Deck 8: Property, Plant, and Equipment

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2013, BigBen purchased a machine, incurring the expenditures listed below. The machine had an estimated useful life of 10 years, and BigBen uses straight-line depreciation for its equipment.  What amount should be capitalized as the cost of the machinery for 2013?

What amount should be capitalized as the cost of the machinery for 2013?

A)$100,000

B)$110,000

C)$115,000

D)$155,000

What amount should be capitalized as the cost of the machinery for 2013?A)$100,000

B)$110,000

C)$115,000

D)$155,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

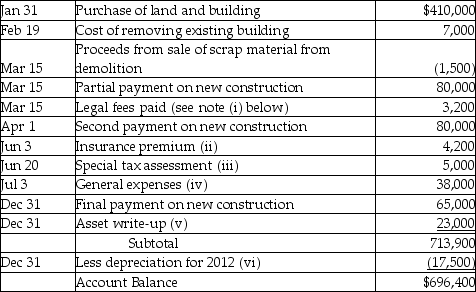

Zach Co. Ltd. was incorporated on January 2, 2012, but was unable to begin their manufacturing operations immediately. The new factory facilities became available for use on July 1, 2012. During the start-up period, the company provisionally used a "Land and Factory Building" account to record the following transactions, in chronological order:

Additional info

Additional info

i. Legal fees of $3,200 covered the following:

ii. Insurance covered the building for a one-year term beginning April 1, 2012.

ii. Insurance covered the building for a one-year term beginning April 1, 2012.

iii. The special tax assessment covered repaving the street in front of the building.

iv. General expenses covered the following for the period January 2, 2012 to June 30, 2012.

v. The board of directors increased the value of the building by $23,000, believing that such an increase was justified to reflect the current market at the time the building was completed; Retained Earnings was credited for this amount.

v. The board of directors increased the value of the building by $23,000, believing that such an increase was justified to reflect the current market at the time the building was completed; Retained Earnings was credited for this amount.

vi. Engineers estimate the useful life of the building to be 40 years. The company believes that the declining balance method at a 5% rate is appropriate. The company's policy for new PPE is to depreciate the assets according to the time available for use in the fiscal year, rounded to the closest month.

Required:

Prepare entries to reflect correct land, factory building, and accumulated depreciation accounts at December 31, 2012. Round values to the nearest dollar, if necessary.

Additional infoi. Legal fees of $3,200 covered the following:

ii. Insurance covered the building for a one-year term beginning April 1, 2012.iii. The special tax assessment covered repaving the street in front of the building.

iv. General expenses covered the following for the period January 2, 2012 to June 30, 2012.

v. The board of directors increased the value of the building by $23,000, believing that such an increase was justified to reflect the current market at the time the building was completed; Retained Earnings was credited for this amount.vi. Engineers estimate the useful life of the building to be 40 years. The company believes that the declining balance method at a 5% rate is appropriate. The company's policy for new PPE is to depreciate the assets according to the time available for use in the fiscal year, rounded to the closest month.

Required:

Prepare entries to reflect correct land, factory building, and accumulated depreciation accounts at December 31, 2012. Round values to the nearest dollar, if necessary.

Question

Question

Question

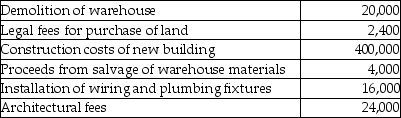

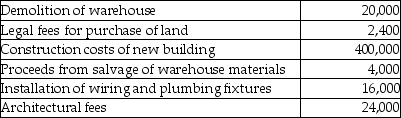

On March 1, 2013, Penguin Company (PC)had been renting its office building for several years and decided to have a new office building constructed. On April 1, 2013, it acquired land with an abandoned warehouse on it for $100,000. Other costs included:  How much will be capitalized to "building" in fiscal 2013?

How much will be capitalized to "building" in fiscal 2013?

A)$380,000

B)$400,000

C)$420,000

D)$440,000

How much will be capitalized to "building" in fiscal 2013?A)$380,000

B)$400,000

C)$420,000

D)$440,000

Question

Question

Question

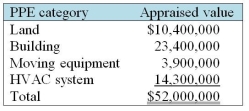

Forest Company paid $38,000,000 for a warehouse and related assets from a company that was in bankruptcy. The warehouse includes land, building, moving equipment, and heating /ventilation/air conditioning (HVAC)system. An independent appraiser valued these items individually as follows:  Required:

Required:

Allocate the purchase price among the assets acquired.

Required:Allocate the purchase price among the assets acquired.

Question

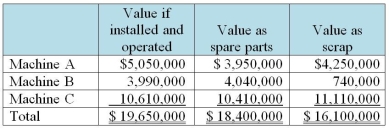

Celtic Company bought three used machines located in Toronto for $20,000,000. The arrangement with the seller is to move all the equipment to Celtic's factory in Edmonton. It is understood that some of the equipment will be sold as scrap or disassembled and used as spare parts. A careful inventory of all the equipment is shown below. Celtic's plans are to maximize the value of each item by using it in its most beneficial manner.  Required:

Required:

Allocate the purchase price among the assets acquired.

Required:Allocate the purchase price among the assets acquired.

Question

Question

Question

Question

Question

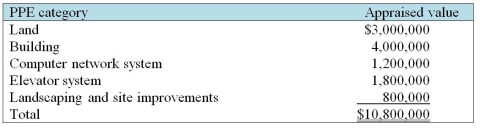

Office Plus Company bought an office building for $9,000,000 so it could consolidate its entire senior management staff in one location. An independent appraiser valued these items individually as follows:  Prior to completing the purchase, Office Plus' management decided that it will remove the computer network system and replace it with fiber-optic cables and related technologies.

Prior to completing the purchase, Office Plus' management decided that it will remove the computer network system and replace it with fiber-optic cables and related technologies.

Required:

Allocate the purchase price among the assets acquired.

Prior to completing the purchase, Office Plus' management decided that it will remove the computer network system and replace it with fiber-optic cables and related technologies.Required:

Allocate the purchase price among the assets acquired.

Question

Question

On March 1, 2013, Pear Company (PC)had been renting its office building for several years and decided to have a new office building constructed. On April 1, 2013, it acquired land with an abandoned warehouse on it for $100,000. Other costs included:  How much will be capitalized to "land" in fiscal 2013?

How much will be capitalized to "land" in fiscal 2013?

A)$100,000

B)$102,400

C)$118,400

D)$124,000

How much will be capitalized to "land" in fiscal 2013?A)$100,000

B)$102,400

C)$118,400

D)$124,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

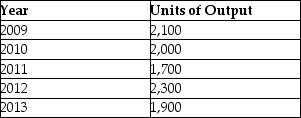

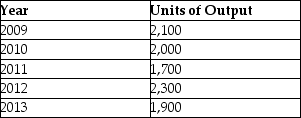

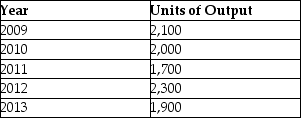

Fantasy Limited purchased equipment on January 1, 2009 for $275,000. The asset's useful life was estimated at 5 years or 10,000 units of output, with no residual value. The company has a December 31 year end. Additional Information

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?

A)$25.00

B)$27.50

C)$52,500

D)$57,750

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?A)$25.00

B)$27.50

C)$52,500

D)$57,750

Question

Question

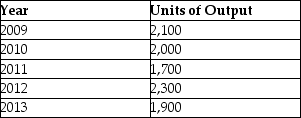

Plastic Moulds purchased equipment on January 1, 2009 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Additional information:  Assuming the company uses the units-of-production depreciation method, what is the depreciation rate per unit for 2009?

Assuming the company uses the units-of-production depreciation method, what is the depreciation rate per unit for 2009?

A)$25.00

B)$27.50

C)$57,750

D)$52,500

Assuming the company uses the units-of-production depreciation method, what is the depreciation rate per unit for 2009?A)$25.00

B)$27.50

C)$57,750

D)$52,500

Question

Question

Question

Billu Limited purchased equipment on January 1, 2009 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Additional information:  Assuming the company uses the units-of-production depreciation method, calculate the depreciation expense for 2012.

Assuming the company uses the units-of-production depreciation method, calculate the depreciation expense for 2012.

A)$25.00

B)$57,500

C)$63,250

D)$202,500

Assuming the company uses the units-of-production depreciation method, calculate the depreciation expense for 2012.A)$25.00

B)$57,500

C)$63,250

D)$202,500

Question

Question

Question

Fantasmic Moulds purchased equipment on January 1, 2009 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Additional Information

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?

A)$25.00

B)$27.50

C)$52,500

D)$57,750

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?A)$25.00

B)$27.50

C)$52,500

D)$57,750

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/127

Play

Full screen (f)

Deck 8: Property, Plant, and Equipment

1

In December 2012, Ami, the owner of Elm, paid for a parcel of land along with a warehouse on behalf of Elm, the registered owner of the property, for a total cost of $700,000. Ami also paid a real estate commission of $35,000 and legal fees of $5,000 in connection with this purchase, plus $25,000 for the demolition of the warehouse. Elm will reimburse Ami for these costs in January 2013 and will begin construction of an office building on this land. Prior to the purchase, the land and warehouse were appraised at $500,000 and $200,000, respectively. How much should be capitalized to the value of the building in 2012?

A)$0

B)$35,000

C)$235,000

D)$270,000

A)$0

B)$35,000

C)$235,000

D)$270,000

A

2

What is the accounting treatment recommended under IFRS for interest capitalization for property, plant and equipment (PPE)?

A)Capitalize cost of debt directly attributable to construction of the PPE.

B)Capitalize cost of internal funds directly attributable to construction of the PPE.

C)Expense cost of debt directly attributable to construction of the PPE.

D)IFRS does not provide any specific guidance for interest capitalization.

A)Capitalize cost of debt directly attributable to construction of the PPE.

B)Capitalize cost of internal funds directly attributable to construction of the PPE.

C)Expense cost of debt directly attributable to construction of the PPE.

D)IFRS does not provide any specific guidance for interest capitalization.

A

3

What costs should not be capitalized to "equipment"?

A)Non-refundable sales tax

B)Equipment purchase cost

C)General training

D)Transportation and delivery

A)Non-refundable sales tax

B)Equipment purchase cost

C)General training

D)Transportation and delivery

C

4

Which of the following is a concern on the initial recognition of property, plant and equipment?

A)Whether a gain or loss to be recorded in the income statement.

B)How much should be recorded on the balance sheet at the acquisition date.

C)What amount should be recorded on the balance sheet at the reporting date.

D)What expenditures should be capitalized on the balance sheet.

A)Whether a gain or loss to be recorded in the income statement.

B)How much should be recorded on the balance sheet at the acquisition date.

C)What amount should be recorded on the balance sheet at the reporting date.

D)What expenditures should be capitalized on the balance sheet.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

5

Under IFRS, what is the acceptable treatment for borrowing costs on a self constructed property, plant and equipment?

A)Capitalize costs that would have been avoided if the expenditure had not been made.

B)Capitalize costs of any internal debt incurred within the corporation.

C)Capitalize all indirectly attributable borrowing costs and expense the directly attributable costs.

D)A company can make a policy choice on the treatment of borrowing costs.

A)Capitalize costs that would have been avoided if the expenditure had not been made.

B)Capitalize costs of any internal debt incurred within the corporation.

C)Capitalize all indirectly attributable borrowing costs and expense the directly attributable costs.

D)A company can make a policy choice on the treatment of borrowing costs.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

6

What is the IFRS treatment for replacements versus repairs?

A)Betterments are expensed because they do not extend the life of the asset.

B)Replacement of significant asset components are capitalized.

C)Repairs are capitalized because they do occur on a recurring basis.

D)A company can make a policy choice on the treatment of these expenditures.

A)Betterments are expensed because they do not extend the life of the asset.

B)Replacement of significant asset components are capitalized.

C)Repairs are capitalized because they do occur on a recurring basis.

D)A company can make a policy choice on the treatment of these expenditures.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

7

What costs should not be capitalized to "equipment"?

A)Non-refundable sales tax

B)Refundable sales tax

C)Interest during construction of equipment

D)Transportation and delivery

A)Non-refundable sales tax

B)Refundable sales tax

C)Interest during construction of equipment

D)Transportation and delivery

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

8

What costs should not be capitalized to "building"?

A)Construction permits

B)Engineering surveys

C)Property transfer tax

D)Interest during construction

A)Construction permits

B)Engineering surveys

C)Property transfer tax

D)Interest during construction

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

9

On January 1, 2013, BigBen purchased a machine, incurring the expenditures listed below. The machine had an estimated useful life of 10 years, and BigBen uses straight-line depreciation for its equipment. What amount should be capitalized as the cost of the machinery for 2013?

A)$100,000

B)$110,000

C)$115,000

D)$155,000

What amount should be capitalized as the cost of the machinery for 2013?A)$100,000

B)$110,000

C)$115,000

D)$155,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

10

What costs should not be capitalized to "equipment"?

A)Non-refundable sales tax

B)Equipment purchase cost

C)Abnormal waste in testing

D)Equipment specific training

A)Non-refundable sales tax

B)Equipment purchase cost

C)Abnormal waste in testing

D)Equipment specific training

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

11

Under ASPE, what is the acceptable treatment for borrowing costs on a self constructed property, plant and equipment?

A)Must capitalize costs that would have been avoided if the expenditure had not been made.

B)Must capitalize costs of any debt incurred for the inventory needs of the corporation.

C)Must expense the directly attributable borrowing costs on qualifying assets.

D)A company can make a policy choice on the treatment of borrowing costs.

A)Must capitalize costs that would have been avoided if the expenditure had not been made.

B)Must capitalize costs of any debt incurred for the inventory needs of the corporation.

C)Must expense the directly attributable borrowing costs on qualifying assets.

D)A company can make a policy choice on the treatment of borrowing costs.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

12

In December 2012, Ami, the owner of Elm, paid for a parcel of land along with a warehouse on behalf of Elm, the registered owner of the property, for a total cost of $700,000. Ami also paid a real estate commission of $35,000 and legal fees of $5,000 in connection with this purchase, plus $25,000 for the demolition of the warehouse. Elm will reimburse Ami for these costs in January 2013 and will begin construction of an office building on this land. Prior to the purchase, the land and warehouse were appraised at $500,000 and $200,000, respectively. How much should be capitalized to the value of the land in 2012?

A)$0

B)$505,000

C)$730,000

D)$765,000

A)$0

B)$505,000

C)$730,000

D)$765,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

13

What costs should be capitalized to "land"?

A)Construction permits.

B)Engineering surveys.

C)Property transfer tax.

D)Interest during construction.

A)Construction permits.

B)Engineering surveys.

C)Property transfer tax.

D)Interest during construction.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is a not characteristic of property, plant and equipment (PPE)?

A)PPE are tangible items.

B)PPE benefit more than one year.

C)PPE are held for use in the ordinary course of business.

D)PPE have fixed and determinable future cash flows.

A)PPE are tangible items.

B)PPE benefit more than one year.

C)PPE are held for use in the ordinary course of business.

D)PPE have fixed and determinable future cash flows.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

15

Explain why earnings manipulation of property, plant and equipment can have long-lasting impact on the financial statements.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is not a characteristic of property, plant and equipment (PPE)?

A)PPE are held for sale in the ordinary course of business.

B)PPE are held for administrative purposes of the business.

C)PPE are held for use in the ordinary course of business.

D)PPE are held for rental to others by the business.

A)PPE are held for sale in the ordinary course of business.

B)PPE are held for administrative purposes of the business.

C)PPE are held for use in the ordinary course of business.

D)PPE are held for rental to others by the business.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

17

What costs should not be capitalized to "building"?

A)Demolition of old structures

B)Engineering surveys

C)Interest during construction

D)Construction permits

A)Demolition of old structures

B)Engineering surveys

C)Interest during construction

D)Construction permits

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is not a characteristic of a property, plant and equipment (PPE)?

A)No physical substance

B)Identifiable

C)Non-monetary

D)Provides future cash flows

A)No physical substance

B)Identifiable

C)Non-monetary

D)Provides future cash flows

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

19

How should $45,000 spent to obtain greater productive efficiency for a machine with a carrying value of $80,000 be accounted for?

A)Capitalized, then depreciated during current and subsequent periods.

B)Expensed in the period in which the cost occurs.

C)Charged to accumulated depreciation with no change in the depreciation rate.

D)Charged to retained earnings.

A)Capitalized, then depreciated during current and subsequent periods.

B)Expensed in the period in which the cost occurs.

C)Charged to accumulated depreciation with no change in the depreciation rate.

D)Charged to retained earnings.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

20

Which question must be considered at the initial recognition of property, plant and equipment?

A)How the costs that have been capitalized should be categorized or classified in the balance sheet?

B)Whether the historical cost or fair value model should be used?

C)Whether the straight-line or double-declining balance method should be used?

D)How the property, plant and equipment should be tested for impairment?

A)How the costs that have been capitalized should be categorized or classified in the balance sheet?

B)Whether the historical cost or fair value model should be used?

C)Whether the straight-line or double-declining balance method should be used?

D)How the property, plant and equipment should be tested for impairment?

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

21

Daniel Manufacturing Limited (DML)purchased a large lathe. The invoice cost of the lathe was $6,200,000 but DML was able to get the price reduced to $5,800,000. The seller provided terms whereby if the entire amount was paid within 30 days a further discount of 3% was available. DML paid on the 25th day. Transportation of the machine cost DML $70,000. Insurance while in transit was $30,000. To encourage DML to purchase another machine, the manufacturer gave DML a $50,000 discount voucher on its next purchase of a similar machine. Workers were paid $45,000 to install the machine. Start-up and testing costs were $45,000. Unfortunately, during the installation, one of the workers accidentally damaged the machine, and it cost $15,000 to repair the damage. Non-refundable sales taxes paid were $700,000, however, later a sales tax rebate of $80,000 was received relating to this transaction. During installation, part of the plant had to be shut down; lost profit from the shutdown was $100,000.

Required:

For each expenditure, identify whether it should be included in the cost of the lathe or expensed. Briefly justify each of your responses.

Required:

For each expenditure, identify whether it should be included in the cost of the lathe or expensed. Briefly justify each of your responses.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

22

A truck has a new engine installed for $155,000 which will increase gas mileage by 25% and reduce pollution. Originally, the truck and engine were not set up as separate assets. Management confidently estimates that the cost of the engine is one-third of the overall cost of the truck. The truck's original cost was $420,000 and it is 40% depreciated.

Prepare the necessary journal entries to record the transaction. Provide a short justification for your chosen treatment.

Prepare the necessary journal entries to record the transaction. Provide a short justification for your chosen treatment.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

23

Steep Mountain Ski Resort has been granted a 20-year permit to develop and operate a snow skiing operation in a national park. After 20 years the site must be returned to its original condition. The roads may remain, as they can be used for fire prevention purposes. In the spring and summer before the ski hill opened, the following transactions and events occurred:

i. Installed three ski lifts for a total cost of $120,000,000.

ii. Built a ski chalet for $60,000,000.

iii. Removed trees and cleared the area for ski runs at a cost of $20,000,000.

iv. Received $8,000,000 for the trees that were removed for the ski runs.

v. Put in roads for a cost of $68,000,000.

vi. Paved an area at the base of the mountain for a parking lot at a cost of $11,000,000.

vii. Estimated that it would cost $36,000,000 to dismantle the ski lifts in 20 years but that these lifts could be sold as scrap steel for $2,000,000. The chalet could be removed for $24,000,000. Reforesting the site would cost $7,000,000. Removing the parking lot will cost $3,800,000.

Required:

a. Prepare journal entries to record transactions i. to vi.

b. Prepare a journal entry to record transaction vii. Assume all these costs will be set up in a single account called "site restoration cost." Assume a 6% discount rate. Round to the nearest dollar.

c. Record all year-end journal entries for the above items for the first year of operations. The company uses straight-line depreciation for all assets. Round to the nearest dollar.

i. Installed three ski lifts for a total cost of $120,000,000.

ii. Built a ski chalet for $60,000,000.

iii. Removed trees and cleared the area for ski runs at a cost of $20,000,000.

iv. Received $8,000,000 for the trees that were removed for the ski runs.

v. Put in roads for a cost of $68,000,000.

vi. Paved an area at the base of the mountain for a parking lot at a cost of $11,000,000.

vii. Estimated that it would cost $36,000,000 to dismantle the ski lifts in 20 years but that these lifts could be sold as scrap steel for $2,000,000. The chalet could be removed for $24,000,000. Reforesting the site would cost $7,000,000. Removing the parking lot will cost $3,800,000.

Required:

a. Prepare journal entries to record transactions i. to vi.

b. Prepare a journal entry to record transaction vii. Assume all these costs will be set up in a single account called "site restoration cost." Assume a 6% discount rate. Round to the nearest dollar.

c. Record all year-end journal entries for the above items for the first year of operations. The company uses straight-line depreciation for all assets. Round to the nearest dollar.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

24

Discuss how inappropriate capitalization of costs during the acquisition of PPE can manipulate earnings.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

25

Zach Co. Ltd. was incorporated on January 2, 2012, but was unable to begin their manufacturing operations immediately. The new factory facilities became available for use on July 1, 2012. During the start-up period, the company provisionally used a "Land and Factory Building" account to record the following transactions, in chronological order:

Additional info

i. Legal fees of $3,200 covered the following:

ii. Insurance covered the building for a one-year term beginning April 1, 2012.

iii. The special tax assessment covered repaving the street in front of the building.

iv. General expenses covered the following for the period January 2, 2012 to June 30, 2012.

v. The board of directors increased the value of the building by $23,000, believing that such an increase was justified to reflect the current market at the time the building was completed; Retained Earnings was credited for this amount.

vi. Engineers estimate the useful life of the building to be 40 years. The company believes that the declining balance method at a 5% rate is appropriate. The company's policy for new PPE is to depreciate the assets according to the time available for use in the fiscal year, rounded to the closest month.

Required:

Prepare entries to reflect correct land, factory building, and accumulated depreciation accounts at December 31, 2012. Round values to the nearest dollar, if necessary.

Additional infoi. Legal fees of $3,200 covered the following:

ii. Insurance covered the building for a one-year term beginning April 1, 2012.iii. The special tax assessment covered repaving the street in front of the building.

iv. General expenses covered the following for the period January 2, 2012 to June 30, 2012.

v. The board of directors increased the value of the building by $23,000, believing that such an increase was justified to reflect the current market at the time the building was completed; Retained Earnings was credited for this amount.vi. Engineers estimate the useful life of the building to be 40 years. The company believes that the declining balance method at a 5% rate is appropriate. The company's policy for new PPE is to depreciate the assets according to the time available for use in the fiscal year, rounded to the closest month.

Required:

Prepare entries to reflect correct land, factory building, and accumulated depreciation accounts at December 31, 2012. Round values to the nearest dollar, if necessary.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

26

A large piece of earth-moving equipment was upgraded at a cost of $440,000 so that it could self-unload. After the upgrade was completed, management estimated that this feature would save the company $40,000 a year for the next six years.

Prepare the necessary journal entry to record the transaction. Provide a short justification for your chosen treatment.

Prepare the necessary journal entry to record the transaction. Provide a short justification for your chosen treatment.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

27

Using the conceptual framework, explain why there is a difference between IFRS and ASPE in accounting for interest capitalization for property, plant and equipment.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

28

On March 1, 2013, Penguin Company (PC)had been renting its office building for several years and decided to have a new office building constructed. On April 1, 2013, it acquired land with an abandoned warehouse on it for $100,000. Other costs included: How much will be capitalized to "building" in fiscal 2013?

A)$380,000

B)$400,000

C)$420,000

D)$440,000

How much will be capitalized to "building" in fiscal 2013?A)$380,000

B)$400,000

C)$420,000

D)$440,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

29

Every three years a major component (part #45)in a machine must be replaced. By doing this regular but expensive repair the machine can be used for 15 years. If Part #45 were not replaced, the machine could be used only for a maximum of six years. When the machine was originally purchased for $5,000,000 it was set up as two components: the machine was depreciated over its estimated useful life of 15 years and Part #45 was recognized as a separate PPE asset and depreciated over three years.

Recently this repair was completed at a cost of $700,000 for Part #45. The earlier Part #45 cost $550,000 when it was installed three years ago. Neither the old nor the new Part #45 has any residual value.

Prepare the necessary journal entries to record the transaction. Provide a short justification for your chosen treatment.

Recently this repair was completed at a cost of $700,000 for Part #45. The earlier Part #45 cost $550,000 when it was installed three years ago. Neither the old nor the new Part #45 has any residual value.

Prepare the necessary journal entries to record the transaction. Provide a short justification for your chosen treatment.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

30

A car rental company has a fleet of 32,000 cars. Every three months all the cars are given scheduled oil changes, rotation, and replacement of small components. The cost per car is $210, ($70 in parts and $140 for the wages of the in-house mechanics), $6,720,000 in total. As well, for half of the cars a satellite radio receiver was installed at a cost of $150 each (total $2,400,000). The gadget allows the car to receive satellite radio. The company will provide this service free and promote it heavily to increase rentals. This advertising campaign will cost $1,500,000. After the original free use of the satellite feature, the company will charge later users a fee for the use of satellite radio.

Prepare the necessary journal entry to record the above transactions. Provide a short justification for your chosen treatment.

Prepare the necessary journal entry to record the above transactions. Provide a short justification for your chosen treatment.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

31

Forest Company paid $38,000,000 for a warehouse and related assets from a company that was in bankruptcy. The warehouse includes land, building, moving equipment, and heating /ventilation/air conditioning (HVAC)system. An independent appraiser valued these items individually as follows: Required:

Allocate the purchase price among the assets acquired.

Required:Allocate the purchase price among the assets acquired.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

32

Celtic Company bought three used machines located in Toronto for $20,000,000. The arrangement with the seller is to move all the equipment to Celtic's factory in Edmonton. It is understood that some of the equipment will be sold as scrap or disassembled and used as spare parts. A careful inventory of all the equipment is shown below. Celtic's plans are to maximize the value of each item by using it in its most beneficial manner. Required:

Allocate the purchase price among the assets acquired.

Required:Allocate the purchase price among the assets acquired.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

33

Explain why it is necessary to separate property, plant and equipment (PPE)items into separate components.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

34

An important piece of equipment requires major maintenance. Management has decided to upgrade the machine, by installing a new component which will extend the useful life of the machine from the three remaining years to five more years. The regular part could have been purchased for $75,000 but a more reliable part cost $225,000. The replaced part was not set up as a separate asset when the machine was purchased.

Prepare the necessary journal entry to record the transaction. Provide a short justification for your chosen treatment.

Prepare the necessary journal entry to record the transaction. Provide a short justification for your chosen treatment.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

35

Praguian Company built two similar buildings. Each building took one year to build and required $30,000,000 in construction costs. The Company had limited internal financial resources, so it could fund only Building A internally and financed Building B by borrowing the $30,000,000 evenly over the year (i.e., zero at the beginning and increasing to $30 million by the end of the year). The interest rate on the loan is 10%. Both projects were finished on December 31, 2012 and were ready for occupancy immediately. The buildings are estimated to have a useful life of 20 years and no residual value. The Company uses the straight-line method for depreciation.

Required:

a. How much interest cost can be capitalized on Building B?

b. What will be the annual depreciation expense for each of the two buildings?

c. ASPE allows interest capitalization while IFRS recommends capitalization of interest on construction-specific loans. Ignoring the complexities of how to determine how much interest to capitalize, which treatment of interest costs is conceptually more correct? Explain your conclusion.

d. Why can interest costs not continue to be capitalized after the self-construction period is completed?

Required:

a. How much interest cost can be capitalized on Building B?

b. What will be the annual depreciation expense for each of the two buildings?

c. ASPE allows interest capitalization while IFRS recommends capitalization of interest on construction-specific loans. Ignoring the complexities of how to determine how much interest to capitalize, which treatment of interest costs is conceptually more correct? Explain your conclusion.

d. Why can interest costs not continue to be capitalized after the self-construction period is completed?

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

36

Explain what costs should be capitalized to property, plant and equipment. Include a discussion of costs incurred for acquired assets, self constructed assets and repairs.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

37

Office Plus Company bought an office building for $9,000,000 so it could consolidate its entire senior management staff in one location. An independent appraiser valued these items individually as follows: Prior to completing the purchase, Office Plus' management decided that it will remove the computer network system and replace it with fiber-optic cables and related technologies.

Required:

Allocate the purchase price among the assets acquired.

Prior to completing the purchase, Office Plus' management decided that it will remove the computer network system and replace it with fiber-optic cables and related technologies.Required:

Allocate the purchase price among the assets acquired.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

38

Every three years a major component (part #45)in a machine must be replaced. By doing this regular but expensive repair the machine can be used for 15 years. If Part #45 were not replaced, the machine could be used only for a maximum of six years. When the machine was originally purchased for $5,000,000 it was set up as one asset and depreciated over its estimated useful life of 15 years. Recently this repair was completed at a cost of $700,000 for Part #45. The earlier Part #45 cost $550,000 when it was installed three years ago. Neither the old nor the new Part #45 has any residual value.

Prepare the necessary journal entry to record the transaction. Provide a short justification for your chosen treatment.

Prepare the necessary journal entry to record the transaction. Provide a short justification for your chosen treatment.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

39

On March 1, 2013, Pear Company (PC)had been renting its office building for several years and decided to have a new office building constructed. On April 1, 2013, it acquired land with an abandoned warehouse on it for $100,000. Other costs included: How much will be capitalized to "land" in fiscal 2013?

A)$100,000

B)$102,400

C)$118,400

D)$124,000

How much will be capitalized to "land" in fiscal 2013?A)$100,000

B)$102,400

C)$118,400

D)$124,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

40

Coffee-Bean Company built two similar buildings. Each building took one year to build and required $25 million in construction costs. Given the Company's limited internal financial resources, only Building Hazel could be internally financed; Building Cinnamon was financed by a $20 million loan evenly over the year (i.e., zero at the beginning and increasing to $20 million by the end of the year). The interest rate on the loan is 8%.

Both projects were finished on December 31, 2013 and were ready for occupancy immediately. The Hazel building will have an estimated useful life of 30 years while the Cinnamon building will have an expected useful life of 40 years. Neither value will have a residual value. The Company uses the straight-line method for depreciation.

Required:

a. How much interest cost can be capitalized on Building Cinnamon?

b. What will be the annual depreciation expense for each of the two buildings?

c. ASPE allows interest capitalization while IFRS recommends capitalization of interest on construction-specific loans. Ignoring the complexities of how to determine how much interest to capitalize, which treatment of interest costs is conceptually more correct? Explain your conclusion.

d. Why can interest costs not continue to be capitalized after the self-construction period is completed?

Both projects were finished on December 31, 2013 and were ready for occupancy immediately. The Hazel building will have an estimated useful life of 30 years while the Cinnamon building will have an expected useful life of 40 years. Neither value will have a residual value. The Company uses the straight-line method for depreciation.

Required:

a. How much interest cost can be capitalized on Building Cinnamon?

b. What will be the annual depreciation expense for each of the two buildings?

c. ASPE allows interest capitalization while IFRS recommends capitalization of interest on construction-specific loans. Ignoring the complexities of how to determine how much interest to capitalize, which treatment of interest costs is conceptually more correct? Explain your conclusion.

d. Why can interest costs not continue to be capitalized after the self-construction period is completed?

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

41

Which factor will affect the estimated useful life of property, plant or equipment?

A)Legal life of the asset.

B)Technological obsolescence.

C)Residual value.

D)Salvage value.

A)Legal life of the asset.

B)Technological obsolescence.

C)Residual value.

D)Salvage value.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

42

What is the meaning of "straight-line method"?

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

43

What is the meaning of "useful life"?

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed through depreciation.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed through depreciation.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

44

What is the meaning of "value in use"?

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The discounted value of cash flows expected from using an asset for its intended purpose.

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The discounted value of cash flows expected from using an asset for its intended purpose.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

45

What factor will not affect the estimated useful life of property, plant or equipment?

A)Legal life of the asset.

B)Technological obsolescence.

C)Competitive pressures.

D)Productive capacity.

A)Legal life of the asset.

B)Technological obsolescence.

C)Competitive pressures.

D)Productive capacity.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

46

What is the meaning of "depreciation"?

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

47

What is the meaning of "depreciation"?

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

48

What is the meaning of "entry value"?

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

49

Seall-Test Ltd. owns a machine that it purchased on Jan 1, 2010 for $600,000. The machine had an estimated useful life of 10 years and an estimated residual value of $100,000. The company uses the declining balance method with a rate of 20%. The machine was sold on December 31, 2012 for $140,000. What was the depreciation expense for 2011?

A)$50,000

B)$60,000

C)$96,000

D)$120,000

A)$50,000

B)$60,000

C)$96,000

D)$120,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

50

What is the meaning of "exit value"?

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

51

What is the meaning of "declining balance method"?

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

52

What is the meaning of "depreciable amount"?

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed through depreciation.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed through depreciation.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

53

Hotel-R-Us owns a machine that it purchased on Jan 1, 2010 for $600,000. The machine had an estimated useful life of 5 years and an estimated residual value of $100,000. The company uses the declining balance method with a rate of 20%. The machine was sold on December 31, 2012 for $140,000. What was the accumulated depreciation at December 31, 2012?

A)$292,800

B)$180,000

C)$150,000

D)$76,800

A)$292,800

B)$180,000

C)$150,000

D)$76,800

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

54

What is the meaning of "replacement cost"?

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

55

What is the meaning of "historical cost"?

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

56

What is the meaning of "net realizable value"?

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

57

What is the meaning of "units-of-production method"?

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

A)The systematic allocation of an asset's depreciable amount allocated in proportion to the productive capacity used.

B)The systematic allocation of an asset's depreciable amount allocated evenly over the asset's estimated useful life.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The systematic allocation of an asset's depreciable amount whereby a period's depreciation equals the asset's net carrying amount multiplied by a fixed percentage.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

58

What issue does not relate to the subsequent measurement of property, plant and equipment?

A)Which model to use to record depreciation.

B)How impairment should be recorded.

C)How to classify the expenditure.

D)Whether to use the fair value model.

A)Which model to use to record depreciation.

B)How impairment should be recorded.

C)How to classify the expenditure.

D)Whether to use the fair value model.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

59

What is the meaning of "current value"?

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

A)The cost required to replace the productive capacity of an asset.

B)The value of an asset in an input market or output market on the date of measurement.

C)The value expected from the sale of an asset, net of any costs of disposal.

D)The actual cost of an asset at the time it was purchased.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

60

What is the meaning of "residual value"?

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed through depreciation.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

A)The estimated amount that an entity would currently obtain from disposal of the asset, after deducting disposal costs, for an asset of similar age and condition expected at the end of its useful life.

B)The total amount to be expensed through depreciation.

C)The systematic allocation of an asset's depreciable amount over its estimated useful life.

D)The estimated period of time over which an asset is expected to be available for use by an entity.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

61

Base-Forward owns a machine that it purchased on Jan 1, 2010 for $600,000. The machine had an estimated useful life of 5 years and an estimated residual value of $100,000. The company uses the declining balance method with a rate of 20%. The machine was sold on December 31, 2012 for $140,000. What was the depreciation expense for 2012?

A)$292,800

B)$76,800

C)$60,000

D)$50,000

A)$292,800

B)$76,800

C)$60,000

D)$50,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

62

Seneca Valley owns a machine that it purchased on Jan 1, 2010 for $600,000. The machine had an estimated useful life of 5 years and an estimated residual value of $100,000. The company uses the declining balance method with a rate of 40%. The machine was sold on December 31, 2012 for $140,000. What was the depreciation expense for 2010?

A)$100,000

B)$120,000

C)$200,000

D)$240,000

A)$100,000

B)$120,000

C)$200,000

D)$240,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

63

CeeMore owns a machine that it purchased on Jan 1, 2010 for $400,000. The machine had an estimated useful life of 10 years and a production capacity of 80,000 units and was expected to have no residual value. The company uses the units-of-production method to record depreciation. The machine produced 15,000 units in 2010, 18,000 units in 2011 and 25,000 units in 2012. The machine was sold on December 31, 2012 for $350,000. What was the accumulated depreciation at the end of 2011?

A)$75,000

B)$80,000

C)$90,000

D)$165,000

A)$75,000

B)$80,000

C)$90,000

D)$165,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

64

Seneca Valley owns a machine that it purchased on Jan 1, 2010 for $600,000. The machine had an estimated useful life of 10 years and an estimated residual value of $100,000. The company uses the double-declining balance method. The machine was sold on December 31, 2012 for $140,000. What is the depreciation rate for 2010?

A)10%

B)20%

C)40%

D)Any of the above can be used

A)10%

B)20%

C)40%

D)Any of the above can be used

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

65

Historic Pieces Inc. purchased equipment on January 1, 2012 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Assuming the company uses straight-line depreciation, what is the depreciation expense for 2012?

A)$27,500

B)$50,000

C)$55,000

D)$60,000

A)$27,500

B)$50,000

C)$55,000

D)$60,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

66

Oregona Ltd. owns a machine that it purchased on Jan 1, 2010 for $750,000. The machine had an estimated useful life of 5 years and an estimated residual value of $50,000. The company uses straight-line depreciation and records monthly depreciation. The machine was sold on December 31, 2013 for $200,000. What is the accumulated depreciation at December 31, 2013?

A)$600,000

B)$560,000

C)$150,000

D)$140,000

A)$600,000

B)$560,000

C)$150,000

D)$140,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

67

Centennial owns a machine that it purchased on Jan 1, 2010 for $400,000. The machine had an estimated useful life of 10 years with a production capacity for 80,000 units and was expected to have no residual value. The company uses the units-of-production method to record depreciation. The machine produced 15,000 units in 2010, 18,000 units in 2011 and 25,000 units in 2012. The machine was sold on December 30, 2012 for $350,000. What was the accumulated depreciation at December 31, 2010?

A)$39,000

B)$40,000

C)$75,000

D)$90,000

A)$39,000

B)$40,000

C)$75,000

D)$90,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

68

Ontario Ltd. owns a machine that it purchased on Jan 1, 2010 for $750,000. The machine had an estimated useful life of 5 years and an estimated residual value of $50,000. The company uses straight-line depreciation and records monthly depreciation. The machine was sold on December 31, 2013 for $200,000. What was the annual depreciation expense?

A)$10,000

B)$140,000

C)$150,000

D)$560,000

A)$10,000

B)$140,000

C)$150,000

D)$560,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

69

Fantasy Limited purchased equipment on January 1, 2009 for $275,000. The asset's useful life was estimated at 5 years or 10,000 units of output, with no residual value. The company has a December 31 year end. Additional Information

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?

A)$25.00

B)$27.50

C)$52,500

D)$57,750

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?A)$25.00

B)$27.50

C)$52,500

D)$57,750

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

70

Castle Rock owns a machine that it purchased on Jan 1, 2010 for $400,000. The machine had an estimated useful life of 10 years with a production capacity for 80,000 units and was expected to have no residual value. The company uses the units-of-production method to record depreciation. The machine produced 15,000 units in 2010, 18,000 units in 2011 and 25,000 units in 2012. The machine was sold on December 31, 2012 for $350,000. What was the depreciation expense for 2012?

A)$39,000

B)$40,000

C)$90,000

D)$125,000

A)$39,000

B)$40,000

C)$90,000

D)$125,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

71

Plastic Moulds purchased equipment on January 1, 2009 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Additional information: Assuming the company uses the units-of-production depreciation method, what is the depreciation rate per unit for 2009?

A)$25.00

B)$27.50

C)$57,750

D)$52,500

Assuming the company uses the units-of-production depreciation method, what is the depreciation rate per unit for 2009?A)$25.00

B)$27.50

C)$57,750

D)$52,500

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

72

Bountiful Limited purchased equipment on January 1, 2009 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Assuming the company uses straight-line depreciation, what is the net book value of the asset on December 31, 2012?

A)$125,000

B)$75,000

C)$55,000

D)$50,000

A)$125,000

B)$75,000

C)$55,000

D)$50,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

73

Easter Corp. owns a machine that it purchased on Jan 1, 2010 for $600,000. The machine had an estimated useful life of 10 years and an estimated residual value of $100,000. The company uses the declining balance method with a rate of 20%. The machine was sold on December 31, 2012 for $140,000. What was the accumulated depreciation at December 31, 2011?

A)$100,000

B)$120,000

C)$180,000

D)$216,000

A)$100,000

B)$120,000

C)$180,000

D)$216,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

74

Billu Limited purchased equipment on January 1, 2009 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Additional information: Assuming the company uses the units-of-production depreciation method, calculate the depreciation expense for 2012.

A)$25.00

B)$57,500

C)$63,250

D)$202,500

Assuming the company uses the units-of-production depreciation method, calculate the depreciation expense for 2012.A)$25.00

B)$57,500

C)$63,250

D)$202,500

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

75

Seally Corp. owns a machine that it purchased on Jan 1, 2010 for $600,000. The machine had an estimated useful life of 10 years and an estimated residual value of $100,000. The company uses the declining balance method with a rate of 20%. The machine was sold on December 31, 2012 for $140,000. What was the depreciation expense for 2011?

A)$50,000

B)$60,000

C)$80,000

D)$96,000

A)$50,000

B)$60,000

C)$80,000

D)$96,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

76

Ceila Manufacturing purchased equipment on January 1, 2012 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Assuming the company uses the double-declining-balance depreciation method, what is the depreciation expense for 2012?

A)$50,000

B)$55,000

C)$100,000

D)$110,000

A)$50,000

B)$55,000

C)$100,000

D)$110,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

77

Fantasmic Moulds purchased equipment on January 1, 2009 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Additional Information

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?

A)$25.00

B)$27.50

C)$52,500

D)$57,750

Assuming the company uses the units-of-production depreciation method, what is the depreciation expense for 2009?A)$25.00

B)$27.50

C)$52,500

D)$57,750

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

78

Francisco owns a machine that it purchased on July 1, 2010 for $600,000. The machine had an estimated useful life of 8 years and an estimated residual value of $10,000. The company uses straight-line depreciation and records monthly depreciation. The machine was sold on December 31, 2015 for $350,000. What was the depreciation expense for 2010?

A)$30,729

B)$36,875

C)$73,750

D)$75,000

A)$30,729

B)$36,875

C)$73,750

D)$75,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

79

Scandsia Ltd. owns a machine that it purchased on Jan 1, 2010 for $750,000. The machine had an estimated useful life of 5 years and an estimated residual value of $50,000. The company uses straight-line depreciation and records monthly depreciation. The machine was sold on December 31, 2013 for $200,000. What is the carrying value (net book value)at the date of sale?

A)$10,000

B)$150,000

C)$190,000

D)$560,000

A)$10,000

B)$150,000

C)$190,000

D)$560,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

80

FeelGood Corp. purchased equipment on January 1, 2011 for $275,000. It was estimated that the equipment would have a residual value of $25,000 at the end of its useful life. The asset's useful life was estimated at 5 years or 10,000 units of output. The company has a December 31 year end. Assuming the double-declining-balance depreciation method is used, what is the net book value (carrying value)of the asset on December 31, 2012?

A)$66,000

B)$99,000

C)$110,000

D)$165,000

A)$66,000

B)$99,000

C)$110,000

D)$165,000

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 127 flashcards in this deck.