Deck 17: International Portfolio Theory and Diversification

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

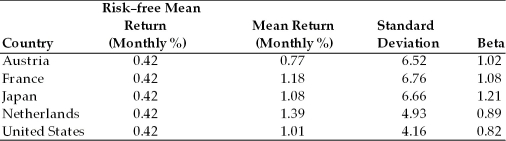

TABLE 17.1

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Treynor Measure for the Netherlands?

A)0.197

B)0.0109

C)either A or B

D)neither A nor B

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Treynor Measure for the Netherlands?

A)0.197

B)0.0109

C)either A or B

D)neither A nor B

Question

Question

Question

Question

Question

Question

TABLE 17.1

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Sharpe Measure for France?

A)0.113

B)0.0071

C)either A or B

D)neither A nor B

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Sharpe Measure for France?

A)0.113

B)0.0071

C)either A or B

D)neither A nor B

Question

Question

TABLE 17.1

Use the information to answer following question(s).

Refer to Table 17.1. ________ appears to have the greatest amount of risk as measured by monthly standard deviation, but ________ has the best return per unit of risk according to the Sharpe Measure.

A)United States; Austria

B)France; Austria

C)United States; Netherlands

D)France; Netherlands

Use the information to answer following question(s).

Refer to Table 17.1. ________ appears to have the greatest amount of risk as measured by monthly standard deviation, but ________ has the best return per unit of risk according to the Sharpe Measure.

A)United States; Austria

B)France; Austria

C)United States; Netherlands

D)France; Netherlands

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/36

Play

Full screen (f)

Deck 17: International Portfolio Theory and Diversification

1

An internationally diversified portfolio

A)should result in a portfolio with a lower beta than a purely domestic portfolio.

B)has the same overall risk shape as a purely domestic portfolio.

C)is only about 12% as risky as the typical individual stock.

D)all of the above

A)should result in a portfolio with a lower beta than a purely domestic portfolio.

B)has the same overall risk shape as a purely domestic portfolio.

C)is only about 12% as risky as the typical individual stock.

D)all of the above

all of the above

2

Beta may be defined as

A)the measure of systematic risk.

B)a risk measure of a portfolio.

C)the ratio of the variance of the portfolio to the variance of the market.

D)all of the above

A)the measure of systematic risk.

B)a risk measure of a portfolio.

C)the ratio of the variance of the portfolio to the variance of the market.

D)all of the above

all of the above

3

Increasing the number of securities in a portfolio reduces the unsystematic risk but not the systematic risk.

True

4

Portfolio diversification can eliminate 100% of risk.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

5

A U.S. investor makes an investment in Britain and earns 14% on the investment while the British pound appreciates against the U.S. dollar by 8%. What is the investor's total return?

A)22.00%

B)23.12%

C)6.00%

D)4.88%

A)22.00%

B)23.12%

C)6.00%

D)4.88%

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

6

Use the information to answer the following question(s).

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. At the end of the year the investor sells his stock that now has an average price per share of €57. What is the investor's average rate of return after converting the stock back into dollars?

A)-1.35%

B)5.0%

C)-5.0%

D)-7.24%

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. At the end of the year the investor sells his stock that now has an average price per share of €57. What is the investor's average rate of return after converting the stock back into dollars?

A)-1.35%

B)5.0%

C)-5.0%

D)-7.24%

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

7

Use the information to answer the following question(s).

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. How many euros will the U.S. investor acquire with his initial $500,000 investment?

A)€650,000

B)€370,370

C)€500,000

D)€384,615

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. How many euros will the U.S. investor acquire with his initial $500,000 investment?

A)€650,000

B)€370,370

C)€500,000

D)€384,615

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

8

________ risk is measured with beta.

A)Systematic

B)Unsystematic

C)International

D)Domestic

A)Systematic

B)Unsystematic

C)International

D)Domestic

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

9

A fully diversified domestic portfolio has a beta of ________.

A)0.0

B)1.0

C)-1.0

D)Not enough information to answer this question.

A)0.0

B)1.0

C)-1.0

D)Not enough information to answer this question.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements is NOT true?

A)International diversification benefits induce investors to demand foreign securities.

B)An international security adds value to a portfolio if it reduces risk without reducing return.

C)Investors will demand a security that adds value.

D)All of the above are true.

A)International diversification benefits induce investors to demand foreign securities.

B)An international security adds value to a portfolio if it reduces risk without reducing return.

C)Investors will demand a security that adds value.

D)All of the above are true.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

11

In some respects, internationally diversified portfolios are the same in principle as a domestic portfolio because

A)the investor is attempting to combine assets that are perfectly correlated.

B)investors are trying to reduce systematic risk.

C)investors are trying to reduce the total risk of the portfolio.

D)all of the above

A)the investor is attempting to combine assets that are perfectly correlated.

B)investors are trying to reduce systematic risk.

C)investors are trying to reduce the total risk of the portfolio.

D)all of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

12

In some respects, internationally diversified portfolios are different from a domestic portfolio because

A)investors may also acquire foreign exchange risk.

B)international portfolio diversification increases expected return but does not decrease risk.

C)investors must leave the country to acquire foreign securities.

D)all of the above

A)investors may also acquire foreign exchange risk.

B)international portfolio diversification increases expected return but does not decrease risk.

C)investors must leave the country to acquire foreign securities.

D)all of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

13

Portfolio theory assumes that investors are risk-averse. This means that investors

A)cannot be induced to make risky investments.

B)prefer more risk to less for a given return.

C)will accept some risk, but not unnecessary risk.

D)All of the above are true.

A)cannot be induced to make risky investments.

B)prefer more risk to less for a given return.

C)will accept some risk, but not unnecessary risk.

D)All of the above are true.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

14

A well-diversified portfolio has about ________ of the risk of the typical individual stock.

A)8%

B)19%

C)27%

D)52%

A)8%

B)19%

C)27%

D)52%

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

15

Unsystematic risk

A)is the remaining risk in a well-diversified portfolio.

B)is measured with beta.

C)can be diversified away.

D)all of the above

A)is the remaining risk in a well-diversified portfolio.

B)is measured with beta.

C)can be diversified away.

D)all of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

16

The addition of foreign securities to the domestic portfolio opportunity set shifts the efficient frontier

A)down and to the left.

B)up and to the right.

C)up and to the left.

D)down and to the right.

A)down and to the left.

B)up and to the right.

C)up and to the left.

D)down and to the right.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

17

Use the information to answer the following question(s).

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. At an average price of €60/share, how many shares of stock will the investor be able to purchase?

A)8333 shares

B)6410 shares

C)6173 shares

D)10,833 shares

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. At an average price of €60/share, how many shares of stock will the investor be able to purchase?

A)8333 shares

B)6410 shares

C)6173 shares

D)10,833 shares

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

18

Use the information to answer the following question(s).

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. At the end of the year the investor sells his stock that now has an average price per share of €57. What is the investor's average rate of return before converting the stock back into dollars?

A)5.0%

B)-3.0%

C)-5.0%

D)3.0%

In September 2009 a U.S. investor chooses to invest $500,000 in German equity securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is $1.35/euro.

Refer to Instruction 17.1. At the end of the year the investor sells his stock that now has an average price per share of €57. What is the investor's average rate of return before converting the stock back into dollars?

A)5.0%

B)-3.0%

C)-5.0%

D)3.0%

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

19

Relative to the efficient frontier of risky portfolios, it is impossible to hold a portfolio that is located ________ the efficient frontier.

A)to the left of

B)to the right of

C)on

D)to the right or left of

A)to the left of

B)to the right of

C)on

D)to the right or left of

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

20

The efficient frontier of the domestic portfolio opportunity set

A)runs along the extreme left edge of the opportunity set.

B)represents optimal portfolios of securities that represent minimum risk for a given level of expected portfolio return.

C)contains the portfolio of risky securities that the logical investor would choose to hold.

D)all of the above

A)runs along the extreme left edge of the opportunity set.

B)represents optimal portfolios of securities that represent minimum risk for a given level of expected portfolio return.

C)contains the portfolio of risky securities that the logical investor would choose to hold.

D)all of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

21

If an investor is able to determine a global beta for his portfolio and holds a portfolio that is well-diversified with international investments, which performance measure is more appropriate, the Sharpe Measure or the Treynor Measure? Why? Explain each performance measure.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

22

The Sharpe and Treynor measures are each measures of return per unit of risk.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

23

The graph for the efficient frontier has beta on the vertical axis and standard deviation of the horizontal axis.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

24

Use the information to answer the following question(s).

A U.S. investor is considering a portfolio consisting of 60% invested in the U.S. equity index fund and 40% invested in the British equity index fund. The expected returns for the funds are 10% for the U.S. and 8% for the British, standard deviations of 20% for the U.S. and 18% for the British, and a correlation coefficient of 0.15 between the U.S. and British equity funds.

Refer to Instruction 17.2. What is the expected return of the proposed portfolio?

A)9.2%

B)9.0%

C)19.2%

D)19%

A U.S. investor is considering a portfolio consisting of 60% invested in the U.S. equity index fund and 40% invested in the British equity index fund. The expected returns for the funds are 10% for the U.S. and 8% for the British, standard deviations of 20% for the U.S. and 18% for the British, and a correlation coefficient of 0.15 between the U.S. and British equity funds.

Refer to Instruction 17.2. What is the expected return of the proposed portfolio?

A)9.2%

B)9.0%

C)19.2%

D)19%

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

25

The standard deviation of a portfolio is the weighted average standard deviations of the individual assets.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

26

The portfolio with the least risk among all those possible in the domestic portfolio opportunity set is called the minimum risk domestic portfolio.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

27

TABLE 17.1

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Treynor Measure for the Netherlands?

A)0.197

B)0.0109

C)either A or B

D)neither A nor B

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Treynor Measure for the Netherlands?

A)0.197

B)0.0109

C)either A or B

D)neither A nor B

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

28

Draw the curve representing the Optimal Domestic Efficient Frontier. Be sure to draw and label the following: The vertical axis and the horizontal axis, the risk-free security, the minimum risk portfolio, the domestic portfolio opportunity set, the optimal domestic portfolio, and the capital market line. Choose a point along the domestic portfolio opportunity set between the optimal domestic portfolio and the minimum risk domestic portfolio and explain why that point is not the optimal risky domestic portfolio for investors to hold.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

29

Capital markets around the world are on average less integrated today than they were 20 years ago.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

30

The Sharpe and Treynor Measures tend to be consistent in their ranking of portfolios when the portfolios

A)are poorly diversified.

B)are properly diversified.

C)contain only U.S. equity investments.

D)none of the above

A)are poorly diversified.

B)are properly diversified.

C)contain only U.S. equity investments.

D)none of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

31

The optimal domestic portfolio of risky securities is the portfolio of minimum risk.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

32

The ________ connects the risk-free security with the optimal domestic portfolio.

A)security market line

B)capital asset pricing model

C)capital market line

D)none of the above

A)security market line

B)capital asset pricing model

C)capital market line

D)none of the above

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

33

TABLE 17.1

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Sharpe Measure for France?

A)0.113

B)0.0071

C)either A or B

D)neither A nor B

Use the information to answer following question(s).

Refer to Table 17.1. What is the value of the Sharpe Measure for France?

A)0.113

B)0.0071

C)either A or B

D)neither A nor B

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

34

The Sharpe measure uses ________ as the measure of risk and the Treynor measure uses ________ as the measure of risk.

A)standard deviation; variance

B)beta; variance

C)standard deviation; beta

D)beta; standard deviation

A)standard deviation; variance

B)beta; variance

C)standard deviation; beta

D)beta; standard deviation

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

35

TABLE 17.1

Use the information to answer following question(s).

Refer to Table 17.1. ________ appears to have the greatest amount of risk as measured by monthly standard deviation, but ________ has the best return per unit of risk according to the Sharpe Measure.

A)United States; Austria

B)France; Austria

C)United States; Netherlands

D)France; Netherlands

Use the information to answer following question(s).

Refer to Table 17.1. ________ appears to have the greatest amount of risk as measured by monthly standard deviation, but ________ has the best return per unit of risk according to the Sharpe Measure.

A)United States; Austria

B)France; Austria

C)United States; Netherlands

D)France; Netherlands

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

36

Use the information to answer the following question(s).

A U.S. investor is considering a portfolio consisting of 60% invested in the U.S. equity index fund and 40% invested in the British equity index fund. The expected returns for the funds are 10% for the U.S. and 8% for the British, standard deviations of 20% for the U.S. and 18% for the British, and a correlation coefficient of 0.15 between the U.S. and British equity funds.

Refer to Instruction 17.2. What is the standard deviation of the proposed portfolio?

A)38.00

B)19.20

C)19.00

D)14.45

A U.S. investor is considering a portfolio consisting of 60% invested in the U.S. equity index fund and 40% invested in the British equity index fund. The expected returns for the funds are 10% for the U.S. and 8% for the British, standard deviations of 20% for the U.S. and 18% for the British, and a correlation coefficient of 0.15 between the U.S. and British equity funds.

Refer to Instruction 17.2. What is the standard deviation of the proposed portfolio?

A)38.00

B)19.20

C)19.00

D)14.45

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 36 flashcards in this deck.