Deck 10: Accounting Changes

Full screen (f)

Question

Question

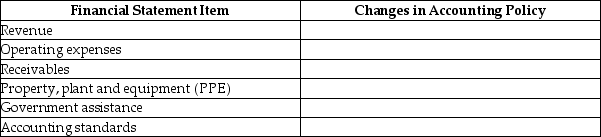

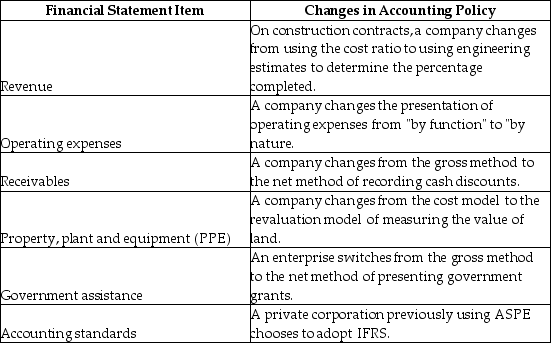

Complete the following table by giving one example of a change in accounting policy for each financial statement item.

Question

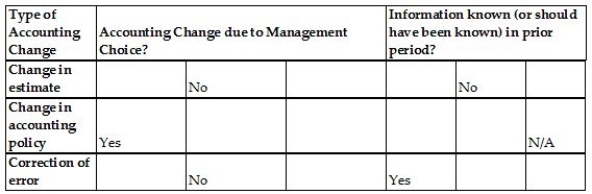

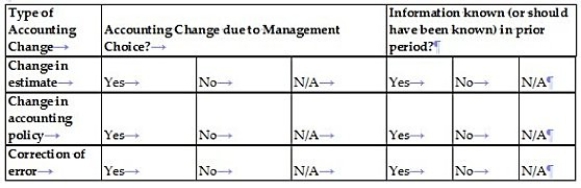

For the following types of accounting changes,identify the relevant criteria for each accounting change by selecting "yes," "no," or "n/a" (not applicable).

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

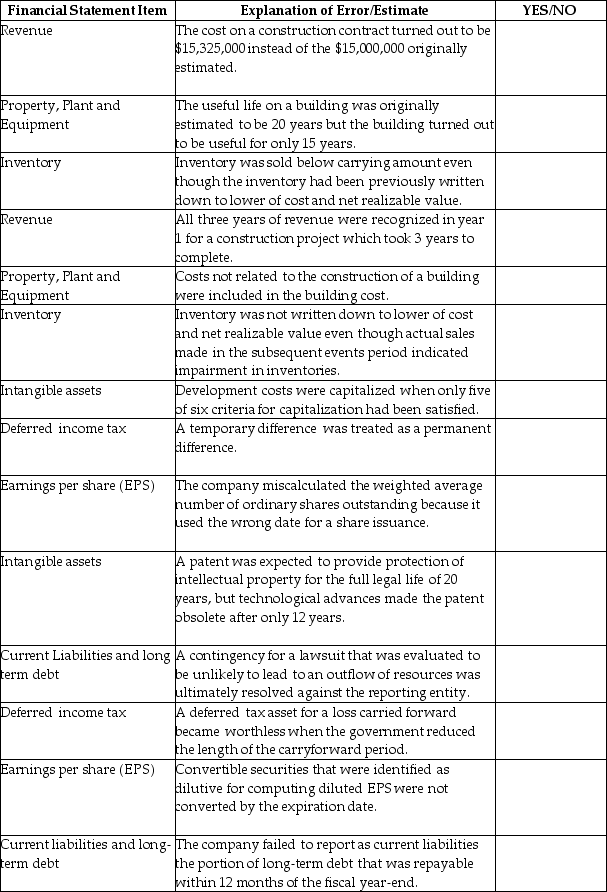

Complete the following table indicating which of the following requires a correction due to an error from a prior period?

Question

Question

Question

Question

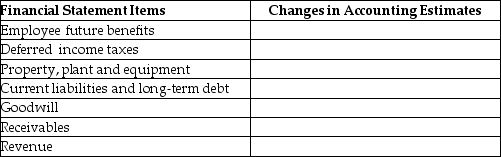

Complete the table giving an example of a change in estimate from each of the given areas.

Question

Question

Question

For the following financial statement accounts,provide a description of a change in accounting estimates.

Question

Question

Question

Question

Question

Question

During the audit of Keats Island Brewery for the fiscal year-ended June 30,2018,the auditors identified the following issues:

For each of the three issues described below,using the following table,identify both the direction (increase or decrease)and the amount of the effect relative to the amount without the accounting change.

a.The company sells beer for $1 each plus $0.10 deposit on each bottle.The deposit collected is payable to the provincial recycling agency.During 2017,the company had recorded $12,000 of deposits as revenue.The auditors believe this amount should have been recorded as a liability.

b.The company had been using the first-in,first-out cost flow assumption for its inventories.In fiscal 2018,management decided to switch to the weighted-average method.This change reduced inventory by $25,000 at June 30,2017,and $40,000 at June 30,2018.

c.The company has equipment costing $6,000,000 that it has been depreciating over 10 years on a straight-line basis.The depreciation for fiscal 2017 was $600,000 and accumulated depreciation on

June 30,2017,was $1,200,000.During 2018,management revises the estimate of useful life to 12 years,reducing the amount of depreciation to $480,000 per year.

For each of the three issues described below,using the following table,identify both the direction (increase or decrease)and the amount of the effect relative to the amount without the accounting change.

a.The company sells beer for $1 each plus $0.10 deposit on each bottle.The deposit collected is payable to the provincial recycling agency.During 2017,the company had recorded $12,000 of deposits as revenue.The auditors believe this amount should have been recorded as a liability.

b.The company had been using the first-in,first-out cost flow assumption for its inventories.In fiscal 2018,management decided to switch to the weighted-average method.This change reduced inventory by $25,000 at June 30,2017,and $40,000 at June 30,2018.

c.The company has equipment costing $6,000,000 that it has been depreciating over 10 years on a straight-line basis.The depreciation for fiscal 2017 was $600,000 and accumulated depreciation on

June 30,2017,was $1,200,000.During 2018,management revises the estimate of useful life to 12 years,reducing the amount of depreciation to $480,000 per year.

Question

Question

Question

Question

Evaluate each of the following independent situations to determine the type of accounting change (correction of error,change in accounting policy,or change in estimate)and the appropriate accounting treatment (retrospective or prospective).

Question

Question

Question

Question

Question

For each of the following scenarios,determine the effects (if any)of the accounting change (correction of error,change in accounting policy,or change in estimate)on the relevant asset or liability,equity,and comprehensive income in the year of change and the prior year.Use the following table for your response:

a.Company A increases the allowance for doubtful accounts (ADA).Using the old estimate,ADA would have been $45,000.The new estimate is $50,000.

a.Company A increases the allowance for doubtful accounts (ADA).Using the old estimate,ADA would have been $45,000.The new estimate is $50,000.

b.Company B omitted to record an invoice for a $10,000 sale made on credit at the end of the previous year and incorrectly recorded the sale in the current year.The related inventory sold has been accounted for.

c.Company C changes its revenue recognition to a more conservative policy.The result is a decrease in prior-year revenue by $4,000 and a decrease in current-year revenue by $5,000 relative to the amounts under the old policy.

a.Company A increases the allowance for doubtful accounts (ADA).Using the old estimate,ADA would have been $45,000.The new estimate is $50,000.b.Company B omitted to record an invoice for a $10,000 sale made on credit at the end of the previous year and incorrectly recorded the sale in the current year.The related inventory sold has been accounted for.

c.Company C changes its revenue recognition to a more conservative policy.The result is a decrease in prior-year revenue by $4,000 and a decrease in current-year revenue by $5,000 relative to the amounts under the old policy.

Question

Question

For the following accounting changes,identify the appropriate treatment under IFRS.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

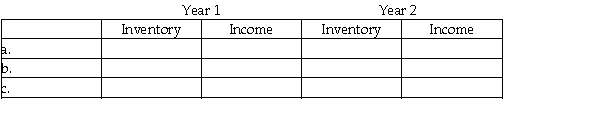

Canlan Inc.is a subsidiary of a Canadian publicly traded manufacturer of construction materials.The company uses the first-in,first-out (FIFO)cost flow assumption.

a.An invoice for $55,000 of material received and used in production arrived after the year-end.Neither the purchase nor the accounts payable was recorded until year two.However,the amount of raw materials in ending inventory was correct based on the inventory count.

b.One of Canlan's products became obsolete and worthless during Year 1,but the inventory writedown did not occur until Year 2.The cost of this inventory was $225,000.

c.In the Year 1 closing inventory count,employees improperly included 2,000 units of finished goods that had already been sold to customers.These units had a cost of $20,000 under FIFO.

Required:

For each of the above independent scenarios (a)through (c),indicate in the following table the effect of the accounting errors on the books of Canlan Inc.Specifically,identify the amount and direction of over- or understatement of inventory and income for Year 1 and Year 2.If an account requires no adjustment,indicate that the account is "correct."

a.An invoice for $55,000 of material received and used in production arrived after the year-end.Neither the purchase nor the accounts payable was recorded until year two.However,the amount of raw materials in ending inventory was correct based on the inventory count.

b.One of Canlan's products became obsolete and worthless during Year 1,but the inventory writedown did not occur until Year 2.The cost of this inventory was $225,000.

c.In the Year 1 closing inventory count,employees improperly included 2,000 units of finished goods that had already been sold to customers.These units had a cost of $20,000 under FIFO.

Required:

For each of the above independent scenarios (a)through (c),indicate in the following table the effect of the accounting errors on the books of Canlan Inc.Specifically,identify the amount and direction of over- or understatement of inventory and income for Year 1 and Year 2.If an account requires no adjustment,indicate that the account is "correct."

Question

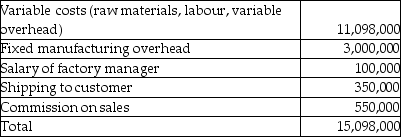

Albacore Sailboats manufactures small sailing dinghies.In 2019,the company's accountant recorded the following costs into the inventory account:

The company had no work in process at the end of both 2018 and 2019.Finished goods at the end of 2018 amounted to 6,000 sailboats at $300/boat.Production was 50,000 sailboats and 4,000 boats remained in inventory at December 31,2019.The company uses a periodic inventory system and the FIFO cost flow assumption.

The company had no work in process at the end of both 2018 and 2019.Finished goods at the end of 2018 amounted to 6,000 sailboats at $300/boat.Production was 50,000 sailboats and 4,000 boats remained in inventory at December 31,2019.The company uses a periodic inventory system and the FIFO cost flow assumption.

Required:

a.Of the $15,098,000,how much should have been capitalized into inventories?

b.Compute the ending value of inventory and the cost of goods sold for 2019.

c.If the error in inventory costing had not been corrected as per part (a),by how much would inventory be overstated at the end of 2019?

d.Record the journal entry to correct the error in inventory costing.

The company had no work in process at the end of both 2018 and 2019.Finished goods at the end of 2018 amounted to 6,000 sailboats at $300/boat.Production was 50,000 sailboats and 4,000 boats remained in inventory at December 31,2019.The company uses a periodic inventory system and the FIFO cost flow assumption.Required:

a.Of the $15,098,000,how much should have been capitalized into inventories?

b.Compute the ending value of inventory and the cost of goods sold for 2019.

c.If the error in inventory costing had not been corrected as per part (a),by how much would inventory be overstated at the end of 2019?

d.Record the journal entry to correct the error in inventory costing.

Question

Question

Star Company Ltd.,is a private company that started on January 1,2017.During an external audit that was conducted at the end of the second year of the company's operation (2018),the following information was presented:

Star Company has one huge machine that cost $6,000,000 and was depreciated over an estimated useful life of 10 years.Upon reviewing the manufacturer's reports in 2018,management now firmly believes the machine will last a total of 15 years from date of purchase.They would like to change last year's depreciation charge based on this analysis.

Star Company has one huge machine that cost $6,000,000 and was depreciated over an estimated useful life of 10 years.Upon reviewing the manufacturer's reports in 2018,management now firmly believes the machine will last a total of 15 years from date of purchase.They would like to change last year's depreciation charge based on this analysis.

The company's building (cost $5,000,000,estimated salvage value $0 useful life 20 years)was depreciated using the 10% declining-balance method.The company and auditor now agree that the straight-line method would be a more appropriate method to use.

Star Company does not accrue for warranties; rather it records the warranty expense when amounts are paid.Star provides a one-year warranty for defective goods.Payments to satisfy warranty claims in 2017 were $100,000,and $270,000 in 2018.Out of the $270,000 paid in 2018,$150,000 related to 2017 sales.A reasonable estimate of warranties payable at the end of 2018 is $275,000.

Required:

a.As the auditor on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,changes in estimate? Explain your conclusion.

b.Assume that management of Star Company agrees with your recommendations.How would the balances above be presented in the corrected income statements for 2012 and 2013?

Star Company has one huge machine that cost $6,000,000 and was depreciated over an estimated useful life of 10 years.Upon reviewing the manufacturer's reports in 2018,management now firmly believes the machine will last a total of 15 years from date of purchase.They would like to change last year's depreciation charge based on this analysis.The company's building (cost $5,000,000,estimated salvage value $0 useful life 20 years)was depreciated using the 10% declining-balance method.The company and auditor now agree that the straight-line method would be a more appropriate method to use.

Star Company does not accrue for warranties; rather it records the warranty expense when amounts are paid.Star provides a one-year warranty for defective goods.Payments to satisfy warranty claims in 2017 were $100,000,and $270,000 in 2018.Out of the $270,000 paid in 2018,$150,000 related to 2017 sales.A reasonable estimate of warranties payable at the end of 2018 is $275,000.

Required:

a.As the auditor on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,changes in estimate? Explain your conclusion.

b.Assume that management of Star Company agrees with your recommendations.How would the balances above be presented in the corrected income statements for 2012 and 2013?

Question

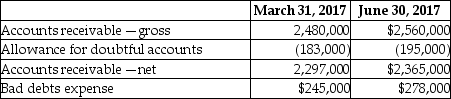

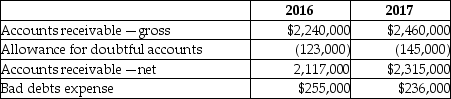

Anfield Corp.is analyzing its accounts receivable for purposes of preparing its second- quarter financial report for June 30,2017.For interim reporting,the company uses the percentage-of-sales method to estimate bad debts.During this analysis,Anfield identified an account for $42,000 that should have been written off in the first quarter ended March 31,2017 but was actually written off in May 2017.

The following table provides information relating to Anfield accounts receivables after recording the provision for bad debts for the quarter but prior to the discovery of the $42,000 error:

Required:

Required:

Record any adjusting journal entries necessary to correct the error in Anfield's accounts receivable.

The following table provides information relating to Anfield accounts receivables after recording the provision for bad debts for the quarter but prior to the discovery of the $42,000 error:

Required:Record any adjusting journal entries necessary to correct the error in Anfield's accounts receivable.

Question

Question

Question

Question

Star Company Ltd.,is a private company that started on January 1,2017.During an external audit that was conducted at the end of the second year of the company's operation (2018),the following information was presented:

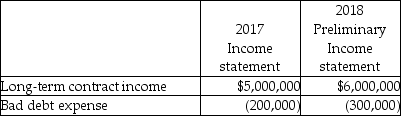

The company used the completed contract method for revenue recognition in 2017.Management now believes that the percentage of completion method would be better.If the percentage of completion method had been used,the incomes for 2017 and 2018 would have been $5,500,000 and $5,700,000 respectively.

The company used the completed contract method for revenue recognition in 2017.Management now believes that the percentage of completion method would be better.If the percentage of completion method had been used,the incomes for 2017 and 2018 would have been $5,500,000 and $5,700,000 respectively.

The accounts receivable on December 31,2017 included a $50,000 account that was not provided for but subsequently was written off during 2018 as the customer went bankrupt after the issuance of the financial statements.Star Company would like to adjust 2017 for this oversight as it sees this as an error.

Required:

a.As the auditor on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,changes in estimate? Explain your conclusion.

b.Assume that management of Star Company agrees with your recommendations.How would the balances above be presented in the corrected income statements for 2017 and 2018?

The company used the completed contract method for revenue recognition in 2017.Management now believes that the percentage of completion method would be better.If the percentage of completion method had been used,the incomes for 2017 and 2018 would have been $5,500,000 and $5,700,000 respectively.The accounts receivable on December 31,2017 included a $50,000 account that was not provided for but subsequently was written off during 2018 as the customer went bankrupt after the issuance of the financial statements.Star Company would like to adjust 2017 for this oversight as it sees this as an error.

Required:

a.As the auditor on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,changes in estimate? Explain your conclusion.

b.Assume that management of Star Company agrees with your recommendations.How would the balances above be presented in the corrected income statements for 2017 and 2018?

Question

Question

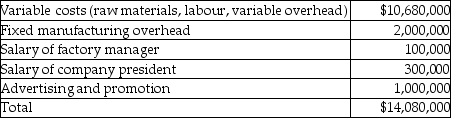

Sampson Jet Skis manufactures state-of-the-art jet skis.In 2015,the company's accountant recorded the following costs into the inventory account:

The company had no work in process at the end of both 2014 and 2015.Finished goods at the end of 2014 amounted to 8,000 jet skis at $900/jet ski.Production was 13,453 jet skis and 4,000 jet skis remained in inventory at December 31,2015.The company uses a periodic inventory system and the FIFO cost flow assumption.

The company had no work in process at the end of both 2014 and 2015.Finished goods at the end of 2014 amounted to 8,000 jet skis at $900/jet ski.Production was 13,453 jet skis and 4,000 jet skis remained in inventory at December 31,2015.The company uses a periodic inventory system and the FIFO cost flow assumption.

Required:

a.Of the $14,080,000,how much should have been capitalized into inventories?

b.Compute the ending value of inventory and the cost of goods sold for 2015.

c.If the error in inventory costing had not been corrected as per part (a),by how much would inventory be overstated at the end of 2015?

d.Record the journal entry to correct the error in inventory costing.

e.If the company uses the weighted-average cost method,how much would be the ending value of inventory and cost of goods sold for 2015?

The company had no work in process at the end of both 2014 and 2015.Finished goods at the end of 2014 amounted to 8,000 jet skis at $900/jet ski.Production was 13,453 jet skis and 4,000 jet skis remained in inventory at December 31,2015.The company uses a periodic inventory system and the FIFO cost flow assumption.Required:

a.Of the $14,080,000,how much should have been capitalized into inventories?

b.Compute the ending value of inventory and the cost of goods sold for 2015.

c.If the error in inventory costing had not been corrected as per part (a),by how much would inventory be overstated at the end of 2015?

d.Record the journal entry to correct the error in inventory costing.

e.If the company uses the weighted-average cost method,how much would be the ending value of inventory and cost of goods sold for 2015?

Question

Question

Zyler Company is analyzing its accounts receivable for purposes of preparing its financial report for the year-ended December 31,2017.The company uses the aging method to estimate bad debts.During this analysis,Zyler discovered that staff had written off a $55,000 account in 2017 even though the company had received information about the bankruptcy of the client in late 2016.

The company has already recorded bad debts expense for 2017,but the general ledger for the year has not yet been closed.The following table provides information relating to Zyler's accounts receivables just prior to the discovery of the $55,000 error:

Required:

Required:

Record any adjusting journal entries necessary to correct the error in Zyler's accounts receivable.

The company has already recorded bad debts expense for 2017,but the general ledger for the year has not yet been closed.The following table provides information relating to Zyler's accounts receivables just prior to the discovery of the $55,000 error:

Required:Record any adjusting journal entries necessary to correct the error in Zyler's accounts receivable.

Question

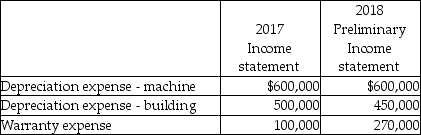

Stretton Company Limited,a private company,was started on January 1,2018.For the first year,the chief accountant prepared the financial statements and a local accountant completed the necessary review of these statements.However,for the year ended December 31,2019,an external auditor was appointed.The income statement for 2018 and the preliminary amounts for 2019 are as follows:

In the process of examining the accounting records the auditor noted the following issues:

In the process of examining the accounting records the auditor noted the following issues:

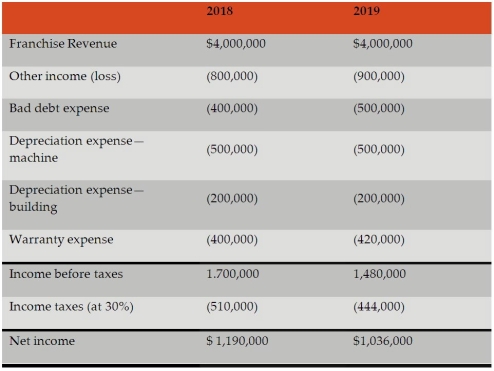

Franchise Revenue: The Stretton Company signed a franchise agreement to allow a franchisee to operate in a specific area for 10 years.The agreement required the franchisee to pay $4,000,000 initially with a royalty of 2% of sales revenue thereafter.In 2018,the 2% of sales revenue was recorded correctly by Stretton Company.However,management recorded the entire $4,000,000 as having been earned in 2018.In 2019,management realized that 40% of the $4,000,000 pertained to ongoing services to be provided over the next ten years.

Accounts receivable: The Stretton Company uses the aging method to estimate bad debts.During 2019,it was discovered that staff had written off a $103,000 account in 2019,even though the company had received information about the bankruptcy of the client in late 2018.

Machine impairment: Stretton Company has one machine that cost $5,000,000 with a useful life of 10 years and has been depreciated on a straight-line basis for 4 years,including 2019.Stretton carries this asset under the revaluation model and its auditors find that the machine should have been written down for impairments by $450,000 in 2018.No impairment has been recorded by Stretton in 2018 or 2019.

Building depreciation: The company's building (cost $4,000,000,estimated salvage value $0,useful life 20 years)was depreciated last year using the straight line method.The company and the auditor now agree that 10% declining-balance method would be a more appropriate method to use.A depreciation provision of $200,000 has been made for 2018.

Inventories: The accountant failed to apply the lower of cost and net realizable value test to ending inventory in 2018.Upon review,the inventory balance for 2019 should have been reduced by $200,000.The closing inventory allowance balance for 2019 should be $400,000.No entry has been made for this matter.

Warranties: Stretton Company does not accrue for warranties; rather,it records the warranty expense when amounts are paid.Stretton provides a one-year warranty for defective goods.Payments to satisfy warranty claims in 2018 were $400,000,and $420,000 in 2019.Out of the $420,000 paid in 2019,$250,000 related to 2018 sales.A reasonable estimate of warranties payable at the end of 2019 is $375,000.There is nothing relating to 2018 warranty claims left owing at the end of 2019.

Required:

a.As the audit senior on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,or changes in estimate? Explain your conclusion.

b.Assume that management of Stretton Company agrees with your recommendations.Prepare the corrected statements of comprehensive income for 2018 and 2019.

In the process of examining the accounting records the auditor noted the following issues:Franchise Revenue: The Stretton Company signed a franchise agreement to allow a franchisee to operate in a specific area for 10 years.The agreement required the franchisee to pay $4,000,000 initially with a royalty of 2% of sales revenue thereafter.In 2018,the 2% of sales revenue was recorded correctly by Stretton Company.However,management recorded the entire $4,000,000 as having been earned in 2018.In 2019,management realized that 40% of the $4,000,000 pertained to ongoing services to be provided over the next ten years.

Accounts receivable: The Stretton Company uses the aging method to estimate bad debts.During 2019,it was discovered that staff had written off a $103,000 account in 2019,even though the company had received information about the bankruptcy of the client in late 2018.

Machine impairment: Stretton Company has one machine that cost $5,000,000 with a useful life of 10 years and has been depreciated on a straight-line basis for 4 years,including 2019.Stretton carries this asset under the revaluation model and its auditors find that the machine should have been written down for impairments by $450,000 in 2018.No impairment has been recorded by Stretton in 2018 or 2019.

Building depreciation: The company's building (cost $4,000,000,estimated salvage value $0,useful life 20 years)was depreciated last year using the straight line method.The company and the auditor now agree that 10% declining-balance method would be a more appropriate method to use.A depreciation provision of $200,000 has been made for 2018.

Inventories: The accountant failed to apply the lower of cost and net realizable value test to ending inventory in 2018.Upon review,the inventory balance for 2019 should have been reduced by $200,000.The closing inventory allowance balance for 2019 should be $400,000.No entry has been made for this matter.

Warranties: Stretton Company does not accrue for warranties; rather,it records the warranty expense when amounts are paid.Stretton provides a one-year warranty for defective goods.Payments to satisfy warranty claims in 2018 were $400,000,and $420,000 in 2019.Out of the $420,000 paid in 2019,$250,000 related to 2018 sales.A reasonable estimate of warranties payable at the end of 2019 is $375,000.There is nothing relating to 2018 warranty claims left owing at the end of 2019.

Required:

a.As the audit senior on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,or changes in estimate? Explain your conclusion.

b.Assume that management of Stretton Company agrees with your recommendations.Prepare the corrected statements of comprehensive income for 2018 and 2019.

Question

Question

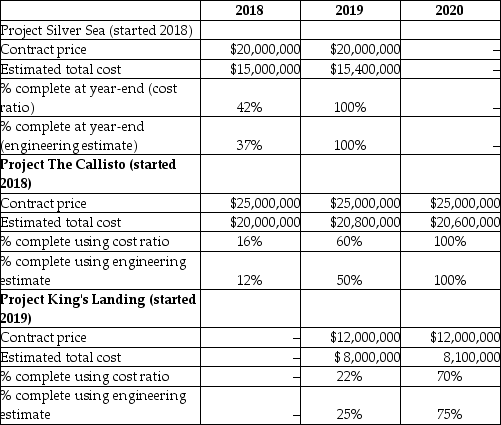

Sawatsky & Company Ltd is involved in the construction of top class luxury condos in Vancouver,Canada.Until the end of 2019,the company used the cost ratio method to estimate the percentage complete.After that point,the company switched to using estimates from architectural engineers to estimate the degree of completion.To prepare the financial report for the 2020 fiscal year,you have gathered the following data on projects that were in progress at the end of fiscal years 2018,2019,and 2020:

Required:

Required:

a.Compute the amount of revenue and cost of sales that was recognized in 2018 and 2019 using the old accounting policy.

b.Compute the amount of revenue and cost of sales that should be recognized in each year using the new accounting policy.

c.Record the adjusting journal entries to adjust revenue to reflect the change in accounting policy from using the cost ratio to using engineering estimates.The general ledger accounts for 2020 have not yet been closed.Ignore income tax effects.

Required:a.Compute the amount of revenue and cost of sales that was recognized in 2018 and 2019 using the old accounting policy.

b.Compute the amount of revenue and cost of sales that should be recognized in each year using the new accounting policy.

c.Record the adjusting journal entries to adjust revenue to reflect the change in accounting policy from using the cost ratio to using engineering estimates.The general ledger accounts for 2020 have not yet been closed.Ignore income tax effects.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/66

Play

Full screen (f)

Deck 10: Accounting Changes

1

What is the essential characteristic that distinguishes a change in accounting policy from either an error correction or a change in estimate?

The essential characteristic that distinguishes a change in accounting policy from either an error correction or a change in estimates is that a change in accounting policy involves a management choice among acceptable alternatives.An error is an unintentional misstatement an a change in estimate should reflect new information that has come to light.

2

Complete the following table by giving one example of a change in accounting policy for each financial statement item.

3

For the following types of accounting changes,identify the relevant criteria for each accounting change by selecting "yes," "no," or "n/a" (not applicable).

4

Which of the following statements is true?

A) A correction of an error is the result of information that was unknown at the time of the error.

B) A change is accounting policy is the result of new information.

C) A change in estimate is not due to management choice and not due to information known in a prior period.

D) A correction of an error is due to management choice.

A) A correction of an error is the result of information that was unknown at the time of the error.

B) A change is accounting policy is the result of new information.

C) A change in estimate is not due to management choice and not due to information known in a prior period.

D) A correction of an error is due to management choice.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

5

The discussion in IAS 16 paragraphs 60-62 indicates that a change in depreciation method is usually a change in accounting estimate.Explain the logic behind why a change in depreciation method is normally considered a change in estimate.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statements is true?

A) The last-in, first-out (LIFO) cost flow assumption is an acceptable method for costing inventories in Canada.

B) Over time, the number of areas where management has a free choice over accounting policies has increased.

C) A change in accounting policy is an accounting change made at the discretion of management.

D) Changes in accounting policy occur more frequently than changes in estimates.

A) The last-in, first-out (LIFO) cost flow assumption is an acceptable method for costing inventories in Canada.

B) Over time, the number of areas where management has a free choice over accounting policies has increased.

C) A change in accounting policy is an accounting change made at the discretion of management.

D) Changes in accounting policy occur more frequently than changes in estimates.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is an accounting error?

A) A company changes from the gross method to the net method of recording cash discounts.

B) A private corporation previously using ASPE chooses to adopt IFRS.

C) Costs not related to the construction of a building were included in the building cost.

D) A patent was expected to provide protection of intellectual property for the full legal life of 20 years, but technological advances made the patent obsolete after only 12 years.

A) A company changes from the gross method to the net method of recording cash discounts.

B) A private corporation previously using ASPE chooses to adopt IFRS.

C) Costs not related to the construction of a building were included in the building cost.

D) A patent was expected to provide protection of intellectual property for the full legal life of 20 years, but technological advances made the patent obsolete after only 12 years.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is an accounting error?

A) Inventory was sold below carrying amount even though the inventory had been previously written down to the lower of cost and net realizable value.

B) Convertible securities that were identified as dilutive for computing diluted EPS were not converted by the expiration date.

C) A change in economic conditions resulted in the fair value of goodwill declining from $15 million to $10 million.

D) Development costs of an intangible asset were capitalized when only five of six criteria for capitalization had been satisfied.

A) Inventory was sold below carrying amount even though the inventory had been previously written down to the lower of cost and net realizable value.

B) Convertible securities that were identified as dilutive for computing diluted EPS were not converted by the expiration date.

C) A change in economic conditions resulted in the fair value of goodwill declining from $15 million to $10 million.

D) Development costs of an intangible asset were capitalized when only five of six criteria for capitalization had been satisfied.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

9

Which statement is correct about a correction of an error from prior periods?

A) The correct information was available at the time the error was made.

B) The correct information was not available at the time the error was made.

C) One should use hindsight to judge whether there is an accounting error that requires correction.

D) An example of a correction of an error is the difference between the allowance for doubtful accounts and the actual outcome of bad debts.

A) The correct information was available at the time the error was made.

B) The correct information was not available at the time the error was made.

C) One should use hindsight to judge whether there is an accounting error that requires correction.

D) An example of a correction of an error is the difference between the allowance for doubtful accounts and the actual outcome of bad debts.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

10

A company changes the depreciation for a piece of equipment from 20% declining- balance to units-of-production.Describe a plausible circumstance that would support this change as one of the following: (i)an error,(ii)a change in estimate,or (iii)a change in accounting policy.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is a change in an estimate?

A) A company changes the presentation of operating expenses from "by function" to "by nature."

B) An enterprise switches from the gross method to the net method of presenting government grants.

C) A temporary difference was treated as a permanent difference.

D) The useful life on a building was originally estimated to be 20 years but the estimated useful life of the building is changed to only 15 years as at the beginning of the year.

A) A company changes the presentation of operating expenses from "by function" to "by nature."

B) An enterprise switches from the gross method to the net method of presenting government grants.

C) A temporary difference was treated as a permanent difference.

D) The useful life on a building was originally estimated to be 20 years but the estimated useful life of the building is changed to only 15 years as at the beginning of the year.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

12

For a company using the straight-line method of depreciation that changes the estimated useful life from 20 years to 15 years remaining as at the beginning of the year,the accountant should do the following:

A) Compute current year depreciation as (carrying amount - residual value) divided by 15 years.

B) Adjust prior year's depreciation.

C) Adjust the amount of accumulated depreciation as at the beginning of the year.

D) Compute current year depreciation as (carrying amount) X 15/20.

A) Compute current year depreciation as (carrying amount - residual value) divided by 15 years.

B) Adjust prior year's depreciation.

C) Adjust the amount of accumulated depreciation as at the beginning of the year.

D) Compute current year depreciation as (carrying amount) X 15/20.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

13

Complete the following table indicating which of the following requires a correction due to an error from a prior period?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is a change in policy?

A) A company changes from the gross method to the net method of recording cash discounts.

B) A change in the terms of a loan from repayment on demand to a fixed repayment date two years after the fiscal year-end.

C) A contingency for a lawsuit that was evaluated to be likely to lead to an outflow of resources was ultimately resolved against the reporting entity.

D) A temporary tax difference was treated as permanent tax difference.

A) A company changes from the gross method to the net method of recording cash discounts.

B) A change in the terms of a loan from repayment on demand to a fixed repayment date two years after the fiscal year-end.

C) A contingency for a lawsuit that was evaluated to be likely to lead to an outflow of resources was ultimately resolved against the reporting entity.

D) A temporary tax difference was treated as permanent tax difference.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

15

What is the essential characteristic that distinguishes an error correction from a change in estimate?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

16

Over time,has management's free will over accounting changes increased or decreased? Explain why.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

17

Complete the table giving an example of a change in estimate from each of the given areas.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

18

For a company using the straight-line method of depreciation that changes the estimated useful life from 20 years to 15 years as at the beginning of the year,the accountant should do (or not do)the following:

A) Compute current year depreciation as (carrying amount - residual value) divided by 20 years.

B) Do not adjust prior year's depreciation.

C) Adjust the amount of accumulated depreciation as at the beginning of the year.

D) Compute current year depreciation as (carrying amount) × 15/20.

A) Compute current year depreciation as (carrying amount - residual value) divided by 20 years.

B) Do not adjust prior year's depreciation.

C) Adjust the amount of accumulated depreciation as at the beginning of the year.

D) Compute current year depreciation as (carrying amount) × 15/20.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is a change in policy?

A) Inventory was sold below carrying amount even though the inventory had been previously written down to lower of cost and net realizable value.

B) A company changes from the cost model to the revaluation model of measuring the value of land.

C) Development costs were capitalized when only five of six criteria for capitalization had been satisfied.

D) The company miscalculated the weighted average number of ordinary shares outstanding because it used the wrong date for a share issuance.

A) Inventory was sold below carrying amount even though the inventory had been previously written down to lower of cost and net realizable value.

B) A company changes from the cost model to the revaluation model of measuring the value of land.

C) Development costs were capitalized when only five of six criteria for capitalization had been satisfied.

D) The company miscalculated the weighted average number of ordinary shares outstanding because it used the wrong date for a share issuance.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

20

For the following financial statement accounts,provide a description of a change in accounting estimates.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

21

What are two reasons why an accounting change may be permitted to give modified retrospective or prospective treatment?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

22

Why are retrospective adjustments to past years' income and expenses recorded directly in retained earnings?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

23

For a construction contract where the company uses the percentage of completion method and there is a change in the estimated total cost of the contract from 12 million to 13 million,the accountant should do the following:

A) Use the average cost of 12.5 million.

B) Compute the percentage completed using the new cost total if the company uses the cost ratio to estimate percentage completed.

C) Use estimated costs determined at the beginning of the contract, not actual costs to date.

D) Use retrospective treatment.

A) Use the average cost of 12.5 million.

B) Compute the percentage completed using the new cost total if the company uses the cost ratio to estimate percentage completed.

C) Use estimated costs determined at the beginning of the contract, not actual costs to date.

D) Use retrospective treatment.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

24

Why is the retrospective approach conceptually appropriate for changes in accounting policy?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

25

Give an example of a change in accounting policy which does not require retrospective treatment and explain why.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

26

During the audit of Keats Island Brewery for the fiscal year-ended June 30,2018,the auditors identified the following issues:

For each of the three issues described below,using the following table,identify both the direction (increase or decrease)and the amount of the effect relative to the amount without the accounting change.

a.The company sells beer for $1 each plus $0.10 deposit on each bottle.The deposit collected is payable to the provincial recycling agency.During 2017,the company had recorded $12,000 of deposits as revenue.The auditors believe this amount should have been recorded as a liability.

b.The company had been using the first-in,first-out cost flow assumption for its inventories.In fiscal 2018,management decided to switch to the weighted-average method.This change reduced inventory by $25,000 at June 30,2017,and $40,000 at June 30,2018.

c.The company has equipment costing $6,000,000 that it has been depreciating over 10 years on a straight-line basis.The depreciation for fiscal 2017 was $600,000 and accumulated depreciation on

June 30,2017,was $1,200,000.During 2018,management revises the estimate of useful life to 12 years,reducing the amount of depreciation to $480,000 per year.

For each of the three issues described below,using the following table,identify both the direction (increase or decrease)and the amount of the effect relative to the amount without the accounting change.

a.The company sells beer for $1 each plus $0.10 deposit on each bottle.The deposit collected is payable to the provincial recycling agency.During 2017,the company had recorded $12,000 of deposits as revenue.The auditors believe this amount should have been recorded as a liability.

b.The company had been using the first-in,first-out cost flow assumption for its inventories.In fiscal 2018,management decided to switch to the weighted-average method.This change reduced inventory by $25,000 at June 30,2017,and $40,000 at June 30,2018.

c.The company has equipment costing $6,000,000 that it has been depreciating over 10 years on a straight-line basis.The depreciation for fiscal 2017 was $600,000 and accumulated depreciation on

June 30,2017,was $1,200,000.During 2018,management revises the estimate of useful life to 12 years,reducing the amount of depreciation to $480,000 per year.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

27

For a company using the straight-line method of depreciation that changes the estimated useful life from 20 years to 15 years as at the beginning of the year,the accountant should do (or not do)the following:

A) Compute current year depreciation as (carrying amount - residual value) divided by 20 years.

B) Adjust prior year's depreciation.

C) Do not adjust the amount of accumulated depreciation as at the beginning of the year.

D) Compute current year depreciation as (carrying amount) × 15/20.

A) Compute current year depreciation as (carrying amount - residual value) divided by 20 years.

B) Adjust prior year's depreciation.

C) Do not adjust the amount of accumulated depreciation as at the beginning of the year.

D) Compute current year depreciation as (carrying amount) × 15/20.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

28

A retailer increases bad debts expense from 2.5% to 3% of credit sales.Given this information,which of the following statements is correct?

A) The net income of prior years is overstated and a retrospective correction should be made.

B) This is a change in estimate and should be treated prospectively.

C) This is a change in accounting policy and treatment is retrospective.

D) This is a correction of an error and a retrospective correction should be made.

A) The net income of prior years is overstated and a retrospective correction should be made.

B) This is a change in estimate and should be treated prospectively.

C) This is a change in accounting policy and treatment is retrospective.

D) This is a correction of an error and a retrospective correction should be made.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

29

Define "a retrospective adjustment."

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

30

Evaluate each of the following independent situations to determine the type of accounting change (correction of error,change in accounting policy,or change in estimate)and the appropriate accounting treatment (retrospective or prospective).

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

31

How should enterprises reflect changes in accounting standards?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

32

Why is the prospective treatment conceptually appropriate for changes in estimates?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

33

Define the term "prospective adjustment." Which type of accounting changes is it applied to?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

34

An analysis of a company's inventory indicates that inventory at the end of 2016 was understated by $30,000 due to an inventory count error.Inventory at the end of 2017 was correctly stated.The company uses the periodic system of inventory and its fiscal year-end is December 31.Given this information,which of the following statements is correct?

A) The net income of 2016 is overstated and a retrospective correction should be made.

B) The net income of 2017 is overstated and should be corrected.

C) The 2017 year-end retained earnings are overstated and a prospective correction should be made.

D) The net income of 2017 is understated and should be corrected.

A) The net income of 2016 is overstated and a retrospective correction should be made.

B) The net income of 2017 is overstated and should be corrected.

C) The 2017 year-end retained earnings are overstated and a prospective correction should be made.

D) The net income of 2017 is understated and should be corrected.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

35

For each of the following scenarios,determine the effects (if any)of the accounting change (correction of error,change in accounting policy,or change in estimate)on the relevant asset or liability,equity,and comprehensive income in the year of change and the prior year.Use the following table for your response:

a.Company A increases the allowance for doubtful accounts (ADA).Using the old estimate,ADA would have been $45,000.The new estimate is $50,000.

b.Company B omitted to record an invoice for a $10,000 sale made on credit at the end of the previous year and incorrectly recorded the sale in the current year.The related inventory sold has been accounted for.

c.Company C changes its revenue recognition to a more conservative policy.The result is a decrease in prior-year revenue by $4,000 and a decrease in current-year revenue by $5,000 relative to the amounts under the old policy.

a.Company A increases the allowance for doubtful accounts (ADA).Using the old estimate,ADA would have been $45,000.The new estimate is $50,000.b.Company B omitted to record an invoice for a $10,000 sale made on credit at the end of the previous year and incorrectly recorded the sale in the current year.The related inventory sold has been accounted for.

c.Company C changes its revenue recognition to a more conservative policy.The result is a decrease in prior-year revenue by $4,000 and a decrease in current-year revenue by $5,000 relative to the amounts under the old policy.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

36

Which statement is true regarding accounting accruals?

A) Errors or changes in accounting policy that affect non-current items like equipment will result in follow-through changes over a relatively short period.

B) The purchase of equipment involves an initial accrual to record the asset followed by accrual reversals in the form of depreciation expense and derecognition of the asset upon disposal.

C) Operating activities generally have relatively long cash cycles.

D) Financing and investing activities generally have relatively short cash cycles.

A) Errors or changes in accounting policy that affect non-current items like equipment will result in follow-through changes over a relatively short period.

B) The purchase of equipment involves an initial accrual to record the asset followed by accrual reversals in the form of depreciation expense and derecognition of the asset upon disposal.

C) Operating activities generally have relatively long cash cycles.

D) Financing and investing activities generally have relatively short cash cycles.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

37

For the following accounting changes,identify the appropriate treatment under IFRS.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

38

How many balance sheets are required by IAS 1 when there is a change in accounting policy and why?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

39

Which statement is true regarding accounting accruals?

A) The nature of accrual accounting is that accruals will reverse when cash cycles are complete.

B) Operating activities generally have relatively long cash cycles.

C) Financing and investing activities generally have relatively short cash cycles.

D) Errors or changes in accounting policy that affect non-current items like equipment will result in follow-through changes over a relatively short period.

A) The nature of accrual accounting is that accruals will reverse when cash cycles are complete.

B) Operating activities generally have relatively long cash cycles.

C) Financing and investing activities generally have relatively short cash cycles.

D) Errors or changes in accounting policy that affect non-current items like equipment will result in follow-through changes over a relatively short period.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

40

What types of accounting changes are treated retrospectively and why?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

41

Chisholm Appliances is a relatively new producer of commercial grade appliances.To enhance the competitiveness of its products,on July 1,2018,the company introduced a warranty against defects for 12 months from the date of installation.

No warranty claims were received in 2018.However,in February 2020,when the auditors examined the records for the year ended December 31,2019,they noted $255,000 of warranty claims relating to 2019 recorded as miscellaneous expense.The auditors requested the company to accrue for the expected warranty costs retrospectively to 2018.

The auditors agreed with Chisholm's management that the estimated warranty fulfillment costs should be 0.5% of revenue.The company recorded revenue of $55,598,000 in 2018 and $56,213,000 in 2019.The company's tax rate is 30%.The general ledger for 2019 has not yet been closed.

Required:

Record any adjusting journal entries required to correct Chisholm's books.Include the effect of income taxes.

No warranty claims were received in 2018.However,in February 2020,when the auditors examined the records for the year ended December 31,2019,they noted $255,000 of warranty claims relating to 2019 recorded as miscellaneous expense.The auditors requested the company to accrue for the expected warranty costs retrospectively to 2018.

The auditors agreed with Chisholm's management that the estimated warranty fulfillment costs should be 0.5% of revenue.The company recorded revenue of $55,598,000 in 2018 and $56,213,000 in 2019.The company's tax rate is 30%.The general ledger for 2019 has not yet been closed.

Required:

Record any adjusting journal entries required to correct Chisholm's books.Include the effect of income taxes.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

42

Arbutus Inc.issued a 10-year bond on July 1,2016.The $30,000,000 par bond pays $900,000 of interest on December 31 and June 30.The company has a calendar year-end.

It is now February 2020.During the audit of the 2019 financial statements,it was discovered that the bond indenture allowed holders to convert the bonds to common shares.The terms of the conversion allow each $1,000 bond to be converted into 50 shares.Additional investigation concluded that the bond would have yielded 8%/a,had it not included the conversion option.

Required:

Record any adjusting journal entries required to correct Arbutus's accounts.The books for 2019 have not yet been closed.

It is now February 2020.During the audit of the 2019 financial statements,it was discovered that the bond indenture allowed holders to convert the bonds to common shares.The terms of the conversion allow each $1,000 bond to be converted into 50 shares.Additional investigation concluded that the bond would have yielded 8%/a,had it not included the conversion option.

Required:

Record any adjusting journal entries required to correct Arbutus's accounts.The books for 2019 have not yet been closed.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

43

Pracene Sports Supply is a relatively new producer of sporting goods.To enhance the competitiveness of its products,on July 1,2018,the company introduced a warranty against defects for 12 months from the date of sale.

The company's products are of a sufficiently high quality such that no warranty claims were received in 2018.However,in February 2020,when the auditors examined the records for the year ended December 31,2019,they noted a small number of warranty claims in 2019 amounting to $243,000,which was recorded as miscellaneous expense.These claims alerted the auditors to the fact that the company should have but did not accrue for the expected warranty costs starting in 2018.

Pracene's management estimates warranty fulfillment costs to be 0.10% of revenue.The company recorded revenue of $51,500,000 in 2018 and $55,300,000 in 2019.There is very little seasonality in the sales pattern through the year.The company's tax rate is 40%.The general ledger for 2019 has not yet been closed.

Required:

Record any adjusting journal entries required to correct Pracene's books.Include the effect of income taxes.

The company's products are of a sufficiently high quality such that no warranty claims were received in 2018.However,in February 2020,when the auditors examined the records for the year ended December 31,2019,they noted a small number of warranty claims in 2019 amounting to $243,000,which was recorded as miscellaneous expense.These claims alerted the auditors to the fact that the company should have but did not accrue for the expected warranty costs starting in 2018.

Pracene's management estimates warranty fulfillment costs to be 0.10% of revenue.The company recorded revenue of $51,500,000 in 2018 and $55,300,000 in 2019.There is very little seasonality in the sales pattern through the year.The company's tax rate is 40%.The general ledger for 2019 has not yet been closed.

Required:

Record any adjusting journal entries required to correct Pracene's books.Include the effect of income taxes.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

44

For each of the following independent scenarios,indicate the effect of the error (if any)on:

i.2017 net income

ii.2018 net income

iii.2018 closing retained earnings

The company uses the periodic system of inventory and its fiscal year-end is

December 31.Ignore income tax effects.

a)Invoices in the amount of $42,000 for inventory received in December 2017 were not entered on the books in 2017.They were recorded as purchases in January 2018 when they were paid.The goods were counted in the 2017 inventory count and included in ending inventory on the 2017 financial statements.

b)Goods received on consignment amounting to $73,000 were included in the physical count of goods at the end of 2018 and included in ending inventory on the 2018 financial statements.

c)Your analysis of inventory indicates that inventory at the end of 2017 was overstated by $152,000 due to an inventory count error.Inventory at the end of 2018 was correctly stated.

d)Provide the journal entry in 2018 to correct the error for (a)to (c).

i.2017 net income

ii.2018 net income

iii.2018 closing retained earnings

The company uses the periodic system of inventory and its fiscal year-end is

December 31.Ignore income tax effects.

a)Invoices in the amount of $42,000 for inventory received in December 2017 were not entered on the books in 2017.They were recorded as purchases in January 2018 when they were paid.The goods were counted in the 2017 inventory count and included in ending inventory on the 2017 financial statements.

b)Goods received on consignment amounting to $73,000 were included in the physical count of goods at the end of 2018 and included in ending inventory on the 2018 financial statements.

c)Your analysis of inventory indicates that inventory at the end of 2017 was overstated by $152,000 due to an inventory count error.Inventory at the end of 2018 was correctly stated.

d)Provide the journal entry in 2018 to correct the error for (a)to (c).

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

45

Wasson Company purchased land and a building in 2016 at a cost of $6,000,000.The land was valued at $1,000,000.At the time of purchase,the estimated useful life of the building was 25 years.The company depreciates the building on a straight-line basis and has chosen to record a full year of depreciation in the year of acquisition,and none in the year of disposal.

It is now 2026 and Wasson has found it necessary to replace all of the windows in this building at a cost of $1,000,000.Upon further review,management concluded that the windows should have been recorded as a separate component because,as of 2016,their useful lives did not extend for 25 years-the manufacturer's specifications indicate that the windows would be expected to remain in functioning condition until 2026.The estimated value of the windows when the building was purchased was $800,000.

Required:

a.Record the journal entry to record the replacement of the windows assuming that the windows were recorded as a separate component.

b.Assume that LaSalle committed an error in not componentizing the windows separately from the building.Record the adjusting journal entry or entries required to correct this error.

c.Record the journal entry to record the replacement of the windows after having properly recorded the windows as a separate component in part (b).

It is now 2026 and Wasson has found it necessary to replace all of the windows in this building at a cost of $1,000,000.Upon further review,management concluded that the windows should have been recorded as a separate component because,as of 2016,their useful lives did not extend for 25 years-the manufacturer's specifications indicate that the windows would be expected to remain in functioning condition until 2026.The estimated value of the windows when the building was purchased was $800,000.

Required:

a.Record the journal entry to record the replacement of the windows assuming that the windows were recorded as a separate component.

b.Assume that LaSalle committed an error in not componentizing the windows separately from the building.Record the adjusting journal entry or entries required to correct this error.

c.Record the journal entry to record the replacement of the windows after having properly recorded the windows as a separate component in part (b).

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

46

Grant Pharmaceuticals Ltd.undertook a research and development project in 2017.As of May 1 of that year,management concluded that the project had met the requirements for the capitalization of development costs.For the remainder of 2017 and 2018,the company capitalized $9.9 million of development costs for the project.Had these costs been expensed,the company would have reported losses.In 2019,Grant began amortizing the development cost over the estimated useful life of 10 years,beginning with a full year of amortization in 2019.

In 2022,the auditors concluded that the development cost did not meet the criteria for capitalization.Specifically,Grant did not demonstrate that the company had sufficient financial resources to complete the development project.Grant's management agreed to correct the error in order to obtain a clean audit opinion.The company's tax rate is 30%.

Required:

Record the journal entries necessary to correct Grant's accounts.Include the effect of income taxes.

In 2022,the auditors concluded that the development cost did not meet the criteria for capitalization.Specifically,Grant did not demonstrate that the company had sufficient financial resources to complete the development project.Grant's management agreed to correct the error in order to obtain a clean audit opinion.The company's tax rate is 30%.

Required:

Record the journal entries necessary to correct Grant's accounts.Include the effect of income taxes.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

47

Cantac Construction purchased a piece of equipment for $40 million in early 2017.The company depreciates the equipment using the straight-line method over its useful life of 20 years,when it will have zero residual value.Cantac's income tax rate is 40%.At the end of 2020,after four years of depreciation,the company wrote down the carrying amount of the equipment from $32 million to $24 million after performing an impairment test on the cash generating unit (CGU)to which the equipment belonged.As a result of the impairment,the annual depreciation declined from $2 million to $1.5 million.In 2023,prior to recording depreciation for that year,the company's staff discovered an error in one of the formulas in the spreadsheet used to compute the value in use for the impairment test carried out at the end of 2020.Removing the error in the spreadsheet,the value in use for the CGU exceeded its carrying value.Therefore,the CGU was in fact not impaired,and Cantac should not have recorded an impairment writedown on the demolition equipment at the end of 2020.

Required:

Prepare the journal entries to correct the error including subsequent years' depreciation and related tax effects.

Required:

Prepare the journal entries to correct the error including subsequent years' depreciation and related tax effects.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

48

Canlan Inc.is a subsidiary of a Canadian publicly traded manufacturer of construction materials.The company uses the first-in,first-out (FIFO)cost flow assumption.

a.An invoice for $55,000 of material received and used in production arrived after the year-end.Neither the purchase nor the accounts payable was recorded until year two.However,the amount of raw materials in ending inventory was correct based on the inventory count.

b.One of Canlan's products became obsolete and worthless during Year 1,but the inventory writedown did not occur until Year 2.The cost of this inventory was $225,000.

c.In the Year 1 closing inventory count,employees improperly included 2,000 units of finished goods that had already been sold to customers.These units had a cost of $20,000 under FIFO.

Required:

For each of the above independent scenarios (a)through (c),indicate in the following table the effect of the accounting errors on the books of Canlan Inc.Specifically,identify the amount and direction of over- or understatement of inventory and income for Year 1 and Year 2.If an account requires no adjustment,indicate that the account is "correct."

a.An invoice for $55,000 of material received and used in production arrived after the year-end.Neither the purchase nor the accounts payable was recorded until year two.However,the amount of raw materials in ending inventory was correct based on the inventory count.

b.One of Canlan's products became obsolete and worthless during Year 1,but the inventory writedown did not occur until Year 2.The cost of this inventory was $225,000.

c.In the Year 1 closing inventory count,employees improperly included 2,000 units of finished goods that had already been sold to customers.These units had a cost of $20,000 under FIFO.

Required:

For each of the above independent scenarios (a)through (c),indicate in the following table the effect of the accounting errors on the books of Canlan Inc.Specifically,identify the amount and direction of over- or understatement of inventory and income for Year 1 and Year 2.If an account requires no adjustment,indicate that the account is "correct."

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

49

Albacore Sailboats manufactures small sailing dinghies.In 2019,the company's accountant recorded the following costs into the inventory account:

The company had no work in process at the end of both 2018 and 2019.Finished goods at the end of 2018 amounted to 6,000 sailboats at $300/boat.Production was 50,000 sailboats and 4,000 boats remained in inventory at December 31,2019.The company uses a periodic inventory system and the FIFO cost flow assumption.

Required:

a.Of the $15,098,000,how much should have been capitalized into inventories?

b.Compute the ending value of inventory and the cost of goods sold for 2019.

c.If the error in inventory costing had not been corrected as per part (a),by how much would inventory be overstated at the end of 2019?

d.Record the journal entry to correct the error in inventory costing.

The company had no work in process at the end of both 2018 and 2019.Finished goods at the end of 2018 amounted to 6,000 sailboats at $300/boat.Production was 50,000 sailboats and 4,000 boats remained in inventory at December 31,2019.The company uses a periodic inventory system and the FIFO cost flow assumption.Required:

a.Of the $15,098,000,how much should have been capitalized into inventories?

b.Compute the ending value of inventory and the cost of goods sold for 2019.

c.If the error in inventory costing had not been corrected as per part (a),by how much would inventory be overstated at the end of 2019?

d.Record the journal entry to correct the error in inventory costing.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

50

On December 15,2017,The Dutton Company factored $1,600,000 of accounts receivable for proceeds of $1,500,000.The company recorded the transaction as being without recourse,with $100,000 recorded to interest expense.During the preparation of the financial statements dated December 31,2018,staff concluded that the factoring arrangement should have been classified as being with recourse.Additional information about the factoring is as follows:

The factor withheld $40,000 for potential uncollectible accounts.Actual uncollectible accounts amounted to $50,000; Dutton paid the additional $10,000 to the factor on August 7,2018 and recorded this amount as "miscellaneous expense."

Required:

1.Reproduce the incorrect journal entry that was recorded on December 15,2017,and on August 7,2018.

2.Provide the correct journal entries that should have been recorded on December 15,2017,and on August 7,2018.

3.Record any correcting journal entries necessary to correct the error in Dutton's accounts.

The factor withheld $40,000 for potential uncollectible accounts.Actual uncollectible accounts amounted to $50,000; Dutton paid the additional $10,000 to the factor on August 7,2018 and recorded this amount as "miscellaneous expense."

Required:

1.Reproduce the incorrect journal entry that was recorded on December 15,2017,and on August 7,2018.

2.Provide the correct journal entries that should have been recorded on December 15,2017,and on August 7,2018.

3.Record any correcting journal entries necessary to correct the error in Dutton's accounts.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

51

Star Company Ltd.,is a private company that started on January 1,2017.During an external audit that was conducted at the end of the second year of the company's operation (2018),the following information was presented:

Star Company has one huge machine that cost $6,000,000 and was depreciated over an estimated useful life of 10 years.Upon reviewing the manufacturer's reports in 2018,management now firmly believes the machine will last a total of 15 years from date of purchase.They would like to change last year's depreciation charge based on this analysis.

The company's building (cost $5,000,000,estimated salvage value $0 useful life 20 years)was depreciated using the 10% declining-balance method.The company and auditor now agree that the straight-line method would be a more appropriate method to use.

Star Company does not accrue for warranties; rather it records the warranty expense when amounts are paid.Star provides a one-year warranty for defective goods.Payments to satisfy warranty claims in 2017 were $100,000,and $270,000 in 2018.Out of the $270,000 paid in 2018,$150,000 related to 2017 sales.A reasonable estimate of warranties payable at the end of 2018 is $275,000.

Required:

a.As the auditor on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,changes in estimate? Explain your conclusion.

b.Assume that management of Star Company agrees with your recommendations.How would the balances above be presented in the corrected income statements for 2012 and 2013?

Star Company has one huge machine that cost $6,000,000 and was depreciated over an estimated useful life of 10 years.Upon reviewing the manufacturer's reports in 2018,management now firmly believes the machine will last a total of 15 years from date of purchase.They would like to change last year's depreciation charge based on this analysis.The company's building (cost $5,000,000,estimated salvage value $0 useful life 20 years)was depreciated using the 10% declining-balance method.The company and auditor now agree that the straight-line method would be a more appropriate method to use.

Star Company does not accrue for warranties; rather it records the warranty expense when amounts are paid.Star provides a one-year warranty for defective goods.Payments to satisfy warranty claims in 2017 were $100,000,and $270,000 in 2018.Out of the $270,000 paid in 2018,$150,000 related to 2017 sales.A reasonable estimate of warranties payable at the end of 2018 is $275,000.

Required:

a.As the auditor on this engagement,what is your recommended treatment for each of these matters in terms of whether they are errors,changes in accounting policy,changes in estimate? Explain your conclusion.

b.Assume that management of Star Company agrees with your recommendations.How would the balances above be presented in the corrected income statements for 2012 and 2013?

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

52

Anfield Corp.is analyzing its accounts receivable for purposes of preparing its second- quarter financial report for June 30,2017.For interim reporting,the company uses the percentage-of-sales method to estimate bad debts.During this analysis,Anfield identified an account for $42,000 that should have been written off in the first quarter ended March 31,2017 but was actually written off in May 2017.

The following table provides information relating to Anfield accounts receivables after recording the provision for bad debts for the quarter but prior to the discovery of the $42,000 error:

Required:

Record any adjusting journal entries necessary to correct the error in Anfield's accounts receivable.

The following table provides information relating to Anfield accounts receivables after recording the provision for bad debts for the quarter but prior to the discovery of the $42,000 error:

Required:Record any adjusting journal entries necessary to correct the error in Anfield's accounts receivable.

Unlock Deck

Unlock for access to all 66 flashcards in this deck.

Unlock Deck

k this deck

53

CBC Biomedical undertook a research and development project in 2016.As of March 1 of that year,management concluded that the project had met the requirements for the capitalization of development costs.For the remainder of 2016 and 2017,the company capitalized $4.3 million of development costs for the project.Capitalizing these costs helped CBC Biomedical to remain profitable; had these costs been expensed,the company would report losses.In 2018,CBC Biomedical began amortizing the development cost over the estimated useful life of 10 years,beginning with a full year of amortization in 2018.

In 2021,in preparation for an initial public offering (IPO),the company engaged a public accounting firm to conduct an external audit of its financial statements.The auditors concluded that the development cost did not meet the criteria for capitalization.Specifically,it is their opinion that CBC Biomedical,at the time,did not demonstrate that the company had sufficient financial resources to complete the development project due to the recurring operating losses incurred.After some heated debate,CBC Biomedical management agreed with the auditors' position in order to obtain an unqualified audit opinion.The company had not yet recorded any amortization for 2021 when it agreed to correct the error.The company's tax rate is 30%.

Required:

Record the journal entries necessary to correct CBC's accounts.Include the effect of income taxes.