Deck 14: Corporate Financing Decisions and Efficient Capital Markets

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

You have observed an apparent, yet odd, increase stock prices when companies have spun-off divisions. You have just collected the data on 50 such events. The average beta (market value weighted) is 1.15 for this group.

Question

Question

Question

Question

Question

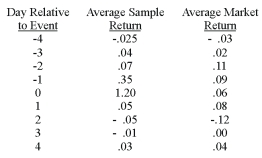

The Pan Fries Company just announced a new model of their cooker which will reduce cooking time and fat absorption. The price reaction of their stock is listed below. Calculate the abnormal return behavior, graph it and explain the behavior.

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/39

Play

Full screen (f)

Deck 14: Corporate Financing Decisions and Efficient Capital Markets

1

According to the efficient market hypothesis, financial markets fluctuate daily because they:

A) are inefficient.

B) slowly react to new information.

C) are continually reacting to new information.

D) offer tremendous arbitrage opportunities.

A) are inefficient.

B) slowly react to new information.

C) are continually reacting to new information.

D) offer tremendous arbitrage opportunities.

are continually reacting to new information.

2

Insider trading does not offer any advantages if the financial markets are:

A) weak form efficient.

B) semiweak form efficient.

C) semistrong form efficient.

D) strong form efficient.

A) weak form efficient.

B) semiweak form efficient.

C) semistrong form efficient.

D) strong form efficient.

strong form efficient.

3

The abnormal return on a security for a particular day can be estimated by the equation:

A) AR = R - Rm.

B) AR = Rm - R.

C) AR = Rm - Rf.

D) AR = R - Rf.

E) AR = Rf - Rm.

A) AR = R - Rm.

B) AR = Rm - R.

C) AR = Rm - Rf.

D) AR = R - Rf.

E) AR = Rf - Rm.

AR = R - Rm.

4

In an efficient market, the price of a security will:

A) always rise immediately upon the release of new information with no further price adjustments related to that information.

B) react to new information over a two-day period after which time no further price adjustments related to that information will occur.

C) rise sharply when new information is first released and then decline to a new stable level by the following day.

D) react immediately to new information with no further price adjustments related to that information.

A) always rise immediately upon the release of new information with no further price adjustments related to that information.

B) react to new information over a two-day period after which time no further price adjustments related to that information will occur.

C) rise sharply when new information is first released and then decline to a new stable level by the following day.

D) react immediately to new information with no further price adjustments related to that information.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

5

The market price of a stock moves or fluctuates daily. This fluctuation is:

A) inconsistent with the semi-strong efficient market hypothesis because prices should be stable.

B) inconsistent with the weak form efficient market hypothesis because all past information should be priced in.

C) consistent with the semi-strong form of the efficient market hypothesis because as new information arrives daily prices will adjust to it.

D) consistent with the strong form because prices are controlled by insiders.

A) inconsistent with the semi-strong efficient market hypothesis because prices should be stable.

B) inconsistent with the weak form efficient market hypothesis because all past information should be priced in.

C) consistent with the semi-strong form of the efficient market hypothesis because as new information arrives daily prices will adjust to it.

D) consistent with the strong form because prices are controlled by insiders.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

6

Which one of the following statements is correct concerning market efficiency?

A) Real asset markets are more efficient than financial markets.

B) If a market is efficient, arbitrage opportunities should be common.

C) In an efficient market, some market participants will have an advantage over others.

D) A firm will generally receive a fair price when it sells shares of stock.

A) Real asset markets are more efficient than financial markets.

B) If a market is efficient, arbitrage opportunities should be common.

C) In an efficient market, some market participants will have an advantage over others.

D) A firm will generally receive a fair price when it sells shares of stock.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

7

Serial correlation studies generally show that:

A) semi-strong efficiency is supported.

B) the relationships are significant and can be used to predict price in the next period.

C) the correlations are small relative to both the estimation errors and transactions costs.

D) patterns exist in the data that can be exploited.

A) semi-strong efficiency is supported.

B) the relationships are significant and can be used to predict price in the next period.

C) the correlations are small relative to both the estimation errors and transactions costs.

D) patterns exist in the data that can be exploited.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

8

Which form of the efficient market hypothesis implies that security prices reflect all information contained in past prices?

A) The weak form.

B) The semi-strong form.

C) The strong form.

D) The hard form.

E) The past form.

A) The weak form.

B) The semi-strong form.

C) The strong form.

D) The hard form.

E) The past form.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

9

A lawyer works for a firm that advises corporate firms planning to sue other corporations for antitrust damages. He finds that he can "beat the market" by short-selling the stock of the firm that will be sued. This finding is a violation of the:

A) moderate form of the efficient market hypothesis.

B) semi-strong form of the efficient market hypothesis.

C) strong form of the efficient market hypothesis.

D) weak form of the efficient market hypothesis.

A) moderate form of the efficient market hypothesis.

B) semi-strong form of the efficient market hypothesis.

C) strong form of the efficient market hypothesis.

D) weak form of the efficient market hypothesis.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

10

An investor discovers that predictions about weather patterns published years in advance and found in the Farmer's Almanac are amazingly accurate. In fact, these predictions enable the investor to predict the health of the farm economy and therefore certain security prices. This finding is a violation of the:

A) moderate form of the efficient market hypothesis.

B) semi-strong form of the efficient market hypothesis.

C) strong form of the efficient market hypothesis.

D) weak form of the efficient market hypothesis.

A) moderate form of the efficient market hypothesis.

B) semi-strong form of the efficient market hypothesis.

C) strong form of the efficient market hypothesis.

D) weak form of the efficient market hypothesis.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

11

In analyzing the financial decision of the firm, it turns out that the typical firm:

A) has more capital expenditure opportunities with positive NPVs than financing opportunities.

B) has more financing opportunities with positive NPVs than capital expenditure opportunities.

C) has about the same number of capital expenditure opportunities and financing opportunities.

D) has no opportunities for positive NPVs in either capital expenditures or in financing.

A) has more capital expenditure opportunities with positive NPVs than financing opportunities.

B) has more financing opportunities with positive NPVs than capital expenditure opportunities.

C) has about the same number of capital expenditure opportunities and financing opportunities.

D) has no opportunities for positive NPVs in either capital expenditures or in financing.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

12

The model, Pt = Pt-1 + Expected Return + Random error, supports the weak form of the efficient market hypothesis if:

A) the random error can be predicted by past prices.

B) there is correlation between random errors period to period.

C) the random errors are unrelated from one period to the next period.

D) the expected return is not based on the security's risk.

A) the random error can be predicted by past prices.

B) there is correlation between random errors period to period.

C) the random errors are unrelated from one period to the next period.

D) the expected return is not based on the security's risk.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

13

If the financial markets are efficient, then investors should expect their investments in those markets to:

A) earn extraordinary returns on a routine basis.

B) generally have positive net present values.

C) generally have zero net present values.

D) produce arbitrage opportunities on a routine basis.

A) earn extraordinary returns on a routine basis.

B) generally have positive net present values.

C) generally have zero net present values.

D) produce arbitrage opportunities on a routine basis.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

14

Under the concept of an efficient market a random walk in stock prices means that:

A) there is no driving force behind price changes.

B) technical analysts can predict future price movements to earn excess returns.

C) the unexplained portion of price change in one period is unrelated to the unexplained portion of price change in any other period.

D) the unexplained portion of price change in one period that can not be explained by expected return can only be explained by the unexplained portion of price change in a prior period.

A) there is no driving force behind price changes.

B) technical analysts can predict future price movements to earn excess returns.

C) the unexplained portion of price change in one period is unrelated to the unexplained portion of price change in any other period.

D) the unexplained portion of price change in one period that can not be explained by expected return can only be explained by the unexplained portion of price change in a prior period.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

15

Suppose that firms with unexpectedly high earnings earn abnormally high returns for several months after the announcement. This would be evidence of:

A) efficient markets in the weak form.

B) inefficient markets in the weak form.

C) efficient markets in the semi-strong form.

D) inefficient markets in the semi-strong form.

E) inefficient markets in the strong form.

A) efficient markets in the weak form.

B) inefficient markets in the weak form.

C) efficient markets in the semi-strong form.

D) inefficient markets in the semi-strong form.

E) inefficient markets in the strong form.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

16

When the stock price follows a random walk the price today is said to be equal to the prior period price plus the expected return for the period with any remaining difference to the actual return due to:

A) a predictable amount based on the past prices.

B) a component based on new information unrelated to past prices.

C) the security's risk.

D) the risk free rate.

A) a predictable amount based on the past prices.

B) a component based on new information unrelated to past prices.

C) the security's risk.

D) the risk free rate.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

17

An investor discovers that for a certain group of stocks, large positive price changes are always followed by large negative price changes. This finding is a violation of the:

A) moderate form of the efficient market hypothesis.

B) semi-strong form of the efficient market hypothesis.

C) strong form of the efficient market hypothesis.

D) weak form of the efficient market hypothesis.

A) moderate form of the efficient market hypothesis.

B) semi-strong form of the efficient market hypothesis.

C) strong form of the efficient market hypothesis.

D) weak form of the efficient market hypothesis.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

18

If you excel in analyzing the future outlook of firms, you would prefer that the financial markets be ____ form efficient so that you can have an advantage in the marketplace.

A) weak

B) semiweak

C) semistrong

D) strong

A) weak

B) semiweak

C) semistrong

D) strong

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

19

In an efficient market when a firm makes an announcement of a new product or product enhancement with superior technology providing positive NPV the price of the stock will:

A) rise gradually over the next few days.

B) decline gradually over the next few days.

C) rise on the same day to the new price.

D) stay at the same price, with no net effect.

E) drop on the same day to the new price.

A) rise gradually over the next few days.

B) decline gradually over the next few days.

C) rise on the same day to the new price.

D) stay at the same price, with no net effect.

E) drop on the same day to the new price.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is not true about serial correlation?

A) It measures the correlation between the current return on a security and the current return on another security.

B) It involves only one security.

C) Positive serial correlation indicates a tendency for continuation.

D) Negative serial correlation indicates a tendency toward reversal.

E) Significant positive or negative serial correlation coefficients are indicative of market inefficiency in the weak form.

A) It measures the correlation between the current return on a security and the current return on another security.

B) It involves only one security.

C) Positive serial correlation indicates a tendency for continuation.

D) Negative serial correlation indicates a tendency toward reversal.

E) Significant positive or negative serial correlation coefficients are indicative of market inefficiency in the weak form.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

21

If the market is weak form efficient:

A) semistrong form efficiency holds.

B) strong form efficiency must hold.

C) semistrong form efficiency may hold.

D) markets are not weak form efficient.

A) semistrong form efficiency holds.

B) strong form efficiency must hold.

C) semistrong form efficiency may hold.

D) markets are not weak form efficient.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

22

The stock market crash of October 1987 and the Great Crash of 1929, although not fully explained, may be (partially) explained by:

A) new information coming to the market; being efficient the market was priced down.

B) technical difficulties in order processing.

C) the bubble theory that prices move wildly above equilibrium values and eventually fall back to equilibrium causing large losses.

D) the conspiracy theory that large institutions and rich investors control the market and caused the general population to suffer large wealth losses.

A) new information coming to the market; being efficient the market was priced down.

B) technical difficulties in order processing.

C) the bubble theory that prices move wildly above equilibrium values and eventually fall back to equilibrium causing large losses.

D) the conspiracy theory that large institutions and rich investors control the market and caused the general population to suffer large wealth losses.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

23

On May 12, 2001 the WWF announced the demise of the XFL. The WWF stock price jumped up significantly on the day.

A) These results are consistent with strong from efficiency because insiders knew the league would fold.

B) These results are consistent with semi-strong form efficiency as the demise would reverse the negative cashflow.

C) These results are inconsistent with weak form efficiency because past price behavior predicted the collapse.

D) These results are inconsistent with all forms of market efficiency because a failure is a negative event.

E) These results are consistent with all forms of market efficiency as all information is known and priced in.

A) These results are consistent with strong from efficiency because insiders knew the league would fold.

B) These results are consistent with semi-strong form efficiency as the demise would reverse the negative cashflow.

C) These results are inconsistent with weak form efficiency because past price behavior predicted the collapse.

D) These results are inconsistent with all forms of market efficiency because a failure is a negative event.

E) These results are consistent with all forms of market efficiency as all information is known and priced in.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

24

The Nu-Tux Seat Company has an expansion opportunity and is considering selling their 100,000 share investment in Slip-Cover currently worth $2 million or raising other external funding. The share price has been holding in a narrow range day to day. If Nu-Tux decides to unload their holding is there any concern about getting the full $2 million, aside from investment banker/brokerage fees. Explain these concerns about market behavior and cite the evidence.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

25

Studies of the performance of professionally managed mutual funds find that these funds:

A) Do not outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding refutes the semi-strong form of the efficient market hypothesis.

B) Do not outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding supports the semi-strong form of the efficient market hypothesis.

C) Outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding refutes the semi-strong form of the efficient market hypothesis.

D) Outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding supports the semi-strong form of the efficient market hypothesis.

A) Do not outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding refutes the semi-strong form of the efficient market hypothesis.

B) Do not outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding supports the semi-strong form of the efficient market hypothesis.

C) Outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding refutes the semi-strong form of the efficient market hypothesis.

D) Outperform a market index. Assuming mutual fund managers rely primarily on public information, this finding supports the semi-strong form of the efficient market hypothesis.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

26

In examining the issue of whether the choice of accounting methods affects stock prices, studies have found that:

A) accounting depreciation methods can significantly affect stock prices.

B) switching depreciation methods can significantly affect stock prices.

C) accounting changes that increase accounting earnings also increases stock prices.

D) accounting changes can affect stock prices if the company were either to withhold information or provide incorrect information.

A) accounting depreciation methods can significantly affect stock prices.

B) switching depreciation methods can significantly affect stock prices.

C) accounting changes that increase accounting earnings also increases stock prices.

D) accounting changes can affect stock prices if the company were either to withhold information or provide incorrect information.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

27

Explain why it is that in an efficient market, investments have an expected NPV of zero.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

28

When the stock return data has been divided into market capitalization groups the return performance of:

A) all such groups has been the same over time.

B) small capitalization stocks have outperformed large capitalization stocks even after risk adjustment.

C) small capitalization stocks have under performed large capitalization stocks once adjusted for risk.

D) small and large capitalization stocks have performed equally on a risk-adjusted basis.

A) all such groups has been the same over time.

B) small capitalization stocks have outperformed large capitalization stocks even after risk adjustment.

C) small capitalization stocks have under performed large capitalization stocks once adjusted for risk.

D) small and large capitalization stocks have performed equally on a risk-adjusted basis.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

29

Suppose your cousin invests in the stock market and doubles her money in a single year while the market, on average, earned a return of only about 15%. Is your cousin's performance a violation of market efficiency?

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

30

You have observed an apparent, yet odd, increase stock prices when companies have spun-off divisions. You have just collected the data on 50 such events. The average beta (market value weighted) is 1.15 for this group.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

31

Evidence on stock prices finds that the sudden death of a chief executive officer causes stock prices to fall and the sudden death of an active founding chief executive officer causes stock price to rise. This contrary evidence happens because:

A) markets are inefficient and unsure of the real value of the events.

B) death is inevitable and market prices are random.

C) things simply happen.

D) the value of the founding executive was a negative to the firm.

A) markets are inefficient and unsure of the real value of the events.

B) death is inevitable and market prices are random.

C) things simply happen.

D) the value of the founding executive was a negative to the firm.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

32

Studies on the timing of corporate issues of new equities suggest that corporations tend to offer

A) New issues after stock price increases. This behavior is consistent with the weak form of the efficient market hypothesis.

B) New issues after stock price increases. This behavior is inconsistent with the weak form of the efficient market hypothesis.

C) New issues randomly with regard to stock price changes. This behavior is consistent with the weak form of the efficient market hypothesis.

D) New issues randomly with regard to stock price changes. This behavior is inconsistent with the weak form of the efficient market hypothesis.

A) New issues after stock price increases. This behavior is consistent with the weak form of the efficient market hypothesis.

B) New issues after stock price increases. This behavior is inconsistent with the weak form of the efficient market hypothesis.

C) New issues randomly with regard to stock price changes. This behavior is consistent with the weak form of the efficient market hypothesis.

D) New issues randomly with regard to stock price changes. This behavior is inconsistent with the weak form of the efficient market hypothesis.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

33

Individuals that continually monitor the financial markets seeking mispriced securities:

A) tend to make substantial profits on a daily basis.

B) tend to make the markets more efficient.

C) are never able to find a security that is temporarily mispriced.

D) are always quite successful using only well-known public information as their basis of evaluation.

A) tend to make substantial profits on a daily basis.

B) tend to make the markets more efficient.

C) are never able to find a security that is temporarily mispriced.

D) are always quite successful using only well-known public information as their basis of evaluation.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

34

The abnormal returns for initial public offerings over longer time periods seem to call market efficiency into question because:

A) the average returns at announcement are large and positive while the long-term results are much lower than the returns for seasoned equity offerings.

B) the average returns at announcement are small and negative while the long-term results are much lower than the returns for seasoned equity offerings.

C) the average returns at announcement are zero while the long-term results are much higher than the returns for seasoned equity offerings.

D) the average returns at announcement are large and positive while the long-term results are much higher than the returns for seasoned equity offerings.

E) the average returns at announcement are zero while the long-term results are much lower than the returns for seasoned equity offerings.

A) the average returns at announcement are large and positive while the long-term results are much lower than the returns for seasoned equity offerings.

B) the average returns at announcement are small and negative while the long-term results are much lower than the returns for seasoned equity offerings.

C) the average returns at announcement are zero while the long-term results are much higher than the returns for seasoned equity offerings.

D) the average returns at announcement are large and positive while the long-term results are much higher than the returns for seasoned equity offerings.

E) the average returns at announcement are zero while the long-term results are much lower than the returns for seasoned equity offerings.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

35

The Pan Fries Company just announced a new model of their cooker which will reduce cooking time and fat absorption. The price reaction of their stock is listed below. Calculate the abnormal return behavior, graph it and explain the behavior.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

36

Technical analysts believe that the:

A) future stock prices are unpredictable and therefore plot past prices.

B) stock prices are in equilibrium and advise not to follow price patterns.

C) future stock prices are a reflection of the past and plot prices to find reoccurring price patterns.

D) stock prices are only predictable based on the outlook for corporations earnings.

E) SML is the most reliable predictor.

A) future stock prices are unpredictable and therefore plot past prices.

B) stock prices are in equilibrium and advise not to follow price patterns.

C) future stock prices are a reflection of the past and plot prices to find reoccurring price patterns.

D) stock prices are only predictable based on the outlook for corporations earnings.

E) SML is the most reliable predictor.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

37

If the securities market is efficient an investor need only throw darts at the stock pages to pick securities and be just as well off.

A) This is true because there are no differences in risk and return.

B) This is true because in an efficient stock market prices do not fluctuate.

C) This is false because professional portfolio managers prefer to generate commissions.

D) This is false because investors may not hold a desirable risk-return combination in their portfolio.

E) This is false because the markets are controlled by the institutional investors.

A) This is true because there are no differences in risk and return.

B) This is true because in an efficient stock market prices do not fluctuate.

C) This is false because professional portfolio managers prefer to generate commissions.

D) This is false because investors may not hold a desirable risk-return combination in their portfolio.

E) This is false because the markets are controlled by the institutional investors.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

38

A car maker announced a recall for faulty brakes. The company stock returned .004 the day before the announcement; -.001 the day of the announcement and .0045 the day after the announcement. The market average was .006, .0072 and .004 for the three days respectively. The daily beta for the car maker is .9. What are the three abnormal returns for the car maker's stock?

A) -.002, -.0082, .0005

B) -.002, -.00748, .0005

C) .01, .0062, .0085

D) -.0014, -.00748, .0009

A) -.002, -.0082, .0005

B) -.002, -.00748, .0005

C) .01, .0062, .0085

D) -.0014, -.00748, .0009

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

39

Ritter's study of Initial Public Offerings (IPOs) showed that the post offering stock performance was:

A) less than the control group by about 2% in the five years following the IPO.

B) incorrectly priced at issuance because over the next five years the abnormal returns were greater than zero on average.

C) immaterial to the pricing of the IPO because future market performance is unknown at issuance.

D) equal across IPOs, irrespective of risk or which year they were issued.

A) less than the control group by about 2% in the five years following the IPO.

B) incorrectly priced at issuance because over the next five years the abnormal returns were greater than zero on average.

C) immaterial to the pricing of the IPO because future market performance is unknown at issuance.

D) equal across IPOs, irrespective of risk or which year they were issued.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 39 flashcards in this deck.