Deck 11: Optimal Portfolio Choice and the Capital Asset Pricing Model

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

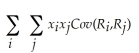

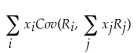

Which of the following equations is INCORRECT?

A)xi =![<strong>Which of the following equations is INCORRECT?</strong> A)x<sub>i</sub> = B)R<sub>p</sub> = Σ<sub>i</sub> x<sub>i</sub>R<sub>i</sub> C)R<sub>p</sub> = x<sub>1</sub>R<sub>1</sub> + x<sub>2</sub>R<sub>2</sub> + ... + x<sub>n</sub>R<sub>n</sub> D)E[R<sub>p</sub>] = E[Σ<sub>i</sub> x<sub>i</sub>R<sub>i</sub>] <div style=padding-top: 35px>](https://storage.examlex.com/TB2790/11ea7ff7_a543_6b17_846e_2b10e1620c25_TB2790_11.jpg)

B)Rp = Σi xiRi

C)Rp = x1R1 + x2R2 + ... + xnRn

D)E[Rp] = E[Σi xiRi]

A)xi =

B)Rp = Σi xiRi

C)Rp = x1R1 + x2R2 + ... + xnRn

D)E[Rp] = E[Σi xiRi]

Question

Question

Question

Question

Question

Question

Question

Question

Question

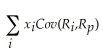

Which of the following equations is INCORRECT?

A)Cov(Ri,Rj)=![<strong>Which of the following equations is INCORRECT?</strong> A)Cov(R<sub>i</sub>,R<sub>j</sub>)= Σ(R<sub>i</sub> - R<sub>i</sub>)(R<sub>j</sub> - R<sub>j</sub>) B)Var(R<sub>p</sub>)= x<sub>1</sub><sup>2</sup><sup>Var</sup>(R<sub>1</sub>)+ x<sub>2</sub><sup>2</sup><sup>Var</sup>(R<sub>2</sub>)+ 2X<sub>1</sub>X<sub>2</sub>Cov(R<sub>1</sub>,R<sub>2</sub>) C)Corr(R<sub>i</sub>,R<sub>j</sub>)= D)Cov(R<sub>i</sub>,R<sub>j</sub>)= E[(R<sub>i</sub> - E[R<sub>i</sub>])(R<sub>j</sub> - E[R<sub>j</sub>])] <div style=padding-top: 35px>](https://storage.examlex.com/TB2790/11ea7ff7_a544_a398_846e_73d450525eb0_TB2790_11.jpg) Σ(Ri - Ri)(Rj - Rj)

Σ(Ri - Ri)(Rj - Rj)

B)Var(Rp)= x12Var(R1)+ x22Var(R2)+ 2X1X2Cov(R1,R2)

C)Corr(Ri,Rj)=![<strong>Which of the following equations is INCORRECT?</strong> A)Cov(R<sub>i</sub>,R<sub>j</sub>)= Σ(R<sub>i</sub> - R<sub>i</sub>)(R<sub>j</sub> - R<sub>j</sub>) B)Var(R<sub>p</sub>)= x<sub>1</sub><sup>2</sup><sup>Var</sup>(R<sub>1</sub>)+ x<sub>2</sub><sup>2</sup><sup>Var</sup>(R<sub>2</sub>)+ 2X<sub>1</sub>X<sub>2</sub>Cov(R<sub>1</sub>,R<sub>2</sub>) C)Corr(R<sub>i</sub>,R<sub>j</sub>)= D)Cov(R<sub>i</sub>,R<sub>j</sub>)= E[(R<sub>i</sub> - E[R<sub>i</sub>])(R<sub>j</sub> - E[R<sub>j</sub>])] <div style=padding-top: 35px>](https://storage.examlex.com/TB2790/11ea7ff7_a544_a399_846e_470339a6879a_TB2790_11.jpg)

D)Cov(Ri,Rj)= E[(Ri - E[Ri])(Rj - E[Rj])]

A)Cov(Ri,Rj)=

Σ(Ri - Ri)(Rj - Rj)B)Var(Rp)= x12Var(R1)+ x22Var(R2)+ 2X1X2Cov(R1,R2)

C)Corr(Ri,Rj)=

D)Cov(Ri,Rj)= E[(Ri - E[Ri])(Rj - E[Rj])]

Question

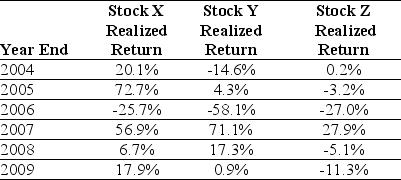

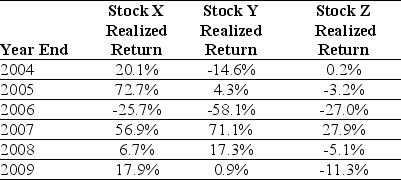

Use the table for the question(s)below.

Consider the following returns:

The covariance between Stock X's and Stock Y's returns is closest to:

A)0.10

B)0.29

C)0.12

D)0.69

Consider the following returns:

The covariance between Stock X's and Stock Y's returns is closest to:

A)0.10

B)0.29

C)0.12

D)0.69

Question

Question

Question

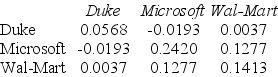

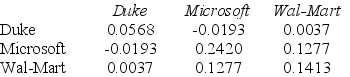

Use the table for the question(s)below.

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 20 stocks. If the average volatility of these stocks is 35% and the average correlation between the stocks is .4, then the volatility of this equally weighted portfolio is closest to:

A).17

B).41

C).14

D).37

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 20 stocks. If the average volatility of these stocks is 35% and the average correlation between the stocks is .4, then the volatility of this equally weighted portfolio is closest to:

A).17

B).41

C).14

D).37

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following formulas is INCORRECT?

A)Variance of an equally Weighted Portfolio = (1 - )(Average Variance of Individual Stocks)+

)(Average Variance of Individual Stocks)+

(Average covariance between the stocks)

(Average covariance between the stocks)

B)Variance of a portfolio =

C)Variance of a portfolio =

D)Variance of a portfolio =

Consider the following covariances between securities:

Which of the following formulas is INCORRECT?

A)Variance of an equally Weighted Portfolio = (1 -

)(Average Variance of Individual Stocks)+ (Average covariance between the stocks)B)Variance of a portfolio =

C)Variance of a portfolio =

D)Variance of a portfolio =

Question

Use the table for the question(s)below.

Consider the following returns:

The Volatility on Stock Z's returns is closest to:

A)3%

B)13%

C)16%

D)18%

Consider the following returns:

The Volatility on Stock Z's returns is closest to:

A)3%

B)13%

C)16%

D)18%

Question

Use the table for the question(s)below.

Consider the following returns:

The Correlation between Stock X's and Stock Y's returns is closest to:

A)0.58

B)0.29

C)0.69

D)0.10

Consider the following returns:

The Correlation between Stock X's and Stock Y's returns is closest to:

A)0.58

B)0.29

C)0.69

D)0.10

Question

Use the table for the question(s)below.

Consider the following returns:

The Volatility on Stock X's returns is closest to:

A)35%

B)10%

C)13%

D)42%

Consider the following returns:

The Volatility on Stock X's returns is closest to:

A)35%

B)10%

C)13%

D)42%

Question

Use the table for the question(s)below.

Consider the following returns:

The Correlation between Stock X's and Stock Z's returns is closest to:

A)0.71

B)0.60

C)0.62

D)0.05

Consider the following returns:

The Correlation between Stock X's and Stock Z's returns is closest to:

A)0.71

B)0.60

C)0.62

D)0.05

Question

Use the table for the question(s)below.

Consider the following returns:

Calculate the variance on a portfolio that is made up of equal investments in Stock Y and Stock Z stock .

Consider the following returns:

Calculate the variance on a portfolio that is made up of equal investments in Stock Y and Stock Z stock .

Question

Use the table for the question(s)below.

Consider the following returns:

The Volatility on Stock Y's returns is closest to:

A)35%

B)31%

C)42%

D)18%

Consider the following returns:

The Volatility on Stock Y's returns is closest to:

A)35%

B)31%

C)42%

D)18%

Question

Use the table for the question(s)below.

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Z stock is closest to:

A)0.62

B)0.05

C)0.12

D)0.06

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Z stock is closest to:

A)0.62

B)0.05

C)0.12

D)0.06

Question

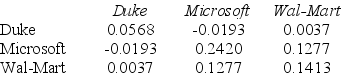

Use the table for the question(s)below.

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Microsoft and a $4000 investment in Wal-Mart stock is closest to:

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Microsoft and a $4000 investment in Wal-Mart stock is closest to:

Question

Use the table for the question(s)below.

Consider the following returns:

Calculate the covariance between Stock Y's and Stock Z's returns .

Consider the following returns:

Calculate the covariance between Stock Y's and Stock Z's returns .

Question

Use the table for the question(s)below.

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Y stock is closest to:

A)0.12

B)0.10

C)0.69

D)0.29

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Y stock is closest to:

A)0.12

B)0.10

C)0.69

D)0.29

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains five stocks. If the average volatility of these stocks is 40% and the average correlation between the stocks is .5, then the volatility of this equally weighted portfolio is closest to:

A).17

B)..03

C).41

D).19

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains five stocks. If the average volatility of these stocks is 40% and the average correlation between the stocks is .5, then the volatility of this equally weighted portfolio is closest to:

A).17

B)..03

C).41

D).19

Question

Use the table for the question(s)below.

Consider the following returns:

The covariance between Stock X's and Stock Z's returns is closest to:

A)0.05

B)0.06

C)0.10

D)0.71

Consider the following returns:

The covariance between Stock X's and Stock Z's returns is closest to:

A)0.05

B)0.06

C)0.10

D)0.71

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The expected return of a portfolio is equal to the weighted average expected return, but the volatility of a portfolio is less than the weighted average volatility.

B)Each security contributes to the volatility of the portfolio according to its volatility, scaled by its covariance with the portfolio, which adjusts for the fraction of the total risk that is common to the portfolio.

C)Nearly half of the volatility of individual stocks can be eliminated in a large portfolio as a result of diversification.

D)The overall variability of the portfolio depends on the total co-movement of the stocks within it.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The expected return of a portfolio is equal to the weighted average expected return, but the volatility of a portfolio is less than the weighted average volatility.

B)Each security contributes to the volatility of the portfolio according to its volatility, scaled by its covariance with the portfolio, which adjusts for the fraction of the total risk that is common to the portfolio.

C)Nearly half of the volatility of individual stocks can be eliminated in a large portfolio as a result of diversification.

D)The overall variability of the portfolio depends on the total co-movement of the stocks within it.

Question

Use the table for the question(s)below.

Consider the following returns:

Calculate the correlation between Stock Y's and Stock Z's returns .

Consider the following returns:

Calculate the correlation between Stock Y's and Stock Z's returns .

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Duke Energy and a $4000 investment in Wal-Mart stock is closest to:

A).050

B).045

C).051

D)-0.020

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Duke Energy and a $4000 investment in Wal-Mart stock is closest to:

A).050

B).045

C).051

D)-0.020

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The volatility declines as the number of stocks in a portfolio grows.

B)An equally weighted portfolio is a portfolio in which the same amount is invested in each stock.

C)As the number of stocks in a portfolio grows large, the variance of the portfolio is determined primarily by the average covariance among the stocks.

D)When combining stocks into a portfolio that puts positive weight on each stock, unless all of the stocks are uncorrelated with the portfolio, the risk of the portfolio will be lower than the weighted average volatility of the individual stocks.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The volatility declines as the number of stocks in a portfolio grows.

B)An equally weighted portfolio is a portfolio in which the same amount is invested in each stock.

C)As the number of stocks in a portfolio grows large, the variance of the portfolio is determined primarily by the average covariance among the stocks.

D)When combining stocks into a portfolio that puts positive weight on each stock, unless all of the stocks are uncorrelated with the portfolio, the risk of the portfolio will be lower than the weighted average volatility of the individual stocks.

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

The variance on a portfolio that is made up of equal investments in Duke Energy and Microsoft stock is closest to:

A).065

B)0.090

C).149

D)-0.020

Consider the following covariances between securities:

The variance on a portfolio that is made up of equal investments in Duke Energy and Microsoft stock is closest to:

A).065

B)0.090

C).149

D)-0.020

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The variance of a portfolio is equal to the weighted average correlation of each stock within the portfolio.

B)The variance of a portfolio is equal to the sum of the covariances of the returns of all pairs of stocks in the portfolio multiplied by each of their portfolio weights.

C)The variance of a portfolio is equal to the weighted average covariances of each stock within the portfolio.

D)The volatility declines as the number of stocks in a portfolio grows.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The variance of a portfolio is equal to the weighted average correlation of each stock within the portfolio.

B)The variance of a portfolio is equal to the sum of the covariances of the returns of all pairs of stocks in the portfolio multiplied by each of their portfolio weights.

C)The variance of a portfolio is equal to the weighted average covariances of each stock within the portfolio.

D)The volatility declines as the number of stocks in a portfolio grows.

Question

Suppose you have $10,000 in cash to invest. You decide to sell short $5,000 worth of Kinston stock and invest the proceeds from your short sale, plus your $10,000 into one-year U.S. treasury bills earning 5%. At the end of the year, you decide to liquidate your portfolio. Kinston Industries has the following realized returns:  The return on your portfolio is closest to:

The return on your portfolio is closest to:

A)-0.5%

B)13.5%

C)-2.5%

D)14.5%

The return on your portfolio is closest to:A)-0.5%

B)13.5%

C)-2.5%

D)14.5%

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is long those stocks that have negative portfolio weights.

B)The efficient portfolios are those portfolios offering the highest possible expected return for a given level of volatility.

C)When two stocks are perfectly negatively correlated, it becomes possible to hold a portfolio that bears absolutely no risk.

D)The lower the correlation of the securities in a portfolio the lower the volatility we can obtain.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is long those stocks that have negative portfolio weights.

B)The efficient portfolios are those portfolios offering the highest possible expected return for a given level of volatility.

C)When two stocks are perfectly negatively correlated, it becomes possible to hold a portfolio that bears absolutely no risk.

D)The lower the correlation of the securities in a portfolio the lower the volatility we can obtain.

Question

Question

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

Consider a portfolio consisting of only Duke Energy and Microsoft. The percentage of your investment (portfolio weight)that you would place in Duke Energy stock to achieve a risk-free investment would be closest to:

A)15%

B)40%

C)23%

D)10%

Consider the following expected returns, volatilities, and correlations:

Consider a portfolio consisting of only Duke Energy and Microsoft. The percentage of your investment (portfolio weight)that you would place in Duke Energy stock to achieve a risk-free investment would be closest to:

A)15%

B)40%

C)23%

D)10%

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)When stocks are perfectly positively correlated, the set of portfolios is identified graphically by a straight line between them.

B)An investor seeking high returns and low volatility should only invest in an efficient portfolio.

C)When the correlation between securities is less than 1, the volatility of the portfolio is reduced due to diversification.

D)Efficient portfolios can be easily ranked, because investors will choose from among them those with the highest expected returns.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)When stocks are perfectly positively correlated, the set of portfolios is identified graphically by a straight line between them.

B)An investor seeking high returns and low volatility should only invest in an efficient portfolio.

C)When the correlation between securities is less than 1, the volatility of the portfolio is reduced due to diversification.

D)Efficient portfolios can be easily ranked, because investors will choose from among them those with the highest expected returns.

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)A short sale is a transaction in which you buy a stock that you do not own and then agree to sell that stock back in the future.

B)The efficient portfolios are those portfolios offering the lowest possible level of volatility for a given level of expected return.

C)A positive investment in a security can be referred to as a long position in the security.

D)It is possible to invest a negative amount in a stock or security call a short position.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)A short sale is a transaction in which you buy a stock that you do not own and then agree to sell that stock back in the future.

B)The efficient portfolios are those portfolios offering the lowest possible level of volatility for a given level of expected return.

C)A positive investment in a security can be referred to as a long position in the security.

D)It is possible to invest a negative amount in a stock or security call a short position.

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is an efficient portfolio whenever it is possible to find another portfolio that is better in terms of both expected return and volatility.

B)We can rule out inefficient portfolios because they represent inferior investment choices.

C)The volatility of the portfolio will differ, depending on the correlation between the securities in the portfolio.

D)Correlation has no effect on the expected return on a portfolio.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is an efficient portfolio whenever it is possible to find another portfolio that is better in terms of both expected return and volatility.

B)We can rule out inefficient portfolios because they represent inferior investment choices.

C)The volatility of the portfolio will differ, depending on the correlation between the securities in the portfolio.

D)Correlation has no effect on the expected return on a portfolio.

Question

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)Graphically, the efficient portfolios are those on the northeast edge of the set of possible portfolios, an area which we call the efficient frontier.

B)To arrive at the best possible set of risk and return opportunities, we should keep adding stocks until all investment opportunities are represented.

C)We say a portfolio is short those stocks that have negative portfolio weights.

D)Adding new investment opportunities allows for greater diversification and improves the efficient frontier.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)Graphically, the efficient portfolios are those on the northeast edge of the set of possible portfolios, an area which we call the efficient frontier.

B)To arrive at the best possible set of risk and return opportunities, we should keep adding stocks until all investment opportunities are represented.

C)We say a portfolio is short those stocks that have negative portfolio weights.

D)Adding new investment opportunities allows for greater diversification and improves the efficient frontier.

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 100 stocks. If the average volatility of these stocks is 50% and the average correlation between the stocks is .7, then the volatility of this equally weighted portfolio is closest to:

A).72

B).63

C).40

D).50

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 100 stocks. If the average volatility of these stocks is 50% and the average correlation between the stocks is .7, then the volatility of this equally weighted portfolio is closest to:

A).72

B).63

C).40

D).50

Question

Question

Question

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A)8%

B)9%

C)11%

D)6%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A)8%

B)9%

C)11%

D)6%

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

What is the variance on a portfolio that has $2000 invested in Duke Energy, $3000 invested in Microsoft, and $5000 invested in Wal-Mart stock?

Consider the following covariances between securities:

What is the variance on a portfolio that has $2000 invested in Duke Energy, $3000 invested in Microsoft, and $5000 invested in Wal-Mart stock?

Question

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A)9%

B)14%

C)11%

D)12%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A)9%

B)14%

C)11%

D)12%

Question

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is consists of a long position of $10000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A)21%

B)12%

C)27%

D)18%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is consists of a long position of $10000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A)21%

B)12%

C)27%

D)18%

Question

Question

Use the table for the question(s)below.

Consider the following covariances between securities:

What is the variance on a portfolio that has $3000 invested in Duke Energy, $4000 invested in Microsoft, and $3000 invested in Wal-Mart stock?

Consider the following covariances between securities:

What is the variance on a portfolio that has $3000 invested in Duke Energy, $4000 invested in Microsoft, and $3000 invested in Wal-Mart stock?

Question

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A)28%

B)29%

C)24%

D)23%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A)28%

B)29%

C)24%

D)23%

Question

Question

Use the following information to answer the question(s)below.

The volatility of the market portfolio is 10%, the expected return on the market is 12%, and the risk-free rate of interest is 4%.

The volatility of the market portfolio is 10%, the expected return on the market is 12%, and the risk-free rate of interest is 4%.

The Sharpe Ratio for the market portfolio is closest to:

A)0.40

B)0.48

C)0.56

D)0.80

The volatility of the market portfolio is 10%, the expected return on the market is 12%, and the risk-free rate of interest is 4%.The Sharpe Ratio for the market portfolio is closest to:

A)0.40

B)0.48

C)0.56

D)0.80

Question

Question

Question

Question

Use the information for the question(s)below.

You are presently invested in the Luther Fund, a broad based mutual fund that invest in stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of -.20 with the Luther Fund.

The beta of the precious metals fund with the Luther Fund is closest to:

is closest to:

A)-0.3

B)-0.6

C)0.3

D)0.6

You are presently invested in the Luther Fund, a broad based mutual fund that invest in stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of -.20 with the Luther Fund.

The beta of the precious metals fund with the Luther Fund

is closest to:A)-0.3

B)-0.6

C)0.3

D)0.6

Question

Question

Question

Question

Question

Question

Question

Which of the following statements is FALSE?

A)A portfolio is efficient if it has the highest possible Sharpe ratio; that is it is efficient if it provides the largest increase in expected return possible for a given increase in volatility.

B)The required return for an investment is equal to a risk premium that is equal to the risk premium of the investor's current portfolio scaled by![<strong>Which of the following statements is FALSE?</strong> A)A portfolio is efficient if it has the highest possible Sharpe ratio; that is it is efficient if it provides the largest increase in expected return possible for a given increase in volatility. B)The required return for an investment is equal to a risk premium that is equal to the risk premium of the investor's current portfolio scaled by . C)Increasing the investment in investment I will increase the Sharpe ratio of portfolio P if its expected return E[R<sub>i</sub>] exceeds the required return r<sub>i</sub>, which is given by r<sub>i</sub> = r<sub>f</sub> + × (E[R<sub>p</sub>] - r<sub>f</sub>). D)If a security i's expected return is less than the required return r<sub>i</sub>, we should reduce our holding of security i. <div style=padding-top: 35px>](https://storage.examlex.com/TB2790/11ea7ff7_a548_c266_846e_cd8952804115_TB2790_11.jpg) .

.

C)Increasing the investment in investment I will increase the Sharpe ratio of portfolio P if its expected return E[Ri] exceeds the required return ri, which is given by ri = rf +![<strong>Which of the following statements is FALSE?</strong> A)A portfolio is efficient if it has the highest possible Sharpe ratio; that is it is efficient if it provides the largest increase in expected return possible for a given increase in volatility. B)The required return for an investment is equal to a risk premium that is equal to the risk premium of the investor's current portfolio scaled by . C)Increasing the investment in investment I will increase the Sharpe ratio of portfolio P if its expected return E[R<sub>i</sub>] exceeds the required return r<sub>i</sub>, which is given by r<sub>i</sub> = r<sub>f</sub> + × (E[R<sub>p</sub>] - r<sub>f</sub>). D)If a security i's expected return is less than the required return r<sub>i</sub>, we should reduce our holding of security i. <div style=padding-top: 35px>](https://storage.examlex.com/TB2790/11ea7ff7_a548_e977_846e_cf7b0f78618b_TB2790_11.jpg) × (E[Rp] - rf).

× (E[Rp] - rf).

D)If a security i's expected return is less than the required return ri, we should reduce our holding of security i.

A)A portfolio is efficient if it has the highest possible Sharpe ratio; that is it is efficient if it provides the largest increase in expected return possible for a given increase in volatility.

B)The required return for an investment is equal to a risk premium that is equal to the risk premium of the investor's current portfolio scaled by

.C)Increasing the investment in investment I will increase the Sharpe ratio of portfolio P if its expected return E[Ri] exceeds the required return ri, which is given by ri = rf +

× (E[Rp] - rf).D)If a security i's expected return is less than the required return ri, we should reduce our holding of security i.

Question

Which of the following equations is INCORRECT?

A)E[Rxp] = rf + x(E[Rp] - rf)

B)E[Rxp] = (1 - x)rf + xE[Rp]

C)Sharpe ratio =![<strong>Which of the following equations is INCORRECT?</strong> A)E[R<sub>xp</sub>] = r<sub>f</sub> + x(E[R<sub>p</sub>] - r<sub>f</sub>) B)E[R<sub>xp</sub>] = (1 - x)r<sub>f</sub> + xE[R<sub>p</sub>] C)Sharpe ratio = D)SD( R<sub>xp</sub>)= xSD(R<sub>p</sub>) <div style=padding-top: 35px>](https://storage.examlex.com/TB2790/11ea7ff7_a548_7445_846e_e57dd86135f9_TB2790_11.jpg)

D)SD( Rxp)= xSD(Rp)

A)E[Rxp] = rf + x(E[Rp] - rf)

B)E[Rxp] = (1 - x)rf + xE[Rp]

C)Sharpe ratio =

D)SD( Rxp)= xSD(Rp)

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/133

Play

Full screen (f)

Deck 11: Optimal Portfolio Choice and the Capital Asset Pricing Model

1

Which of the following statements is FALSE?

A)Without trading, the portfolio weights will decrease for the stocks in the portfolio whose returns are above the overall portfolio return.

B)The expected return of a portfolio is simply the weighted average of the expected returns of the investments within the portfolio.

C)Portfolio weights add up to 1 so that they represent the way we have divided our money between the different individual investments in the portfolio.

D)A portfolio weight is the fraction of the total investment in the portfolio held in an individual investment in the portfolio.

A)Without trading, the portfolio weights will decrease for the stocks in the portfolio whose returns are above the overall portfolio return.

B)The expected return of a portfolio is simply the weighted average of the expected returns of the investments within the portfolio.

C)Portfolio weights add up to 1 so that they represent the way we have divided our money between the different individual investments in the portfolio.

D)A portfolio weight is the fraction of the total investment in the portfolio held in an individual investment in the portfolio.

Without trading, the portfolio weights will decrease for the stocks in the portfolio whose returns are above the overall portfolio return.

2

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The weight on Lowes in your portfolio after one year is closest to:

A)20.0%

B)34.8%

C)30.0%

D)36.0%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The weight on Lowes in your portfolio after one year is closest to:

A)20.0%

B)34.8%

C)30.0%

D)36.0%

34.8%

3

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The return on your portfolio over the year is:

A)0%

B)7.5%

C)3.5%

D)5.0%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The return on your portfolio over the year is:

A)0%

B)7.5%

C)3.5%

D)5.0%

3.5%

4

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

The weight on Abbott Labs in your portfolio is:

A)50%

B)40%

C)30%

D)20%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

The weight on Abbott Labs in your portfolio is:

A)50%

B)40%

C)30%

D)20%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

5

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The weight on Abbott Labs in your portfolio after one year is closest to:

A)-10.0%

B)43.5%

C)45.0%

D)50.0%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The weight on Abbott Labs in your portfolio after one year is closest to:

A)-10.0%

B)43.5%

C)45.0%

D)50.0%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statements is FALSE?

A)The covariance and correlation allow us to measure the co-movement of returns.

B)Correlation is the expected product of the deviations of two returns.

C)Because the prices of the stocks do not move identically, some of the risk is averaged out in a portfolio.

D)The amount of risk that is eliminated in a portfolio depends on the degree to which the stocks face common risks and their prices move together.

A)The covariance and correlation allow us to measure the co-movement of returns.

B)Correlation is the expected product of the deviations of two returns.

C)Because the prices of the stocks do not move identically, some of the risk is averaged out in a portfolio.

D)The amount of risk that is eliminated in a portfolio depends on the degree to which the stocks face common risks and their prices move together.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

7

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The value of your portfolio over the year is:

A)$21,000

B)$20,000

C)$20,700

D)$21,500

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The value of your portfolio over the year is:

A)$21,000

B)$20,000

C)$20,700

D)$21,500

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following equations is INCORRECT?

A)xi =

B)Rp = Σi xiRi

C)Rp = x1R1 + x2R2 + ... + xnRn

D)E[Rp] = E[Σi xiRi]

A)xi =

B)Rp = Σi xiRi

C)Rp = x1R1 + x2R2 + ... + xnRn

D)E[Rp] = E[Σi xiRi]

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

9

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose you invest $15,000 in Merck stock and $25,000 in Home Depot stock. You receive an actual return of -8% for Merck and 12% for Home Depot. What is the actual return on your portfolio?

A)4.50%

B)4.00%

C)10.00%

D)2.00%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose you invest $15,000 in Merck stock and $25,000 in Home Depot stock. You receive an actual return of -8% for Merck and 12% for Home Depot. What is the actual return on your portfolio?

A)4.50%

B)4.00%

C)10.00%

D)2.00%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements is FALSE?

A)If two stocks move in opposite directions, one will tend to be above average when to other is below average, and the covariance will be negative.

B)The correlation between two stocks has the same sign as their covariance, so it has a similar interpretation.

C)The covariance of a stock with itself is simply its variance.

D)The covariance allows us to gauge the strength of the relationship between stocks.

A)If two stocks move in opposite directions, one will tend to be above average when to other is below average, and the covariance will be negative.

B)The correlation between two stocks has the same sign as their covariance, so it has a similar interpretation.

C)The covariance of a stock with itself is simply its variance.

D)The covariance allows us to gauge the strength of the relationship between stocks.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is FALSE?

A)While the sign of the correlation is easy to interpret, its magnitude is not.

B)Independent risks are uncorrelated.

C)When the covariance equals 0, the returns are uncorrelated.

D)To find the risk of a portfolio, we need to know more than the risk and return of the component stocks; we need to know the degree to which the stocks' returns move together.

A)While the sign of the correlation is easy to interpret, its magnitude is not.

B)Independent risks are uncorrelated.

C)When the covariance equals 0, the returns are uncorrelated.

D)To find the risk of a portfolio, we need to know more than the risk and return of the component stocks; we need to know the degree to which the stocks' returns move together.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

12

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The weight on Ball Corporation in your portfolio after one year is closest to:

A)20.0%

B)12.5%

C)20.7%

D)21.7%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose over the next year Ball has a return of 12.5%, Lowes has a return of 20%, and Abbott Labs has a return of -10%. The weight on Ball Corporation in your portfolio after one year is closest to:

A)20.0%

B)12.5%

C)20.7%

D)21.7%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following statements is FALSE?

A)Dividing the covariance by the volatilities ensures that correlation is always between -1 and +1.

B)Volatility is the square root of variance.

C)The closer the correlation is to 0, the more the returns tend to move together as a result of common risk.

D)If two stocks move together, their returns will tend to be above or below average at the same time, and the covariance will be positive.

A)Dividing the covariance by the volatilities ensures that correlation is always between -1 and +1.

B)Volatility is the square root of variance.

C)The closer the correlation is to 0, the more the returns tend to move together as a result of common risk.

D)If two stocks move together, their returns will tend to be above or below average at the same time, and the covariance will be positive.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

14

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

The weight on Ball Corporation in your portfolio is:

A)50%

B)40%

C)20%

D)30%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

The weight on Ball Corporation in your portfolio is:

A)50%

B)40%

C)20%

D)30%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

15

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

The weight on Lowes in your portfolio is:

A)40%

B)20%

C)50%

D)30%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

The weight on Lowes in your portfolio is:

A)40%

B)20%

C)50%

D)30%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements is FALSE?

A)Stock returns will tend to move together if they are affect similarly by economic events.

B)Stocks in the same industry tend to have more highly correlated returns than stocks in different industries.

C)Almost all of the correlations between stocks are negative, illustrating the general tendency of stocks to move together.

D)With a positive amount invest in each stock, the more the stocks move together and the higher their covariance or correlation, the more variable the portfolio will be.

A)Stock returns will tend to move together if they are affect similarly by economic events.

B)Stocks in the same industry tend to have more highly correlated returns than stocks in different industries.

C)Almost all of the correlations between stocks are negative, illustrating the general tendency of stocks to move together.

D)With a positive amount invest in each stock, the more the stocks move together and the higher their covariance or correlation, the more variable the portfolio will be.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following equations is INCORRECT?

A)Cov(Ri,Rj)= Σ(Ri - Ri)(Rj - Rj)

B)Var(Rp)= x12Var(R1)+ x22Var(R2)+ 2X1X2Cov(R1,R2)

C)Corr(Ri,Rj)=

D)Cov(Ri,Rj)= E[(Ri - E[Ri])(Rj - E[Rj])]

A)Cov(Ri,Rj)=

Σ(Ri - Ri)(Rj - Rj)B)Var(Rp)= x12Var(R1)+ x22Var(R2)+ 2X1X2Cov(R1,R2)

C)Corr(Ri,Rj)=

D)Cov(Ri,Rj)= E[(Ri - E[Ri])(Rj - E[Rj])]

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

18

Use the table for the question(s)below.

Consider the following returns:

The covariance between Stock X's and Stock Y's returns is closest to:

A)0.10

B)0.29

C)0.12

D)0.69

Consider the following returns:

The covariance between Stock X's and Stock Y's returns is closest to:

A)0.10

B)0.29

C)0.12

D)0.69

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

19

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose you invest $15,000 in Merck stock and $25,000 in Home Depot stock. You expect a return of 16% for Merck and 12% for Home Depot. What is the expected return on your portfolio?

A)13.50%

B)14.00%

C)13.75%

D)14.50%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share, 200 shares of Lowes (LOW)at $30 per share, and 100 shares of Ball Corporation (BLL)at $40 per share.

Suppose you invest $15,000 in Merck stock and $25,000 in Home Depot stock. You expect a return of 16% for Merck and 12% for Home Depot. What is the expected return on your portfolio?

A)13.50%

B)14.00%

C)13.75%

D)14.50%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements is FALSE?

A)A stock's return is perfectly positively correlated with itself.

B)When the covariance equals 0, the stocks have no tendency to move either together or in opposition of one another.

C)The closer the correlation is to -1, the more the returns tend to move in opposite directions.

D)The variance of a portfolio depends only on the variance of the individual stocks.

A)A stock's return is perfectly positively correlated with itself.

B)When the covariance equals 0, the stocks have no tendency to move either together or in opposition of one another.

C)The closer the correlation is to -1, the more the returns tend to move in opposite directions.

D)The variance of a portfolio depends only on the variance of the individual stocks.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

21

Use the table for the question(s)below.

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 20 stocks. If the average volatility of these stocks is 35% and the average correlation between the stocks is .4, then the volatility of this equally weighted portfolio is closest to:

A).17

B).41

C).14

D).37

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 20 stocks. If the average volatility of these stocks is 35% and the average correlation between the stocks is .4, then the volatility of this equally weighted portfolio is closest to:

A).17

B).41

C).14

D).37

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

22

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following formulas is INCORRECT?

A)Variance of an equally Weighted Portfolio = (1 - )(Average Variance of Individual Stocks)+

(Average covariance between the stocks)

B)Variance of a portfolio =

C)Variance of a portfolio =

D)Variance of a portfolio =

Consider the following covariances between securities:

Which of the following formulas is INCORRECT?

A)Variance of an equally Weighted Portfolio = (1 -

)(Average Variance of Individual Stocks)+ (Average covariance between the stocks)B)Variance of a portfolio =

C)Variance of a portfolio =

D)Variance of a portfolio =

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

23

Use the table for the question(s)below.

Consider the following returns:

The Volatility on Stock Z's returns is closest to:

A)3%

B)13%

C)16%

D)18%

Consider the following returns:

The Volatility on Stock Z's returns is closest to:

A)3%

B)13%

C)16%

D)18%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

24

Use the table for the question(s)below.

Consider the following returns:

The Correlation between Stock X's and Stock Y's returns is closest to:

A)0.58

B)0.29

C)0.69

D)0.10

Consider the following returns:

The Correlation between Stock X's and Stock Y's returns is closest to:

A)0.58

B)0.29

C)0.69

D)0.10

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

25

Use the table for the question(s)below.

Consider the following returns:

The Volatility on Stock X's returns is closest to:

A)35%

B)10%

C)13%

D)42%

Consider the following returns:

The Volatility on Stock X's returns is closest to:

A)35%

B)10%

C)13%

D)42%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

26

Use the table for the question(s)below.

Consider the following returns:

The Correlation between Stock X's and Stock Z's returns is closest to:

A)0.71

B)0.60

C)0.62

D)0.05

Consider the following returns:

The Correlation between Stock X's and Stock Z's returns is closest to:

A)0.71

B)0.60

C)0.62

D)0.05

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

27

Use the table for the question(s)below.

Consider the following returns:

Calculate the variance on a portfolio that is made up of equal investments in Stock Y and Stock Z stock .

Consider the following returns:

Calculate the variance on a portfolio that is made up of equal investments in Stock Y and Stock Z stock .

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

28

Use the table for the question(s)below.

Consider the following returns:

The Volatility on Stock Y's returns is closest to:

A)35%

B)31%

C)42%

D)18%

Consider the following returns:

The Volatility on Stock Y's returns is closest to:

A)35%

B)31%

C)42%

D)18%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

29

Use the table for the question(s)below.

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Z stock is closest to:

A)0.62

B)0.05

C)0.12

D)0.06

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Z stock is closest to:

A)0.62

B)0.05

C)0.12

D)0.06

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

30

Use the table for the question(s)below.

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Microsoft and a $4000 investment in Wal-Mart stock is closest to:

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Microsoft and a $4000 investment in Wal-Mart stock is closest to:

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

31

Use the table for the question(s)below.

Consider the following returns:

Calculate the covariance between Stock Y's and Stock Z's returns .

Consider the following returns:

Calculate the covariance between Stock Y's and Stock Z's returns .

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

32

Use the table for the question(s)below.

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Y stock is closest to:

A)0.12

B)0.10

C)0.69

D)0.29

Consider the following returns:

The variance on a portfolio that is made up of equal investments in Stock X and Stock Y stock is closest to:

A)0.12

B)0.10

C)0.69

D)0.29

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

33

Use the table for the question(s)below.

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains five stocks. If the average volatility of these stocks is 40% and the average correlation between the stocks is .5, then the volatility of this equally weighted portfolio is closest to:

A).17

B)..03

C).41

D).19

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains five stocks. If the average volatility of these stocks is 40% and the average correlation between the stocks is .5, then the volatility of this equally weighted portfolio is closest to:

A).17

B)..03

C).41

D).19

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

34

Use the table for the question(s)below.

Consider the following returns:

The covariance between Stock X's and Stock Z's returns is closest to:

A)0.05

B)0.06

C)0.10

D)0.71

Consider the following returns:

The covariance between Stock X's and Stock Z's returns is closest to:

A)0.05

B)0.06

C)0.10

D)0.71

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

35

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The expected return of a portfolio is equal to the weighted average expected return, but the volatility of a portfolio is less than the weighted average volatility.

B)Each security contributes to the volatility of the portfolio according to its volatility, scaled by its covariance with the portfolio, which adjusts for the fraction of the total risk that is common to the portfolio.

C)Nearly half of the volatility of individual stocks can be eliminated in a large portfolio as a result of diversification.

D)The overall variability of the portfolio depends on the total co-movement of the stocks within it.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The expected return of a portfolio is equal to the weighted average expected return, but the volatility of a portfolio is less than the weighted average volatility.

B)Each security contributes to the volatility of the portfolio according to its volatility, scaled by its covariance with the portfolio, which adjusts for the fraction of the total risk that is common to the portfolio.

C)Nearly half of the volatility of individual stocks can be eliminated in a large portfolio as a result of diversification.

D)The overall variability of the portfolio depends on the total co-movement of the stocks within it.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

36

Use the table for the question(s)below.

Consider the following returns:

Calculate the correlation between Stock Y's and Stock Z's returns .

Consider the following returns:

Calculate the correlation between Stock Y's and Stock Z's returns .

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

37

Use the table for the question(s)below.

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Duke Energy and a $4000 investment in Wal-Mart stock is closest to:

A).050

B).045

C).051

D)-0.020

Consider the following covariances between securities:

The variance on a portfolio that is made up of a $6000 investments in Duke Energy and a $4000 investment in Wal-Mart stock is closest to:

A).050

B).045

C).051

D)-0.020

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

38

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The volatility declines as the number of stocks in a portfolio grows.

B)An equally weighted portfolio is a portfolio in which the same amount is invested in each stock.

C)As the number of stocks in a portfolio grows large, the variance of the portfolio is determined primarily by the average covariance among the stocks.

D)When combining stocks into a portfolio that puts positive weight on each stock, unless all of the stocks are uncorrelated with the portfolio, the risk of the portfolio will be lower than the weighted average volatility of the individual stocks.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The volatility declines as the number of stocks in a portfolio grows.

B)An equally weighted portfolio is a portfolio in which the same amount is invested in each stock.

C)As the number of stocks in a portfolio grows large, the variance of the portfolio is determined primarily by the average covariance among the stocks.

D)When combining stocks into a portfolio that puts positive weight on each stock, unless all of the stocks are uncorrelated with the portfolio, the risk of the portfolio will be lower than the weighted average volatility of the individual stocks.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

39

Use the table for the question(s)below.

Consider the following covariances between securities:

The variance on a portfolio that is made up of equal investments in Duke Energy and Microsoft stock is closest to:

A).065

B)0.090

C).149

D)-0.020

Consider the following covariances between securities:

The variance on a portfolio that is made up of equal investments in Duke Energy and Microsoft stock is closest to:

A).065

B)0.090

C).149

D)-0.020

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

40

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The variance of a portfolio is equal to the weighted average correlation of each stock within the portfolio.

B)The variance of a portfolio is equal to the sum of the covariances of the returns of all pairs of stocks in the portfolio multiplied by each of their portfolio weights.

C)The variance of a portfolio is equal to the weighted average covariances of each stock within the portfolio.

D)The volatility declines as the number of stocks in a portfolio grows.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)The variance of a portfolio is equal to the weighted average correlation of each stock within the portfolio.

B)The variance of a portfolio is equal to the sum of the covariances of the returns of all pairs of stocks in the portfolio multiplied by each of their portfolio weights.

C)The variance of a portfolio is equal to the weighted average covariances of each stock within the portfolio.

D)The volatility declines as the number of stocks in a portfolio grows.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

41

Suppose you have $10,000 in cash to invest. You decide to sell short $5,000 worth of Kinston stock and invest the proceeds from your short sale, plus your $10,000 into one-year U.S. treasury bills earning 5%. At the end of the year, you decide to liquidate your portfolio. Kinston Industries has the following realized returns: The return on your portfolio is closest to:

A)-0.5%

B)13.5%

C)-2.5%

D)14.5%

The return on your portfolio is closest to:A)-0.5%

B)13.5%

C)-2.5%

D)14.5%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

42

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is long those stocks that have negative portfolio weights.

B)The efficient portfolios are those portfolios offering the highest possible expected return for a given level of volatility.

C)When two stocks are perfectly negatively correlated, it becomes possible to hold a portfolio that bears absolutely no risk.

D)The lower the correlation of the securities in a portfolio the lower the volatility we can obtain.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is long those stocks that have negative portfolio weights.

B)The efficient portfolios are those portfolios offering the highest possible expected return for a given level of volatility.

C)When two stocks are perfectly negatively correlated, it becomes possible to hold a portfolio that bears absolutely no risk.

D)The lower the correlation of the securities in a portfolio the lower the volatility we can obtain.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following statements is FALSE?

A)A portfolio that consists of a long position in the risk-free investment is known as a levered portfolio.

B)The optimal portfolio will not depend on the investor's personal tradeoff between risk and return.

C)The volatility of the risk-free investment is zero.

D)Our total volatility is only a fraction of the volatility of the efficient portfolio, based on the amount we invest in the risk free asset.

A)A portfolio that consists of a long position in the risk-free investment is known as a levered portfolio.

B)The optimal portfolio will not depend on the investor's personal tradeoff between risk and return.

C)The volatility of the risk-free investment is zero.

D)Our total volatility is only a fraction of the volatility of the efficient portfolio, based on the amount we invest in the risk free asset.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

44

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

Consider a portfolio consisting of only Duke Energy and Microsoft. The percentage of your investment (portfolio weight)that you would place in Duke Energy stock to achieve a risk-free investment would be closest to:

A)15%

B)40%

C)23%

D)10%

Consider the following expected returns, volatilities, and correlations:

Consider a portfolio consisting of only Duke Energy and Microsoft. The percentage of your investment (portfolio weight)that you would place in Duke Energy stock to achieve a risk-free investment would be closest to:

A)15%

B)40%

C)23%

D)10%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

45

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)When stocks are perfectly positively correlated, the set of portfolios is identified graphically by a straight line between them.

B)An investor seeking high returns and low volatility should only invest in an efficient portfolio.

C)When the correlation between securities is less than 1, the volatility of the portfolio is reduced due to diversification.

D)Efficient portfolios can be easily ranked, because investors will choose from among them those with the highest expected returns.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)When stocks are perfectly positively correlated, the set of portfolios is identified graphically by a straight line between them.

B)An investor seeking high returns and low volatility should only invest in an efficient portfolio.

C)When the correlation between securities is less than 1, the volatility of the portfolio is reduced due to diversification.

D)Efficient portfolios can be easily ranked, because investors will choose from among them those with the highest expected returns.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

46

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)A short sale is a transaction in which you buy a stock that you do not own and then agree to sell that stock back in the future.

B)The efficient portfolios are those portfolios offering the lowest possible level of volatility for a given level of expected return.

C)A positive investment in a security can be referred to as a long position in the security.

D)It is possible to invest a negative amount in a stock or security call a short position.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)A short sale is a transaction in which you buy a stock that you do not own and then agree to sell that stock back in the future.

B)The efficient portfolios are those portfolios offering the lowest possible level of volatility for a given level of expected return.

C)A positive investment in a security can be referred to as a long position in the security.

D)It is possible to invest a negative amount in a stock or security call a short position.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

47

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is an efficient portfolio whenever it is possible to find another portfolio that is better in terms of both expected return and volatility.

B)We can rule out inefficient portfolios because they represent inferior investment choices.

C)The volatility of the portfolio will differ, depending on the correlation between the securities in the portfolio.

D)Correlation has no effect on the expected return on a portfolio.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)We say a portfolio is an efficient portfolio whenever it is possible to find another portfolio that is better in terms of both expected return and volatility.

B)We can rule out inefficient portfolios because they represent inferior investment choices.

C)The volatility of the portfolio will differ, depending on the correlation between the securities in the portfolio.

D)Correlation has no effect on the expected return on a portfolio.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

48

What is the efficient frontier and how does it change when more stocks are used to construct portfolios?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

49

Use the table for the question(s)below.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)Graphically, the efficient portfolios are those on the northeast edge of the set of possible portfolios, an area which we call the efficient frontier.

B)To arrive at the best possible set of risk and return opportunities, we should keep adding stocks until all investment opportunities are represented.

C)We say a portfolio is short those stocks that have negative portfolio weights.

D)Adding new investment opportunities allows for greater diversification and improves the efficient frontier.

Consider the following covariances between securities:

Which of the following statements is FALSE?

A)Graphically, the efficient portfolios are those on the northeast edge of the set of possible portfolios, an area which we call the efficient frontier.

B)To arrive at the best possible set of risk and return opportunities, we should keep adding stocks until all investment opportunities are represented.

C)We say a portfolio is short those stocks that have negative portfolio weights.

D)Adding new investment opportunities allows for greater diversification and improves the efficient frontier.

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

50

Use the table for the question(s)below.

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 100 stocks. If the average volatility of these stocks is 50% and the average correlation between the stocks is .7, then the volatility of this equally weighted portfolio is closest to:

A).72

B).63

C).40

D).50

Consider the following covariances between securities:

Consider an equally weighted portfolio that contains 100 stocks. If the average volatility of these stocks is 50% and the average correlation between the stocks is .7, then the volatility of this equally weighted portfolio is closest to:

A).72

B).63

C).40

D).50

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

51

Consider a portfolio consisting of only Microsoft and Wal-Mart stock. Calculate the expected return on such a portfolio when the weight on Microsoft stock is 0%, 25%, 50%, 75%, and 100%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

52

Consider a portfolio consisting of only Microsoft and Wal-Mart stock. Calculate the volatility of such a portfolio when the weight on Microsoft stock is 0%, 25%, 50%, 75%, and 100%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

53

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A)8%

B)9%

C)11%

D)6%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A)8%

B)9%

C)11%

D)6%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

54

Use the table for the question(s)below.

Consider the following covariances between securities:

What is the variance on a portfolio that has $2000 invested in Duke Energy, $3000 invested in Microsoft, and $5000 invested in Wal-Mart stock?

Consider the following covariances between securities:

What is the variance on a portfolio that has $2000 invested in Duke Energy, $3000 invested in Microsoft, and $5000 invested in Wal-Mart stock?

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

55

Use the table for the question(s)below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A)9%

B)14%

C)11%

D)12%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A)9%

B)14%

C)11%

D)12%

Unlock Deck

Unlock for access to all 133 flashcards in this deck.

Unlock Deck

k this deck

56

Use the table for the question(s)below.