Deck 24: Translation of Foreign Currency Statements

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

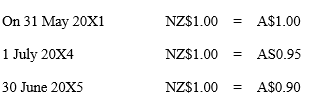

Ozzie Ltd has control over Islander Ltd.The functional currency of Islander Ltd is the NZ$.On 31 May 20X1 Islander Ltd borrowed NZ$15 million.Ozzie Ltd uses the A$ as its presentation currency.The following spot rates applied.

Which of the following is not given in the text as a reasons for allocating FCT reserve proportionately between parent entity owners and non-controlling interest (NCI):

A)translation involves a data adjustment preceding the consolidation process that involves the owners equity of the foreign operation, and should therefore be allocated to both MI and parent entity

B)to do so is consistent with the concept of control underlying the consolidation process.

C)it is more neutral and consistent with the entity view of the consolidation process

D)that the analogy with consolidation difference is not persuasive

Which of the following is not given in the text as a reasons for allocating FCT reserve proportionately between parent entity owners and non-controlling interest (NCI):

A)translation involves a data adjustment preceding the consolidation process that involves the owners equity of the foreign operation, and should therefore be allocated to both MI and parent entity

B)to do so is consistent with the concept of control underlying the consolidation process.

C)it is more neutral and consistent with the entity view of the consolidation process

D)that the analogy with consolidation difference is not persuasive

Question

Question

Question

Question

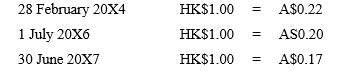

Aus Ltd has control over Hong Ltd.The functional currency of Hong Ltd is HK$, its domestic currency.On 28 February 20X4 Hong Ltd purchased a building for HK$8 million.Aus Ltd uses its domestic currency, the A$, as its presentation currency.

The relevant spot rates are:

What is the amount of this building in Aus Ltd's consolidated financial statements for the reporting period ending 30 June 20X7?

A)$1 600 000

B)$1 360 000

C)$10 000 000

D)$2 000 000

The relevant spot rates are:

What is the amount of this building in Aus Ltd's consolidated financial statements for the reporting period ending 30 June 20X7?

A)$1 600 000

B)$1 360 000

C)$10 000 000

D)$2 000 000

Question

Aus Ltd has control over Hong Ltd.The functional currency of Hong Ltd is HK$, its domestic currency.On 28 February 20X4 Hong Ltd purchased a building for HK$8 million.Aus Ltd uses its domestic currency, the A$, as its presentation currency.

The relevant spot rates are:

What is the exchange difference recognised in the reporting period ending 30 June 20X7 on translation of the building's carrying amount and how is it recognised?

A)$240 000 expense included in period profit or loss

B)$400 000 expense included in period profit or loss

C)$400 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

D)$240 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

The relevant spot rates are:

What is the exchange difference recognised in the reporting period ending 30 June 20X7 on translation of the building's carrying amount and how is it recognised?

A)$240 000 expense included in period profit or loss

B)$400 000 expense included in period profit or loss

C)$400 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

D)$240 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/19

Play

Full screen (f)

Deck 24: Translation of Foreign Currency Statements

1

Under AASB 121, the process of translation of the financial statements of a foreign operations involves:

A)converting from the functional currency of the foreign operation into the parent entity's functional currency

B)converting from the parent entity's functional currency into the functional currency of the foreign operation

C)converting from the functional currency of the foreign operation into the presentation currency used in the parent entity's consolidated financial statements

D)converting from the domestic currency of the foreign operation into the parent entity's functional currency

A)converting from the functional currency of the foreign operation into the parent entity's functional currency

B)converting from the parent entity's functional currency into the functional currency of the foreign operation

C)converting from the functional currency of the foreign operation into the presentation currency used in the parent entity's consolidated financial statements

D)converting from the domestic currency of the foreign operation into the parent entity's functional currency

C

2

Little Ozzie Battlefield Equipment Ltd acquired 100% ownership of BigTrench plc for A$18 million on 1 July 20X4.At that date net fair value of the identifiable assets and liabilities of BigTrench plc were €10 million.The following exchange rates are given:

-At the control date

A)goodwill of €18 800 000 is recognised which translates to A$11 750 000

B)goodwill of €1 250 000 is recognised which translates to A$2 000 000

C)goodwill is recognised at A$2 000 000

D)goodwill is recognised at A$11 750 000

-At the control date

A)goodwill of €18 800 000 is recognised which translates to A$11 750 000

B)goodwill of €1 250 000 is recognised which translates to A$2 000 000

C)goodwill is recognised at A$2 000 000

D)goodwill is recognised at A$11 750 000

goodwill of €1 250 000 is recognised which translates to A$2 000 000

3

Little Ozzie Battlefield Equipment Ltd acquired 100% ownership of BigTrench plc for A$18 million on 1 July 20X4.At that date net fair value of the identifiable assets and liabilities of BigTrench plc were €10 million.The following exchange rates are given:

-For the reporting period ending 30 June 20X6 the consolidated financial statements of Little Ozzie Battlefield Equipment Ltd will show

A)goodwill of A$1 875 000 and a translation difference expense of A$312 500 which is recognised as other comprehensive profit

B)goodwill of A$2 000 000 and a translation difference expense of A$312 500 which is recognised as other comprehensive profit

C)goodwill of A$1 875 000 and a translation difference expense of A$125 000 which is recognised as other comprehensive profit

D)goodwill of A$1 875 000 and a translation difference revenue of A$312 500 which is recognised as other comprehensive profit

-For the reporting period ending 30 June 20X6 the consolidated financial statements of Little Ozzie Battlefield Equipment Ltd will show

A)goodwill of A$1 875 000 and a translation difference expense of A$312 500 which is recognised as other comprehensive profit

B)goodwill of A$2 000 000 and a translation difference expense of A$312 500 which is recognised as other comprehensive profit

C)goodwill of A$1 875 000 and a translation difference expense of A$125 000 which is recognised as other comprehensive profit

D)goodwill of A$1 875 000 and a translation difference revenue of A$312 500 which is recognised as other comprehensive profit

goodwill of A$1 875 000 and a translation difference expense of A$312 500 which is recognised as other comprehensive profit

4

The presentation currency for consolidated financial statements must be the same as the presentation currency for the parent entity's financial statements.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

5

Prior Ltd controls Before Ltd.Prior Ltd's consolidated financial statements will recognise foreign exchange fluctuations on translation of Before Ltd's financial statements:

A)in a foreign currency translation (FCT) reserve account

B)in retained earnings

C)as part of the period profit or loss

D)as an extraordinary gain or loss

A)in a foreign currency translation (FCT) reserve account

B)in retained earnings

C)as part of the period profit or loss

D)as an extraordinary gain or loss

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

6

The method used to translate the financial statements relating to a foreign operation depends on the nature of the relationship between the parent entity and the foreign operation.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

7

Little Ozzie Battlefield Equipment Ltd acquired 100% ownership of BigTrench plc for A$18 million on 1 July 20X4.At that date net fair value of the identifiable assets and liabilities of BigTrench plc were €10 million.The following exchange rates are given:

-At 30 June 20X5

A)goodwill is recognised at A$11 750 000

B)goodwill of €1 250 000 is recognised which translates to A$714 286

C)goodwill is recognised at A$2 000 000

D)goodwill of €1 250 000 is recognised which translates to A$2 187 500

-At 30 June 20X5

A)goodwill is recognised at A$11 750 000

B)goodwill of €1 250 000 is recognised which translates to A$714 286

C)goodwill is recognised at A$2 000 000

D)goodwill of €1 250 000 is recognised which translates to A$2 187 500

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

8

Ozzie Ltd has control over Islander Ltd.The functional currency of Islander Ltd is the NZ$.On 31 May 20X1 Islander Ltd borrowed NZ$15 million.Ozzie Ltd uses the A$ as its presentation currency.The following spot rates applied.

Which of the following is not given in the text as a reasons for allocating FCT reserve proportionately between parent entity owners and non-controlling interest (NCI):

A)translation involves a data adjustment preceding the consolidation process that involves the owners equity of the foreign operation, and should therefore be allocated to both MI and parent entity

B)to do so is consistent with the concept of control underlying the consolidation process.

C)it is more neutral and consistent with the entity view of the consolidation process

D)that the analogy with consolidation difference is not persuasive

Which of the following is not given in the text as a reasons for allocating FCT reserve proportionately between parent entity owners and non-controlling interest (NCI):

A)translation involves a data adjustment preceding the consolidation process that involves the owners equity of the foreign operation, and should therefore be allocated to both MI and parent entity

B)to do so is consistent with the concept of control underlying the consolidation process.

C)it is more neutral and consistent with the entity view of the consolidation process

D)that the analogy with consolidation difference is not persuasive

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

9

The impact of translating transactions and financial statements from one currency into another:

A)is included in determining period profit or loss in both cases

B)is normally included in period profit and loss for transactions, but for financial statements is recognised as other comprehensive profit and accumulated in a reserve called the foreign currency translation (FCT) reserve in chapter 24

C)is normally included in period profit and loss for transactions, but is recognised as other comprehensive profit through retained profits for financial statements

D)are both recognised directly as other comprehensive profit, with transactions recognised in retained profits and for financial statement in a reserve called the FCT reserve in chapter 24

A)is included in determining period profit or loss in both cases

B)is normally included in period profit and loss for transactions, but for financial statements is recognised as other comprehensive profit and accumulated in a reserve called the foreign currency translation (FCT) reserve in chapter 24

C)is normally included in period profit and loss for transactions, but is recognised as other comprehensive profit through retained profits for financial statements

D)are both recognised directly as other comprehensive profit, with transactions recognised in retained profits and for financial statement in a reserve called the FCT reserve in chapter 24

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

10

Under AASB 121 which of the following is not expressly required when translating financial statements:

A)amounts for assets and liabilities in balance sheet are translated using the spot rate at reporting date

B)owner's equity items are all translated at the spot rate at the date of the relevant event

C)the amounts for income (revenues and gains) and expenses are translated at the spot rate on the date of the transaction - average rates can be used if the exchange rate does not fluctuate significantly

D)all resulting exchange differences are recognised as a separate component of equity

A)amounts for assets and liabilities in balance sheet are translated using the spot rate at reporting date

B)owner's equity items are all translated at the spot rate at the date of the relevant event

C)the amounts for income (revenues and gains) and expenses are translated at the spot rate on the date of the transaction - average rates can be used if the exchange rate does not fluctuate significantly

D)all resulting exchange differences are recognised as a separate component of equity

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

11

Little Ozzie Battlefield Equipment Ltd acquired 100% ownership of BigTrench plc for A$18 million on 1 July 20X4.At that date net fair value of the identifiable assets and liabilities of BigTrench plc were €10 million.The following exchange rates are given:

-For the reporting period ending 30 June 20X5 the consolidated financial statements of Little Ozzie Battlefield Equipment Ltd will show

A)goodwill of A$2 187 500 and a translation difference expense of A$187 500 recognised as other comprehensive profit

B)goodwill of A$2 187 500 and a translation difference of A$187 500 recognised in period profit or loss

C)goodwill of A$2 187 500 and a translation difference revenue of A$187 500 recognised as other comprehensive profit.

D)goodwill of A$2 187 500 and a translation difference expense of A$187 500 recognised as other comprehensive profit.

-For the reporting period ending 30 June 20X5 the consolidated financial statements of Little Ozzie Battlefield Equipment Ltd will show

A)goodwill of A$2 187 500 and a translation difference expense of A$187 500 recognised as other comprehensive profit

B)goodwill of A$2 187 500 and a translation difference of A$187 500 recognised in period profit or loss

C)goodwill of A$2 187 500 and a translation difference revenue of A$187 500 recognised as other comprehensive profit.

D)goodwill of A$2 187 500 and a translation difference expense of A$187 500 recognised as other comprehensive profit.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

12

Aus Ltd has control over Hong Ltd.The functional currency of Hong Ltd is HK$, its domestic currency.On 28 February 20X4 Hong Ltd purchased a building for HK$8 million.Aus Ltd uses its domestic currency, the A$, as its presentation currency.

The relevant spot rates are:

What is the amount of this building in Aus Ltd's consolidated financial statements for the reporting period ending 30 June 20X7?

A)$1 600 000

B)$1 360 000

C)$10 000 000

D)$2 000 000

The relevant spot rates are:

What is the amount of this building in Aus Ltd's consolidated financial statements for the reporting period ending 30 June 20X7?

A)$1 600 000

B)$1 360 000

C)$10 000 000

D)$2 000 000

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

13

Aus Ltd has control over Hong Ltd.The functional currency of Hong Ltd is HK$, its domestic currency.On 28 February 20X4 Hong Ltd purchased a building for HK$8 million.Aus Ltd uses its domestic currency, the A$, as its presentation currency.

The relevant spot rates are:

What is the exchange difference recognised in the reporting period ending 30 June 20X7 on translation of the building's carrying amount and how is it recognised?

A)$240 000 expense included in period profit or loss

B)$400 000 expense included in period profit or loss

C)$400 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

D)$240 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

The relevant spot rates are:

What is the exchange difference recognised in the reporting period ending 30 June 20X7 on translation of the building's carrying amount and how is it recognised?

A)$240 000 expense included in period profit or loss

B)$400 000 expense included in period profit or loss

C)$400 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

D)$240 000 expense recognised as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

14

Ozzie Ltd has control over Islander Ltd.The functional currency of Islander Ltd is the NZ$.On 31 May 20X1 Islander Ltd borrowed NZ$15 million.Ozzie Ltd uses the A$ as its presentation currency.The following spot rates applied.

On 31 May 20X1 NZ

1 July 20X4 NZ AS0.95

30 June 20X5

-At what amount will the loan be reported in Ozzie's consolidated financial statements for the reporting period ending 30 June 20X5?

A)$15 000 000

B)$14 250 000

C)$15 789 474

D)$13 500 000

On 31 May 20X1 NZ

1 July 20X4 NZ AS0.95

30 June 20X5

-At what amount will the loan be reported in Ozzie's consolidated financial statements for the reporting period ending 30 June 20X5?

A)$15 000 000

B)$14 250 000

C)$15 789 474

D)$13 500 000

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

15

AASB 121 regulates the hedging of the net investment in a foreign operation but not the hedging of individual transactions denominated in a foreign currency.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

16

Ozzie Ltd has control over Islander Ltd.The functional currency of Islander Ltd is the NZ$.On 31 May 20X1 Islander Ltd borrowed NZ$15 million.Ozzie Ltd uses the A$ as its presentation currency.The following spot rates applied.

On 31 May 20X1 NZ

1 July 20X4 NZ AS0.95

30 June 20X5

-What is exchange difference on translation of the loan and how is it recognised in Ozzie's financial statements:

A)$750 000 revenue included in period profit or loss

B)$750 000 revenue recognised other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

C)$750 000 expense recognised other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

D)$1 500 000 revenue as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

On 31 May 20X1 NZ

1 July 20X4 NZ AS0.95

30 June 20X5

-What is exchange difference on translation of the loan and how is it recognised in Ozzie's financial statements:

A)$750 000 revenue included in period profit or loss

B)$750 000 revenue recognised other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

C)$750 000 expense recognised other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

D)$1 500 000 revenue as other comprehensive profit and accumulated in the reserve called the FCT reserve in chapter 24

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

17

Under AASB 121 when an entity gains control of a foreign operation, the amount of the goodwill is measured in the functional currency of the foreign operation, not the functional currency of the parent.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

18

The nature and purpose of the foreign currency translation reserve are both fully explained in AASB 121.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following most nearly reflects the requirements of AASB 121?

A)The presentation currency must be the A$.

B)When the presentation currency is other than the A$, the reason and justification must be disclosed.

C)When the presentation currency is other than the A$, the reason must be disclosed.

D)No limitation is placed on the selection of the presentation currency.

A)The presentation currency must be the A$.

B)When the presentation currency is other than the A$, the reason and justification must be disclosed.

C)When the presentation currency is other than the A$, the reason must be disclosed.

D)No limitation is placed on the selection of the presentation currency.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 19 flashcards in this deck.