Deck 14: Swaps

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Given the following information, does a comparative advantage opportunity exist?

A)Yes - both parties can pay less interest by borrowing where they have a comparative advantage and swapping their interest payments.

B)Yes - the potential savings from entering a swap are 1 per cent.

C)Yes -but a swap would reduce the cost of funds for B only.

D)No.

E)Cannot say with the available information.

A)Yes - both parties can pay less interest by borrowing where they have a comparative advantage and swapping their interest payments.

B)Yes - the potential savings from entering a swap are 1 per cent.

C)Yes -but a swap would reduce the cost of funds for B only.

D)No.

E)Cannot say with the available information.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

What are the potential swap savings given the following comparative advantage?

A)0 per cent

B)0.5 per cent

C)1 per cent

D)2 per cent

E)3 per cent

A)0 per cent

B)0.5 per cent

C)1 per cent

D)2 per cent

E)3 per cent

Question

Question

Question

Question

Question

Which strategy below would take advantage of the following comparative advantage?

A)Company X should borrow fixed and Company Y should borrow floating, then they should swap their interest payments.

B)Company X should borrow floating and Company Y should borrow fixed, then they should swap their interest payments.

C)Company X should borrow fixed and Company Y should borrow floating, but there is no benefit to a entering a swap.

D)Company X should borrow floating and Company Y should borrow fixed, but there is no benefit from entering a swap.

E)There is no opportunity for comparative advantage here.

A)Company X should borrow fixed and Company Y should borrow floating, then they should swap their interest payments.

B)Company X should borrow floating and Company Y should borrow fixed, then they should swap their interest payments.

C)Company X should borrow fixed and Company Y should borrow floating, but there is no benefit to a entering a swap.

D)Company X should borrow floating and Company Y should borrow fixed, but there is no benefit from entering a swap.

E)There is no opportunity for comparative advantage here.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

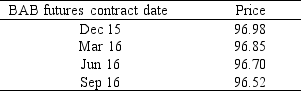

Calculate the approximate one-year swap rate beginning in December 2015 based on the following BAB futures prices:

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/88

Play

Full screen (f)

Deck 14: Swaps

1

The fixed-rate payer's position in a swap would become valuable if interest rates decreased unexpectedly.

False

2

An interest rate swap is the exchange of fixed interest payments for floating interest payments where the two sets of payments have the same overall dollar value.

False

3

BBSW refers to the swap rate in an interest rate swap.

False

4

Swaps have little exposure to default risk.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

5

The swap rate offered by swap dealers must align with the forward rates in the BAB futures market, since a strip of forwards could serve the same purpose as a swap.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

6

Swap dealers need to match each swap-rate paying and swap-rate receiving client.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

7

Swaps are an example of an exchange-traded instrument.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

8

If the BBSW is below the swap rate at the start of the swap period, the fixed-rate payer pays the cash settlement at the end of the payment period.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

9

When a swap is first established at a fair swap rate, its net present value will be zero.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

10

Swap dealers earn commissions on the swaps they write.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

11

In a fixed-for-floating swap, a floating-rate borrower would agree to pay the swap rate, whereas the fixed-rate borrower would agree to receive the swap rate.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

12

The swap rate should result in the present value of the expected payments equalling the present value of the expected receipts.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

13

All swaps are used to manage interest-rate risk posed by financing.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

14

By acting as swap dealers, financial institutions reduce the search costs of parties requiring swap contracts.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

15

The payment obligations in a swap are netted at the end of each swap period, and so only a relatively small cash settlement results.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

16

When there is a normal yield curve, the floating-rate payer will make the initial swap payments and the fixed-rate payer will make the later payments.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

17

A fixed-for-floating interest rate swap is the exchange of payments based on a fixed interest rate for payments based on a floating interest rate.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

18

All swaps require quarterly cash settlements.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

19

Swap contracts have an active secondary market.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

20

An interest-rate swap converts a floating-rate borrower into a fixed-rate borrower.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

21

Credit default swaps are contracts where the protection buyer agrees to pay a fee to the protection seller in return for a specified series of payments.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

22

Swap contracts are risk-transfer instruments that are used to manage risk arising from:

A)the payments system

B)the flow-of-funds

C)incentive problems

D)derivative contracts.

E)All of these.

A)the payments system

B)the flow-of-funds

C)incentive problems

D)derivative contracts.

E)All of these.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

23

An interest rate swap uncouples the source-of-finance decision from the basis of the interest payments.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

24

A plain vanilla interest rate swap:

A)requires the fixed-rate borrower to make fixed-rate swap payments

B)is an arrangement that modifies a borrower's obligation to their lender

C)is the exchange of interest and principal payments

D)requires a floating-interest rate payment calculated using the 'swap rate'

E)is settled by a swap payment which is the difference between the floating- and fixed-rate interest payments calculated on an agreed notional principal.

A)requires the fixed-rate borrower to make fixed-rate swap payments

B)is an arrangement that modifies a borrower's obligation to their lender

C)is the exchange of interest and principal payments

D)requires a floating-interest rate payment calculated using the 'swap rate'

E)is settled by a swap payment which is the difference between the floating- and fixed-rate interest payments calculated on an agreed notional principal.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

25

The swap rate in the overnight indexed swap market can serve to indicate the market's expectation about future changes by the RBA in its target cash rate.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

26

A floating rate borrower who enters an interest rate swap as the fixed-rate payer will:

A)now make fixed rate interest payments to their lender

B)agree to pay fixed interest payments and receive floating interest payments through the swap contract

C)receive swap interest payments based on the swap rate

D)make the swap cash settlement payments when the BBSW exceeds the swap rate.

E)None of these are correct.

A)now make fixed rate interest payments to their lender

B)agree to pay fixed interest payments and receive floating interest payments through the swap contract

C)receive swap interest payments based on the swap rate

D)make the swap cash settlement payments when the BBSW exceeds the swap rate.

E)None of these are correct.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

27

Cross-currency swaps are widely used by banks to manage the exchange rate risk on their foreign debt.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

28

During the term of a swap, whenever interest rates vary unexpectedly, the swap will develop value for one swap party or the other.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

29

For a floating rate borrower wishing to hedge an exposure to higher than expected spot rates, interest rate swaps lock in varying forward rates in the same way as a strip of FRAs or a strip of BAB futures.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

30

A cross-currency swap exchanges the interest payments only associated with a foreign currency loan.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

31

Credit derivatives are instruments or agreements that transfer price risk between the risk seller and the risk buyer.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

32

A comparative advantage can arise when the effect of a superior credit rating differs in different markets.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

33

Swap contracts can be used to manage various risks including:

A)interest-rate risk

B)foreign exchange risk

C)credit risk

D)an exposure to the cash rate.

E)All of these.

A)interest-rate risk

B)foreign exchange risk

C)credit risk

D)an exposure to the cash rate.

E)All of these.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

34

The effective interest rate payable by a floating rate borrower who has become the fixed rate payer in a swap is the swap rate.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

35

Non-financial companies are the biggest users of swaps.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

36

The fixed rate in the OIS market will be above the current cash rate when the market expects the RBA to reduce the cash rate.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

37

The exchange rate used to swap payments in a cross-currency swap will be adjusted throughout the swap's term.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

38

Identify the correct statement regarding a plain vanilla swap.

A)Interest and principal payments are exchanged at the beginning of the swap.

B)The net settlement is a single payment at the end of the swap term.

C)The fixed-rate payments are set equal to the expected floating-rate payments.

D)The flow of payments between parties may change direction during the life of the swap.

E)There is no default risk involved in a plain vanilla swap.

A)Interest and principal payments are exchanged at the beginning of the swap.

B)The net settlement is a single payment at the end of the swap term.

C)The fixed-rate payments are set equal to the expected floating-rate payments.

D)The flow of payments between parties may change direction during the life of the swap.

E)There is no default risk involved in a plain vanilla swap.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

39

Credit default swaps inflicted large losses on Australian banks during the GFC.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

40

One reason that comparative advantage may occur in debt markets is that fixed-rate investors could be less sensitive to credit risk than floating rate lenders and acceptors.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

41

What type of swap arrangement is commonly used by Australian banks to manage their exchange rate risk on foreign bond issues?

A)Fixed-for-floating swap

B)Overnight indexed swaps

C)Cross-currency swaps

D)Credit default swaps

E)FX swaps

A)Fixed-for-floating swap

B)Overnight indexed swaps

C)Cross-currency swaps

D)Credit default swaps

E)FX swaps

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

42

Given the following information, does a comparative advantage opportunity exist?

A)Yes - both parties can pay less interest by borrowing where they have a comparative advantage and swapping their interest payments.

B)Yes - the potential savings from entering a swap are 1 per cent.

C)Yes -but a swap would reduce the cost of funds for B only.

D)No.

E)Cannot say with the available information.

A)Yes - both parties can pay less interest by borrowing where they have a comparative advantage and swapping their interest payments.

B)Yes - the potential savings from entering a swap are 1 per cent.

C)Yes -but a swap would reduce the cost of funds for B only.

D)No.

E)Cannot say with the available information.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

43

The swap rate in a plain vanilla swap:

A)is the rate paid by the floating-rate payer

B)may require interest payments in a foreign currency

C)is an exact average of the forward rates

D)is a multi-period fixed rate

E)is set at the commencement of each swap period.

A)is the rate paid by the floating-rate payer

B)may require interest payments in a foreign currency

C)is an exact average of the forward rates

D)is a multi-period fixed rate

E)is set at the commencement of each swap period.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following is NOT a reason for entering a plain vanilla swap?

A)To provide a cheaper method of raising funds than borrowing in the preferred market.

B)To achieve a lower overall borrowing rate.

C)To hedge an interest rate exposure.

D)To hedge an exchange rate exposure.

E)None of these.

A)To provide a cheaper method of raising funds than borrowing in the preferred market.

B)To achieve a lower overall borrowing rate.

C)To hedge an interest rate exposure.

D)To hedge an exchange rate exposure.

E)None of these.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

45

If a floating rate borrower hedges their interest rate risk by entering a swap as the fixed rate payer, and the swap subsequently develops a negative value:

A)then the swap has not been an effective hedge

B)the cost of funds for the borrower will rise

C)then the borrower has paid lower than expected interest to their lender

D)the cost of funds will exceed the swap rate

E)then the borrower has paid higher than expected interest to their lender.

A)then the swap has not been an effective hedge

B)the cost of funds for the borrower will rise

C)then the borrower has paid lower than expected interest to their lender

D)the cost of funds will exceed the swap rate

E)then the borrower has paid higher than expected interest to their lender.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

46

In a fixed-for-floating interest rate swap:

A)if the BBSW is lower than expected, the swap develops a positive value for the floating-rate payer

B)if the BBSW is higher than expected, the swap develops a positive value for the floating-rate payer

C)if the BBSW is lower than expected, the swap develops a positive value for the fixed-rate payer

D)if the BBSW is higher than expected, the swap develops a negative value for the fixed-rate payer

E)if the BBSW is higher than the swap rate, the cash settlement is paid by the fixed-rate payer.

A)if the BBSW is lower than expected, the swap develops a positive value for the floating-rate payer

B)if the BBSW is higher than expected, the swap develops a positive value for the floating-rate payer

C)if the BBSW is lower than expected, the swap develops a positive value for the fixed-rate payer

D)if the BBSW is higher than expected, the swap develops a negative value for the fixed-rate payer

E)if the BBSW is higher than the swap rate, the cash settlement is paid by the fixed-rate payer.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following statements is FALSE?

A)The fixed rate in the OIS market can be expected to be above the current cash rate when the market expects the RBA will increase the cash rate.

B)An OIS is used by parties who have an exposure to the cash rate.

C)Most OISs have terms of six months or less.

D)The cash settlement in an OIS swap, if any, is made when the swap matures.

E)None of these.

A)The fixed rate in the OIS market can be expected to be above the current cash rate when the market expects the RBA will increase the cash rate.

B)An OIS is used by parties who have an exposure to the cash rate.

C)Most OISs have terms of six months or less.

D)The cash settlement in an OIS swap, if any, is made when the swap matures.

E)None of these.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

48

The main users of swaps are:

A)households

B)small business

C)large companies

D)banks

E)the Commonwealth government.

A)households

B)small business

C)large companies

D)banks

E)the Commonwealth government.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

49

If the yield curve is inverse, in a newly arranged interest rate swap:

A)the floating-rate payer will expect to receive the first swap cash settlement

B)the first swap cash settlement is expected to be zero

C)the swap cash settlements are expected to increase each period

D)the fixed rate payer will expect to pay the later swap cash settlements

E)the cash settlements will be expected to fluctuate randomly from quarter to quarter.

A)the floating-rate payer will expect to receive the first swap cash settlement

B)the first swap cash settlement is expected to be zero

C)the swap cash settlements are expected to increase each period

D)the fixed rate payer will expect to pay the later swap cash settlements

E)the cash settlements will be expected to fluctuate randomly from quarter to quarter.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

50

The timing of plain vanilla swap payments is generally:

A)at the end of the swap period (i.e.in arrears)

B)quarterly for plain-vanilla swaps with terms up to three years

C)half-yearly for plain-vanilla swaps with terms more than three years

D)in arrears, but uses the BBSW at the start of the swap period.

E)All of these are correct.

A)at the end of the swap period (i.e.in arrears)

B)quarterly for plain-vanilla swaps with terms up to three years

C)half-yearly for plain-vanilla swaps with terms more than three years

D)in arrears, but uses the BBSW at the start of the swap period.

E)All of these are correct.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

51

Cross-currency swaps do NOT involve:

A)The exchange of principal at the start of the loan.

B)The exchange of fixed local currency interest payments for floating foreign currency interest payments.

C)A fixed exchange rate for the swap's term.

D)The exchange of floating local currency interest payments for floating foreign currency interest payments.

E)The exchange of principal at the end of the loan.

A)The exchange of principal at the start of the loan.

B)The exchange of fixed local currency interest payments for floating foreign currency interest payments.

C)A fixed exchange rate for the swap's term.

D)The exchange of floating local currency interest payments for floating foreign currency interest payments.

E)The exchange of principal at the end of the loan.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

52

What are the potential swap savings given the following comparative advantage?

A)0 per cent

B)0.5 per cent

C)1 per cent

D)2 per cent

E)3 per cent

A)0 per cent

B)0.5 per cent

C)1 per cent

D)2 per cent

E)3 per cent

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is NOT a reason advanced for the existence of comparative advantages within financial markets?

A)The imposition of larger credit risk premiums by long-term investors, relative to those imposed by shorter-term investors.

B)Smaller credit risk premiums are appropriate in short-term financing because of the shorter repayment period.

C)Taxes and regulation may impact borrowers differently.

D)Indifference regarding the risk profile of borrowers in some markets.

E)Some borrowers will have a 'home-ground advantage'.

A)The imposition of larger credit risk premiums by long-term investors, relative to those imposed by shorter-term investors.

B)Smaller credit risk premiums are appropriate in short-term financing because of the shorter repayment period.

C)Taxes and regulation may impact borrowers differently.

D)Indifference regarding the risk profile of borrowers in some markets.

E)Some borrowers will have a 'home-ground advantage'.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

54

Suppose the swap rate is 8% and the BBSW is 11% for the first quarter.Given that the amount hedged is $50 million, which of the following statements is true about the swap settlement? (Assume d/diy = 0.25)

A)The fixed rate payer pays the floating rate payer $375 000.

B)The floating rate payer pays the fixed rate payer $375 000.

C)The fixed rate payer pays the floating rate payer $4 million.

D)The floating rate payer pays the fixed rate payer $4 million.

E)The obligations of each party are zero in this quarter.

A)The fixed rate payer pays the floating rate payer $375 000.

B)The floating rate payer pays the fixed rate payer $375 000.

C)The fixed rate payer pays the floating rate payer $4 million.

D)The floating rate payer pays the fixed rate payer $4 million.

E)The obligations of each party are zero in this quarter.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

55

Given a normal yield curve, the swap rate will be:

A)just above the average of the forward rates

B)above the BBSW expected in the first period

C)equal to the BBSW expected in the first period

D)below the BBSW expected in the first period.

E)More than one of these is correct.

A)just above the average of the forward rates

B)above the BBSW expected in the first period

C)equal to the BBSW expected in the first period

D)below the BBSW expected in the first period.

E)More than one of these is correct.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

56

A swap arrangement where the floating payment is the average cash rate over the swap term is called:

A)a credit default swap

B)a fixed-for-floating interest rate swap

C)an overnight indexed swap

D)a currency swap

E)a plain vanilla interest rate swap.

A)a credit default swap

B)a fixed-for-floating interest rate swap

C)an overnight indexed swap

D)a currency swap

E)a plain vanilla interest rate swap.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

57

Which strategy below would take advantage of the following comparative advantage?

A)Company X should borrow fixed and Company Y should borrow floating, then they should swap their interest payments.

B)Company X should borrow floating and Company Y should borrow fixed, then they should swap their interest payments.

C)Company X should borrow fixed and Company Y should borrow floating, but there is no benefit to a entering a swap.

D)Company X should borrow floating and Company Y should borrow fixed, but there is no benefit from entering a swap.

E)There is no opportunity for comparative advantage here.

A)Company X should borrow fixed and Company Y should borrow floating, then they should swap their interest payments.

B)Company X should borrow floating and Company Y should borrow fixed, then they should swap their interest payments.

C)Company X should borrow fixed and Company Y should borrow floating, but there is no benefit to a entering a swap.

D)Company X should borrow floating and Company Y should borrow fixed, but there is no benefit from entering a swap.

E)There is no opportunity for comparative advantage here.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

58

Identify the CORRECT statement below regarding an overnight indexed swap (OIS).

A)Interest and principal payments are exchanged at the beginning of the swap.

B)The net settlement is a single payment at the end of the swap term.

C)The fixed-rate payments are set to be equal to the cash rate.

D)OISs are usually long-term arrangements.

E)OISs are used to hedge an exposure to money-market yields.

A)Interest and principal payments are exchanged at the beginning of the swap.

B)The net settlement is a single payment at the end of the swap term.

C)The fixed-rate payments are set to be equal to the cash rate.

D)OISs are usually long-term arrangements.

E)OISs are used to hedge an exposure to money-market yields.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

59

In what type of swap contract is the loan principal exchanged?

A)All swap arrangements

B)Fixed-for-floating swap

C)Overnight indexed swaps

D)Cross-currency swaps

E)Credit default swaps

A)All swap arrangements

B)Fixed-for-floating swap

C)Overnight indexed swaps

D)Cross-currency swaps

E)Credit default swaps

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

60

Swap dealers:

A)charge an up-front fee for arranging a swap

B)reduce the search costs of parties requiring swap transactions

C)sell standardised, liquid swap contracts

D)act as agents for swap parties, not as counterparties.

E)All of these are correct.

A)charge an up-front fee for arranging a swap

B)reduce the search costs of parties requiring swap transactions

C)sell standardised, liquid swap contracts

D)act as agents for swap parties, not as counterparties.

E)All of these are correct.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

61

What type of swap contract played a significant role in the GFC?

A)All swap arrangements

B)Fixed-for-floating swap

C)Overnight indexed swaps

D)Cross-currency swaps

E)Credit default swaps

A)All swap arrangements

B)Fixed-for-floating swap

C)Overnight indexed swaps

D)Cross-currency swaps

E)Credit default swaps

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

62

TDK Industries approaches a bank in April to organise financing through a 180-day bank bill facility.The facility will begin in June, using 90-day bank bills with a total face value of $10 million.The company wishes to know what they can do now to hedge against interest rate risk.The June six-month swap rate is 4.5%, and it turns out that the 90-day BBR is 4% in June and 5% in September.Calculate the effective interest rate established for the duration of the bill facility, through the use of a swap contract.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

63

Given an inverse yield curve, would the fixed-rate payer in a plain vanilla swap expect to pay or receive the first net swap payment.Why?

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

64

What type of swap arrangement is most like an insurance policy?

A)All swap arrangements

B)Fixed-for-floating swap

C)Overnight indexed swaps

D)Cross-currency swaps

E)Credit default swaps

A)All swap arrangements

B)Fixed-for-floating swap

C)Overnight indexed swaps

D)Cross-currency swaps

E)Credit default swaps

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

65

Explain how opportunities for comparative advantage may arise.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

66

Suppose that a fixed-rate borrower (A)has to repay $50 million at an interest rate of 5% p.a., and a floating-rate borrower (B)has to repay $50 million at rates similar to the BBSW.These parties enter into a two-quarter swap arrangement with an agreed principal of $50 million and a swap rate of 5% per annum.At the commencement of each quarter, the BBSW rates are 4% and 5.75% p.a.respectively.

A.Calculate the net settlement payments under the swap.(Use d/diy = 0.25)

B.Show how the fixed-rate borrower becomes a floating-rate payer.

C.Show how the floating-rate borrower becomes a fixed-rate payer.

A.Calculate the net settlement payments under the swap.(Use d/diy = 0.25)

B.Show how the fixed-rate borrower becomes a floating-rate payer.

C.Show how the floating-rate borrower becomes a fixed-rate payer.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

67

How can OIS rates be interpreted as the market's view regarding the level of cash rates in the future?

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

68

Describe how a swap converts a floating-rate payer into a fixed-rate payer, and vice versa.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

69

Compare the features of a plain vanilla swap with those of a cross-currency swap.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

70

Why can parties enter a plain vanilla interest rate swap without paying for the privilege?

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

71

Compare the hedging outcome of a strip of FRAs or futures contracts to that of a fixed-rate payer in a swap contract.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

72

Explain the main features and use of overnight indexed swaps.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

73

Calculate the approximate one-year swap rate beginning in December 2015 based on the following BAB futures prices:

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

74

Describe the main features of a fixed-for-floating (plain vanilla)interest rate swap.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

75

Why might an ADI that has raised funds in the bond market wish to enter a fixed-for-floating interest rate swap as the floating-rate payer?

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

76

Black Corporation, a large Australian company, can borrow funds at the BBSW+60bps in the money market or at 8% fixed in the corporate bond market.It prefers a fixed rate exposure.Blue Bank can borrow at the BBSW by issuing CDs at the BBSW or at 6.8% fixed, and prefers a floating rate exposure.Is there a comparative advantage opportunity and if so, how can it be exploited?

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

77

How does a borrower who desires a swap contract find a counterparty with whom to swap interest payments with?

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

78

Black Corporation, a large Australian company, can borrow funds at the BBSW+60bps in the money market or at 8% fixed in the corporate bond market.It prefers a fixed rate exposure.Blue Bank can borrow at the BBSW by issuing CDs or at 6.8% fixed and prefers a floating rate exposure.Explain how a swap can be arranged to the advantage of both parties assuming savings are evenly shared.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

79

A one year interest rate swap with quarterly settlements is agreed at a swap rate of 7.5% p.a.on a notional principal of $1 million.Given the BBSW at the start of each quarter is 8%, 9.5%, 7% and 7.5% respectively throughout the year, calculate the swap cash settlements and indicate whether the settlement is payable by the fixed-rate or floating-rate payer in the swap.(Use d/diy = 0.25)

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

80

Suppose that the two-year swap rate is currently 6 per cent and that you are interested in entering an interest rate swap as the fixed-rate payer.How could you check whether the rate is fair?

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 88 flashcards in this deck.