Deck 9: Accounting for Associates and Joint Ventures: the Equity Method

Full screen (f)

Question

Question

Question

Question

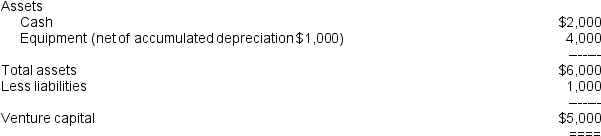

In July 20X6,Midstream Ltd entered into a joint venture operation with Delta Ltd to explore for minerals in the area of interest KP97.Midstream Ltd contributed $5,000,000 in cash and Delta Ltd contributed specialised drilling equipment with an agreed fair value of $5,000,000.The venturers shared control of the operation.All the assets of the operation were held by the venturers as tenants in common.The estimated useful life of the plant was 5 years.In the accounts of Delta Ltd,this equipment was carried at cost $6,000,000 less accumulated depreciation $3,000,000.For the year ended June 30 20X7,the following financial statements were prepared by the joint venture manager (amounts in thousands): Balance Sheet as at June 30 20X7

Performance Statement for the Year ended June 30 20X7

Performance Statement for the Year ended June 30 20X7

At June 30 20X7,the exploration had not yet advanced to the stage where a reliable estimate could be made of the recoverable mineral reserves in KP97.

At June 30 20X7,the exploration had not yet advanced to the stage where a reliable estimate could be made of the recoverable mineral reserves in KP97.

The journal entry to record the initial investment of Midstream Ltd would be:

A) Debit Investment in Joint Venture $5,000,000 and Credit Cash $5,000,000.

B) Debit Cash $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

C) Debit Investment in Joint Venture $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

D) None of the above.

Performance Statement for the Year ended June 30 20X7 At June 30 20X7,the exploration had not yet advanced to the stage where a reliable estimate could be made of the recoverable mineral reserves in KP97.The journal entry to record the initial investment of Midstream Ltd would be:

A) Debit Investment in Joint Venture $5,000,000 and Credit Cash $5,000,000.

B) Debit Cash $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

C) Debit Investment in Joint Venture $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

D) None of the above.

Question

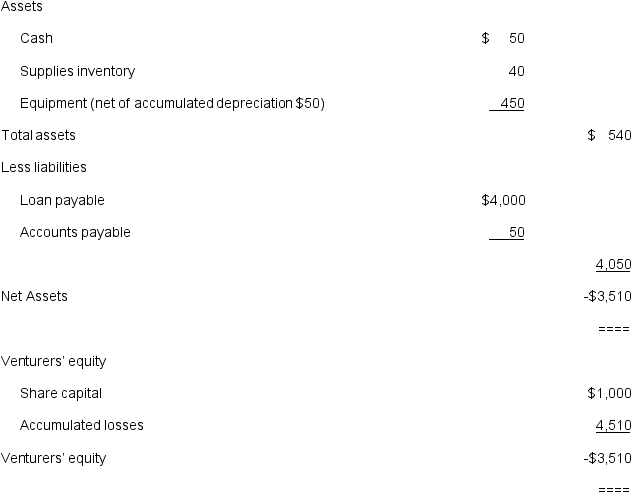

On July 1 20X4,Gold Ltd formed a joint venture entity with Maggs Ltd,Research Pty Ltd,to research for ultimate sale in the hamburger market the Giant Genetic Spud (GGS)and the Square Tomato (SR).There was a contractual agreement under which each company shared control of the venture.Each company contributed $500,000 in share capital on that date; and,during the first year of operations,each contributed a further $2,000,000 through loans.For the year ended June 30 20X5,the following financial statements were produced for the joint venture entity (amounts in thousands): Balance Sheet as at June 30 20X5

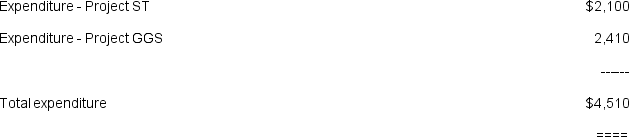

Statement of Research and Development Activity for the Year ended June 30 20X5

Statement of Research and Development Activity for the Year ended June 30 20X5

At June 30 20X5,Gold Ltd was uncertain as to the outcome of Project GT; but felt reasonable certain that Project GGS would develop into an economically viable patent right in the following year.

At June 30 20X5,Gold Ltd was uncertain as to the outcome of Project GT; but felt reasonable certain that Project GGS would develop into an economically viable patent right in the following year.

At June 30 20X5,the net investment of Gold Ltd in the joint venture entity calculated using the equity method was:

A) $ 500,000

B) $2,500,000

C) $2,000,000

D) None of the above.

Statement of Research and Development Activity for the Year ended June 30 20X5 At June 30 20X5,Gold Ltd was uncertain as to the outcome of Project GT; but felt reasonable certain that Project GGS would develop into an economically viable patent right in the following year.At June 30 20X5,the net investment of Gold Ltd in the joint venture entity calculated using the equity method was:

A) $ 500,000

B) $2,500,000

C) $2,000,000

D) None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/37

Play

Full screen (f)

Deck 9: Accounting for Associates and Joint Ventures: the Equity Method

1

On September 30 20X7,Auction Ltd acquired a 10% interest in an oil exploration joint venture operation,Deepwell Enterprises from Creeker Ltd at a cost of $3,000,000.At June 30 20X7,exploration had not yet reached the stage where an accurate evaluation of the area of interest could be made and each venturer had capitalised the expenditures incurred to that date in their own financial statements.For the year ended June 30 20X8,the financial statements of the UJV disclosed: a)Net assets at July 1 20X7 $9,000,000 - sundry assets $10,000,000 less sundry liabilities $1,000,000.Up to that stage $25,000,000 had been spent on exploration.

B)Exploration expenditure to September 30 20X7 $4,000,000.

C)Net assets at September 30 20X7 $5,000,000 - sundry assets $6,000,000 less sundry liabilities $1,000,000.

D)Exploration expenditure October 1 20X7 to June 30 20X8 $20,000,000.

E)Cash contributions from venturers in the period October 1 20X7 to June 30 20X8 (in proportion to percentage interest held)$26,000,000.

F)Net assets at June 30 20X8 $11,000,000 - sundry assets of $13,000,000 less sundry liabilities of $2,000,000.Deferred exploration expenditure to June 30 20X8 $49,000,000.

At the date of acquisition,September 30 19X7,which of the following journal entries would be used by Auction Ltd to record the cost of acquiring the investment in Deepwell Enterprises?

A)Dr Sundry Assets $600,000,Dr Deferred Exploration Expenditure $2,500,000,Cr Sundry Liabilities $100,000 Cr Cash $3,000,000.

B)Dr Investment in UJV $3,000,000,Cr Cash $3,000,000.

C)Dr Deferred Exploration Expenditure $3,000,000,Cr Cash $3,000,000.

D)None of the above.

B)Exploration expenditure to September 30 20X7 $4,000,000.

C)Net assets at September 30 20X7 $5,000,000 - sundry assets $6,000,000 less sundry liabilities $1,000,000.

D)Exploration expenditure October 1 20X7 to June 30 20X8 $20,000,000.

E)Cash contributions from venturers in the period October 1 20X7 to June 30 20X8 (in proportion to percentage interest held)$26,000,000.

F)Net assets at June 30 20X8 $11,000,000 - sundry assets of $13,000,000 less sundry liabilities of $2,000,000.Deferred exploration expenditure to June 30 20X8 $49,000,000.

At the date of acquisition,September 30 19X7,which of the following journal entries would be used by Auction Ltd to record the cost of acquiring the investment in Deepwell Enterprises?

A)Dr Sundry Assets $600,000,Dr Deferred Exploration Expenditure $2,500,000,Cr Sundry Liabilities $100,000 Cr Cash $3,000,000.

B)Dr Investment in UJV $3,000,000,Cr Cash $3,000,000.

C)Dr Deferred Exploration Expenditure $3,000,000,Cr Cash $3,000,000.

D)None of the above.

B

2

The essential element which would distinguish the business undertaking BKT Enterprises as a partnership and not a joint venture operation would be:

A) The business undertaking makes a profit in the year.

B) There is no joint control agreement so that the undertaking is neither a joint venture entity nor a joint venture operation.

C) The business activity is an undertaking formed by the investors with the intention of making a profit.

D) None of the above.

A) The business undertaking makes a profit in the year.

B) There is no joint control agreement so that the undertaking is neither a joint venture entity nor a joint venture operation.

C) The business activity is an undertaking formed by the investors with the intention of making a profit.

D) None of the above.

B

3

Accounting Standard AASB131 Interests in Joint Ventures does not apply to investments in joint ventures:

A) by venture capital organisations

B) by unit trusts

C) which are held for sale

D) all of the above

A) by venture capital organisations

B) by unit trusts

C) which are held for sale

D) all of the above

D

4

In July 20X6,Midstream Ltd entered into a joint venture operation with Delta Ltd to explore for minerals in the area of interest KP97.Midstream Ltd contributed $5,000,000 in cash and Delta Ltd contributed specialised drilling equipment with an agreed fair value of $5,000,000.The venturers shared control of the operation.All the assets of the operation were held by the venturers as tenants in common.The estimated useful life of the plant was 5 years.In the accounts of Delta Ltd,this equipment was carried at cost $6,000,000 less accumulated depreciation $3,000,000.For the year ended June 30 20X7,the following financial statements were prepared by the joint venture manager (amounts in thousands): Balance Sheet as at June 30 20X7

Performance Statement for the Year ended June 30 20X7

At June 30 20X7,the exploration had not yet advanced to the stage where a reliable estimate could be made of the recoverable mineral reserves in KP97.

The journal entry to record the initial investment of Midstream Ltd would be:

A) Debit Investment in Joint Venture $5,000,000 and Credit Cash $5,000,000.

B) Debit Cash $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

C) Debit Investment in Joint Venture $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

D) None of the above.

Performance Statement for the Year ended June 30 20X7 At June 30 20X7,the exploration had not yet advanced to the stage where a reliable estimate could be made of the recoverable mineral reserves in KP97.The journal entry to record the initial investment of Midstream Ltd would be:

A) Debit Investment in Joint Venture $5,000,000 and Credit Cash $5,000,000.

B) Debit Cash $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

C) Debit Investment in Joint Venture $2,500,000, Debit Plant and Equipment $2,500,000 and Credit Cash $5,000,000.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

5

On July 1 20X4,Gold Ltd formed a joint venture entity with Maggs Ltd,Research Pty Ltd,to research for ultimate sale in the hamburger market the Giant Genetic Spud (GGS)and the Square Tomato (SR).There was a contractual agreement under which each company shared control of the venture.Each company contributed $500,000 in share capital on that date; and,during the first year of operations,each contributed a further $2,000,000 through loans.For the year ended June 30 20X5,the following financial statements were produced for the joint venture entity (amounts in thousands): Balance Sheet as at June 30 20X5

Statement of Research and Development Activity for the Year ended June 30 20X5

At June 30 20X5,Gold Ltd was uncertain as to the outcome of Project GT; but felt reasonable certain that Project GGS would develop into an economically viable patent right in the following year.

At June 30 20X5,the net investment of Gold Ltd in the joint venture entity calculated using the equity method was:

A) $ 500,000

B) $2,500,000

C) $2,000,000

D) None of the above.

Statement of Research and Development Activity for the Year ended June 30 20X5 At June 30 20X5,Gold Ltd was uncertain as to the outcome of Project GT; but felt reasonable certain that Project GGS would develop into an economically viable patent right in the following year.At June 30 20X5,the net investment of Gold Ltd in the joint venture entity calculated using the equity method was:

A) $ 500,000

B) $2,500,000

C) $2,000,000

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

6

At the reporting date,June 30 20X7,the effect of the adjustments to record the interest of Midstream Ltd in the joint venture would be:

A) Debit Deferred Exploration Expenditure $2,650,000, Credit Interest Revenue $150,000, Credit Investment in Joint Venture $2,500,000.

B) Debit Deferred Exploration Expenditure $2,650,000, Debit Cash $1,000,000, Debit Plant and Equipment $2,500,000, Credit Accumulated Depreciation - Plant $500,000, Credit Sundry Liabilities $500,000, Credit Interest Revenue $150,000 and Credit Investment in Joint Venture $5,000,000.

C) Debit Exploration Expense $2,650,000, Credit Interest Revenue $150,000 and credit Investment in Joint Venture $2,500,000.

D) None of the above.

A) Debit Deferred Exploration Expenditure $2,650,000, Credit Interest Revenue $150,000, Credit Investment in Joint Venture $2,500,000.

B) Debit Deferred Exploration Expenditure $2,650,000, Debit Cash $1,000,000, Debit Plant and Equipment $2,500,000, Credit Accumulated Depreciation - Plant $500,000, Credit Sundry Liabilities $500,000, Credit Interest Revenue $150,000 and Credit Investment in Joint Venture $5,000,000.

C) Debit Exploration Expense $2,650,000, Credit Interest Revenue $150,000 and credit Investment in Joint Venture $2,500,000.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

7

The journal entry to record the initial investment of Delta Ltd would be:

A) Debit Investment in Joint Venture $5,000,000, Credit Plant and Equipment $6,000,000, Debit Accumulated Depreciation $3,000,000, Credit Gain on Disposal of Property, Plant and Equipment $1,000,000, Credit Unearned Income $1,000,000.

B) Debit Cash $2,500,000, Debit Plant $2,500,000, Credit Plant and Equipment $6,000,000, Debit Accumulated Depreciation $3,000,000, Credit Gain on Disposal of Property, Plant and Equipment $1,000,000, Credit Unearned Income $1,000,000.

C) Debit Investment in Joint Venture $5,000,000 and Credit Plant Disposal account $5,000,000.

D) None of the above.

A) Debit Investment in Joint Venture $5,000,000, Credit Plant and Equipment $6,000,000, Debit Accumulated Depreciation $3,000,000, Credit Gain on Disposal of Property, Plant and Equipment $1,000,000, Credit Unearned Income $1,000,000.

B) Debit Cash $2,500,000, Debit Plant $2,500,000, Credit Plant and Equipment $6,000,000, Debit Accumulated Depreciation $3,000,000, Credit Gain on Disposal of Property, Plant and Equipment $1,000,000, Credit Unearned Income $1,000,000.

C) Debit Investment in Joint Venture $5,000,000 and Credit Plant Disposal account $5,000,000.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

8

Midstream Ltd and Delta Ltd enter into a business undertaking to lease a 100-hectare vineyard from Pinot Ltd.There is a contractual agreement between the two companies whereby they share control and must agree on all strategic financial and operating decisions.The two companies appoint Todman Management Pty Ltd as the vineyard manager.A separate set of accounting database is established for the undertaking and each investor contributes cash capital to the undertaking.The intention of the investing companies is to market the produce of the vineyard and make a profit.The business undertaking is:

A) A joint venture operation since the investors have agreed to a sharing of control.

B) A joint venture entity since it has been established to operate the vineyard with the intention of making a profit.

C) A simple partnership in which two companies operate as partners in a business undertaking.

D) None of the above.

A) A joint venture operation since the investors have agreed to a sharing of control.

B) A joint venture entity since it has been established to operate the vineyard with the intention of making a profit.

C) A simple partnership in which two companies operate as partners in a business undertaking.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

9

A jointly controlled entity can be:

A) a company

B) a partnership

C) a trust

D) all of the above

A) a company

B) a partnership

C) a trust

D) all of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

10

A venture must recognise its interest in a jointly controlled entity using:

A) proportionate consolidation

B) equity method

C) either proportionate consolidation or equity method

D) one line method

A) proportionate consolidation

B) equity method

C) either proportionate consolidation or equity method

D) one line method

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

11

Midstream Ltd and Delta Ltd enter into a business undertaking to lease a 100-hectare vineyard from Pinot Ltd.There is a contractual agreement between the two companies whereby they share control and must agree on all strategic financial and operating decisions.The two companies appoint Todman Management Pty Ltd as the vineyard manager.A separate set of accounting database is established for the undertaking and each investor contributes cash capital to the undertaking and hold the assets as tenants in common.The intention of the investing companies is to take their proportionate share of the produce of the vineyard to use in their own wineries.The business undertaking is:

A) A joint venture operation since the investors have agreed to a sharing of control and to a sharing of the produce of the vineyard.

B) A joint venture entity since the undertaking has been established as a separate entity in which there is a simple sharing of control.

C) A simple partnership in which two companies operate as partners in a business undertaking.

D) None of the above.

A) A joint venture operation since the investors have agreed to a sharing of control and to a sharing of the produce of the vineyard.

B) A joint venture entity since the undertaking has been established as a separate entity in which there is a simple sharing of control.

C) A simple partnership in which two companies operate as partners in a business undertaking.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

12

The line by line method of accounting for interests in jointly controlled entities is recommended by AASB131 because:

A) it reflects the venturer's control over the future economic benefits

B) it is the method used for jointly controlled operations and jointly controlled assets which only differ from jointly controlled entities in their legal form

C) it is consistent with the legal form of a joint arrangement

D) none of the above

A) it reflects the venturer's control over the future economic benefits

B) it is the method used for jointly controlled operations and jointly controlled assets which only differ from jointly controlled entities in their legal form

C) it is consistent with the legal form of a joint arrangement

D) none of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

13

Where a venturer is a subsidiary company the equity method would be applied to an investment in a jointly controlled entity:

A) in the joint venture entity financial statements

B) in the subsidiary's financial statements

C) in the consolidated financial statements

D) none of the above

A) in the joint venture entity financial statements

B) in the subsidiary's financial statements

C) in the consolidated financial statements

D) none of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

14

Midstream Ltd and Delta Ltd enter into a business undertaking in which they each commit 50-hectare vineyards.There is a contractual agreement between the two companies whereby they share control and must agree on all strategic financial and operating decisions relating to the two vineyards.The two companies appoint Todman Management Pty Ltd as the manager of the vineyard undertaking.A separate set of accounting database is established for the undertaking and each investor contributes additional cash capital to the undertaking and hold assets other than the vineyards as tenants in common.The intention of the investing companies is to take their proportionate share of the produce from the two vineyards to use in their own wineries.The business undertaking is:

A) A joint venture operation since the investors have agreed to a sharing of control and to a sharing of the produce of the vineyard.

B) A joint venture entity since the undertaking has been established as a separate entity in which there is a simple sharing of control.

C) A simple partnership in which two companies operate as partners in a business undertaking.

D) None of the above.

A) A joint venture operation since the investors have agreed to a sharing of control and to a sharing of the produce of the vineyard.

B) A joint venture entity since the undertaking has been established as a separate entity in which there is a simple sharing of control.

C) A simple partnership in which two companies operate as partners in a business undertaking.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

15

The concept of joint control:

A) includes unilateral control

B) includes significant influence

C) excludes unilateral control and significant influence

D) none of the above

A) includes unilateral control

B) includes significant influence

C) excludes unilateral control and significant influence

D) none of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

16

The line by line method of accounting is required for interests in joint ventures which are:

A) jointly controlled entities

B) jointly controlled operations

C) jointly controlled assets

D) both B and C

A) jointly controlled entities

B) jointly controlled operations

C) jointly controlled assets

D) both B and C

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

17

Midstream Ltd and Delta Ltd enter into a business undertaking to lease a 100-hectare vineyard from Pinot Ltd.There is a contractual agreement between the two companies whereby they share control and must agree on all strategic financial and operating decisions.The two companies appoint Todman Management Pty Ltd as the vineyard manager.A separate set of accounting database is established for the undertaking and each investor contributes cash capital to the undertaking and holds the assets as tenants in common.Each of the investing companies enters into a separate agreement with the vineyard manager to sell the produce of the vineyard in the market on their behalf.The business undertaking is:

A) A joint venture operation since the investors have agreed to a sharing of control and to a sharing of the produce of the vineyard.

B) A joint venture entity since the undertaking has been established as a separate entity in which there is a simple sharing of control.

C) A simple partnership in which two companies operate as partners in a business undertaking with the intention of making a profit.

D) None of the above.

A) A joint venture operation since the investors have agreed to a sharing of control and to a sharing of the produce of the vineyard.

B) A joint venture entity since the undertaking has been established as a separate entity in which there is a simple sharing of control.

C) A simple partnership in which two companies operate as partners in a business undertaking with the intention of making a profit.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

18

The one line method of accounting for interests in jointly controlled entities is appropriate because:

A) venturers have joint control

B) Venturers have control

C) Venturers have significant influence

D) none of the above

A) venturers have joint control

B) Venturers have control

C) Venturers have significant influence

D) none of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

19

In a venture in which there are jointly controlled assets,the venturers share the assets as tenants in common; which means that:

A) Each venturer has a proportionate interest in each joint controlled asset.

B) Each venturer has a distinct but unidentifiable share of each jointly controlled asset.

C) Each venturer has a distinct and identifiable share of each jointly controlled asset.

D) None of the above.

A) Each venturer has a proportionate interest in each joint controlled asset.

B) Each venturer has a distinct but unidentifiable share of each jointly controlled asset.

C) Each venturer has a distinct and identifiable share of each jointly controlled asset.

D) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

20

The one line method of reporting jointly controlled operations and jointly controlled assets:

A) discloses joint venture liabilities

B) offsets joint venture liabilities against assets

C) does not recognise liabilities

D) none of the above

A) discloses joint venture liabilities

B) offsets joint venture liabilities against assets

C) does not recognise liabilities

D) none of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

21

Jointly controlled operations and jointly controlled assets result from an unincorporated contractual association

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

22

An investor in a joint venture is required to account for the investment in accordance with AASB131

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

23

The main advantage of the one line method of disclosing interests in jointly controlled operations and jointly controlled assets is disclosure of these interests.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

24

For a joint venture to be recognised under AASB131 there must be a contractual arrangement

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

25

A 40% venturer in a jointly controlled operation sells an asset to the joint venture.The asset has a fair value of $5,000,000.The carrying amount in the books of the venture was $4,000,000.The profit to be recognised by the venturer is:

A) $5,000.000

B) $4,000,000

C) $1,000,000

D) $600,000

A) $5,000.000

B) $4,000,000

C) $1,000,000

D) $600,000

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

26

What factors are relevant to the choice of accounting methods for venturers in jointly controlled entities?

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

27

Alternative reporting formats are allowed under AASB131 for jointly controlled entities

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

28

Supplementary disclosure requirements for joint ventures in the financial statements of venturers include:

A) significant joint venture interests

B) contingent liabilities arising from joint ventures

C) capital commitments arising from joint ventures

D) all of the above

A) significant joint venture interests

B) contingent liabilities arising from joint ventures

C) capital commitments arising from joint ventures

D) all of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

29

Discuss the issue of entitlement of venturers to share in profits of a jointly controlled entity.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

30

Discuss the principles applying to the calculation of a gain on the sale of a portion of a jointly controlled operation.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

31

The one line method of accounting for joint ventures is the same as the equity method of accounting for investments in associates

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

32

What is meant by the statement that a venturer will account for an interest in a jointly controlled operation or jointly controlled asset by 'converting from the one line method to the line by line method'?

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

33

The line by line method of accounting hides the existence of interests in jointly controlled operations and jointly controlled assets.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

34

The line by line method of accounting for joint venture categories of jointly controlled operations and jointly controlled assets is the same as the proportionate consolidation method of accounting for jointly controlled entities

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

35

Discuss the control test for asset recognition in relation to the line by line method of accounting for interests in jointly controlled operations and jointly controlled assets.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

36

A 50% joint venturer acquires a further 10% interest in a jointly controlled operation,paying $2,000,000 to the jointly controlled operation whose assets including cash $1,000,000 have a fair value of $4,000,000.The acquisition will have the following effect on the venturer's cash position:

A) reduced by $2,000,000

B) reduced by $700,000

C) reduced by $1,000,000

D) none of the above

A) reduced by $2,000,000

B) reduced by $700,000

C) reduced by $1,000,000

D) none of the above

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

37

Unrealised profits or losses on the transfer of assets to a jointly controlled operation are always offset against the joint venture investment account.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 37 flashcards in this deck.