Deck 3: Accrual Accounting

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

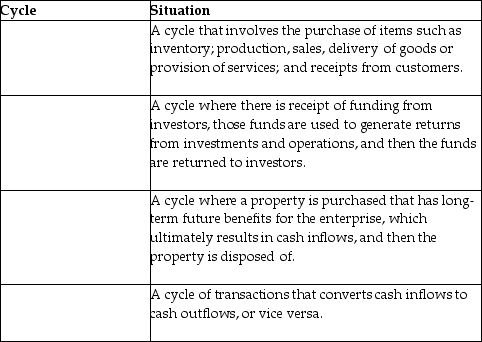

Which cycle is being described in the following situations?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

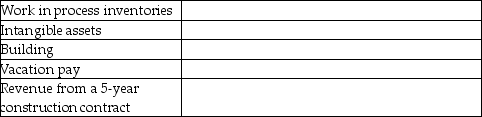

Identify at least one estimate that would be required in measuring the following financial statement items.

Question

Question

Question

Question

Question

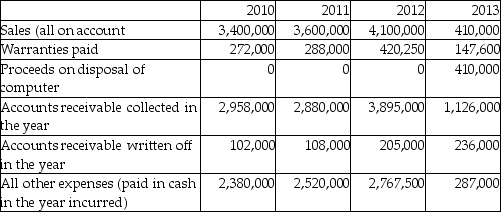

Question

Question

Question

Question

Xavier Computer Limited was started in early 2010 and continued to operate until early 2013, when it was wound up due to disputes between the two principal shareholders. When it started, the company used the following accounting policies:

1. Use 50% declining-balance depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 10% of sales.

3. The year-end allowance for doubtful accounts should be 40% of gross accounts receivable.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

1. Use 50% declining-balance depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 10% of sales.

3. The year-end allowance for doubtful accounts should be 40% of gross accounts receivable.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

Question

Computer Consulting Limited was started in early 2010 and continued to operate until early 2013, when it was wound up due to disputes between the two principal shareholders. When it started, the company used the following accounting policies:

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

Question

Question

Computer Consulting Limited was started in early 2010 and continued to operate until early 2013, when it was wound up due to disputes between the two principal shareholders. When it started, the company used these accounting policies:

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive the annual net cash flows for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive the annual net cash flows for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

Question

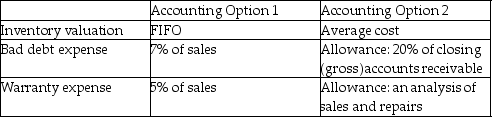

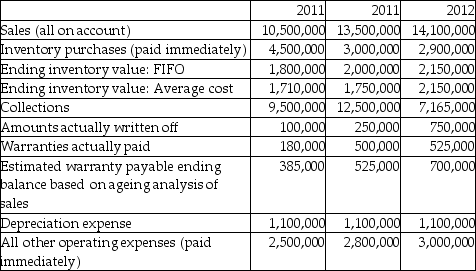

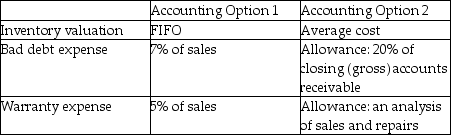

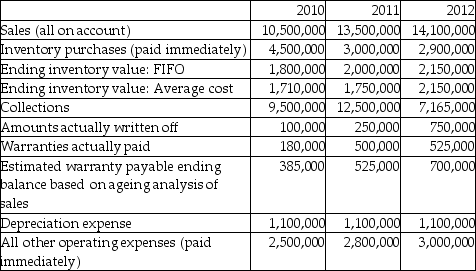

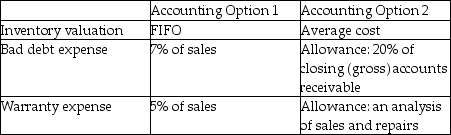

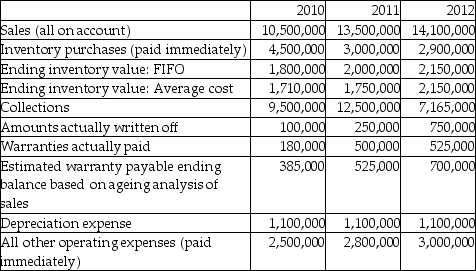

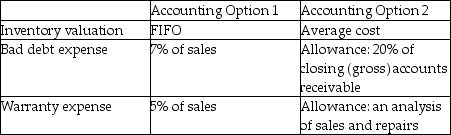

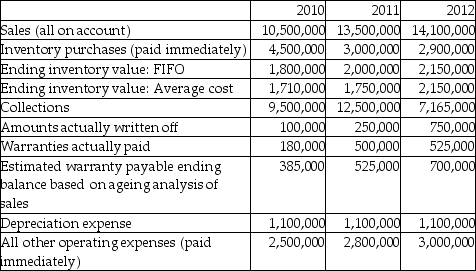

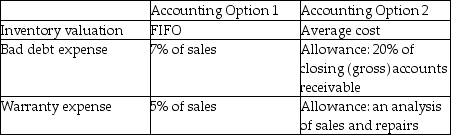

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Using the following information about activities for 2010-2012, derive the net income for each year under both accounting options:

Using the following information about activities for 2010-2012, derive the net income for each year under both accounting options:

Using the following information about activities for 2010-2012, derive the net income for each year under both accounting options: Question

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

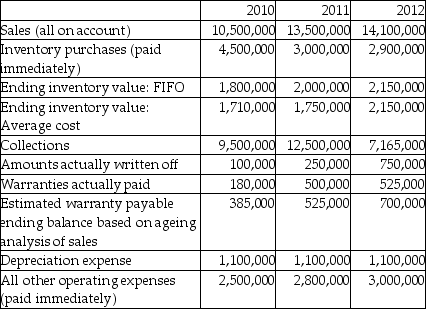

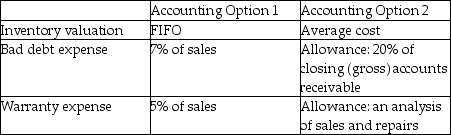

Using the following information about activities for 2010-2012, derive the 2010 net income (only)under both accounting options and explain why the net incomes are not the same.

Using the following information about activities for 2010-2012, derive the 2010 net income (only)under both accounting options and explain why the net incomes are not the same.

Using the following information about activities for 2010-2012, derive the 2010 net income (only)under both accounting options and explain why the net incomes are not the same. Question

Question

Question

Question

Question

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Assume that the company selected Accounting Option 1. Using the following information about activities for 2010-2012, derive the net income for each year:

Assume that the company selected Accounting Option 1. Using the following information about activities for 2010-2012, derive the net income for each year:

Assume that the company selected Accounting Option 1. Using the following information about activities for 2010-2012, derive the net income for each year: Question

Question

Question

Question

Question

Question

Question

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Assume that the company selected Accounting Option 2. Using the following information about activities for 2010-2012, derive the net income for each year:

Assume that the company selected Accounting Option 2. Using the following information about activities for 2010-2012, derive the net income for each year:

Assume that the company selected Accounting Option 2. Using the following information about activities for 2010-2012, derive the net income for each year: Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Using the information provided below, discuss whether the cumulative cash flows will be the same or different each accounting option.

Using the information provided below, discuss whether the cumulative cash flows will be the same or different each accounting option.

Using the information provided below, discuss whether the cumulative cash flows will be the same or different each accounting option. Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Explain why the net incomes would not be the same under both accounting options.

Explain why the net incomes would not be the same under both accounting options.

Explain why the net incomes would not be the same under both accounting options.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/159

Play

Full screen (f)

Deck 3: Accrual Accounting

1

Explain the meaning of the cash basis of accounting and the accrual basis of accounting. When is the cash basis appropriate? Why is the accrual basis used in financial reporting?

•Cash basis of accounting: Record transactions when they have been settled in cash as of the balance sheet date.

•Accrual basis of accounting: Record transactions even if they have not been settled in cash as of the balance sheet date.

•Cash accounting sufficiently meets information demand when enterprises have finite and short lives because all cash cycles close when the entity dissolves.

•Accrual accounting better satisfies the demand for information because it provides additional information on cash cycles that are not yet complete at the reporting date.

•Accrual basis of accounting: Record transactions even if they have not been settled in cash as of the balance sheet date.

•Cash accounting sufficiently meets information demand when enterprises have finite and short lives because all cash cycles close when the entity dissolves.

•Accrual accounting better satisfies the demand for information because it provides additional information on cash cycles that are not yet complete at the reporting date.

2

Which of the following is an example of the "financing" cash cycle?

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

A

3

Which of the following is not an example of a "cash" cycle?

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

C

4

What is an investing cash cycle?

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

5

What is a "cash" cycle?

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

6

Explain how financial information prepared using accrual accounting provides better information to predict future cash flows than financial information prepared using the cash basis of accounting.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

7

Explain how "accruals" are used in financial reporting. Provide an example to support your discussion.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

8

What is a financing cash cycle?

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

9

Explain the difference between a cash cycle, a financing cash cycle, an investing cash cycle and an operating cash cycle.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

10

What is a "deferral"?

A)An entry to record payments received from customers that had been outstanding for 100 days.

B)An entry that reflects accounting events or transactions after the related cash flow.

C)An entry that reflects transactions in a period different from its corresponding cash flow.

D)An entry to record the receipt of inventory that will be paid in 60 days.

A)An entry to record payments received from customers that had been outstanding for 100 days.

B)An entry that reflects accounting events or transactions after the related cash flow.

C)An entry that reflects transactions in a period different from its corresponding cash flow.

D)An entry to record the receipt of inventory that will be paid in 60 days.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

11

Explain why companies prepare financial statements on an annual basis.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

12

What is meant by the "going concern assumption" in financial accounting? Explain the implications to financial accounting if the going concern assumption is not valid.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

13

Which cycle is being described in the following situations?

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

14

What is an "accrual"?

A)An entry to record deposits received from a customer for services to be provided next year.

B)An entry that reflects accounting events or transactions after the related cash flow.

C)An entry that reflects transactions in a period different from its corresponding cash flow.

D)An entry to record the payment of a supplier invoice for goods received last month.

A)An entry to record deposits received from a customer for services to be provided next year.

B)An entry that reflects accounting events or transactions after the related cash flow.

C)An entry that reflects transactions in a period different from its corresponding cash flow.

D)An entry to record the payment of a supplier invoice for goods received last month.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is an example of an "operating" cash cycle?

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is an example of an "investing" cash cycle?

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

A)Receipt of funding from investors that is used to generate returns from investments and operations, and then returned to investors.

B)Purchase of property with long-term future benefits which results in cash inflows and then the property is disposed of.

C)Planning for product growth which results in investment opportunities that will create returns for investors.

D)Purchase of inventory, conversion into products that are delivered to customers, and receipts from customers.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

17

What is an "operating" cycle?

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

A)A cycle of transactions that converts cash inflows to cash outflows, or vice versa.

B)A cycle where there is receipt of funding from investors, those funds are used to generate returns from investments and operations, and then the funds are returned to investors.

C)A cycle where a property is purchased that has long-term future benefits for the enterprise, which ultimately results in cash inflows, and then the property is disposed of.

D)A cycle that involves the purchase of items such as inventory; production, sales, delivery of goods or provision of services; and receipts from customers.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

18

What is the accrual basis of accounting?

A)A basis of accounting that records economic events when they happen rather than only when cash exchanges occur.

B)A method of accounting that does not require accruals for amounts due or outstanding at year-end.

C)An entry that reflects accounting events and transactions after the related cash flow.

D)An entry that reflects events in a period different from their corresponding cash flow.

A)A basis of accounting that records economic events when they happen rather than only when cash exchanges occur.

B)A method of accounting that does not require accruals for amounts due or outstanding at year-end.

C)An entry that reflects accounting events and transactions after the related cash flow.

D)An entry that reflects events in a period different from their corresponding cash flow.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

19

What is the cash basis of accounting?

A)A method of accounting that records accounting transactions based on economic substance.

B)A method of accounting that requires accruals for amounts due or outstanding at year-end.

C)A method of accounting that records transactions only when cash is received or paid.

D)An entry that reflects events in a period different from their corresponding cash flow.

A)A method of accounting that records accounting transactions based on economic substance.

B)A method of accounting that requires accruals for amounts due or outstanding at year-end.

C)A method of accounting that records transactions only when cash is received or paid.

D)An entry that reflects events in a period different from their corresponding cash flow.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

20

What is the difference between accrual accounting and cash accounting?

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

21

A company's reported earnings are $2,000 and cash flows are $1,600. Based on economic conditions during the year, the company booked allowances of $150. As a result of contractual incentives, the company booked a further $250 in accruals. What is the amount of unbiased earnings?

A)$150

B)$400

C)$1,750

D)$2,000

A)$150

B)$400

C)$1,750

D)$2,000

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

22

Which statement is correct about accrual accounting?

A)Accounting estimates or professional judgment are not necessary with accrual accounting.

B)A true measure of economic or accounting income is possible with accrual accounting.

C)An accounting method that records events when they have an economic effect on the company.

D)A method of accounting that does not require accruals for amounts due or outstanding at year-end.

A)Accounting estimates or professional judgment are not necessary with accrual accounting.

B)A true measure of economic or accounting income is possible with accrual accounting.

C)An accounting method that records events when they have an economic effect on the company.

D)A method of accounting that does not require accruals for amounts due or outstanding at year-end.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

23

Dexter Corp. received cash for a service that is to be performed in the next accounting period. How should this transaction be accounted for?

A)As accrued revenue.

B)As an expense.

C)As a prepaid expense.

D)As a liability.

A)As accrued revenue.

B)As an expense.

C)As a prepaid expense.

D)As a liability.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

24

What are biased accruals?

A)Accruals based on applying GAAP.

B)Accruals based on overly optimistic estimates.

C)Accruals based on ethical considerations.

D)Accruals based on applying professional judgment.

A)Accruals based on applying GAAP.

B)Accruals based on overly optimistic estimates.

C)Accruals based on ethical considerations.

D)Accruals based on applying professional judgment.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

25

Which statement is correct?

A)The amount and types of excessive accruals are directly related to earnings quality.

B)Excessive accruals are transparent and improve the quality of financial reporting.

C)Users can routinely determine the contractual incentives causing excessive accruals.

D)Users like earnings that closely correspond to reported results without management bias.

A)The amount and types of excessive accruals are directly related to earnings quality.

B)Excessive accruals are transparent and improve the quality of financial reporting.

C)Users can routinely determine the contractual incentives causing excessive accruals.

D)Users like earnings that closely correspond to reported results without management bias.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

26

What is the impact of overstating an accrued expense during the 2013 fiscal year?

A)There is no effect on 2013 income.

B)Net income for 2013 will be overstated.

C)Current liabilities for 2013 will be understated.

D)Ending retained earnings for 2013 will be understated.

A)There is no effect on 2013 income.

B)Net income for 2013 will be overstated.

C)Current liabilities for 2013 will be understated.

D)Ending retained earnings for 2013 will be understated.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

27

Which is not an example of a biased accrual?

A)Accruals based on overly optimistic estimates.

B)Accruals based on overly conservative estimates.

C)Accruals based on achieving target level of revenues.

D)Accruals based on applying professional judgment.

A)Accruals based on overly optimistic estimates.

B)Accruals based on overly conservative estimates.

C)Accruals based on achieving target level of revenues.

D)Accruals based on applying professional judgment.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

28

A company's cash flows are $3,600. Based on economic conditions during the year, the company booked allowances of $1,500. As a result of contractual incentives, the company booked a further $700 in accruals. What is the total reported earnings of the company?

A)$1,400

B)$2,200

C)$3,600

D)$5,800

A)$1,400

B)$2,200

C)$3,600

D)$5,800

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

29

A company's reported earnings are $1,000 and cash flows are $600. Based on economic conditions during the year, the company booked allowances of $250. As a result of contractual incentives, the company booked a further $150 in accruals. What is the total of the unbiased accruals and excessive accruals?

A)$150

B)$400

C)$600

D)$1,000

A)$150

B)$400

C)$600

D)$1,000

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

30

What is meant by the phrase "true and fair view" of financial reporting?

A)The financial statements provide a true representation of the company's economic conditions and performance.

B)The financial statements provide an unbiased representation of the company's economic conditions and performance.

C)The financial statements provide a fair representation of the company's economic conditions and performance.

D)The financial statements provide an accurate representation of the company's economic conditions and performance.

A)The financial statements provide a true representation of the company's economic conditions and performance.

B)The financial statements provide an unbiased representation of the company's economic conditions and performance.

C)The financial statements provide a fair representation of the company's economic conditions and performance.

D)The financial statements provide an accurate representation of the company's economic conditions and performance.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

31

Which statement is correct?

A)Lower amounts of excessive accruals results in higher earnings quality.

B)Excessive accruals are directly observable in financial reporting.

C)It is easy to determine the contractual incentives causing excessive accruals.

D)Excessive accruals improve the comparability of financial reporting.

A)Lower amounts of excessive accruals results in higher earnings quality.

B)Excessive accruals are directly observable in financial reporting.

C)It is easy to determine the contractual incentives causing excessive accruals.

D)Excessive accruals improve the comparability of financial reporting.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

32

Identify at least one estimate that would be required in measuring the following financial statement items.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

33

Explain why estimates are necessary in accrual accounting and why a "true" measure of income cannot be provided.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

34

Why are excessive accruals a concern for accounting and financial reporting?

A)They improve the quality of earnings of the company.

B)They may represent unethical practices by the company.

C)They require too much professional judgment.

D)They result in standards overload.

A)They improve the quality of earnings of the company.

B)They may represent unethical practices by the company.

C)They require too much professional judgment.

D)They result in standards overload.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

35

A company's reported earnings are $1,000 and cash flows are $600. Based on economic conditions during the year, the company booked allowances of $250. As a result of contractual incentives, the company booked a further $150 in accruals. How much are the unbiased accruals?

A)$150

B)$250

C)$400

D)$600

A)$150

B)$250

C)$400

D)$600

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

36

What are excessive accruals?

A)Accruals that are based on professional judgment.

B)Accruals that are based on ethical considerations.

C)Accruals based on contractual incentives or opportunism.

D)Accruals required by GAAP.

A)Accruals that are based on professional judgment.

B)Accruals that are based on ethical considerations.

C)Accruals based on contractual incentives or opportunism.

D)Accruals required by GAAP.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

37

A company's reported earnings are $2,000 and cash flows are $1,600. Based on economic conditions during the year, the company booked allowances of $150. As a result of contractual incentives, the company booked a further $250 in accruals. What is the total of the excessive accruals?

A)$150

B)$250

C)$400

D)$1,600

A)$150

B)$250

C)$400

D)$1,600

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

38

Explain what is meant by "quality of earnings."

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

39

Which statement correctly explains the relationship between cash flows, accruals and reported earnings?

A)Cash flows are the best representation of a company's financial position and performance because of excessive accruals.

B)The cash basis of accounting provides the best representation of a company's financial position and performance.

C)The accrual basis of accounting provides the best representation of a company's financial position and performance.

D)Accruals reduce earnings quality but are needed in financial reporting because GAAP is founded on professional judgment.

A)Cash flows are the best representation of a company's financial position and performance because of excessive accruals.

B)The cash basis of accounting provides the best representation of a company's financial position and performance.

C)The accrual basis of accounting provides the best representation of a company's financial position and performance.

D)Accruals reduce earnings quality but are needed in financial reporting because GAAP is founded on professional judgment.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

40

What is meant by "earnings quality"?

A)A measure of how closely expense accruals correspond to actual expenses without management bias.

B)A measure to determine management bias by comparing actual reported profits with "true" earnings.

C)A measure to determine management bias by comparing reported income to actual cash flows.

D)A measure of how closely earnings correspond to earnings reported without management bias.

A)A measure of how closely expense accruals correspond to actual expenses without management bias.

B)A measure to determine management bias by comparing actual reported profits with "true" earnings.

C)A measure to determine management bias by comparing reported income to actual cash flows.

D)A measure of how closely earnings correspond to earnings reported without management bias.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

41

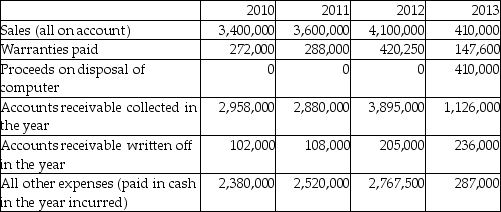

Xavier Computer Limited was started in early 2010 and continued to operate until early 2013, when it was wound up due to disputes between the two principal shareholders. When it started, the company used the following accounting policies:

1. Use 50% declining-balance depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 10% of sales.

3. The year-end allowance for doubtful accounts should be 40% of gross accounts receivable.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

1. Use 50% declining-balance depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 10% of sales.

3. The year-end allowance for doubtful accounts should be 40% of gross accounts receivable.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

42

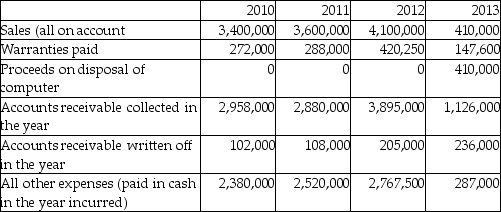

Computer Consulting Limited was started in early 2010 and continued to operate until early 2013, when it was wound up due to disputes between the two principal shareholders. When it started, the company used the following accounting policies:

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive net income for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

43

The following event occurred after the company's year-end but before the completion of the audit. For this subsequent event, determine whether the event:

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

A major client unexpectedly goes bankrupt and it is determined that you will get only 30% of the value of their account receivable as full and final settlement. (Justify your recommendation.)

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

A major client unexpectedly goes bankrupt and it is determined that you will get only 30% of the value of their account receivable as full and final settlement. (Justify your recommendation.)

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

44

Computer Consulting Limited was started in early 2010 and continued to operate until early 2013, when it was wound up due to disputes between the two principal shareholders. When it started, the company used these accounting policies:

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive the annual net cash flows for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

1. Use straight-line depreciation for the firm's only asset, a computer which cost $1,100,000 and has an estimated useful life of four years.

2. Estimate warranty expense as 9% of sales.

3. Estimate bad debts expense as 5% of sales.

Derive the annual net cash flows for 2010 to 2012. For the year-end balance for 2013, assume accounts receivable, allowance for doubtful accounts, and the warranty accrual are $0, as the firm wound itself up during the year and all timing differences have been resolved.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

45

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Using the following information about activities for 2010-2012, derive the net income for each year under both accounting options:

Using the following information about activities for 2010-2012, derive the net income for each year under both accounting options: Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

46

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Using the following information about activities for 2010-2012, derive the 2010 net income (only)under both accounting options and explain why the net incomes are not the same.

Using the following information about activities for 2010-2012, derive the 2010 net income (only)under both accounting options and explain why the net incomes are not the same. Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

47

What is the significance of the subsequent events period for accrual accounting?

A)The subsequent events period can affect the recognition of business transactions and events.

B)The subsequent events period can affect the measurement of business transactions and events.

C)The subsequent events period can affect the recognition and measurement of business transactions and events.

D)Transactions must be reported in the cut-off period before the statements are authorized.

A)The subsequent events period can affect the recognition of business transactions and events.

B)The subsequent events period can affect the measurement of business transactions and events.

C)The subsequent events period can affect the recognition and measurement of business transactions and events.

D)Transactions must be reported in the cut-off period before the statements are authorized.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

48

Assume that a company has a fiscal year of July 1, 2012-June 30, 2013. August 15, 2013, was the end of the period for gathering information pertaining to the financial statements. The financial statements were authorized for issue on August 24, 2013. What is the cut off point for the "measurement" of transactions and events in a reporting period?

A)July 1, 2012.

B)The end of the subsequent events period.

C)August 24, 2013.

D)June 30, 2013.

A)July 1, 2012.

B)The end of the subsequent events period.

C)August 24, 2013.

D)June 30, 2013.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

49

What is meant by "quality of earnings"? Discuss if earnings quality should be assessed by comparing earnings to cash flows.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

50

Assume that a company has a calendar year of January 1, 2012-December 31, 2012. March 15, 2013 was the end of the period for gathering information pertaining to the financial statements. The financial statements were authorized for issue on March 24, 2013. What is the cut off point for the "recognition" of transactions and events in a reporting period?

A)January 1, 2012.

B)March 15, 2013.

C)March 24, 2013.

D)December 31, 2012.

A)January 1, 2012.

B)March 15, 2013.

C)March 24, 2013.

D)December 31, 2012.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

51

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Assume that the company selected Accounting Option 1. Using the following information about activities for 2010-2012, derive the net income for each year:

Assume that the company selected Accounting Option 1. Using the following information about activities for 2010-2012, derive the net income for each year: Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

52

The following event occurred after the company's year-end but before the completion of the audit. For this subsequent event, determine whether the event:

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

New technology makes a major capital asset redundant or causes it to lose significant fair market and salvage value. (Justify your recommendation).

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

New technology makes a major capital asset redundant or causes it to lose significant fair market and salvage value. (Justify your recommendation).

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

53

The following event occurred after the company's year-end but before the completion of the audit. For this subsequent event, determine whether the event:

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

There is a significant fall in the market price of a major portion of inventory due to new technology making the existing items obsolete. The market price is lower than the current carrying value. (Justify your recommendation.)

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

There is a significant fall in the market price of a major portion of inventory due to new technology making the existing items obsolete. The market price is lower than the current carrying value. (Justify your recommendation.)

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

54

The following event occurred after the company's year-end but before the completion of the audit. For this subsequent event, determine whether the event:

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

There is a fire at the company's only warehouse; the company has insufficient fire insurance to replace the warehouse and contents such that a material loss will result and operations will be curtailed for six months. (Justify your recommendation)

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

There is a fire at the company's only warehouse; the company has insufficient fire insurance to replace the warehouse and contents such that a material loss will result and operations will be curtailed for six months. (Justify your recommendation)

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

55

Why is determining the "cut-off" point critical in the accrual basis of accounting?

A)Based on the periodicity concept, financial statements are prepared on a regular basis.

B)It is important to reflect business transactions and events in the subsequent accounting period.

C)The point in time at which one reporting period ends and another begins is important.

D)Transactions must be reported in the cut-off period before the statements are authorized.

A)Based on the periodicity concept, financial statements are prepared on a regular basis.

B)It is important to reflect business transactions and events in the subsequent accounting period.

C)The point in time at which one reporting period ends and another begins is important.

D)Transactions must be reported in the cut-off period before the statements are authorized.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

56

The Rihanna Company owns 1,000 shares in Abhay Corp, a public company listed on the stock exchange. The share price was as follows: - At date of purchase, July 2, 2012 = $100/share

- At year end, June 30, 2013 = $100/share

- At start of next fiscal year, July 1, 2013 = $95/share

- At date financial statements authorized for issue, September 1, 2013 = $90/share

Materiality for the Rhianna's financial statements is $500,000. What is the appropriate treatment of the subsequent event in the June 30, 2013 financial statements?

A)Adjustment in the financial statement for the decline in value of $10,000.

B)No adjustment is needed for the subsequent decline in share price to $90/share.

C)Note disclosure in the financial statements for the decline in value of $5,000.

D)Both an adjustment and note disclosure in the financial statements for the decline to $90/share.

- At year end, June 30, 2013 = $100/share

- At start of next fiscal year, July 1, 2013 = $95/share

- At date financial statements authorized for issue, September 1, 2013 = $90/share

Materiality for the Rhianna's financial statements is $500,000. What is the appropriate treatment of the subsequent event in the June 30, 2013 financial statements?

A)Adjustment in the financial statement for the decline in value of $10,000.

B)No adjustment is needed for the subsequent decline in share price to $90/share.

C)Note disclosure in the financial statements for the decline in value of $5,000.

D)Both an adjustment and note disclosure in the financial statements for the decline to $90/share.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

57

The following event occurred after the company's year-end but before the completion of the audit. For this subsequent event, determine whether the event:

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

The company experiences a major labour strike. Workers are still on strike when the audit is finished. Does your answer change if this strike might force the company into bankruptcy? (Justify your recommendation).

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

The company experiences a major labour strike. Workers are still on strike when the audit is finished. Does your answer change if this strike might force the company into bankruptcy? (Justify your recommendation).

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

58

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Assume that the company selected Accounting Option 2. Using the following information about activities for 2010-2012, derive the net income for each year:

Assume that the company selected Accounting Option 2. Using the following information about activities for 2010-2012, derive the net income for each year: Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

59

The following event occurred after the company's year-end but before the completion of the audit. For this subsequent event, determine whether the event:

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

A new competitor enters the marketplace, which will result in serious price competition and, likely, reduced income next year. (Justify your recommendation.)

•requires an adjustment to the year-end financial statements,

•requires note disclosure, or

•requires neither adjustment to recognized amounts nor disclosure.

A new competitor enters the marketplace, which will result in serious price competition and, likely, reduced income next year. (Justify your recommendation.)

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

60

Why is it important to properly define the reporting period when using the accrual basis of accounting?

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

61

If the gross profit percentage used in the gross profit inventory method were understated, which of the following is correct?

A)Cost of goods sold would be understated.

B)Ending inventory would be understated.

C)Ending inventory would be correctly stated, but beginning inventory would be incorrect.

D)Ending inventory would be overstated.

A)Cost of goods sold would be understated.

B)Ending inventory would be understated.

C)Ending inventory would be correctly stated, but beginning inventory would be incorrect.

D)Ending inventory would be overstated.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is an example of a change in accounting estimate?

A)Switching from straight-line to the declining balance method of depreciation.

B)Using 3% for the allowance for bad debts, instead of 1% as stated in the company's procedures manual.

C)Using 5% for the allowance for bad debts because of the increased possibility of bankruptcy by customers.

D)Changing from weighted average to the first-in, first-out method of inventory valuation.

A)Switching from straight-line to the declining balance method of depreciation.

B)Using 3% for the allowance for bad debts, instead of 1% as stated in the company's procedures manual.

C)Using 5% for the allowance for bad debts because of the increased possibility of bankruptcy by customers.

D)Changing from weighted average to the first-in, first-out method of inventory valuation.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

63

A correction of an accounting error involves

A)the use of hindsight.

B)retrospective restatement.

C)professional judgment.

D)prospective adjustment.

A)the use of hindsight.

B)retrospective restatement.

C)professional judgment.

D)prospective adjustment.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

64

A correction of an accounting error does not involve

A)note disclosure.

B)retrospective adjustment.

C)retrospective restatement.

D)management bias.

A)note disclosure.

B)retrospective adjustment.

C)retrospective restatement.

D)management bias.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

65

Which one of the following errors would cause a company's unadjusted trial balance to be out of balance?

A)Overstating an asset balance by $100 and a revenue balance by the same amount.

B)Failure to post the debit portion of a journal entry to the proper account (recorded, for example, in a revenue rather than an expense account).

C)Recording a $5,000 revenue transaction by crediting the accounts receivable account and debiting the revenue account.

D)Recording $1,000 cash collected from a customer as a debit to the cash account and a debit to the accounts receivable account.

A)Overstating an asset balance by $100 and a revenue balance by the same amount.

B)Failure to post the debit portion of a journal entry to the proper account (recorded, for example, in a revenue rather than an expense account).

C)Recording a $5,000 revenue transaction by crediting the accounts receivable account and debiting the revenue account.

D)Recording $1,000 cash collected from a customer as a debit to the cash account and a debit to the accounts receivable account.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

66

Correction of an error is based on

A)new information that has now become available.

B)information available at the time of preparing the financial statements.

C)the use of hindsight.

D)comparable industry practice.

A)new information that has now become available.

B)information available at the time of preparing the financial statements.

C)the use of hindsight.

D)comparable industry practice.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

67

Which statement is not correct?

A)Accruals involve uncertainty about future transactions and events.

B)Companies must use the same accounting estimates year-over-year in preparing statements.

C)A company can change its accounting policies if it provides more relevant information.

D)Higher earnings quality provides users with more decision useful financial statements.

A)Accruals involve uncertainty about future transactions and events.

B)Companies must use the same accounting estimates year-over-year in preparing statements.

C)A company can change its accounting policies if it provides more relevant information.

D)Higher earnings quality provides users with more decision useful financial statements.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

68

Changes in accounting estimates

A)are accounted for in the same manner as changes in accounting policies.

B)reduce the relevance and reliability of financial reporting.

C)are applied to current and past reporting periods.

D)are applied to current and future reporting periods.

A)are accounted for in the same manner as changes in accounting policies.

B)reduce the relevance and reliability of financial reporting.

C)are applied to current and past reporting periods.

D)are applied to current and future reporting periods.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

69

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Using the information provided below, discuss whether the cumulative cash flows will be the same or different each accounting option.

Using the information provided below, discuss whether the cumulative cash flows will be the same or different each accounting option. Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

70

A change in accounting policy

A)is accounted for on a retrospective basis, without restatement.

B)allows management to bias financial reporting.

C)is accounted for on a prospective basis, with restatement.

D)is accounted for in the same manner as an error correction.

A)is accounted for on a retrospective basis, without restatement.

B)allows management to bias financial reporting.

C)is accounted for on a prospective basis, with restatement.

D)is accounted for in the same manner as an error correction.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

71

Changes in accounting estimates are

A)accounted for in the same manner as accounting policy changes.

B)accounted for on a prospective basis.

C)applied to current and past reporting periods.

D)accounted for in the same manner as error corrections.

A)accounted for in the same manner as accounting policy changes.

B)accounted for on a prospective basis.

C)applied to current and past reporting periods.

D)accounted for in the same manner as error corrections.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is an example of an error that should be corrected?

A)Switching from straight-line to the declining balance method of depreciation.

B)Changing from weighted average to the first-in, first out method of inventory valuation.

C)Using 5% for bad debts provision, but 1% is required in the company's procedures manual.

D)Starting to capitalize fixed assets under $1,000 which were previously considered immaterial.

A)Switching from straight-line to the declining balance method of depreciation.

B)Changing from weighted average to the first-in, first out method of inventory valuation.

C)Using 5% for bad debts provision, but 1% is required in the company's procedures manual.

D)Starting to capitalize fixed assets under $1,000 which were previously considered immaterial.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

73

Changes in accounting estimates are based on

A)information available from the use of hindsight.

B)information available at the time financial statements are prepared.

C)providing comparable information in the financial statements.

D)low quality of professional judgment being exercised.

A)information available from the use of hindsight.

B)information available at the time financial statements are prepared.

C)providing comparable information in the financial statements.

D)low quality of professional judgment being exercised.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

74

The method of depreciation was changed from the double-declining-balance method to the straight-line method in fiscal 2013. A machine was purchased on January 1, 2011, at a cost of $150,000. The machine has an estimated useful life of 10 years and a residual value of $9,000. What is the appropriate accounting?

A)Retrospective adjustment for fiscal 2013.

B)Retrospective adjustment for fiscal 2011 and 2012.

C)Prospective adjustment from fiscal 2012 going forward.

D)Error correction for fiscal 2013.

A)Retrospective adjustment for fiscal 2013.

B)Retrospective adjustment for fiscal 2011 and 2012.

C)Prospective adjustment from fiscal 2012 going forward.

D)Error correction for fiscal 2013.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

75

A change in accounting policy should

A)be based on changes in the underlying economics of business transactions.

B)not be based on management's best discretion.

C)be based on improving the comparability of financial reporting.

D)not be based on changes to accounting standards.

A)be based on changes in the underlying economics of business transactions.

B)not be based on management's best discretion.

C)be based on improving the comparability of financial reporting.

D)not be based on changes to accounting standards.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

76

Which of the following is an example of a change in accounting policy?

A)Changing from weighted average to the first-in, first-out method of inventory valuation.

B)Capitalizing a delivery truck that had previously been expensed.

C)Using 5% for the allowance for bad debts because of the increased possibility of bankruptcy by customers.

D)Using 4% for the allowance for bad debts, instead of 2% as stated in the company's procedures manual.

A)Changing from weighted average to the first-in, first-out method of inventory valuation.

B)Capitalizing a delivery truck that had previously been expensed.

C)Using 5% for the allowance for bad debts because of the increased possibility of bankruptcy by customers.

D)Using 4% for the allowance for bad debts, instead of 2% as stated in the company's procedures manual.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

77

Which of the following would result in an overstatement in reported net income?

A)Failure to record $45,000 collection of accounts receivable.

B)Expensing rather than capitalizing the $12,500 cost of a capital asset.

C)Failure to record an accrued revenue of $24,000.

D)Failure to record an accrued expense of $18,000.

A)Failure to record $45,000 collection of accounts receivable.

B)Expensing rather than capitalizing the $12,500 cost of a capital asset.

C)Failure to record an accrued revenue of $24,000.

D)Failure to record an accrued expense of $18,000.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

78

Changes in accounting estimates are based on

A)new information that has now become available.

B)management bias.

C)information available from the use of hindsight.

D)comparable industry practice.

A)new information that has now become available.

B)management bias.

C)information available from the use of hindsight.

D)comparable industry practice.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

79

Which statement is correct?

A)Accounting policy changes should reflect changes in economic circumstances.

B)Accounting errors are corrected prospectively in the financial statements.

C)Changes in accounting estimates are corrected retrospectively in the statements.

D)Correction of accounting errors proves that management bias exists in reporting.

A)Accounting policy changes should reflect changes in economic circumstances.

B)Accounting errors are corrected prospectively in the financial statements.

C)Changes in accounting estimates are corrected retrospectively in the statements.

D)Correction of accounting errors proves that management bias exists in reporting.

Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

80

Sing Songs Ltd. started operations on January 1, 2010. During its first year of operations, the company had a choice of accounting policies:

Explain why the net incomes would not be the same under both accounting options.

Explain why the net incomes would not be the same under both accounting options. Unlock Deck

Unlock for access to all 159 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 159 flashcards in this deck.