; Operating lease;

B: Operating lease; Finance lease

C: Finance lease; Finance lease;

D: Finance lease; Operating lease;

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

16

On 1 January 2012 Dobel Ltd signed a ten-year non-cancellable lease that requires a payment of $100 000 at the end of each year.Ownership of the leased asset remains with the lessor at expiry of the lease.The incremental borrowing rate of Dobel Ltd is 12% while the implicit rate of the lessor known to Dobel Ltd is 10%. The following information is also available:

At what amount should the leased property be recorded in the books of Dobel Ltd?

A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

At what amount should the leased property be recorded in the books of Dobel Ltd?A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

17

Describe how a lessee would account for the amortisation of a leased asset.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

18

Kingslake Ltd signed a non-cancellable lease contract on 1 January 2012 for a machine that requires 5 annual payments of $200 000 at the start of each year.On the last annual payment,ownership will transfer from the lessor to Kingslake Ltd.The fair value of the asset if paid in cash is $75,964. The following information is also available:

What is the implicit rate of this lease arrangement in accordance with AASB 117?

A: 10%

B: 12%

C: 16%

D: Between 10% and 12%

E)Between 12% and 16%

What is the implicit rate of this lease arrangement in accordance with AASB 117?A: 10%

B: 12%

C: 16%

D: Between 10% and 12%

E)Between 12% and 16%

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

19

Contingent rent is included in the determination of minimum lease payments under AASB 117 "Leases".

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

20

Describe 'lease incentives' and how they should be accounting according to AASB 117.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

21

Johnson Ltd enters into a lease agreement with Peterson Ltd under the following conditions: The lease may be cancelled only with the permission of the lessor.If the rate of interest implicit in the lease is 10 per cent,what is the fair value of the asset at the inception of the lease,and is the lease a finance or operating lease?

A) $56,745, finance lease.

B) $52,596, operating lease.

C) $56,745, operating lease.

D) $52,596, finance lease.

E) None of the given answers.

The lease may be cancelled only with the permission of the lessor.If the rate of interest implicit in the lease is 10 per cent,what is the fair value of the asset at the inception of the lease,and is the lease a finance or operating lease?A) $56,745, finance lease.

B) $52,596, operating lease.

C) $56,745, operating lease.

D) $52,596, finance lease.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

22

Kensington Ltd decides to lease some equipment from Piccadilly Ltd on the following terms: If the interest rate implicit in the lease is 8 per cent,what is the fair value of the equipment at the inception of the lease (rounded to the nearest dollar)?

A) $44 518

B) $46 094

C) $40 094

D) $48 399

E) None of the given answers.

If the interest rate implicit in the lease is 8 per cent,what is the fair value of the equipment at the inception of the lease (rounded to the nearest dollar)?A) $44 518

B) $46 094

C) $40 094

D) $48 399

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

23

A guaranteed residual value is that part of the residual value that is guaranteed by the lessee,or by a party related to the lessee.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

24

An owner of an asset may sell it and then lease it back from the new owner.Where this lease meets the conditions to be classified as a finance lease,the profit or loss on the sale of the asset recorded by the lessee should be classified as a finance item in the income statement in the year of the sale.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

25

AASB 117 defines the benefits of ownership to include.

A) Those obtainable from the insurance claims associated with it.

B) Those obtainable from gains in the realisable value of the asset.

C) Those obtainable from the profitable use of the asset.

D) Those obtainable from gains in the realisable value of the asset and those obtainable from the profitable use of the asset.

E) All of the given answers.

A) Those obtainable from the insurance claims associated with it.

B) Those obtainable from gains in the realisable value of the asset.

C) Those obtainable from the profitable use of the asset.

D) Those obtainable from gains in the realisable value of the asset and those obtainable from the profitable use of the asset.

E) All of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

26

In reference to the statement,'.....if the non-cancellable lease term is for the major part of the economic life of the asset,the lease is generally considered to be a finance lease",AASB 117 defines "major part" as 75 per cent:

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

27

An operating lease is one in which:

A) The lessee agrees to maintain the operating capability of the asset to a level specified by the lessor.

B) The risks and benefits of ownership reside with the lessor.

C) The lessee is required to maintain the leased asset according to an agreed maintenance schedule.

D) The risks and benefits of ownership reside with the lessor and the lessee is required to maintain the leased asset according to an agreed maintenance schedule.

E) None of the given answers.

A) The lessee agrees to maintain the operating capability of the asset to a level specified by the lessor.

B) The risks and benefits of ownership reside with the lessor.

C) The lessee is required to maintain the leased asset according to an agreed maintenance schedule.

D) The risks and benefits of ownership reside with the lessor and the lessee is required to maintain the leased asset according to an agreed maintenance schedule.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

28

The term 'bargain purchase option' is not used explicitly in AASB 117 but is described as:

A) The option to purchase the leased asset for significantly less than its cost at the date the option becomes exercisable, for it be reasonable certain at the inception of the lease, that the option will be exercised.

B) The option to purchase the asset at a price that is expected to be sufficiently lower that the fair value at the date the option becomes exercisable, for it be reasonable certain at the inception of the lease, that the option will be exercised.

C) Being in place when the lessee is guaranteed to undertake the option at the end of the lease.

D) The option to purchase the asset at a price that is expected to be sufficiently lower that the fair value at the date the option becomes exercisable, for it be reasonable certain at the inception of the lease, that the option will be exercised and being in place when the lessee is guaranteed to undertake the option at the end of the lease.

E) None of the given answers.

A) The option to purchase the leased asset for significantly less than its cost at the date the option becomes exercisable, for it be reasonable certain at the inception of the lease, that the option will be exercised.

B) The option to purchase the asset at a price that is expected to be sufficiently lower that the fair value at the date the option becomes exercisable, for it be reasonable certain at the inception of the lease, that the option will be exercised.

C) Being in place when the lessee is guaranteed to undertake the option at the end of the lease.

D) The option to purchase the asset at a price that is expected to be sufficiently lower that the fair value at the date the option becomes exercisable, for it be reasonable certain at the inception of the lease, that the option will be exercised and being in place when the lessee is guaranteed to undertake the option at the end of the lease.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

29

In determining if the risk and rewards of ownership have been transferred,AASB 117 states the following would indicate a finance lease is in effect:

A) Ownership of the assets transfers at the end of the lease term for a variable payment equal to its then fair value.

B) Contingent rents exist.

C) The lease is non-cancellable by the lessor.

D) The lease term is for a major part of the economic life of the asset.

E) All of the given answers.

A) Ownership of the assets transfers at the end of the lease term for a variable payment equal to its then fair value.

B) Contingent rents exist.

C) The lease is non-cancellable by the lessor.

D) The lease term is for a major part of the economic life of the asset.

E) All of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

30

At the commencement of the lease term,lessees are to recognise finance leases as assets and liabilities in their balance sheets measured at the lower of: the fair value of the leased asset and the present value of minimum lease payment; determined at the inception of the lease.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

31

A non-cancellable lease,which transfers the risks and rewards associated with asset ownership,can still be terminated early with the permission of the lessor.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

32

The central accounting issue associated with leases is:

A) The timing of the recognition of the lease payments.

B) Whether or not the leased assets should be treated as assets of the lessee.

C) The treatment of provisions for the repairs and maintenance on leased assets.

D) The method of recording any commitment to guarantee the value of the asset at the end of the lease term.

E) All of the given answers.

A) The timing of the recognition of the lease payments.

B) Whether or not the leased assets should be treated as assets of the lessee.

C) The treatment of provisions for the repairs and maintenance on leased assets.

D) The method of recording any commitment to guarantee the value of the asset at the end of the lease term.

E) All of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

33

In the situation where there is an unguaranteed residual in a finance lease agreement,the leased asset will be recorded in the books of the lessee at an amount less than its fair value at the inception of the lease.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

34

A leased asset under a finance lease should be amortised over the asset's expected useful life if there is a bargain purchase option in the lease agreement:

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

35

A finance lease is one in which substantially all the risks and benefits of ownership pass to the lessee.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

36

Minimum lease payments include.

A) Any bargain purchase option amount.

B) Any rentals paid to reimburse the lessor for executory costs.

C) Contingent rentals.

D) Unguaranteed residuals.

E) All of the given answers.

A) Any bargain purchase option amount.

B) Any rentals paid to reimburse the lessor for executory costs.

C) Contingent rentals.

D) Unguaranteed residuals.

E) All of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

37

In the case of a finance lease,the accounting treatment by the lessee could.

A) Calculate the IRR implicit in the lease contract and disclose it in the notes to the accounts.

B) Provide note disclosure to the accounts and recognise the lease payments in the same way as a rental expense.

C) Accrue the lease payments and match them against revenues earned by using a unit of production method.

D) Recognise an asset and associated liability equal in value to the present value of the minimum lease payments.

E) None of the given answers.

A) Calculate the IRR implicit in the lease contract and disclose it in the notes to the accounts.

B) Provide note disclosure to the accounts and recognise the lease payments in the same way as a rental expense.

C) Accrue the lease payments and match them against revenues earned by using a unit of production method.

D) Recognise an asset and associated liability equal in value to the present value of the minimum lease payments.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

38

The initial direct costs of a sales-type lease,borne by the lessor,are to be accounted for by the lessor as part of the lease receivable.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

39

In circumstances where the lessee is unable to determine the implicit interest rate in a lease agreement,AASB 117 requires the lessee to use.

A) The incremental lending rate of the lessor.

B) The weighted average cost of capital of the lessee.

C) The incremental borrowing rate of the lessee.

D) The internal rate of return on similar projects adopted by the lessor.

E) None of the given answers.

A) The incremental lending rate of the lessor.

B) The weighted average cost of capital of the lessee.

C) The incremental borrowing rate of the lessee.

D) The internal rate of return on similar projects adopted by the lessor.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

40

If a lease transfers ownership of the property to the lessee,or contains a bargain purchase option,then this is consistent with the lease being an operating lease.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

41

The rental payments made during the term of a finance lease.

A) Are reductions of the lease liability that should be debited to the liability account.

B) Are an expense that should be recognised in the annual income statements.

C) Need to be divided into an interest component and an expense component. The expense effectively shows the amortisation of the lease asset.

D) Should be considered as a payment of principal (reduction in the lease liability) and interest (an annual expense).

E) None of the given answers.

A) Are reductions of the lease liability that should be debited to the liability account.

B) Are an expense that should be recognised in the annual income statements.

C) Need to be divided into an interest component and an expense component. The expense effectively shows the amortisation of the lease asset.

D) Should be considered as a payment of principal (reduction in the lease liability) and interest (an annual expense).

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

42

Cobalt Ltd owns an item of machinery that has a cost of $700,000 and accumulated depreciation of $200,000 as at 1 July 2003.On that date the machine is sold to Blue Ltd for $533,493,and then leased back over 8 years (the remaining life of the machine).The lease is non-cancellable.The lease payments are $100,000 per annum,payable in arrears on 30 June each year.The interest rate implicit in the lease is 10 per cent and the economic benefits of the asset are expected to be realised evenly over its life.What are the entries to record the transactions in Cobalt's books on 1 July 2003 and 30 June 2004 (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

43

Under AASB 117,operating leases require the following disclosures by lessees:

A) The total of future minimum sublease payments expected to be received under non-cancellable subleases at the balance sheet date.

B) A general description of the lessee's significant leasing arrangements.

C) No disclosures are required as operating leases are expensed each year.

D) The total of future minimum sublease payments expected to be received under non-cancellable subleases at the balance sheet date and a general description of the lessee's significant leasing arrangements.

E) The net carrying amount at balance sheet date for each class of asset.

A) The total of future minimum sublease payments expected to be received under non-cancellable subleases at the balance sheet date.

B) A general description of the lessee's significant leasing arrangements.

C) No disclosures are required as operating leases are expensed each year.

D) The total of future minimum sublease payments expected to be received under non-cancellable subleases at the balance sheet date and a general description of the lessee's significant leasing arrangements.

E) The net carrying amount at balance sheet date for each class of asset.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

44

Fresco Ltd enters into a non-cancellable lease agreement with Meola Ltd to lease some equipment under the following conditions: The interest rate implicit in the lease is 9 per cent and the fair value of the asset at the inception of the lease is $81,199.What are the journal entries to record the lease payment at inception of the lease,and the next two lease payments,in the books of the lessee (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 9 per cent and the fair value of the asset at the inception of the lease is $81,199.What are the journal entries to record the lease payment at inception of the lease,and the next two lease payments,in the books of the lessee (rounded to the nearest dollar)?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

45

Medusa Ltd enters into a non-cancellable 10-year lease with Lennox Ltd on 1 July 2003.The lease is for an item of equipment that at the inception of the lease has a fair value of $322,572 (the amount that Medusa paid for the asset on 1 July 2003).The equipment is expected to have a useful life of 12 years and the lease term is for 10 years.The lease contract includes a bargain purchase option of $4,000 that Lennox Ltd will be able to exercise at the end of the 10-year lease.The lease payments will be made on 30 June each year,beginning 30 June 2004.The payments are to be $55,000 each year with $5,000 of this being for executory costs to cover maintenance of the equipment.The maintenance will be carried out annually.The interest rate implicit in the lease is 9 per cent.What are the entries in the books of Medusa Ltd for 1 July 2003 and 30 June 2004 (round amounts to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

46

A non-cancellable lease is a lease that is cancellable only:

A) Upon the occurrence of some probable contingency.

B) With the permission of the lessee.

C) If the lessee enters into a new lease for the same or equivalent asset with the same lessor.

D) Upon payment by the lessor of such an additional amount that, at inception of the lease, continuation of the lease is certain.

E) All of the given answers.

A) Upon the occurrence of some probable contingency.

B) With the permission of the lessee.

C) If the lessee enters into a new lease for the same or equivalent asset with the same lessor.

D) Upon payment by the lessor of such an additional amount that, at inception of the lease, continuation of the lease is certain.

E) All of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

47

Gerbert Ltd enters into a finance lease with Hokiman Ltd on 1 July 2002 for an item of machinery that has a fair value at that date of $226,718.The lease is for a period of 4 years,with annual lease payments of $62,000 due on 30 June each year,the first payment to be made in 2003.There is a bargain purchase option of $15,000 available for Hokiman to exercise at the end of the lease period.The rate of interest implicit in the lease is 6 per cent.It cost Gerbert Ltd $190,000 to manufacture the machine.What are the entries in the books of Gerbert Ltd for 1 July 2002 and 30 June 2003 (round amounts to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

48

A finance lease in which the lessor provides the financial resources to acquire an asset and retains ownership while the control of the asset and the risks and benefits of ownership pass to the lessee,may be considered from the perspective of the lessor to be a(n):

A) Sales-type lease.

B) Operating lease.

C) Direct finance lease.

D) Executory lease.

E) None of the given answers.

A) Sales-type lease.

B) Operating lease.

C) Direct finance lease.

D) Executory lease.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

49

Where a sale and leaseback arrangement involves the benefits and risks of ownership being maintained by the lessee.

A) The lease back is classified as a finance lease.

B) The owner has effectively refinanced the asset.

C) Any profit on the sale should be deferred in the balance sheet and amortised.

D) The owner has managed to obtain funds from the sale but also maintained control of the asset.

E) None of the given answers.

A) The lease back is classified as a finance lease.

B) The owner has effectively refinanced the asset.

C) Any profit on the sale should be deferred in the balance sheet and amortised.

D) The owner has managed to obtain funds from the sale but also maintained control of the asset.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

50

Quaid Ltd entered into a lease agreement on 1 July 2002 to lease equipment on the following terms: The interest rate implicit in the lease is 8 per cent and the fair value of the leased asset is $24,987.The lease is cancellable if the lessee immediately enters into a further lease for the same or equivalent asset.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.The lease payment has not been made on 30 June before the adjusting entries are made for the year end.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2003?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 8 per cent and the fair value of the leased asset is $24,987.The lease is cancellable if the lessee immediately enters into a further lease for the same or equivalent asset.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.The lease payment has not been made on 30 June before the adjusting entries are made for the year end.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2003?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

51

From the point of view of the lessor,any lease rentals that are a recovery of executory costs should be treated as:

A) A reduction in the lease receivable in the period in which they are received.

B) A reduction in interest revenue in the period that the costs are incurred.

C) An increase in unearned revenue in the period in which the lease rental is received.

D) Revenue in the periods in which the related costs are incurred.

E) None of the given answers.

A) A reduction in the lease receivable in the period in which they are received.

B) A reduction in interest revenue in the period that the costs are incurred.

C) An increase in unearned revenue in the period in which the lease rental is received.

D) Revenue in the periods in which the related costs are incurred.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

52

Schwann Ltd enters into a non-cancellable 5-year lease for office space in Bigtown's central business district.The building has an expected remaining life of 40 years.Schwann Ltd has been offered a free fit-out of the office as an incentive to take up the lease.The fit-out would have cost Schwann Ltd $90,000 to do itself.The benefits of the fit-out are to be recognised on a straight-line basis.The rental payments are $110,000 per annum.How would the signing of the lease and the first rental payment be recorded by Schwann Ltd in accordance with UIG Abstract 3?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

53

Where there is a lease involving a manufacturer or dealer:

A) There are really two parts to the transaction.

B) There will be a difference between the cost of the asset to the lessor and its fair value at the inception of the lease.

C) The lessor's investment would be accounted for in the same way as a direct-financing lease.

D) There are really two parts to the transaction and there will be a difference between the cost of the asset to the lessor and its fair value at the inception of the lease.

E) All of the given answers.

A) There are really two parts to the transaction.

B) There will be a difference between the cost of the asset to the lessor and its fair value at the inception of the lease.

C) The lessor's investment would be accounted for in the same way as a direct-financing lease.

D) There are really two parts to the transaction and there will be a difference between the cost of the asset to the lessor and its fair value at the inception of the lease.

E) All of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

54

The amount of a lease receivable recorded by the lessor for a direct finance lease should equal at the beginning of the lease term:

A) The aggregate of the present value of the minimum lease and executory payments and the present value of any unguaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term.

B) The aggregate of the present value of the minimum lease payments and the present value of any unguaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term. Any initial direct costs should also be included in the lease receivable.

C) The aggregate of the present value of the total lease payments and the present value of any guaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term.

D) The aggregate of the present value of the minimum lease payments and the present value of any guaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term, plus any initial direct costs.

E) None of the given answers.

A) The aggregate of the present value of the minimum lease and executory payments and the present value of any unguaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term.

B) The aggregate of the present value of the minimum lease payments and the present value of any unguaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term. Any initial direct costs should also be included in the lease receivable.

C) The aggregate of the present value of the total lease payments and the present value of any guaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term.

D) The aggregate of the present value of the minimum lease payments and the present value of any guaranteed residual value expected to accrue to the benefit of the lessor at the end of the lease term, plus any initial direct costs.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

55

Cobalt Ltd owns an item of machinery that has a cost of $700,000 and accumulated depreciation of $200,000 as at 1 July 2003.On that date the machine is sold to Blue Ltd for $533,493,and then leased back over 8 years (the remaining life of the machine).The lease is non-cancellable.The lease payments are $100,000 per annum,payable in arrears on 30 June each year.The interest rate implicit in the lease is 10 per cent and the economic benefits of the asset are expected to be realised evenly over its life.What are the entries to record the transactions in Blue's books on 1 July 2003 and 30 June 2004 (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

56

Where a lessor is involved in a finance lease (risk has passed to the lessee)the lessor must:

A) Remove the asset in question from their balance sheet as they no longer own it.

B) Record a new asset on their balance sheet, a lease receivable, to replace the leased asset.

C) Only record the revenue earned from lease payments in the income statement as they are received.

D) Record the sale of the asset to the lessee to ensure the accounting records accurately reflect control of the leased asset.

E) None of the given answers.

A) Remove the asset in question from their balance sheet as they no longer own it.

B) Record a new asset on their balance sheet, a lease receivable, to replace the leased asset.

C) Only record the revenue earned from lease payments in the income statement as they are received.

D) Record the sale of the asset to the lessee to ensure the accounting records accurately reflect control of the leased asset.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

57

Mitchum Ltd entered into a lease agreement on 1 July 2003 to lease equipment on the following terms: The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset is $13,316.The lease is cancellable at the option of the lessee.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2004?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset is $13,316.The lease is cancellable at the option of the lessee.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What are the appropriate entries in the books of the lessee at the end of the reporting period 30 June 2004?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

58

A sale and leaseback arrangement may involve an operating lease where the benefits and risks of ownership have effectively passed to the lessor.In this situation if the sale is not made at the fair value of the asset,the appropriate treatment is to:

A) Write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is above fair value the excess of sales price over fair value must be deferred and amortised by the lessee in proportion to the rental payments over the lease term.

B) Revalue the asset to fair value and in the case that the sale price is less than the fair value write-off the loss to the income statement in the period of the sale. In the case that the sale price is greater than the fair value, the profit should be deferred and amortised against the future rental payments.

C) Write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is below fair value any profit or loss must be recognised immediately by the lessee except that, to the extent the loss is compensated by future rentals at below market price, it must be deferred and amortised in proportion to the rental payments over the lease term.

D) Write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is above fair value the excess of sales price over fair value must be deferred and amortised by the lessee in proportion to the rental payments over the lease term and write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is below fair value any profit or loss must be recognised immediately by the lessee except that, to the extent the loss is compensated by future rentals at below market price, it must be deferred and amortised in proportion to the rental payments over the lease term.

E) None of the given answers.

A) Write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is above fair value the excess of sales price over fair value must be deferred and amortised by the lessee in proportion to the rental payments over the lease term.

B) Revalue the asset to fair value and in the case that the sale price is less than the fair value write-off the loss to the income statement in the period of the sale. In the case that the sale price is greater than the fair value, the profit should be deferred and amortised against the future rental payments.

C) Write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is below fair value any profit or loss must be recognised immediately by the lessee except that, to the extent the loss is compensated by future rentals at below market price, it must be deferred and amortised in proportion to the rental payments over the lease term.

D) Write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is above fair value the excess of sales price over fair value must be deferred and amortised by the lessee in proportion to the rental payments over the lease term and write-down the asset to its fair value where the carrying value is greater than the fair value. Where the sale price is below fair value any profit or loss must be recognised immediately by the lessee except that, to the extent the loss is compensated by future rentals at below market price, it must be deferred and amortised in proportion to the rental payments over the lease term.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

59

Joplin Ltd entered into a lease agreement on 1 July 2002 with Thomas Ltd.The terms of the lease are as follows: The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset at the inception of the lease is $20,517.The lease is non-cancellable and at the end of the lease the asset is returned to the lessor.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What is the value of the lease asset and lease liability in the books of the lessee after adjusting entries made on 30 June 2003?

A) Lease asset: $17,908 Lease liability: $18,064

B) Lease asset: $21,352 Lease liability: $21,954

C) Lease asset: $18,465 Lease liability: $18,188

D) Lease asset: $17,460 Lease liability: $17,004

E) None of the given answers.

The interest rate implicit in the lease is 6 per cent and the fair value of the leased asset at the inception of the lease is $20,517.The lease is non-cancellable and at the end of the lease the asset is returned to the lessor.The economic benefits provided by the lease asset are expected to be consumed evenly over its life.What is the value of the lease asset and lease liability in the books of the lessee after adjusting entries made on 30 June 2003?A) Lease asset: $17,908 Lease liability: $18,064

B) Lease asset: $21,352 Lease liability: $21,954

C) Lease asset: $18,465 Lease liability: $18,188

D) Lease asset: $17,460 Lease liability: $17,004

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

60

Hoof & Tail Ltd enters into a non-cancellable lease agreement with Equine Industries to lease some equipment under the following conditions: The interest rate implicit in the lease is 11 per cent and the fair value of the asset at the inception of the lease is $37 031.What are the journal entries to record the lease,the payment at lease inception and the first lease payment in the books of the lessee (rounded to the nearest dollar)?

A)

B)

C)

D)

E) None of the given answers.

The interest rate implicit in the lease is 11 per cent and the fair value of the asset at the inception of the lease is $37 031.What are the journal entries to record the lease,the payment at lease inception and the first lease payment in the books of the lessee (rounded to the nearest dollar)?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

61

Lease incentives are.

A) Not covered by AASB 117 and therefore may lead to divergent practices.

B) Revenues for the lessees and may be recorded in the initial period of the lease contract.

C) Designed to entice lessees to enter into non-cancellable operating leases.

D) Not covered by AASB 117 and therefore may lead to divergent practices and designed to entice lessees to enter into non-cancellable operating leases.

E) None of the given answers.

A) Not covered by AASB 117 and therefore may lead to divergent practices.

B) Revenues for the lessees and may be recorded in the initial period of the lease contract.

C) Designed to entice lessees to enter into non-cancellable operating leases.

D) Not covered by AASB 117 and therefore may lead to divergent practices and designed to entice lessees to enter into non-cancellable operating leases.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

62

The following journal entry,in the books of Lessee Pty Limited,records the lease payment made at 30 June 2010.The actual lease payment,the present value of which was included in the calculation of minimum lease payments at the inception of the lease,is: 30 June 2010

A) 87,000.

B) 93,000.

C) 97,000.

D) 100,000.

E) 110,000

A) 87,000.

B) 93,000.

C) 97,000.

D) 100,000.

E) 110,000

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

63

The following is an extract from a lease payment schedule for Lessee Pty Limited.What is the present value of the lease liability at 30 June 2010?

A) 18,006.

B) 19,355.

C) 25,006.

D) 23,657

E) 20,157.

A) 18,006.

B) 19,355.

C) 25,006.

D) 23,657

E) 20,157.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

64

On 1 January 2012 Dobel Ltd signed a ten-year non-cancellable lease that requires a payment of $100 000 at the end of each year.Ownership of the leased asset remains with the lessor at expiry of the lease.The incremental borrowing rate of Dobel Ltd is 12% while the implicit rate of the lessor known to Dobel Ltd is 10%. The following information is also available:

At what amount should the leased property be recorded in the books of Dobel Ltd?

A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

At what amount should the leased property be recorded in the books of Dobel Ltd?A: $0;

B: $565 020;

C: $614 460;

D: $1 000 000;

E)None of the given answer.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

65

Alpine Ltd signed a 10-year non-cancellable lease with Mt Buller Ltd for the use of high-tech equipment.No bargain purchase option is provided in the lease contract. The following information is available.

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?

A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

What is the amount to be recorded as an asset and a liability in the books of the lessee that is in accordance with AASB 117 "Leases"?A: $0;

B: $120 000;

C: $125 000;

D: $200 000;

E) None of the given answers

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

66

For a lessee entering into a finance lease,initial direct costs are.

A) Expensed immediately.

B) Expensed at the end of the lease term.

C) Capitalised as part of the lease receivable.

D) Capitalised as part of the cost of the leased asset.

E) None of the given answers.

A) Expensed immediately.

B) Expensed at the end of the lease term.

C) Capitalised as part of the lease receivable.

D) Capitalised as part of the cost of the leased asset.

E) None of the given answers.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

67

Paragraph 47 of AASB 117 requires that for a finance lease,the lessor must disclose.

A) the guaranteed residual values accruing to the lessor.

B) unearned finance income.

C) contingent rents recognised as expenses in the period.

D) the guaranteed residual values accruing to the lessor and unearned finance income.

E) None of the given answers

A) the guaranteed residual values accruing to the lessor.

B) unearned finance income.

C) contingent rents recognised as expenses in the period.

D) the guaranteed residual values accruing to the lessor and unearned finance income.

E) None of the given answers

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

68

For a depreciable asset,the amount of depreciation recognised shall be in accordance with AASB 116.The asset shall be.

A) Fully depreciated over the shorter of the lease term and its useful life, if there is a reasonable certainty that the lessee will obtain ownership by the end of the lease term.