Deck 5: Consolidation of Non-Wholly Owned Subsidiaries

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

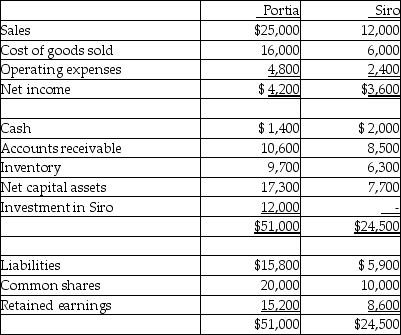

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What amount should be shown on the consolidated statement of financial position for the non-controlling interest at December 31, 20X1?

A)$ 720

B)$1,720

C)$3,480

D)$3,720

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What amount should be shown on the consolidated statement of financial position for the non-controlling interest at December 31, 20X1?

A)$ 720

B)$1,720

C)$3,480

D)$3,720

Question

Question

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What portion of consolidated net income for 20X1 is attributable to Portia?

A)$6,120

B)$6,240

C)$6,600

D)$7,080

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What portion of consolidated net income for 20X1 is attributable to Portia?

A)$6,120

B)$6,240

C)$6,600

D)$7,080

Question

Question

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What is Portia's consolidated cost of goods sold for 20X1?

A)$13,800

B)$16,200

C)$16,800

D)$22,000

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What is Portia's consolidated cost of goods sold for 20X1?

A)$13,800

B)$16,200

C)$16,800

D)$22,000

Question

Question

Question

Question

Question

Question

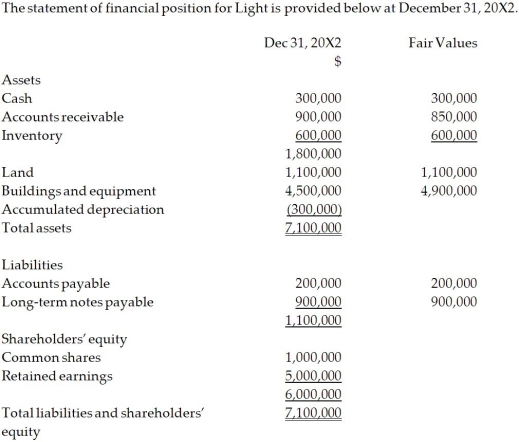

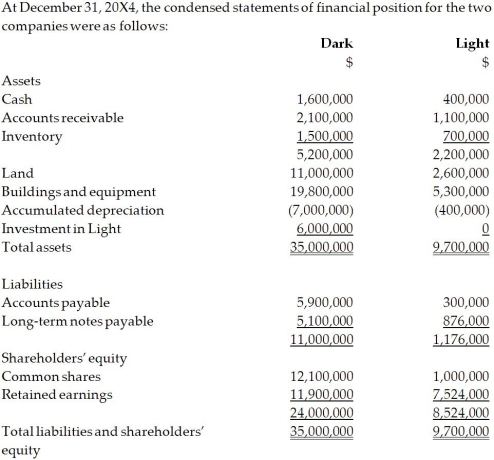

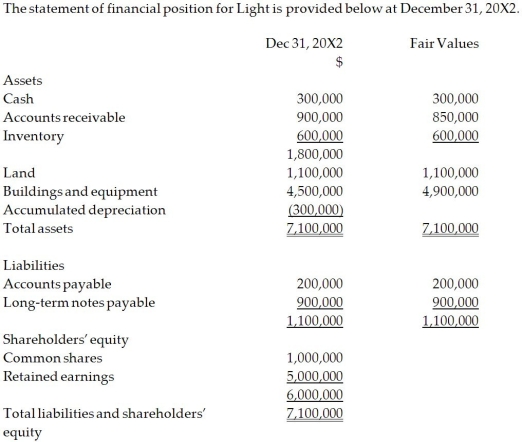

On December 31, 20X2, Dark Company purchased 75% of the outstanding common shares of Light Company for $6.0 million in cash. On that date, the shareholders' equity of Light totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization.  For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

OTHER INFORMATION:

OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000 while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the non-controlling interest on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Calculate the NCI's share of earnings for 20X4.

For the year ending December , the statements of comprehensive income for Dark and Light were as follows: OTHER INFORMATION:1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000 while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the non-controlling interest on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Calculate the NCI's share of earnings for 20X4.

Question

Question

Question

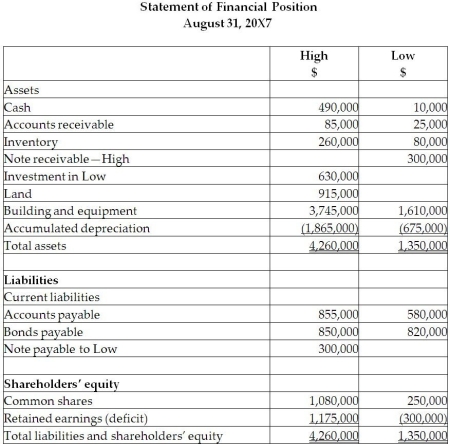

On September 1, 20X5, High Limited decided to buy 80% of the shares outstanding of Low Inc. for $630,000. High will pay for this acquisition by using cash of $500,000 and issuing share capital for the remaining amount. The balances showing on the statement of financial position for the two companies at August 31, 20X5, are as follows:

After a review of the assets and liabilities, High determines that some of the assets of Low have fair values different from their carrying values. These items are listed below:

• Land has a fair value of $295,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Brand value is $60,000. The brand has an indefinite life.

During the 20X7 fiscal year, the following events occurred:

1. On March 1, 20X7, Low sold land to High for $390,000, which had a carrying value of $275,000. High paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. High sold inventory (included in High sales)to Low for $200,000. Profit margin on these sales is 25%. Low still has supplies on hand of $75,000.

3. In 20X6, Low had provided seat space on flights to High for a value of $500,000. This amount was included in sales for Low. Profit margin on these sales is 40%. At the end of August, 20X6, High still had an amount of $200,000 in these prepaid seats that had not yet been used. (High includes this in inventory.)

4. The brand name was found to be impaired and an impairment loss of $40,000 was recognized. Required:

Required:

Calculate the balances for the following consolidated balances of High assuming High uses the parent-company extension method approach:

a. Goodwill at August 31, 20X5

b. Retained earnings at August 31, 20X7

c. Brand name, net, at August 31, 20X7.

After a review of the assets and liabilities, High determines that some of the assets of Low have fair values different from their carrying values. These items are listed below:

• Land has a fair value of $295,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Brand value is $60,000. The brand has an indefinite life.

During the 20X7 fiscal year, the following events occurred:

1. On March 1, 20X7, Low sold land to High for $390,000, which had a carrying value of $275,000. High paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. High sold inventory (included in High sales)to Low for $200,000. Profit margin on these sales is 25%. Low still has supplies on hand of $75,000.

3. In 20X6, Low had provided seat space on flights to High for a value of $500,000. This amount was included in sales for Low. Profit margin on these sales is 40%. At the end of August, 20X6, High still had an amount of $200,000 in these prepaid seats that had not yet been used. (High includes this in inventory.)

4. The brand name was found to be impaired and an impairment loss of $40,000 was recognized.

Required:Calculate the balances for the following consolidated balances of High assuming High uses the parent-company extension method approach:

a. Goodwill at August 31, 20X5

b. Retained earnings at August 31, 20X7

c. Brand name, net, at August 31, 20X7.

Question

Question

Question

Question

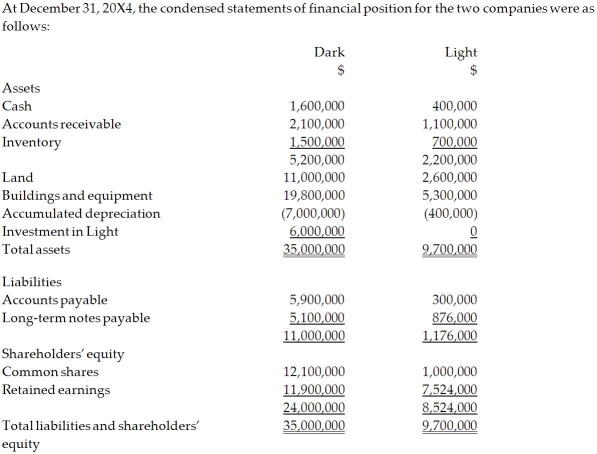

On December 31, 20X2, Dark Company purchased 75% of the outstanding common shares of Light Company for $6.0 million in cash. On that date, the shareholders' equity of Light totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization.  For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

OTHER INFORMATION:

OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000, while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the retained earnings balance on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Prepare the consolidated statement of financial position at December 31, 20X4.

For the year ending December , the statements of comprehensive income for Dark and Light were as follows: OTHER INFORMATION:1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000, while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the retained earnings balance on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Prepare the consolidated statement of financial position at December 31, 20X4.

Question

Question

Question

Question

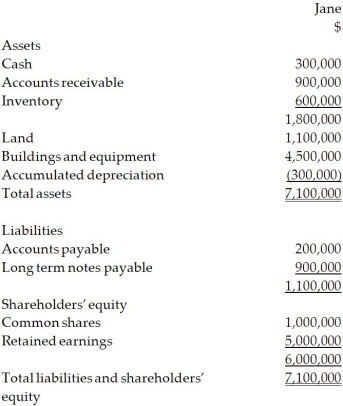

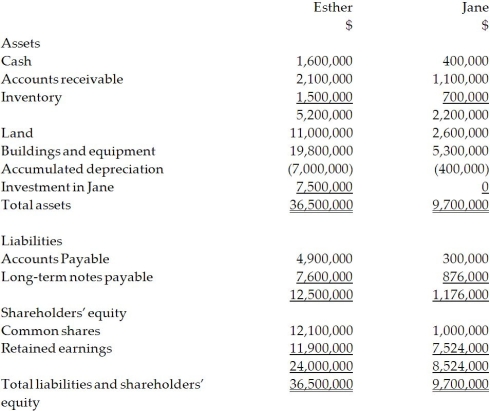

On December 31, 20X2, Esther Company purchased 80% of the outstanding common shares of Jane Company for $7.5 million in cash. On that date, the shareholders' equity of Jane totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization. The statement of financial position for Jane is provided below at December 31, 20X2.  For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: At December 31, 20X4, the condensed statement of financial position for the two companies were as follows:

For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: At December 31, 20X4, the condensed statement of financial position for the two companies were as follows:  OTHER INFORMATION:

OTHER INFORMATION:

1. On December 31, 20X2, Jane had a building with a fair value that was $450,000 greater than its carrying value. The building had an estimated remaining useful life of 15 years.

2. On December 31, 20X2, Jane had inventory with a fair value that was $150,000 less than its carrying value. This inventory was sold in 20X3.

3. During 20X3, Jane sold merchandise to Esther for $100,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Esther and the other 60% remained in its December 31, 20X3, inventories. On December 31, 20X4, the inventories of Esther contained merchandise purchased from Jane on which Jane had recognized a gross profit in the amount of $20,000. Total sales from Jane to Esther were $150,000 during 20X4.

4. During 20X4, Esther declared and paid dividends of $300,000, while Jane declared and paid dividends of $100,000.

5. Esther accounts for its investment in Jane using the cost method.

Required:

Calculate goodwill on the consolidated balance sheet at December 31, 20X4, under the entity method and the parent-company extension method. Explain the differences between the two balances.

For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: At December 31, 20X4, the condensed statement of financial position for the two companies were as follows: OTHER INFORMATION:1. On December 31, 20X2, Jane had a building with a fair value that was $450,000 greater than its carrying value. The building had an estimated remaining useful life of 15 years.

2. On December 31, 20X2, Jane had inventory with a fair value that was $150,000 less than its carrying value. This inventory was sold in 20X3.

3. During 20X3, Jane sold merchandise to Esther for $100,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Esther and the other 60% remained in its December 31, 20X3, inventories. On December 31, 20X4, the inventories of Esther contained merchandise purchased from Jane on which Jane had recognized a gross profit in the amount of $20,000. Total sales from Jane to Esther were $150,000 during 20X4.

4. During 20X4, Esther declared and paid dividends of $300,000, while Jane declared and paid dividends of $100,000.

5. Esther accounts for its investment in Jane using the cost method.

Required:

Calculate goodwill on the consolidated balance sheet at December 31, 20X4, under the entity method and the parent-company extension method. Explain the differences between the two balances.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/41

Play

Full screen (f)

Deck 5: Consolidation of Non-Wholly Owned Subsidiaries

1

In preparing consolidation working papers, why is it necessary to eliminate intercompany profits?

A)To nullify the effect of intercompany transactions on consolidated financial statements

B)To defer intercompany profits until the following year

C)To allocate unrealized profits until the following year

D)To differentiate between realized and unrealized profits

A)To nullify the effect of intercompany transactions on consolidated financial statements

B)To defer intercompany profits until the following year

C)To allocate unrealized profits until the following year

D)To differentiate between realized and unrealized profits

A

2

Assume that a parent company has four subsidiaries. Under IFRS 3, which of the following statements is true?

A)All four subsidiaries must be reported using the parent-company extension method.

B)All four subsidiaries must be reported using the entity method.

C)Each subsidiary must be reported using either the parent-company extension method or the entity method. Consistency is not required.

D)All four subsidiaries must be reported using either the parent-company extension method or the entity method. Consistency is required.

A)All four subsidiaries must be reported using the parent-company extension method.

B)All four subsidiaries must be reported using the entity method.

C)Each subsidiary must be reported using either the parent-company extension method or the entity method. Consistency is not required.

D)All four subsidiaries must be reported using either the parent-company extension method or the entity method. Consistency is required.

D

3

Sunny Co. purchased 80% of Reuben Ltd. for $1,200,000. At the date of acquisition, the carrying value of Reuben's net identifiable assets was $1,000,000, and the fair value was $1,300,000. What is the amount of the goodwill under the entity method?

A)$0

B)$200,000

C)$240,000

D)$300,000

A)$0

B)$200,000

C)$240,000

D)$300,000

B

4

Arnez Ltd. acquired 70% of Bedard Ltd. At the acquisition date, Bedard's net identifiable assets had a carrying value of $825,000 and a fair value of $1,000,000. Arnez paid $910,000 for the acquisition. Under the parent-company extension method, what amount should be reported for goodwill on Arnez's consolidated statement of financial position?

A)$210,000

B)$300,000

C)$332,500

D)$475,000

A)$210,000

B)$300,000

C)$332,500

D)$475,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

5

Which consolidation approach excludes the NCI?

A)Proportionate consolidation

B)Parent-company method

C)Parent-company extension method

D)Entity method

A)Proportionate consolidation

B)Parent-company method

C)Parent-company extension method

D)Entity method

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

6

Amber Ltd. purchased 80% of Patel Ltd. for $1,000,000. At the time of acquisition, the carrying value of Patel's net identifiable assets was $1,000,000 and the fair value was $1,350,000. What is the amount of the goodwill under the entity method?

A)$(100,000)

B)$100,000

C)$280,000

D)$350,000

A)$(100,000)

B)$100,000

C)$280,000

D)$350,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

7

Under IAS 27, where does the non-controlling interest (NCI)appear on the statement of financial position?

A)Under the liabilities section

B)Under the shareholders' equity section

C)Between the liabilities and shareholders' equity sections

D)NCI does not appear on the statement of financial position.

A)Under the liabilities section

B)Under the shareholders' equity section

C)Between the liabilities and shareholders' equity sections

D)NCI does not appear on the statement of financial position.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements about IFRS 3, Business Combinations is true?

A)IFRS 3 allows organizations to use either the parent-company method or the entity method.

B)IFRS 3 allows organizations to use either the parent-company extension method or the entity method.

C)IFRS 3 allows organizations to use either the parent-company method or the parent-company extension method.

D)IFRS 3 allows organizations to use either the parent-company method, the parent-company extension method, or the entity method.

A)IFRS 3 allows organizations to use either the parent-company method or the entity method.

B)IFRS 3 allows organizations to use either the parent-company extension method or the entity method.

C)IFRS 3 allows organizations to use either the parent-company method or the parent-company extension method.

D)IFRS 3 allows organizations to use either the parent-company method, the parent-company extension method, or the entity method.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

9

A parent company chooses to acquire only a 65% interest in its subsidiary. Which of the following is not a reason why the parent would choose to acquire less than a 100% interest in a subsidiary?

A)Reduction of ownership risk

B)Potential for increased share dilution

C)Maintenance of a market for the subsidiary's shares

D)Potential links to government support and management expertise through the NCI

A)Reduction of ownership risk

B)Potential for increased share dilution

C)Maintenance of a market for the subsidiary's shares

D)Potential links to government support and management expertise through the NCI

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

10

On December 31, 20X2, Bates Ltd. purchased 75% of the outstanding common shares of Ted Ltd. for $1,050,000 in cash. The balance sheets of Bates and Ted immediately before the acquisition were as follows (in 000s): At the time of acquisition, Ted's capital assets still had a remaining useful life of 10 years. Under the entity method, what amount should be allocated to goodwill?

A)$ 67,500

B)$ 90,000

C)$ 97,500

D)$130,000

A)$ 67,500

B)$ 90,000

C)$ 97,500

D)$130,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

11

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What amount should be shown on the consolidated statement of financial position for the non-controlling interest at December 31, 20X1?

A)$ 720

B)$1,720

C)$3,480

D)$3,720

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What amount should be shown on the consolidated statement of financial position for the non-controlling interest at December 31, 20X1?

A)$ 720

B)$1,720

C)$3,480

D)$3,720

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

12

Olthius Ltd. purchased 60% of Fredo Ltd. for $1,500,000. At the date of acquisition, the carrying value of Fredo's net identifiable assets was $1,800,000 and the fair value was $2,200,000. What is the amount of the goodwill under the entity method?

A)$(300,000)

B)$120,000

C)$300,000

D)$400,000

A)$(300,000)

B)$120,000

C)$300,000

D)$400,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

13

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What portion of consolidated net income for 20X1 is attributable to Portia?

A)$6,120

B)$6,240

C)$6,600

D)$7,080

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What portion of consolidated net income for 20X1 is attributable to Portia?

A)$6,120

B)$6,240

C)$6,600

D)$7,080

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

14

What is the purpose of showing an allocation of the net income between the parent and the subsidiary companies on the consolidated statement of comprehensive income?

A)To report the net income of the parent company to its shareholders

B)To report the net income of the subsidiary company to its shareholders

C)To report the net income of the parent and subsidiary companies to their respective shareholders

D)To report the net income of the parent and subsidiary companies to the tax department

A)To report the net income of the parent company to its shareholders

B)To report the net income of the subsidiary company to its shareholders

C)To report the net income of the parent and subsidiary companies to their respective shareholders

D)To report the net income of the parent and subsidiary companies to the tax department

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

15

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What is Portia's consolidated cost of goods sold for 20X1?

A)$13,800

B)$16,200

C)$16,800

D)$22,000

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What is Portia's consolidated cost of goods sold for 20X1?

A)$13,800

B)$16,200

C)$16,800

D)$22,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

16

Taguchi Ltd. owns 80% of Shag Co. Shag declared and paid $100,000 in dividends. Taguchi uses the cost method to record its investment in Shag. In preparing Taguchi's consolidated financial statements, what elimination entry must be made with respect to the dividends?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

17

Bates Ltd. owns 60% of the outstanding common shares of Sam Ltd. During 20X6, sales from Sam to Bates were $200,000. Merchandise was priced to provide Sam with a gross margin of 20%. Bates's inventories contained $40,000 at December 31, 20X5, and $15,000 at December 31, 20X6, of merchandise purchased from Sam. Cost of goods sold for Bates and Sam for 20X6 on their separate-entity income statements were as follows: What is the balance of the inventory account on Bates's consolidated statement of financial position at December 31, 20X6?

A)$140,000

B)$160,000

C)$162,000

D)$165,000

A)$140,000

B)$160,000

C)$162,000

D)$165,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

18

Which consolidation approach includes only the parent's share of a subsidiary's goodwill?

A)Proportionate consolidation

B)Parent-company method

C)Parent-company extension method

D)Entity method

A)Proportionate consolidation

B)Parent-company method

C)Parent-company extension method

D)Entity method

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is not a reason why a parent company would prefer to be involved with an NCI?

A)Reduction on ownership risk

B)Potential for increased share dilution

C)Maintenance of a market for the subsidiary's shares

D)Potential links to resources such as government support and management expertise

A)Reduction on ownership risk

B)Potential for increased share dilution

C)Maintenance of a market for the subsidiary's shares

D)Potential links to resources such as government support and management expertise

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

20

Lopez Ltd. purchases 65% of Wheatfall Co. Under the entity method of consolidation, what is allocated to non-controlling interest?

A)35% of Wheatfall's net assets at fair value

B)35% of Wheatfall's net assets at carrying value

C)35% of Wheatfall's net assets at carrying value plus 35% of Wheatfall's fair value increments excluding goodwill

D)35% of Wheatfall's net assets at carrying value plus 35% of Wheatfall's fair value increments including goodwill

A)35% of Wheatfall's net assets at fair value

B)35% of Wheatfall's net assets at carrying value

C)35% of Wheatfall's net assets at carrying value plus 35% of Wheatfall's fair value increments excluding goodwill

D)35% of Wheatfall's net assets at carrying value plus 35% of Wheatfall's fair value increments including goodwill

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

21

On December 31, 20X2, Dark Company purchased 75% of the outstanding common shares of Light Company for $6.0 million in cash. On that date, the shareholders' equity of Light totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization. For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000 while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the non-controlling interest on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Calculate the NCI's share of earnings for 20X4.

For the year ending December , the statements of comprehensive income for Dark and Light were as follows: OTHER INFORMATION:1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000 while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the non-controlling interest on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Calculate the NCI's share of earnings for 20X4.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

22

On December 31, 20X6, the statements of financial position of Power Company and Pro Company are as follows (amounts in thousands):

Power Company has 100,000 shares of common stock outstanding. Pro Company has 45,000 shares outstanding. All assets and liabilities have book values equal to fair values, except as noted above.

The plant and equipment has an estimated remaining useful life of nine years from the date of acquisition. The long-term liabilities mature on December 31, 2020. Market value of the new shares issued was $90 per share at issuance.

Required:

Assume that 90% of the outstanding shares of Pro were acquired for cash of $8.1 million. Calculate goodwill and the non-controlling interest on the consolidated balance sheet at December 31, 20X6, under the entity method and the parent-company extension method. Explain the differences between the two balances for goodwill.

Which method is preferred under IFRS? Why are the two methods allowed? Which methods are allowed under ASPE?

Power Company has 100,000 shares of common stock outstanding. Pro Company has 45,000 shares outstanding. All assets and liabilities have book values equal to fair values, except as noted above.

The plant and equipment has an estimated remaining useful life of nine years from the date of acquisition. The long-term liabilities mature on December 31, 2020. Market value of the new shares issued was $90 per share at issuance.

Required:

Assume that 90% of the outstanding shares of Pro were acquired for cash of $8.1 million. Calculate goodwill and the non-controlling interest on the consolidated balance sheet at December 31, 20X6, under the entity method and the parent-company extension method. Explain the differences between the two balances for goodwill.

Which method is preferred under IFRS? Why are the two methods allowed? Which methods are allowed under ASPE?

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

23

On December 31, 20X6, the balance sheets of Power Company and Pro Company are as follows (amounts in thousands):

Power Company has 100,000 shares of common stock outstanding; Pro Company has 45,000 shares outstanding. All assets and liabilities have book values equal to fair values, except as noted.

The plant and equipment has an estimated remaining useful life of nine years from the date of acquisition. The long-term liabilities mature on December 31, 2020. The company estimates that straight-line amortization will approximate the effective interest rate method.

Required:

Assume that 80% of the outstanding shares of Pro were acquired for cash of $5.8 million. Calculate goodwill and the non-controlling interest on the consolidated statement of financial position at December 31, 20X6, under the entity method and the parent-company extension method.

At December 31, 20X9, the balance in the long term liabilities of Pro is still $500,000 and the balance of long term liabilities for Power is $900,000. Calculate the balance in the consolidated long-term liabilities at December 21, 20X9.

Power Company has 100,000 shares of common stock outstanding; Pro Company has 45,000 shares outstanding. All assets and liabilities have book values equal to fair values, except as noted.

The plant and equipment has an estimated remaining useful life of nine years from the date of acquisition. The long-term liabilities mature on December 31, 2020. The company estimates that straight-line amortization will approximate the effective interest rate method.

Required:

Assume that 80% of the outstanding shares of Pro were acquired for cash of $5.8 million. Calculate goodwill and the non-controlling interest on the consolidated statement of financial position at December 31, 20X6, under the entity method and the parent-company extension method.

At December 31, 20X9, the balance in the long term liabilities of Pro is still $500,000 and the balance of long term liabilities for Power is $900,000. Calculate the balance in the consolidated long-term liabilities at December 21, 20X9.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

24

On September 1, 20X5, High Limited decided to buy 80% of the shares outstanding of Low Inc. for $630,000. High will pay for this acquisition by using cash of $500,000 and issuing share capital for the remaining amount. The balances showing on the statement of financial position for the two companies at August 31, 20X5, are as follows:

After a review of the assets and liabilities, High determines that some of the assets of Low have fair values different from their carrying values. These items are listed below:

• Land has a fair value of $295,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Brand value is $60,000. The brand has an indefinite life.

During the 20X7 fiscal year, the following events occurred:

1. On March 1, 20X7, Low sold land to High for $390,000, which had a carrying value of $275,000. High paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. High sold inventory (included in High sales)to Low for $200,000. Profit margin on these sales is 25%. Low still has supplies on hand of $75,000.

3. In 20X6, Low had provided seat space on flights to High for a value of $500,000. This amount was included in sales for Low. Profit margin on these sales is 40%. At the end of August, 20X6, High still had an amount of $200,000 in these prepaid seats that had not yet been used. (High includes this in inventory.)

4. The brand name was found to be impaired and an impairment loss of $40,000 was recognized. Required:

Calculate the balances for the following consolidated balances of High assuming High uses the parent-company extension method approach:

a. Goodwill at August 31, 20X5

b. Retained earnings at August 31, 20X7

c. Brand name, net, at August 31, 20X7.

After a review of the assets and liabilities, High determines that some of the assets of Low have fair values different from their carrying values. These items are listed below:

• Land has a fair value of $295,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Brand value is $60,000. The brand has an indefinite life.

During the 20X7 fiscal year, the following events occurred:

1. On March 1, 20X7, Low sold land to High for $390,000, which had a carrying value of $275,000. High paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. High sold inventory (included in High sales)to Low for $200,000. Profit margin on these sales is 25%. Low still has supplies on hand of $75,000.

3. In 20X6, Low had provided seat space on flights to High for a value of $500,000. This amount was included in sales for Low. Profit margin on these sales is 40%. At the end of August, 20X6, High still had an amount of $200,000 in these prepaid seats that had not yet been used. (High includes this in inventory.)

4. The brand name was found to be impaired and an impairment loss of $40,000 was recognized.

Required:Calculate the balances for the following consolidated balances of High assuming High uses the parent-company extension method approach:

a. Goodwill at August 31, 20X5

b. Retained earnings at August 31, 20X7

c. Brand name, net, at August 31, 20X7.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

25

Under the parent-company extension method, to which company should the impairment of goodwill be attributed?

A)Solely to the parent company

B)Solely to the subsidiary company

C)Allocated between the parent and subsidiary companies

D)No attribution of goodwill is shown under this method.

A)Solely to the parent company

B)Solely to the subsidiary company

C)Allocated between the parent and subsidiary companies

D)No attribution of goodwill is shown under this method.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

26

Bates Ltd. owns 60% of the outstanding common shares of Sam Ltd. During 20X6, sales from Sam to Bates were $200,000. Merchandise was priced to provide Sam with a gross margin of 20%. Bates's inventories contained $40,000 at December 31, 20X5, and $15,000 at December 31, 20X6, of merchandise purchased from Sam. Cost of goods sold for Bates and Sam for 20X6 on their separate-entity income statements were as follows:

- What is cost of sales on the consolidated statement of income for 20X6?

A)$687,000

B)$680,000

C)$685,600

D)$660,000

- What is cost of sales on the consolidated statement of income for 20X6?

A)$687,000

B)$680,000

C)$685,600

D)$660,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

27

On September 1, 20X5, High Limited decided to buy 70% of the shares outstanding of Low Inc. for $630,000. High will pay for this acquisition by using cash of $500,000 and issuing share capital for the remaining amount. The balances showing on the statement of financial position for the two companies at August 31, 20X5, are as follows: After a review of the assets and liabilities, High determines that some of the assets of Low have fair values different from their carrying values. These items are listed below:

• Accounts payable had a fair value of $295,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Patent is $80,000. The patent is estimated to have a useful life of five years.

During the 20X7 fiscal year, the following events occurred:

1. On March 1, 20X7, Low sold land to High for $390,000, which had a carrying value of $275,000. High paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. High sold inventory to Low for $300,000. Profit margin on these sales is 25%. Low still has inventory on hand of $80,000.

3. In 20X6, Low had provided inventory to High for a value of $600,000. This amount was included in sales for Low. Profit margin on these sales is 35%. At the end of August, 20X6, High still had an amount of $200,000 in these prepaid seats that had not yet been used. Required:

Calculate the balances for the following consolidated balances of High at August 31, 20X7, assuming High uses the entity approach:

a. Goodwill

b. Non-controlling interest

c. Buildings and equipment, net

• Accounts payable had a fair value of $295,000.

• The building has a fair value of $1,090,000. The remaining useful life of the building is 20 years.

• Patent is $80,000. The patent is estimated to have a useful life of five years.

During the 20X7 fiscal year, the following events occurred:

1. On March 1, 20X7, Low sold land to High for $390,000, which had a carrying value of $275,000. High paid for this with $90,000 cash and a note payable for the difference. This note pays interest at 10%, which is paid monthly.

2. High sold inventory to Low for $300,000. Profit margin on these sales is 25%. Low still has inventory on hand of $80,000.

3. In 20X6, Low had provided inventory to High for a value of $600,000. This amount was included in sales for Low. Profit margin on these sales is 35%. At the end of August, 20X6, High still had an amount of $200,000 in these prepaid seats that had not yet been used. Required:

Calculate the balances for the following consolidated balances of High at August 31, 20X7, assuming High uses the entity approach:

a. Goodwill

b. Non-controlling interest

c. Buildings and equipment, net

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

28

On December 31, 20X2, Dark Company purchased 75% of the outstanding common shares of Light Company for $6.0 million in cash. On that date, the shareholders' equity of Light totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization. For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000, while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the retained earnings balance on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Prepare the consolidated statement of financial position at December 31, 20X4.

For the year ending December , the statements of comprehensive income for Dark and Light were as follows: OTHER INFORMATION:1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000, while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the retained earnings balance on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Prepare the consolidated statement of financial position at December 31, 20X4.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

29

Under ASPE reporting requirements for investments in subsidiaries, how should the NCI at the time of acquisition be valued?

A)At fair value

B)At carrying value

C)At the acquiree's proportionate share of net identifiable assets

D)At fair value or at the acquiree's proportionate share of net identifiable assets

A)At fair value

B)At carrying value

C)At the acquiree's proportionate share of net identifiable assets

D)At fair value or at the acquiree's proportionate share of net identifiable assets

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

30

Devon Ltd. acquired 90% of Luka Ltd. for $100,000 less than the fair value. How should this $100,000 be treated on Devon's consolidated financial statements?

A)As goodwill on the consolidated statement of financial position

B)Allocated as fair value increments over Luka's net identifiable assets

C)As a gain on the consolidated statement of comprehensive income

D)As a separate item under shareholders' equity

A)As goodwill on the consolidated statement of financial position

B)Allocated as fair value increments over Luka's net identifiable assets

C)As a gain on the consolidated statement of comprehensive income

D)As a separate item under shareholders' equity

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

31

Bates Ltd. owns 60% of the outstanding common shares of Sam Ltd. During 20X6, sales from Sam to Bates were $200,000. Merchandise was priced to provide Sam with a gross margin of 20%. Bates's inventories contained $40,000 at December 31, 20X5, and $15,000 at December 31, 20X6, of merchandise purchased from Sam. Cost of goods sold for Bates and Sam for 20X6 on their separate-entity income statements were as follows:

- What is the balance of the consolidated inventory account at December 31, 20X6?

A)$160,000

B)$162,000

C)$165,000

D)$168,000

- What is the balance of the consolidated inventory account at December 31, 20X6?

A)$160,000

B)$162,000

C)$165,000

D)$168,000

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

32

On December 31, 20X2, Esther Company purchased 80% of the outstanding common shares of Jane Company for $7.5 million in cash. On that date, the shareholders' equity of Jane totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization. The statement of financial position for Jane is provided below at December 31, 20X2. For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: At December 31, 20X4, the condensed statement of financial position for the two companies were as follows: OTHER INFORMATION:

1. On December 31, 20X2, Jane had a building with a fair value that was $450,000 greater than its carrying value. The building had an estimated remaining useful life of 15 years.

2. On December 31, 20X2, Jane had inventory with a fair value that was $150,000 less than its carrying value. This inventory was sold in 20X3.

3. During 20X3, Jane sold merchandise to Esther for $100,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Esther and the other 60% remained in its December 31, 20X3, inventories. On December 31, 20X4, the inventories of Esther contained merchandise purchased from Jane on which Jane had recognized a gross profit in the amount of $20,000. Total sales from Jane to Esther were $150,000 during 20X4.

4. During 20X4, Esther declared and paid dividends of $300,000, while Jane declared and paid dividends of $100,000.

5. Esther accounts for its investment in Jane using the cost method.

Required:

Calculate goodwill on the consolidated balance sheet at December 31, 20X4, under the entity method and the parent-company extension method. Explain the differences between the two balances.

For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: At December 31, 20X4, the condensed statement of financial position for the two companies were as follows: OTHER INFORMATION:1. On December 31, 20X2, Jane had a building with a fair value that was $450,000 greater than its carrying value. The building had an estimated remaining useful life of 15 years.

2. On December 31, 20X2, Jane had inventory with a fair value that was $150,000 less than its carrying value. This inventory was sold in 20X3.

3. During 20X3, Jane sold merchandise to Esther for $100,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Esther and the other 60% remained in its December 31, 20X3, inventories. On December 31, 20X4, the inventories of Esther contained merchandise purchased from Jane on which Jane had recognized a gross profit in the amount of $20,000. Total sales from Jane to Esther were $150,000 during 20X4.

4. During 20X4, Esther declared and paid dividends of $300,000, while Jane declared and paid dividends of $100,000.

5. Esther accounts for its investment in Jane using the cost method.

Required:

Calculate goodwill on the consolidated balance sheet at December 31, 20X4, under the entity method and the parent-company extension method. Explain the differences between the two balances.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

33

Fleming Ltd. acquired 75% of Donner Ltd. on April 30, 20X1. Both companies have April 30th year-ends. Which of the following should be made to the opening non-controlling interest (NCI)balance to arrive at the April 30, 20X2, NCI balance on Fleming's statement of financial position?

A)Add in the NCI's share of Donner's fiscal 20X2 net income and subtract the NCI's share of Donner's dividends declared.

B)Subtract the NCI's share of Donner's fiscal 20X2 net income and add in the NCI's share of Donner's dividends declared.

C)Add in both the NCI's share of Donner's fiscal 20X2 net income and dividends declared.

D)Subtract both the NCI's share of Donner's fiscal 20X2 net income and dividends declared.

A)Add in the NCI's share of Donner's fiscal 20X2 net income and subtract the NCI's share of Donner's dividends declared.

B)Subtract the NCI's share of Donner's fiscal 20X2 net income and add in the NCI's share of Donner's dividends declared.

C)Add in both the NCI's share of Donner's fiscal 20X2 net income and dividends declared.

D)Subtract both the NCI's share of Donner's fiscal 20X2 net income and dividends declared.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

34

Jordan Ltd. acquired 80% of Cool Co. in 20X1. During 20X1, Cool sold inventory to Jordan. At the end of 20X2, the goods were still in Jordan's inventory. Jordan correctly eliminated the $10,000 of unrealized profits on its 20X2 consolidated financial statements and the goods were finally sold in 20X3. In preparing its 20X3 consolidated financial statements, what adjustments should be made with respect to the previously unrealized profit?

A)Increase cost of sales by $10,000, increase retained earnings by $8,000, and increase the non-controlling interest by $2,000.

B)Decrease cost of sales by $10,000, decrease retained earnings by $8,000, and decrease the non-controlling interest by $2,000.

C)Increase both cost of sales and retained earnings by $10,000.

D)No entry is required.

A)Increase cost of sales by $10,000, increase retained earnings by $8,000, and increase the non-controlling interest by $2,000.

B)Decrease cost of sales by $10,000, decrease retained earnings by $8,000, and decrease the non-controlling interest by $2,000.

C)Increase both cost of sales and retained earnings by $10,000.

D)No entry is required.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

35

Pooke Co. acquired 75% of Finch Ltd. three years ago. In calculating the balance for the non-controlling interest, Pooke started with the net income from Finch's current year-end separate-entity financial statements. Which of the following adjustments must be added to Finch's net income in calculating Finch's adjusted net income?

A)Amortization of fair value increments

B)Unrealized gain on an upstream sale of a capital asset

C)Unrealized profit on upstream sales of inventory in the current year

D)Realized profits in the current year on upstream sales of inventory from the previous year

A)Amortization of fair value increments

B)Unrealized gain on an upstream sale of a capital asset

C)Unrealized profit on upstream sales of inventory in the current year

D)Realized profits in the current year on upstream sales of inventory from the previous year

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following statements is true about a bargain purchase?

A)The purchase consideration paid by the parent for its share of the aquiree is less than the fair value of the shares.

B)The purchase consideration paid by the parent for its share of the aquiree is equal to the fair value of the shares.

C)The purchase consideration paid by the parent for its share of the aquiree is more than the fair value of the shares.

D)The purchase consideration paid by the parent for its share of the aquiree is less than the carrying value of the shares.

A)The purchase consideration paid by the parent for its share of the aquiree is less than the fair value of the shares.

B)The purchase consideration paid by the parent for its share of the aquiree is equal to the fair value of the shares.

C)The purchase consideration paid by the parent for its share of the aquiree is more than the fair value of the shares.

D)The purchase consideration paid by the parent for its share of the aquiree is less than the carrying value of the shares.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

37

On December 31, 20X5, Paper Co. purchased 60% of the outstanding common shares of Book Ltd. for $760,000 in shares and $200,000 in cash. The statements of financial position of Paper and Book immediately before the acquisition were as follows (in 000s):

The difference in the carrying value and the fair value of the property, plant, and equipment for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X7, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin in these products is 25%. At the end of 20X7, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

5. Goodwill was tested and found to be impaired, resulting in $100 impairment loss.

6. Paper uses the cost method to report its investment in Book.

Required:

Calculate the following items as they would appear on the Paper Co.'s consolidated statement of financial position at December 31, 20X7, under the entity method:

a. Goodwill

b. Non-controlling interest

c. Property, plant, and equipment, net

The difference in the carrying value and the fair value of the property, plant, and equipment for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X7, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin in these products is 25%. At the end of 20X7, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

5. Goodwill was tested and found to be impaired, resulting in $100 impairment loss.

6. Paper uses the cost method to report its investment in Book.

Required:

Calculate the following items as they would appear on the Paper Co.'s consolidated statement of financial position at December 31, 20X7, under the entity method:

a. Goodwill

b. Non-controlling interest

c. Property, plant, and equipment, net

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

38

On December 31, 20X5, Paper Co. purchased 60% of the outstanding common shares of Book Ltd. for $760,000 in shares and $200,000 in cash. The statements of financial position of Paper and Book immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

The difference in the carrying value and the fair value of the property, plant, and equipment for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 35% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 35% of selling price. At December 31, 20X6, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

Paper uses the cost method to report its investment in Book.

Required:

Paper has determined that it does not have control but only has significant influence over Book. Calculate the balance in the investment account at December 31, 20X7.

Calculate the investment income from this investee for 20X7 that Paper would show on its statement of comprehensive income.

The difference in the carrying value and the fair value of the property, plant, and equipment for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 35% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 35% of selling price. At December 31, 20X6, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

Paper uses the cost method to report its investment in Book.

Required:

Paper has determined that it does not have control but only has significant influence over Book. Calculate the balance in the investment account at December 31, 20X7.

Calculate the investment income from this investee for 20X7 that Paper would show on its statement of comprehensive income.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

39

There are alternative ways to calculate consolidated retained earnings. One of the methods requires adjustments to be made to the parent company's separate-entity ending retained earnings balance as of the consolidation date. What adjustments must be made to determine ending consolidated retained earnings?

A)Add in the dividends from the subsidiary to the parent and the parent's share of the subsidiary's adjusted income.

B)Subtract the dividends from the subsidiary to the parent and the parent's share of the subsidiary's adjusted income.

C)Add in the dividends from the subsidiary to the parent and subtract the parent's share of the subsidiary's adjusted income.

D)Subtract the dividends from the subsidiary to the parent and add in the parent's share of the subsidiary's adjusted income.

A)Add in the dividends from the subsidiary to the parent and the parent's share of the subsidiary's adjusted income.

B)Subtract the dividends from the subsidiary to the parent and the parent's share of the subsidiary's adjusted income.

C)Add in the dividends from the subsidiary to the parent and subtract the parent's share of the subsidiary's adjusted income.

D)Subtract the dividends from the subsidiary to the parent and add in the parent's share of the subsidiary's adjusted income.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

40

On December 31, 20X5, Paper Co. purchased 60% of the outstanding common shares of Book Ltd. for $760,000 in shares and $200,000 in cash. The statements of financial position of Paper and Book immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

The difference in the carrying value and the fair value of the capital assets for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X6, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin in these products is 25%. At the end of 20X6, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

5. An impairment loss of $100,000 was recognized related to the goodwill.

6. Paper uses the cost method to report its investment in Book.

Required:

Prepare the consolidated statement of comprehensive income for Paper Co. for the year ended December 31, 20X7, under the entity method.

Calculate the consolidated retained earnings for Paper Co. as at December 31, 20X6, and 20X7.

Prepare the consolidated statement of retained earnings for Paper Co. as at December 31, 20X7.

The difference in the carrying value and the fair value of the capital assets for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X6, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin in these products is 25%. At the end of 20X6, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

5. An impairment loss of $100,000 was recognized related to the goodwill.

6. Paper uses the cost method to report its investment in Book.

Required:

Prepare the consolidated statement of comprehensive income for Paper Co. for the year ended December 31, 20X7, under the entity method.

Calculate the consolidated retained earnings for Paper Co. as at December 31, 20X6, and 20X7.

Prepare the consolidated statement of retained earnings for Paper Co. as at December 31, 20X7.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

41

Explain why a parent might want to own less than 100% of the shares of a subsidiary.

Unlock Deck

Unlock for access to all 41 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 41 flashcards in this deck.